THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY

The 2017/18 production forecast is unchanged at 10.9 million bags, which is a slight increase from the output in 2016/17. Reportedly, lowland Robusta production has not been as high as expected. As a result of strong overseas demand, green bean exports are forecast higher. Coffee and coffee products are among Indonesia’s leading agricultural exports to the U.S., averaging about $330 million annually.

Commodities:

Production

Indonesia’s coffee farming is low input with minimal management on holdings averaging less than 1 hectare per farmer. The lack of good agronomic practices leads to low productivity and causes large production swings as weather patterns vary. Reportedly, excessive rainfall in highland production areas negatively impacted production, while lowland areas had more favorable growing conditions. However, higher production in the lowland areas was not as high as expected, and could not compensate for the drop in the upland areas. Therefore, the 2017/18 production forecast is maintained at 10.9 million bags, Green Bean equivalent (GBE), a 300,000 bag increase compared to output in 2016/17.

Coffee production is 80-90 percent Robusta and mostly grown in Southern Sumatera. Meanwhile, most Arabica is grown in the mountainous areas of Northern Sumatera, with some also grown in Java and Sulawesi. Indonesia’s Arabica is marketed with denominations of origin to denote unique

characteristics.

Table 1. Indonesia Coffee Production Characteristics

Region Topography Key Production

Northern Sumatera Highland areas (>90 pct) Arabica Southern Sumatera Low (40 pct) and Highland (60 pct) Robusta

Java and others Low and Highland Arabica, Robusta

Source: industry contacts

Consumption

Coffee consumption is forecast to grow slightly to 3.29 million bags GBE in 2017/18, about 2 percent above 2016/17. Expansion in the number of coffee outlets, a leading trend in the local food service scene, is driving demand growth. In line with a growing middle class and rising incomes, more coffee outlets are opening in malls, airports, train stations, and office buildings. In addition, coffee chains are also expanding into smaller cities. The industry is making extensive use of social media and advertising to market to a growing consumer base. Demand for instant mixed coffee is also growing as these beverages are favored for their low prices and convenience.

Trade

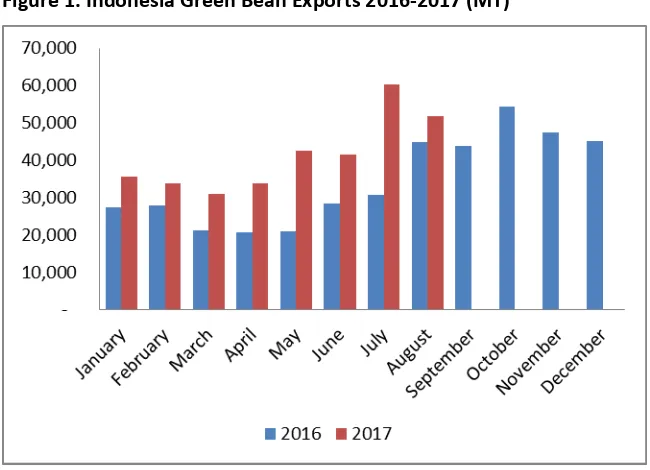

Due to the strong pace of exports in 2017, the forecast for green bean exports is raised to 7.45 million GBE in 2017/18. Shipments during January-August 2017 are 108,000 tons above the corresponding period in 2016 (See Figure 1). In 2017, the major destinations have been the United States, Germany, Malaysia, Russia, Italy, Japan, United Kingdom, Algeria, Egypt and China.

Imports are forecast at 730,000 GBE in MY 2017/18. Robusta bean imports from Vietnam are expected to be lower due to increased local production, while Arabica beans from Brazil are expected to increase slightly due to increasing domestics demand for specialty coffee.

Figure 1. Indonesia Green Bean Exports 2016-2017 (MT)

Production, Supply and Demand Statistics

Coffee, Green 2015/2016 2016/2017 2017/2018 Market Begin Year Apr-15 Apr-16 Apr-17

Indonesia USDA

Total Production 12,100 12,100 10,600 10,600 10,900 10,900

Bean Imports 311 311 320 342 300 340

Total Distribution 13,117 13,117 11,404 11,389 11,649 11,642

- - - -

(1000 HA) ,(MILLION TREES) ,(1000 60 KG BAGS)