It is my great pleasure to submit my internship report on “Credit Operation system & Retail banking of Trust Bank Limited” as a requirement of our BBA program. I am Mithila Momo, would like to declare that this internship report titled ""Credit Operation system & Retail banking of Trust Bank Limited" has been submitted to the BBA department of UIU as a partial requirement for my academic program. This report is authentically prepared by me after completing three months internship with Trust Bank Ltd, Cumilla Cantonment Branch.

First of all, I would like to express my deepest gratitude to Almighty Allah that I have done my internship in Trust Bank Ltd (Cumilla Cantonment Branch, Cumilla) from February 2022 to May 2022. Next, I would like to mention some people without the contribution their would not be possible to complete my internship report. Moreover, I would like to convey my gratitude to all my faculty members of our BBA program who helped with their valuable guidance.

I am so happy that I got the opportunity to work as an intern at Trust Bank Limited. In addition, I would also like to express my gratitude to the Human Resources Department of Trust Bank Limited for giving me the opportunity to do my internship program in this organization. Trust Bank Limited plays a vital role in the socio-economic development of our country by meeting demand and improving banking services in our country.

TBL – Trust Bank Limited AWT- Army Welfare Trust FIS- Financial Institutions MNC- Multinational Corporation CIB- Credit Information Bureau NPL- Non-Performing Loan SLA- Service Level Agreement CLP-Credit Line Proposal BCC- Branch Credit Committee.

INTRODUCTION

- Background of the Report

- Objectives of the Report

- Scope and limitations of the Report

- Definition of Key terms

- Risk Management

- Credit Risk

- Credit Risk types

- Credit Analysis

- Credit Risk Management

- Non-Performing Loan

Furthermore, This report was prepared through a substantial discussion with the employees of the bank. Limitations: Various studies and analyzes have been done from start to finish to make this report complete and precise. One of the limitations was that it was not possible for me to go to the entire area of the bank.

So, despite having some limitations, I have tried my best to make this report informative. In the credit risk management process, the amount of risks depends on the financial instrument that is taken by the borrower. As exposure to credit risk has become a major problem in the banking system around the world, so banks need to take the appropriate session through the experience they have made in the past.

Moreover, banks must have a keen awareness of this risk and must identify, monitor and control credit risk. Credit analysis is another word for a default risk analysis in which a loan officer attempts to assess a borrower's ability and willingness to repay the loan. Before granting the loan, banks must check the honesty of the borrower and their intention to repay the loan.

Collateral is therefore an asset that the bank can use to seize and sell if a borrower cannot pay his debts. The main objective of credit risk management is to improve the bank's risk-adjusted returns and manage credit risk disclosure within acceptable parameters. Credit risk management requires banks to manage the inherent credit risk and other risks associated with the individual loan or transactions.

They must also manage credit risk and other risk relationships. Therefore, effective credit risk management is an essential component for the bank's long-term success. Consistently managing credit activities such as measurement, administration and monitoring in the best possible way and ensuring control over credit risk. In banking, a loan is considered unprofitable if the borrower does not pay the principal and interest within 90 days.

COMPANY AND INDUSTRY PREVIEW

- Company Analysis

- Overview and history

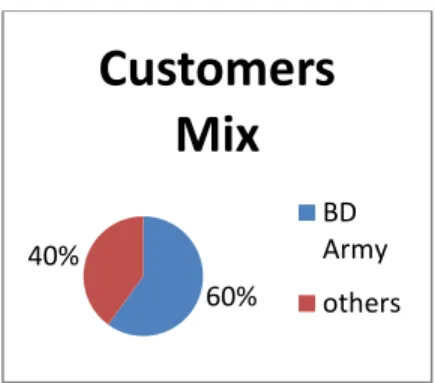

- Customer mix

- Product/service mix

- Operations

- Industry Analysis

- Specification of the industry

- External economic factors

- Technological factors

- Barriers to entry

- Supplier Power

- Buyer Power

- Threat of Substitutes

- Industry rivalry

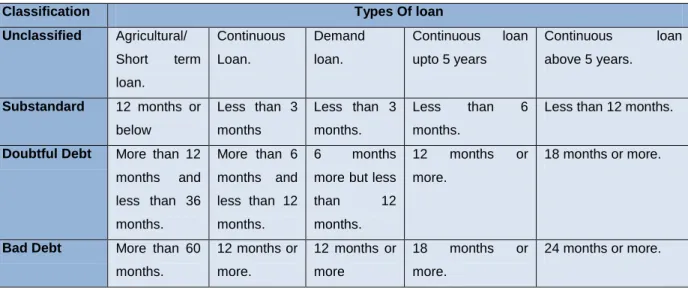

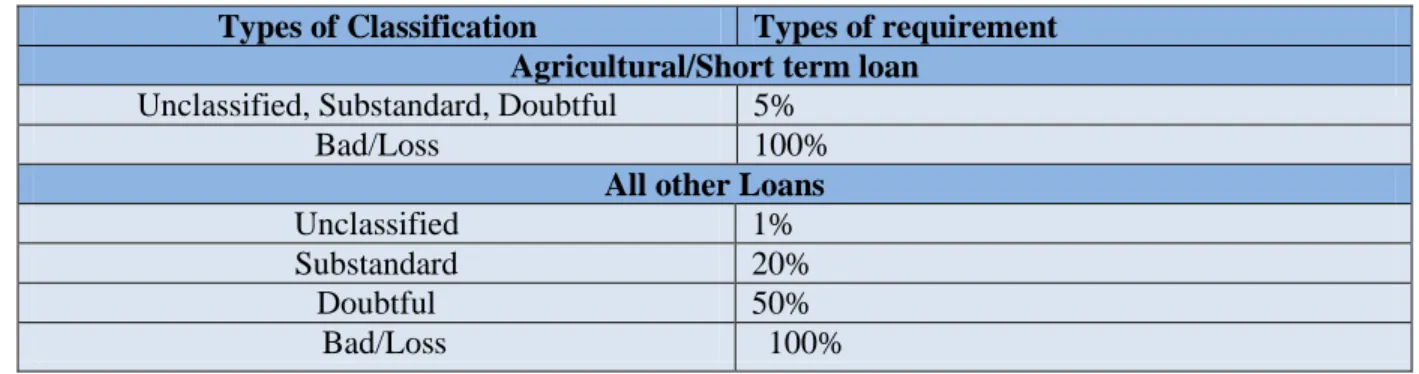

- Loan Classification

- Loan Classification Procedure

Trust bank limited serves its customers with various types of services apart from the traditional services offered by banks. Commercial banks one of the most important functions is to create and pay out loans and in this way the bank earns a profit. Usually the secured loans are given based on the applicant organization's creditworthiness and the banks' discretion, that's why the interest rate is usually high in business loans.

The secured loan is backed by collateral, so here the creditor's risk is low, because if the borrower defaults, the lender has the right to own the asset as well. Customers can now use their credit card at stores, malls or restaurants across the country and even abroad. Credit Department of TBL: One of the essential functions of a commercial bank is to extend credit to potential borrowers and the credit department manages the entire lending process of a bank.

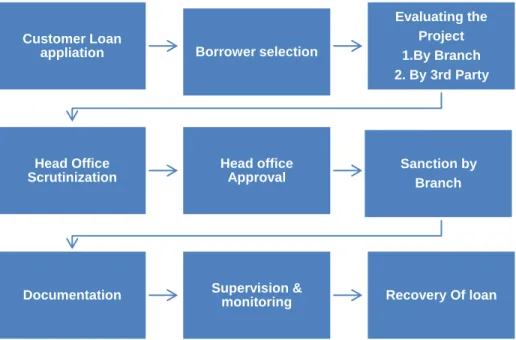

Borrower selection process at TBL: Borrower selection is an important part of TBL's loan approval process. Obtaining the CIB Report: After receiving the customer's loan application to get the customer's credit inquiry report, the bank sends a letter to the Credit Information Bureau of Bangladesh Bank called the CIB (Credit Information Bureau) report. Typically, the branch loan officer is responsible for gathering this information by consulting with them.

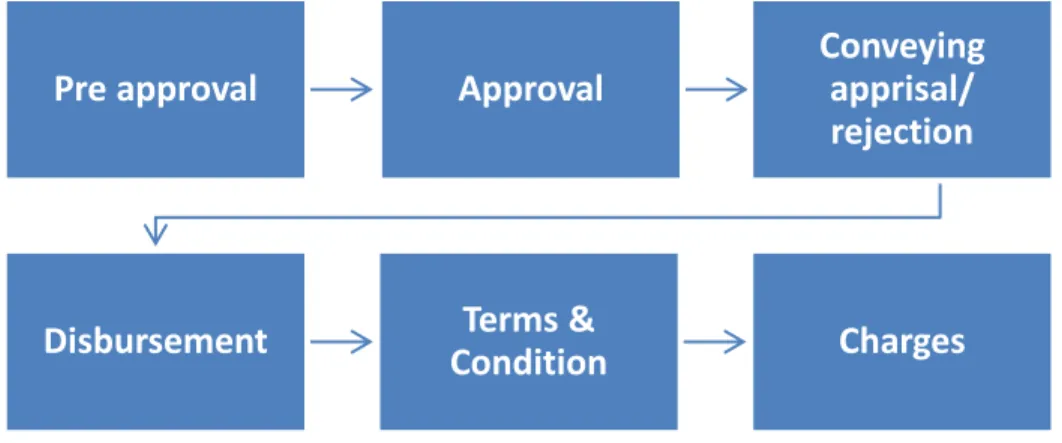

Then, to measure the financial soundness of the borrower, the bank conducts a financial statement analysis, which includes: Collection of charged documents: Finally, the branch disburses the loan through a loan account in the borrower's name, and begins the formal supervision of the loan. Credit Approval Process The process that Trust Bank Limited goes through for credit approval is mentioned below.

Strength: One of the strengths of TBL is its founded and funded by the Army Welfare Fund. One of the biggest problems is that their banking software & ATM service is not very satisfactory. Opportunity: One of the big opportunities of TBL could be their growing consumer credit holders as we have found out from one of our analysis.

Threats: Extensive competition between private commercial bank and MNC is one of the major advantages of TBL. Because competing banks also offer lucrative products and services such as more efficient banking, mobile banking and ATMs, so if TBL fails to cope with It will be a major threat to them. Trustbank is a private commercial bank/financial institution of our country which comes under the banking sector of Bangladesh.

INTERNSHIP EXPERIECNE

Position, duties, and responsibilities

New skill development

Application of academic knowledge

Loans & Advances in TBL

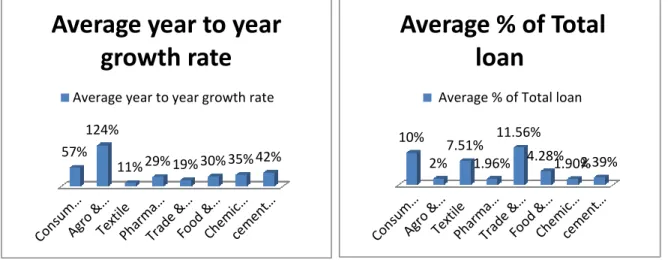

Moreover, the year-on-year growth rate is 57% which is also high, although there has been some decline in some years. Therefore, since the average growth rate and average percentage of consumer loans are high, our main focus will be the consumer loan provided by Trust Bank Limited.

Time series analysis of TBL Consumer loan

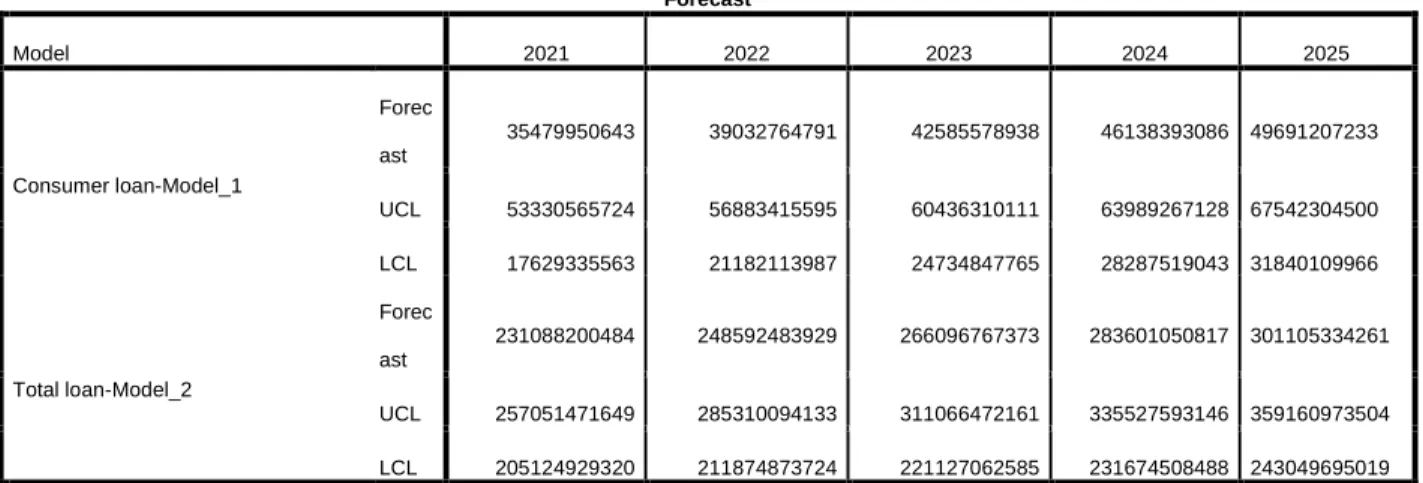

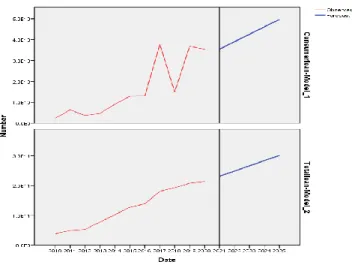

We can see here the predicted amount of the total loan and consumer loans increase over years. Here the red line indicates the historical data and blue line indicates the predicted values. As shown in the graph, the historical total amount of the loan curve is upward sloping and the consumer loan curve is also moving upwards, although there was a big up and down in the year 2017 and 2018, but in the next 2 years it adjusted with the previous trend.

Thereby, in the predicted outcome, both the curves are upward sloping indicating that the total and consumer loan amount will increase in the next 5 years, as there were upward trends in the historical data. So, from this time series forecast we can predict that in the next 5 years the total loan amount and the loan amount given to the consumer will increase for TBL.

Demographic analysis of term Loan TBL cantt branch (2015, 2016)

The monthly payment of bad loans was not clear as missing 12 payments makes a loan as a non-performing loan or a bad loan. Among the five different categories of loans, the marriage loans and army officer loans are not clear and the maximum time for missed payment is 12 months. Over the period, 67% of BL is from the Marriage Loan Scheme (MLS) for Other Ranks and 33% from the Housing Loan Scheme for Army Officers-2.

CONCLUSIONS AND KEY FACTS

Key Understanding

Recommendations for improving departmental operations

Conclusion