www.elsevier.com / locate / econbase

First-difference estimator for panel censored-selection models

*

Myoung-jae Lee

Institute of Policy and Planning Sciences, University of Tsukuba, Tsukuba, Ibaraki 305-8573, Japan

Received 19 October 1999; accepted 20 July 2000

Abstract

We propose a semiparametric first-difference estimator for panel censored-selection models where the selection equation is of tobit type. The estimator allows the unit-specific term to be arbitrarily related to regressors. The estimator minimizes a convex function and does not require any smoothing. A simulation study is provided comparing our proposal with the estimators of Wooldridge (Journal of Econometrics 68 (1995) 115)

´

and Honore and Kyriazidou (Econometric Reviews (2000)). 2001 Elsevier Science B.V. All rights reserved.

Keywords: Panel data; Related-effect; Sample selection; Censored model

JEL classification: C24; C34

1. Introduction

Consider a panel ‘related-effect’ censored-selection model:

*

9

*

dit5xita1ci1´it, dit;1[dit .0], di;d di 1 i 2,

(1.1)

9

yit5xitb1pi1u ,it t51,2,

*

*

9

9

(max(di 1,0),max(di 2,0),di 1y ,i 1di 2y ,x ,x )i 2 i 1 i 2 9observed, i51, . . . ,N, iid across i,

*

where thedit equation is a ‘selection equation’, x is a time-variant regressor vector,it ´it and u areit error terms, the y equation is the ‘outcome equation’ of interest,it ci and pi are unit-specific effects including all the time-invariants, a and b are parameter vectors, and 1[A]51 if A holds and 0 otherwise; we allow ci and pi to be related to xit (hence the term ‘related-effect’, following Lee,

*

1999). A well-known example of censored-selection is:dit is hours worked and y is the wage. Here,it

*

y is observed only for the workers, but we also observeit dit when dit51.

*Tel.:181-298-53-5375; fax: 181-298-55-3849. E-mail address: [email protected] (M.-j. Lee).

In the literature of linear panel data with no selection problems, a standard way to handle a related-effect is first-differencing. In this paper, we propose a bandwidth-free semiparametric estimator forb. The gist of the estimator is removingpi by first-differencing and then controlling for the selection bias using ´i 22´i 1 as a regressor.

In Section 2, we present our estimator. In Section 3, other estimators forb are reviewed. In Section 4, a simulation study is provided. In Section 5, conclusions are drawn. Throughout the paper, we use

p

aN5 b for aN N2bN5o (1) as Np →`, and ⇒ for weak convergence. The subscript i for individuals will often be omitted. The fourth moment is assumed to exist for all random variables.

2. The Estimator

Define

9

9

xi;(x ,x )i 1 i 2 9, yi;( y , y )i 1 i 2 9, ui;(u ,u )i 1 i 2 9, ´i;(´i 1,´i 2)9,

Dyi;yi 22y ,i 1 Dxi;xi 22x ,i 1 D´i;´i 22´i 1.

We impose four assumptions. First,

E(uitux ,i´i)5h(x )i 1E(uitu´i), t51,2, (2.1)

where h(x ) is an unknown function exchangeable in xi i 1 and x : h(x ,x )i 2 i 1 i 2 5h(x ,x ); (2.1) allowsi 2 i 1 h(?)50, with which (2.1) becomes the mean-independence of uit from x giveni ´i. Second, for unknown parameters rt1 and rt 2

E(uitu´i)5r ´t1 i 11r ´t 2 i 2, t51,2, (2.2)

which is a linear projection. Third,

r115r22;r0andr125r21;r1. (2.3)

A sufficient condition for (2.3) is a (joint) ‘exchangeability’: for any 431 constant vectort and for a.e. xi

P((´i 1,´i 2,u ,u )i 1 i 2 9 #tux )i 5P((´i 2,´i 1,u ,u )i 2, i 1 9 #tux );i (2.4)

the sufficiency holds because (2.4) implies

E(ui 1u´i 1,´i 2)5E(ui 2u´i 2,´i 1), for a.e. (´i 1,´i 2). (2.5)

Fourth, (2.12) below holds. Using (2.1) and (2.2), we get

9

E( yitux ,i´i)5xitb1E(piux ,i´i)1h(x )i 1r ´t1 i 11r ´t 2 i 2, t51,2.

Rewrite the y equation asit

9

y 5x b1p 1h(x )1r ´ 1r ´ 1v , (2.6)

where

which is the key equation for our proposal. If D´i were observable, then the least squares estimator (LSE) would be applicable to (2.9), for

E(Dvux ,´)5E(v ux ,´)2E(v ux ,´ )502050. (2.10) i i i i 2 i i i 1 i i

´ AœN-consistent estimator for D´i can be obtained using the fourth estimator, say a , in HonoreN (1992) (the LSE version for a panel censored model) that minimizes a convex function with no

ˆ

*

smoothing. Specifically, with dit;max(dit,0), the minimand (for a) is

2

The LSE for this with h?j as the error term is our estimator, which is not applicable to panel

ˆ

‘binary-selection’ models where onlydit, not dit, is observed, for D´i is not identified. No exclusion ´ restriction is necessary in censored-selection, differently from binary-selection. Since Honore and Kyriazidou (2000) show that a requires the stationarity ofN

(´i 1,´i 2)u(ci,x ),i (2.12)

ˆ

Replace z with z in (2.13), which can be shown to make only an o (1) difference. The first-stagei i p

ˆ

V can be consistently estimated by replacing E(?) by its sample version.

3. Estimators for panel censored-selection

For Wooldridge’s (1995) estimator, rewrite the selection equation:

*

9

dit 5xita1E(ciux )i 1ci2E(ciux )i 1´it. (3.1) 2

Wooldridge requires that, for some constants st, t51,2,

(a) E(ciux ) is a linear function of x ,i i

(3.2) 2

(b)ci2E(ciux )i 1´itfollows N(0,st) independently of x .i

˜ ˜

Then, for some conformably defined parameter vectors at1 and at 2

As for the outcome equation, Wooldridge requires

The assumption (3.4) is comparable to (2.1) and (2.2). The main difference in our estimator’s assumptions and Wooldridge’s is (2.3) vs. (3.2): ours needs only a weak form of exchangeability,

˜

while Wooldridge specifies the conditional mean ofcion x and requires the marginal normality ofi ´it. This normality for the selection equation in addition to the linear projection (3.4) for the outcome equation makes Wooldridge’s a panel censored-selection analog of Heckman (1979).

9

´for b; Honore and Kyriazidou (2000) propose a number of estimators, and (3.9) is only (computation-ally convenient) one of them. The idea for (3.9) is based upon the event in 1[?] of (3.9) being equivalent to

9

9

9

9

´i 1.max(xi 1a2ci,2xi 2a2ci), ´i 2.max(xi 1a2ci,2xi 2a2ci); (3.10)

9

under (3.8), conditional on this event and zi, Dyi2 Dxib is symmetrically distributed about zero. In minimizing (3.9) numerically, our estimator can be used as a convenient initial value, for it requires only a LSE once aN is obtained.

´

Honore and Kyriazidou (2000) do not need any linear projection type nor mean-independence type assumptions, while our estimator and Wooldridge’s (1995) do. On the other hand, they require exchangeability involving four error terms, while Wooldridge needs a marginal normality and our estimator needs a weak form of exchangeability.

(´i 1,u ) and (i 1 ´i 2,u ) are iid conditional uponi 2 ci,pi,x .i (3.11)

Differently from the other estimators, however, there is no guarantee that their method-of-moment estimator converges well; in fact, it hardly ever did in our trials, although a grid search worked. For this reason, in the following simulation, Ai and Chen’s (1992) estimator is not considered.

4. A simulation study

´

In Table 1, we compare our estimator with Wooldridge (1995) and Honore and Kyriazidou (2000) in nine designs with one time-variant regressor. The bench mark model is

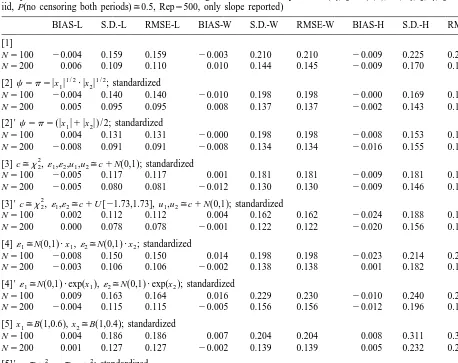

Table 1

´

Comparison of our estimator with those of Wooldridge and Honore and Kyriazidou (x ,x1 2(N(0,1), iid,´1,´2,u ,u1 2(N(0,1), iid, P(no censoring both periods)(0.5, Rep5500, only slope reported)

BIAS-L S.D.-L RMSE-L BIAS-W S.D.-W RMSE-W BIAS-H S.D.-H RMSE-H

[1]

N5100 20.004 0.159 0.159 20.003 0.210 0.210 20.009 0.225 0.225 N5200 0.006 0.109 0.110 0.010 0.144 0.145 20.009 0.170 0.171

1 / 2 1 / 2

[2]c 5 p 5ux1u ?ux2u ; standardized

N5100 20.004 0.140 0.140 20.010 0.198 0.198 20.000 0.169 0.169 N5200 0.005 0.095 0.095 0.008 0.137 0.137 20.002 0.143 0.143

[2]9c 5 p 5(ux1u1ux2u) / 2; standardized

N5100 0.004 0.131 0.131 20.000 0.198 0.198 20.008 0.153 0.153 N5200 20.008 0.091 0.091 20.008 0.134 0.134 20.016 0.155 0.156

2

[3] c(x2, ´1,´2,u ,u1 2(c1N(0,1); standardized

N5100 20.005 0.117 0.117 0.001 0.181 0.181 20.009 0.181 0.181 N5200 20.005 0.080 0.081 20.012 0.130 0.130 20.009 0.146 0.146

2

[3]9c(x2,´1,´2(c1U [21.73,1.73], u ,u1 2(c1N(0,1); standardized

N5100 0.002 0.112 0.112 0.004 0.162 0.162 20.024 0.188 0.189 N5200 0.000 0.078 0.078 20.001 0.122 0.122 20.020 0.156 0.157

[4]´1(N(0,1)?x ,1 ´2(N(0,1)?x ; standardized2

N5100 20.008 0.150 0.150 0.014 0.198 0.198 20.023 0.214 0.215 N5200 20.003 0.106 0.106 20.002 0.138 0.138 0.001 0.182 0.182

[4]9´1(N(0,1)?exp(x ),1 ´2(N(0,1)?exp(x ); standardized2

N5100 0.009 0.163 0.164 0.016 0.229 0.230 20.010 0.240 0.240 N5200 20.004 0.115 0.115 20.005 0.156 0.156 20.012 0.196 0.196

[5] x1(B(1,0.6), x2(B(1,0.4); standardized

N5100 0.004 0.186 0.186 0.007 0.204 0.204 0.008 0.311 0.311

N5200 0.001 0.127 0.127 20.002 0.139 0.139 0.005 0.232 0.232 2 2

[5]9x1(x2, x2(2x2; standardized

*

dit5a11a2 itx 1ci1´it, yit5b11b2 itx 1pi1u ,it

c5p5(x11x ) / 2,2 x ,x1 2(N(0,1), iid, ´1,´2,u ,u1 2(N(0,1), iid,

a25b15b251, a1(0.8 for P(d51)(0.5, N5100,200, Rep5500;

only outcome equation slope estimates are reported. BIAS-L, S.D.-L, and RMSE-L are, respectively, the bias, standard deviation, and root-mean-squared error of our estimator, while BIAS-W, S.D.2W

´

and RMSE-W are for Wooldridge, and BIAS-H, S.D.-H and RMSE-H are for Honore and Kyriazidou (2000); c, x , x ,1 2 ´1, ´2, u , and u are always standardized.1 2

The bench mark model is estimated in panel [1]. In [2] and [2]9, c is nonlinear, violating (3.2(a)). 2

In [3] and [3]9, all error terms are correlated through a common factor c followingx2 (in [3]9,´1 and

´2 are c plus uniformly distributed errors), violating (2.2), (3.2(b)) and (3.4). In [4] and [4]9,´1 and´2 are multiplicatively heteroskedastic, violating (2.1) and (3.2(b)) and (3.4). In [5] and [5]9, dummy regressors and asymmetrically distributed regressors are used to avoid too much smoothness in regressors and symmetry everywhere.

In all designs, three estimators are surprisingly robust with almost no bias despite violated assumptions. This seems to be due to the cancellation of bias-causing factors in first-differencing; good performance of first-difference estimators in panel binary-selection models has also been observed by Verbeek and Nijman (1992). In all designs, our estimator has much smaller standard deviations compared with the other estimators; it often takes N5200 for the other estimators to have comparable standard deviations to ours with N5100.

5. Conclusions

In this paper we have proposed a simple semiparametric first-difference estimator for panel related-effect censored-selection models. The estimator is based upon weak assumptions and is easy to implement by minimizing a convex function with no smoothing. With a simulation study, we have

´ shown that the estimator performs well relative to those of Wooldridge (1995) and Honore and Kyriazidou (2000), and that all three estimators are quite robust to model assumption violations.

References

Ai, C., Chen, C., 1992. Estimation of a fixed effects bivariate censored regression model. Economics Letters 40, 403–406. Heckman, J.J., 1979. Sample selection bias as a specification error. Econometrica 47, 153–161.

´

Honore, B.E., 1992. Trimmed LAD and LSE of truncated and censored regression models with fixed effects. Econometrica 60, 533–565.

´

Honore, B.E., Kyriazidou, E., 2000. Estimation of tobit-type models with individual specific effects. Econometric Reviews, forthcoming.

Lee, M.J., 1999. A root-N consistent semiparametric estimator for related-effect binary response panel data. Econometrica 67, 427–434.

Verbeek, M., Nijman, T., 1992. Testing for selectivity bias in panel data models. International Economic Review 33, 681–703.