Finally, I am also grateful to all the respected lecturers on the Bachelor of Business Administration for their continuous inspiration and assistance over the years. Accordingly, while processing and evaluating a loan proposal, banks essentially analyze the information about borrowers, assess the purposes of the loan and determine the viability of the loan proposal. The report discusses the management practices of various credit facilities, approval process, monitoring and performance of the bank under investigation.

Third, concept and analysis of the impact of loans and advances and also guidelines from the Bangladesh Bank. In the introductory part of the report that discussed the origin of the report, it was mentioned that this report is part of the fulfillment required to complete the BBA degree under the Sonargaon University curriculum. The purpose of the report is to analyze the credit business of Janata Bank Limited.

But the management of the bank is now very concerned and proactive about the collection of loans. This bank should be more aware of the analysis of the repayment capacity of the borrower, the value of the collateral and the risk involved. As a state-owned bank, Janata Bank Ltd.

Findings & Analysis

Recommendations & Conclusion

- Introduction

- Origin of the Report

- Purpose of the Report

- Scope of the Study

- Objectives of the Study

- Methodology of the Study

- Research Design

- Sources of Information

- SAMPLE INFORMATION

- PRIMARY SOURCES OF DATA

- SECONDARY SOURCES OF DATA

- Limitations of the Study

- Literature Review

- History of Janata Bank Ltd

- Vision of Janata Bank Ltd

- Mission of Janata Bank Ltd

- Janata Bank Ltd at a glance

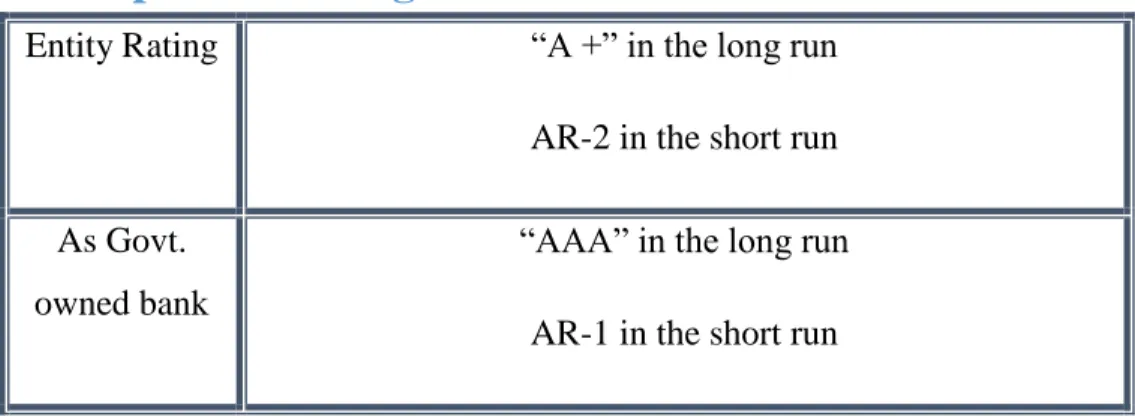

- Corporate Rating Status

- Management system

- ORGANIZATIONAL STRUCTURE OF JANATA BANK LTD

- Products

The level of literacy in the country is very low; therefore, the skills of the labor force are also low. This report contains descriptive analysis and theoretical approach as it is based on the analysis of loan and advance activities of JBL. The main source of information is Janata Bank Limited annual report, annual meeting report, brochures and websites.

The number of committees appointed by the government of Bangladesh have also looked into the country's banking problems. In the ability of craftsmen to meet the bank's requirements to use easy loans has forced. In the survey, they state that most of the borrowers use medium and long-term loans for their personal and unproductive purposes.

The objective of the scheme cannot be achieved if such loans are made to financially healthy persons. The research also shows that the bank loans contribute to the generation of employment and income of the people, thereby increasing the living standards of the poor. They also believe that the government's policy of loan forgiveness makes it more difficult to get bank loans back.

Janata Bank Limited, one of the state-owned commercial banks in Bangladesh, has an authorized capital of Tk.

Services

SWOT Analysis Strengths

Weaknesses

Strengths

Threats Opportunities

Opportunities

Threats

- Business Area of Janata Bank Ltd

- Sector wise Loans and Advances are shown below

- Risk Management

- Character

- Capacity

- Capital

- Conditions

- Collateral

- Cash Flow

- Types of Credit Risk Management

- Objectives of Loans and Advances Policy

- Lending guidelines

- Types of credit facilities

- Essential Components of Loans and Advances Policy

- Loan Sanction Activities

- Nature wise distribution of loans and advances

- Maturity grouping of distribution loans and advances

- Securities in credit management

- Basel II Compliancy

- Core capital (basic equity or Tier 1)

- Supplementary capital (Tier 2)

- Short-term subordinated debt covering market risk (Tier 3)

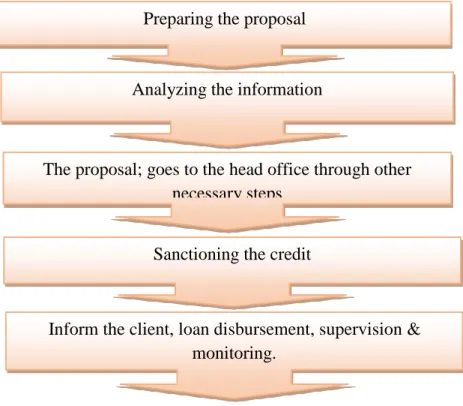

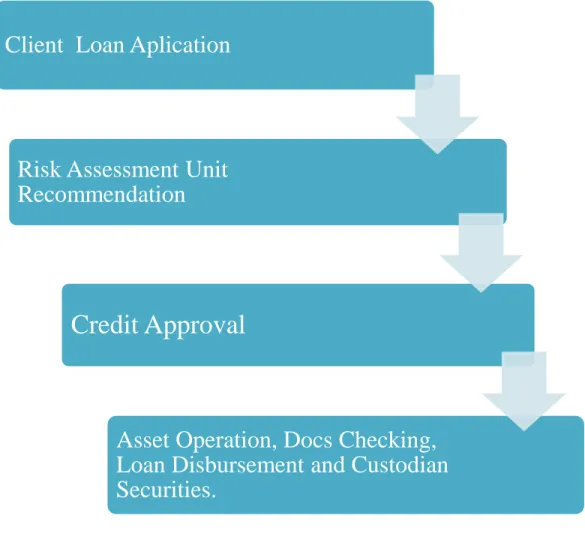

- Diagrammatically the whole loan appraisal and approval process is below

- Procedure of Loan Disbursement of Janata Bank Ltd

Loans and advances constitute the most important asset as well as the main sources of the bank's profit. On the other hand; credit is also the main source of risk for bank management. Loans and advances are used to pay current liabilities, employee wages and salaries, and business tax liability. Under the Banking Company Act 1991, every company must maintain a specified minimum (currently 16%) of its total demand and time liabilities in the form of cash and securities approved with Bangladesh Bank.

The bank's loan portfolio includes a wide range of credit programs covering around 200 items. Credit facilities are extended as per guidelines of Bangladesh Bank (Central Bank of Bangladesh) and Bank's operational procedures. Types of credit extension: One of the most essential parts of a loan is a delineation of which types of loans are acceptable and which types are not.

Loan Standard: This is a definition of the types of credit to be issued, outlining the qualitative standards for acceptable loans. The SME head approves the loan and sends the sanction letter including all documents to the AOD for disbursement and informs the relevant unit office about the sanction of the loan. The sources of information are suppliers with regard to the payment of the customer, customers with regard to the delivery of goods or services as ordered, various banks where the customer has an account showing the nature of the customer's banking transactions.

Although there are some exceptions occur by the special permission of the authority to repay with another bank account. In some cases, if the client is illiterate, the CRO completes the form on behalf of the client. Sanctioning of advances to customers and others is one of the most important services of a modern bank.

It usually grants short-term advances that are used to meet the working capital requirements of the borrower. Only a small portion of the bank's demand and time liability is advanced on a long-term basis where the banker usually insists on a regular repayment by the borrower in installments. One of the most important functions of a bank is to deploy its funds by way of loans and advances to its customers and a bank's strength depends significantly on the quality of its loans and advances.

But by providing security, the bank obtains a claim against the borrower's assets if the repayment does not occur as planned. The bank's qualitative and quantitative disclosures under Basel II requirements based on the audited financial statements are prepared according to Bangladesh Bank's guidelines on “Risk Based Capital Adequacy for Banks” to create a more transparent and disciplined financial market to bring.

Getting credit information

Information collection

Information about personal assets, name of subsidiaries, percentage of shareholding and nature of the company.

Lending Risk Analysis (LRA)

Collateral evaluation

Bank officials simultaneously evaluate the party's collateral provided by the private firm.

Final decision about the project

Proper supervision of the project

- Loan Disbursement Procedure

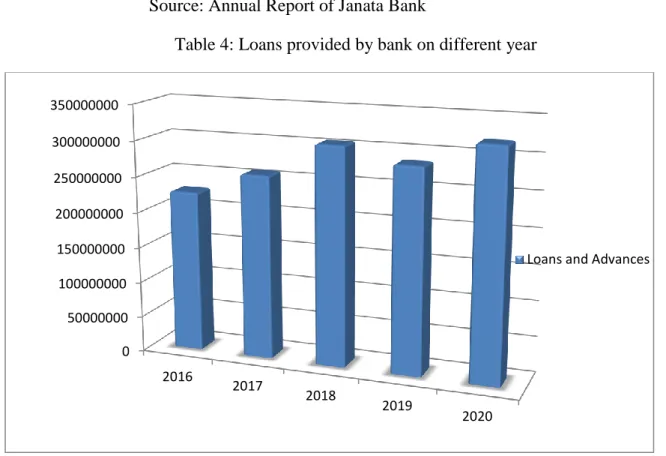

- Loans and Advances of last five years

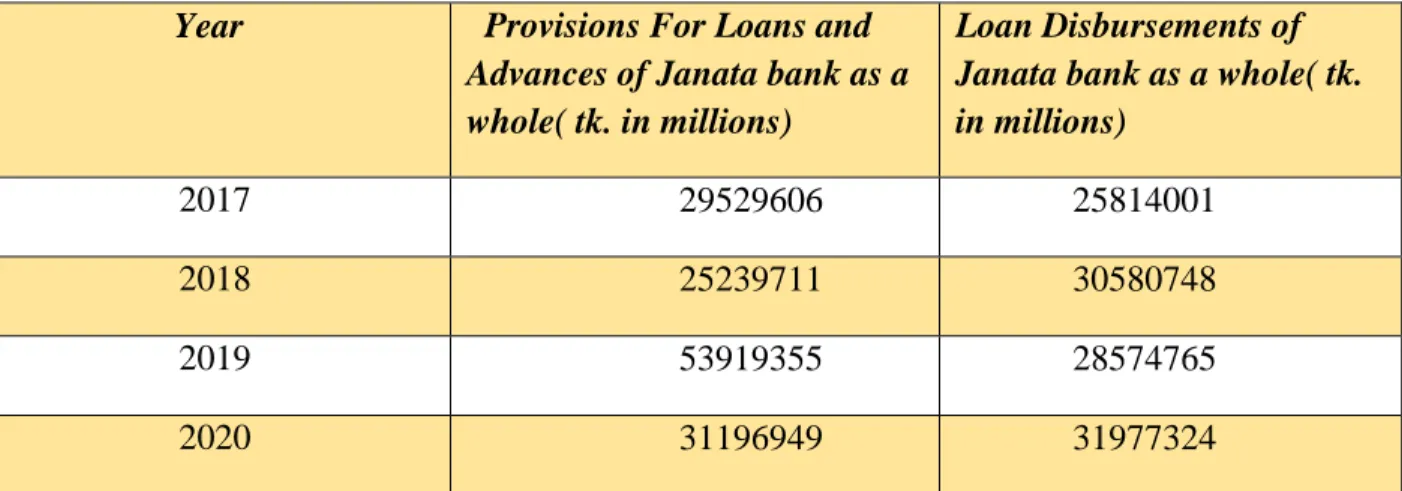

- Provision for Loans and Advances

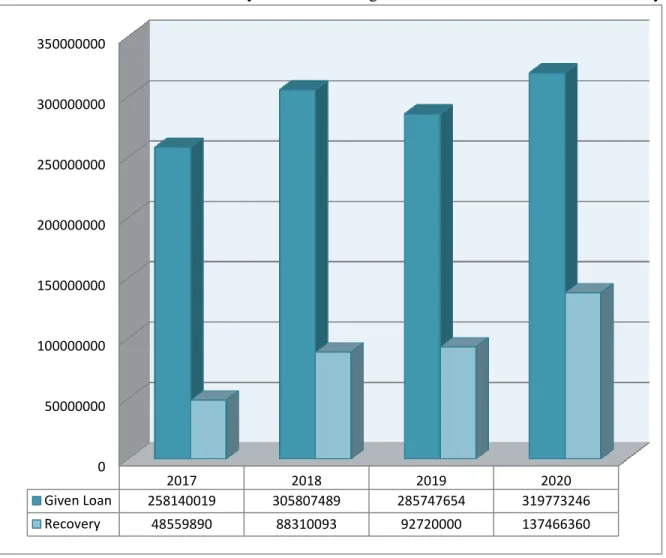

- Recovery of Loan

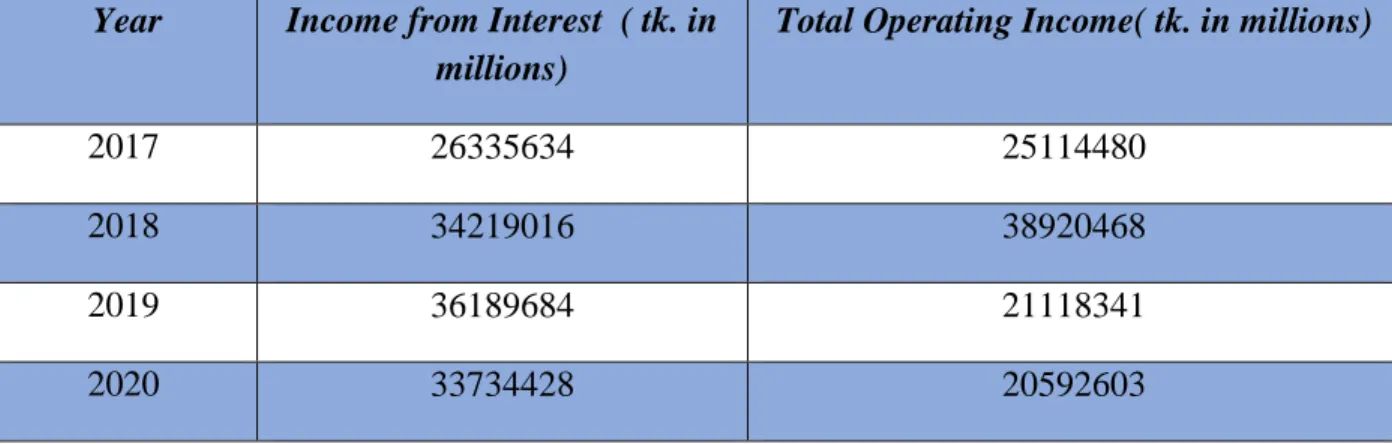

- Income from Interest

Comment: The chart above shows the comparative amount of loans issued by Janata Bank from 2010 to 2014. The provision for loans and advances increased to BDT 1947.36 million in 2014 compared to the previous year. As the percentage of classified loans increased from that in 2013, provisions also increased in 2014. The bank was also able to recover BDT 7337.30 million through December 2014, which is 97.72 percent of its recovery target.

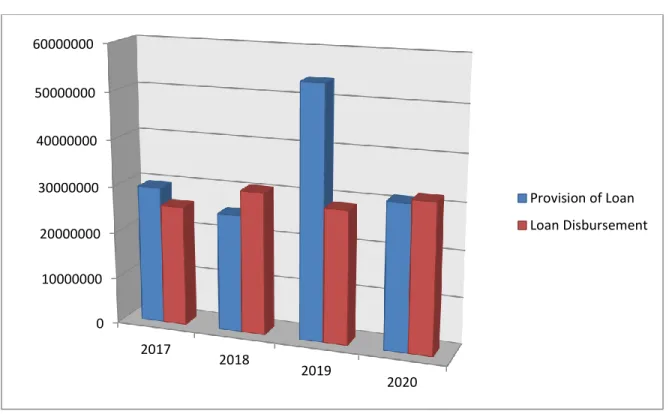

Comment: The chart above shows the comparative amount of loan and advance provisions and loan disbursements of Janata Bank from 2017 to 2020. Comment: The chart above shows the loan recovery in terms of loan origination of Janata Bank from 2017 to 2020. The operating profit did not reach the expected level due to the decrease in interest income and the increase in interest expenses compared to last year.

Source: Janata Bank Annual Report Table 7: Interest income and total operating income of the bank in different years.

Comment

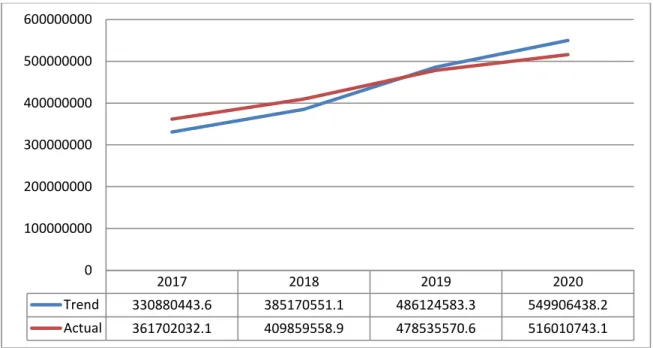

Trend analysis

As an aspect of technical analysis that tries to predict the profit of the future movement on past data. Trend analysis is based on the idea that what has happened in the past gives traders an idea of what happens in the future. Positive value of y means positive slope and negative value of y means negative slope. From the graph above, we see that the bank increases loans and advances day by day.

Performance of JBL

Comments

- Findings

- Analysis

- Recommendation

- Conclusion

- Cash flows from operating activities

Banks are financial services companies that produce and sell professional management of public assets and perform many other roles in the economy. In this chapter, I would like to focus on the classification process, provisioning for each classification, the bank's performance on the classified loan and the recovery of the classified loan. The title of the circular was "Revised rules for classification and formation of provisions for loans and advances", which began to be implemented from

Processing costs are higher compared to the other large-scale loan services provided by the bank because careful monitoring and supervision of the credit operation becomes necessary. There is a shortage of manpower and a lack of proper training for the employees in the credit department of the branch. The credit management of JBL is not fully in accordance with the guidelines prescribed in the Banking Companies Act 1991 and International Accounting Standard-30(IAS-30).

The bank should spread loans more to finance small entrepreneurs for better growth of the country. Law and order should make it easier for the bank to cash in the collateral so that the borrower can repay the debt without any problems. The bank should modernize its lending and borrowing strategy so that it is sustainable and suitable enough to survive in the market.

The bank should develop quality service related to prompt disposal as in the head office of the branch related to loan and advance operations. It goes without saying that credit policy cannot be isolated from the broader policy of monitoring the country. Like any other segment of economic policy, credit is very important for any financial institution, as it generates profits and strengthens the country's economic activities.

In other words, credit is business and it is input into the production process of the country. Since credit has an inherent risk, proper utilization of the loans is therefore essential to meet the requirements of the borrower. In this regard, the Janata Bank Limited must closely monitor the progress of the loan and the manner in which the borrower utilizes the funds.

In this way, Janata Bank Limited will deter any bogus activity on the part of the borrower. Janata Bank Limited's credit rating system is a very lengthy process. Ministry of Commerce (December 2012), Credit Policy Ministry of Commerce, Government of the People's Republic of Bangladesh.