Additionally, to Ajarn Piyapas Tharavanij for improving understanding regarding valuation in terms of mathematical valuation for both relative valuation and discounted cash flow valuation. The firm's free cash flow represents the value of the firm's activities resulting from the root of the firm's value derived from future earnings.

VALUATION

Highlights

- CENTEL Go Smaller and Wider

- Diversified and Supportive Business

- Economic Recovery and Support

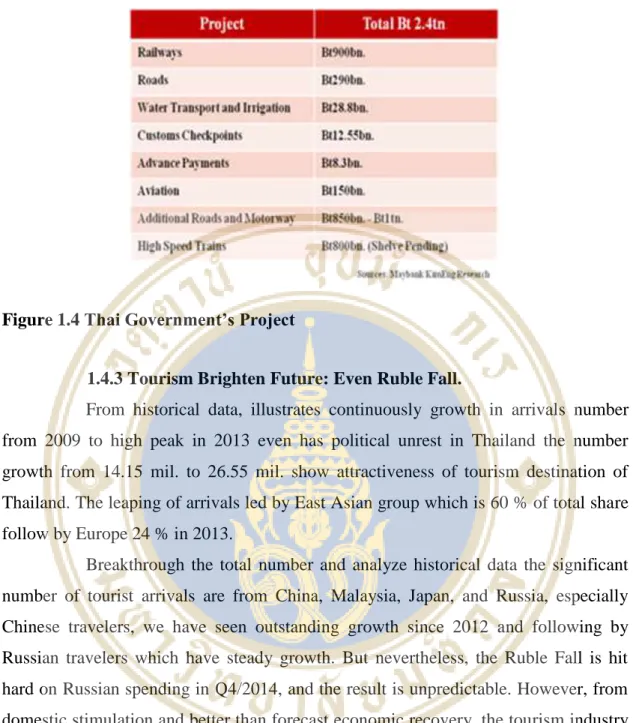

Due to the unstable political issue in Thailand, the number of tourists has dropped sharply, which directly affects CENTEL companies. However, the new government needs to increase the country's GDP and CPI, so it supports and initiates a promotion to persuade both Thai and foreign tourists to travel to Thailand.

Business Description

- Hotel Brands under CENTEL (Flagship) .1 Centara Grand Hotels& Resorts

- Food Chain Brands under CENTEL (Flagship) .1 Mister Donut

Centara Grands are classified as five-star hotels and resorts located in the capital city and along the coast, which are full of outstanding facilities and impressive services for a luxury value for the guest. The leading brand of soft pretzels in Thailand with the aim of being "the best snack chain" which has shown a remarkable growth in success in 2012.

SWOT Analysis

- Strength

- Opportunities

- Threat

The capital expenditure to maintain the same level of performance every year is also very high. So, the entry barrier and exit barrier are very high for the hospitality industry, while the business expansion to other locations is limited under the high price of real estate in tourist destination and also law and regulation of local government. Investing and owning a hotel is very difficult these days, so asset-light strategy is applied, but it may cause a management problem for CENTEL.

The reduction of capital usage from the management change gives free cash flow to decide on M&A transaction, for example for transactions considering the CLMV transaction (Cambodia, Lao, Myanmar and Vietnam), which the management team is very confident about their investment opportunity. The COSI project, under the strong brand and management team of "Centara", the COSI brand should respond well to the budget traveler's needs. The boom of Russia and China is very beneficial for CENTEL according to their strength and customer portfolio proves that two groups of customers are growing fast.

Nevertheless, CENTEL is a very strong player in the Southeast Asia region, but competing to prevent market share will be a crucial task for them.

Industry Analysis

- Well Macroeconomic: Oil Price& QE Driver

- Tourism Brighten Future: Even Ruble Fall

- F&B Industry: Confidence from Happiness

Breakthrough of the total number and analyze historical data, the significant number of tourist arrivals are from China, Malaysia, Japan and Russia, especially Chinese travelers, we have seen exceptional growth since 2012 and subsequently of Russian travelers, which has a steady growth. But nevertheless, the fall of the ruble has been hit hard by Russian consumption in the 4th quarter of 2014, and the result is unpredictable. The change in lifestyle and urbanization affects consumer behavior that tends to save time and healthy concerns, the food chain industry is reinforced by both drastic flow of behavioral changes.

Notably, Thai people prefer to eat out rather than cook for themselves, this sent the total value of the food chain industry to Bt96 billion. The coup d'état and the military government hit hard at the confidential level and broke domestic consumption. The result is a lower forecast if same-store sales growth (SSSG) declines to 5% from the 7% expected at the end of 2014.

As in the figure, we show the statistical data of 2013 both in the amount of income and in growth which illustrates the potential of spending outside the capital.

Competition Analysis

- Hotel Business: Place for Big Players

- Choices of Customer: Fast food or Japanese

In the F&B business sector, CENTEL and MINT decided on different actions, from the previous 10 years CENTEL had acquired many Japanese food brands such as Pepper Lunch, Chabuton, Ootoya and Yoshinoya with reasons due to the popularity of Japanese food in Thailand and the growth of considerably. in the quick service restaurant (QSR). CENTEL wants to prevent the leading position in QSR (all acquired brands are QSR: . Tepanyaki, Ramen, premium cooked food, one dish food). While MINT aims to revive the brand as Burger King tries to compete with major brands such as KFC and McDonald which command 53% and 10% of the fast food market share respectively.

The Terrace and also an acquired overseas Chinese restaurant. This deal is ongoing but not yet in the Red Ocean stage in this segment. Rapid urbanization and changing consumer behavior increase the CAGR of the food chain industry as predicted to 14%, in fact the number is higher than the average and also has a huge market gap available.

Investment Summary

- Cyclical Stock correlated with market and economic movement and leading indicators

- Huge massive tourism from China

- Not only Thailand but Maldives and Not only big but small one CENTEL has many hotels and resorts in Thailand, but the capacity is

Discounted Cash Flow Valuation

- Forecast Revenue Growth Rate

- Working Capital and Capital Expenditures Calculation

- Terminal Growth

- Weighted average cost of capital and FCFF Model

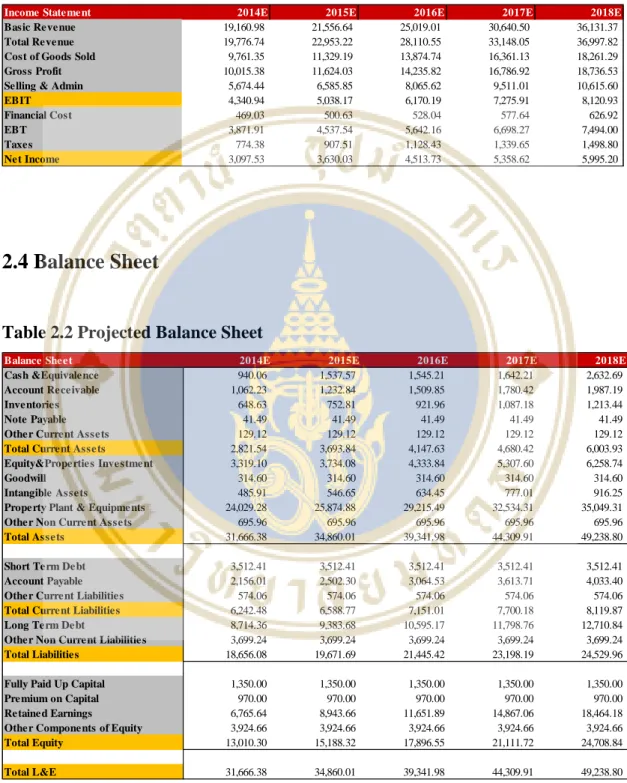

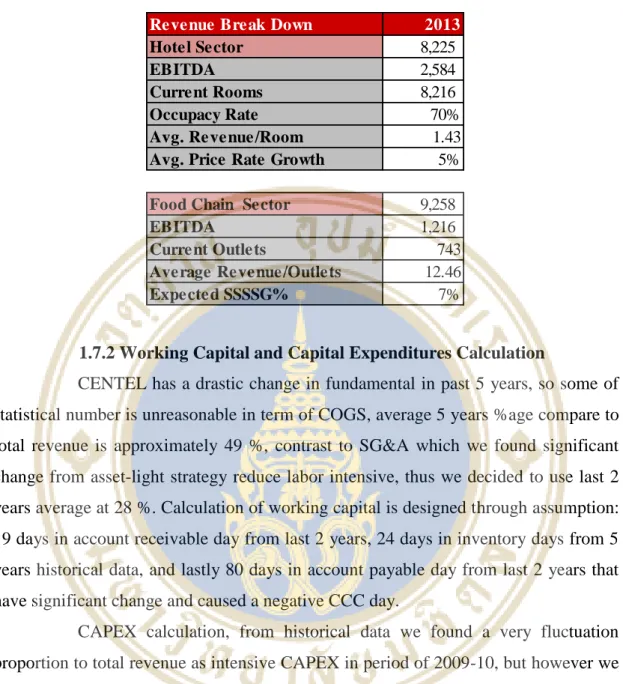

CENTEL has a drastic change in fundamental in the last 5 years so some of the statistical numbers are unreasonable compared to COGS, average 5 year % age compared to total revenue is approx. 49%, in contrast to SG&A, which we found significant change from asset-light strategy reduce labor intensive, therefore we decided to use last 2 years average of 28. CAPEX calculation, from historical data we found a very fluctuating share of the total turnover as intensive CAPEX in the period 2009-10, but we found a very stable figure in the last 3 years of approx. 11% compared to revenue, so we assume that the sustained CAPEX rate remains the lowest revenue growth of 9. In our assumption, we use average GDP growth to reflect terminal growth rate, in historical data Thailand GDP growth is approximately 5.

Nevertheless, on the negative side as a signal from the US on QE program, weak property sector and fear of debt default in China, and economic recession in Japan, on the reverse side of the coin, we have a positive signal as lower oil price, improvement in production number from the US and China, and finally mega projects in infrastructure investment, we therefore decided to use terminal growth of 4% as. WACC is calculated according to the assumption: first is the weight of the debt, we decided to use 5 years average debt ratio to represent the capital structure of the company, which gives a very stable figure of 0.67, the reason for no use the market value base is problematic around PE -ratio in 2013 -14 is overstated, second cost of debt, we use average 5 year historical cost of finance of 4.02% to represent CENTEL's ability to find cheap cost of finance, third is the risk premium for the market (Rm-Rf), we use geometric mean return of SET Index in past 10 years of 12.8% minus risk free rate of 3.62% from 10 year Thai government bond yield and finally CENTEL beta usage of 1.64 represents 3 year beta from Bangkok Business Newspaper. The FCFF model is formed to calculate the actual enterprise value and share price using working capital and CAPEX, terminal growth and WACC from previous assumptions.

In this case, CENTEL has a negative change in working capital due to negative CCC days that add value to the business.

Financial statement Analysis

- Size analysis: Income statement

- Size analysis: Balance sheet

- Trend analysis: Income statement

- Trend analysis: Balance sheet

- Cash flow statement analysis

- Liquidity and Solvency

- Profitability

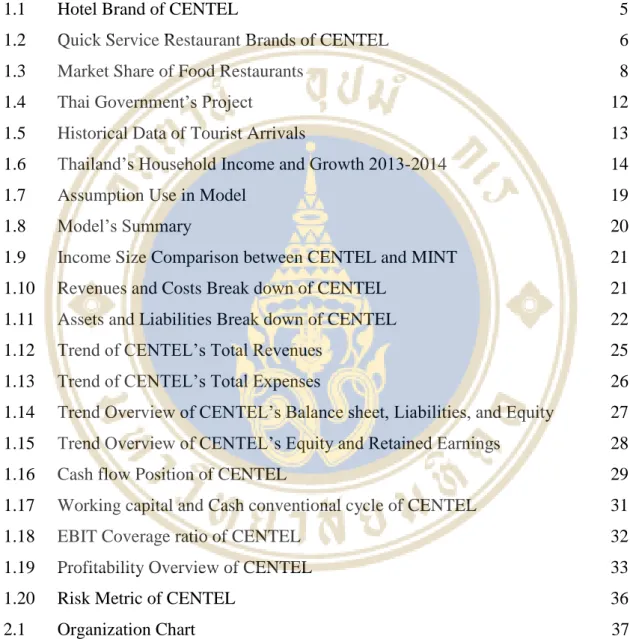

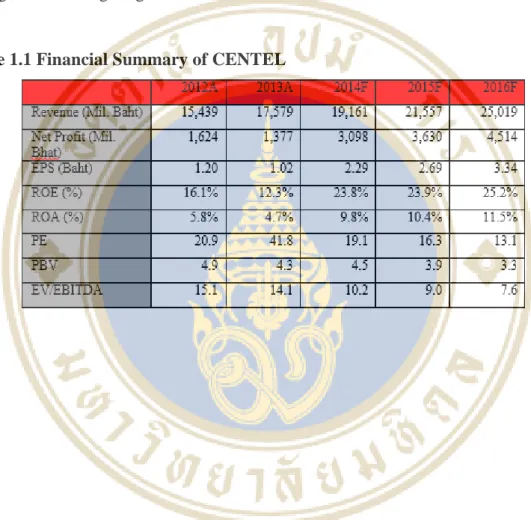

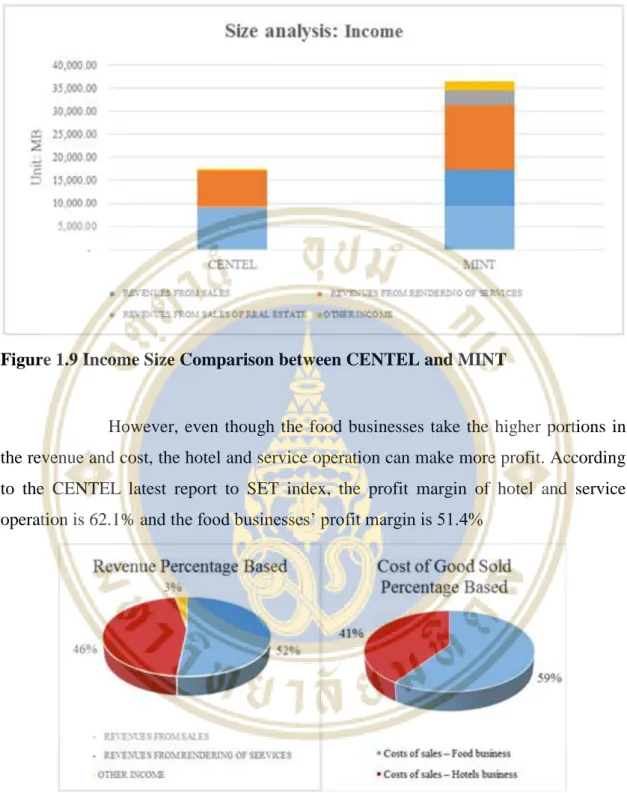

As a result of calculating the stock price through the FCFF method, we get a price of CENTEL of Bt43.85 per share. Most of CENTEL's assets are fixed assets, which account for 90% of total assets, as CENTEL has owned the hotels and resorts in Thailand and other countries. Because CENTEL needs a lot of money to expand its business, the most important part of CENTEL's liability is its long-term liability, namely long-term debt.

Although MINT has the highest proportion of current assets, CENTEL relies on the higher proportion of current liabilities. According to the profit in each year of CENTEL, the retained earnings of CENTEL is also increasing every year with the average growth rate of 33.08. Historical EBITDA for CENTEL illustrates a good form of ongoing earnings growth via flagship hotel drivers, particularly the Maldives, which showed significant growth of approximately 20%.

To summarize cash flow position of CENTEL is very strong and healthy, continuous growth in EBITDA and debt repayment will lead to lower financial risk and better liquidity. In fact, collected data over 5 years is represented as bad day of CENTEL, but they still show a good performance and therefore we have a very positive view about our research. Debt to equity ratio and interest coverage ratio of CENTEL is improved year by year from higher internal fund generation, Beginning of debt to equity ratio, from 2009 to 2011 showed high financial leverage and low bargaining power to suppliers (shown in AP days about 40 days ), significant change occurred in 2012. DE ratio decreased from 2.58 to 1.76 and also in interest coverage ratio in 2011 and 2012 at 3.04 and 4.78 respectively, in working capital management we tend to see an improvement in cash convention cycle (CCC days) in 2012 to see. which came from the jump of account payable day (AP Days) from 40 days to 80 days.

Investment Risks and Downside Possibilities

- Investment Risks

- Additional Downside Possibility

- Risk’s Summary

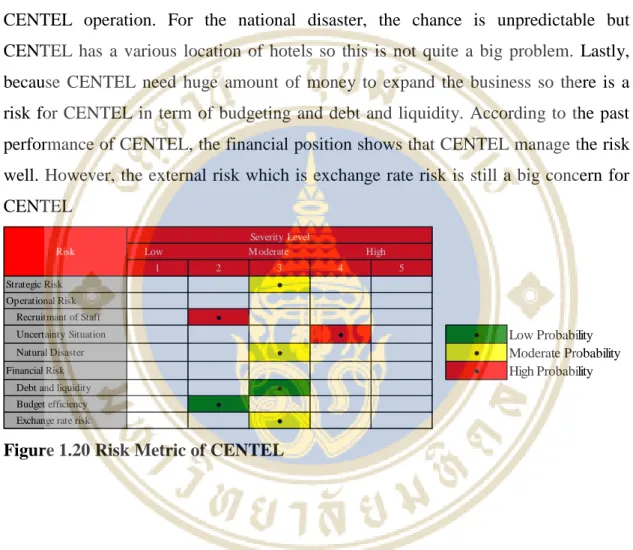

Not only efficiency of funds but CENTEL should also be concerned about their liquidity and the cost structure of capital, D/E ratio because it will affect the credibility of CENTEL to the investors. To avoid this risk, CENTEL can therefore use the financial instrument to hedge the exchange rate risk. Strategic risk is moderate because the analysis teams of CENTEL are professional and have a lot of experience, but the situation keeps changing every year so it can cause the wrong decision.

For operational risk, CENTEL does not have to worry more about the risk from their staff due to difficult selection and training of employees. However, the policy in Thailand is not stable so there may be a threat to the operation of CENTEL. Finally, because CENTEL needs a large amount of money to expand the business, so there is a risk for CENTEL in terms of budgeting and debt and liquidity.

However, the external risk, which is exchange rate risk, is still a major concern for CENTEL.

DATA

- CENTEL Organization’s Chart

- Five Forces Analysis

- Buyer Power (Rating Hotel: Moderate, F&B: Strong)

- Supplier Power (Rating Hotel: Moderate, F&B: Weak)

- New Entrants (Rating Hotel: Weak, F&B: Strong)

- Threat of Substitutes (Rating Hotel: Weak, F&B: Strong)

- Degree of Rivalry (Rating Hotel: Moderate, F&B: Strong)

- Income Statement

- Balance Sheet

- Statement of Cash Flow

- Financial Ratios

In low-end segment (1-2 stars) is completely contrast with previous segment, price sensitivity has become significant factor and few big players compete in this segment, means opportunities for well-known brand to utilize buyer power. The overall sales volume of quick service restaurant (QSR) and large number of sales channels create a very high bargaining power of buyers for QSR segment and reduce the bargaining power of ingredient suppliers. The change in consumer preference, which tends towards concern in premium experience, brand recognition has become more important and operating costs increase through product and service differentiation.

Moreover, the hotel industry is heavily dependent on tourism prospects and tends to seasonal performance, which is why small and sour financial players survive in the long run. The market outlook for the food and beverage industry is in good shape due to urbanization and middle class boom. Drastic changes in consumer behavior are the most important factor creating new substitutes in the form of fashion and new offerings.

Meanwhile, the exit barrier is also very low, so the level of rivalry is very strong in the form of price war and product differentiation.