AN ANALYSIS OF TRANSLATION OF ACCOUNTING TERM IN FESS AND WARREN’S 14TH ACCOUNTING PRINCIPLES AND ITS TRANSLATION INTO INDONESIAN

A THESIS

BY:

RUMALA DESSY

REG. STUDENT NO: 050705046

ENGLISH DEPARTMENT FACULTY OF LETTERS

UNIVERSITY OF SUMATERA UTARA MEDAN

ACKNOWLEDGEMENT

Alhamdulillah,

My highest thank to Allah who is forever faithful to lead and help me to finish

my study, especially to complete my thesis entitle An Analysis Of An Accounting

Term In Fess And Warren’s 14th Accounting Principles And Its Translation Into

Indonesian.

I would like to express my deepest gratitude to my supervisor, Dr. Edi Setia, M. Ed

TESP who has given me attention and contribution to guide me to finish this thesis,

and my Co-supervisor, Drs. Chairul Husni, Med TESOL, for his constructive

outcomes towards this thesis.

Then, I address my high gratitude to Dra. Swesana Mardia Lubis, M. Hum the

head of English Department and Drs. Yulianus Harefa, GradDipEd TESOL., Med

Tesol., the secretary of English Department for their advice and encouragement

during my study at the faculty.

I would like to thank to all my lecturers in the English Department who have

taught me lesson so long that I can get knowledge. My gratitude for my academic

Supervisor, Dra. Nurlela, M. Hum., who has supported me during my study in the

English Department And also bang Samsul for his help in administration matters.

My deepest and highest attitude is expressed to my beloved father, Nasrul

Latief, and my mother, Mariam, for their pure love that given to me. I truly appreciate

their spirit for struggling much to support my daily life and my study. For my lovely

sisters and Brothers, Ina, Meri, Agus and Darby. You all put colors in my life and

give me worth as your sister. My ‘aa’, Riza wijaya, thanks you for supporting me,

thanks for your love. Thanks for ‘caem bersodara’ (Wiwin, Pipi, Ayu, Tia, Qiqi, Aik),

sharing sweet memories and all the moments during academic years, “may this

friendship remind forever’. All my seniors and juniors, too many enumerate one by

one here, without whose invaluable help. I could not have carried out the task it was

entrusted with.

Despite my effort to produce a faultless paper, I am well aware that the reader

will find numerous imperfections, for which I apologize.

Finally I hope this thesis will add our knowledge about literature.

Medan, Juni 2009

ABSTRAK

Skripsi ini menganalisis terjemahan istilah-istilah akuntansi yang terdapat pada buku Fess dan Warren, Edisi ke-14 Prinsip-prinsip Akuntansi dan terjemahannya dalam bahasa Indonesia. Teori yang digunakan adalah teori penerjemahan Vinay dan Darbelnet. Teori ini membagi metode penerjemahan menjadi dua bagian: (1) terjemahan harfiah (literal translation) dan (2) wajib (oblique translation) yang kemudian di pecah lagi menjadi tujuh bagian yang dikenal dengan sebutan prosedur: (a) peminjaman (borrowing), (b) calque, (c) terjemahan

harfiah, (d) transposisi, (e) modulasi, (f) kesepadanan dan (g) penyesuaian.

Dari hasil analisis, dapat dilihat adanya kompleksitas pemahaman tentang prosedur penerjemahan. Hal ini harus lebih dipahami secara benar. Bayak hal yang perlu diperhatikan dalam proses penerapan metode penerjemahan seperti hal-hal yang berkaitan dengan proses peminjaman, calque, terjemahan harfiah, modulasi, transposisi, kesepadanan dan penyesuaian. Hasil dari analisis yaitu tidak terdapatnya modulasi dan penyesuaian.

Kata Kunci: Peminjaman, Calque, Terjemahan Harfiah, Modulasi, Transposisi, Kesepadanan dan Penyesuaian.

TABLE OF CONTENTS

ACKNOWLEDGEMENTS ... i

ABSTRACT ... iii

TABLE OF CONTENTS ... iv

LIST OF TABLES ... v

ABREVIATION AND SYMBOLS USED ... vi

CHAPTER I: INTRODUCTION ... 1

1. 1 Background of the Analysis ... 1

1. 2 Problem of the Analysis ... 3

1. 3 Objectives of the Analysis ... 3

1. 4 Scope of the Analysis ... 4

1. 5 Significances of the Analysis ... 4

CHAPTER: II AN OVERVIEW OF TRANSLATION PROCEDURES ... 5

2. 1 Type of Seven Procedures ... 6

2. 1. 1 Procedure 1: Borrowing ... 6

2. 1. 2 Procedure 2: Calque ... 9

2. 1. 3 Procedure 3: Literal Translation ... 9

2. 1. 4 Procedure 4: Transposition ... 10

2. 1. 5 Procedure 5: Modulation ... 11

2. 1. 6 Procedure 6: Equivalence... 12

2. 1. 7 Procedure 7: Adaptation ... 12

CHAPTER III: METHODOLOGY ... 15

3. 1 Research Method ... 15

3. 2. Data Collecting Method ... 15

3. 3 Data Analysis Method ... 15

3. 4 Models of Presenting the Result of Analysis ... 16

CHAPTER IV: AN ANALYSIS OF PROCEDURE OF TRANSLATION ... 18

4. 1 Data Analysis ... 18

4. 1. 1 Collecting The Data ... 18

4. 1. 2 Identifying The Seven Procedures from The Data ... 21

4. 1.3. Classifying The seven Procedures from The Data ... 24

4. 1. 3. 1 Borrowing... 24

4. 1. 3. 2 Calque ... 31

4. 1. 3. 3 Literal Translation ... 33

4. 1. 3. 4 Equivalence ... 34

4. 1. 3. 5 Transposition ... 36

4. 1. 3. 6 Modulation ... 41

4. 1. 3. 7 Adaptation ... 41

4. 2 Findings ... 41

CHAPTER V: CONCLUSION AND SUGGESTION ... 43

5.1 Conclusion... 43

5.2 Suggestion ... 44

List of Tables

Table 1: Percentage of each of lexical borrowing ... 13

Table 2: Educational statistic ... 16

Table 3: An example of presenting the result of analysis ... 17

Table 4: Data collection ... 19

Table 5: Data identification ... 21

Table 6: Pure loanwords ... 25

Table 7: Mix loanwords ... 25

Table 8: Loan blend ... 28

Table 9: Calque ... 32

Table 10: Literal translation ... 33

Table 11: Equivalence... 35

Table 12: Transposition ... 36

Abbreviations and Symbols Used

adj adjective [C] countable noun

n noun

ABSTRAK

Skripsi ini menganalisis terjemahan istilah-istilah akuntansi yang terdapat pada buku Fess dan Warren, Edisi ke-14 Prinsip-prinsip Akuntansi dan terjemahannya dalam bahasa Indonesia. Teori yang digunakan adalah teori penerjemahan Vinay dan Darbelnet. Teori ini membagi metode penerjemahan menjadi dua bagian: (1) terjemahan harfiah (literal translation) dan (2) wajib (oblique translation) yang kemudian di pecah lagi menjadi tujuh bagian yang dikenal dengan sebutan prosedur: (a) peminjaman (borrowing), (b) calque, (c) terjemahan

harfiah, (d) transposisi, (e) modulasi, (f) kesepadanan dan (g) penyesuaian.

Dari hasil analisis, dapat dilihat adanya kompleksitas pemahaman tentang prosedur penerjemahan. Hal ini harus lebih dipahami secara benar. Bayak hal yang perlu diperhatikan dalam proses penerapan metode penerjemahan seperti hal-hal yang berkaitan dengan proses peminjaman, calque, terjemahan harfiah, modulasi, transposisi, kesepadanan dan penyesuaian. Hasil dari analisis yaitu tidak terdapatnya modulasi dan penyesuaian.

Kata Kunci: Peminjaman, Calque, Terjemahan Harfiah, Modulasi, Transposisi, Kesepadanan dan Penyesuaian.

CHAPTER I

INTRODUCTION

1.1Background of the Analysis

All physical aspects in this world and all aspects of human life are subjects to

change and language are no exception. Language as a media to communicate changes

continuously. One of the reasons language changes is that they come into contact with

other languages.

Schendl (2001:67) says “One obvious answer to the question why language

change in general is that everything changes in human affair.” It means that language

always changes follow the changes of human affair necessities. Whenever human

need, the language will serve it.

This universe is filled by many people with different cultures, activities and

also languages. When they come into contact with others they may overcome a new

variety of language. In doing translation, this case often occur. The difference of

culture is one of the big caused of it. For example, some new words in English caused

by cultural phenomena, thug (from Hindi), sherry (from Spanish), waltz (from

German), ski (from Norwegian), sauna (from Finnish) and more recently, glasnost

(from Russian), and sushi (from Japanese).

These kinds of new words often called borrowing word or loan word. Besides,

there are a lot of new words overcome into one language in many different ways and

factors. As a social community, Indonesian language also grows and changes caused

by contact with other language such as English, Sanskrit, Arabic, and other languages.

This new word can be classified into some procedure, not only borrowing but also as

a calque, modulation, adaptation etc.

According to Vinay and Darbelnet in Wilss (1977:96) there are seven

procedures of translation which classify the new variety of language. This procedure

in order to control the translator work, in the listing which follows, the first three

procedures are direct and the others are oblique.

a. Procedure 1:Borrowing

b. Procedure 2: Calque

c. Procedure 3: Literal translation

d. Procedure 4: Transposition

e. Procedure 5: Modulation

f. Procedure 6: Equivalence

g. Procedure 7: Adaptation

The writer wants to analyze the data (accounting term) which are taken from

an accounting book to see whether the procedure above exist or not.

Bolinger (1975:419) says, “Borrowings are concentrates in the areas where

contact is most intense. Therefore, it is not surprising that science and technology lead

the field nowadays, with sport and tourism close behind. But the contact has grown so

close in recent time with press, radio, television, and international travel, that a kind

of universal diffusion is taking place.”

Accounting as one of the science where contact is most intense and grown so

close in recent time with many media of communication become a very interesting

object to analyze related to the borrowing. That is the reason of the writer in choosing

the object of the analysis which later not only discus about borrowing but also about

There are statements from some linguists which talk about some of those

procedures. Cadford (1965:20) defines “translation as the process of changing a

written text form one language (SL) to the equivalence which is written in another

language”. In this statement, he emphasizes the equivalence in doing translation.

Besides, Herbet Schendl (2001-56) says “however, speaker may feel the need for

borrowing not because their language does not have a word for a particular object or

concept, but because they think that the equivalent word in the donor language is

better or more prestigious.” He insists that borrowing sometimes occurs in doing

translation with some factor of the need.

1.2Problems of the Analysis

Based on the background above there are some problems of the analysis which

are discussed.

a. How to identify the seven procedures of translation in the target text?

b. How to classify the seven procedures of translation in the target text?

c. Does each of the procedure found in the target text?

d. What is the most dominant procedure found in the target text?

1.3Objective of the Analysis

The objectives of the analysis are to answer the problems above that can be

described as follow:

a. To identify the seven procedures in the target text by using Vinay and

Dalbernet’ theory.

b. To classify the seven procedures in the target text by using Vinay and

c. To find out whether the seven procedures are found in the target text.

d. To find out the dominant type of the procedure found in the target text.

1.4Scope of the Analysis

In this thesis, the writer focused on analyzing the data from Fess and Warren’s

14th Accounting Principles and its translation into Indonesian by seven procedures

The data are accounting terms only which collected from chapter one to chapter

fourteen. The analysis covers the seven procedures in other to get the results of the

analysis related to the procedures.

1.5Significances of the Analysis

There are theoretical and practical significances that can be taken from this

thesis. Theoretically, this thesis can be used for the readers and especially for the

students of English department to expand their knowledge about translation.

Practically, this thesis can be used by translator in practicing the translation and also

CHAPTER II

AN OVERVIEW OF TRANSLATION PROCEDURES

Vinay and Darbelnet (1958) have been able to condense translation procedures

to just seven different ones. They have differentiated two basic translation methods:

direct (literal translation) and the indirect (oblique translation),. The first three

procedures fall into the category of direct (literal translation) and the last four fall into

category of indirect (oblique translation).

According to Vinay and Darbelnet (1958:61-64), literal translation means that

the source language message can be translated perfectly into target language, because

the message is based on parallel categories or concepts. Oblique translation comes

into use when there are gaps in target language which have to be fiiled by some

equivalent meant, so that the meaning or impression is the same for the source

language and target language. Oblique translation must be used also, when the

language have some structural or metalinguistic differences so that certain stylistic

effect can not be transferred without radical semantic or lexical change. More

precisely, the translator must turn to oblique translation if the literally translated

message either has another meaning than the source language one, correspond to

something in the metalinguistics of the target language but not at the same linguistic

level. As an example, Vinay and Darbelnet (1958:64) take the following utterances:

He looked at the map and He looked the picture of health, of which two examples the

first can be translated literally to French Il regarda la carte, but the second must be

translated more idiomatically, for example like Il se portrait comme une charme.

Vinay and Darbelnet’s theory of translation procedures is so compact and

introduce the seven translation procedures paraphrase Vinay and Darbelnet writing

closely.

2.1

Type of Seven Procedures:

2. 1. 1 Procedure 1: Borrowing

This procedure is the simplest translation procedure. It is used usually when

there is a metalinguistic gap in the target language, for example when a new technique

or an unknown concept is introduced. It can also be used to create a particular stylistic

effect, for example to introduce an element of local, source language color to the

target language: tortilla, tequila, and sauna. Many old loanwords have later become a

fixed part of the lexis of the borrowing language, for example word from English to

French: alcool from alcohol, and redingote from riding-coat. There are some

possibilities that may occur in this procedure; first, borrowing with no change in form

and meaning ( pure loanwords), the second, borrowing with changes in form but

without changes the meaning (mix loanwords) and the third, borrowing when part of

the term is native and other part is borrowed, but the meaning is fully borrowed (loan

blends)

Examples:

a. Borrowing with no change in form and meaning (pure loanwords)

voucher → voucher

bonanza → bonanza

bank → bank

b. Borrowing with change in form but without change the meaning (mix

loanwords)

accrual → akrual

credit → kredit

debit → debet

c. Loan blend

nominal account → perkiraan nominal

bussines transaction → transaksi usaha

temporary investment → investasi sementara

There are other general statements about the understanding of borrowing

giving by some linguists. Hockett (1958:402) defines borrowing as follow, “the

feature which is imitated is called the model; the language which is the model occurs,

or the speaker of that language, called donor, the language which acquires something

new in the process is borrowing language. The process itself called borrowing. From

the statement bellow, it can be understood that loan word or borrowing word should

not be return, which means that the donor makes no sacrifice and does not have to ask

for permission. So, there is nothing change because the donor goes on speaking as

before and only the borrower’s speech is altered. Lehman (1962:213) states, “The

process by which word are imported into a language is known as borrowing.” Then,

he also concludes that the influence of one language on another, the result of which

have been termed borrowing. Thus, based on those statements, the understanding of

borrowing can be simplified as a process whereby one language adopts a meaningful

unit from another language, or a process in which one language adopts elements of

another.

Hockett (1958:408-416) says that borrowing can be classified into three; they

According to Bolinger (1975:421) that both form and meaning in loanwords is

borrowed, with whatever degree of adaptation to the phonology of the borrowing

languages.

The borrower may adopt the donor’s word along with the object of practice:

the new form in the borrower’s speech is then called loanword. The term loanword is

used to denote words taken from foreign language and used it as though it were native

to the language into which it has been borrowed. Therefore, the acquisition of a

loanword constitutes in itself a lexical change and probably should say it constitutes

or entails a semantic change. Loanwords are almost always free form (words or

phrases); bound forms are borrowed as such only with extreme rarity. Then they also

show some phonemic substitutions, which occur mainly depends on how those direct

word borrowing from source language, assimilate into receptor’s language. Moreover,

loanwords are direct borrowing from English whose overall morphemic shape is

recognizable English, and which do not show any fusion with receptor’s language.

If a speaker imitates someone else’s pronunciation of a word, which is already

familiar to the borrower, we may speak of pronunciation borrowing. Usually the

donor and borrowing idiolects are mutually intelligible, and the motive is prestige. A

style of pronunciation can also be imitated, usually for prestige reason, without

specific reference to a particular word. Besides, pronunciation borrowing can operated

across language boundaries.

Grammatical change can be brought about indirectly by borrowing-via sets of

related loanwords. Grammatical change is the change in the grammatical core, which

includes forms, which collectively called ‘functors’ and some functors are separate

retaining its functional status, the immediate consequence to be a grammatical change

in the borrowing language might be naturally expected.

2. 1. 2 Procedure 2: Calque

Calque is another form of loan translation: a complete syntagma (syntactic

unit) is borrowed, but its individual elements are translated literally. The result can be

a calque of expression, which preserves the syntsctic structure of the source language

while introducing a new mode of expression to the target language. It consists of

phrases in direct (literal) translations of fixed expression in target language, for

example French Compliment de la saison, which come from English Christmas

greeting compliments of the season. The result can also be a structural calque, which

introduces a whole new construction into the target language, for example

science-fiction, used as such in French. Calque is loan translation (linear substitution) of

morphologically analyzable source language syntagms which after a time, are often

accepted, or at least tolerated by the target language community.

2. 1. 3 Procedure 3: Literal Translation

This procedure is a word for word translation, replacement of source language

syntactic structures, normally on the clause or sentence scale, by syntactic which are

isomorphic (or near isomorphic) concerning number and type of speech parts and

synonymous in term of content, where the resulting target language is grammatically

correct and idiomatic. The translation has not needed to make any changes other than

the obvious one, like those concerning grammatical concord or inflectional endings,

procedure is most commonly found in translations between closely related language,

for example French-Italian, and especially those having a similar culture. There are

other examples of literal translation.

Examples:

deferral → penangguhan

revenue expenditure → pengeluaran pendapatan

capital element → unsur modal

capital increase → modal bertambah

close the book → menutup buku

2. 1. 4 Procedure 4: Transposition

Transposition means the replacing of one word-class by another without

changing the meaning of the message. It can also be used within a language, as when

rewarding the phrase, for example ‘He announced that he would return’ to ‘He

announced his return’ (the subordinate verb becomes a noun). In translation, there are

two types of transposition: obligatory and optimal.

It is also a change in the grammar from source language to target language (singular

to plural; position of the adjective, changing the word class or part of speech). There

are more examples of transposition

Examples:

sales journal → buku harian Penjualan

equity → hak pemilikan hak

proceeds → hasil diskonto

2. 1. 5 Procedure 5: Modulation

Modulation means a variation in the message due to a change in the point of

view: seeing something in different light. Using modulation is justified when a literal

or transposed translation results in a form which is not quite natural and going against

the felling of the target language. There are two types of modulation: fixed and free.

Fixed or obligatory modulation must be used when for example translating a phrase

‘the time when’ to French as ‘le moment ou’. In this example, the time become

moment, and when becomes where. In this case of fixed modulation, a competent

bilingual will not hesitate to have recourse to this procedure if it supported by

frequency or total acceptance of usage, or a status establish by the dictionary or

grammar.

Free or optimal modulation takes place for example, when a negative

expression in the source language positive in the target language because of

language-specific stylistic features: ‘it is not difficult to show’ becomes ‘il est facile de

demontrer’ (‘it is easy to show’). With the free modulation the process must be

undergone anew in this case, and no fixation has taken place.

However, free modulation is not really optimal in the strict sense, for when it

is correctly done, it must result in the ideal target language solution corresponding to

the source language situation: a correct usage of free modulation makes a native

reader of a target language say: “Yes, that just how it would be said.” A free

modulation may at any moment become fixed as soon as it becomes frequent, or is

2. 1. 6 Procedure 6: Equivalence

Two texts in different language will account for the same situation by means

of very different stylistic and structural devices. The change which happened in the

message with this procedure is usually syntagmatic, and it affects the whole message.

Most examples of this procedure belong to the phraseological repertoire of idiom,

clichés, proverbs, nominal or adjectival collocation, etc. For example the proverbs

‘too many cooks spoil the broth’ becomes ‘deux patrons font chavirer la barque’ (two

skippers will capsize the boat”) in French. It must be remembered, that idioms, for

example as like as two peas must not be translated as calques or any account, for the

responsibility of introducing calques (of idiom) into a language that is already

perfectly organized should be the author’s choice, not the translators. There are other

examples of equivalence in accounting term:

Examples:

account payable → hutang dagang

account receivable → piutang dagang

marketable security → surat berharga

2. 1. 7 Procedure 7: Adaptation

This procedure is used in cases where the situation to which the message

refers does not exist at all in the target language and must thus be created by reference

to a new situation, which is judged to be equivalent. For example, it is culturally

normal for an English father to kiss his daughter on the mouth, but a similar action

would be culturally unacceptable in a French text, and must be translated as

something like ‘il serra tendrement sa fille dans ses bras’ (‘he tenderly embraced his

A refusal to make use of adaptations which are not only structural but also

pertain to the presentation of idea or their arrangement in the paragraph, leads to a text

that is perfectly correct but nevertheless invariably betray its status as translation by

something indefinable in its tone, something that does not quite ring true.

2. 2 Relevant Studies

To support the ideas of this thesis, the writer provides some relevant studies.

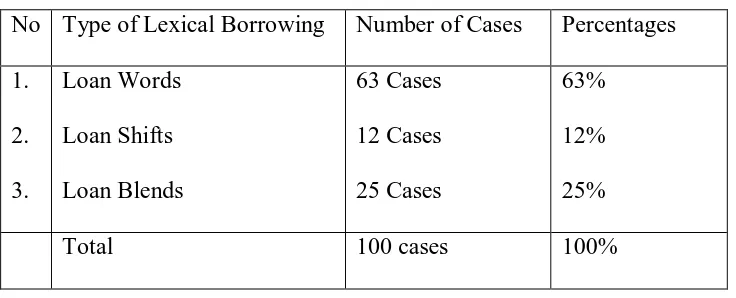

Tatari Prasasty (2002) in her thesis “An Analysis of English Lexical Borrowing Found

in PT. Nestle Indonesia’s Catalogue” gives a contribution to this thesis. She uses the

descriptive method in writing the thesis. She also uses common statistic formula

based on ‘Educational Statistic’ to count the percentage of each type of lexical

borrowing. Then she draws the percentages of each of lexical borrowing on a table.

The following table is the result of the thesis.

Table 1: Percentage of each of lexical borrowing

Roswani Siregar (2009) in her thesis “Analisis Penerjemahan Dan

Pemaknaan Istilah Teknik: Studi Kasus Pada Terjemahan Dokumen Kontrak” has

given a lot of contribution to this thesis. Her thesis is very closely relevant to this

thesis. She talks about methodology for translation which some theory that she uses is

relevant to this thesis, such as Vinay and Dalbernet theory’s about translation No Type of Lexical Borrowing Number of Cases Percentages

procedures. Some of the methodology that she used in her thesis is also used by the

writer in writing this thesis.

The writer takes some relevant information from the written text too. Some of

the relevant information mentioned as follow:

Larson (1984:3) state that translation consist of transferring the meaning of

source text (ST) to target text (TT), and it is done by going from the form of source

text to the form of target text by way of semantic structure. It is the meaning being

transferred and it cannot be added or changed; only the surface structure or form can

be changed.

Larson’s statement is close to non literal (oblique) translation in Vinay and

darbelnet’s translation procedures. Larson says it as meaning based translation.

Catford in Venuti (2000:141) states that shift mean the departures from formal

correspondence in the process of going from source language to target language.

Catford statement is related to transposition in Vinay and Darbelnet’s seven

procedures.

Nababan (32: 1999) ‘penerjemahan harfiah (literal translation) terletak

antara penerjemahan kata demi kata dan penerjemahan bebas. Penerjemahan

harfiah mungkin mula-mula dilakukan seperti penerjemahan kata demi kata, tetapi

penerjemah kemudian menyesuaikan susunan kata dalam kalimat terjemahannya

yang sesuai dengan susunan kata dalam kalimat bahasa sasaran.’

From the statement above we can conclude that literal translation is that where

the text in source language is translated word for word into target language within

CHAPTER III

METHODOLOGY

Method of the analysis is an important thing in doing a scientific study. The

method used must be relevant to the analysis because the analysis will not be

successful if we use the wrong method.

3. 1

Research MethodIn this thesis, the writer uses library research in analyzing the data. Nawawi

(1991:30) says that library research is done by collecting the data from every

literature, even in the library or in the other places. The writer uses an accounting

book as the data of analysis.

3. 2

Data Collecting MethodThe data in this thesis are collect from the accounting book Accounting

Principles 14th Edition by Fess and Warren and also from the translation of the book

into Indonesian Edisi ke-14 Prinsip-Prinsip Akutansi translated by Marianus Sinaga.

To make the analysis easier, the data is collect in random way. Some chapters are

chooses as a samples for the analysis.

3. 3 Data Analysis Method

In analyzing the data, descriptive method is used. Nawawi (1991:63) says that

descriptive method can be define as problem solving procedure which is researched

by describing the subject or object of the research based on the real fact nowadays.

a. Collecting the data from the original book and its translation into

Indonesian.

b. Identifying the seven procedures from the data.

c. Classifying the seven procedures from the data.

d. Drawing some conclusions after finishing the analysis.

The writer uses the common statistic formula based on ‘Educational Statistic’

(1967) to draw the percentage of each procedure and then put it on the table.

Table 2: Educational Statistic.

N= X x 100% Y

N= the percentage of types of procedure.

X = the number of types of procedure.

Y= the total number of all types of procedure.

3. 4

Models of Presenting the Result of AnalysisFirst of all, list of the data, i. e. accounting terms are identified into seven

procedures. Afterward, the data that have been identified, are classified into seven

procedures, presented by using table form and followed by the explanation for each

classification. The letters, words or phrases which are analyzed, are underlined. The

following table is an illustration of presenting the result of analysis which then

followed by the explanation:

Table 3: An example of presenting the result of analysis.

No No of

The Data Source Text Target Text

1. 53. inflation inflasi

And the explanation is:

inflation → inflasi

‘Inflasi’ in target text is borrowed from source language ‘inflation’ with the change in

target language writing system. The suffix ‘-tion’ in source language is changes to ‘si’

in target language. This is a kind of mix loanwords.

The example above illustrated borrowing namely mix loanwords that imported

source language lexeme with some orthographical change in target language. This is

CHAPTER IV

AN ANALYSIS OF PROCEDURE OF TRANSLATION

4.1 Data Analysis

As this thesis is using descriptive method which the method defined as

problems solving procedure which is researched by describing the subject or object of

the research based on the real fact nowadays. So the writer does some procedures to

carry out this analysis:

a. Collecting the data from the original book and its translation into

Indonesian.

b. Identifying the seven procedures from the data.

c. Classifying the seven procedures from the data.

4. 1. 1 Collecting the data

It has been said in the previous chapter that the data in this thesis are collected

from the accounting book Accounting Principles 14th Edition by Fess and Warren and

also from the translation of the book into Indonesian Edisi ke-14 Prinsip-Prinsip

Akutansi translated by Marianus Sinaga. Some chapters are chosen as samples for the

analysis.

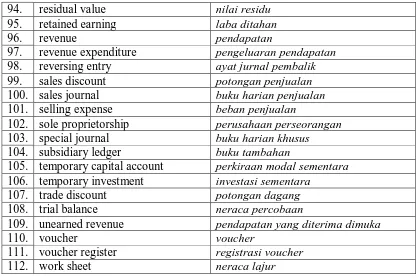

The writer has found 112 accounting terms from the data which collected from

the accounting book Accounting Principles 14th Edition by Fess and Warren and the

translation of the book into Indonesian Edisi ke-14 Prinsip-Prinsip Akutansi translated

by Marianus Sinaga. The samples are sellected from chapter one to chapter fourteen.

Tables 4: Data collection.

No. Source Text Target Text

1. account perkiraan

2. accounting akuntansi

3. accounting cycle siklus akuntansi

4. account payable hutang dagang

5. account receivable piutang dagang

6. account payable ledger buku besar hutang dagang

7. accrual akrual

8. accumulated depreciation account perkiraan akumulasi penyusutan 9. adjusting entry ayat jurnal penyesuaian

10. allowance method metode penyisihan

11. amortization amortisasi

12. asset aktiva

13. average cost method metode harga pokok rata-rata

14. balance of an account saldo perkiraan

15. balance sheet neraca

16. bank reconciliation rekonsiliasi bank

17. bookkeeping pembukuan

18. book value of an asset nilai buku aktiva

19. business entity concept konsep kesatuan usaha

20. business transaction transaksi usaha

21. capital modal

22. capital expenditure pengeluaran modal

23. capital statement laporan modal

24. cash discount potongan tunai

25. cash payment journal buku harian pengeluaran kas

26. chart of account bagan perkiraan

27. conservatism konservatisme

28. consistency konsistensi

29. contingent liability kewajiban bersyarat

30. contra asset account perkiraan lawan aktiva

31. corporation perseroan

32. cost principle prinsip harga perolehan

33. credit kredit

34. credit memorandum nota kredit

35. current asset aktiva lancar

36. current liability kewajiban lancar

37. debit debet

38. debit memorandum nota debet

39. deferral penangguhan

40. deflation deflasi

41. depletion deplesi

42. depreciation penyusutan

43. dishonored note receivable wesel tagih yang ditolak bank

44. dividend dividen

46. equity hak pemilikaan hak

47. expense beban

48. fiscal year tahun fiskal

49. general expense beban umum

50. general ledger buku besar

51. income from operation laba operasi

52. income statement perhitungan rugi-laba

53. inflation inflasi

54. intangible asset aktiva takberwujud

55. interim statement laporan interim

56. internal accounting control pengendalian akuntansi internal

57. internal administrative control pengendalian administrative internal

58. internal control pengendalian internal

59. invoice faktur

60. ledger buku besar

61. liability kewajiban

62. long term liability kewajiban jangka panjang

63. marketable security surat berharga

64. materiality materialitas

65. maturity value nilai jatuh tempo

66. merchandise inventory persediaan barang dagangan

67. monetary items pos-pos moneter

68. moving average rata-rata bergerak

69. natural business year tahun usaha alami

70. net income laba bersih

71. net loss kerugian bersih

72. net worth kekayaan bersih

73. nominal account perkiraan nominal

74. nonmonetary items pos-pos nonmoneter

75. normal pension cost biaya pension normal

76. note payable wesel bayar

77. note receivable wesel tagih

78. other expense beban lain-lain

79. other income pendapatan lain-lain

80. partnership firma

81. past service cost biaya masa kerja pada masa lalu

82. payroll upah

83. plant asset aktiva tetap

84. post closing trial balance neraca percobaan setelah tutup buku

85. posting membukukan

86. prepaid expense beban dibayar dimuka

87. private accounting akuntansi internal

88. proceeds hasil diskonto

89. promissory note surat promis

90. public accounting akuntansi public

91. purchase discount potongan pembelian

92. purchase journal buku harian pembelian

94. residual value nilai residu

95. retained earning laba ditahan

96. revenue pendapatan

97. revenue expenditure pengeluaran pendapatan

98. reversing entry ayat jurnal pembalik

99. sales discount potongan penjualan

100. sales journal buku harian penjualan

101. selling expense beban penjualan

102. sole proprietorship perusahaan perseorangan

103. special journal buku harian khusus

104. subsidiary ledger buku tambahan

105. temporary capital account perkiraan modal sementara

106. temporary investment investasi sementara

107. trade discount potongan dagang

108. trial balance neraca percobaan

109. unearned revenue pendapatan yang diterima dimuka

110. voucher voucher

111. voucher register registrasi voucher

112. work sheet neraca lajur

4. 1. 2 Identifying the seven procedures from the data

After collecting the data, the next step that the writer does is to identify the

seven procedures from the data. The following table shows the result of data

identification.

Table 5: Data identification.

No. Source Text Target Text Types of

Procedures

1. account perkiraan literal translation

2. accounting akuntansi borrowing

3. accounting cycle siklus akuntansi borrowing

4. account payable hutang dagang equivalence

5. account receivable piutang dagang equivalence 6. account payable ledger buku besar hutang dagang equivalence

7. accrual akrual borrowing

8. accumulated depreciation perkiraan akumulasi

penyusutan

borrowing

9. adjusting entry ayat jurnal penyesuaian equivalence 10. allowance method metode penyisihan borrowing

11. amortization amortisasi borrowing

13. average cost method metode harga pokok rata-rata

transposition

14. balance of an account saldo perkiraan transposition

15. balance sheet neraca transposition

16. bank reconciliation rekonsiliasi bank calque

17. bookkeeping pembukuan literal translation

18. book value of an asset nilai buku aktiva transposition 19. business entity concept konsep kesatuan usaha borrowing 20. business transaction transaksi usaha borrowing

21. capital modal literal translation

22. capital expenditure pengeluaran modal literal translation 23. capital statement laporan modal literal translation 24. cash discount potongan tunai literal translation 25. cash payment journal buku harian pengeluaran

kas

transposition

26. chart of account bagan perkiraan transposition

27. conservatism konservatisme borrowing

28. consistency konsistensi borrowing

29. contingent liability kewajiban bersyarat literal translation 30. contra asset account perkiraan lawan aktiva literal translation

31. corporation perseroan literal translation

32. cost principle prinsip harga perolehan transposition

33. credit kredit borrowing

34. credit memorandum nota kredit borrowing

35. current asset aktiva lancar literal translation 36. current liability kewajiban lancar literal translation

37. debit debet borrowing

38. debit memorandum nota debet borrowing

39. deferral penangguhan literal translation

40. deflation deflasi borrowing

41. depletion deplesi borrowing

42. depreciation penyusutan literal translation

43. dishonored note receivable

wesel tagih yang ditolak bank

transposition

44. dividend dividen borrowing

45. double entry accounting akuntansi buku berpasangan

equivalence

46. equity hak pemilikaan hak transposition

47. expense beban literal translation

48. fiscal year tahun fiskal borrowing

49. general expense beban umum literal translation

50. general ledger buku besar transposition

51. income from operation laba operasi transposition 52. income statement perhitungan rugi-laba equivalence

53. inflation inflasi borrowing

control internal

58. internal control pengendalian internal borrowing

59. invoice faktur literal translation

60. ledger buku besar transposition

61. liability kewajiban literal translation

62. long term liability kewajiban jangka panjang literal translation 63. marketable security surat berharga equivalence

64. materiality materialitas borrowing

65. maturity value nilai jatuh tempo transposition 66. merchandise inventory persediaan barang

dagangan

transposition

67. monetary items pos-pos moneter borrowing 68. moving average rata-rata bergerak literal translation 69. natural business year tahun usaha alami literal translation

70. net income laba bersih literal translation

71. net loss kerugian bersih literal translation 72. net worth kekayaan bersih literal translation 73. nominal account perkiraan nominal borrowing 74. nonmonetary items pos-pos nonmoneter borrowing 75. normal pension cost biaya pension normal borrowing 76. note payable wesel bayar literal translation 77. note receivable wesel tagih literal translation 78. other expense beban lain-lain literal translation 79. other income pendapatan lain-lain literal translation

80. partnership firma literal translation

81. past service cost biaya masa kerja pada masa lalu

transposition

82. payroll upah literal translation

83. plant asset aktiva tetap equivalence

84. post closing trial balance neraca percobaan setelah tutup buku

transposition

85. Posting membukukan equivalence

86. prepaid expense beban dibayar dimuka transposition 87. private accounting akuntansi internal borrowing

88. Proceeds hasil diskonto transposition

89. promissory note surat promis borrowing

90. public accounting akuntansi public calque

91. purchase discount potongan pembelian literal translation 92. purchase journal buku harian pembelian transposition 93. report form of balance

sheet

neraca bentuk laporan transposition

94. residual value nilai residu borrowing

95. retained earning laba ditahan literal translation

96. revenue pendapatan literal translation

99. sales discount potongan penjualan transposition 100. sales journal buku harian penjualan transposition 101. selling expense beban penjualan literal translation 102. sole proprietorship perusahaan perseorangan literal translation 103. special journal buku harian khusus transposition 104. subsidiary ledger buku tambahan equivalence 105. temporary capital account perkiraan modal sementara literal translation 106. temporary investment investasi sementara borrowing 107. trade discount potongan dagang literal translation 108. trial balance neraca percobaan literal translation 109. unearned revenue pendapatan yang diterima

dimuka

transposition

110. voucher voucher borrowing

111. voucher register registrasi voucher calque

112. work sheet neraca lajur equivalence

4. 1. 3 Classifying the seven procedures from the data

After identifying the data, the writer comes to the next procedure,i. e.

classifying the seven procedures from the data. In this section the writer brings up the

explanation for each classification. Table 6, 7, and 8 represents borrowing:

4. 1. 3. 1 Borrowing

Borrowing is the procedure which carryover source language lexeme or

lexemes combinations into target language in order to fill the gaps between the

languages. It is translated literally into target language. There are some possibilities

that may occur in this procedure; first, borrowing with no change in form and

meaning ( pure loanwords), the second, borrowing with changes in form but without

changes the meaning (mix loanwords) and the third, borrowing when part of the term

is native and other part is borrowed, but the meaning is fully borrowed (loan blends).

A loan blend is the result of process that combines morphemic importation and

substitution in the same items. Furthermore, a structural loan occurs when

its components are transferred and then target language items substitute the other

form.

The following table is borrowing which is found from the data and followed

by the analysis.

Table 6 shows pure loanwords.

Table 6: Pure loanwords

No. Data

no. Source Text Target Text

1. 110. voucher voucher

1.) voucher → voucher

‘Voucher’ is purely borrowed from source language ‘voucher’ without any

change in target language writing system.

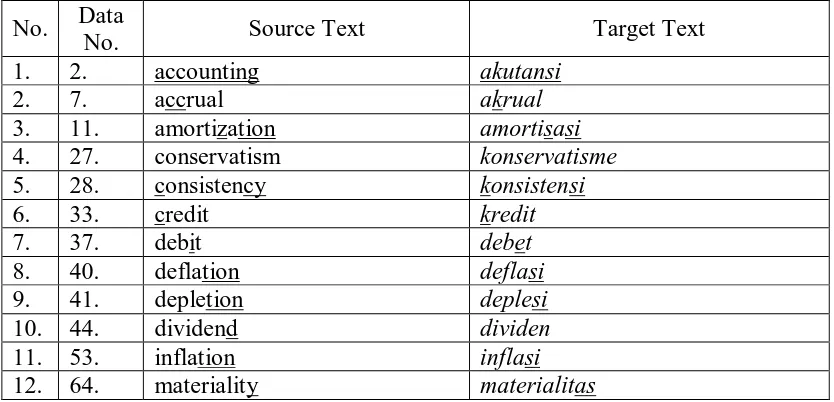

Table 7 shows mix loanwords.

Table 7: Mix loanwords.

No. Data

No. Source Text Target Text

1. 2. accounting akutansi

2. 7. accrual akrual

3. 11. amortization amortisasi

4. 27. conservatism konservatisme

5. 28. consistency konsistensi

6. 33. credit kredit

1.) accounting → akuntansi

‘Accouting’ is translated as ‘akuntansi’. It has undergone complete assimilation

into target language. It becomes incorporated into the system and the feeling of

the language to such extend that there are as much a part of vocabulary in target

language as any native words.

2.) accrual → akrual

‘Accrual’ is translated literally into target language as ‘akrual’. The word

‘akrual’ is imported from source language ‘accrual’ within the change of form

in target language. The letters ‘cc’ in source language is replaced by target

language respelling ‘k’.

3.) amortization → amortisasi

‘Amortization’ is translated literally into target language as ‘amortisasi’. The

word ‘amortisasi’ is import/borrowed from source language ‘amortization with

some change in writing system (form). The letter ‘z’ in source language changes

to letter‘s’ in target language and suffix ‘-tion’ in source language changes to

‘si’ in target language.

4.) consistency → konsistensi

‘Konsistensi’ is borrowed from source language ‘consistency’ with some

changes in writing system. The letter ‘c’ in source language is replaced by target

language respelling ‘k’ and the end letters ‘cy’ in source language is replaced by

5.) conservatism → konservatisme

‘Konservatisme’ is borrowed from source language ‘conservatism’ with some

changes in target language writing system. The letter ‘c’ in source language is

replace by target language respelling ‘k’ and the suffix ‘-ism’ in source language

changes to ‘-isme’ in target language.

6.) credit → kredit

‘Kredit’ is borrowed from source language ‘credit’. The letter ‘c’ in source

language is replaced by target language respelling ‘k’.

7.) debet → debit

‘Debit’ is borrowed from source language ‘debet’. The second letter ‘e’ in

source language is changes to ‘i’ in target language.

8.) eflation → deflasi

‘Deflasi’ is borrowed from source language ‘deflation’ with some

orthographical change in target language. The suffix ‘-tion’ in source language

is changes to ‘si’ in target language.

9.) dividend → dividen

‘Dividen’ is borrowed from source language ‘dividend’ with the change in target

language writing system. The final letters ‘d’ in source language is omitted in

10.) depletion → deplesi

‘Deplasi’ is borrowed from source language ‘depletion’ with the change in

target language writing system. The suffix ‘-tion’ in source language is changes

to ‘si’ in target language.

11.) inflation → inflasi

‘Inflasi’ is borrowed from source language ‘inflation’ with the change in target

language writing system. The suffix ‘-tion’ in source language is changes to ‘si’

in target language.

12.) materiality → materialitas

‘Materialitas’ is borrowed from source language ‘materiality’ with the change

in target language writing system. The final letter ‘y’ in source language

changes to ‘as’ in target language.

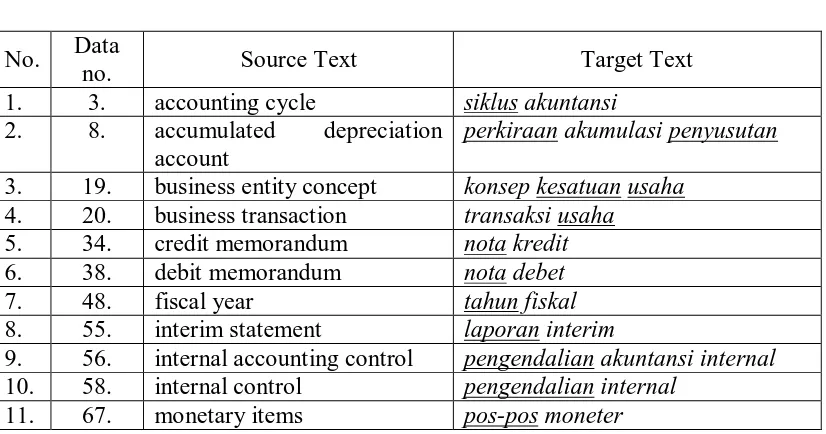

Loan blends: One of the two or more morphemes making up the compound form is

replaced by native morpheme. Table 8 shows loan blends.

Table 8: Loan blend.

No. Data

no. Source Text Target Text

1. 3. accounting cycle siklus akuntansi

2. 8. accumulated depreciation account

perkiraan akumulasi penyusutan

3. 19. business entity concept konsep kesatuan usaha

4. 20. business transaction transaksi usaha

5. 34. credit memorandum nota kredit

6. 38. debit memorandum nota debet

7. 48. fiscal year tahun fiskal

8. 55. interim statement laporan interim

9. 56. internal accounting control pengendalian akuntansi internal

10. 58. internal control pengendalian internal

12 73. nominal account perkiraan nominal

13. 74. nonmonetary items pos-pos nonmoneter

14. 75. normal pension cost biaya pensiun normal

15. 87. private accounting akuntansi internal

16. 89. promissory note surat promis

17. 94. residual value nilai residu

18. 106. temporary investment investasi sementara

19. 57. internal administrative control

pengendalian admimistratif internal

20. 10. allowance method metode penyisihan

1.) siklus akuntansi’

‘Siklus’ is native while ‘akuntansi’ is borrowed from source language

‘accounting’.

2.) ‘perkiraan akumulasi penyusutan’

‘Perkiraan’ is native, ‘penyusutan’ also native while ‘akumulasi’ is borrowed

from source language ‘accumulated’

3.) ‘konsep kesatuan usaha’

‘Konsep’ is borrowed from source language ‘concept’ while ‘kesatuan’ is native

and also ‘usaha’.

4.) ‘transaksi usaha’

‘Transaksi’ is borrowed from source language while ‘usaha’ is native.

5.) ‘nota kredit’

6.) ‘nota debet’

‘Nota’ is native while ‘debet’ is borrowed from source language ‘debit’.

7.) ‘tahun fiskal’

‘Tahun’ is native while ‘fiskal’ is borrowed from source language ‘fiscal’.

8.) ‘laporan interim’

‘Laporan’ is native while ‘interim’ is borrowed from source language ‘interim’.

9.) ‘pengendalian akuntansi internal’

‘Pengendalian’ is native while ‘akuntansi’ is borrowed from source language

‘accounting’ and ‘internal’ also borrowed from source language ‘internal’.

10.) ‘pengendalian internal’

‘Pengendalian’ is native while ‘internal’ is borrowed from source language

‘internal’.

11.) ‘pos-pos moneter’

‘Pos-pos’ is native while ‘moneter’ is borrowed from source language

‘monetary’.

12.) ‘perkiraan nominal’

‘Perkiraan’ is native while ‘nominal’ is borrowed from source language

13.) ‘pos-pos nonmoneter’

‘Pos-pos’ is native while ‘nonmoneter’ is borrowed from source language

‘nonmonetary’.

14.) ‘biaya pensiun normal’

‘Biaya’ is native while ‘pensiun’ is borrowed from source language ‘pension’

and ‘nominal’ is also borrowed from source language ‘nominal’.

15.) ‘akuntansi internal’

‘Akuntansi’ is borrowed from source language ‘Accounting’ while ‘private’ in

source language is translated to native as ‘internal’.

16.) ‘surat promis’

‘Surat’ is native while ‘promis’ is borrowed from source language ‘promissory’

17.) ‘nilai residu’

‘Nilai’ is native while ‘residu’ is borrowed from source language ‘residual’.

18.) ‘investasi sementara’

‘Sementara’ is native while ‘investasi’ is borrowed from source language

‘investment’.

‘Pengendalian’ is native while ‘administratif’ is borrowed from source

language and ‘internal’ also borrowed from source language ‘internal’.

20.) ‘metode penyisihan’

‘Metode’ is borrowed from source language ‘method’ while ‘penyisihan’ is

native.

4. 1. 3. 2 Calque

Calque is the procedure when there are some independent morphemes making

up the compound form, one of the morphemes is replaced by native (target language)

morpheme and the other morphemes are imported from source language. It is loand

words within linear substitution. Table 9 shows calque.

Table 9: Calque.

No. Data

no. Source Text Target Text

1. 16. bank reconciliation rekonsiliasi bank

2. 90. public accounting akuntansi public

3. 111. voucher register registrasi voucher

1.) bank reconciliation → bank rekonsiliasi

“Bank reconciliation’ is translated with linear substitution into target language.

‘Bank’ which is come as a first word in source language goes to second word in

target language and vice versa. Each item in source language is borrowed by

target language.

The word ‘bank’ is purely imported from source language ‘bank’ but the word

‘rekonsiliasi’ is imported from source language ‘reconciliation’ with some

is replaced by target language respelling ‘k’, the second letter ‘c’ in source

language is replaced by target language respelling ‘s’ and the suffix ‘-tion’ in

source language changes to ‘si’ in target language.

2.) public accounting → akuntansi publik

‘Public accounting’ has translated within linear substitution into target language.

The word ‘public’ which is come as a first word in source language goes to

second word in target language and vice versa. Each item in source language is

borrowed by target language with some orthographical change.

‘Accouting’ is translated as ‘akuntansi’. It has undergone complete assimilation

into target language. It becomes incorporated into the system and the feeling of

the language to such extend that there are as much a part of vocabulary in target

language as any native words.

‘Publik’ is borrowed from source language ‘public’ with the letter final letter ‘c’

in source language is replaced by target language ‘k’.

3.) voucher register → registrasi voucher

‘Voucher register’ has translated into target language within linear substitution.

First word in source language goes to second word in target language. Each

items in source language is borrowed by target language.

‘Voucher’ is purely borrowed from source language ‘voucher’ without any

change in target language writing system and ‘register’ is borrowed by target

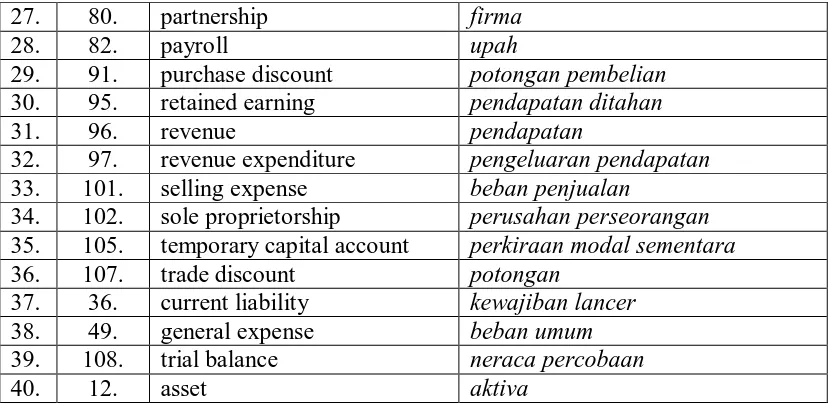

4. 1. 3. 3 Literal translation

Nababan (32: 1999) ‘penerjemahan harfiah (literal translation) terletak

antara penerjemahan kata demi kata dan penerjemahan bebas. Penerjemahan

harfiah mungkin mula-mula dilakukan seperti penerjemahan kata demi kata, tetapi

penerjemah kemudian menyesuaikan susunan kata dalam kalimat terjemahannya

yang sesuai dengan susunan kata dalam kalimat bahasa sasaran.’

These following table shows the data which concluded into literal translation where

the text in source language is translated word for word into target language by

adopting target language structure. Table 10 shows literal translation.

Table 10: Literal translation.

4. 22. capital expenditure pengeluaran modal

5. 23. capital statement laporan modal

6. 24. cash discount potongan tunai

7. 29. contingent liability kewajiban bersyarat

8. 30. contra asset account perkiraan lawan aktiva

9. 31. corporation perseroan

10. 35. current asset aktiva lancar

11. 39. deferral penangguhan

12. 42. depreciation penyusutan

13. 47. expense beban

14. 54. intangible asset aktiva takberwujud

15. 59. invoice faktur

16. 61. liability kewajiban

17. 62. long term liability kewajiban jangka panjang

18. 68. moving average rata-rata bergerak

19. 69. natural business year tahun usaha alami

27. 80. partnership firma

28. 82. payroll upah

29. 91. purchase discount potongan pembelian

30. 95. retained earning pendapatan ditahan

31. 96. revenue pendapatan

32. 97. revenue expenditure pengeluaran pendapatan

33. 101. selling expense beban penjualan

34. 102. sole proprietorship perusahan perseorangan

35. 105. temporary capital account perkiraan modal sementara

36. 107. trade discount potongan

37. 36. current liability kewajiban lancer

38. 49. general expense beban umum

39. 108. trial balance neraca percobaan

40. 12. asset aktiva

4. 1. 3. 4 Equivalence

Equivalence is a replacement of a source language situation by a

communicatively comparable target language situation. It is where two different

languages are equal whether a syntagmatic changes occur in target language.

Tables 11 show equivalence.

Table 11: Equivalence.

No. Data

no. Source Text Target Text

1. 4. account payable hutang dagang

2. 5. account receivable piutang dagang

3. 6. account payable ledger buku besar hutang dagang

4. 45. double entry accounting akuntansi buku berpasangan

5. 52. income statement perhitungan laba rugi

6. 63. marketable security surat berharga

7. 83. plant asset aktiva tetap

8. 85. posting membukukan

9. 104. subsidiary ledger buku tambahan

10. 112. work sheet neraca lajur

11. 9. adjusting entry ayat jurnal penyesuaian

The writer gives a brief definition for each accounting term by consulting the

dictionary (Oxford Advance Dictionary of Current English). So it can be seen the

equivalence of source language accounting term and target language accounting term.

1.) Account: [U] estimation.

2.) Payable: adj which must or may be paid.

3.) Receivable: adj that can be received; fit to be received.

4.) Ledger: n book in which a business firm’s account are kept.

5.) Entry: items notes in account book.

6.) Double: in twos; in pairs or couples.

7.) Income: n money received during a given period (as salary, receipts from trade,

interest from investment, etc)

8.) Statement: [c] stating of facts, views, a problem, etc; report.

9.) Accounting: give a reckoning of (money that has been entrusted to one)

10.) Marketable: adj that can be sold; fit to be sold.

11.) Security: [C, U] something valuable.

12.) Plant: n living organism which is not an animal.

13.) Asset: n (usu pl) anything owned by person, company etc that has money

value and that may be sold to pay debts.

14.) Posting: transfer item from a day-book to a ledger.

15.) Subsidiary: serving a help or support but not of first importance.

16.) Work: used of bodily or mental powers with the purpose of doing or making

something.

17.) Sheet: broad, flat piece (of some thin material).

18.) Adjusting: [U] settling of, eg insurance.

4. 1. 3. 5 Transposition

Transposition: is the same with shift, when literal translation produces an

‘unnatural’ passage. Table 12 shows transposition.

Table 12: Transposition.

No. Data

no. Source Text Target Text

1. 13. average cost method metode harga pokok rata-rata

2. 15. balance sheet neraca

3. 25. cash payment journal buku harian pengeluaran kas

4. 32. cost principle prinsip harga perolehan

5. 43. dishonored note receivable wesel tagih yang ditolak bank

6. 46. equity hak pemilikan hak

7. 50. general ledger buku harian

8. 51. income from operation laba operasi

9. 60. ledger buku besar

10. 65. maturity value nilai jatuh tempo

11. 66. merchandise inventory persediaan barang dagangan

12. 81. past service cost biaya masa kerja pada masa lalu

13. 84. post closing trial balance neraca percobaan setelah tutup buku

14. 86. prepaid expense beban dibayar di muka

15. 88. proceed hasil diskonto

16. 93. report form of balance sheet neraca bentuk laporan

17. 100. sales journal buku harian penjualan

18 103. special journal buku harian khusus

19. 109. unearned revenue pendapatan yang diterima di muka

20. 92. purchase journal buku harian pembelian

21. 14. balance of an account saldo perkiraan

22. 18. book value of an account nilai buku aktiva

23. 99. sales discount potongan penjualan

24. 26. chart of account bagan perkiraan

1.) cost → harga pokok

(a word) (a phrase)

‘Cost’ is a word level in source language which turns into a phrase level in

2.) balance sheet→ neraca

(a phrase) (a word)

‘Balance sheet’, a phrase level in source language turning into a word level in

target language.

3.) journal → buku harian

(a word) (a phrase)

‘Journal’ which is a word level in source language turning into phrase level in

target language.

4.) cost → harga perolehan

(a word) (a phrase)

‘Cost’ is a word level in source language which turns into a phrase level in

target language.

5.) dishonored → yang ditolak Bank (a word) (a clause)

‘Dishonored’ which is a word level in source language turning into a clause

level in target language.

6.) equity → hak pemilikan hak

(a word) (a phrase)

‘Equity’ which is a word level in source language turning into a phrase in target

language.

7.) general → is omitted, but does not change the meaning of the

8.) from → is omitted, but does not change the meaning of the

message.

9.) ledger → buku besar

(a word) (a phrase)

‘Ledger’ which is a word level in source language turning into a phrase level

in target language.

10.) maturity → jatuh tempo

(a word) (a phrase)

‘Maturity’ which is a word level in source language turning into a phrase level

in target language.

11.) merchandise → barang dagangan

(a word) (a phrase)

‘Merchandise’ which a word level in source language turning into a phrase level

in target language.

12.) past service → masa kerja pada masa lalu

(a phrase) (a clause)

‘Past service’ that is a phrase in source language turning into a clause in target

language.

13.) post closing → setelah tutup buku

(a phrase) (a clause)

‘Post closing’ that is phrase in source language turning into a clause in target

14.) prepaid → dibayar di muka

(a word) (a clause)

‘Prepaid’ which is a word in source language turning into a clause in target

language.

15.) proceed → hasil diskonto

(a word) (a phrase)

‘Proceed’ which is a word level in source language turning into a phrase level in

target language.

16.) of → is omitted, but does not change the meaning of the

message.

balance sheet → neraca

(a phrase) (a word)

‘Balance sheet’, a phrase level in source language turning into a word level in

target language.

17.) journal → buku harian

(a word) (a phrase)

‘Journal’ that is a word level in source language turning into a phrase level in

target language.

18.) journal → buku harian

(a word) (a phrase)

‘Journal’ that is a word level in source language turning into a phrase level in