“To be recognized, domesically and internaionally, as a credible bank through the strength of our values and achievement of low, stable rates of inlaion.”

“To achieve and maintain price stability by maintaining monetary stability and by promoing inancial system stability for Indonesia’s long term sustainable development.”

“Competence, Accountability, Integrity, Cohesiveness, Transparency.”

VISION

MISSION

“As an open economy, Indonesia is obviously in no posiion to isolate itself from the fallout of slowing global economic acivity. Nevertheless, in relaive terms, Indonesia’s overall posiion is not as precarious as for other countries. Alongside this, fundamentals in the external, iscal and banking sectors are sill adequately strong to withstand the fallout from the global crisis ...”

CONTENTS

CHAPTER I

CHAPTER II

CHAPTER III

Performance of the Indonesian Economy, Outlook and Policy Direcion

1

Economic Integraion and the Challenges of the Global Crisis

81

Exploring the Outlook for Global Economic Recovery

53

Contents

iv

Tables and Charts

vi

Board of Governors of Bank Indonesia

xi

Foreword

xii

Overview

xiv

1.1 Condiion of the Economy

4

1.2 Economic Outlook and Policy Direcion

34

Box: Evaluaing Achievement of the Inlaion Target

47

Box: Indonesia’s External Debt and Repayment Plan for 200949

2.1 Introducion

56

2.2 The Financial Crisis and Resuling Impact

61

2.3 Global Policy Role in Resoluion of the 2008 Crisis

67

2.4 Outlook for Global Economic Recovery

74

Box: The Fall of Lehman Brothers

76

Box: Credit Default Swaps (CDS): Mechanism and Development

78

3.1 Introducion

84

3.2 Flows of internaional Trade

86

3.3 Integraion of Capital Flows

93

CHAPTER IV

CHAPTER V

Policy Response of Bank Indonesia137

Domesic Financial Sector Performance amid the Ongoing Global Crisis

105

Appendices

159

4.1 Domesic Financial System:Resilience and its Role in

Financing the Economy

108

4.2 Payment System

126

Box: Knowing the Structured Products

133

5.1 Monetary Policy

140

5.2 Banking Policy

148

5.3 Payment System Policy

152

5.4 Coordinaion of Monetary, Fiscal, and Real Secor Policies

155

List of Bank Indonesia Regulaions in 2008

160

Various Important Regulaions and Policies in Economic and

Finance Areas in 2008

163

Staisics Table

169

Abbreviaions

199

Editorial Team

204

TABLES AND CHARTS

TABLES

TABLES

TABLES

Chapter I. Performance of the Indonesian Economy, Outlook and Policy Direcion

Chapter III. Economic Integraion and the Challenges of the Global Crisis Chapter II. Exploring the Outlook for Global Economic Recovery

Table 1.1. GDP Growth and Distribuion by Expenditures

7

Table 1.2. GDP Growth and Distribuion by Sector

9

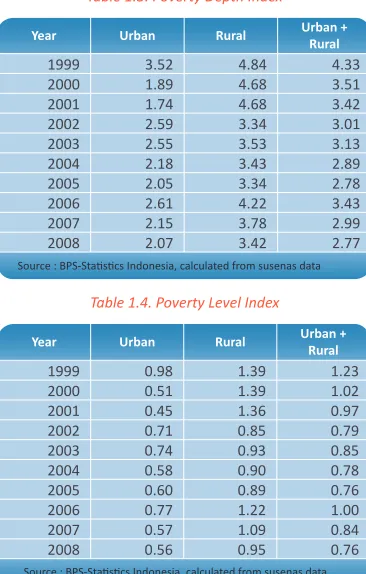

Table 1.3. Poverty Depth Index

12

Table 1.4. Poverty Level Index

12

Table 1.5. Employed Populaion and Unemployment Rate by Region

14

Table 1.6. Rural Poverty Rate

15

Table 1.7. Indonesia’s Balance of Payment

16

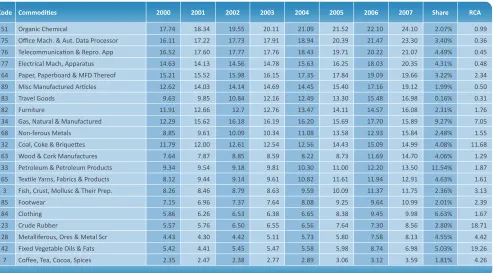

Table 1.8. Non-Oil and Gas Main Exports Commodiies

17

Table 1.9. Oil and Gas Exports Imports

18

Table 1.10. Indicators of BOP

19

Table 1.11. Indonesia’s Outstanding Foreign Debts

19

Table 1.12. Indonesia’s Foreign Debts Withdrawal

20

Table 1.13. Foreign Debts Repayment

21

Table 1.14. Inlaion and Its Contribuion by Categories

25

Table 1.15. Core and Non-Core Inlaion and Its Contribuion

25

Table 1.16. The Impact of First and Second Round Fuel Price Hike

26

Table 1.17. Administered Commodiies Contribuion to Inlaion

in 2008

26

Table 1.18. Volaile Food Commodiies Contribuion to Inlaion

in 2008

26

Table 1.19. Increase in Internaional Commodity Prices and Related

Domesic Commodity Prices

27

Table 1.20. Economic Growth Outlook by Expenditures

36

Table 1.21. Economic Growth Outlook by Sector

38

Table 1.22. Balance of Payments Outlook

41

Table 1.23. Government Foreign Debt Withdrawal Plan for 2009

43

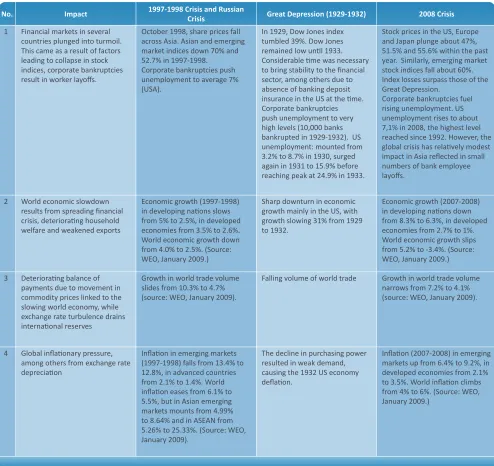

Table 2.1. Comparison of the Impact of Global Crisis in 2008

with Previous Crisis

64

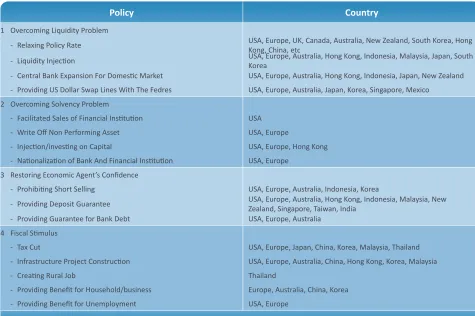

Table 2.2. Summary of Policy to Overcome Crisis in 2008

70

Table 2.3. World + G3 Economic Growth Outlook

75

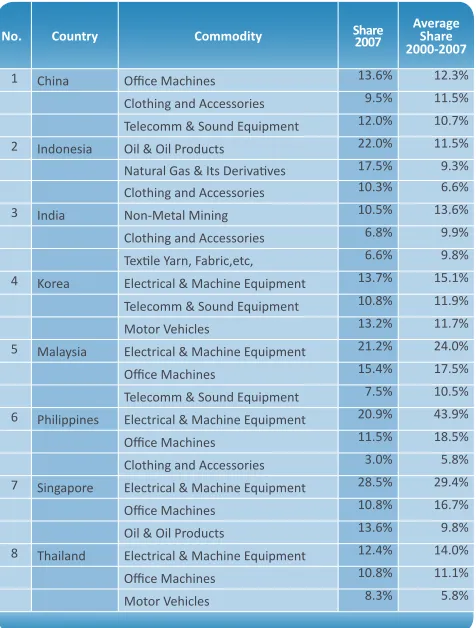

Table 3.1. Exports Share by Sector

86

Table 3.2. Three Largest Contributor to Exports Commodiies in

Several Countries

87

Table 3.3. Exports Composiion by Desinaion Country

87

Table 3.4. Producivity of 20 Indonesia’s Major Exports

Commodiies

88

Table 3.5. Non-Oil and Gas Imports

90

Table 3.6. Capital Goods Imports

90

Table 3.7. Share of the Final Demand of the Imports Industry

91

Table 3.8. Imports Composiion by Country of Origin

91

Table 3.9. Three Largest Imports Contributor in Several Asian

Countries

92

Table 3.10. Comparison of Internaional Investment Posiion

94

Table 3.11. Japan’s FDI in Several Asian Countries

98

Table 3.12. Ranking of Infrastructure in Several Countries, GCI 2008

98

Table 3.13. FDI in Indonesia by Economic Sector

100

TABLES

TABLES

Chapter V. Policy Response of Bank IndonesiaChapter IV. Domesic Financial Sector Performance amid the Ongoing Global Crisis

Table 4.1. Indicators of Commercial Banks

110

Table 4.2. Banks Credits

110

Table 4.3. Deposits

111

Table 4.4. Sharia Banking Performance

113

Table 4.5. Composiion of Sharia Banking Deposits

114

Table 4.6. Sharia Financing

114

Table 4.7. Rural Banks Indicators

116

Table 4.8. Sharia Rural Banks Indicators

117

Table 4.9. MSMEs Credits

118

Table 4.10. Indicators of Finance Companies

123

Table 4.11. Average of Currency in Circulaion and Growth

in 2005-2008

127

Table 4.12. Cash Posiion and Raio to Ouflow

127

Table 4.13. Share of Currency in Circulaion

127

Table 4.14. Inlow/Ouflow and Neflow of Currency

128

Table 4.15. BI-RTGS Transacions by Type of Transacion

129

Tabel 5.1. Series of Measures on Improvement of Monetary Policy

Operaion

143

CHARTS

CHARTS

Chapter I. Performance of the Indonesian Economy, Outlook and Policy Direcion

Chapter II. Exploring the Outlook for Global Economic Recovery

Chart 1.1. Exports Growth by Region

8

Chart 1.2. Exports Share by Region

8

Chart 1.3. Capacity Uilizaion,(BTI-BPS)

9

Chart 1.4. Capacity Uilizaion (SKDU)

9

Chart 1.5. Company Sales and Inventory in Agriculture Sector

10

Chart 1.6. Company Sales and Inventory in Manufacturing Sector

10

Chart 1.7. Labor Use

11

Chart 1.9. Labor Force by Sector

11

Chart 1.8. Economic Growth and Open Unemployment Rate

11

Chart 1.10. Labor Producivity

11

Chart 1.11. Labor Force by Educaion Level

12

Chart 1.12. Farmers Term of Trade in Sumatera

13

Chart 1.13. Farmers Term of Trade in Kali-Sulampua

13

Chart 1.14. Inlaion by Region

15

Chart 1.15. Current Account

17

Chart 1.16. Commodity Price Index

18

Chart 1.17. Capital and Financial Account

18

Chart 1.18. Indonesia Debt Indicators

19

Chart 1.19. Comparison of Debt Service Raio

20

Chart 1.20. Comparison of Debt to GDP Raio

20

Chart 1.21. Internaional Reserve

21

Chart 1.22. Average Exchange Rate

22

Chart 1.23. Exchange Rate Volaility

22

Chart 1.24. Average Appreciaion (+)/Depreciaion (-) in 2008

compared to 2007

22

Chart 1.25. BoP and Exchange Rate

23

Chart 1.26. Credit Default Swap Rate

23

Chart 1.27. Household Fuel Contribuion to Inlaion

26

Chart 1.28. Rice Procurement by Bulog

27

Chart 1.29. Rice Inlaion

27

Chart 1.30. Consensus Forecast Inlaion Expectaion

28

Chart 1.31. Consumers Price Expectaion

28

Chart 1.32. Retailer Price Expectaion

28

Chart 1.33. Exchange Rate and Inlaion of Trading Partner Countries

28

Chart 1.34. WPI Import and Imported Commodiies CPI

29

Chart 1.35. M0 and Currency Growth

30

Chart 1.36. Credit Growth per Currency

30

Chart 1.37. Currency and Credit Growth

30

Chart 1.38. Growth of Private Demand Deposits and ICI

30

Chart 1.39. M1, M2, and Rupiah M2 Growth

31

Chart 1.40. Growth of Real Currency, M1, and M2

31

Chart 1.41. Stock of Banking Excess Liquidity

31

Chart 1.42. Liquidity Premium (JIBOR - OIS)

31

Chart 1.43. Premium Among Tenor

32

Chart 1.44. O/N PUAB and BI Rate

32

Chart 1.45. World Economic Growth

35

Chart 1.46. World Trade Volume

35

Chart 2.1. Internaional Oil Price

57

Chart 2.2. Non Commercial Contract in Oil Market

58

Diagram 2.1. Subprime Crisis Chronology

59

Chart 2.3. LIBOR Rate and T-Bills Spread

60

Chart 2.4. Stock Prices Indices in Europe, Japan, and USA

61

Chart 2.5. Stock Prices Indices in Asia, Emerging Markets,

and the World

62

Chart 2.6. World Economic Growth

62

Chart 2.7. USA’s Personal Income and Expenditures

62

Chart 2.8. Retail Sales in Europe

62

Chart 2.9. Unemployment Rate in USA

63

Chart 2.10. USA Economic Growth

63

Chart 2.11. Japan’s Export by Country of Desinaion

65

Chart 2.12. Asian Economic Growth

65

Chart 2.13. IMF Commodity Price Index

67

Chart 2.14. World Inlaion

68

Chart 2.15.CPI Inlaion in Developed Countries

68

Chart 2.16.Inlaion in Developing Countries

68

CHARTS

CHARTS

Chapter III. Economic Integraion and the Challenges of the Global Crisis

Chapter IV. Domesic Financial Sector Performance amid the Ongoing Global Crisis

Chart 3.1. Exports Value by Sector

86

Chart 3.2. Contribuion of Commodity to Exports Producivity

89

Chart 3.3. Major Commodiies Compeiion in the Internaional

Market

89

Chart 3.4. Imports Share : Oil & Gas and Non-Oil & Gas

89

Chart 3.5. Oil Trade Balance

90

Chart 3.6. Oil and Gas Trade Balance

90

Chart 3.7. Structure of Capital Inlow to Indonesia

93

Chart 3.8. Capital Inlow Composiion

93

Chart 3.9. Private and Public Porfolio Investment

94

Chart 3.10. Foreign Porfolio Composiion

94

Chart 3.11. Yield Comparison of Money Market in 2008

95

Chart 3.12. Yield Comparison of 5 Years Bonds in 2008

95

Chart 3.13. Yield Comparison of Stocks in 2008

95

Chart 3.14. Stocks Capitalizaion and Bonds/GDP

96

Chart 3.15. Depth of Stocks and Government Bonds Market

96

Chart 3.16. FDI Flows and Growth of Indonesia’s GDP

96

Chart 3.17. Net FDI and Poliical Risk

97

Chart 3.18. FDI Flows to Southeast Asia

97

Chart 3.19. FDI to GDP Raio in Several Countries

97

Chart 3.20. Transportaion, Communicaion, and FDI

99

Chart 3.21. Land, Water, and Air Transportaion

99

Chart 3.22. Foreign Investment in Indonesia (1997-2007)

99

Chart 4.1. Growth of Credits, Deposits and SBI

111

Chart 4.2. Growth of Deposits

112

Chart 4.3. Non Performing Loan (NPL)

112

Chart 4.4. Growth of Assets, Deposits, PYD, and FDR of Sharia

Banking

113

Chart 4.5. NPF of Sharia Banks

115

Chart 4.6. NPF by Sector

115

Chart 4.7. ICI and Net Foreign Buy

119

Chart 4.8. ICI and Regional Stock Exchange

119

Chart 4.9. IPO, Right Issue, and Stock Issuance Accumulaion

120

Chart 4.10. The Price of Government Bonds

120

Chart 4.11. Volume and Frequency of Government Bonds

Trading Aciviies

120

Chart 4.12. Government Bonds Holders

121

Chart 4.13. Corporate Bonds Issuance

122

Chart 4.14. NAV of Mutual Funds

122

Chart 4.15. Insurance Industry

123

Chart 4.16. Insurance Company Investment Porfolio

124

Chart 4.17. Pension Funds

124

Chart 4.18. Pension Funds Investment Porfolio

124

Chart 4.19. Currency in Circulaion in 2004-2008

126

Chart 4.20. Transacions of BI-RTGS

128

Chart 4.21. Transacions Aciviies by Group of Banks

129

Chart 4.22. Throughput BI-RTGS

130

Chart 4.23. Clearing Aciviies

130

Chart 4.24. Nominal Debit Clearing

130

Chart 4.25. Volume Debit Clearing

131

Chart 4.26. Based Account Card Aciviies

131

Chart 4.27. Credit Card Aciviies

131

Chart 4.28. Growth of Naional Credit Card’s NPL

131

Chart 4.29. Electronic Money

132

CHARTS

Chapter V. Policy Response of Bank IndonesiaSymbols, Reporing Period and Source of Data

Revised igures r

Provisional igures *

Incomplete igures **

Data are not yet available ...

Not available

-Figures in before and ater mark could not be compared X

Nil or less than the last digit

--United States Dollar $ (dollar)

All source of data is from Bank Indonesia, unless menioned otherwise Chart 5.1. Developing Countries Policy Rate

141

Chart 5.2. Credit Monthly Increase

142

Chart 5.3. Interest Rate and Volume of O/N PUAB

145

Chart 5.4. PUAB Rates

145

Chart 5.5. Deposits Interest Rate

146

Chart 5.6. Credits Interest Rate

146

Chart 5.7. Credits Growth

146

Chart 5.8. BI Rate and ICI

146

Chart 5.9. BI Rate and Government Bonds Yield

147

Chart 5.10. BI Rate and Consumer Conidence

147

BOEDIONO Governor

MIRANDA S. GOELTOM Senior Deputy Governor

HARTADI A. SARWONO Deputy Governor

SITI Ch. FADJRIJAH Deputy Governor

S. BUDI ROCHADI Deputy Governor

MULIAMAN D. HADAD Deputy Governor

BUDI MULYA Deputy Governor ARDHAYADI MITROATMODJO

Deputy Governor

BOARD OF GOVERNORS

Boediono

GovernorFOREWORD

The deepening of global inancial crisis is taking its toll in the world economy. The scale and

suddenness of the crises has let the world economy to shrink signiicantly, paricularly in the industrial countries. In Indonesia, the efects of global crisis started to take hold in the last quarter of 2008, with economic slowdown looming larger in 2009. Faced with the gloomy economic outlook, it is essenial that we assume heightened alertness while maintaining objecivity in assessing issues within their full scope. This is necessary so that we will be able to take acions that properly address the challenges we face.

As an open economy, Indonesia is obviously in no posiion to isolate itself from the fallout of slowing global economic acivity. Nevertheless, in relaive terms, Indonesia’s overall posiion is not as bad as for many other countries. Despite the downward pressure in Q4/2008, the Indonesian economy was sill able to manage 6.1% growth for 2008, buoyed by private consumpion and exports. Alongside this, fundamentals in the external, iscal and banking sectors were sill adequately strong to withstand the fallout from the global crisis.

With regard to the resilience of the banking system, the nature of our inancial system has aforded the domesic economy some protecion from the efects of the inancial crisis. Our inancial system, most of which, sill coninues to operate along convenional lines with comparaively simple instruments. Unlike in developed countries, intermediaion process in our inancial sector coninued to operate during

2008, despite potenial for slowing performance in 2009.

One lesson that we can learned from the current global crisis is the importance of the inancial system to go back to the basics. First, banks should concentrate on inancing aciviies with ideniiable underlying transacions and based on clear risk calculaions. Second, the basic principles of convenional macro management are proven to be relevant in confroning the crisis. With regard to management of macroeconomy, domesic sector in Indonesia is demonstrably capable of generaing economic momentum amid the global crisis.

Looking forward, the Indonesian economy in 2009 is forecasted to grow around 4%, with considerable downside risk, should global economic recovery proceed more slowly than expected. Besides this, ight availability of inancing in domesic economy also poses a risk that must be taken into account.

Jakarta, March 2009

Boediono

Bank Indonesia and the Government will strengthen coordinaion to safeguard macroeconomic stability and to secure public purchasing power through policy measures, so as to prevent a sharp slowdown of domesic economy. We also hope that the economic growth will remain broadly distributed and bring beneits to the public at large.

The global economic crisis has changed the shape of the world economy. The crisis that began in the United States in 2007 spread worldwide, with no excepion to developing countries. Several aggresive policies have been adopted at the global level to promote economic recovery. In the United States, the epicentre of the crisis, the resolve of the new administraion in taking bold acions to stem the crisis is a posiive factor that could miigate pessimism over the likelihood of prolonged economic recession and risks of depression. At the same ime, the willingness of other industrial

countriescountries to coordinate their economic

recovery policies is also expected to bolster market conidence. However, the ongoing deleveraging process among inancial insituions and the impact of the crisis from the real sector back to the inancial sector, means that global markets remain beset by heightened risk and uncertainies.

In Indonesia, the fallout from the crisis began to take hold towards the end of 2008. In Q3/2008, the economy was sill charing above 6% growth with coninued healthy performance in the inancial sector relected in a stable exchange rate, mouning stock index and declining yield on Government Securiies. However, in Q4/2008, the global inancial turbulence began to bear down on the Indonesian economy. Weakening exports, pressure on the balance of payments and turmoil on the money market took their toll on Indonesia’s economic growth. On the external side, the balance of payments began to accumulate a rising deicit and the exchange rate underwent signiicant depreciaion. On inancial markets, global liquidity condiions ightened up in tandem with mouning percepions of emerging market risks. This in turn triggered a slide in the Indonesian Stock Market, and Government Securiies prices alongside a sharp

Maintaining Economic Stability

During the Global Financial Crisis

1997 2008

GDP 4.7% 6.1%

Inlaion 11.05% 11.06%

External

- Current Account (% of GDP) -2.3% 0.1%

- Internaional Reserve

(billions of USD) 21.4 51.6

(Month of Imports and Oicial Foreign Debt Repayment) 5.5 4.0

-Foreign Debt (% of GDP) 62.2% 29.0%

Fiscal

- Fiscal Balance (% PDB) 2.2% 0.1%

- Public Debt (% PDB) 62.2% 32%

Banking

- LDR (%) 111.1% 77.2%

- CAR (%) 9.19% 16.2%

- NPL (%) 8.15% 3.8%

Table 1. Indonesia Macroeconomic Condiion: Asian Crisis (1997) and Global Crisis (2008)

downturn in the exchange the causing the risk spread on Indonesian securiies widened considerably, promping ouflows of foreign capital from the stock market and from Government Securiies and Bank Indonesia Ceriicates (SBIs).

In relaive terms, Indonesia’s overall posiion is not as precarious as for many other countries. The Indonesian economy was sill able to chart 6.1% growth in 2008. Indonesia’s fundamentals in the external sector, iscal sector and banking industry are also quite strongly posiioned to weather the global crisis (Table 1). However, the crisis will have more pronounced efects on the Indonesian economy. The increasing integraion of the global economy and the deepening of the crisis augurs for the slowing of economies across all countries during 2009. Indonesia is no excepion. Bank Indonesia projects a drop in economic growth in 2009 to around 4.0% with downside risk if the global economic downturn is greater than predicted. The more modest growth in Indonesia cannot be regarded as bad when compared to the many other countries forecasted to record negaive growth. For these reasons, acions by the Government and Bank Indonesia, employing iscal, monetary and real sector policies to contain the impact of the crisis, will be vital and essenial during 2009.

Indonesian’s Economy in 2008

During 2008, Indonesian’s economy maintained adequate performance amid the global turmoil. Overall economic growth reached 6.1% in 2008, slightly below the 6.3% recorded in the previous year. This growth was driven by private consumpion and exports. The high consumpion growth during 2008 was supported by coninued strong purchasing power and improving levels of consumer conidence. Factors bolstering public purchasing power include rising incomes from the surge in export commodity prices, higher income levels for middle and upper income earners and the government safety net policy in the form

of Direct Cash Transfers to compensate for the impact of

the fuel price hike midway through the year.

Investment expanded by 11.7% during 2008 as a whole, ahead of investment growth one year earlier. Investment began to slow in Q4/2008 in response to weakening domesic demand and plunging external demand. In disaggregaion by investment component, the primary contribuion to growth in 2008 came from non-construcion investment. However, construcion investment slowed in comparison to the preceding year.

Government investment was also lower in 2008, due to the low rate of realised government capital expenditures.

Externally, despite the slowing growth in the global economy, Indonesia’s exports sill managed 9.5% growth from the preceding year. The high rate of export growth was contributed by soaring world oil prices in the irst half of 2008, followed by surging prices for exported agricultural and mining commodiies. Further support came with high export demand from China and India, ofseing the slowing growth in major trading partners such as the United States and Europe. Growth in non-oil and gas exports, like before, was bolstered by primary commodiies led by agricultural products such as palm oil and mining products, among others coal. Imports grew by 10.03%, ahead of the preceding year, due to the growing need for raw materials and capital goods to meet demand for exports and domesic consumpion. This trend was especially noiceable in the iniial quarters of 2008.

On the supply side, all economic sectors in Indonesia managed stable growth in 2008. Manufacturing, trade, hotels and restaurants sector and agriculture again accounted for the largest share of economic growth. However, analysed by contribuion, the most important sources of growth were trade, hotels and restaurants sector, transport and communicaions and the

manufacturing sector. In Q4/2008, the economy began to slow in all sectors, with the tradable sectors worst afected due to the fall in world demand.

Unil mid-2008, economic growth in Indonesia was sill contribuing to the labour market. However, early in the second half and especially in Q4/2008, the deepening global crisis bore down on the labour market in Indonesia. During the irst half of the year, open unemployment was in decline. Key to this was the performance of the agriculture sector, one the most important sources of employment. Workers were also absorbed into all business sectors, such as public services, trade and the transport and communicaions sector. Early in Q4/2008, pressure from the global crisis compelled several companies to make changes to their operaions and upgrade business eiciency, with the result that some factories closed. These changes led to a rise in planned worker layofs at some companies.

internaional commodity prices had a posiive efect on export growth. Alongside this, robust domesic demand spurred vigorous growth in imports of capital goods, raw materials and even consumpion items. Sharply rising imports shited the current account into deicit in Q2/2008. At the same ime, the capital and inancial account and paricularly porfolio investments coninued to chart a surplus. The capital account surplus was buoyed by the issue of global bonds and foreign capital inlows, especially on the Government Bond market, which saw signiicantly increased acivity in Q2/2008.

Early in the second half of 2008, pressure on the balance of payments mounted from the deepening world economic crisis. Within the current account, exports began tapering of in response to falling commodity prices. Similarly, the capital and inancial account was impacted by diminishing investor interest in the domesic inancial market. Foreign investors pulled out their capital in light to quality exacerbated by deleveraging as inancial insituions struggled to clean up balance sheets amid the growing intensity of the global crisis.

The brisk exodus of foreign capital, especially on the markets for Government Securiies and Bank Indonesia Ceriicates (SBIs), resulted in a porfolio investment deicit in Q3/2008 that widened further in Q4/2008. The combined deicits in the current account and the capital and inancial account contributed to a surging balance of payments deicit in the inal quarter of the year. Measured for 2008 overall, the esimated balance of payments deicit came to USD2.2 billion. At end-December 2008, internaional reserves stood at USD51.6 billion. This represented a comfortable level of reserves, equivalent to 4.0 months of imports and servicing of oicial debt. The various dynamics in the global economy and balance of payments have inluenced movement in the rupiah exchange rate. For the most part, the rupiah maintained relaive stability unil mid-September 2008. Key to this was the performance of the current account, which coninued to chart a surplus, as well as prudent macroeconomic policy. However, ater mid-September 2008, the deterioraing global crisis put pressure on the rupiah. The crisis triggered a global liquidity crunch and fuelled percepions of risk on emerging markets, including Indonesia, while generaing negaive inancial market seniment. These factors prompted foreign investors to oload signiicant amounts of rupiah assets. Pressure mounted on the rupiah from early Q4/2008, causing the rupiah to fall 15.5%. However, looking at 2008 overall, the

average value of the rupiah was fall only 5.4% at Rp 9,666 to the US dollar.

Concerning prices, inlaionary pressure in Indonesia remained strong unil Q3/2008, but began to ease in Q4/2008. The high inlaion unil Q3/2008 was fuelled primarily by soaring internaional commodity prices, led by oil and food. This upswing impacted administered prices when the government was compelled to raise its prices for subsidised fuels. Early in the second half of 2008, inlaionary pressure began to subside in line with the downturn in internaional commodity, food and energy prices. Following this, the Government acted to reduce prices for automoive diesel and gasoline in December 2008. In other developments, Indonesia beneited from a very good year of food crop producion which, combined with slowing aggregate demand, contributed to lower inlaionary pressure. In regard to fundamentals, falling inlaionary pressure was also atributable to success in miigaing expectaions of inlaion that had mounted sharply in the wake of the fuel price hike. Taken together, CPI inlaion in 2008 came to 11.06%, with core inlaion recorded at 8.29%.

Bank Indonesia Policy Response

In 2008, the Indonesian economy came under the inluence of events in the global economy. From the irst half to the third quarter of 2008, rising internaional commodity prices and mouning pressure from aggregate demand fuelled high inlaionary pressure. However, during Q3/2008, growth contracted in advanced countries, seing of a slowdown in the global economy. As the year entered the fourth quarter, internaional commodity prices began climbing down alongside slowing aggregate demand.

Responding to the the events in 2008, Bank Indonesia has adopted a range of policy acions adjusted to these developments in order to control inlaion and bolster sustainable economic growth in the medium-term (Chapter V).

was expanding vigorously at 36.3% (yoy). The rate of credit expansion was well ahead of the growth in bank depositor funds recorded at only 14.3% (yoy).

To curb the mouning inlaionary pressure, Bank Indonesia progressively raised the BI Rate from 8% in May 2008 to 9.5% in October 2008. This monetary policy stance kept public inlaion expectaions from climbing further and eased the downward pressure on the balance of payments.

Following this, in early Q4/2008, Bank Indonesia predicted a declining inlaionary pressure in the wake of falling world commodity prices and slowing aggregate demand as a result of the global economic crisis. Thus in December 2008, the BI Rate was lowered a further 25 bps.

In the banking sector, Bank Indonesia policy has focused primarily on strengthening the resilience of the banking system, paricularly in preparaion for implementaion of Basel II. This banking policy includes expansion of the service capacity of the sharia-compliant banking industry.

However, in the second half of 2008 as pressure mounted from the global crisis, banking policy shited to measures to miigate risk of fallout from the global crisis on the domesic banking system. Due to pressure from the global crisis, liquidity became scarce on global and domesic inancial markets. Several policies were introduced in response. Among the most important was increased access for commercial banks and rural banks to funding faciliies in order to cope with the liquidity crunch.

Bank Indonesia has taken these acions while keeping close atenion to risks in the domesic banking system and broader impact on the grassroots economy of society. Therefore, measures to ensure availability of funding for the Micro, Small and Medium Enterprise (MSME) sector, an important bufer for the grassroots economy, will also be monitored closely. This MSME lending plays a vital role for grassroots communiies in enabling them to hold on and grow their businesses during diicult imes, such as now in 2009.

In this regard, Bank Indonesia has issued regulatory provisions to allow banks greater room in managing their lending without sacriicing prudenial banking and overall economic stability. These regulaions encompass the following: extension of the transiion period for Basel II implementaion in calculaion of capital charges for operaional risk, simpliicaion in opening of bank oices,

including sharia-compliant oices, adjustment in the risk weighted average assets (ATMR) for SMEs beneiing from loan guarantee schemes, changes in assessment of credit within certain ceilings, USD repurchase agreement (repo) facility for banks with Bank Indonesia and reducions in the required loan loss provision (PPAP).

These regulaions will then be followed by regulatory measures at an intense level to improve banking transparency, strengthen liquidity risk management and regulate banking industry derivaive products. Under this policy, all banking industry agents, including convenional and sharia-compliant commercial banks, will have adequate space for operaing the intermediaion funcion while maintaining a high priority on banking prudence and risk management.

Within the payment system, Bank Indonesia will do its part to ensure that the global inancial crisis does not disrupt the naional payment system. To prevent systemic risk and risk of counterparty default, which tends to mount under crisis condiions, and to safeguard the smooth operaion of payments, Bank Indonesia has introduced changes in the payment system setlement schedule on certain days. Payment system setlement will operate ater calculaing the required funds for the Short-Term Funding Facility (FPJP), if any banks have applied for FPJP on that day. Even with this added step, setlement will sill be completed on the same day. This measure is intended to provide an extra measure of ime for members in the systemic bank category and experiencing short-term funding mismatch to setle their obligaions at end of day.

In the payment system, the general policy of Bank Indonesia is to improve currency circulaion in terms of speed, eiciency, security and reliability, strengthen front-line cash services and improve the quality of currency. In non-cash payments, policy is directed at miigaion of payment system risks, oversight of the payment system, improved discipline in use of cheques and clearing payment orders (bilyet giro), regulaion of money

remitances, eiciency improvements in the management of government accounts and promoion of non-cash payments.

Extent of the Crisis and Outlook for Global Economic Recovery

Bank Indonesia and economic actors in responding to the dynamics of the global economy (Chapter (II). The global economic recovery process is likely to have major bearing on the Indonesian economy in 2009. Within this context, an assessment of the outlook for global economic recovery is essenial.

The world economy is now in the depths of the most severe global economic crisis since the depression of 1929. The various measures taken to cope with the present crisis of 2009 comprise the leading agenda for policy makers and economic actors around the world.

The current global inancial crisis is not the irst that has struck the world. Economic crises and inancial instability have come and gone throughout history. The changing characterisics of crisis over ime have resulted in diferent impacts on the global economy. In recent years, global inancial markets have been marked by a phenomenon of global excess liquidity, soaring oil prices and the proliferaion of inancial innovaions relected in the carry trade, securiisaion and leveraging acivity by inancial insituions. These events have stretched the global inancial system to the limit. The emergence of these inancial innovaions also led to increased moral hazard, in paricular from the percepion of “too big to fall” in the case of US inancial products. Also supporing this were stellar raings issued even for subprime mortgage-based products. The collapse in property prices followed by falling prices for subprime mortgage-based securiies in the United States ulimately rocked the US inancial market to its foundaions. This crisis, taking place within an integrated global economy, then muliplied and spread throughout the world.

Having learned from the failures in dealing with the Great Depression during the 1930’s that led to a very slow recovery, some countries have taken aggressive measures. Governments around the world have launched iscal simulus packages to provide a boost to weakening economies. Central banks in various countries have joined together in pumping liquidity into economies at unprecedented levels. These acions were taken to prevent a downward spiral that would devastate the inancial sector and real sector.

In the inancial sector, government of various countries have taken acion to rescue their economies through a range of intervenions, including blanket guarantees for bank deposits, underwriing or takeover of toxic assets,

capital injecion in inancial insituions or even takeover of those insituions.

Although these acions have not been suicient to resolve all the emerging problems, the aggressive policies also ofer some light at the end of the tunnel. If these policies can be properly implemented and operate in a consistent

manner, there is greater hope for a turnaround in the

world economy in Q4/2009. If this happens, the current global crisis will not slide into a depression such as sufered during the 1930’s.

Integraion of the Indonesian Economy amid the Challenges of the Global Crisis

For the Indonesian economy, the current global crisis is a lesson on the consequences of the growing integraion of Indonesia into the global economy (Chapter III). Analysed by trade, Indonesia has become progressively more integrated into the global economy in recent years. This is relected in the raio of exports and imports to GDP, which has climbed sharply since 1980. This integraion has also been accompanied by diversiicaion of export desicountries and commodiies.

On the inancial side, the Indonesian economy is one of the most open in ASEAN, ranking ater Singapore. Relecing this is the expanding share of Net Foreign

Assets or even Foreign Direct Investment to GDP, in

addiion to foreign holdings in various investment

instruments. Even so, inlows coninue to be dominated by porfolio capital, rendering Indonesia suscepible to capital reversal due to the very sensiive nature of these funds to seniment. Furthermore, the majority of FDI lowing into Indonesia is not export oriented, for the reason that Indonesia has not become part of the supply chain in the global economy,

On one hand, the economic integraion has generated added dynamism and provided many beneits for the Indonesian economy. The other side to this, however, is that economic integraion also carries the risk of instability, as can be seen during a ime of global crisis.

Concerning beneits, economic integraion will bring greater prosperity through increased movement of goods and capital among the countries involved. The movement of goods through internaional trade has raised the general levels of prosperity in needy countries. At the same ime, movement of capital will bring

to the most producive venues of economic acivity. Financial globalisaion is also seen as assising a country in minimising domesic economic luctuaions. Access to ofshore funds can be used to accelerate growth in aggregate demand during imes of limited availability of domesic inancing.

The integraion of foreign capital inlows has also simulated expansion in the domesic inancial sector through increased market liquidity. For this reason, increased integraion of the inancial sector is seen as key to applying market discipline on decision makers, introducing inancial product innovaions, promoing technological advancement, and promoing the compeiion that will strengthen eiciency within the naional banking industry.

The downside is that economic integraion also carries risk of instability. The beneits of inancial liberalisaion have been eroded by asymmetric informaion and distorions in the global and domesic economy. The reality is that lows of informaion on inancial markets are imperfect in both transparency and integrity. This has led to problems in regard to incenives, such as moral hazard and adverse selecion. As a result, investors tend to herding, taking

their cues from other investors perceived to possess

beter quality informaion.

The global inancial crisis triggered by the subprime mortgage failures is an example of the vulnerability of inancial liberalisaion. The crisis, having spread to many countries, has now led to highly volaile movements of capital. The global crisis has forced corporaions, inancial insituions and households in developed countries to clean up their balance sheets, among others by pulling porfolio capital back to their home countries. The porfolio capital that once poured into Indonesia has suddenly been pulled out in signiicant volume, puing pressure on the balance of payments and driving down the value of the rupiah. Nevertheless, the capital reversal from emerging market countries, including Indonesia, has now eased.

The various recovery acions pursued by advanced countries are expected to halt the downward spiral in economic acivity. When normality in lending can be restored in advanced countries, inlows into emerging markets, including Indonesia, are also forecasted to recover progressively to normal. Accordingly, the

Indonesian economy needs to posiion itself to retain the image of a secure, comfortable environment for business

and investment. It is important to maintain joint eforts to reassure investors of the quality and prudence of Indonesia’s macroeconomic management. In addiion, to promote longer-term capital lows, improvement of the investment climate remains a priority.

Indonesian Economic Outlook for 2009

As an open economy, Indonesia is inevitably impacted by the fallout from the ongoing global crisis. This is the natural consequence of the growing integraion of Indonesia into the world economy. In 2009, the world economy is predicted to head towards a deeper recession, and this will naturally inluence the dynamics of the Indonesian economy. However, the various acions taken by some countries to move forward with aggressive iscal and monetary simulus are expected to keep the world economy from sliding into depression.

To this end, common eforts by the government and other naional stakeholders to minimise shocks to the Indonesian economy during 2009 will be vitally important. Also necessary are sustained acions to build macroeconomic resilience, improve compeiiveness and bolster the sources of domesic economic resilience.

In the global banking sector, the recapitalisaion process in some countries will also take considerable ime and require enormous injecions of capital. At the end of 2008, recapitalisaion in the global banking system had reached a total of 890 billion US dollars. This igure for the cost of the crisis only takes account of losses from the inancial crisis ater 2007. The second round efects on the banking system from deterioraion in world business from recession have not been fully assessed. Accordingly, the world economy sill faces serious issues and diiculies in mouning a quick recovery in 2009.

In assessing these global developments and the capacity of the domesic economy, Indonesia is predicted to chart signiicantly reduced growth in 2009. Economic growth will reach around 4.0%, due to falling exports that will in turn impact consumpion and investment. Nevertheless, this forecast sill carries signiicant downside risk, especially if the global economic recovery advances more slowly than expected. On the domesic front, constraints on bank inancing also pose a risk that must be monitored carefully.

supporing economic growth. During 2009, economic growth in Indonesia will be driven primarily by domesic demand and especially household consumpion. Despite predicions of slowing, household consumpion is sill expected to show resilience, paricularly in view of the government plans for an added iscal simulus in 2009. Furthermore, Government plans for earlier realisaion of the simulus, civil servant pay rises, the elecion year and increases in provincial minimum wage levels are also predicted to foster increased household consumpion.

Unabated external turbulence means that further

pressure is predicted to bear down on Indonesia’s balance of payments, despite a levelling trend. Falling exports on one hand will be ofset by less vigorous imports, result of weakening aggregate demand. This in turn may bring improvement to the current account during 2009.

Concerning the capital and inancial account, the persistent global liquidity crunch and sill strong

percepions of emerging market risk, combined with the added sale of US treasury bills to inance the enlarged iscal simulus, mean that capital inlows will fall short of opimum levels. Nevertheless, the pressure of capital ouflows from Indonesia is predicted to ease in 2009. Government capital lows are also expected to improve in view of plans to issue foreign currency bonds, foreign currency Islamic bonds (sukuk), draw down external borrowings and draw on standby loans.

While external pressure is mouning, the downward trend in internaional commodity prices has eased domesic inlaion. The decline in commodity prices has

created room for the Government to reduce prices for

automoive diesel and gasoline. In addiion, government eforts to ensure adequate supplies of foodstufs through the dry season helped stabilise food prices and bring down volaile foods inlaion. This in turn has assisted in lowering public expectaions of inlaion.

Through these developments, CPI inlaion in 2009 is forecasted to maintain a declining trend to 5.0%-7.0%. Looking forward, Bank Indonesia will monitor potenial inlaionary pressure from the exchange rate in order to keep future inlaion on track with the medium and long-term inlaion target.

In 2009, Indonesia’s banking industry faces the twin challenges of slowing domesic economic growth and prolonged ight liquidity on the global market. Nevertheless, the overall banking industry will sill retain

considerable resilience, as relected in the CAR and NPL key banking indicators (Chapter IV). In 2009, the capital adequacy raio (CAR) is expected to remain high, above the 8% regulatory minimum. With capital adequacy in good shape, the domesic banking industry also has ample

funding sources from depositor funds and other resources

to support exports and promote economic growth.

Based on the current strength of capital, credit growth in Indonesia is predicted to hold in the 15%-18% range during 2009, in contrast the faltering credit expansion in

advanced countries such as the European Union and the

United States in 2008 and possible negaive credit growth in 2009. This credit expansion will be targeted a high performing sectors with low risk, such as MSMEs, while maintaining prudence to ensure that NPLs remain within safe limits.

Risks, Challenges and Bank Indonesia Policy Direcion

Risks for the Indonesian Economy

a. Further slowing in the global economy

A major risk for the Indonesian economy is the possibility of the global economic slowdown moving beyond projecions . Various indicators show that the global recession will last throughout 2009. The impact of this prolonged recession will be felt in the weakening of the Indonesian economy as a whole. This will pose challenges for acions aimed at haling the economy from steeper decline.

Some advanced countries are expected to maintain negaive growth, while more and more emerging

economies are likely to sufer from the impact of the crisis. This will erode Indonesian exports even further, puing added pressure on the current account.

The current adverse condiion of the global economy also increases the risk of protecionist policies in various countries aimed at protecing their domesic economies and prevening increased unemployment, while also keeping out foreign goods. The risk of this protecionism will lead to deterioraing volume of world trade, which in turn may prolong the global crisis.

b. Stability of the banking industry

interbank market. If this situaion is allowed to persist, liquidity will not be evenly distributed within the banking system even though aggregate banking liquidity remains suicient. Added to this, the potenial for rising non-performing loans during the economic downturn in Indonesia means that domesic banks must take acion to raise capital. This portends to constrain available liquidity on the market.

c. Fiscal Financing

The counter-cyclical policies pursued by the government through a range of acions, such as the iscal simulus, will in turn require inancing. Under the present condiion of the global economy, there is steadily diminishing room to raise iscal inancing on either the internaional or domesic inancial markets. At this ime, the space for raising funds on the global inancial market is ight. If these inancing issues cannot be properly resolved, pressure could bear down on the balance of payments and this in turn would pose even more severe diiculies for economic recovery.

Future Challenges for the Economy

a. Resolving external imbalances

The global economic crisis has inluenced the domesic

economy primarily through the external channel. The source of vulnerability and direct impact from the crisis lies in the pressure on Indonesia’s balance of payments. The lagging global economy has depressed demand, which in turn has hit exports. In 2009, the current account is forecasted to run a deicit at about 0.53% of GDP due to deterioraing export performance, while imports will decline but not at the same rate. The impact on the balance of payments from the global crisis will bear down mainly on the capital and inancial account. With the processes of deleveraging and global bank recapitalisaion expected to last a considerable ime and demand vast quaniies of capital, global liquidity is forecasted to remain ight. Only very limited capital inlows on the domesic inancial market are therefore expected.

External imbalances emerging from the pressure on Indonesia’s balance of payments pose a challenge for the Indonesian economy in 2009. In regard to the capital and inancial account, the ongoing global liquidity crunch may add to the diiculies of raising external inancing. Furthermore, limited supply of foreign currency on the domesic market under the present condiions of ight

global liquidity will exacerbate risk in the rupiah exchange rate.

In responding to these various pressures, Bank Indonesia will keep a close watch on developments in the rupiah over ime. To prevent excessive pressure on the rupiah exchange rate, during 2008 Bank Indonesia pursued a serious of measure involving the restructuring of forex trading acivity. This move was crucially important in minimising foreign currency speculaion.

For the most part, the regulaion of customer purchases of foreign currency from banks has help curb speculaive transacions. Nevertheless, Bank Indonesia envisages improvements to opimise and strengthen eiciency in ongoing policies.

To cope with these issues, Bank Indonesia will opimise policy further to minimise uncertainty over movement in the exchange rate. In addiion, Bank Indonesia has taken further acion to regulate inancial derivaive instruments not based on underlying transacions in the real sector, which let to themselves could fuel pressure on the rupiah.

The steady slowing in the global economy will in turn also worsen the liquidity crunch on the internaional inancial market. This will become a challenge in maintaining stability in the rupiah. So far, export revenues and foreign capital inlows have been vital in keeping Indonesia supplied with foreign exchange, especially to cover the heavy demand for foreign currency to pay for imports and service external debt. The persistent uncertainty over global market liquidity has kept capital inlows at a limited level.

The high risk spread for Indonesia is an added factor spurring exchange rate volaility when changes occur in market seniment. The growing diversity of inancial market instruments such as structured products, which may be used for speculaion, also represents a potenial source of downward pressure on the rupiah.

b. Improving the efeciveness of monetary policy

transmission

in tandem with the BI Rate. Bank Indonesia will work coninually to improve monetary policy efeciveness and expedite the transmission of monetary policy.

Challenges prevening opimum monetary policy response on the inancial market include uncertainty over business prospects, which raises the risk premium for debtors. To address this issue, Bank Indonesia works constantly to inform the public of the economic outlook and future direcion of monetary policy. In addiion, Bank Indonesia will keep encouraging some banks to act more as market leaders in seing the pace in deposit and loan interest rates. These acions will enable reducions in the monetary policy rate (the BI Rate) to be followed by similar movement in bank deposit and lending rates.

c. Segmentaion and liquidity problems on the inancial market

The liquidity crunch has taken on urgent importance for banks and inancial markets during this ime of global crisis. Pressure from porfolio adjustments has squeezed the liquidity of several banks, although aggregate banking liquidity remains suicient. In the view of Bank Indonesia, however, the problem faced by the banking industry involves the segmentaion of the inancial market. Segmentaion among banks has led to dispariies in availability of liquidity and is a cause of the ightened liquidity in recent months. This segmentaion is also the factor that poses recurrent challenges for Bank Indonesia in policy implementaion.

The segmentaion on inancial markets has lead to a widening in the spread between the lowest and highest overnight (O/N) rates in interbank transacions. Also relecing this is the wide diferenial between interbank rates and rates with longer tenors, due to persistently heavy demand for liquidity at certain banks. As a result, some banks have been plunged into liquidity diiculies and one bank was suspended from clearing by Bank Indonesia during 2008. However, the loose bias monetary policy and the various BI policy acions in monetary policy operaions have reduced interbank risk. Relecing this is the yield on interbank rates, which has returned to normal and has steadily eased since the end of 2008.

Diiculies are predicted to arise in bank compliance with the 2.5% secondary reserve requirement in October 2009 if the issues of segmentaion and ight liquidity at some banks are not resolved. Within this context, Bank Indonesia will coninue appealing to banks to take

immediate steps to prepare themselves and develop comprehensive plans for compliance with the secondary reserve requirement.

The various policy thrusts to be pursued by Bank Indonesia in 2009 to resolve the segmentaion and liquidity issues include: extension of the tenor for the Bank Indonesia short-term facility, expanded scope of assets eligible for pledging as collateral for the Bank Indonesia short-term facility and further consolidaion of the banking system.

Bank Indonesia Policy Direcion

On the monetary side, Bank Indonesia has pursued a series of acions to keep the economy from steeper decline. This involves a monetary policy stance conducive to promoing domesic demand, while upholding the commitment to safeguard economic stability in the medium and long term. Opportunity remains for further relaxaion of monetary policy, paricularly if the inlaion outlook stays on track with the medium-term inlaion target. This expansionary monetary policy direcion is vital to reducing the uncertainies and vulnerability of the Indonesian economy in both the inancial sector and real sector.

In regard to eforts to stabilise the exchange rate, Bank Indonesia will consistently seek the most opimum use of various policies to minimise exchange rate volaility. In addiion, Bank Indonesia has taken further acion to regulate inancial derivaive instruments not based on underlying transacions in the real sector, which let to themselves could fuel pressure on the rupiah.

On the other hand, relaxaion of monetary policy through interest rate cuts will not provide a complete soluion. Amid the uncertain outlook for the economy and growing risks, banks will coninue to exercise greater cauion in lending by applying an increased risk premium. In addiion, the risk of mouning non-performing loans (NPLs) will compel banks to raise addiional capital.

has demonstrated its capacity for growth and is strongly resilient to crisis.

In the naional payment system, Bank Indonesia policy coninues to focus on meeing public demand for payment instruments and services, supporing monetary and banking policy efeciveness and maintaining inancial system stability.

In the real sector, weakening global demand has also prompted downsizing in export-oriented companies, which has reduced credit demand from the real sector. Nevertheless, with bank capital now in a relaively strong posiion, reinforced by adequate liquidity, good reasons exist to expect a posiive response from the banking system. In this regard, Indonesian banks are expected not to hold interest rates at current levels, as this in turn would set of a negaive feedback efect from the real sector.

On the iscal side, a range of public policies is aimed at counter-cyclical acions to keep the economy from weakening further. Amid the constraints on other sources of growth, the iscal simulus is a key instrument for spurring the domesic economy to grow and delivery posiive beneits to the public. The iscal consolidaion and reforms implemented by the government in recent years have not only strengthened iscal sustainability, but also created greater iscal space for simulus. On the other hand, the slowing economy and gloomy condiion of the inancial market has also adversely impacted the simulus capability of the government.

Concluding Remarks

With the current global inancial crisis taking its toll on all sides, the Indonesian economy faces enormous challenges in 2009. The dynamics in the global economy will have a major bearing on the future of the Indonesian economy. Despite this, the domesic fundamentals underpinning the Indonesian economy are demonstrably in good shape and ofer a plaform for securing the economic future.

The execuion of the iscal simulus will be key to prevening a sharp drop in domesic demand. The iscal simulus is expected to deliver beneits to the public more rapidly than would a monetary simulus due to the lag in transmission of monetary policy before efecive impact is felt in the inancial market and banking system. Moreover, when business is shrouded with uncertainty, banks tend to exercise greater cauion in their lending. Under the condiions of the present global crisis, with uncertainies on all sides, monetary policy must be supported by other policies in the banking, iscal and real sectors. To keep economic growth at about the 4.0% mark, it will be important to give consideraion to policies capable of bringing quick results in the real sector.

In 2009, there is conidence that Indonesia will be in beter condiion compared to other countries facing the prospect of sharply reduced growth and even deep contracion. Developed countries such as the United States, Japan and the UK will chart negaive growth. In China and India, growth will be signiicantly reduced. With growth rates sliding on a global scale, many countries have launched iscal simulus packages in various forms aimed at shielding the poor from even worse impact from the crisis. These simulus packages consist of investment, educaion, reducions in fuel prices, free transport for the poor, credit for MSMEs and even construcion of infrastructure.

Condiion of the Economy | Economic Outlook and Policy Direcion

PERFORMANCE OF THE

INDONESIAN ECONOMY, OUTLOOK

AND POLICY DIRECTION

In 2008, the Indonesian economy

came under enormous pressure

from mouning uncertainty on

global inancial markets, the

signiicant world economic

slowdown and drasic changes

in global commodity prices.

Even though almost on par with

the previous year, economic

growth in 2008 tapered of

with increasing pressure on

macroeconomic stability during

the second half of the year.

The sheer weight of external

pressure was relected in the

deterioraing performance in the

balance of payments, downward

trend in the exchange rate and

high inlaion. Even so, the

Indonesian economy did not

fare too badly in comparison

to other countries. This was largely atributable

to strong domesic demand supported by

prudent, consistent iscal and monetary policies.

Those policies were also reinforced by various

measures in the real sector and inancial sector

aimed at safeguarding macroeconomic stability

while sustaining momentum for long-term

economic growth.

The fallout from the gloomy world economic

turbulence on the Indonesian economy is

relected mainly in the balance of payments for

2008, the exchange rate and inlaion. Posiive

gains in the balance of payments during the irst

half of 2008 were reversed by drasic setbacks

in the second half of the year. The current

OUTLOOK AND POLICY DIRECTION

PERFORMANCE OF THE INDONESIAN ECONOMY,

account began charing a deicit in QII-2008,

and ulimately the capital and inancial account

followed suit in QIV-2008 due to oloading of

inancial assets by foreign investors spooked

by worsening seniment on global inancial

markets. In similar movement, the balance of

payments performed less strongly, eventually

posing a deicit in QIII-2008. The downturn

in the balance of payments in turn triggered

strong exchange rate depreciaion accompanied

by high volaility. The exchange rate, which

had held relaively stable unil August 2008,

came under heavy pressure and registered

steep depreciaion. During this ime, soaring

world oil prices forced the Government to

take acion to safeguard iscal sustainability

by raising prices for subsidised fuels. This

led to rising inlaionary pressure, which had

persisted at a high level since the beginning of

the year due to strong global commodity prices.

Nevertheless, inlaionary pressure gradually

eased near the end of the year, in keeping with

cuts in subsidised fuel prices and falling global

commodity prices.

CONDITION OF

THE ECONOMY

1.1

During 2008, the condiion of the Indonesian economy was marked by highly dynamic, challenging developments brought on by the turbulence in the drasically changed world economy. Despite the high growth unil QIII-2008, the Indonesian economy slowed considerably in the inal quarter as the world economy slid further into decline. Growth slowed across all components of aggregate demand, with exports plunging sharply in line with tumbling commodity prices and slackening growth in trading partner countries.

Despite signiicant slowing in the inal quarter of 2008, economic growth of Indonesia reached 6.1% for 2008 overall, almost on par with the previous year’s growth rate of 6.3%. As late as QIII-2008, the Indonesian economy was sill forging ahead. This is explained to a large

extent by high growth in exports, which soared in line with escalaing global prices for mining and agricultural commodiies. Bolstered by the robust economic growth in China and India, Indonesia’s exports charted buoyant growth in the irst two quarters of 2008. Strong export growth then provided added momentum to purchasing power, especially in export-producing regions, which contributed to high levels of consumpion and investment. As could be expected, import growth also soared in response to the need for raw materials and capital goods. Despite this, Indonesia’s economic growth began tapering

of from the beginning of the second half of 2008, due to the steeper turn in the global economic slowdown and falling global commodity prices. These developments led to falling levels of export growth. In a similar vein, growth in household consumpion, investment and imports also registered decline.

The steep downturn in the world economy was

accompanied by mouning uncertainty and risk on global inancial markets. The spreading fallout from the problems in the US housing sector and bailout of several inancial insituions by the government and the Federal Reserve coninued to meet with negaive response from markets, which intensiied the turmoil on global inancial markets. The unstable condiion of inancial markets subsequently triggered negaive seniment that blunted the risk appeite of investors and set of a trend of global porfolio reshuling. In addiion to the high levels of uncertainty, ight liquidity increasingly hampered eforts to boost exports and atract foreign investment.

US dollars, equivalent to 4.0 months of imports and servicing of oicial external debt. In the irst half of 2008, the balance of payments showed quite solid performance, relected in internaional reserves and a surplus in the overall balance at 59.4 billion and 2.35 billion US dollars. The current account charted a 1.3 billion US dollar surplus on buoyant volume of exports and strong commodity prices. At end-June 2008, Indonesia’s commodity export price index was up 36% over the end-December 2007 posiion. Reinforcing this was the capital and inancial account that booked a surplus at 915 million US dollars, mainly from porfolio capital inlows totalling 3.8 billion US dollars.

However, these relaively conducive external condiions changed with drasic deterioraion in the second half of 2008 triggered by massive losses from the subprime mortgage crisis in the US and the impact on the US real sector that far exceeded expectaions. These changes led to signiicant and rapid downturn in Indonesian exports. The current account surplus quickly evaporated due to falling exports and rising imports driven by the coninued vigorous pace of economic acivity. In the capital and inancial account, loss of foreign investor conidence in emerging markets led to capital ouflows, pushing up the account deicit.

The impact of the global crisis is also relected in the movement of the rupiah, which since October 2008 has seen considerable volaility combined with strong downward pressure. During the irst half of 2008, the current account surplus and prudent macroeconomic responses were suicient to contain pressures generated by external turbulence. However, since QIII-2008, the fallout from the global inancial crisis has mounted with the collapse of major inancial insituions in the US and the deleveraging process on global inancial markets. Heightened risks on a global scale triggered a rush to pull foreign porfolio investments out of Indonesia’s inancial market. On the other hand, the current account sustained pressure from falling commodity prices and declining economic acivity in trading partner countries. These events led to increased pressure on the rupiah, which sank to a low of Rp 12,150 per US dollar in November alongside sharply increased volaility at 4.67%. On average for the year, the rupiah depreciated 5.4% from Rp 9,140 (2007) to Rp 9,666 per US dollar (2008).

At the same ime, soaring global prices for crude oil and food commodiies also afected CPI inlaion in Indonesia, which mounted to 11.06% in 2008. Disaggregaion of inlaion factors shows that the rise in CPI inlaion was spurred mainly by increases in administered prices.

The inlaion contribuion from the administered prices category widened 2.24% from the 0.75% contribuion in 2007 to 2.99% in 2008. This inlaion was triggered by escalaing world oil prices that forced the Government to raise subsidised fuel prices in May 2008 by 28.7%. The impact of this fuel price hike was exacerbated by supply shortages of relevant commodiies, such as kerosene and botled LPG in some regions. Besides the 1.22% irst round efect, the fuel price also produced a second round efect of 0.82% from increases in transport fares. Rising world food prices, despite stable condiion of supply, also increased the volaile foods contribuion to inlaion from 2.09% to 2.59%. Taken together, these factors also led to a 1.73% rise in core inlaion from 6.29% in 2007 to 8.29% in 2008. Another factor in the heightened core inlaion was increased public expectaions of inlaion related to escalaing world food commodity prices and distribuion botlenecks afecing supply.

On the iscal side, the fuel subsidy allocaion in the 2008 Budget was no longer suicient to cope with high world oil prices and heavy volume of crude oil imports, a situaion that was feared could derail iscal sustainability. In response, the Government decided to raise domesic fuel prices by an average 28.7% in May 2008. The increased prices remained unchanged unil December 2008, when world oil prices were in decline. To ensure opimum implementaion of the 2008 Budget, the Government took various safeguard measures on the expenditures side. These acions include the use of iscal risk reserves; approximately 10% savings from expenditure cuts, refocused acivity prioriies and postponement of non-priority aciviies in line ministry/agency budgets; and cuts in budget expenditures for the fuel subsidy and electricity subsidy. In a parallel acion to ease the burden of the populaion from escalaing prices for key domesic foodstuf commodiies, the Government launched the Price Stabilisaion Policy Package (PKSH). While reducing the fuel subsidy, the Government also compensated for this cut by providing Direct Cash Transfers (BLT). Later, however, with oil prices moving lower, the Government announced a cut in fuel prices in December. In the overall outcome, the deicit from Government inancial operaions came to 0.1% of GDP, well below the 1.7% recorded in the previous year.

Responding to the potenial for heightened

consideraion in this decision was that interest rate stability would support economic growth, which was sill in an expansion phase, and would not disrupt inancial system stability. However, uncertainies on the global inancial market and the steep rise in oil prices in April 2008 fuelled strong inlaionary pressure from escalaing food and non-food prices. In view of the potenial for coninued pressure on macroeconomic stability, Bank Indonesia embarked on gradual, measured increases in the BI Rate beginning in April 2008, with the rate climbing 150 bps to 9.5% by October 2008.

These macroeconomic stabilisaion measures were also reinforced by various policy acions aimed at miigaing the negaive impact of the intensifying global inancial crisis. In October 2008, Bank Indonesia (BI) issued the exchange rate stabilisaion package to manage foreign exchange supply and demand. The foreign exchange supply stabilisaion policy includes regulaions on FX Swaps, the foreign currency reserve requirement, services for corporate eniies and export drats (WEB). Similarly, to manage foreign exchange demand, other policies were introduced to prohibit banks from engaging in customer FX transacions without underlying transacions and to make foreign currency available for servicing external borrowings in the short-term. The Government also reinforced these acions with regulaions pertaining to the Indonesia Financial Safety Net (IFSN), increase in the limit of bank customer deposit insurance to Rp 2 billion, controls on selected import com