The Implementation of Smoke-free Law in Bali: Economic Impact among Hotels and Restaurants

dr. Ketut Suarjana, MPH

Background

• The high prevalence of smokers in Bali

(31.0%)

• Since 2012 Bali provincial government has

implemented provincial smoke-free law (Perda KTR) followed by smoke-free law at district level (9)

• Smoke-free law: 7 areas (Health, Education,

Background

• Compliance study in 2014 : overall

17,2% (hotels 11,7%, restaurants 2,3%)

• Bali as an international tourist

destination international standard of

the facilities (hotels and the restaurants)

• The compliance remains low : the

Aims

• To assess the economic impact of

smoke-free law implementation

among the hotels and restaurants in Bali

• To gain perception of employer and

employee regarding the

Methods

• The study is a case study (5 hotels

and 4 restaurants located at Denpasar and Badung district)

• Samples selected purposively,

involving 10 managers, 10 employees and 10 visitors

• Data collected: in-depth interview,

Result

• Most of samples (hotels and restaurants)

has implemented Perda KTR

• The implementation:

– Hotels: no smoking signage at stratetgic spots (lobby, pool, rooms), no ashtray

provision, guest rule including smoking ban and fine for the violation

– Restaurants: no smoking signage at

Result

• The managers and employee

perceived the implementation of the Perda KTR well.

• However, they also perceived the

importance of smoking room provision

• Visitors perceived the hotels and

restaurants has already implemented Perda KTR, and they fully agree to

Result

Since the law issued in 2011 then implemented in 2012, the number of visitors slightly decreased, then the number

increased significantly in the year after (2013 and 2014)

Tahun 20100 Tahun 2011 Tahun 2012 Tahun 2013 Tahun 2014 10000

Grafik 1.1 Gambaran Kunjungan Hotel Tahun 2010 - 2014

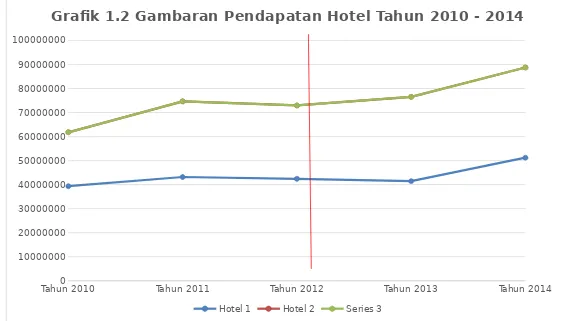

Result

Tahun 20100 Tahun 2011 Tahun 2012 Tahun 2013 Tahun 2014 10000000

Grafik 1.2 Gambaran Pendapatan Hotel Tahun 2010 - 2014

Hotel 1 Hotel 2 Series 3

Result

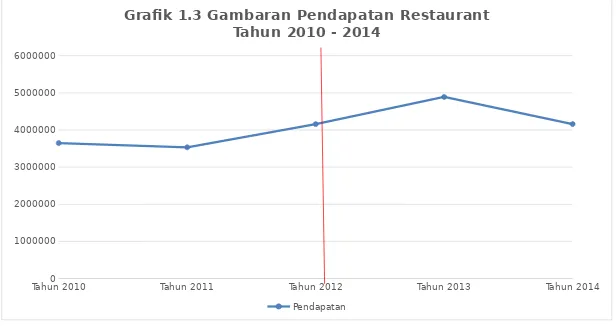

Tahun 20100 Tahun 2011 Tahun 2012 Tahun 2013 Tahun 2014 1000000

Grafik 1.3 Gambaran Pendapatan Restaurant Tahun 2010 - 2014

Pendapatan

The average of revenue in restaurant also fluctuating.

Result

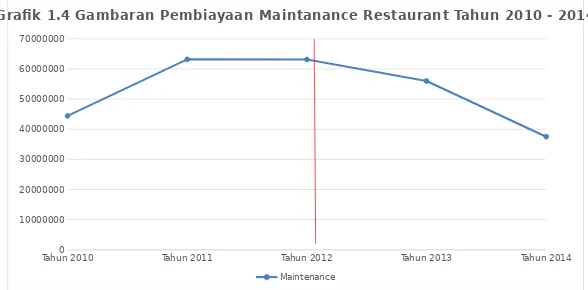

Tahun 20100 Tahun 2011 Tahun 2012 Tahun 2013 Tahun 2014 10000000

Grafik 1.4 Gambaran Pembiayaan Maintanance Restaurant Tahun 2010 - 2014

Maintenance

Conclusion

• The implementation of Perda KTR among

hotels and restaurants was vary

• The managers, employees and visitors

support the implementation of the Perda KTR in hotels and restaurants

• Regarding the economic impact, the

smoke-free law implementation has no relationship and even increases the

Policy Recommendation

• The managers should implement the

Perda KTR completely since its