i THE EFFECT FUNDAMENTAL FACTORS TO DIVIDEND PAYOUT RATIO: EMPIRICAL EVIDENCE ON MANUFACTURE COMPANIES THAT LISTED IN MAIN BOARD INDEX (MBX) AND DEVELOPMENT

BOARD INDEX (DBX) AT INDONESIA STOCK EXCHANGE (IDX) 2009-2010

By:

Taufik Faturahman 109081100016

MANAGEMENT DEPARTMENT INTERNATIONAL CLASS PROGRAM FACULTY OF ECONOMICS AND BUSINESS

STATE ISLAMIC UNIVERSITY SYARIF HIDAYATULLAH JAKARTA

vi CURICULUM VITAE

PERSONAL DATA

Name : Taufik Faturahman

Date of Birth : Muarabungo, Oct 29th 1991

Address : Jl. Rubaya Al-Ikhlas No.27 RT/RW 001/014, Karangpawitan, Karawang barat, Karawang. Religion : Islam

Phone : 087770783891

Email : [email protected]

EDUCATIONAL BACKGROUND

1. 1997-2003 : SDN Dukuh Semar II Cirebon 2. 2003-2006 : SMPN 6 Cirebon

3. 2006-2009 : SMAN 4 Karawang

ORGANIZATIONAL BACKGROUND

1. 2006-2009 Member of Basketball team SMAN 4 KARAWANG.

vii

PREFACE

Assalammu’alaikum Wr.Wb.

Firstly Thanks to Allah SWT, because of His blessing the writer can finished this thesis. Shalawat and Salam also give to the guidance prophet Muhammad SAW also to His Best friends.

Thesis entitled “The Effect Fundamental Factor to Dividend Payout Ratio: Empirical Evidence on Manufacture Companies that Listed in Main Board Index (MBX) and Development Board Index (DBX) at Indonesia Stock Exchange (IDX) period 2009-2014”. This is the final author in completing the undergraduate program at the Faculty of Economics and Business, Management Department of the State Islamic University Syarif Hidayatullah Jakarta.

In this chance, the writer wants to say thanks for supporting and helping from every party. So, thankful would be for :

1. Author parents who always give love, compassion motivation and support on completing this thesis. Accompaniment of uncessing prayer in each of these step.

2. Dr. Arief Mufraini, Lc., M.Si as Dean of Faculty of Economics and Business Syarif Hidayatullah Jakarta.

3. Dr. Indo Yama Nasarudin, SE,. MBA as first supervisor always motivate me and provide the best guidance to the author. So that author

viii 4. Mr. Tarmidzi Taridi Kasbi Ridho MBA as a second who always give

guidance for the creation of my thesis with good result.

5. Ms. Ela Patriana, MM as Secretary of Management Department who always give help and solutions when author still study in Faculty of

Economic and Business, State of Islamic University Syarif Hidayatullah

Jakarta.

6. All lecturers and Staff Management Department International Faculty of Economic and Business, State of Islamic University Syarif

Hidayatullah Jakarta, especially to Mr. Bonik.

7. Author Brother Sandi Muhtadin SH and Syahdan Mujahid, thank you always support author.

8. All author best friend in Management International class program (Akira, Adit, Aly, Ari, Angga, Luqman, Dipa, Gery, Surya, Rizky,

Haris, Khairul, Yaser, Aiya, Rara, Vera, Meta and Innez).

9. Author best friends in The Kostan Family ( Habibi, Fadil, Amir, Panji, Rio, Ghiyast, Faiq, Yoga, Deska, Agung, Nopan, Ryan, Doni, Sahid,

Adit and Natsir).

10. Author beloved girl Rifa Nurul Isromi who always support and give motivation to author for finished this thesis.

11. Author best friend in Karawang (Thole) who always remembering me to finishing author study in university and always support author in any

ix The author realizes There are still many short comings in the writing of this thesis. Therefore, the author beg criticism and suggestions that are built from the readers.

Jakarta, November 26th 2015

Author

x

ABSTRACT

This study aimed to analyze the effect of the financial enterprise or fundamental factors such as Profitability (Return on Assets, Return on Equity), Leverage (Debt to Equity, Debt to Assets), Liquidity (Current Ratio, Quick Ratio), Activity (Total Asset Turn Over) and Market Value (Price Earning Ratio) Dividend Payout Ratio in companies listed on the Main Board and Development Board in Indonesia Stock Exchange Index. The method used in this research is multiple linear regression, with a sample of manufacturing companies that distribute dividends on an ongoing basis for six consecutive years on the Main Board Index is 19 companies and Development Board Index is 10 companies. On the results of research conducted on the Main Board Index simultaneously each variable used to have influence with the results of the F-Test 0.000 less than 0.05, partially with the results of the T-Test of the nine indicators used only DAR and DER which has a significant influence on the dividend payout Adj R2 ratio with 0232 or 23.2% dividend payout ratio is determined by variable DAR and DER. While on the Development Board Index simultaneously each variable used to have influence with the results of the F-Test 0.000 less than 0.05, partially with the results of the T-Test of the nine indicators used only QR and DAR which has a significant influence on the dividend payout ratio to Adj R2 0391 or 39.1% dividend payout ratio is determined by variable QR and DAR.

xi

ABSTRAK

Penelitian ini bertujuan untuk menganalisa pengaruh keuangan perusahaan atau fundamental faktor seperti Profitability (Return on Asset, Return on Equity), Leverage ( Debt to Equity, Debt to Assets), Liquidity (Current Ratio, Quick Ratio), Activity (Total Asset Turn Over), dan Market Value (Price Earning Ratio) terhadap Dividend Payout Ratio di perusahaan manufaktur yang terdaftar pada Main Board dan Development Board Index di Bursa Efek Indonesia. Metode penelitian yang digunakan dalam penelitian ini adalah regresi linier berganda, dengan jumlah sampel perusahaan manufaktur yang membagikan dividen secara berkelanjutan selama 6 tahun berturut-turut pada Main Board Index adalah 19 perusahaan dan Development Board Index adalah 10 perusahaan. Pada hasil penelitian yang dilakukan pada Main Board Index secara simultan setiap variabel yang digunakan memiliki pengaruh dengan hasil F-Test 0.000 kurang dari 0.05, secara parsial dengan hasil T-Test dari sembilan indikator yang digunakan hanya DAR dan DER yang memiliki pengaruh signifikan pada dividen payout ratio dengan Adj R2 0.232

xii

List of Contents

CHAPTER I ... 1

A. Background ... 1

B. Problem formulations... 10

C. Research Objectives ... 11

D. Research Benefits ... 11

CHAPTER II ... 13

A. Theory ... 13

1. Financial report ... 13

2. Dividend ... 16

3. Kinds of dividends ... 16

4. Dividend payment procedure ... 17

5. Dividend policy ... 18

6. Dividend payout ratio ... 21

7. Financial Ratio... 22

8. Liquidity ratio ... 22

9. Leverage ratio ... 24

10. Profitability ratio ... 25

11. Activity ratio ... 26

xiii

B. Previous research ... 29

C. Theoritical framework ... 38

D. Hypothesis ... 41

CHAPTER III ... 43

A. Scope of research ... 43

B. Sampling method ... 43

C. Collecting Sample Method ... 46

1. Type of data ... 47

2. Data Sources ... 47

D. Methodology Data Analysis ... 47

1. Testing requirements analysis ... 48

2. Multiple analysis regressions ... 50

3. Simultaneously test (F test) ... 52

4. Test the partial significant (t-test) ... 53

5. Test the coefficient of determination (adj R2) ... 54

E. Definition Variable Operational ... 55

1. The dependent variable Dividend Payout Ratio (DPR) ... 55

2. Variable independent ... 56

a. Current Ratio ... 56

xiv

c. Debt to Asset Ratio. ... 57

d. Debt to Equity Ratio (DER) ... 57

e. Return on Assets (ROA) ... 58

f. Return on Equity (ROE) ... 58

g. Total Assets Turn Over (TATO) ... 59

h. Price Earning Ratio (PER) ... 60

CHAPTER IV ... 61

A. Scope of research ... 61

1. Indonesia Stock Exchange ... 61

2. Main board and Development board index ... 62

a. Main board index ... 62

b. Development board index ... 64

B. Analysis ... 67

1. Main Board Index Analysis... 68

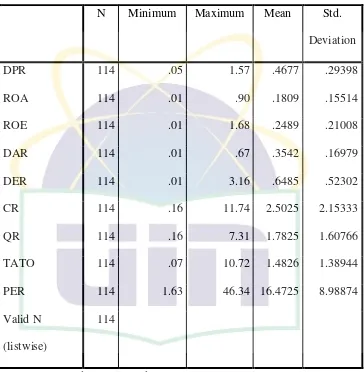

a. Descriptive statistic analysis ... 68

b. Assumption classic test ... 71

c. Hypothesis test of Main Board Index ... 79

2. Development Board Index Analysis ... 86

a. Descriptive analysis ... 86

xv

c. Hypothesis test of Development Board Index ... 99

3. Analysis Result of Main Board Index and Development Board Index. 107 CHAPTER V ... 110

A. Conclusion ... 110

1. Main Board ... 110

2. Development Board Index ... 110

B. Implication ... 112

REFERENCES ... 114

APPENDIX I ... 117

Manufacture Company listed in MBX ... 117

Manufacture Companies Listed in DBX ... 118

APPENDIX II MAIN BOARD INDEX ... 119

Raw Data 2009 ... 119

Raw Data 2010 ... 120

Raw Data 2011 ... 121

Raw Data 2012 ... 122

Raw Data 2013 ... 123

Raw Data 2014 ... 124

APPENDIX III DEVELOPMENT BOARD INDEX ... 125

xvi

Raw Data 2010 ... 125

Raw Data 2011 ... 126

Raw Data 2012 ... 126

Raw Data 2013 ... 127

APPENDIX IV ... 128

MBX SPSS 21.00 RESULT ... 128

APPENDIX V ... 132

DBX SPSS 21.00 RESULT (BEFORE TRANSFORM) ... 132

1

CHAPTER I

INTRODUCTIONA. Background

Currently economy growth is a main focus of all developing countries, especially Indonesia. Due to economy growth is the main capital to compete with other developed countries. With expected economic growth to increase investment and competition in all sectors of industrial owned thereby creating economic stability.

Based on Indonesia's economy report published by Bank of Indonesia in 2013 and news of Indonesian economic growth in 2014 were published by Badan Pusat Statistik declared current Indonesia economic growth on 2014 decreased become

5.02% more than contrast previous years. Where, in 2013 Indonesia's economic growth in 2013 reached 5.8% and in 2012 reached 6.2%. Decline on economic growth in Indonesia for 2 years in a row that has a major impact on the value of investments in capital markets and the performance of companies listed on the stock market to create profit.

2 deciding to invest in capital markets. Indexes that exist today in the Indonesian capital market is IHSG ,MBX, DBX, KOMPAS-100, LQ-45, JII, INFOBANK-15, PEFINDO-25, IDX-30 BUSINESS-27 INVESTOR-33, SMinfra-18 SRI-KEHATI, MNC-36 and ISSI.

3 Table 1.1

MBX and DBX stock return

Years Main Board Index (%) Development Board Index (%)

2003 62.57 62.86

2004 46.79 34.09

2005 18.96 2.15

2006 59.54 31.52

2007 40.97 137.03

2008 -46.36 -70.78

2009 87.77 80.80

2010 46.32 44.98

2011 3.74 -0.65

2012 13.15 11.39

2013 -2.47 9.60

Source: http://rudiyanto.blog.kontan.co.id/

Although both indexes are created based on size, the index have nearly the same movement. Based on table 1.1 of return growth generated during the development board index is not always under the main board index. The annual return is based on comparison of data both indices during the periods 2003-2013 can be seen the return of the majority of the development board is filled by a company with a small size can be aligned with the main board index. So, by the data expected to be the choice of investors to invest in Indonesia capital market.

4 stock exchange which are Main Board and Development Board Index. Where, the manufactures company virtually unaffected by fluctuations in the economy. The company will continue to exist and survive due to the products produced by the manufacturing company. Demand for the products that produced by the company will remain stable despite a decline. However, not affect the activity of the enterprise to generate optimal profit. The statement can be proved by the inconsistency of the number of companies that distribute dividends from 2010 to 2014 which can be seen in Table 1.2.

Table 1.2

Total manufacture Company distributed dividend period 2010-2014 Years Total Manufacture distributed dividend

2010 45 companies

2011 49 companies

2012 54 companies

2013 47 companies

2014 54 companies

5 Destination of investors to buying shares is expecting profit from arising the shares price they purchase before. An investor can get two benefits on its shares which are capital gains and dividend. Capital gain is the return obtained by the difference between the purchase price and the selling price of stock transactions by investors, while the dividend is part of the company profits are distributed to shareholders. (Brigham and Houston,2009). According Warsono (2003) said dividend is part of earnings that available to distribute for common shareholders were the distributed to shareholders in cash or other form from cash.

Dividend policy is a decision to determine how much dividend to be distributed

to the shareholders. This policy made from how the treatment of management on corporate profits there is generally a portion of net income after taxes distributed to investors in the form of percentage of retained earnings to be paid to shareholders in form of cash dividend (Riyanto, 2001).

6 estimates the flow of a stock dividend in the future by means predicting earnings per share and cash dividend. (Sharpe, Alexander and Bailey, 1999).

To conduct fundamental analysis an investor would have to financial information about the company. One of information that can be used by investors is a financial report. Financial report will report the financial position at a certain point in time and its operation for a period in the past. However, the value can be used to help predict profits and dividends in the future. From the standpoint of investors, predicting the future nature of financial report analysis (Brigham and Houston, 2009).

Financial analysis provides information about the assessment and company's

financial condition, which have past and present as well as future expectations. The purpose of this analysis to identify any weaknesses of the financial situation could an advantages of the company. In addition, financial analysis conducted by outside parties can be used to determine the credibility and potential companies for investment (Tampubolon, 2013).

Financial ratios helped us to identify some of the weaknesses and strengths of

7 According Kasmir (2014) there are six forms of financial ratios including liquidity, leverage, activity, profitability, growth and market valuation ratio.

Where, every financial ratio has different purpose, usefulness and sense.

Liquidity ratio is a ratio that shows the relationship between cash and current

assets of a company, compare by its current liabilities. In other words, the liquidity

ratio serves to indicate or measure a company's ability to meet obligations that have matured, both liability to parties outside and within the company. Thus, it can be said that the usefulness of this ratio is to determine the company's ability to finance and fulfill the obligations of companies that include dividend payments. (Kasmir,2014). This ratio very important becaused higher companies can fulfill they liabilities can influence to avaibility of cash. If avaibility of cash decrease make dividend paid by cash also decreased.

Leverage ratio is a financial ratio used to measure a company's ability to meet

its long-term liabilities. Any use by the company's debt will affect the risks and returns. The smaller this ratio are make more company can pay dividends and risk

of company become smaller (Warsono, 2003). Higher leverage make paid dividend decreased because Management of companies must paid they liabilities first Ike obligations. Its mean higher debt companies own make dividend paid more small.

Profitability ratio is a ratio for assessing the ability of the enterprise for profit.

8 2014). Dividend can paid if the companies have a profit. Higher profit companies have, more higher dividend can paid by companies.

Activity ratio is the ratio that indicates how fast assets elements converted into

sales or cash. This ratio aims to assess the company's ability to create the company's

liquidity. The higher the activity ratio, higher the possibility of the company to solve

its obligations (Moeljadi, 2006). The greater this ratio the more likely companies to get cash. Because, dividend distributed in cash.

Market value ratio is the ratio that describes conditions that occur in the market.

This ratio is able to provide insight for the management of the company on the condition that the application will be implemented and its impact on the future (Fahmi,2014). This ratio has a decisive influence on the company's dividend policy and its impact on the company.

This study aims to analyze the influence of financial ratios namely liquidity, leverage, activity, profitability and market valuation to dividend payout in public companies listed on the stock exchange Indonesia, particularly in the company's shares are listed on Main Board and Development Board Index on the stock exchange of Indonesia as population place that researchers choose. While previous studies proposed by Farah Margaretha leon and Pradana Maulana Putra (2014) and Eliasu Nuhu, Abubakar Musah and Damankah Basil Senyo (2014).

9 linear regression method. The variables examined in the study was the profitability (return on assets), debt to equity, market book value, tax rate and sale growth to

the sample companies as much as 6 companies Indonesia Stock Exchange in the period 2006-2009. Of the overall results of research variables have an influence on the dividend payout ratio. Partial research return on asset and debt to equity has an influence on the dividend payout ratio. Whereas, the other ratio does not have an influence on the dividend payout ratio.

Abubakar Musah and Damankah Basil Senyo (2014) research by "determinant of dividen payout of Financial firms and nun Financial firms in ghana". The

research aimed to find out the factors that influence cash dividend policy with panel data method. The variables examined in this study is debt to assets ratio profitability (return on assets), market to book value, tax, and size. The samples are

10 companies Financial firms and 10 companies non Financial firms in ghana stock exchange over the period 2000-2009. Of the overall results of his research have a significant influence on dividend payout ratio. Partial studies have a significant influence size on the dividend payout ratio.

10 price earnings ratio (PER), (3) liquidity (quick ratio and current ratio), and

profitability with return on equity addition, (4) the period of the research is 6 years from 2009-2014, This research is expected to provide information to the investor-oriented long-term investments with hope in dividend and management in determining dividend policy is based on the company's financial condition.

Based on this background, the authors are interested in doing research on the analysis of the effect of the liquidity ratio (current assets, quick ratio), profitability (return on assets, return on equity), leverage (debt to assets, debt to equity), activity

(total assets turnover) and market valuation (price-earnings ratio) of the dividend

policy (payout ratio) in the form of a thesis with the title

“The Effect Fundamental Factor to Dividend Payout Ratio: Empirical

Evidence on Manufacture Companies that Listed in Main Board Index (MBX) and Development Board Index (DBX) at Indonesia Stock Exchange (IDX) period 2009-2014”

B. Problem formulations

1. Are there any influence of liquidity ratio (Current Ratio & Quick Ratio), profitability (Return on Assets & Return on Equity), Activities (Total Assets Turn Over), Leverage (Debt to Assets & Debt to Equity) and market valuation (Price Earning Ratio) simultaneously to Dividend Payout Ratio to the company in Main Board and Development Board Index.

11 Turn Over), Leverage (Debt to Assets & Debt to Equity) and market

valuation (Price Earning Ratio) are partially to Dividend Payout Ratio to

the company in Main Board and Development Board Index.

C. Research Objectives

1. To analyze the effect of liquidity ratio (Current Ratio & Quick Ratio), profitability (Return on Assets & Return on Equity), Activities (Total Assets

Turn Over), Leverage (Debt to Assets & Debt to Equity) and market

valuation (Price Earning Ratio) are partially to Dividend Payout Ratio to

the company in Main Board and Development Board Index.

2. To analyze the effect of liquidity ratio (Current Ratio & Quick Ratio), profitability (Return on Assets & Return on Equity), Activities (Total Assets

Turn Over), Leverage (Debt to Assets & Debt to Equity) and market

valuation (Price Earning Ratio) are partially to Dividend Payout Ratio to

the company in Main Board and Development Board Index.

D. Research Benefits

Results of this research will be useful for :

12 2. For management, can be taken into consideration in determining dividend policy. is expected to help financial managers in decision-making to determine the amount of dividend paid mainly in the form of cash dividend. 3. For academic, this study may provide empirical evidence about the financial ratios that affect dividend policy. So as to provide insight and deep knowledge as well as a basis for further research on dividend policy. 4. For authors, this study is not only useful as one of the requirements for

13

CHAPTER II

LITERATURE REVIEWS A. Theory

1. Financial report

Financial report is a report that provides information on changes and

the company's financial position which has occurred on assets, earnings and dividends over the last year be some (Brigham & Houston, 2009: 46).

According Munawir (2002) in Fahmi (2014:21) said financial report is a very important tool to obtain information relating to the financial position and the results that have been achieved by the company concerned. Wherein, the financial report may be expected to be helpful for the users to make economic decisions.

Kasmir (2014:10) argues financial report prepared based on various purposes. The main purpose of financial report are for the benefit of owners, management companies and provide information to the various parties are very interested in the company. Which include :

a. Owner

Owners at the moment are those who have the business. This is reflected in its share ownership. The interests of the shareholders who are owners of the company to the reports that have been made are

14 3) To see the development and progress of the company during the

period.

b. Management

The interests of the management company to the company's financial statements they make has a specific meaning. For the management of financial statements that are made is a reflection of their performance within a specific period following important value of financial reports for management :

1) Management can assess and evaluate their performance in a period.

2) To see management capabilities to optimize the resources of the company so far.

3) To see the strengths and weaknesses of the company at this time so that it can be a basis for decision making in the future.

4) To take financial decisions based on the strengths and weaknesses of the company.

c. Creditor

15 1) To see the company's ability to repay the loan.

2) To assess the feasibility of which will be financed and the large number of loans approved will be illustrated by the financial report.

d. Government

Government has an important value to the financial statements the company made. Even the government through the finance department require every company to develop and the company's financial report periodically. The importance of the financial statements for the government are:

1) To assess the honesty of the company in the company's financial reports all true.

2) To determine the company's obligation to the state of the reported financial results. Of these financial statements will be seen the amount of taxes to be paid to the state are honest.

e. Investor

16 the business now and in the future. The prospect in question is an advantage to be gained such as dividends and capital gains.

2. Dividend

The definition of dividends in some literature basically have the same core that is part of the company's net profit distributed to shareholders. The explanation of the meaning of dividend on some literature is as follows

Dividend is part of the earnings available to common shareholders were distributed to the holders of common stock in cash. Retained earnings are the portion of income available to holders of ordinary shares held by the company to be reinvested in a particular project, with the aim to pursue the growth of the company (Warsono, 2003: 271).

According Ambarwati (2010: 64) stated dividend is a payment by the company to the shareholders derived from income or earnings in cash for the shares. The amount of dividend given specified in the shareholders' general meeting of members and expressed in an amount or a certain percentage of the nominal value and not on its market value.

3. Kinds of dividends

Warsono (2003: 272) states that the types of dividends a company is divided into three kinds of them.

a. Cash dividend

17 form of cash. Cash dividend received by the common shareholders by check or sometimes they reinvest in ordinary shares in the company.

b. Stock dividend

Stock dividend is the dividend payment in shares. This stock dividend is often used in lieu of the dividend in cash or supplies of cash dividend. The company will provide its common stock dividend to announce the amount of the dividend in a certain percentage.

c. Property dividend

Property dividend is prorated distribution of a physical asset. The asset is usually in the form of the products produced by the company. Dividend property is given if the number of shareholders of the company are still few and companies produce something easily distributed.

4. Dividend payment procedure

According Ambarwati (66: 2010) in dividend payments, there are several stages or procedure is as follows:

a. Date of declaration

18 b. Date of record

The date on which shareholders are determined, so that declared itself on that date are shareholders obtaining dividend on the payment date.

c. Ex-dividend date

Before the record date, the company should be notified in case of buying and selling on the stock. Therefore, the international exchanges agreed on the ex-dividend date is three days recording date. After the listing, the shares no longer have the right to dividend on the payment date.

d. Date of payment

On this date, the dividend paid to shareholders. After holding the dividend, cash on debit and receivables are eliminated. Dividend payments will be subject to income tax withholding.

5. Dividend policy

19 a. Theory of dividend policy

According Ambarwati (86: 2010) says there are three theories on the preferences of investors, namely

1) Dividend irrelevance theory

A theory which states that the dividend policy has no effect, good to firm value and the cost of capital. This theory follow the opinion of Modigliani and Miller stating that the value of a company is not determined by the size dividend payout ratio but is determined by the net income before tax and business risk. Thus, this theory assumes that investors do not have differences in terms of dividends and capital gains.

2) Bird in hand theory

According to Gordon and Litner, dividends received is something that certainly at hand so that it has a lower risk than capital gains. Gordon and Litner think investors prefer dividends because more certain revenue, rather than expecting an income that is uncertain if reinvesting the dividend in a particular investment.

3) Tax preference theory

20 b. Kinds of dividend policy

According Sundjaja and Barlin (2010: 388) There are three types of dividend policy, which are:

1) Dividend policy payout ratio constant

This policy is based to a certain percentage of revenue. Wherein, the ratio of repayment of every penny generated and distributed to the owners in the form of cash, calculated by dividing the cash dividend per share by earnings per share. The problem with this policy is that if the company's earnings fell or loss in a given period. The dividend to be low or non-existent. Because the dividend is an indicator of the condition of the company that will come then it may have a negative impact on stock prices.

2) Regular dividend policy

Dividend policy is based on the payment of dividends by the rupiah remains in each period. Regular policy is often used in wearing a target dividend payout ratio. Wherein, the target dividend payout ratio is a policy whereby companies try to pay dividend a certain percentage of such dividend declared in rupiah and adjusted to the target payment that proves the increase results.

3) Low dividend policy on a regular and plus extras

21 higher than usual in certain periods. Companies must pay an additional dividend is called an extra dividend.

c. Factors affecting the payment of dividends

1) Liquidity position of company

The stronger the greater the company's liquidity position dividends paid.

2) Needs the funds to pay debt

When most of the profits are used to pay the debt then the rest is used to pay a smaller dividend.

3) Expansion plans

The larger the company's business expansion, diminishing the funds can be paid.

4) Supervision of the company

Financing policy for the expansion was financed with funds from internal sources include earnings. Consideration when financed with the sale of new shares will weaken the control of the dominant shareholder group. Because the sound is reduced majority shareholder.

6. Dividend payout ratio

22 if there are retained earnings, a company should not distribute dividend if retained earnings at the end of the year is still negative.

7. Financial Ratio

Based on James C Van Horne in Kasmir (2014) financial ratio is an index that connects two accounting numbers and is obtained by dividing one number by another number. In which, the financial ratios used to evaluate the financial condition and performance of the company. The ratios can be seen financial condition of the company. Financial ratios is a study see the comparison between the amounts contained in the financial statements using the formulas are considered representative to be applied. there are have 6 ratios that describe By Fahmi (2014) but on this research used 5 ratios that is liquidity, profitability, leverage, activities, and market value.

8. Liquidity ratio

According to Brigham and Houston (2009:95) liquidity is a ratio that shows the relationship between the cash and other current assets of a company by its current liabilities. Fahmi (2014: 65) states the ratio of liquidity is the ability of a company meet short-term obligations on a timely basis. That ability can be realized if the amount of current assets is greater than the sum of current liabilities. Kasmir (2014: 131) states that the purpose and benefits of liquidity ratios, among others

23 b. To measure a company's ability to pay short-term liabilities with

current assets overall.

c. To measure a company's ability to pay short-term liabilities with current assets without taking into account the inventory.

d. As a planning tool for the future, especially with regard to cash planning and debt.

e. Be a trigger tool for the management to improve its performance by looking at the ratio of liquidity that exists today.

Therefore, the company that liquid is a company that is able to meet its maturing obligations and companies that are not liquid is a company that is unable to fulfill all its obligations maturing. Companies that are not liquid will lose the trust of outsiders, especially creditors and suppliers and of the parties to that employee.

Fahmi (2014: 65) states there are two indicators to measure the liquidity that is commonly used, the current ratio and quick ratio.

a. Current asset

Current ratio is the result of a comparison between the current assets by current liabilities. Current ratio can also be said as a form to measure the degree of margin of safety of a company.

b. Quick ratio

24 9. Leverage ratio

Leverage ratio is a ratio used to measure the extent of the company's assets are financed by debt (Fahmi, 2014: 72). Means how much the debt burden borne by the company as compared to its assets.

According Kasmir (2014: 155) the types of ratios that exist in the leverage ratio, among others, as follows:

a. Debt to asset ratio

Debt to asset ratio is one measure of the leverage ratio is calculated by measuring the ratio between total debt both current liabilities and non-current debt to total assets of both current assets and fixed assets. In other words, how much of the company's assets are financed by debt affect the asset management company.

b. Debt to equity ratio

Debt to equity ratio is one measure of the leverage ratio which is a company's ability to pay its obligations if liquidated. Debt to equity ratio is used to assess the debt with equity. This ratio is sought by comparing the entire debt to total capital owned.

c. Long-term debt to equity

25 d. Time interest earned

Time interest earned is a ratio to measure the extent to which income can be decreased without making the company feel embarrassed unable to pay its annual interest costs.

But in this study the indicators used to measure the leverage ratio is Debt to asset and debt to equity ratio.

10.Profitability ratio

According to Brigham and Houston (2009:107) profitability is a group that shows the ratio of the combined effects of liquidity, asset and debt management on operating results. Profitability ratio is the ratio used to measure the effectiveness of the overall management addressed by the size of the level of profits in connection with the sale or investment. The better the profitability ratio, the better the company's ability to gain a firm (Fahmi, 2014: 80). According to Kashmir (2014: 196) ratio is the ratio of profitability to assess the company's ability to make a profit. The types of profitability ratios that can be used are:

a. Return on assets

26 b. Return on equity

Return on equity is the ratio of net profit after tax measure with their own capital. This ratio indicates the efficient use of capital itself.

c. Net profit margin

Profit margin on sales is a ratio used to measure the profit margin on the sale. Measurement of this ratio is to compare net profit after tax to net sales.

d. Earning per share

Earnings per share is the ratio to measure management success in achieving profits for shareholders. A low ratio means that the management has not managed to satisfy shareholders, in contrast with the high ratio, increasing shareholder wealth.

But in this study the indicators used to measure the profitability ratio is return on assets and return on equity.

11.Activity ratio

27 a. Receivable turn over

Receivable turnover ratio is used to measure how deep the receivables collection period. Calculation to find receivable turnover is divided by the loans it sold receivables.

b. Inventory turn over

Inventory turnover is a ratio used to measure how many times the funds invested in this inventory rotates in a period.

c. Fixed asset turn over

Fixed asset turnover ratio is used to measure how many times the funds invested in fixed assets spun in one period. Formula to find the fixed asset turnover is it sold divided by total fixed assets.

d. Total asset turn over

Total assets turnover is a ratio used to measure the velocity of all assets owned company and quantify how much of each rupiah assets acquired in accordance with the preceding discussion, the total asset turnover formula used is it sold divided by total assets.

In this study the indicators used to measure the activity is the total asset turnover.

12.Market valuation

28 company on the condition that the application will be implemented and its impact on the future (Fahmi, 2014:82). According to Brigham and Houston (2009: 110) the ratio of market value is a set ratio that connects the company's stock price to earnings, cash flow and book value per share.

a. Price earning ratio

Price earnings ratio is the ratio of the price per share to earnings per share, indicating the dollar amount the investor is willing to pay any profits run.

b. Earning per share

Earnings per share is the price per share divided by cash flow per share, showing the amount of money paid by the NII investor willing to every cash flow.

c. Book value of share

29 B. Previous research

Research on “Influence Fundamental Factors to Dividend Payout Ratio ” is

using some references of previous research conducted by

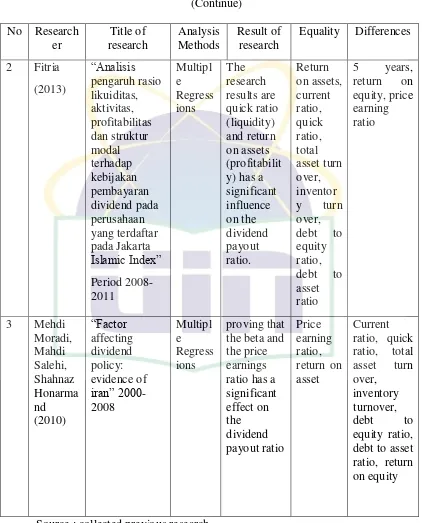

Research on dividend policy has never been done before, namely research typically involves the Fitria (2013) who conducted the research in Jakarta Islamic Index (JII) with 15 samples are distributed dividend in succession during the period 2008-2011 which proves that all the variables studied were liquidity, activity, profitability and capital structure. Wherein, the research results are quick ratio (liquidity) and return on assets (profitability) has a significant influence on the dividend payout ratio.

Rizka (2013) with 31 companies manufacture listed on the Indonesia Stock Exchange in 2008-2011. Found that only a variable return on investment (ROI) that significantly influence the dividend payout ratio. Whereas, liquidity ratio (current ratio), leverage (debt to equity ratio) and size has no effect on the dividend payout ratio.

Moradi, Salehi and honarmand (2010) with 73 samples listed on the stock exchange Theran in the study period 2000-2008, proving that the beta and the price earnings ratio has a significant effect on the dividend payout ratio.

30 share, market value to book value, cash flow, leverage, liquidity and return on assets have no effect on dividend payout ratio.

Other research conducted by komrattanapanya (2013) with a sample of 435 companies listed on the stock exchange of Thailand during the period 2006-2010. with the results that the debt to equity, growth, market to book value, size, small firm profit, large profit firm, medium and firm profits have significant influence on the dividend payout ratio.

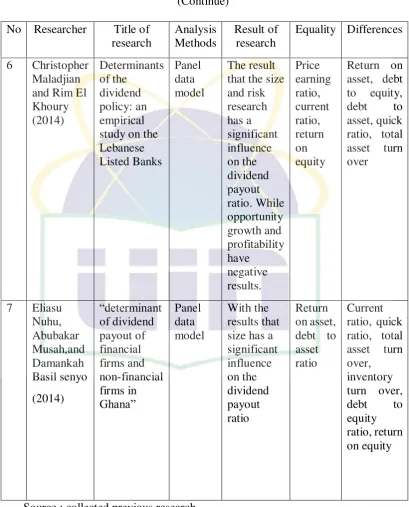

Conducted by Maladjian and Khoury (2014) with a sample of 28 companies listed on the Beirut Stock Exchange during the period from 2005 to 2011. With the result that the size and risk research has a significant influence on the dividend payout ratio. While opportunity growth and profitability have negative results.

Research conducted by Nuhu, Musah and Senyo (2014) with a sample of 30 companies listed on the Ghana Stock Exchange during the 2000-2009 period. With the results that size has a significant influence on the dividend payout ratio.

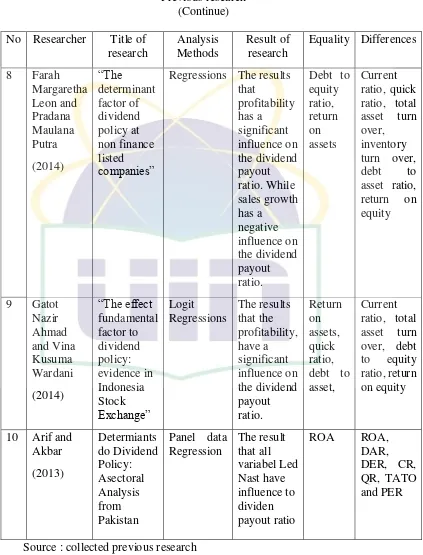

Research conducted by Leon and Putra (2014) with a sample of 26 companies listed on the Ghana Stock Exchange during the period 2006-2009. With the results that profitability has a significant influence on the dividend payout ratio. While sales growth has a negative influence on the dividend payout ratio.

31 With the results that the profitability, liquidity, leverage, firm size and growth opportunities have a significant influence on the dividend payout ratio.

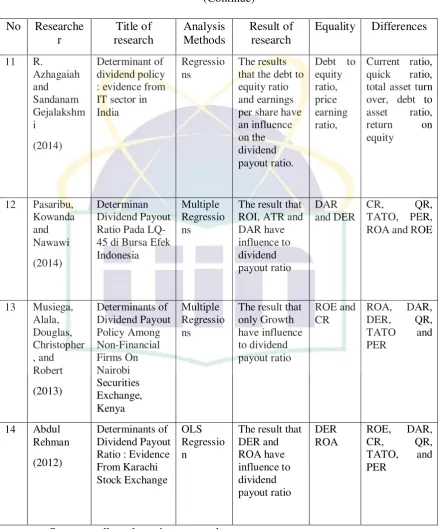

Research conducted by Azhagaiah and Gajalakshmi (2014) with a sample of 84 companies listed on the IT sector of India Stock Exchange during the period 2008-2012. With the results that the debt to equity ratio and earnings per share have an influence on the dividend payout ratio.

Research conducted by Arif and Akbar (2013) with a sample of 174 companies listed on Karachi Stock Exchange during the period 2005-2010. With the results that the profitabilitas, tax, size and Investment opportunity have an influence on the dividend payout ratio.

Research conducted by Pasaribu, Kowanda and Nawawi (2014) with a sample of 45 companies listed on LQ-45 in Indonesia Stock Exchange during the period 2007-2011. With the results that the return on Investment, total Asset turn over and debat ratio have an influence on the dividend payout ratio.

Research conducted by Musiege, Alala, Douglas, Christopher and Robert (2013) with a sample of 30 companies listed on the Nairobi Security Exchange during the period 2007-2011. With the results that the growth opportunity (market price to book value) have an influence on the dividend payout ratio.

32

33

34

35

36

37

38 C. Theoritical framework

The framework is part of a literature review which contains an overview of all the basics of the theories have used as a basis in this study. This study intends to test the effect of variable analysis of liquidity, leverage, profitability, activity and growth in dividend payout ratio in the companies listed on the main board and the development board index in the Indonesia Stock Exchange (BEI) in the study period 2009-2014.

To predict the dividend income cannot consider factors management policy, as a management policy decisions relating to the internal company. The only information relating to the condition of the company is a financial statement that shows the financial performance generated by the company's management. If the company decides to split the profits in dividends, all ordinary shareholders gain ownership rights based on shares held. The size of the dividend that is distributed is influenced by various factors which may affect the dividend. Fundamental factors which will affect the dividend in this study is liquidity (CR, QR), Leverage (DAR, DER), profitability (ROA, ROE), activity (TATO) and market value (PER) which will be used as independent variables and Dividend Payout Ratio as the dependent variable.

39 characteristics of the population. Kinds of data used in this research is secondary data obtained from the center of the capital market reference point.

In this study, calculate partial financial ratios will be calculated by using the Microsoft software in 2010 by entering each formula and the calculation results of each variable. Having obtained the results, the data is formatted excel converted into SPSS version 21.0 for Windows release for further testing to the requirements of data analysis is the normality test to determine whether the data were normally distributed or not. Where, no autocorrelation, and heteroscedasticity multikoloniritas. Otherwise the multiple regression analysis, F test, t test and Adj R2.

From the above explanation it will be calculated based on the sample studied were in the company listed on the Main Board Index and Development Board Index 2009-2014. From the results of data calculation using multiple regression analysis test, F test, t test, Adj R2. It can be seen how the effect of variable

40 Figure 2.1

Framework

IDX

ASSUMPTION CLASSIC TEST NORMALITY, AUTOCORELATION,

MULTICOLLONIERITY, HETEROCEDASTICITY MANUFACTURE COMPANIES

DEVELOPMENT BOARD INDEX MAIN BOARD INDEX

INTERPRETATION INDEPENDENT VARIABLE

1. LIQUIDITY (CR&QR) 2. LEVERAGE (DAR&DER) 3. PROFITABILITY (ROA&ROE) 4. ACTIVITY (TATO)

5. MARKET VALUE (PER)

DEPENDENT VARIABLE DIVIDEND PAYOUT RATIO

MULTIPLE REGRESSIONS

R2 test t test

41 D. Hypothesis

1. a. H0: b1, b2, b3, b4, b5, ... bn = H0 there is no influence of liquidity ratio (CR,

QR), Leverage (DAR, DER), profitability (ROA, ROE), Activities (TATO) and Market Value (P/E) simultaneously to the dividend payout ratio at companies listed on the Main Board and Development Board Index.

b. Ha: b1≠ b2, or b2≠ b3 or b3≠

b4 or b4≠ b5 or b5.... ≠ 0

42

2. a. H0: b = 0 there is no influence of liquidity ratio (CR,

QR), Leverage (DAR, DER), profitability (ROA, ROE), Activities (TATO) and Market Value (P/E) partially against dividend policy (DPR) to the companies listed on the Main Board and Development Board Index.

b. Ha: b1≠ 0 there are significant influence of liquidity

43

CHAPTER III

Research MethodologyA. Scope of research

In this study the authors chose the Indonesian Stock Exchange as a place to do research. Location of research have been regarded as a great place for researchers to obtain the necessary data in the form of financial reports. Sampled from companies listed on the Main Board Index and Development Board Index in Indonesia 2009-2014. B. Sampling method

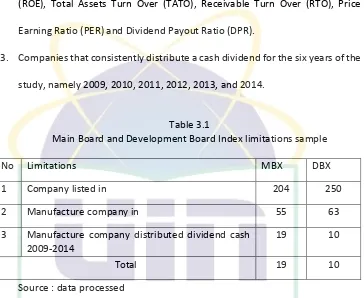

Selection of the sample were selected by purposive sampling of all companies listed on the Main Board Index and Development Index in Indonesia Stock Exchange (BEI) in order to obtain a representative sample based on predetermined criteria. Purposive sampling technique is a technique in which non-probability sampling is not random selection techniques which information is obtained based on certain considerations and generally adapted to the purpose or research problems (Indriantoro and Supomo, 2002: 131). This study took a sample to the criteria of the companies listed in the Indonesia Stock Exchange during the five years in the period 2009-2014. Thus, consideration or criteria for the determination of the sample in this study, namely:

44 2. Companies that deliver the data in full accordance with the required information, the Current Ratio (CR), Quick Ratio (QR), Debt to Asset Ratio (DAR), Debt to Equity Ratio (DER), Return on Assets (ROA), return on Equity (ROE), Total Assets Turn Over (TATO), Receivable Turn Over (RTO), Price Earning Ratio (PER) and Dividend Payout Ratio (DPR).

3. Companies that consistently distribute a cash dividend for the six years of the study, namely 2009, 2010, 2011, 2012, 2013, and 2014.

Table 3.1

Main Board and Development Board Index limitations sample

No Limitations MBX DBX

1 Company listed in 204 250

2 Manufacture company in 55 63

3 Manufacture company distributed dividend cash 2009-2014

19 10

Total 19 10

Source : data processed

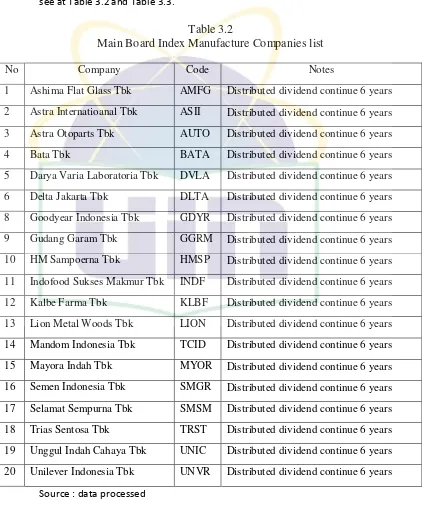

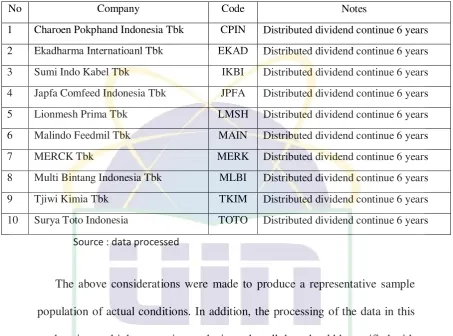

45 2014. The total manufacture companies distributed companies from 2009 to 2014 are 19 companies in Main Board Index and 10 Companies in Development Board Index. With list name of manufacture companies list can see at Table 3.2 and Table 3.3.

Table 3.2

Main Board Index Manufacture Companies list

No Company Code Notes

1 Ashima Flat Glass Tbk AMFG Distributed dividend continue 6 years 2 Astra Internatioanal Tbk ASII Distributed dividend continue 6 years 3 Astra Otoparts Tbk AUTO Distributed dividend continue 6 years 4 Bata Tbk BATA Distributed dividend continue 6 years 5 Darya Varia Laboratoria Tbk DVLA Distributed dividend continue 6 years 6 Delta Jakarta Tbk DLTA Distributed dividend continue 6 years 8 Goodyear Indonesia Tbk GDYR Distributed dividend continue 6 years 9 Gudang Garam Tbk GGRM Distributed dividend continue 6 years 10 HM Sampoerna Tbk HMSP Distributed dividend continue 6 years 11 Indofood Sukses Makmur Tbk INDF Distributed dividend continue 6 years 12 Kalbe Farma Tbk KLBF Distributed dividend continue 6 years 13 Lion Metal Woods Tbk LION Distributed dividend continue 6 years 14 Mandom Indonesia Tbk TCID Distributed dividend continue 6 years 15 Mayora Indah Tbk MYOR Distributed dividend continue 6 years 16 Semen Indonesia Tbk SMGR Distributed dividend continue 6 years 17 Selamat Sempurna Tbk SMSM Distributed dividend continue 6 years 18 Trias Sentosa Tbk TRST Distributed dividend continue 6 years 19 Unggul Indah Cahaya Tbk UNIC Distributed dividend continue 6 years 20 Unilever Indonesia Tbk UNVR Distributed dividend continue 6 years

46 Table 3.2

Main Board Index Manufacture Companies list

No Company Code Notes

1 Charoen Pokphand Indonesia Tbk CPIN Distributed dividend continue 6 years 2 Ekadharma Internatioanl Tbk EKAD Distributed dividend continue 6 years 3 Sumi Indo Kabel Tbk IKBI Distributed dividend continue 6 years 4 Japfa Comfeed Indonesia Tbk JPFA Distributed dividend continue 6 years 5 Lionmesh Prima Tbk LMSH Distributed dividend continue 6 years 6 Malindo Feedmil Tbk MAIN Distributed dividend continue 6 years 7 MERCK Tbk MERK Distributed dividend continue 6 years 8 Multi Bintang Indonesia Tbk MLBI Distributed dividend continue 6 years 9 Tjiwi Kimia Tbk TKIM Distributed dividend continue 6 years 10 Surya Toto Indonesia TOTO Distributed dividend continue 6 years

Source : data processed

The above considerations were made to produce a representative sample population of actual conditions. In addition, the processing of the data in this study using multiple regression analysis so that all data should be verified with the classic assumption test beforehand. Objective classic assumption test to produce a good regression model. To avoid errors in the classic assumption test, the number of samples used must be free from bias.

C. Collecting Sample Method

47 1. Type of data

For the purposes of this research data used are secondary data drawn from the financial statements, the Indonesian Capital Market Directory (ICMD) and Indonesian Central Securities Depository (KSEI) companies Included in Main Board Index and Development Index in Indonesia Stock Exchange. Advantages of secondary data is data availability, economical and quickly obtained while the disadvantage is not able to answer on the whole issue is being researched and less accuracy for data collected by others for specific purposes by an unknown method (Sarwono and Suhayati, 2010: 69)

2. Data Sources

Source of data obtained from the Indonesia Stock Exchange (BEI) during the study period 2009-2014. In addition, data obtained through the Indonesian Capital Market Directory (ICMD), Indonesian Central Securities Depository (KSEI) and through literature by reading and studying the book, Journal science and literature of literature that is closely connected with the object of research.

D. Methodology Data Analysis

48 1. Testing requirements analysis

This test is used as a requirement in the use of linear regression analysis model. In regression line, to ensure that the model is BLUE (Best Linear Unbiased Estimator) testing as follows:

a. Normality Test

Normality test to test the normal distribution of data, or the data is not normal, good data is normally distributed data, one of the easiest ways to see the residual normality is seen histogram graph that compares the observation data is approximately normally distributed. However, just by looking at the histogram it can be misleading, especially to the small sample size, it is to see the data that has met the test for normality is to use a normal probability plots comparing the cumulative distribution and normal distribution. The normal distribution will form a straight diagonal line and plotting the data residua will be compared with the diagonal lines. If the residual data distribution is normal, then the line that describes the actual data will follow the diagonal gari (Imam Ghozali, 2009: 147).

b. Test multicoloniarity

49 at the value tolerance ≤ 0.10 and his opponent variance inflation factor (VIF) ≥ 10 means that the data is no problem multikolonearitas.

c. Autocorrelation test

According to Imam Ghozali (2009: 99) autocorrelation test aims to test whether the linear regression model was no correlation between bullies error in period t with bullies error in period t-1 (previously). To test for the presence or absence of symptoms, the autocorrelation can be detected with the Durbin-Watson test (DW test). To determine whether there is autocorrelation, the following is a table of autocorrelation Durbin-Waston (Damodar Gujarati, 1995: 216).

Table 3.1 Durbin-Watson

Zero Hypothesis Decision If

No autocorrelation positive rejected 0 < dw < dl No autocorrelation positive No conclusion dl < dw <du No correlation negative rejected 4-dl < dw <4

no correlation negative Co conclusion 4-du < dw < 4-dl No autocorrelation, positive or

negative No autocorrelation

du < dw <4-du

d. Heterokestisity

50 Good data is homoskedastisitas are similarities and residual variance. Method for detecting the presence or absence of heteroscedasticity is to see the results of SPSS output through scatterplot graph between the predicted value variable (dependent) is ZPRED with residual SRESID. Detection of the presence or absence of heteroscedasticity can be done by looking at whether there is a specific pattern on a scatterplot graph between SRESID and ZPRED where the axis Y is predicted, and the X axis is the residual (prediction Y - Y in fact) that has been in studentized. Basic analysis:

1) If there is a specific pattern such as an existing point to form a certain regular pattern (wavy, widened and then narrowed), indicating there has been a heteroskedastisitas.

2) If there is no clear pattern, and the point spread above and below the number 0 on the Y axis, it does not happen heteroskedastisitas (Ghozali, 2009: 125).

2. Multiple analysis regressions

51 Y = a + b1X1 + b2X2 + b3X3 + b4X4 + b5X5 + b6X6 + b7X7 + b8X8 + b9X9 + e

MBX = DPR = a + b1CR + b2QR + b3DAR + b4DER + b5ROA + b6ROE + b7TATO

+ b9PER + e

DBX = DPR = a + b1CR + b2QR + b3DAR + b4DER + b5ROA + b6ROE + b7TATO

+ b9P/E + e

Description :

DPR = is the ratio between the dividend paid and the number of shares outstanding.

CR = ratio of current assets to current liabilities.

QR = ratio of current assets minus inventories to current liabilities.

DAR = The ratio of total debt to total assets.

DER = The ratio of total debt to total equity.

ROA = ratio of net profit after tax to total assets.

ROE = ratio between the net profit after tax to total equity.

TATO = The ratio between sales to total assets.

P / E = The ratio between the price per share to earnings per share.

a = a constant value.

b = koefisiean regression.

52 3. Simultaneously test (F test)

F test to prove whether the independent variable (X) simultaneously (together) have an influence on the dependent variable (Y). (Ghozali, 2006: 88). The formula is as follows:

Where R2= coefficient of regression.

N = number of samples

K = the number of independent variables

According Suliyanto (2001: 61) F count is used to test the accuracy of the model (goodness of fit). F test is also often referred to as a simultaneous test, to test whether the independent variables used in the model is able to explain changes in the value of the dependent variables or not. To conclude whether the model in the category of fit or not. Testing was done with the test-f at the 95% confidence level and an error rate analysis (a) 5% to the provisions of degree of freedom (DF1) = k-1 degree of freedom (DF2) = n - k. where n is the number of data, and k as the number of variables (independent variables and the dependent variable).

After acquired fhitung then inpresentation results apply to the following

provisions:

F = 2/

53 a. If the value of sig > 5% means h0 ha accepted and rejected, meaning all

independent variable has no significant effect on the variable dependent.

b. If the value of sig < 5% means h0 rejected and Ha accepted, meaning that all independent variables have a significant influence on the variable dependent.

Hypothesis used are as follows:

H0: β = 0, there is no significant effect simultaneously between the

independent variable on the dependent variable.

Ha: β = 0, there is a simultaneous significant influence between

independent variable on the dependent variable.

4. Test the partial significant (t-test)

t statistical test basically shows how far the influence of individual variables independent (explanatory) individually in explaining the dependent variable (Imam Ghozali, 2006: 88). The formula is as follows:

Where: r = coefficient of regression

n = number of data

54 After acquired thitung then inpresentation results apply to the following

provisions:

c. If the value of sig > 5% means h0 ha accepted and rejected, meaning

independent variable has no significant effect on the variable dependent.

d. If the value of sig < 5% means h0 rejected and Ha accepted, meaning

that the independent variables have a significant influence on the variable dependent.

According Suliyanto (2011: 55), t value is used to test the effect partially to the dependent. Whether or not the dependent variable. To find the value of t-table using the equation degree of freedom df : a, (nk) where n as the number of observations and k as the number of variables. Each variable is said to be significant if it has a value t count larger than t-table.

H0: β = 0 there are no partial significant influence between independent

variable to variable dependent.

Ha: β ≠ 0 no significant effect partially between the independent variables

on the dependent variable.

5. Test the coefficient of determination (adj R2)

The coefficient of determination (adj R2) essentially measures how far

55 one means of independent variables provide almost all the information needed to predict the variation of the dependent variable (Ghozali, 2009: 87).

E. Definition Variable Operational

1. The dependent variable Dividend Payout Ratio (DPR) A. Dividend

Cash dividend paid in cash by the company to each shareholder. At the time of the shareholders meeting of the company decided that a certain number of the company's profit will be shared in the form of cash dividend. The Company is only obligated to pay a dividend after the company announced it would pay a dividend. Dividend paid to shareholders whose names are registered in the register of shareholders. Here is the definition and formula of the dependent and independent variables according Warsono (2003), the dividend payout ratio is the annual cash dividend or the dividend divided by the annual earnings per share divided by earnings per share. To calculate the dividend payout ratio is used the following formula:

Companies with higher profit detention ratio generally have higher growth rates than firms with lower ratios detention.

DPR = � � ℎ

56 2. Variable independent

a. Current Ratio

Current ratio is a ratio to measure a company's ability to pay short-term obligations or debt immediately due at the time billed as a whole. In other words, how much assets are available to cover short-term liabilities that will mature soon. This manifest variables given symbol X1. Mathematically current ratio can be calculated by the formula:

The magnitude of the current ratio calculation results show the amount of current liabilities were secured by current assets. This means that the greater the current ratio, the higher the company's liquidity.

b. Quick Ratio (QR)

Quick Ratio shows the company's ability to meet or pay liabilities or current liabilities (short-term debt) with current assets without taking into account the value of the inventory (inventory, was given the manifest variable symbol X2, mathematically, quick ratio can be calculated by the formula

:

CR = � � � ��

57 The amount of calculation results quick ratio indicates the amount of current liabilities secured by current assets outside supplies. With characteristics that current assets outside supplies relatively easily melted, it guarantees the liquidity of the company with this indicator is more accountable. Thus, the higher the quick ratio, the safety factor for the company to meet its short term obligations will be higher.

c. Debt to Asset Ratio.

Debt to asset ratio is the ratio of debt that is used to measure the ratio between total debt by total assets. In other words, how much of the company's assets are financed by debt or how much debt the company influence on asset management. This manifest variables given symbols X3. According to Kashmir (2014: 156), the higher the debt ratio a company indicates that the capital structure, financial risk borne by the

holders of ordinary shares higher. The formula used to calculate the debt to asset ratio is;

d. Debt to Equity Ratio (DER)

Debit to equity ratio is a ratio used to assess the debt with equity. This manifest variables given symbol X4. The level of use of the debt of a company may be indicated by one of them using debt to equity ratio

58 (DER), which is the ratio of total debt to total capital high own. If DER indicates that the capital structure, financial risk borne by shareholders could be higher, In measuring Debt to equity ratio can be given by:

e. Return on Assets (ROA)

Return on assets is a ratio that shows the results (return) on the amount of assets used in the company or a measure of management effectiveness. This manifest variables given symbol X5. Kasmir (2014: 203) to measure return on assets can be calculated using the formula:

The smaller the ratio is, the less good, and vice versa. It means that this ratio is used to measure the effectiveness of the overall operation of the company.

f. Return on Equity (ROE)

Return on equity is a ratio that shows the results (return) on the amount of equity used in the company or a measure of the effectiveness of management in generating profits based on capital. This manifest

DER = �

59 variables given symbol X6. Kasmir (2014: 203) to measure return on assets can be calculated using the formula:

The smaller the ratio is, the less good, and vice versa. It means that this ratio is used to measure the effectiveness of the overall investment.

g. Total Assets Turn Over (TATO)

Is a ratio used to measure the ability of the company's assets in creating sales This manifest variables given symbol X7 to calculate the amount TATO use the following formula:

The amount of the calculation results in total asset turnover ratio shows the rate of speed throughout the company's assets into cash or receivables. The higher the entire asset turnover ratio, the more effective the company in utilizing all assets owned.

ROE = � �

60 h. Price Earning Ratio (PER)

Earnings per share is the price per share divided by cash flow per share, showing the amount of money paid by NII investor willing to every cash flow. By doing so, the price earnings ratio is the ratio between market price per share by its earnings per share. The formula used is: (Fahmi, 2014: 83)

61

CHAPTER IV

ANALYSIS

A. Scope of research

1. Indonesia Stock Exchange

Indonesia stock exchange was established in Jakarta on 14 December 1912. The Indonesian stock exchange was established long before Indonesia's independence by the government of the Dutch East Indies held by Vereniging Voord de Effectenhandel which at that time still called the Jakarta Stock Exchange. On the 11th of January 1925 stock exchanges opened in Surabaya and was followed by the opening of the stock exchange in Semarang on date 1 August 1925. The Jakarta Stock Exchange was first unveiled by President Suharto in 1977.

In 2007, the Jakarta Stock Exchange Surabaya stock exchanges merged to become Indonesia Stock Exchange. Step merger of Jakarta Stock Exchange with the stock exchange Surabaya is an effort to improve the efficiency of capital markets in order to compete with foreign exchanges.

62 shares is the stock price index. Indonesia stock exchange today have some kind of stock price index, namely:

a. Composite index (IHSG) b. LQ-45

c. Jakarta Islamic Index (JII) d. Kompas-100

e. Main Board and Development Board Index (MBX and DBX) f. Sector index

2. Main board and Development board index

Issuers listed on the Indonesia Stock Exchange is divided into two boards, namely the recording of Main Board and the Development Board in which the placement of the issuer and the issuer approved the recording based on the requirements of each recording on board recording.

a. Main board index

Main board is intended for issuers who has the size (size) is large and has a good track record. While the Development Board is intended for companies that cannot meet the requirements of the listing on the Main Board, including the company have a nice prospective However the not yet profitable, and is a means for companies who are in recovery.