In addition, this study examines the relationship of the credit cycle and the risk cycle to the performance of individual banks. This phase of the analysis focuses on the impact of tricycles on bank performance. The standard model of the real business cycle (RBC) is based on the seminal work of Kydland and Prescott (1982).

In the standard model, the most important factors of the business cycle are the state budget shock and technological development (Romer, 2012). First, they internalized money and price invariance to examine the role of frictions in the transmission of monetary policy. The main contribution of the model is how the financial accelerator significantly affects the dynamics of the business cycle.

Starting from the standard RBC model, and influenced by the Financial Accelerator model, Kiyotaki (2011) describes the effects of the business cycle towards the credit cycle. In general, the relationship between the two cycles is affected by asset quality at each stage of the business cycle. The obtained result suggests that income diversification does not have a significant effect on the performance of banks in Indonesia.

Conceptual Framework

Bank attracts deposits - Bank observes success probability θ and sets a lending rate rL and borrowing rate rD - Investments made and bank reserves reserves R. Bank faces early withdrawals, xD - Bank incurs penalty if xD > R. Bank projects succeed either with probability. If , then the bank faces a liquidity shortage and will be fined by , which is proportional to the liquidity shortage, where . The bank manager has an unobservable level of effort so that, assuming that while the loans are affected by effort, they are not completely determined by it.

The manager earns income, which can be interpreted as bonuses, which increase as the manager sells more loans. But the manager also risks a fine, if the principal conducts an audit and it turns out that the manager acted too aggressively to increase loan volume by setting a loan rate lower than the rate that maximizes the principal's expected profit. The administrative penalty is part of the penalty costs that the bank must incur due to liquidity shortages.

The probability of success depends partly on the realization of the state variable and partly on the entrepreneur's effort decision, e, which determines whether the entrepreneur is diligent ( ) or evasive ( ), in which case entrepreneurs gain private benefit. If the entrepreneur is diligent, the probability of success is as before given by , and in the presence of shirking, the probability of success is , where. Meanwhile, constraint (11) implies that the expected entrepreneurial return conditional on the entrepreneur being diligent exceeds his expected shirking return.

Then there is the case that the entrepreneur's offer to the investors is not enough to satisfy the investors' reservation utility. Intuitively, if the macroeconomic risk is sufficiently high, the probability of success is low, and the entrepreneur therefore has little incentive to exert effort and is better off by shirking and consuming his private benefit. Because investors profit on average from depositing money in the bank, in the presence of moral hazard for entrepreneurs, investors are better off by depositing their endowments in banks.

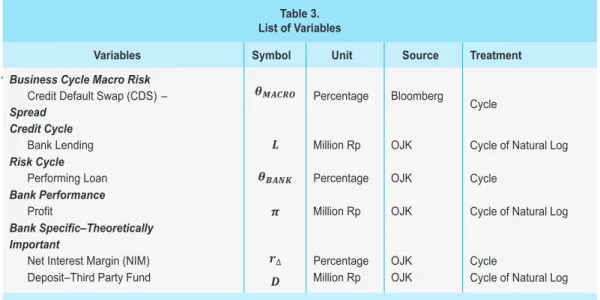

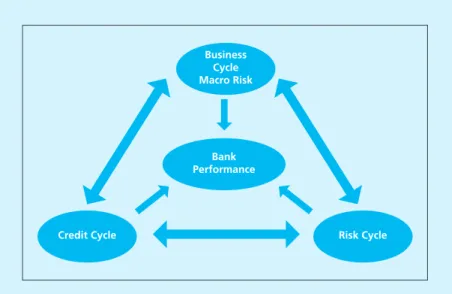

First, macroeconomic risk, , which plays an important role in determining deposit flushing received by the banks. Second, individual bank risk, , which is represented as the share of the performing loan compared to the total loan made by the bank.

METHODOLOGY

- Characteristic of the Data and Some Related Issues

- Overview of Panel Vector Autoregressive (PVAR) Model

- Empirical Model

- List of Variables

One of the benefits of using panel data is being able to provide interpretation that can meet these objectives, in terms of variation between individuals and over time (Baltagi, 2005). One of the most popular models for cycle analysis is the dynamic panel model as used by Ferri, et.al. The dynamic model in practice is implemented by introducing the lag of the dependent variable as one of the independent variables (Baltagi, 2005).

Such relationships create dynamic panel model cannot be separated from the autocorrelation lag due to the presence of one of the dependent variables as independent variables. Therefore, this study needs such a method that can observe potential bidirectional relationships between each cycle. In the context of business cycle analysis, the approach can provide insight into the dynamics between the business cycle and the financial cycle, which is of great concern in the developing literature.

This disadvantage was then avoided in this study since the selection process of the variables in this study is all based on the theoretical framework as explained in Section 3. This study then uses PVAR user-based package developed by Abrigo and Love (2015) which uses GMM -estimate to estimate Panel VAR. Due to data property, rather than using Loan Rate ( ) and Deposit Rate ( ), this study uses data of Net Interest Margin, , which is different from the and is.

In line with theoretical framework of this study which is based on Acharya and Naqvi (2012), this study then uses CDS spread rather than GDP which is very common to represent business cycles. However, due to the limitation and irregularity of commercial paper spread data in Indonesia, this study then uses credit default swap (CDS) spread data, which also represents macroeconomic risk. Bank lending data used in this study uses outstanding credit data on the balance sheet.

In addition to the focus variables, there are also two other variables that are theoretically important, the deposit and net interest margin. The deposit data is the sum of the total of third-party funds, consisting of giro, savings and time deposit.

RESULT AND ANALYSIS 4.1. Estimation Result

Discussion

Third, the heterogeneity of firms is represented by the extent of the data covering the entire population of conventional banks in Indonesia. As Acharya and Naqvi (2012) published their work on “Seeds of Crisis”, the scope of the business cycle became once again more comprehensive. This study applies only the initial stage of the model presented by Acharya and Naqvi (2012).

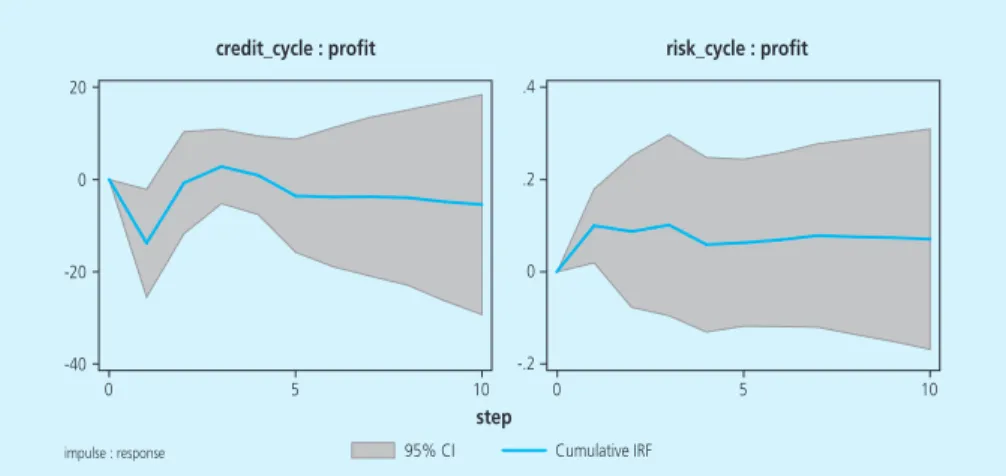

The estimation result shows procyclical behavior in the credit cycle towards macro risk in the business cycle. Unfortunately, the data and capacity of the model used in this study cannot observe this phenomenon more closely. The only channel available to explain risk-taking activity in the model is represented by the bank distributing more credit.

This function then causes the model to assume that the risk in the model is solely caused by an increasing amount of credit. Meanwhile, the risk profile of the projects in which the banks invest does not vary. The dynamics of the risk cycle then no longer depend solely on credit growth, but also on the bank's capital structure.

From the bank's internal perspective, the model states that this behavior is supposed to result in punishment if the manager of the bank is "caught" practicing excessive lending. Another concern for the bank manager's behavior in the moment of liquidity fluke is that the manager may underestimate the risk of projects or a credit. This study further contributes by accommodating bank performance dynamics in the discussion of the context of business cycle dynamics.

The model presented by Acharya and Naqvi (2012) is very suitable not only for discussing the policy making context but also for the profit maximization behavior of the bank. In the context of the crisis, the model in its full definition can be applied to examine step by step the rise of risk and the bursting of the bubble in the economy.

CONCLUSION

- Tri-Cycles Dynamics and Bank Performance

- Notable Contributions

- Recommendations

- Disadvantages and Suggestion for Further Research

The macro risk of a business cycle shock clearly has a more destabilizing effect on the risk cycle than on the credit cycle. In the meantime, regulators need to focus clearly on the risk cycle because of its greater sensitivity rather than the credit cycle for a shock in business cycle macro risk. First, business cycle macro risk and the credit cycle show a strong two-way relationship, in which a credit cycle shock has a significant impact on business cycle macro risk and vice versa.

Seventh, it can be inferred that the risk cycle is more sensitive when comparing the impact of macro risk shocks in the business cycle relative to the credit cycle and risk cycle. Cholesky IRF reveals response to risk cycle response to business cycle macro risk shocks. The result shows the dynamics of the financial cycle - in the form of credit cycle and risk cycle - preceded the macro risk of the business cycle.

This study subsequently contributed to the business literature by highlighting this phenomenon in emerging countries in particular. This study is also one of the first to use CDS spread as an alternative representation of business cycle fluctuations in Indonesia. So GDP can explain almost nothing when examining cyclical swings in the period of the 2007/8 financial crisis in Indonesia.

The credit cycle can no longer alone explain the dynamics of the financial cycle and its connection with the business cycle. From the perspective of the policy maker, specifically the banking regulator, the result obtained in this study reveals the cyclical and unstable response of the financial cycle (credit and risk) due to macro risk shocks in the business cycle. For market participants, especially bankers, this study has revealed volatile earnings response due to the business cycle shock through the risk and credit channel.

The Beginnings of the Crisis: A Theory of Bank Liquidity and Business Cycle Risk Taking. Bank ownership and credit over the business cycle: is state bank lending less procyclical.

Some specification tests for panel data: Monte Carlo evidence and application to employment equations. Bank capital buffers, risk and performance in the Canadian banking system: The impact of business cycles and regulatory changes.