Ekkachai Keeratikittrin and Miss Kanthika Boonyakarn for their grateful knowledge sharing in relation to alternative energy sectors, their helpfulness in collecting information from Bloomberg, I would not have come this far and this thematic paper would not have been completed without all their support as I always have received from them. Finally, thanks for all the academic support from the College of Management, Mahidol University program coordinators throughout the courses that help make this thematic paper a perfect end. This thematic paper intentionally illustrates the discounted cash flow valuation on my company of interest, SPCG Public Company Limited, which reflects the value of the company and ultimately investment decisions.

I used the concept of the discounted cash flow valuation model, which is financial planning to project a company's cash flow, weighted average cost of capital, and terminal value to determine the reasonable value of the company.

VALUATION

Highlights

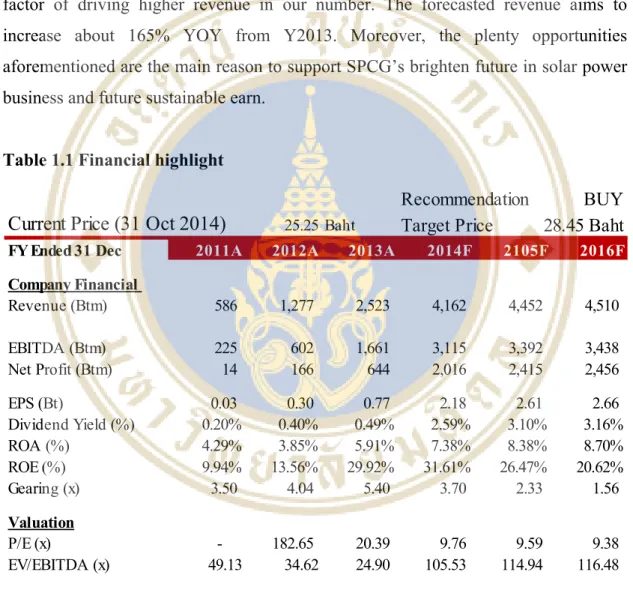

By taking advantage of the refinancing of debt from a 10-year bridging loan to 5-year bonds with a lower interest rate, this will significantly reduce SPCG's financing costs in 2014. Together with the completion of the start of the commercial electricity distribution from 36 solar farm projects in the second quarter of 2014 will lead to increased efficiency, operating costs and SG&A costs, which is the key factor in generating higher revenues for our number.

Business Description

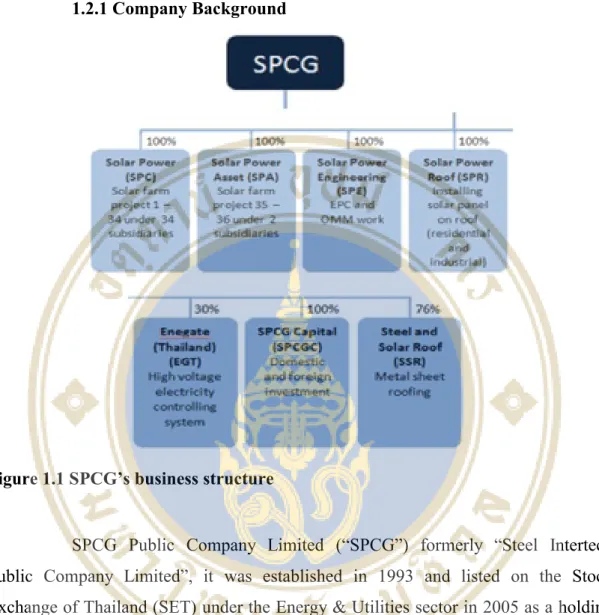

- Company Background

- Overall Business Operations

The Ministry of Energy announced its support for renewable energy and alternative energy policies, after which SPCG merged with Solar Power Company Limited ("SPC") in 2011 to develop its existing 34 solar power projects under a purchase agreement power agreement (PPA) with the Provincial Electricity Authority ("PEA"). SPCG currently has a total of 36 solar power projects in Thailand with a total of approximately 261 MW in 10 provinces throughout Northeast Thailand and Lopburi Provinces with a total area of approximately 5,000 Rai (2,000 hectares). SPCG continues to provide a full range of solar power plant services and also has a Solar Power Engineering Company Limited (“SPE”) which aims to provide Engineering, Procurement and Construction (EPC) services and to provide Operation, Maintenance and Monitoring (OMM). Service of solar power plants at home and abroad.

As its solar farm projects located in rural Thailand, which has helped improve skills, knowledge and the quality of life of rural Thais and helped boost Thailand's economy over the past 5 years. It continues to investigate the solar farm's operations to operate its solar farm as clean energy that produces no pollution, no noise, no dust and no fuel costs in electricity generation, as well as helping to reduce global warming due to climate change. SPCG operates in 3 main businesses 1) Investment and Development of Sonplaas Engineering, Procurement and Construction (EPC) and Operation, Maintenance and Monitoring (OMM) 2) Manufacture, distribution and installation of roll forming metal sheet including other related roof and wall cladding materials and 3 ) Supply and installation of Solar Rooftop for residence, small building and medium and large building.

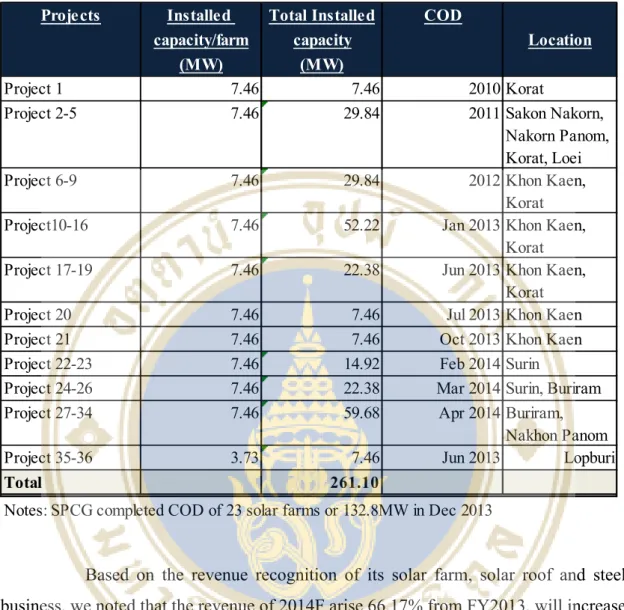

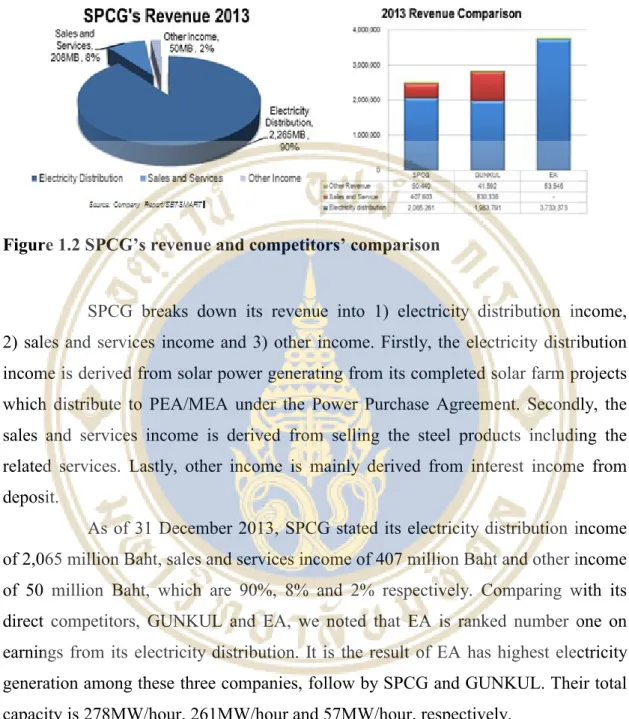

In terms of the financial results, the revenue breakdown is 1) electricity distribution derived from its solar farm projects and solar roof business, 2) sales and service of solar roof and steel business and 3) other income ie. according to the above breakdown of SPCG's revenue, SPCG's main income comes from the electricity distribution that SPCG earns from its completed 23 solar farm projects. Based on the revenue recognition of its solar park, solar roof and steel business, we noted that the revenue for 2014F arises by 66.17% from FY2013, will increase from the additional completed solar plant project, which will be fully completed in Q2'.

Macro-Economic Analysis and Industry Analysis

In addition, the Alternative Energy Development Plan 2015-36 will be implemented in parallel with the new PDP policy. According to the new PDP 2015, the share of alternative energy should increase by 25% of the country's total capacity by 2013, which will attract investment in the alternative energy sector. Based on the increasing 25% share of alternative energy, we estimate that new solar capacity will increase to 4,600 MW (17%) assuming 27% of the total forecasted alternative energy capacity in 2030.

In addition to the great opportunities mentioned above, he pointed to new solar power plant projects; The Power Purchase Agreement (PPA) will change from the "Adder" subsidy scheme to According to the Adapted Alternative Energy Development Plan (AEDP) under the new PDP 2015, we found that solar power capacity is expected to increase to 3,000 MW by 2021. Of the original target of 2,000 MW of solar energy, only 1,493 MW is in solar plant capacity. got a PPA.

The remaining 500MW+ capacity will need to be added to meet the AEDP's target.

Competition Analysis

- Competition Analysis

- Competition Opportunities

EA is a company that produces and distributes biodiesel (B100), diesel fuel, pure glycerine and raw materials and by-products. The company also has a business involved in the production and distribution of electricity from solar energy, such as biodiesel and renewable energy. GUNKUL is a manufacturer of electrical power systems and renewable energy systems with a variety of products.

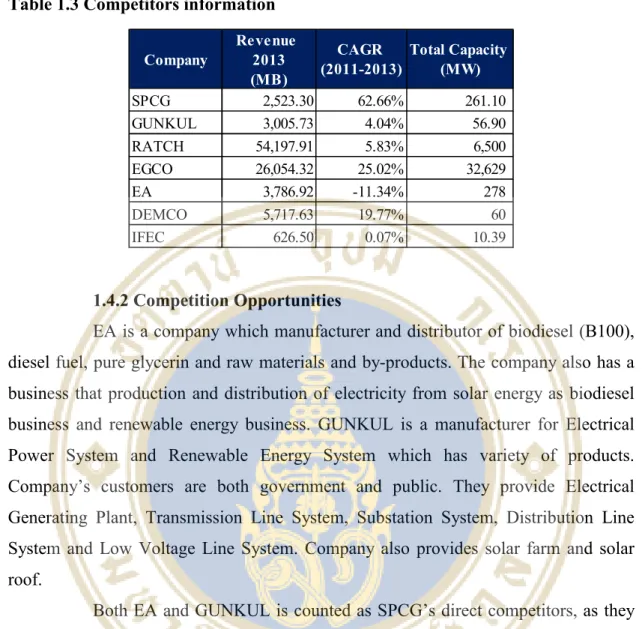

They provide power generation plant, transmission line system, substation system, distribution line system and low voltage line system. Both EA and GUNKUL are considered direct competitors of SPCG as they are both producers and distributors of solar energy. Comparing each company's own solar power capacity, we observed that EA is the largest player in the solar industry, followed by SPCG and GUNKUL respectively.

To increase its solar power capacity as the opportunity opens under PDP 2015, SPCG is expected to be the first rank of beneficiaries gaining more experience under solar farm operator, rooftop solar installation as SPCG is the pioneer in rooftop business guarantees solar. Meanwhile, GUNKUL will benefit more from the EPC assignments from its greater experience compared to others. The offer to continue will be the main revenue growth assumption among the three of them.

Investment Summary

The total investment cost of the factory is expected to be approximately 1.0 billion Baht (or 100 million Baht for SPCG's portion). In the initial stage, the factory will be able to produce up to 1MW of solar modules per year, but the capacity can be increased to 5MW per year in the future. SPCG expects to start production of 1MW of solar modules in early 2015.

With these announcements both positive for SPCG as they will add value and increase future cash flow for the company. Although the expected return from the solar farm project in Japan is not particularly attractive compared to the company's projects in Thailand, due to the higher investment cost (mainly due to higher land prices) and the availability of more low sunlight, we believe this move will open a new channel of investment for SPCG internationally. As for the investment in the solar module manufacturing plant, we expect it to create cost savings for future solar projects and also generate small incremental cash flows for the company.

Valuation

- Five-Years Projected Cash Flow

- Weighted Cost of Capital (WACC)

- Terminal Value

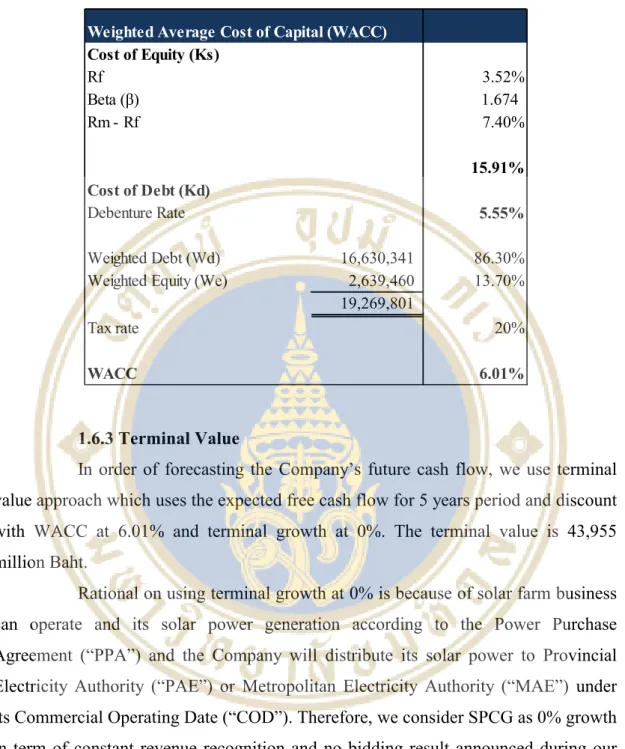

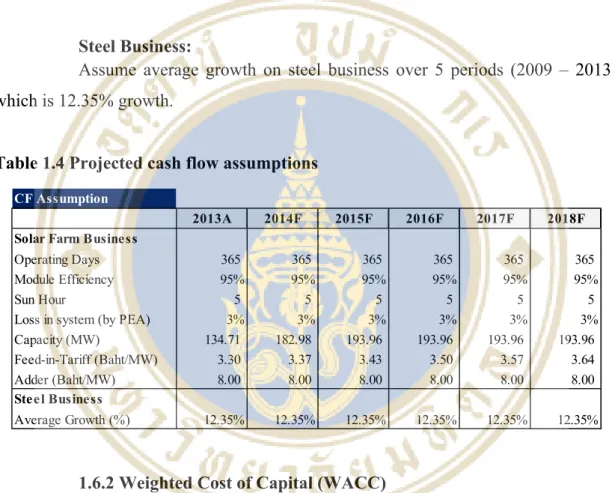

Solar Power Plant Capacity – SPCG Solar Power can now generate a total of 261MW across its 36 solar power projects, assuming its solar module can generate 95% efficiency. Capital Expenditure (CAPEX) – Since there is an additional result of bidding for the solar power plant project, SPCG maintains its CAPEX amount at an average of 10 million baht per year for the maintenance cost of the solar power plant project during its operation. Under a business model that has a funding policy of 86:14, SPCG's cost of debt was derived from its current debenture rate of 5.55% (before tax).

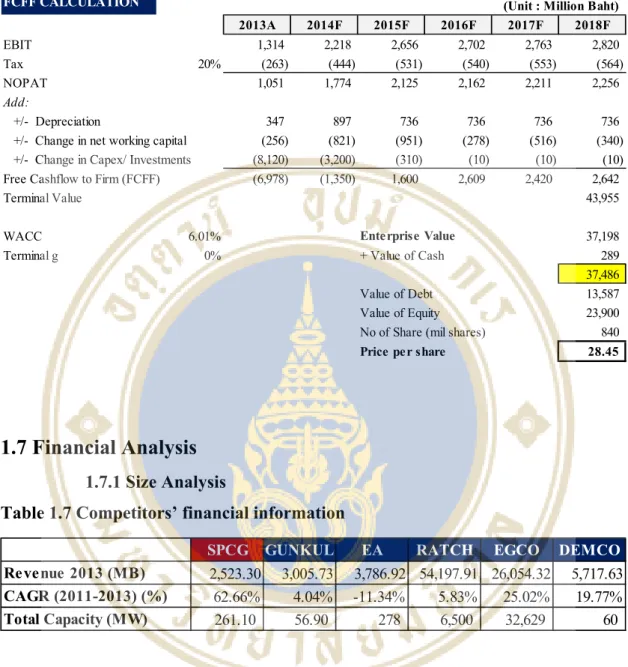

To forecast the Company's future cash flow, we use the terminal value method which uses expected free cash flow over a 5-year period and discounts with WACC at 6.01% and terminal growth at 0%. The rationale for using the 0% terminal increase is because the solar farm business can operate and generate its own solar power under a Power Purchase Agreement ("PPA") and the Company will deliver its solar power to the Authority. Provincial Electricity Authority (“PAE”) or Metropolitan Electricity Authority (“MAE”) according to its commercial operation date (“COD”). Therefore, we consider SPCG as 0% growth in terms of ongoing revenue recognition and no tender results announced during our assessment period.

However, any additional bidding result or PPA submission will count as a benefit to the company.

Financial Analysis

- Size Analysis

- Common Size Analysis

- Trend Analysis

- Financial Ratios

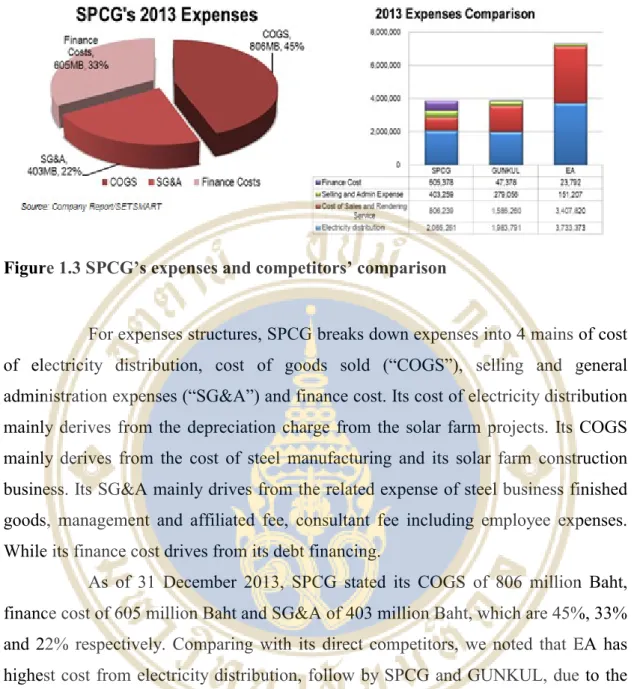

Compared to its direct competitors, we observed that EA has the highest electricity distribution costs, followed by SPCG and GUNKUL, due to the different proportion of the total capacity that the company could generate. SPCG's liability side is mainly long-term borrowing, according to the company's financing policy, which will finance 75% debt and 25% equity when investing in its solar power plant project. Also on the assets and liabilities side, it increases in line with the number of solar power plant projects that the company has invested in.

According to the main assets that will generate income for the company are its solar farm projects, the efficiency ratio shows increasing trends since 2011A to 2018F. To support the company's better performance, its profitability ratio shows ever-increasing trend of its total revenue, its net profit margin, its ROA and its ROE during the forecast period, which will be good reasons to say that the company has its good performance at least over 25 years according to the PPA sustainable. The interpretation of current ratio shows how capable the Company can meet its obligation in 12 months.

Considering the solvency risk itself in SPCG, we have observed that the Company has high risk in relation to its funding policy which will use 75:25. Higher D/E ratio indicates higher leverage and also indicates higher financial risk of the company. Additionally, the Company is dealing with debt refinancing which may reduce its interest in the company's leverage and long-term management.

Investment Risks

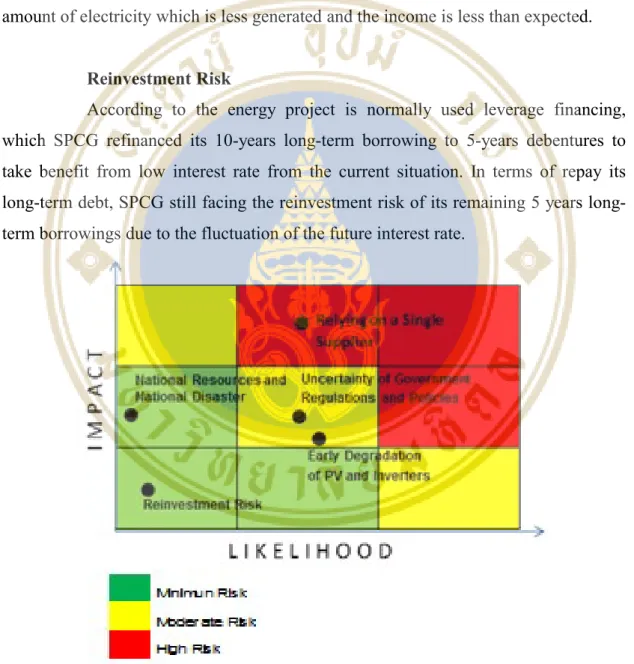

One of the factors that results in the amount of electricity is the breakdown of solar panels. If the breakdown is earlier than usual, it can have an impact on the amount of electricity, which is less produced, and the income is less than expected. According to the energy project, gear financing is usually used, which SPCG refinanced its 10-year long-term loans into 5-year bonds to take advantage of the low interest rate from the current situation.

Regarding the repayment of its long-term debt, SPCG still faces the reinvestment risk of its remaining 5-year long-term loans due to fluctuations in future interest rates.

DATA

Income Statement

Balance Sheet

Statement of Cash Flow

Common Size

Trend

Financial Ratio

WACC Calculation

Discounted Cash Flow Calculation