FACULTY OF ECONOMICS UNISSULA ‑ SEMARANG

FACULTY OF ISLAMIC AND BUSINESS UIN SUNAN KALIJAGA ‑ YOGYAKARTA

INSTITUTE OF ISLAMIC BANKING AND FINANCE IIUM ‑ MALAYSIA

The Role of Zakah and Islamic Financial Institution into Poverty Alleviation and

Economics Security

SEMARANG, NOVEMBER 18–19

TH2015

No ISBN: 978‑602‑1154‑24‑1

No ISBN: 978‑602‑1154‑24‑1

i

FACULTY OF ECONOMICS UNISSULA ‑ SEMARANG

FACULTY OF ISLAMIC AND BUSINESS UIN SUNAN KALIJAGA ‑ YOGYAKARTA

INSTITUTE OF ISLAMIC BANKING AND FINANCE IIUM ‑ MALAYSIA

ii

Assalamualaykum.Wr.Wb

Wassalamualaykum.Wr.Wb

As a steering committe of 3rd ASEAN INTERNATIONAL CONFERENCE ON ISLAMIC FINANCE (AICIF-2015), firstly I would like to say “Thank You Very Much” to all parties for their enermous effort toward the detailed arrangement for hosting this conference.

The 3rd AICIF is organized by Faculty of Economics - Sultan Agung Islamic Unisversity (UNISSULA), Faculty of Islamic Economics and Busisness - State Islamic University Sunan Kalijaga Yogyakarta (UIN Yogyakarta), and Institute of Islamic Banking and Finance – International Islamic University Malaysia.

The conference is aimed to discuss “Role of Zakah and Islamic Financial Institution into Poverty Alleviation and Economoics Security”. Islamic financial institution, such as Islamic banking, Islamic unit trust, Islamic insurance, etc..

has growth very fast for last decade. They become important part relating to the efforts improving the quality of life of the society as well as relieving the society from the riba trap. In the context of recent economy, the Islamic financial institutions as economy pillar continues to chalange effort of poverty alleviation.

Conference aims to bring together researchers, scientists, and practitioners to share their experiences, new ideas and research results in all aspects of the main conference topics.

Furthermore, I would like to extend my gratitude to authors who submitted their papers to AICIF 2015 conference and also reviewers for their contribution and effort to excellent conference proceeding.

Finally, for all of you, welcome to AICIF 2015. I hope you will enjoy the conference and have a nice time during your stay in Semarang Indonesia.

Regards,

3rd AICIF 2015 Steering Committe , Dean

Faculty of Economics

Sultan Agung Islamic University Indonesia.

Olivia Fachrunnisa, PhD

FOREWORD

iii TABLE OF CONTENT

i ii iii Key Factors Affecting Credit Risk In Indonesian Islamic Banking

Yono Haryono Noraini Mohd. Ariffin Mustapha Hamat

1

Efficiency Of The Banking Sector In Malaysia Fekri Ali Shawtari

Mohamed Ariff

2

The Role Of Relational Capital In Increas ing The Collection And Distribution Of Zakah To Eradicate Poverty In Central Java

Heru Sulistyo

3

Creating Sustainable Competitive Advantages And Improving Salesperson Performance Through Intelligence, Emotional, And Spiritual Quotients And Selling Abilit y Of Smes In Central Java Province

Asyhari

Sri Hindah Pudjihastuti Dian Marhaeni Kurdaningsih

4

Woman’s Portrait in the Chain of Poverty: Looking at Early Marriage from Gender and Sexuality Perspectives

Inayah Rohmaniyah

5

Angels: Islamic Bank Of Health Maya Indriastuti

Luluk Muhimatul Ifada

6

Child Labor in Indonesia: Education and Health Consequences Sunaryati

7

Determinants Of The Factors That Cause Abandoned Housing Projects: A Study Of Home Buyers Of Islamic Home Financing In Malaysia

Dzuljastri Abdul Razak

8

Corporate Governance And Capital Structure Analysis At Islamic Bank In Indonesia

Mutamimah

9 EDITORS

FOREWORD

TABLE OF CONTENT

iv

The Effect Of Investment Decision, Funding Decision And Dividend Policy On Corporate Value

Dista Amalia Arifah Siti Roifah

10

Mobile Payment System Framework Based On Gold As A Measurement Of Value

Bedjo Santoso

Ahamed Kameel Meera Salina Hj. Kasim

Khaliq Ahmad

11

Corporate Financing Behaviour Of Shariah Compliant E50 Smes.

A Panel Data Approach Of GMM Razali Haron

12

Crude Palm Oil Market Volatility: Pre And Post Crisis Periods Evidence From Garch

Razali Haron

Salami Mansurat Ayojimi

13

Legal And Regulatory Framework Of Islamic Banking In Libya - Regulatory Authority, Licensing Of Islamic Bank, Shariah

Governance And Dispute Resolution Zainab Belal

Rusni Hassan

14

Developing a Comprehensive Performance Measurement System for Waqf Institutions

Nazrul Hazizi Noordin Siti Nurah Haron Salina Kassim

15

Improving Financial Education To The Poor At The Bottom - Of Pyramid: The Role Of Social Finance Vis A Vis Financial

Institutions Laily Dwi Arsyianti Salina Kassim

16

Regulatory Framework Of Islamic Banking In Afghanistan:

A Cursory Overview Mohsen Abduljamil Khan Rusni Hassan

17

v

Efektivitas Transmisi Kebijakan Moneter S yariah Jalur Pembiayaan

Rizqi Umar

Muh. Ghafur Wibowo Abdul Qoyum

18

The Environmental Development Model For Poverty Eradication Through Corporate Social Responsibility (CSR) Program

Abdul Hakim

19

The Role of Bank as Waqf Institution to Promote Indonesian Agricultural Sector

Faaza Fakhrunnas

20

The Analysis Of Profit Equalization Reserve (PER) In Income Smoothing Of Islamic Banking

Prima Shofiani Arief Bachtiar

21

The Analysis Of Determinants Selected Corporate Governance Attributes And Company Attributes On Financial Reporting Timeliness In Indonesia (Evidence From Sharia Security List The Period Of 2009-2013)

Ifa Luthfiana Iwan Budiyono Nyata Nugraha

22

The potential role of Social Impact Bond (SIB) as a financial tool that can help address the issues of poverty and socio-economic security

Syed Marwan Mujahid

23

Zakat Productive: Transforming Mustahiq To Muzakki Musviyanti

Fibriyani Nur Khairin

24

The Ways To Increase Shareholders Wealth In Indonesia Sharia Stock Index

Naqiyyah

Nunung Ghoniyah

25

Accountability Of Fund Management In Mosques, Kalimantan Timur, Indonesia

Yunita Fitria

Ahmad Zamri Osman Zaini Zainol

26

vi

Intellectual Capital And Performance Of Islamic Banks Hendri Setyawan

Tri Dewi Jayanthi

27

Risk Management And Management Accounting Parctice Of BPRS In East Java

Ulfi Kartika Oktaviana

28

Using ZIS (Zakat Infaq Shodaqoh) Institution to Expand Access to Renewable Energy Services In Indonesia

Aji Purba Trapsila

29

Collabrate Farmer Association Based Production House and Baitul Maal Wat Tamwil : Increasing Farmer Productivity

Through Optimalization ZIS Funding and Sharia Finance Product by Farmer (Walfare Farmer) CardScheme

Rifaldi Majid Evita Meilani

30

Workplace Spirituality and Employee Engagement for Islamic Financial Institution: A Conceptual Model

Olivia Fachrunnisa

31

Transformation Of Charities By Islamic Social Movements In Yogyakarta, 1912-1931: A History Of Islamic Wealth

Management Ghifari Yuristiadhi

32

Customer Interaction Management Capabilities And Market Intelligence Quality For New Product Performance

Tatiek Nurhayati Hendar

33

Assessing The Appropriateness And Adequacy Of The Provision For Housing Under The Haddul-Kifayah For Asnaf Faqr And

Asnaf Miskin

Khairuddin Abdul Rashid Sharina Farihah Hasan Azila Ahmad Sarkawi

34

An Overview Of Corporate Governance Practices Of Selected Islamic Banks: Case Of Rhb Islamic Bank, Masraf Al Rayan And European Islamic Investment Bank

Zainab Belal Lawhaishy Mustapha Hamat

35

vii

Asnaf Of Zakat: A Comparison Between Zakat Regulations In Wilayah Persekutuan And Selangor Darul Ehsan

Aznan Hasan

Nurun Nadia Binti Mohamad

36

Review of the Theory and Practice of Islamic Banking in Indonesia

Ibnu Haitam

37

Zakatable Items: A Comparison of Definition between Syeikh Yusuf al-Qardawi and States Enactments in Malaysia

Aznan Hasan

Raja Madihah Binti Raja Alias

38

Shariah Committee Composition In Malaysian Islamic Financial Institutions: Post Implementationof The Shariah Governance Framework 2010 And Islamic Financial Services Act 2013 Muhammad Issyam b. Itam@Ismail

Rusnibt. Hassan

39

Interpretation Of Integrated Zakat And Tax: Review Of Planned Behavior Theory

Agus Setiawaty Fibriyani Nur Khairin

40

Financial Consumer Protection: An Exploratory Study On Islamic Financial Services Act 2013 (IFSA), Bnm Regulations And Other Relevant Statutes

Norzarina Nor azman Sabarina Abu Bakar

Solara Hunud Abia Kadouf Rusnibt. Hassan

MuhammdIssyam bin Itam@Ismail

41

Zakat Houses For Asnaf Faqr And Miskin: Are Houses Appropriate And Adequate?

Khairuddin Abdul Rashid Azila Ahmad Sarkawi Sharina Farihah Hasan Srazali Aripin

42

[Re] Defining Mudharabah Financing Musviyanti

Salmah Pattisahusiwa

43

viii

Analysis Influence Of Difference Perception Between Shari’a Banking With Consumer Perception Towards Customer’s Purchase Intension Shari’a Banking in Semarang

Sri Rahayu Tri Astuti

44

Marketing at the Bottom of Pyramid: Cultural Ethnic Linkage to Islamic Microfinance Sales Promotion Scheme

Permata Wulandari Salina Hj. Kassim Liyu Adikasari Sulung Niken Iwani Surya Putri

45

Zakat As Social Function Of Shariah Banking Related To SMEs Empowerment For Poverty Alleviation

Mispiyanti Junaidi

46

Holistic View On Malaysian Islamic Interbank Money Market: A Critical Assessment

Buerhan Saiti

47

The Role Of Islamic Work Ethic, Spiritual Leadership And Organizational Culture Toward Attitude On Change With

Organizational Commitment And Job Involvement As Mediator On Bank Pembiayaan Rakyat Syari’ah (BPRS) Indonesia

Haerudin Bedjo Santoso

48

Implementation of Good Corporate Governance In Indonesian Islamic Banking

Ro’fah Setyowati Bedjo Santoso

49

Ascertaining Transparency And Accountability In The Practice Of Assessment Of Claims For Loss And Damage In Contractor’s All Risks (CAR) Takaful

Puteri Nur Farah Naadia Bt Mohd Fauzi Khairuddin Abd. Rashid

50

Market Reaction Toward Default Notice Of Islamic Bonds In Indonesia

Wuryanti Kuntjoro Happy Sista Devy

51

The Role Of Religiosity And Manifest Needs To Increase The Productivity Of Human Resources

Arizqi

Heru Sulistyo

52

ix

Islamic View On The Gold As Money Bedjo Santoso

Salina Hj. Kasim Mustofa Omar

53

The Prospects Of Islamic Banking In Higher Distance Education In Baskara

Rini Febrianti

Nadia Sri Damajanti

54

Entrusting Zakah (Alms) Administration To The Government: A Review Of Historical Study And Shari’ah Perspective

Abdulsoma Thoarlim Mursalin Maggangka

Mohamamed Muneer’deen Olodo al Shafi’i

55

Protecting Zakat And Waqaf Assets Through Takaful Puteri Nur Farah Naadia Mohd Fauzi

Khairuddin Abd. Rashid Azila Ahmad Sharkawi Sharina Farihah Hasan Srazali Aripin

56

Cooperative Takaful as a New Operational Model: A Conceptual Study

Azman bin Mohd Noor Olorogun, L.A

57

Perceived Fairness in Islamic Home Financing: Selection between BBA and MM

Mohamed Imtiyaz Salina Kassim

58

Ict Creative Industry Development : Sinergized Approach Mutamimah

Mustaghfirin Mustafa

59

The Effect Of Inflation Rate, Liquidity Ratio, And Interest Rate On Investors Reaction With Share Investment Risk As

Intervening Variable (Empirical Studies On The Jakarta Islamic Index)

Yonimah Nurul Husna Imam Setijawan

60

x

Analyzing The Effect Of Debt Level And Book Tax Differences On Persistent Earnings (Empirical Study on Manufacturing Company listed on the Indonesia Stock Exchange in the period of 2011-2013)

Guntur Prasetya Lulu M. Ifada

61

The Effect Of Soundness Of Banks Use Risk Based Banking Rating Method On The Financial Performance Of Islamic Banks Shintya Dewi Adi Putri

62

Organizing Optimization Of Social Insurance Agency (BPJS) Based On Public Satisfaction In Central Java

Alifah Ratnawati Yusriyati Nur Farid Noor Kholis

63

Effect Of Green Supply Chain Management Practices On Supply Chain Performance And Competitive Advantage

Osmad Muthaher Sri Dewi Wahyundaru

64

Testing The Effect Of TQM On The Islamic Microfinance

Institutions Performance Using Partial Least Squares Approach Hamzah Abdul Rahman

Abdo Ali Homaid Mohd Sobri Mina

65

The Perception And Interest Of Teachers On Islamic Bank Any Meilani

Isnina Wahyuning Sapta Utami

66

Implementing Corporate Social Responsibility (CSR) Program Through Zakat Model

Damanhur

Umarudin Usman

67

Improving Competitive Advantage Of Small And Medium Enterprises Through Green Competence And Green Image Sri Ayuni

Abdul Hakim

Agus Wachyutomo Heru Sulistyo

68

Allocation Fiscal Balance Transfers Local Goverment From The Central Government To The Prosperity For Ummah

Khoirul Fuad

69

xii

1

IMPROVING ECONOMIC SECURITY THE POOREST OF THE POOR:

AN INTEGRATED ISLAMIC APPROACH

(ZAKAT, WAQF, MICROFINANCE AND SOCIAL ENTREPRENEURSHIP) Widiyanto bin Mislan Cokrohadisumarto1

Faculty of Economics Sultan Agung Islamic University Semarang, Central Java

Indonesia

E-mail: [email protected]

Paper to be presented at 3rd Asean International Conference on Islamic Finance, Held on 18- 19th of November 2015 at Sultan Agung Islamic University, Semarang, Central Java,

Indonesia

Abstrack

Poverty has multidimensional characteristics (and complex); this would jeopardize the social and economic security of poor people. Employment for the poor is one of the solutions, because the work is the main weapon to solve the problem of poverty. The problem is that not all poor people could work because of the limitations they have. Because of the complex and the extent of the poverty issue, a single approach is not enough and then the solution requires an integrated approach by involving Islamic instruments such as zakat, waqf,Islamic micro finance institutions and also involving social entrepreneurship to obtain greater thrust. Social entrepreneurship constitutes a key to poverty reduction. However, it must be noted that poverty eradication should be based on the Islamic views of social justice and the belief in Allah Almighty.

Key words: poverty, economic securiy, zakat, waqf, microfinance, social entrepreneurship.

JEL: G23, I132, L31.

I. Introduction

At this time poverty2 is still a problem in many parts of the world including Muslim countries. Various efforts have been done in many countries, but the issue of poverty has still not getting satisfactory for resolution. This situation illustrates that the economic and social security of the poor is vulnerable to changes in situation which then needs to be addressed to find a way out with a more serious way. To resolve the problem of poverty it is necessary to understand the profile of poverty and the characteristics of the poor. Zeinalabdin (1996) mentions about the poverty profiles and some characteristcs of the poor, among others are:

1Senior Lecturer of Islamic Economics at Faculty of Economics, and the Head of Magister Management Program Sultan Agung Islamic University, Jl. Raya Kaligawe Km 4 Po. Box 1054/SM Semarang, Central Java, Indonesia.

2Poverty (fakr), meaning that a person has some material difficulties and cannot do certain things and needs others (Guner, 2005), and poverty has been depicted as a great setback by which an individual, a society, faith and belief, manners and morals, words and deeds, thoughts and culture can not remain safe and protected (Al- Qardhawi, 2006).

2

(i) poor people are generally landless, and, hence, they are mostly agricultural labourers in the rural areas. (ii) people who are illiterate, have no or little access to education, have low levels of human capital and capacity to work are particularly vulnerable to poverty.

(iii) poor people are settled, generally, in regions and areas which are not planned and lack the necessary infrastructure and facilities and are, hence, prone to environmental risks and hazards. (iv) access to and usage of public goods and services are very limited in the case of the poor people. (v) poor people in the urban areas are mostly employed in difficult, low-paid and socially looked-down upon jobs such as construction workers, street cleaners, etc. (vi) poor people lack the ownership of physical and financial assets, and, accordingly, are usually wage earners. (vii) poverty has some seasonal dimensions in that people get poorer in a cyclical manner. All of these depict the multi-faceted of poverty nature.

By looking at the nature of poverty as mentioned above, the settlement of the problem of poverty is complex and cannot be done with a single model (approach). It means that solving the problem of poverty required integrative handling model. According to Hoque et al., (2015) poverty reduction requires a multi-dimentional approach (such as based on the development of human capital, creativity, and resourcefulness of the poor, building upon their resources, capabilities, and survival skills ensuring their sustainability against poverty).

However there may be a keyword that can be a starting point of the problem-solving. Al- Qardawi (2006) revealed an important word that can be used as the first weapon to fight poverty and hunger, and the word in question is "working". It is the first source of earning wealth, and is the basic element to habitation on the earth, for which purpose he has been made vicegerent of God. Man has been commanded to establish himself on the earth. Islam encourages Muslims to work and to gain their livelihood, and working to obtain property and maintain a good life is accepted as a valuable effort and worship (Guner, 2005). The problem is that not all poor people could pass up work as he wanted due to the limitations, both the inherent limitations of the person concerned, or limitations that surround around their daily lives (environment).

Then what about the solution? There are several different ideas in solving the problem of poverty. There are those who approach zakat, waqf, microfinance institutions, and social entrepreneurship to solve the problem of poverty (as instrument), and some are using a combination of approaches, for example, combines the zakat and waqf, zakat with social entrepreneurship, as well as microfinance and social entrepreneurship.

Because poverty has a multidimensional characteristics (and complex), this paper seeks to develop a more integrated Islamic approach to get a better solution (in reducing poverty), so that economic security be better protected. This paper consists of sevent parts, the first part is the introduction, the second section discusses the role of microfinance in addressing poverty, the third section discusses about the zakah and poverty, the fourth section discusses the awqaf and the completion of poverty, the fifth part is the role of social entrepreneurship in the eradication of poverty, the sixth part is the development of an integrative approach for overcoming poverty and improved economic security, and the last part is the conclusion.

II.The role of microfinance in addressing poverty

Microfinance consitutes the most useful and popular financial system in the world to face financial difficulties of the poor people. It provides loans and other services to assetless and landless poor people whom no bank give loan. Currently it has many emerging microfinance institutions (MFI) to serve the importance of the poor in many places in this world. Grameen

3

Bank in Bangladesh, BancoSol in Bolivia, Bank Rakyat Indonesia Unit Desa (BRI Unit Desa), Microfinance Bank of Georgia and Constanta in Georgia, Enterprise Mentor International in the US are some examples of micro financial institutions were deemed successful, and many other microfinance institutions that are scattered in many countries.

MFI are seen as a success because of the level of repayments from borrowers nearly 100 percent. But it is unfortunate they charge a very high interest loans. The appearance of many MFIs can provide many opportunities to the poor (micro-enterprises) in getting the capital to build the business and creating self-employment and may it can play a vital role in reducing the rural unemployment and acute poverty. Nevertheless, giving loans with very high interest rate does not assist the poor (micro-enterprises) to develop their business and improve quality of life. Charging high interest rate will be burdensome for them. As an example of the results of research in Grameen Bank, high interest rates cause the poor women cannot use the loan in a high profitable business to bear this burden, so some of the borrowers lose lands and assets to pay the loan (Islam, et al., 2012). If so (charge a high interest rate), the micro-finance will never be a solution to solve the problem of poverty. That means the system of interest has vices or weaknesses. According to Mannan (1986) interest uproots the very foundation of humanity, mutual help and sympathy and creates selfishness in men, and Siddiqi (1981) states that interest involves oppression through exploitation. It illustrates contain any element of injustice in the implementation of conventional microfinance contrary to the principles of Islam. Therefore, the presence of Islamic microfinance institutions (IMFI) with an interest- free system is expected to be a solution to solve the problem of poverty. It constitutes an alternative solution. Islamic micro-financing differs from interest based financing which assures a fixed return to the financer while the borrower is left to bear the entire business risk.

Islamic microfinance is developed based on Islamic principles and of course in general is no different with the principles of Islamic finance. Abdullah (2010) mentions five key principles of Islamic finance; (i) believe in divine guidance (Al-Qur‟an and Sunnah), (ii) no interest (riba), (iii) no haram investment, (iv) risk sharing is encourage, (v) financing based on real asset. It needs to be realized that man does not have the power to reach the truth on his own, man is not only imperfect but also his reasons are often confused with desires, then man needs divine guidance. The prohibition of riba constitutes one of the main elements of Islamic economy. According to Raquib (2007) the elimination of riba from the economic system is intended to promote economically just, socially fair and ethically correct dealings according to Islamic principles. This harmonious trade creates powerful economic incentives and brings about cooperation and co-participation in all walks of life. In addition Islam also forbids all of haram activities (including investment) and forbids admixing all of haq and bathil activities. It is in order to protect mankind form badness and all of kind which endanger human life. Risk sharing also constitutes an important point to promote justice who offers same opportunity to all parties to obtain benefit (to foster the equitable distribution of risk, profit and losses), so properties not only circulate for the rich. Another important point which needs to pay attention to avoid incertitude (vagueness), speculative behavior and gambling is, all financial transactions must be linked to a real economic activity. It means all transactions must be backed by assets, and investments may be made only in real, durable assets.

In line with the above principles, Khan (2008) reveals six principles of Islamic finance;

prohibition of riba (interest), and implementation of murabahah, mudharabah, musyarakah, joalah and qard al-hasan financing. Interest is considered an unjust instrument of financing.

The main reason why Islam abolishes interest is that it is, in essence, oppression through exploitation, and the second reason is that interest transfer wealth from the poor to the rich, increasing in equality in the distribution of wealth (Siddiqi, 1981). Therefore, the prohibition

4

of interest and the implementation Islamic financing constitute a way to establish justice between financer and the entrepreneur. It is the way out of Islam.

Based on the prior discussion, it means that the basic principles of Islamic finance encompassing; act up to Allah and His messenger (Muhammad, pbuh), be just and free from exploitation - which is reflected on prohibition of interest, implementation of profit and loss sharing, risk sharing), halal and ethical - which is reflected on prohibition of speculative behavior and gambling. Concerned with the principles of Islamic microfinance, it can be derived from the above principles, however it still need to be adapted with the primary mission of microfinance – to help the poor people in assisting themselves to become economically independent with an eye to protect them from dangerous (economic vulnerable, apostate, etc) – especially stressing on principle of ta‟awun for economic and social security of the poorest of the poor, since they are really in life difficulties and have a need of aid.

IMFIs have been established in many countries such as, Akhuwat in Pakistan (AsadEjaz and Ramzan, 2012), Baitul Mal Wat Tamwil in Indonesia (Widiyanto and Ismail, 2010), Microfinance Bank of Khartoun in Sudan (Naeem, 2012), Islamic Relief in Bosnia &

Herzegovina, Kosovo, Pakistan, Sudan (Khan, 2008), Al-Amal Microfinance Bank in Yemen (Alathary, 2013). The question is how their role in the eradication of poverty? To be able to answer questions about the role of Islamic micro finance institutions in combating poverty, we must first answer the question of how the effectiveness of Islamic micro finance.

Research on the effectiveness of Islamic micro-financing has not been much done and here are the results of existing research (with a limited number). Results of research on the effectiveness of Islamic micro-financing offered by IMFI as did Al-Akhwat in Pakistan through qard al-hasan financing showed effective results for development tool in order to eradicate poverty and empower people with more speed, although must be combined with entrepreneurship (AsadEjaz and Ramzan, 2012). The other evidence also shows that the qard al-hasan financing is effective for the development of micro-enterprises in Central Java (Widiyanto, et al., 2011). Likewise, the implementation of micro-financing (for various types of financing in general) by BMT in Indonesia (Central Java in particular) shows that Islamic micro-financing effectively to the development of micro enterprises. The selection process, assistance and oversight certainly played a role in increasing the effectiveness of Islamic microfinance (Widiyanto and Ismail, 2010). From the research that has been mentioned shows that Islamic micro-financing is the potential to become an instrument (have a role) in reducing the level of poverty in the Muslim countries.

Several studies have shown; microfinance undertaken by IMFIs is effective to reduce poverty, develop micro-enterprises and contributed quite a lot social benefits to the community. The great hope of the Muslims is that microfinance is not only effective for overcoming poverty but also to reach as many of the poor and needy - especially the poorest of the poor and this is still an issue. IMFIs which develope musharaka, murabaha, bai‟u bithaman ajil and Ijarah financing are more likely to serve the community (micro enterprises) from which is considered the most viable businesses and consequently the poorest communities tend to be forgotten.

Issues that may arise and will be faced by microfinance institutions serving the public is a matter of the preservation of the institution that has to do with the question of how the profitability and microfinance institutions to serve the poor as much as possible. Profitability demands efficiency while serving the poor in large number requires huge cost and faces high risk and also may obtain low profit. There is a conflict between the interests of efficiency (in

5

order to obtain the profit) with the purpose of serving the poor as much as possible. This is often the reason why banks are reluctant to serve the poor. Not supposed IMFIs dealing with the conflict, and must be designed from the beginning of its establishment. The question of how to provide financing to the business layer is not so profitable without disturbing sustainability? Another possible source of funds (which are not based on pure business) as a source of funds from zakat, infaq, alms and endowments (waqf) can be channeled to finance productive enterprises the bottom layers of society via qard al-hasan financing model (benevolent loan). The financing model is a model that seems most appropriate to the characteristics of the poorest layers of society because they are not burdened with an additional cost except return the loan principal. Therefore the qard al-hasan financing model need to be further developed and disseminated its use so as to reach the wider poorest communities.

III. Zakah and poverty reduction

Islam was very attentive to the problem of poverty, as described in several verses of the Qur'an (eg, Surah Al-Baqarah;177, Al- Isra‟; 26-27, Al-Balad;16, Al-Insan; 8). Likewise, Islam concretely gives the right to the poor over the rich treasure through zakat (Surah At- Taubah; 60). In this verse Islam establishes zakat as a compulsory charity tool that can be used on eight purposes. Five are meant for poverty eradication such as the poor, the needy, the debtors, the slaves, and the travelers in need. Others are to the administrative cost of zakat, 'those whose hearts are made inclined' (to Islam), and in the way of Allah. However, according to (Hasan, 2010) there is general agreement that the first priority in the use of zakat funds has to be accorded to the alleviation of poverty through assistance to the poor and the needy. Al-Qarhawi (2006) states that the system of zakat is the first law in action for the economic security, and the main aim of zakat is to eradicate poverty altogether by spending for the welfare of the poor and the destitude. Furthermore Hasan (2007) states zakat is an instrument of social policy similar to the social security system of the West as well as a scheme of insurance againts various misfortune, and zakat has been the outstanding social pilar of Islam, enabling individuals' efforts to be steered towards a common goal.

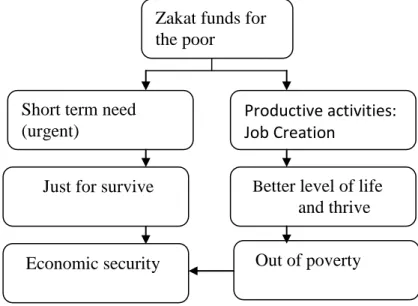

Islam disapproves of people being in poverty and need; it decrees that every man earn his living by his own work, so long as he can, but that he recieve his share from the public monies when for any reason he is unable to work (Qutb (2000), and then zakat is lawful for some personal weakness, such as tender age, old age, disability or non-availability of reasonable work to his status or less income which is not enough for his sustenance (Al- Qardhawi, 2006). For poor people caused by the unavailability of a reasonable job for status or because of less revenue that is not enough for his sustenance, taking into account that in essence they still have the ability to work, then how can they not be dependent on charity funds and they were able to develop themselves so as to have a better quality of life as well as improve their dignity as human beings? According to Ismail (2013) to improve the dignity of poor people as human beings, they should be given assistance in the form of a more comprehensive not just to eat. It indicates that specific programs have to be designed to provide support for education and skill development, provision of physical capital, and making financial capital available to start a business (Ahmed, 2004), and according Hoque, et al., (2015), and Hasan (2010) zakat fund can be used in the productive way (development activities). The above figures show that zakat can be distributed to the beneficiary in two categories. The first, zakat funds are distributed for short-term consumer interests (urgent) for those in need. Second, zakat funds channeled to long-term goal, it is for productive purposes in order to increase the economic resilience of the people to a better level and thrive, not just survive. As example, in the case of Indonesia and Malaysia, the utilization of zakat funds has

6

now been transformed from a charity purpose (short run purpose) into social empowerment and economic development (Ali and Hatta, 2014).

Relating to the distribution of zakat funds for productive purposes (which is complex), its handling requires the involvement of many parties (not just treasury). This requires the involvement of Islamic micro finance institutions and other institutions concerned with the problems of poverty, including the volunteer social entrepreneurs. It is necessary, because the efforts of how to facilitate poor people so they can live better are useful for maintaining the security of their economies from possible fluctuation and uncertainty of their economies. The thing to realize is that their economic circumstances are generally vulnerable to changing situations.

The result of financing zakat funds in productive activities is expected to create new employment opportunities (job creation) which benefit poor people and the wider community as a whole in the long run. As is mentioned in the previous section that the work is a powerful weapon to eradicate poverty, and Islam strongly advocate people to work for the bounty of God on this earth. God demands and other creation to exert his efforts to procue the means of their sustenance. God Says: “ And when the prayer is ended, then disperse in the land and seek of Allah‟s bounty.” (QS: Al-Jum‟ah; 10).

By working in a sustainable manner will affect the release of poverty from which they suffer, although it requires a long process. Keep in mind that poverty eradication was not like taking a panacea that will instantly heal completely drunk. This requires substantial funds and available continuously. Therefor, continuous campaign to build public awareness to pay zakat should be done, and it is the duty of the government and the Muslim community.

Here is a diagram illustrating the flow of zakat funds can serve as a means of reducing poverty and improving the social and economic security.

Figure 1: The role of zakat in reducing poverty and improving economic security.

IV.Waqf and the completion of poverty

Zakat funds availability is still limited, then the community must depend on voluntary donations and fund-raising events to cover the cost of whatever activities they may choose to

Zakat funds for the poor

Short term need (urgent)

Productive activities:

Job Creation (productive)

Just for survive Better level of life

and thrive

Out of poverty Economic security

7

obtain (including to poverty alleviation activities), such as obtaining from sadaqah funds.

According to Hasan & Khan (2007) not only by using zakah, poverty can be tackled through other means such as shadaqah. It can refer to the general concept of charity in Islam and then focuses on the lasting charity (perpetual charity) which then known as waqf.

Waqf is an Arabic word derived from the root verb waqafa. It is a special kind of voluntary charity that has permanence and the capacity to generate income (Ali, 2009). Waqf in Arabic means habs (hold). According to the terms of syara‟ (syari‟ah point of view), waqf mean to hold property and provide benefits in the way of Allah (Sabiq, 1987) and according to Kahf (2014) waqf may be defined as holding a property and preserving it so that its fruits, revenues or usufruct is used exclusively for the benefit of an objective of righteousness while prohibiting any use or disposition of it outside its specific objective. Hence, waqf is a continuously usufruct-giving asset as long as its principal is preserved. Waqf have been implemented at the time of the prophet, and waqf are first in Islam is waqf land in Khaibar conducted by companions of the Prophet namely Umar (Sabiq, 1987):

„‟Ibn „Umar reported: Umar obtained a land at Khaibar. He came to Allah‟s Messenger (pbuh) asking for advice. He said: “Allah‟s Messenger (pbuh), I obtained a land in Khaibar.

I never obtained a property more valuable for me than this, so what do you advise me?

Thereupon he said: “If you want, you can bequeath it, and give it as charity; provided that it should not be sold, bought, given as gift or inherited.” He said, “then Umar gave it as charity for the poor, relatives, slaves, wayfarers, and guests. There is no harm for the person responsible for it to feed himself or a friend from it but for free.” (Al-Bukhari and Muslim)

Rasjid (2006) reveals the advantages of waqf compared to the others, that for the community, waqf can be a way to progress the greatest possible extent, and can even prevent the occurrence of damage. Because of the waqf, muslims (in Muslim countries first - hundreds of years ago) to get progress, which up to now the results of waqf was still eternal. The above figures show that waqf can be a very good way towards progress (benefit) in the future because it is very productive and get results or sustainable benefits (repeatedly), either the future of the wakif 3(in hereafter future)4and the worldly future of the beneficiaries (provide a very broad benefit the public interest). Specifically the above hadith also gives examples of the use of the results of waqf to help the poor (involving waqf in poverty alleviation). This is an indication that the settlement of the problem of poverty one of which can be done by utilizing the waqf instrument. Because waqf has tremendous benefit, therefore today many scholars advocate the use of waqf in structuring and operating takaful (Islamic insurance) and micro-finance even as they continue to emphasise its role in the alleviation of poverty (Ali, 2009).

Waqf development program that is currently be building which allows more people to get involved (both wakif or mauquf alaih/beneficiaries) is cash waqf (in the form of cash waqf sertificate). According to Shaikh (2012), cash waqf certificates are an interesting method to combat poverty in which a cash-waqf fund could be tailored to provide easy access to finance to the poor and help poverty alleviation. This model has been implemented in Bangladesh by Social Islami Bank Limited (SIBL).The SIBL cash-waqf account offers 32 purposes under

3 Wakif is the person making waqf.

4 Hadits: “When a human being dies, his work for Allah comes to an end except for three things:

a lasting charity (sadaqa jaariya), knowledge that benefits others, and a good child who calls on Allah for His favour.”(Muslim)

8

the following major fields: (1) Family rehabilitation (including improving the condition of absolutely poor living below the poverty line, rehabilitation of desitute women), (2) Education & Culture (including da‟wah activities), (3) Health & Sanitation,(4) Social Utility and, (5) Others.

There are two important factors that need attention of the characteristics of the Islamic waqf.

Khaf (2014) refer to it as the main characteristics: (1) perpetuity, and (2) permanence of stipulation of the waqf founder. First, perpetuity means that once a property, is dedicated as waqf it remains waqf for ever. Theoretically at least, perpetuity implies that waqf properties should not decrease. Second, permanence of stipulations of the waqf founder implies that revenues of waqf should exclusively be used for the objectives stipulated by its founder.

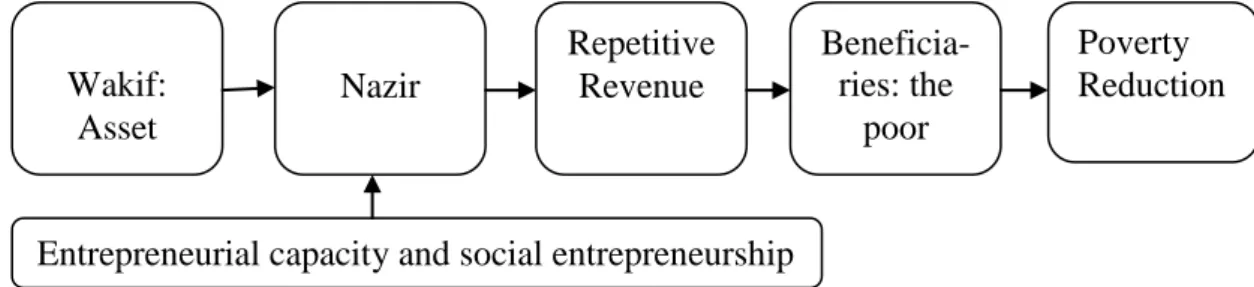

Permanence covers all the founder's stipulations whether they relate to purpose, distribution of revenues, management, supervisory authority, etc. Another important factor that also needs to get the attention of the management of waqf, that is how the waqf property was able to generate sustainable revenue (getting the repetitive) so as to provide the widest possible benefit (maximization of the revenue) to the empowerment program of poverty eradication.

This represents a challenge for Nazir5 (waqf manager). This is what will ensure the sustainability of poverty eradication programs. This suggests a demand that the management of waqf require entrepreneurial capacity and social entrepreneurial insight.

The relationship between waqf with poverty reduction can be summariesed in the following figure:

Figure 2: Relationship waqf with poverty reduction.

It should be noted that revenue from the waqf can be repeated (repetitive revenue), then the waqf becomes very potential to be used as an instrument (source of funds) in the development of community empowerment programs (including for poverty alleviation) which require a considerably long time.

V.The expected role of social entrepreneurship in the eradication of poverty

In the early part of this paper has been discussed that work constitutes one of powerful weapon to solve the problem of poverty. The problem is that poor people have difficulty getting work and it seems the government has not been able to fully provide jobs to them and the government has not been able to provide the best solution. Things like that occurred in many countries and the result is poverty in many countries is still quite high (including in Muslim countries). The question is how to solve these problems? According Baber (2012) social entrepreneurship constitutes a key to poverty reduction. It implied that, in relation to

5The waqf manager is usually called Nazir ,Mutawalli or Qayyim and his\her responsibility is to administer the Waqf property to the best interest of the beneficiaries. The first duty of mutawalli is to preserve the property;

this is followed by maximization of the revenues of the beneficiaries (Kahf, 2014).

Wakif:

Asset

Nazir

Repetitive Revenue

Beneficia- ries: the

poor

Poverty Reduction

Entrepreneurial capacity and social entrepreneurship

9

poverty reduction required the involvement of social entrepreneurs - whose job according to him is “to recognize when a part of society is not working and to solve the problem by changing the system, spreading solutions, and persuading entire societies to take new leaps.

Social entrepreneurship is increasingly being viewed as a way to reduce poverty, to pursue entrepreneurial strategies that are conceptually related to the effectiveness of the eradication of poverty.

Clark (2009) defines social entrepreneurship as doing business in order to solve social problem or solve social problem by doing business. It is by hybrid between business and social purposes in which the implementation of social entrepreneurship is directed to achieve two main goals, they are; societal and business development work concomitantly. According Makhlouf (2011) social entrepreneurship is catching up with business entrepreneurship as a borderless agent of change.6 Therefore, social entrepreneurship involves the activities and processes undertaken to discover, define, and exploit opportunities in order to enhance social wealth by creating new ventures or managing existing organizations in an innovative manner (Zahra, et al., 2009). Then this is reaffirmed by Salarzehi, et al., (2010) that social entrepreneurship is the innovation for the problem and social issues. By this description, it can be expected that the implementation of social entrepreneurship can be as an effective mechanism for solving poverty problem. To be able to perform these tasks, then a social entrepreneur must be those who have a powerful ability, the reformers and revolutionaries with a social mission. Therefore, for social entrepreneurs; (i) the social mission is fundamental - to create lasting improvements and sustaining the impact /social value,7 (ii) acting boldly without being limited by resources currently in hand - explore all resource options, from pure philanthropy to the commercial methods of the business sector, (iii) recognizing and relentlessly pursuing new opportunities - where others see problems, entrepreneurs see opportunity, (iv) engaging in a process of continuous innovation, adaptation, and learning - break new ground, develop new models, and pioneer new approaches, (v) exhibiting a heightened sense of accountability to the constituencies served and for the outcomes created - social entrepreneurs take steps to assure they are creating value (Dees, et al., 1998). However (in the perspective of Islam), there are other important things that should not be abandoned – ie, implementation of the principles and values of Islam8 (Abdullah and Hoetoro, 2011), since in Islam, there is no separation between entrepreneurial activities and religion, and Islam sees everything as a comprehensive element in life, including entrepreneurship (Faizal, et al., 2013).

.

A social entrepreneur can an individual, group, network, organization, or or even communities that band together to create pattern-breaking change (Noruzi, et al., 2010). As an example: Muhammad Yunus (as an individual) has long been a hero of the social entrepreneur community for his work in creating the Grameen Bank (GB), and transforming the microfinance movement. Islam et al., (2012) states that the microfinance system of GB is a revolutionary tool to eradicate poverty of the rural people especially the women of

6 Furthermore he explained, it is the kind of transformational change that makes a difference in solving societal

and environmental problems and reversing actual or threatening negative social, economic and environmental trends.

7 As an additional note that according to Makhlouf (2011) the most part of social entreprise uses the realized

profits for sustainability or for attaining clear social and/or environmentally related objective.

8For examples, suchas commanded in Surah al-Maidah (5: 2): “……Help ye one another in righteousness and piety,but help ye not one another in sin and rancour: fear Allah: for Allah is strict in punishment.” And Surah al-Baqarah (2:195): “Do good to others, surely Allah loves those who do good to others”. Surah Ali-Imron (3:92); “You cannot attain to righteousness unless you spend (in charity) out of those things which you love”.

10

Bangladesh. At present GB is the largest microfinance bank in Bangladesh and probably the biggest microcredit organization in the world - which provides loans to assetless and landless poor people whom no commercial bank give loan. It is only as an example of a social entrepreneur who struggle in the fight for the fate of the poor with a very spectacular results, and gain worldwide recognition. This example also shows the important role of social entrepreneurship in the eradication of poverty.

Currently it has many emerging Islamic microfinance institutions are deliberately set up to participate fully eradicate poverty by helping the poorest of the poor with the empowerment model (business development) by providing benevolent loans (Qard Al-Hasan financing). It is interest-free system which is very different from GB operational system (interest system/riba), because Islam forbids riba. Besides, it has been emerging institutions of waqf manage endowments productive (cash waqf for example) for the empowerment of the poor through a variety of activities that are very useful, and even appeared zakat institutions run by both government and private, which distributes most of zakat funds for productive purposes (in many sectors) to provide job for the poor. All of these may be the part form of Islamic social entrepreneurship - that may still need to be encouraged and fought for progress. Islam encourages entrepreneurship development for economic growth (Sadeq, 1991).

Problems faced - today and probably the next few years - is the poverty rate is quite high and spread in various places (suburban and rural) in many countries - in which it demonstrates the need for a lot of social entrepreneurs who are ready fought to help the poor in order to escape from poverty and secure from economic and social vulnerability. Are social entrepreneurs could be borne by itself or is necessary to establish and build awareness? Perhaps Islamic universities need to prepare candidates for social entrepreneurs. How is the role of the state?

The state shall provide financial assistance, incentives and other services to enable social enterprises to develop into viable and vital anti-poverty agents, and a strong social entrepreneurship movement.

VI.An integrative approach for overcoming poverty and improve economic security

Poverty has been a great threat to faith (beliefs), moral attitudes, worldviews, family lives, and gaining and maintaining individual and societal needs (Guner, 2005; Al-Qardhawi, 2006). Therefore some serious precautions need to be taken to hinder poverty and to maintain the prosperity of the society during his lifetime. Creating job for the poor is one of the solutions, because the work is the main weapon to solve the problem of poverty. In the previous section has discussed how the role of Islamic micro-finance, zakat, waqf and social entrepreneurship to poverty reduction which shows that microfinance, zakat, waqf and social entrepreneurship has an important role. It means that various approach can be undertaken to reduce poverty.

First, that creating selfemployment/job (through microcredit/microfinance) in the rural areas and suburban can play a vital role in reducing the unemployment and acute poverty, since microfinance has enabled the poor to undertake diversified economic activities which generate flow of stable income round the year and thus has strengthened survival strategy of the poor (Kumar, et al., 2013), and then it becomes reasonable if microfinance constitutes the most useful and popular financial system in the world to face financial crisis of the poor people (Islam, et al., 2012). Therefore, Islamic microfinance (in particular via qard al-hasan financing) need to be developed to become a model of eradication of poverty throughout the world especially for the poorest of the poor. Through the qard al- hasan financing, the poor

11

will be able to rise up to build the quality of their lives to a better level, because they only have an obligation to return the principal without additional burden as imposed on the model of other financing or without having to pay interest expense (which is common high) as is the case in conventional loans. This financing model is based on an attitude of compassion and mutual help which are highly recommended in Islam.

Second, the main objective of the institution of zakat is to redistribute income in favor of the poor within a community, so that they are able to upgrade their lives to a least a minimum level of quality living. For this pupose, zakat distribution can take place in two catagories; (i) direct distribution (non productive) for who are not capable of working, and (ii) zakat become resources to run activities that can bring in income and hence, improve the lives of the poor (Abu Bakar and Abd. Gani, 2011). In such a way that the distribution of zakat will be able to produce a greater benefit to the community in order to reduce poverty and improve the quality of live and economic security of poor people in the lowest layer (the poorest of the poor). (Afzalurrahman1 (997) states that zakat constitutes an effective method to reduce the economic difference in the community so there is no neglected people and live in poverty.

Third, the concept of waqf is a well-practiced phenomenon in recent times in both the Muslim and non-Muslim world (Kahf, 2006). This indicates that the waqf has become a model / approach to empowerment is to be universally applicable in various places around the world.

Results of waqf property is repeated (continuously), therefore it becomes very possible to be a source of funding to long-term programs, such as for the empowerment of the poor, given that empower the poor (especially the poorest of the poor) require a long time.9

Four,by its nature, social entrepreneurship is expected can play an important role in development in which it encourages community building, which in turn can facilitate development and poverty reduction. Social entrepreneurship encourages the creative problem solving of community groups when it places community needs and ideas first and prioritizes the development of skills and creativity of community. Social entrepreneurship as well is a door opener and a bridge towards change and development community to better levels - the reduction of poverty and increasing people's welfare. However, to achieve significant benefits of social entrepreneurship, the social entrepreneurship should be prepared more systematically and should state takes on the role (state-led) in this regard (Schneider and Nega, 2013).

For the realization of poverty eradication widely (nantional) and comprehensively, then the cooperation of various parties (the institution of zakat, waqf, IMFI and the institution of da‟wah) is needed to complement and support each other, with the involvment of social entrepreneurs (in each institution) as a humanitarian fighter, defender of the poor, as well as defenders of Islam.10 Improved economic security of the poorest communities can be described briefly as follows; that institutions of zakat and waqf provide funds for IMFI, da‟wah activity and other productive activities aimed at the poor, while social entrepreneurs (with a social mission that is very powerful, creativity and the ability of innovation, as well as

9It refers to philantrophic waqf whic aims at supporting the poor segment of the society and all activities that are of interest to the community such as the poor and needy, education, health services, etc.

10Hasan (2010) warns that poverty eradication should be based on the principles of Islam, which is based on the Islamic views of social justice and the belief in Allah Almighty.

12

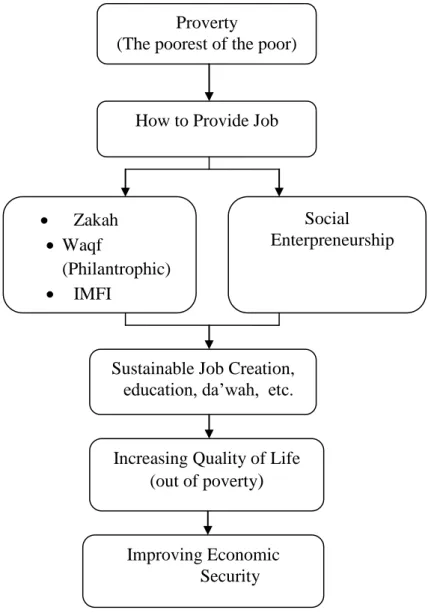

the encouragement of da‟wah mission) develop activities and do control for poverty alleviation programs. The expected results are; increasing the quality of life, reducing the poverty rate, and reducing vulnerability of the economic life of society (as a form of increasing the economic security). An integrated Islamic approach in improving economic security the poorest of the poor can be summarized as follows:

Figure 3: Improving economic security the poorest of the poor.

The challenge to improve the economic security of society with this approach is the preparation of social entrepreneurs (high quality) in large numbers; governments and universities need to take the role.

VII. Conclusion.

Poverty is still a problem in many parts of the world including Muslim countries. Various efforts have been done, however issue of poverty has still not getting satisfactory for resolution. It illustrates that the economic and social security of the poor is still weak, and needs to be addressed to find a way out. Poverty has multidimensional characteristics (and complex); this would jeopardize the social and economic security of poor people and then

Proverty

(The poorest of the poor)

How to Provide Job

Improving Economic Security Increasing Quality of Life

(out of poverty) Sustainable Job Creation,

education, da‟wah, etc.

Social Enterpreneurship

Zakah

Waqf

(Philantrophic)

IMFI

13

need to be reduced. Poverty reduction requires a multi-dimentional approach, and creating job/employment for the poor is one of the solutions, because the work is the main weapon to solve the problem of poverty, and for Muslims, the work is part of worship. The problem is that not all poor people could work because of the limitations they have. Because of the complex and the extent of the poverty issue, a single approach is not enough and then the solution requires an integrated approach by involving Islamic instruments such as zakat, waqf,Islamic micro finance institutions and also involving social entrepreneurship to obtain greater thrust. Social entrepreneurship constitutes a key to poverty reduction. It is increasingly being viewed as a way to reduce poverty, to pursue entrepreneurial strategies that are conceptually related to the effectiveness of the eradication of poverty. To be able to perform these tasks, it requres social entrepreneurs those who have a powerful ability and innovative, the reformers and revolutionaries with a social mission. However, it must be noted that poverty eradication should be based on the principles of Islam, which is based on the Islamic views of social justice and the belief in Allah Almighty.

Refferences

Abdullah, M.A and Hoetoro, A. (2011). Social Entrepreneurship as an Instrument to Empowering Small and Medium Enterprises: An Islamic Perspective. International Journal Management and Business Research, Vol. 1, Issue 1: 35-46.

Abdullah, D.V and Keon Chee. (2010). Islamic Finance Why it Makes Sense. Singapore:

Marshall Cavendish Business.

Abu Bakar, M.H., Abd, Gani, A.H. (2011). Towards Achieving the Quality of Life in the Management of Zakat Distribution to the Rightful Recipients (The Poor and Needy).

International Journal of Business and Social Science. Vol. 2 No. 4; 237-245.

Adebayo, R.I., and Hasan, M.K. (2013). Ethical Principle of Islamic Financial Insitutions.

Journal of Economic Cooperation and Development, Vol.34 No. 1; 63-90.

Afzalurrahman. (1997). Muhammad sebagai seorang pedagang. Jakarta: Swarna Bhumy.

Ahmed. H. (2004). Role of Zakah and Awqaf in Poverty Alleviation. Occasional Paper No. 8. IRTI Islamic Development Bank.

Al-Qardhawi, A.Y. (2006). Economic Security in Islam. New Delhi: Islamic Book Service.

Alathary, A. (2013). Islamic Microfinance in Yemen: Challenges and Opportunities.

http://www.cgap.org/blog/islamic-microfinance-yemen-challenges-and-opportunities.

Accessed on October 10, 2015.

Ali, I and Hatta, Z.A. (2014). Zakat as a Poverty Reduction Mechanism Among the Muslim Community: Case Study of Bangladesh, Malaysia, and Indonesia. Asian Social Work and Policy Review, 8 (2014): 59–70.

Ali, I.B. (2009). Waqf a Sustainable Development Institution for Muslim Communities.

Takaaful T&T Friendly Society:Valsayn Trinidad and Tobago. www.takaafultt.org. AsadEjaz and Ramzan, M. (2012). Microfinance and Entrepreneurship –A Case Study of

Akhuwat. Interdisciplinary Journal Of Contemporary Research In Business, Vol 4, No. 7: 305 – 324.

Barber, K. (2012). Social Entrepreneurship: A Key to Poverty Reduction and Agorism.

http://studentsforliberty.org/blog/2012/12/28/social-entrepreneurship-a-key-to- poverty-reduction-and-agorism/. Accessed on November 0, 2015.

Clark, M. (2009). The Social Entrepreneur Revolution. London: Marshall Cavendish Business.

14

Dees, J.D., Miriam, and Haas, P. (1998). The Meaning of “Social Entrepreneurship”.

http://sehub.stanford.edu/sites/default/files/TheMeaningofsocialEntrepreneurship.pdf.

Accessed on November 04, 2015.

Faizal, P.R.M., Ridhwan, A.A.M., Kalsom, A.W. (2013). The Entrepreneurs Characteristic from al-Quran and al-Hadis. International Journal of Trade, Economics and Finance, Vol. 4, No. 4: 191 – 196.

Guner, O. (2005). Poverty in Traditional Islamic Thought: Is it Virtue or Captivity? Studies in Islam and the Middle East [SIME], Vol. 2, No. 1: 1-12.

Hasan, S. (2007). Philanthropy and Social Justice in Islam. Kuala Lumpur: Zafar Sdn. Bhd.

Hasan, M.K. (2010). An Integrated Poverty Alleviation Model Combining Zakat, Awqaf and Microfinance. Seventh International Conference The Tauhidi Estimology: Zakat and Awqaf Economy; Bangi Malaysia.

Hassan, M. K., & Khan, J. M. (2007). Zakat, external debt and poverty reduction strategy in Bangladesh. Journal of Economic Cooperation, 28(4): 1–38.

Hoque, N., Khan, M.A., Mohammad, K.D. (2015). Poverty alleviation by Zakah in transitional economy: a small business entrepreneurship frame work. Journal of Global Entrepreneurship Research, 5:7 ; 1-20.

Ismail, A.I. (2013). True Islam, Moral, Intelektual, Spiritual. Jakarta: Mitra Wacana Media.

Islam, J.N., Mohajan, H.K., Datta, R. (2012). Aspects Of Microfinance System Of Grameen Bank Of Bangladesh Int. J. Eco. Res. v3i4: 76-96.

Kahf , M. (2014). Role of Waqf in Sustainable Development (P. 1).

http://www.onislam.net/english/shariah/contemporary-issues/islamic-themes/452483- type-goals-islam-waqf-endowment-finance-economy.html. Accessed on November 1, 2015.

---. (2007). The Role of Waqf in Improving the Ummah Welfare, paper presented at the Singapore International Waqf Conference 2007 held in Singapore during March 6-7, 2007, organized by the Islamic Religious Council of Singapore, Islamic Development Bank, Islamic Research and Training Institute, Warees Investments Pvte. Ltd., and Kuwait Awqaf Public Foundation.

---. (2006). Role of Zakat and Awqaf in Reducing Poverty: a Case for Zakat-Awqaf-Based Institutional Setting of Micro-finance, Paper for the Conference on Poverty reduction in the Muslim Countries, Nov. 24-26, 2006

Kareem, R.O. (2015). Impact of Entrepreneurship on Poverty Alleviation. Journal of Business Administration and Education. Volume 7, Number 1:1-16.

Khan, A.A. (2008). Islamic Microfinance Theory, Policy and Practice. Birmingham UK:

Islamic Relief Worldwide.

Khan, M. A. (No Year). Economic Teachings of Prophet Muhammad. Karachi: Darul Ishaat.

Kumar, D., Hossain, A., Gope, M.C. (2013). Role of Micro Credit Program in Empowering Rural Women in Bangladesh: A Study on Grameen Bank Bangladesh Limited. Asian Business Review, Volume 3, Number 4/2013 (Issue 6): 114 - 120

Luke, B., and Chu, V. (2013). Social enterprise versus social entrepreneurship: An

examination of the „why‟ and „how‟ in pursuing social change. International Small Business Journal, 31(7): 764–784.

Makhlouf, H.H. (2011). Social Entrepreneurship: Generating Solution to Global Hallenges.

International Journal of management & Information System, Vol.15 No.1: 1-8.

Mannan, M.A. (1986). Islamic Economics: Theory and Practice. Cambridge: Hodder and Shoughton.

Naeem, K. (2012). Innovation In Islamic Microfinance for Small Farmer in Sudan.

www.cgap.org/blog/innovation-Islamic-microfinance-small-famer-Sudan. Accessed on October 10, 2015.

15

Noruzi, M. R.. Westover, J.H. and Rahimi, G.R. (2010). An Exploration of Social

Entrepreneurship in the Entrepreneurship Era. Asian Social Science, Vol. 6, No. 6: 3- 10.

Qutb, S. (2000). Social Justice In Islam. Kuala Lumpur: Islamic Book Trust.

Rasjid, S. (2006). Fiqh Islam. Sinar Baru algensindo: Bandung.

Sadeq, A.H.M. (1991). Economic Development in Islam. Pelanduk Publication Sdn. Bhd:

Selangor, Malaysia.

Sabiq, S. (1987). Fiqih Sunnah 14. Bandung: PT. Alma‟arif.

Schneider, G and Nega, B. (2013). Democracy, Development and Comparative Institutional Advantage in Africa. Forum for Social Economics 42, 2‐3: 231‐247.

Shaikh, F. (2012). The Waqf Model and Poverty Alleviation.

http://socialfinance.ca/2012/08/22/the-waqf-model-and-poverty-alleviation/. Accessed on October 30, 2015.

Widiyanto, M.C.H, and Ismail, A.G. (2010). Improving the effectiveness of Islamic

micro‐financing: Learning from BMT experience. Humanomics, Vol.26 Issue 1: 65- 75.

Widiyanto, Mutamimah, Hendar. (2011). Effectiveness of Qard Al-Hasan Financing As a povery Alleviation Model. Economic Journal of Emerging Market. Vol 3. No.1: 27- 42.

Zahra, S. A., Gedajlovic, E., Neubaum, D. O., Shulman, Joel. M. (2009). A typology of social entrepreneurs: Motives, search processes and ethical challenges. Journal of Business Venturing 24: 519–532.

462598ISB31710.1177/02662 426124 62598In ternational Sm all Bus iness J ournalLu ke and Chu201 3