Reasons for Cost and Schedule Increase for Engineering

Design Projects

Andrew Shing-Tao Chang, P.E., M.ASCE

1Abstract: Cost and schedule increases are common in engineering design projects. Some research has studied factors associated with better design performance, but the reasons for cost and schedule increases are not formally investigated. This paper identifies the reasons bottom up from four case project documents and further quantifies their contributions to cost and schedule increases. These reasons are complete and can be used to analyze the cause-effect relationship, trace responsibility, and improve performance for engineering design projects.

DOI: 10.1061/~ASCE!0742-597X~2002!18:1~29!

CE Database keywords: Design; Cost; Scheduling; Project management.

Introduction

Engineering design has high level of influence on project costs ~Barrie and Paulson 1992!. However, design performance is usu-ally not satisfactory. A survey reveals that about one third of architectural/engineering ~A/E! projects miss cost and schedule targets ~Anderson and Tucker 1994!. There have been few in-stances where an engineering design was so complete that a project could be built to the exact specifications contained in the original design documents ~Smith 1996!. Many construction problems are due to design defects and can be traced back to the design process ~Bramble and Cipollini 1995!.

Some studies have identified factors that influence design per-formance. Tucker and Scarlett~1986!proposed seven criteria for evaluating design performance, including accuracy, design economy, and constructability. Chalabi et al. ~1986! listed 10 input variables with a major impact on design effectiveness, such as scope definition and owner participation. Alarcon and Ashley ~1992! identified that organization, incentive plans, and team building have high positive impact on design performance. San-vido et al.~1992!identified four critical success factors including facility team and contracts for designing commercial building projects. Anderson and Tucker ~1994!found that the use of best project management~PM!practices is associated with better per-formance of A/E projects. Sternbach ~1988!stated that the pro-cess variables causing A/E project delays are extra work beyond the original scope of agreement, failure of the owner or its other consultants to provide information, and objections by environ-mental or community groups.

The above studies have discussed factors associated with de-sign performance. But the causes or reasons for inadequate cost/

schedule performance are not formally investigated. This paper identifies the reasons for cost/schedule increases and quantifies their contributions by case studies. Case studies are useful when investigating human errors in complicated processes, such as structural design ~Blockley et al. 1986!. Qualitative analysis through case studies is particularly useful for investigating why a relationship exists~Eisenhardt 1989!.

Reasons Identified from Project Documents

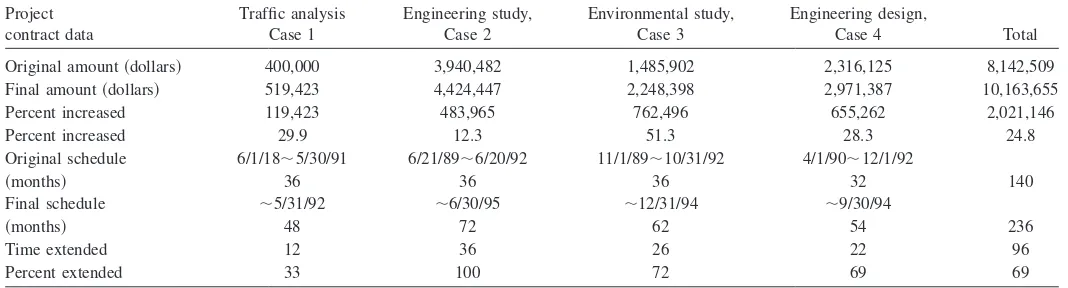

Four completed projects were studied as cases. They were envi-ronmental and engineering design services for roadway construc-tion projects in California. All four cost-plus-fixed-fee projects experienced cost and schedule increases to a certain extent~Table 1!. Cost increased on an average of 24.8%, and schedule in-creased on an average of 69%, based on the four sampled projects.

Amendments are official changes of costs and/or schedules in the contract. In the owner’s internal process, the reasons for changes have to be stated and attached as a backup when request-ing an amendment. After the amendment is approved, a formal amendment stating the new work scope, cost, and time will be signed by the owner and consultant. There are some changes without amendments, such as an interim time adjustment allowed by the owner during the project.

There were about 30 formal and informal changes in the four reviewed amendment backup documents and project files. Each amendment or change included several subchanges and each sub-change included several explanations. More than 100 explana-tions were found. These explanaexplana-tions in the amendment backup documents were prepared by the owner; sometimes the consult-ant’s statements were attached. Those in the project files came from the consultant’s letters or other correspondence.

When an amendment was analyzed in this research, the pre-liminary reasons for changes were first identified against the ex-planations written in the amendment backup documents. Then the relevant letters and correspondence in the project files were fur-ther reviewed to modify or confirm these reasons. The following statements are typical explanations found, listed in the parenthe-ses are the proposed reasons against the explanations.

From amendment backup documents: 1Associate Professor, Dept. of Civil Engineering, National Cheng

Kung Univ., Tainan, Taiwan. E-mail: [email protected] Note. Discussion open until June 1, 2002. Separate discussions must be submitted for individual papers. To extend the closing date by one month, a written request must be filed with the ASCE Managing Editor. The manuscript for this paper was submitted for review and possible publication on November 13, 2000; approved on May 11, 2001. This paper is part of theJournal of Management in Engineering, Vol. 18, No.

1, January 1, 2002. ©ASCE, ISSN

• ‘‘Unanticipated efforts’’ or ‘‘increased level of effort than was originally anticipated for . . . ’’ ~growing needs or owner’s omission in the original scope!;

• ‘‘Additional effort to complete . . . due to changes in Federal requirements’’~standard change!;

• ‘‘Expanded level of effort in response to unanticipated public and agency comments’’~stakeholders’ request!;

• ‘‘Update . . . analysis due to change in focus’’~owner’s request after focus change!;

• ‘‘Additional time due to contracting-out lawsuit’’ ~law change!;

• ‘‘Additional alternative studies requested by the affected com-munity’’~stakeholders’ request!;

• ‘‘The original schedule is optimistic . . . ’’ ~optimistic sched-ule!, and

• ‘‘District did not have sufficient staff to do . . . ’’~owner’s re-quest!.

From project files, mostly from letters and memos: • ‘‘The consultant had difficulty meeting with locals to

get . . . needed’’~consultant’s inability, and/or stakeholders!; • ‘‘Additional costs to coordinate review, attend meetings’’

~growing needs, and/or consultant’s underestimate!;

• ‘‘The actual scope of work was not well understood at the time the hours were originally estimated’’~consultant’s omission!; • ‘‘Underestimated coordination and effort’’~consultant’s

under-estimate!;

• ‘‘The inability of ~other consultants! to meet the original schedule has resulted in . . . ’’~other consultants!;

• ‘‘Lack of data to perform analyses’’ ~other consultants, the owner or stakeholders!;

• ‘‘Addition of another alternative’’~owner’s request!; and • ‘‘Because . . . was not made available to you until . . . we

con-cur with your revised proposed schedule’’~owner’s failure to provide information!.

After all the statements were reviewed, analyzed, and com-pared, the final reasons for cost increases and schedule extensions became apparent. They were also confirmed by the owner’s project managers when interviewed. The final reasons are consis-tent with the findings by Sternbach~1988!but are more detailed and insightful. The 10 reasons and their meanings are described as follows.

1. Owner’s request. The owner or its functional units request additional work or change focus/decision at a later date due to new findings and other considerations.

2. Optimistic schedule. The original schedule is overly opti-mistic and unrealistic, due to inaccurate estimates or politi-cal decisions.

3. Omissions-owner. Work that should have been included in the original scope is omitted by the owner.

4. Owner’s failure.

• The owner or its functional units fail to provide infor-mation, make decisions, or take actions in a timely man-ner.

• The information provided by the owner is incomplete or incorrect.

5. Other consultants. Consultants for other related projects fail to provide necessary information on time.

6. Consultant’s inability. The consultant is not effective or ef-ficient in performing the work, due to complicated work, insufficient staff, and/or lack of competent staff.

7. Omissions or underestimates—consultant. The actual scope of work is not well understood by the consultant at the time the work hours were originally estimated.

8. Growing needs. It is not anticipated at the scoping stage; extra work or additional level of effort is needed after more studies, engineering, or design has been done. The work grows ‘‘naturally’’ without requests from the owner. 9. Stakeholders. Outside stakeholders, e.g., permitting

agen-cies, community, etc., request more alternatives, investiga-tions, and/or explanations.

10. Others. Other reasons beyond the owner’s or consultant’s control exist, such as changes of laws or standards. Originally, it was planned to separate the reasons for cost in-creases from those for time extensions. After preliminary catego-rization, it was found that the reasons for cost increases are nor-mally also the reasons for time extensions, because the increased work takes time to accomplish and vice versa. The optimistic schedule would seem a reason only for a time extension. But an optimistic schedule may force the consultant to accelerate work, which may cause additional costs.

A cost increase appeared as the first amendment in all four projects. The trend is that a cost increase is proposed in the early stage of a project and a time extension follows. This coincides with the impression that the consultant’s major concern is to make a profit ~Oglesby et al. 1989!, and time is more flexible and can be resolved later. If time is the owner’s main concern, every po-tential schedule change should be closely monitored when a cost change is proposed.

It was logical to anticipate that these reasons could be catego-rized according to responsibility. Reasons 1 to 5 are factors within the owner’s control; reasons 6 and 7 are within the consultant’s control; and the rest are beyond either the owner’s or the consult-ant’s control.

Table 1. Summary of Cost and Schedule Increases for Four Projects

Project

Original amount~dollars! 400,000 3,940,482 1,485,902 2,316,125 8,142,509

Final amount~dollars! 519,423 4,424,447 2,248,398 2,971,387 10,163,655

Percent increased 119,423 483,965 762,496 655,262 2,021,146

Percent increased 29.9 12.3 51.3 28.3 24.8

Original schedule 6/1/18;5/30/91 6/21/89;6/20/92 11/1/89;10/31/92 4/1/90;12/1/92

~months! 36 36 36 32 140

Final schedule ;5/31/92 ;6/30/95 ;12/31/94 ;9/30/94

~months! 48 72 62 54 236

Time extended 12 36 26 22 96

Quantification of Cost Schedule Increases

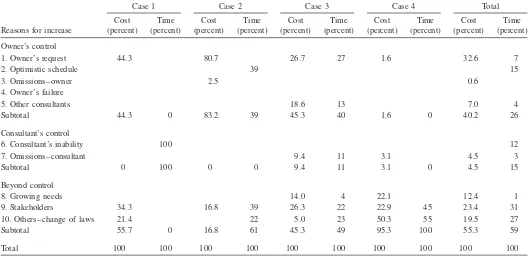

The cost/schedule increase percentage is summarized in Table 2. For the cost of Case 1, 44.3% of the total increase ~$119,423, Table 1!was caused by the owner’s request, which was the only reason within the owner’s control. Beyond control, 34.3 and 21.4% were by stakeholders and law change, respectively. These two ‘‘beyond-control’’ reasons totaled 55.7%. Sources of these numbers and detailed calculations for Case 1 are explained later in the case study; the other three cases are described in the Ap-pendix.

We can see that about half of increased cost and time are contributed by reasons beyond either the owner’s or the consult-ant’s control. One owner’s project manager said that many projects were questioned by the stakeholders during the project period in the early 1990s, many difficult, beyond-control

pro-cesses increased cost and time. Perhaps the increases also resulted from the characteristics of environmental services, which incline to attract the public’s attention. The cost/time increases from sons within the owner’s control total about one-third. Those rea-sons within the consultant’s control contribute the least. The time extension solely caused by the consultant’s inability to complete Case 1 is an exceptional case that will be described in the case study.

Although owner’s failure does not appear in any cost or sched-ule increases in these cases, it certainly does impact a consultant’s schedule and cost performance. These statements were common in the consultants’ correspondence to the owner: ‘‘If these items can be furnished to us in the next two weeks, we can meet our schedule,’’ ‘‘in order to complete this work on time it would be extremely helpful to have the following additional information form~the owner!,’’ etc. Their disappearance in the formal amend-Table 2. Quantification of Cost and Schedule Increases

Reasons for increase

1. Owner’s request 44.3 80.7 26.7 27 1.6 32.6 7

2. Optimistic schedule 39 15

3. Omissions–owner 2.5 0.6

4. Owner’s failure

5. Other consultants 18.6 13 7.0 4

Subtotal 44.3 0 83.2 39 45.3 40 1.6 0 40.2 26

Consultant’s control

6. Consultant’s inability 100 12

7. Omissions–consultant 9.4 11 3.1 4.5 3

Subtotal 0 100 0 0 9.4 11 3.1 0 4.5 15

Beyond control

8. Growing needs 14.0 4 22.1 12.4 1

9. Stakeholders 34.3 16.8 39 26.3 22 22.9 45 23.4 31

10. Others–change of laws 21.4 22 5.0 23 50.3 55 19.5 27

Subtotal 55.7 0 16.8 61 45.3 49 95.3 100 55.3 59

Total 100 100 100 100 100 100 100 100 100 100

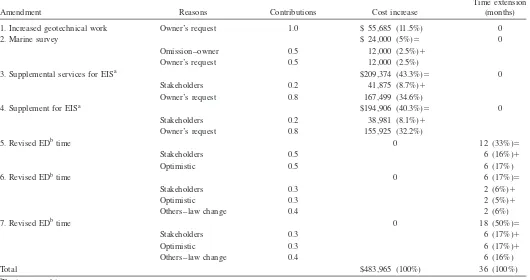

Table 3. Analysis of Cost and Schedule Increases for Case 1

Change or amendment Reasons

Contributions

~percent! Cost increase

Time extension ~months!

Change 1 0 95

Consultant’s inability 0.9 81

Owner’s request 0.1 1

Change 2 Consultant’s inability 1.0 0 5

Amendment 1 $102,344 ~85.7%!5 0

a. Additional corridor Stakeholders 0.8 40,938 ~34.3%!1

traffic study Owner’s request 0.2 10,234 ~8.6%!1

b. Land use forecast using Others-standard change 0.5 25,586 ~21.4%!1

ABAGa1990 projections Owner’s request 0.5 25,586 ~21.4%!

Amendment 2

Time extension for Amendment 1

Consultant’s inability 1.0 0 12~100%!

Amendment 3

Additional impact analysis

Owner’s request 1.0 $17,079 ~14.3%! 0

Total $119,423 ~100%! 12~100%!

a

ments is probably due to the consultants’ unwillingness to dis-close the owner’s responsibility.

Case Study

Case 1 is a traffic operational analysis that provides background data for evaluating the environmental consequences of a

construc-tion project. The following is an amendment analysis as well as schedule and cost increase analysis for this project.

Amendment Analysis

owner’s project manager was asked to distribute contribution per-centages from individual reasons to that change. The increased cost/time amount is prorated accordingly in the fourth and fifth columns. The total cost increase is $119,423; Amendment 1 cost $102,344. The 85.7% cost increase is due to the reasons listed in the second column.

There were two informal time extensions at the beginning without formal amendments~Fig. 1!, but these two extensions did not change the final completion time. The draft report preparation was given another 9 months. The major reason~90%, written as 0.9!was that the consultant could not complete the draft report within the original 5-month time frame. Later, an additional 5 months was granted due to the consultant’s inability ~100%! to complete the work.

In Amendment 1 ~Table 3!, two change items were stated in the backup documents: ~a! additional traffic study; and ~b! the land use forecast based on Association of Bay Area Governments ~ABAG!1990 version.

The preliminary reasons identified for these two changes were stakeholders, owner’s request, and growing needs. From the project files, two memos were found relevant to this amendment: ~1!from an attorney of the owner’s Legal Division questioned if the additional study was related to the original scope, and if yes, why it was not included in the original contract, and the other was the justification by the project manager— ‘‘It wasn’t until that the need to study . . . were determined . . . it is also seen from the results of the traffic study performed to date . . . Therefore, a study is necessary . . . The ABAG 1987~projections!are now ob-solete.’’ From the above explanations, the reasons for changes look like growing needs, owner’s request after decision change, and standard change.

Finally, a discussion with the owner’s project manager re-vealed that the additional study was mainly requested by the local

governments and residents, i.e., the stakeholders and the owner. The ABAG usage was due to standard change and owner’s re-quest.

In conclusion, for the contributions to Amendment 1~a!, as shown in Table 3, about 80% of the change was caused by stake-holders and 20% by the owner’s request. The $40,938~34.3% of $119,423!from stakeholders is four times the $10,234 that is due to owner’s request. The same analysis was done for Amendment 1~b!.

For Amendment 2, a 1-year time extension was granted for the extra work in Amendment 1. The reasons are mostly consultant’s inability to complete the extra work. Time extension could have been included in Amendment 1, but were not, perhaps because 14 months had been already granted for the previous two informal extensions due to the consultant’s own failure to deliver on time. Amendment 3 was an additional impact analysis to study traf-fic operational impacts of various alternatives. The major alterna-tive was the preferential treatment of high-occupancy-vehicles ~HOV! within the study area. It was a new service not in the original scope, and hence an owner’s request.

After sorting the above reasons and adding their contributions to the cost/time increases, the percentages were posted in the second and third columns of Table 2. For example, the owner’s request increased cost by 44.3% for Case 1.

Schedule and Cost Increase Analysis

The draft and final reports were seriously delayed. The owner used such tones in a memo to the consultant: ‘‘We are extreme-ly disappointed that the . . . report has not been complet-ed, . . . schedule is now in jeopardy, . . . if we do not receive the report by . . . we will not process any future invoices for pay-ment.’’ The consultant responded with: ‘‘I . . . apologize for the Table 4. Analysis of Cost and Schedule Increases for Case 2

Amendment Reasons Contributions Cost increase

Time extension ~months!

1. Increased geotechnical work Owner’s request 1.0 $ 55,685 ~11.5%! 0

2. Marine survey $ 24,000 ~5%!5 0

Omission–owner 0.5 12,000 ~2.5%!1

Owner’s request 0.5 12,000 ~2.5%!

3. Supplemental services for EISa $209,374 ~43.3%!

5 0

Stakeholders 0.2 41,875 ~8.7%!1

Owner’s request 0.8 167,499 ~34.6%!

4. Supplement for EISa $194,906 ~40.3%!5 0

Stakeholders 0.2 38,981 ~8.1%!1

Owner’s request 0.8 155,925 ~32.2%!

5. Revised EDbtime 0 12 ~33%!5

Stakeholders 0.5 6 ~16%!1

delay.’’ One consultant’s review comment also stated ‘‘the lack of complete traffic information makes completing the environmental document on schedule very difficult.’’

Fig. 1 provides explanations for these delays. The upper six time scales show delays due to individual changes, and the rea-sons are listed under the delayed periods. The final report was sent in April 1993, way beyond the amended completion time of May 31, 1992.

The bottom of Fig. 1 shows cost expenditures versus time. The original contract amount was $400,000 for 3 years, and the actual total was $519,423 for more than 4 years. At the end of the first year, the actual cost was $240,416, under the budgeted cost of $341,150. This does not mean cost efficiency, because the cost expenditure was actually postponed due to consultant’s delays. The progress, in terms of cost, was only 46.3% ~$240,416/ $519,423!complete, which is much less than the planned 85%.

At the end of the third year, the actual cost was $483,105, which was over the contract amount $400,000. Cost was mainly spent in the first and the third years, as shown by the actual curve. The increased cost was due to reasons beyond the consultant’s control~Table 3!.

Grouping for Easier Use

The reasons for cost/time increases can be reclassified for spotting problems and tracing responsibility. Like construction, these

rea-sons can be grouped as compensable, nonexcusable, and excus-able~Barrie and Paulson 1992!. The new grouping is as follows: A. Mainly within the owner’s control~compensible!

Reason 1. Owner’s request a. Additional work b. Optimistic schedule c. Omissions

Reason 2. Owner’s failure a. Failure to provide information b. Incomplete or incorrect information c. Other consultants

B. Mainly within the consultant’s control~nonexcusable! Reason 3. Consultant’s failure

a. Consultant’s inability b. Underestimates or omissions

C. Beyond either the owner’s or consultant’s control~excusable! Reason 4. Growing needs

Reason 5. Stakeholders a. Agencies

b. Public c. Others

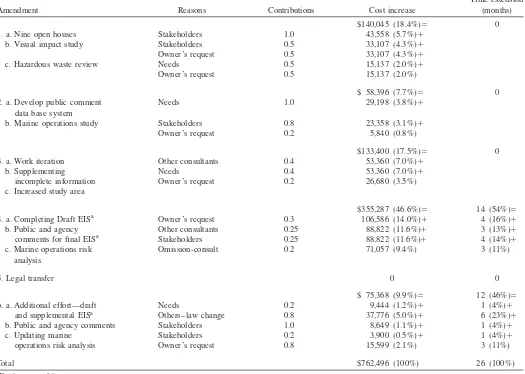

Owner’s request~reason 1!is a scope-related category. Addi-tional work@Reason 1~a!# occurs after engineering design starts. An optimistic schedule@Reason 1~b!#and owner omissions@ Rea-son 1~c!# are scope mistakes made before work is started. The Table 5. Analysis of Cost and Schedule Increases for Case 3

Amendment Reasons Contributions Cost increase

Time extension ~months!

$140,045 ~18.4%!5 0

1. a. Nine open houses Stakeholders 1.0 43,558 ~5.7%!1

b. Visual impact study Stakeholders 0.5 33,107 ~4.3%!1

Owner’s request 0.5 33,107 ~4.3%!1

c. Hazardous waste review Needs 0.5 15,137 ~2.0%!1

Owner’s request 0.5 15,137 ~2.0%!

$ 58,396 ~7.7%!5 0

2. a. Develop public comment data base system

Needs 1.0 29,198 ~3.8%!1

b. Marine operations study Stakeholders 0.8 23,358 ~3.1%!1

Owner’s request 0.2 5,840 ~0.8%!

$133,400 ~17.5%!5 0

3. a. Work iteration Other consultants 0.4 53,360 ~7.0%!1

b. Supplementing Needs 0.4 53,360 ~7.0%!1

incomplete information Owner’s request 0.2 26,680 ~3.5%!

c. Increased study area

$355,287 ~46.6%!5 14 ~54%!5

4. a. Completing Draft EISa Owner’s request 0.3 106,586 ~14.0%!

1 4 ~16%!1

b. Public and agency Other consultants 0.25 88,822 ~11.6%!1 3 ~13%!1

comments for final EISa Stakeholders 0.25 88,822 ~11.6%!

1 4 ~14%!1 c. Marine operations risk

analysis

Omission-consult 0.2 71,057 ~9.4%! 3 ~11%!

5. Legal transfer 0 0

$ 75,368 ~9.9%!5 12 ~46%!5

6. a. Additional effort—draft Needs 0.2 9,444 ~1.2%!1 1 ~4%!1

and supplemental EISa Others–law change 0.8 37,776 ~5.0%!1 6 ~23%!1

b. Public and agency comments Stakeholders 1.0 8,649 ~1.1%!1 1 ~4%!1

c. Updating marine Stakeholders 0.2 3,900 ~0.5%!1 1 ~4%!1

operations risk analysis Owner’s request 0.8 15,599 ~2.1%! 3 ~11%!

Total $762,496 ~100%! 26 ~100%!

a

three are listed under the owner’s request. Growing needs ~ Rea-son 4!refer to extra work not anticipated at the beginning. They can be regarded as unforeseen events that are excusable. Stake-holders~Reason 5!generally include government agencies@ Rea-son 5~a!#and the public@Reason 5~b!#. Others@Reason 5~c!#, such

as law changes or standard changes, are related to the stakeholder, so are merged under stakeholders.

It is then easier to remember that the owner’s request and owner’s failure are the two major reasons mainly within the own-er’s control; consultant’s failure is the reason within the consult-Table 6. Analysis of Hour and Schedule Increases for Case 4

Change in work scope Reasons Contributions Hour increase

Time extension ~months!

180 ~1.9%! 0

1. Stage I project work program, 8/12/91 Owner’s request 1.0

4,320 ~47%!5 0

2. Additional air quality study, 2/24/92 Needs 0.3 1,426 ~15.5%!1

Others–law change 0.7 2,894 ~31.5%!

1,620 ~17.6%! 0

3. Public participation, 2/24/92 Stakeholders 1.0

1,130 ~12.3%!5 10

4. Additional project management Stakeholders 0.4 452 ~4.9%!1

and administration, 5/29/92 Needs 0.4 452 ~4.9%!1

Other–standard change 0.2 226 ~2.5%!

320 ~3.5%! 0

5. Parking, circulation impact study, 5/29/92 Omission-consultant 1.0

320 ~3.5%!5 0

6. Update traffic operations Needs 0.5 160 ~1.7%!1

analysis using ABAGa1990, 12/21/92 Other–standard change 0.5 160 ~1.8%!

44 ~0.5%! 0

7. Additional visual aids, 8/14/92 Stakeholders 1.0

100 ~1.1%! 0

8. Ramp metering analysis, 12/21/92 Others–law change 1.0

1,159 ~12.6%!5 0

9. Design variation impact study, 3/16/93 Stakeholders 0.5 580 ~6.3%!1

Needs 0.5 579 ~6.3%!

Total 9,193 ~100%! 10

aAssociation of Bay Area Governments.

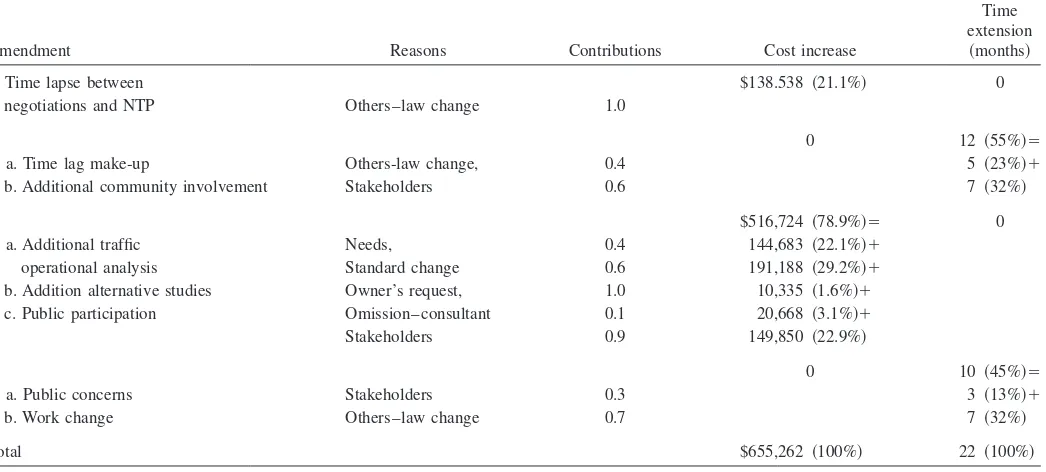

Table 7. Analysis of Cost and Schedule Increases for Case 4

Amendment Reasons Contributions Cost increase

Time extension

~months!

1. Time lapse between $138.538 ~21.1%! 0

negotiations and NTP Others–law change 1.0

0 12 ~55%!5

2. a. Time lag make-up Others-law change, 0.4 5 ~23%!1

b. Additional community involvement Stakeholders 0.6 7 ~32%!

$516,724 ~78.9%!5 0

3. a. Additional traffic Needs, 0.4 144,683 ~22.1%!1

operational analysis Standard change 0.6 191,188 ~29.2%!1

b. Addition alternative studies Owner’s request, 1.0 10,335 ~1.6%!1

c. Public participation Omission–consultant 0.1 20,668 ~3.1%!1

Stakeholders 0.9 149,850 ~22.9%!

0 10 ~45%!5

4. a. Public concerns Stakeholders 0.3 3 ~13%!1

b. Work change Others–law change 0.7 7 ~32%!

ant’s control; and other reasons are beyond either the owner’s or consultant’s control. If a reason occurs in Group A, the owner will compensate both cost and time. For Group B reasons, the consult-ant will absorb the cost and time. For Group C reasons, the time will be extended, but the cost will be absorbed by the consultant ~Kraiem and Diekmann 1987!.

Engineering design cost and schedule overruns are common. Problems generally arise from causes about which we are igno-rant, for which we lack information, or that we cannot control ~Ross 1995!. The three groups of reasons are consistent with the three causes. The reasons in Group A are usually the result of the owner’s ignorance, those in Group B occur when diagnosis infor-mation is lacking and Group C reasons are due to what we cannot control.

Conclusions

Identifying the reasons is usually the first step when addressing a problem, and then corrective action can be taken. Traditional con-trol systems detect project cost and schedule overruns, but seldom further identify the reasons causing this result. The identified rea-sons supplement control systems in analyzing the cause-effect relationship for an engineering design process. This analysis helps trace responsibility and improve the work process. With the cat-egorized reasons, the owner and consultant can have common understanding of cost and schedule change so the change order can be issued and settled with fewer disputes.

Appendix

In Case 2, The consultant was required to prepare an engineering study consisting of three technical reports: ~1!geometric design alternatives study,~2!location hydraulics study, and~3! geotech-nical impact assessment. These reports would be used to prepare environmental documents.

Seven amendments were signed~Table 4!. The first two were technical work scope increases. The third and fourth amendments were supplemental services provided during the environmental review. The supplemental services were originally written in the contract scope and amended as needed. Amendments 5, 6, and 7 were 3-year postponements of the environment document, due to requirements from agencies, residents, and regulation change. During this period, the consultant was used to supplement the owner staff.

After sorting the above reasons and calculating their contribu-tions to cost/time increases, the percentages were posted into the fourth and fifth columns of Table 2.

In Case 3, the consultant was required to assess the environ-mental impact of project alternatives, assist in coordinating the

technical studies being done by other consultants, and prepare the draft and final environmental document, project report, and other documents. The amendment analysis is shown in Table 5.

In Case 4, the consultant was required to prepare preliminary engineering drawings, estimates, project reports, environmental documents, and the project approval report. There were nine work changes as shown in Table 6. The change amount was calculated in work-hours. Later on, these work changes were incorporated into formal amendments, and the hours were transferred into dol-lars in Table 7.

References

Alarcon, L. F., and Ashley, D. B.~1992!. ‘‘Project performance modeling: A methodology for evaluating project execution strategies.’’Source Document 80, The Construction Industry Institute, Univ. of Texas at Austin, Austin, Tex.

Anderson, S. D., and Tucker, R. L.~1994!. ‘‘Improving project manage-ment of design.’’J. Manage. Eng.,10~4!, 35– 44.

Barrie, D. S., and Paulson, B. C.~1992!.Professional construction man-agement, McGraw-Hill, New York.

Blockley, D. I. et al. ~1986!. ‘‘Report of the working group on error control strategies.’’Modeling human error in structural design and construction, A. Nowark, ed., National Science Foundation, Washing-ton, D.C.

Bramble, B. B., and Cipollini, M. D.~1995!.National cooperative high-way research program synthesis of highhigh-way practice 214: Resolution of disputes to avoid construction claims, Transportation Research Board, National Research Council, Washington D.C.

Chalabi, A. F., Salazar, G. F., and Beaudin, B. J.~1986!. ‘‘Defining and evaluating input variables impacting design effectiveness. Research phase I.’’Report, The Construction Industry Institute, Univ. of Texas, Austin, Tex.

Eisenhardt, K. M.~1989!. ‘‘Building theories from case study research.’’ Acad. Manag. Rev.,14~4!, 532–550.

Kraiem, Z. M., and Diekmann, J. F.~1987!. ‘‘Concurrent delays in con-struction projects.’’J. Constr. Eng. Manage.,113~4!, 591– 602. Oglesby, C. H., Parker, H. W., and Howell, G. A. ~1989!.Productivity

improvement in construction, McGraw-Hill, New York.

Ross, T. J.~1995!.Fuzzy logic with engineering applications, McGraw-Hill, New York.

Sanvido, V., Grobler, F., Parfitt, K., and Guvenis, M. ~1992!. ‘‘Critical success factors for construction projects.’’J. Constr. Eng. Manage., 118~1!, 94 –111.

Smith, M. A.~1996!.Construction insurance, bonding, & risk manage-ment, W. J. Palmer, J. M. Maloney, and J. L. Heffron III, eds., McGraw-Hill, New York.

Sternbach, J. ~1988!. National cooperative highway research program synthesis of highway practice 137: Negotiating and contracting for professional services, Transportation Research Board, National Re-search Council, Washington D.C.