l Equity Research l Indonesia l Health Care l

10 October 2014

Indonesia hospitals

Siloam’s l

ong-term growth potential is intact

In the recent South East Asia Hospital Development Summit, we spoke to management of six private hospitals in

Greater Jakarta. We also took the opportunity to visit reputed public hospitals and three other private hospitals.

Our key takeaways: (1) there is still pent-up demand for hospital services in Greater Jakarta;

(2) Siloam’s bed tariff

s

appear to be mid-priced despite its premium image; and (3) Siloam is the only Indonesian private hospital player with

the willingness and ability to deliver on an aggressive expansion plan of 6-8 hospitals per year.

High occupancy at mature private hospitals and their bed-tariff premiums over newer hospitals support a strong

long-term growth outlook for Siloam. Bed-tariff differential among hospitals is a fair indicator of price differences for

medical procedures, in our view, given

hospitals’

practice of charging patients based on bed-tiering.

Pent-up demand in Greater Jakarta

At first glance, the hospital market in Jakarta appears mature

with 2.3 beds per 1,000 population, comparable to Singapore

and Thailand

’s

2.0 and 2.2, respectively. Our discussions with

private hospital players indicate that mature hospitals in

Jakarta have an average occupancy of 70-80%. In contrast,

Siloam’s hospitals in Jakarta

averaged just 58% occupancy, as

of 1H14. We see headroom for growth here as

Siloam’s new

hospitals ramp up patient volumes in the next 3-5 years.

Ample scope for bed tariff hikes

Siloam’s bed tariffs are still lower than

tariffs at leading Jakarta

hospitals, despite its premium image. We estimate that

Siloam’s

peers charge a 7-27% premium over Siloam on tariffs

for SVIP, VIP Class I and Class II beds. Our survey reveals

that a heart bypass procedure costs 7-12% less at Siloam than

at the Medistra, Mitra Keluarga and Omni hospitals.

Dominant player in the making

Although there are many new entrants in the private hospitals

market, we believe Siloam is the only player with the ability

and willingness to deliver a rapid expansion of 6-8 hospitals

p.a. We see three key factors distinguishing Siloam from other

players: (1) its asset-light business model, (2) a strong pipeline

of 29 sites at various stages of development, and (3) its

organisational ability to manage/staff these new hospitals.

The bottom line

We maintain our In-Line rating on Siloam; our price target of

IDR 15,100 implies a 5% upside.

While the company’s long

-term outlook is positive, the stock appears fairly valued to us at

current levels. We would wait for a better entry point.

Siloam hospitals’ occupancy in Jakarta

Source: Company

Average bed tariff for SVIP and VIP - 2013

RSPP ~ Rumah Sakit Pusat Pertamina, RSPAD – Rumah Sakit Pusat Angkatan Darat Source: Companies, Asuransi Sinar Mas, Standard Chartered Research

56%

Did you know…

Most Indonesian hospitals have a

differential pricing policy for doctors, medicine and

procedures depending on bed class?

Pent-up demand for hospitals in Jakarta

Seemingly high concentration of beds

We estimate 2.3 beds per 1,000 population in Greater Jakarta, much higher than the

national average of 1.0. This bed ratio in Jakarta is comparable to those for

Singapore and Thailand at 2.2 and 2.0, respectively.

Figure 1: Hospital beds per 1,000 population

Despite high bed per 1,000

population ratio, private hospital

operators in Jakarta have an

average occupancy of 70-80%

Source: Frost & Sullivan, Ministry of Health, Standard Chartered Research

But occupancy indicates pent-up demand

Most hospital managers we met indicate an average occupancy of 70-80% as the

norm for their hospitals. We see this as a confirmation of the strong growth potential

for Siloam’s younger vintage hospitals.

Mature hospitals enjoy double-digit margins

Hospital operators also indicated that their EBITDA margin is at least 15%, with

larger network players and mid-to-upper segment players delivering 20-30%.

Siloam’s

management guided for its new hospitals to achieve an 18-20% EBITDA

margin from year 4. We estimate that

70% of Siloam’s bed capacity is still less

than

four years old in 2014. We think Siloam could potentially deliver similar margins,

comparable to those of mature private hospital operators, in the next 5-10 years.

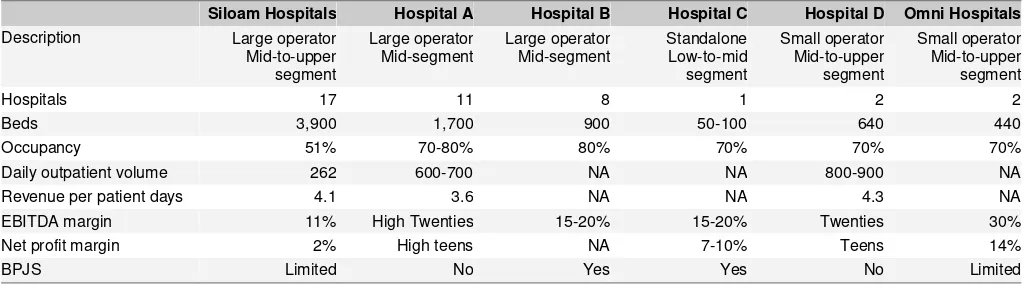

Figure 2: Key metrics of major private hospitals

Siloam Hospitals

Hospital A

Hospital B

Hospital C

Hospital D Omni Hospitals

Description

Large operator

Note: Private hospital players’ names are not disclosed. Source: Companies, Standard Chartered Research

3.0

China

US

UK

Jakarta Singapore Thailand Malaysia

India

Indonesia

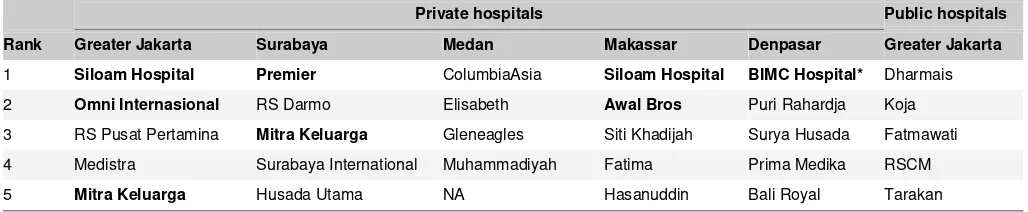

Preferred hospitals in Indonesia

Few leading players

A recent study by

Swa Magazine

, a business publication in Indonesia, named Siloam

as the top hospital brand in Greater Jakarta, Makassar and Surabaya (Siloam

acquired BIMC Hospitals in December 2013). Other network operators that were

named in the survey were Mitra Keluarga, Omni Hospitals (SAME IJ), Awal Bros and

Premier Hospitals.

Figure 3: Top-rated private and public hospitals in Indonesia

Private hospitals

Public hospitals

Rank

Greater Jakarta

Surabaya

Medan

Makassar

Denpasar

Greater Jakarta

1

Siloam Hospital

Premier

ColumbiaAsia

Siloam Hospital

BIMC Hospital*

Dharmais

2

Omni Internasional

RS Darmo

Elisabeth

Awal Bros

Puri Rahardja

Koja

3

RS Pusat Pertamina

Mitra Keluarga

Gleneagles

Siti Khadijah

Surya Husada

Fatmawati

4

Medistra

Surabaya International

Muhammadiyah

Fatima

Prima Medika

RSCM

5

Mitra Keluarga

Husada Utama

NA

Hasanuddin

Bali Royal

Tarakan

Source: Swa Magazine

Potential for strong occupancy ramp-up

We believe Siloam is well positioned to leverage pent-up demand for hospital

services in Greater Jakarta. Siloam’s hospitals in Jakarta had an average occupancy

of 51% in 2013. We believe the 70-80% occupancy at more mature private hospitals

in Jakarta indicates the potential for a strong ramp-

up at Siloam’s new hospitals in

the next five years.

Room for margin expansion

Premium image with mass pricing for Siloam

Despite its

‘premium’ image, our price survey indicates Siloam’s bed and

medical

procedure tariffs are either below or in line with those at leading hospitals in Greater

Jakarta. We surveyed the prices in five hospitals and used the room tariff data

tracked by the website Asuransi Sinar Mas.

Room tariff as a proxy to procedure costs

We view room tariffs as a proxy to procedure prices across hospitals, based on the

practice of Indonesian hospitals in applying differential pricing for procedures,

medical supplies, and nurs

es’

and doctors’ fees based on the patient’s ward

-class

choice

(also known as ‘bed

-

tiering’)

. Hospital CEOs we met at the conference

confirmed that differential pricing is standard practice across both public and private

hospitals in Indonesia.

Siloam’s b

ed tariffs are in the lower range

Siloam charges lower prices than most leading hospitals

Our study indicates that

Siloam’s bed tariffs across six different room types are still

in

the lower range of prices at nine leading hospitals in Greater Jakarta.

Siloam’s top

suite ranked fifth, at IDR 3mn per night, while its SVIP/VIP /Class I, II and III beds

ranked fourth or lower. We believe this indicates that there is room for further tariff

hikes given

Siloam’s

premium image.

Figure 6: Top suite tariff

Figure 7: SVIP tariff

Figure 8: VIP tariff

Source: Companies, Standard Chartered Research Source: Companies, Standard Chartered Research Source: Companies, Standard Chartered Research

Figure 9: Class I tariff

Figure 10: Class II tariff

Figure 11: Class III tariff

Source: Companies, Standard Chartered Research Source: Companies, Standard Chartered Research Source: Companies, Standard Chartered Research

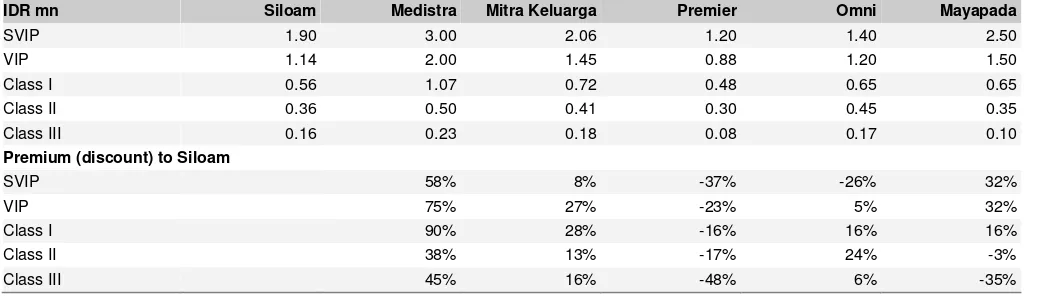

Competitively priced versus other private hospitals

We see Siloam largely as a mid-to-upper segment player with positioning similar to

that of Medistra, Premier, Mitra Keluarga Kelapa Gading (MKKG), Omni and

Mayapada hospitals.

Our analysis shows Siloam’s peers are charging, on average, 7

-27% more for SVIP, VIP Class I and Class II beds.

Cheaper than most mid-to-upper players:

Our study indicates

Medistra’s bed

tariffs are 38-90

% more expensive than Siloam’s bed tariffs. Similarly,

Mitra

Keluarga Kelapa Gading also charges an 8-28% premium over

Siloam’s tariffs

across the five bed classes. We note that MKKG is probably one of the few

hospitals in the Mitra Keluarga network that targets mid-to-upper segment

clientele, given its location in the affluent Kelapa Gading district. Omni and

Maypada largely charge a 5-32% premium over Siloam.

Charging a premium versus Premier:

Siloam is priced at a premium only to

Premier Hospital (affiliated to Ramsay Healthcare) whose rooms are at a 17-48%

discount to Siloam

’s

.

Mixed record for class III beds:

For class III beds, Medistra, MKKG and Omni

still charge a 6-48% premium to Siloam

’s

, while Premier and Mayapada priced a

35-48% discount to Siloam

’s

. However, class III beds make up the smallest

proportion of private hospitals’ bed capacity at 10

-15%.

Figure 12: Hospital bed tariff comparison for leading private hospitals

IDR mn

Siloam

Medistra

Mitra Keluarga

Premier

Omni

Mayapada

SVIP

1.90

3.00

2.06

1.20

1.40

2.50

Source: Companies, Standard Chartered Research

Figure 13: Medistra and Mitra Keluarga

–

Above Siloam

Figure 14: Premier, Mayapada and Omni

–

Mixed record

Source: Companies, Standard Chartered Research Source: Companies, Standard Chartered Research

58%

Siloam’s p

rocedure prices lower than competitors

’

Cheaper on more complex surgeries

We believe Siloam prices more complex procedures at lower rates than its peers.

Siloam’s heart

bypass surgery is 7-12% cheaper than that at Mitra Keluarga,

Medistra and Omni hospitals. Its angioplasty procedure is also 4-10% cheaper than

at its peers.

Still competitive on simpler procedures

In simpler procedures like C-sections and appendectomies

, Siloam’s pricing remains

24-29% below Medistra

’s

, which seems to be the most premium-priced player in the

market. We believe Siloam’s image

as a premium player could be due to its higher

pricing for high-volume procedures.

Figure 15: Comparison of procedure prices

Siloam’s

heart bypass procedure is

7-12% cheaper than its private

hospital peers

Source: Companies, Detik Health, Standard Chartered Research estimates

Figure 16: Procedure cost for C-section

Figure 17: Procedure cost for appendectomy

Source: Companies, Detik Health Source: Companies, Detik Health

Procedure price hikes could boost

Siloam’s

margins

We see three drivers of

Siloam’s lower margins: (1) its relatively lower pricing

; (2)

Siloam’s gross profit and EBIT margins

of 26% and 3%, respectively, in 2013 are still

the lowest among ASEAN hospital players.

Omni Hospital’s (SAME IJ) gross profit

margin of 49% and EBIT margin of 22% indicate

Siloam’s long

-term margin potential,

once the younger

‘

vintage

’

(under 4 years old) hospitals in its portfolio mature. Both

of Omni’s

hospitals are mature, with over 10 years

’

operating history.

Figure 18: Gross profit margin, 2013

Figure 19: EBIT margin, 2013

Source: Companies, Standard Chartered Research Source: Companies, Standard Chartered Research

Higher doctor fee-sharing policy

Siloam’s total expense

s-to-sales ratio was high at 97% in 2013, compared with 78%

for Omni. While start-up losses at its younger vintage hospitals are the primary

reason behind this,

we believe Siloam’s aggressive fee

-sharing arrangement for

doctors at 90-97% also plays a part. Most private hospitals we surveyed during the

conference indicated an 80-85% fee-

sharing arrangement. We see Siloam’s

aggressive offer as part of its bid to attract sufficient quality specialists for its

hospitals. We expect this to taper over time, closer to the market average of 85%.

Figure 20: Total expense to sales ratio, 2013

Figure 21: Total expenses breakdown, 2013

Source: Companies Source: Companies

We expect faster

‘

revenue intensity

’

growth in the long term

We believe Siloam could still increase its tariffs in the longer term, especially as its

hospitals mature. Management is guiding for a revenue intensity

(we define ‘intensity’

as revenue per patient) growth of 5-6% for its younger vintage hospitals and up to 8%

for its mature hospitals in the next 3-5 years. We believe this is conservative

compared with revenue intensity growth of 14% for KPJ Healthcare and 18% for

Bangkok Dusit Medical Services (Figure 22).

49%

Figure 22: Revenue intensity growth

Source: Companies, Standard Chartered Research

18%

14%

7%

6%

6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Bangkok Dusit

KPJ Healthcare

Bumrungrad

Hospital

Siloam Hospitals

Parkway Holding

Siloam

–

A dominant player in the making

Based on our conversations with major hospital operators during the conference, find

Siloam to be the only operator among the Indonesian private hospitals with the

willingness and ability to expand rapidly in the market today. We gauge willingness

based on the different players’ expansion

plans over the next few years, and ability

to

expand based on their capacity to fund and staff these new hospitals.

Most aggressive player in the market

During the conference, we noted that most hospital operators are not pursuing the

same scale of growth like Siloam. Siloam is planning to open 6-8 hospitals p.a. in

2015-17. In contrast, other network operators such as Mitra Keluarga, Awal Bros,

Ciputra Hospital and Eka Hospital are only aiming up to two hospitals p.a, according

to management. While Mitra Keluarga and Awal Bros both have sizeable operations

of 11 and eight hospitals, respectively, neither has expressed any plans to match

Siloam’s expansion

scale.

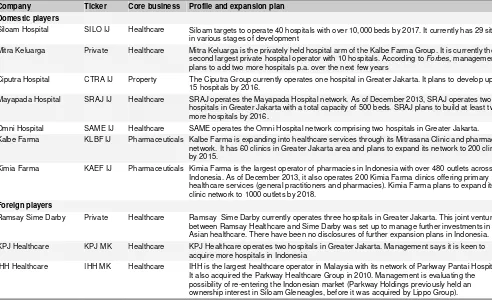

Figure 23: Expansion plans by major private hospital players

Company Ticker Core business Profile and expansion plan Domestic players

Siloam Hospital SILO IJ Healthcare Siloam targets to operate 40 hospitals with over 10,000 beds by 2017. It currently has 29 sites

in various stages of development

Mitra Keluarga Private Healthcare Mitra Keluarga is the privately held hospital arm of the Kalbe Farma Group. It is currently the

second largest private hospital operator with 10 hospitals. According to Forbes, management

plans to add two more hospitals p.a. over the next few years

Ciputra Hospital CTRA IJ Property The Ciputra Group currently operates one hospital in Greater Jakarta. It plans to develop up to

15 hospitals by 2016.

Mayapada Hospital SRAJ IJ Healthcare SRAJ operates the Mayapada Hospital network. As of December 2013, SRAJ operates two

hospitals in Greater Jakarta with a total capacity of 500 beds. SRAJ plans to build at least two more hospitals by 2016.

Omni Hospital SAME IJ Healthcare SAME operates the Omni Hospital network comprising two hospitals in Greater Jakarta.

Kalbe Farma KLBF IJ Pharmaceuticals Kalbe Farma is expanding into healthcare services through its Mitrasana Clinic and pharmacy

network. It has 60 clinics in Greater Jakarta area and plans to expand its network to 200 clinics by 2015.

Kimia Farma KAEF IJ Pharmaceuticals Kimia Farma is the largest operator of pharmacies in Indonesia with over 480 outlets across

Indonesia. As of December 2013, it also operates 200 Kimia Farma clinics offering primary healthcare services (general practitioners and pharmacies). Kimia Farma plans to expand its clinic network to 1000 outlets by 2018.

Foreign players

Ramsay Sime Darby Private Healthcare Ramsay Sime Darby currently operates three hospitals in Greater Jakarta. This joint venture

between Ramsay Healthcare and Sime Darby was set up to manage further investments in Asian healthcare. There have been no disclosures of further expansion plans in Indonesia.

KPJ Healthcare KPJ MK Healthcare KPJ Healthcare operates two hospitals in Greater Jakarta. Management says it is keen to

acquire more hospitals in Indonesia

IHH Healthcare IHH MK Healthcare IHH is the largest healthcare operator in Malaysia with its network of Parkway Pantai Hospitals.

It also acquired the Parkway Healthcare Group in 2010. Management is evaluating the possibility of re-entering the Indonesian market (Parkway Holdings previously held an ownership interest in Siloam Gleneagles, before it was acquired by Lippo Group).

Source: Companies, multiple news sources, Standard Chartered Research

An asset-light business model

Favourable asset-light model:

While some investors find this to be an

unorthodox business model for Asia hospitals, we believe Siloam’s asset

-light

Largely long-term turnover leases:

We find comfort in

Siloam’s

long-term lease

agreements between Siloam and its hospital land and building owners. These

lease agreements are locked for 15 years and operate largely on a turnover-rent

basis at a 1-3% progressive rate from year 1/year 2/year 3 onwards.

Figure 24: Siloam

’s

lease agreements

Hospital Owner

SH Lippo Cikarang First REIT 2025 (12 years) 12+15 Aggregate of a base rent and a variable rent determined by

hospital GOR

SH Sriwijaya Metropolis Propertindo Utama 2022 (9 years) 10+18 IDR 3bn for the first three years, IDR 3.5bn for 4th to 6th years and

IDR 4bn for 7th to 10th years

SH Cinere Anadi Sarana Tatahusada 2018 (5 years) 13+5 IDR 6.5bn p.a

SH Bali* First REIT 2028 (15 years) 15+15 1% of annual GOR in year 1, 2% in year 2 and 3% thereafter

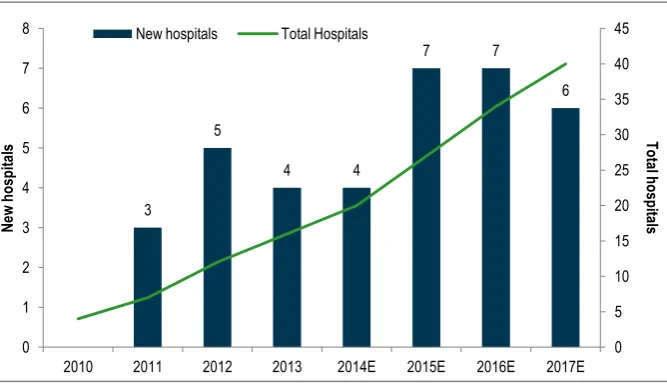

Siloam has a strong pipeline through 2017

Siloam management said it would complete four hospitals in 2014 versus its initial

target to complete 4-5 hospitals. Its Purwakarta hospital was opened in June, and it

plans to open two greenfield hospitals in Medan and Kupang in 4Q14. We believe the

company will potentially acquire one hospital in 2014. It has 29 sites in various stages

of development.

Figure 25:

Siloam’s pipeline

through 2017

Siloam is on track to expand its

network to 40 hospitals in 2017

from 17 hospitals currently. It has

29 sites in various stages of

development

Source: Company, Standard Chartered Research estimates

3

Is there a capital raising risk?

We note that Siloam will continue to report a negative FCF of IDR 408-626bn, as it

remains in an aggressive expansion mode until 2017. Assuming a 4-5 year ramp-up

per new hospital, we expect Siloam to begin delivering a positive FCF from 2018, as

more than half of its bed capacity is mature (year 4 and year 5) and achieves an

EBITDA margin of 17-18%.

Management indicated that capex could be funded by the following means: (1) a

shareholder loan from its parent, Lippo Karawaci; (2) divestment of existing

company-owned hospitals to First REIT; and (3) equity raising. Management

confirmed that there are still no plans for further equity raising from the market to

support its expansion plans.

Figure 26: Leverage and cash flow outlook

We believe net gearing could peak

in 2017, when the rapid expansion

phase is completed

Source: Company, Standard Chartered Research estimates

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

-1000

-500

0

500

1000

1500

2000

2500

2010

2011

2012

2013

2014E

2015E

2016E

2017E

2018E

N

et

g

ea

rin

g

ID

R

b

n

Maintain our In-Line rating on Siloam

While we continue to like Siloam’s long

-term outlook, we believe the stock is fairly

valued at current levels. Our DCF-based price target offers only a 5% potential

upside and implies 23x EV/EBITDA on 2015E. The stock trades at a 28% premium to

regional peers due to its market leadership and strong earnings growth outlook. We

would wait for a better entry point into Siloam.

Key potential downside risks could be: (1) slippage in delivering 6-8 hospitals p.a.;

and (2) slower-than-expected ramp-up at its younger vintage hospitals. We think

Siloam should be a core portfolio holding for Indonesia healthcare exposure, but we

recognise that its short listing history could be an issue for investors.

Figure 27: Asia hospitals

–

Peer comparison

Share prices as of 9 October 2014; Bloomberg consensus estimates for NR stocks Source: Bloomberg, Standard Chartered Research estimates

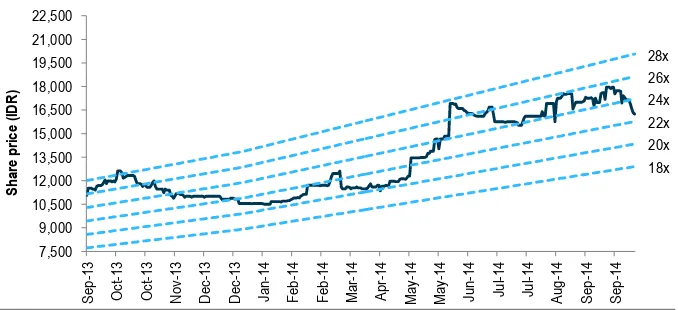

Strong valuation gain YTD

Siloam’s share price

has risen 52% YTD, making it one of the top performers within

our healthcare coverage universe (with Bumrungrad Hospital and Bangkok Dusit

Medical). The stock re-rated strongly in May after its inclusion in the Indonesia MSCI

Index.

Figure 28: Forward 12-month EV/EBITDA

Source: Bloomberg, Standard Chartered Research estimates

Positive longer-term outlook intact

While on a 12-month basis Siloam offers only a limited 6% potential upside, we

reiterate our positive view on its long-term potential. Over three years, we believe

Siloam could offer an average return of 13% p.a. assuming it trades at 15x

EV/EBITDA in 2017E. Meanwhile, over five years, we believe Siloam could deliver an

average return of 17% p.a., assuming it trades at 12x EV/EBITDA in 2019E. We

believe the next stage of re-rating could take place when Siloam proves its track

record in executing its plan to expand its hospital network to 40 hospitals in 2017

from 17 hospitals currently.

Figure 29: Siloam

–

3-year potential returns

Figure 30: Siloam

–

5-year potential returns

IDR bn

Enterprise value

24,534

Net debt

(1,378)

Minorities

(105)

Equity value

23,051

Outstanding shares

1.2

2017E fair value

19,938

2017E EV / EBITDA

15

Current share price

14,300

Share price return

39%

Share price return p.a.

12%

Cumulative dividend return p.a.

0%

Total return p.a.

12%

IDR bn

Enterprise value

36,597

Net debt

(1,378)

Minorities

(105)

Equity value

35,114

Outstanding shares (bn)

1.2

2019E fair value (IDR)

30,373

2019E EV / EBITDA

12

Current share price (IDR)

14,300

Share price return

112%

Share price return p.a.

16%

Cumulative dividend return p.a.

1%

Total return p.a.

17%

Siloam Hospitals Internasional

Income statement (IDR bn) Cash flow statement (IDR bn)

Year-end: Dec 2012 2013 2014E 2015E 2016E Year-end: Dec 2012 2013 2014E 2015E 2016E

Sales 1,788 2,504 3,421 4,995 7,273 EBIT 91 79 184 325 558

Gross profit 445 659 924 1,374 2,037 Depreciation & amortisation 120 202 288 429 582

SG&A (368) (583) (740) (1,049) (1,478) Net interest (14) (7) (27) (77) (141)

Other income 15 3 9 12 18 Tax paid (33) (27) (41) (64) (109)

Other expenses 0 0 0 0 0 Changes in working capital (45) (67) (88) (115) (167)

EBIT 91 79 184 325 558 Others 84 10 (10) (15) (22)

Net interest (5) (0) (27) (77) (141) Cash flow from operations 203 189 307 483 701

Associates 0 0 0 0 0

Other non-operational (9) (7) (10) (15) (22) Capex (523) (598) (716) (1,109) (1,221)

Exceptional items 0 0 0 0 0 Acquisitions & Investments (53) (163) 0 0 0

Pre-tax profit 77 72 147 233 395 Disposals 0 1 0 0 0

Taxation (25) (22) (41) (64) (109) Others 61 0 0 0 0

Minority interests (1) (0) (3) (5) (8) Cash flow from investing (515) (761) (716) (1,109) (1,221)

Exceptional items after tax 0 0 0 0 0

Net profit 50 50 104 164 278 Dividends 0 0 (10) (25) (56)

Issue of shares 0 0 0 0 0

Net profit adj. 50 50 104 164 278 Change in debt 320 (423) 500 500 500

EBITDA 212 281 473 754 1,140 Other financing cash flow 0 1,326 (200) (100) (50)

Cash flow from financing 320 904 290 375 394

EPS (IDR) 50 48 90 142 241

EPS adj. (IDR) 50 48 90 142 241 Change in cash 9 333 (119) (250) (125)

DPS (IDR) 0 5 9 21 48 Exchange rate effect 0 0 0 0 0

Avg fully diluted shares (mn) 1,000 1,047 1,156 1,156 1,156 Free cash flow (320) (409) (408) (626) (520)

Balance sheet (IDR bn) Financial ratios and other

Year-end: Dec 2012 2013 2014E 2015E 2016E Year-end: Dec 2012 2013 2014E 2015E 2016E

Cash 169 515 397 146 21 Operating ratios

Short-term investments 0 0 0 0 0 Gross margin (%) 24.9 26.3 27.0 27.5 28.0

Accounts receivable 187 271 375 547 797 EBITDA margin (%) 11.8 11.2 13.8 15.1 15.7

Inventory 75 95 137 198 287 EBIT margin (%) 5.1 3.1 5.4 6.5 7.7

Other current assets 26 26 50 72 103 Net margin adj. (%) 2.8 2.0 3.0 3.3 3.8

Total current assets 457 907 958 964 1,208 Effective tax rate (%) 32.5 30.1 27.5 27.5 27.5

Sales growth (%) 42.0 40.0 36.6 46.0 45.6 PP&E 865 1,402 1,834 2,518 3,161 Net income growth (%) 15.4 -1.2 107.7 58.1 70.0

Intangible assets 61 188 184 179 175 EPS growth (%) 15.4 -5.6 88.2 58.1 70.0

Associates and JVs 0 0 0 0 0 EPS growth adj. (%) 15.4 -5.6 88.2 58.1 70.0

Other long-term assets 203 103 103 103 103 DPS growth (%) - nm 88.2 137.1 126.7

Total long-term assets 1,129 1,693 2,120 2,800 3,439

Efficiency ratios

Total assets 1,586 2,601 3,079 3,763 4,647 ROE (%) 23.8 5.3 6.1 9.1 14.0

ROCE (%) 8.2 4.3 7.4 10.9 15.6

Short-term debt 16 17 17 17 17 Asset turnover (x) 1.3 1.2 1.2 1.5 1.7

Accounts payable 156 164 222 322 465 Op. cash/EBIT (x) 2.2 2.4 1.7 1.5 1.3

Other current liabilities 96 115 139 180 238 Depreciation/capex (x) 0.2 0.3 0.4 0.4 0.5

Total current liabilities 268 296 378 518 720 Inventory days 16.2 16.8 16.9 16.9 16.9

Accounts receivable days 31.8 33.4 34.4 33.7 33.7 Long-term debt 55 43 543 1,043 1,543 Accounts payable days 36.6 31.6 28.2 27.4 27.4

Convertible bonds 0 0 0 0 0

Deferred tax 0 0 0 0 0 Leverage ratios

Other long-term liabilities 1,019 623 423 323 273 Net gearing (%) -40.0 -27.8 9.4 48.6 72.9

Total long-term liabilities 1,074 666 966 1,366 1,816 Debt/capital (%) 5.4 2.6 20.7 32.7 39.7

Interest cover (x) 10.7 6.5 4.8 3.5 3.7

Total liabilities 1,342 962 1,343 1,884 2,536 Debt/EBITDA (x) 0.4 0.2 0.7 1.1 1.1

Current ratio (x) 1.7 3.1 2.5 1.9 1.7

Shareholders’ funds 245 1,639 1,735 1,879 2,110

Minority interests 0 0 0 0 0 Valuation

EV/sales (x) - 4.1 4.9 3.5 2.5

Total equity 245 1,639 1,735 1,879 2,110 EV/EBITDA (x) - 36.1 35.5 23.2 15.9

EV/EBIT (x) - 129.0 91.1 54.0 32.5

Total liabilities and equity 1,586 2,601 3,079 3,763 4,647 PER (x) - 209.2 160.4 101.5 59.7

PER adj. (x) - 209.2 160.4 101.5 59.7

Net debt (cash) (98) (456) 163 913 1,539 PBR (x) - 6.1 9.6 8.8 7.9

Disclosures appendix

The information and opinions in this report were prepared by Standard Chartered Bank (Hong Kong) Limited, Standard Chartered Bank Singapore Branch, Standard Chartered Securities (India) Limited, Standard Chartered Securities Korea Limited and/or one or more of its affiliates (together with its group of companies, ”SCB”) and the research analyst(s) named in this report. THIS RESEARCH HAS NOT BEEN PRODUCED IN THE UNITED STATES.

Analyst Certification Disclosure: The research analyst or analysts responsible for the content of this research report certify that: (1) the views expressed and attributed to the research analyst or analysts in the research report accurately reflect their personal opinion(s) about the subject securities and issuers and/or other subject matter as appropriate; and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views contained in this research report. On a general basis, the efficacy of recommendations is a factor in the performance appraisals of analysts.

Where “disclosure date” appears below, this means the day prior to the report date. All share prices quoted are the closing price for the business day prior to the date of the report, unless otherwise stated.

9,400

10,700

12,000

13,300

14,600

15,900

Oct-13

Jan-14

Apr-14

Jul-14

Oct-14

IDR

Recommendation and price target history for Siloam Hospital Internasional

1 2 3

Date Recommendation Price target Date Recommendation Price target Date Recommendation Price target

1 8 Apr 14 OUTPERFORM 13,982 2 25 Jun 14 IN-LINE 15,137 3 31 Jul 14 IN-LINE 15,100 Source: FactSet prices, SCB recommendations and price targets

2,325

2,810

3,295

3,780

4,265

4,750

Nov-11

Feb-12

May-12

Aug-12

Nov-12

Feb-13

May-13

Aug-13

Nov-13

Feb-14

May-14

Aug-14

Nov-14

IDR

Recommendation and price target history for Tempo Scan Pacific

1

Date Recommendation Price target Date Recommendation Price target Date Recommendation Price target

1 8 Apr 14 OUTPERFORM 3,878 Source: FactSet prices, SCB recommendations and price targets

Recommendation Distribution and Investment Banking Relationships

% of covered companies currently assigned this rating

% of companies assigned this rating with which SCB has provided investment banking services over the past 12 months

OUTPERFORM 55.6% 10.8%

IN-LINE 33.6% 9.4%

UNDERPERFORM 10.8% 9.7%

As of 30 September 2014

Research Recommendation

Terminology Definitions

OUTPERFORM (OP) The total return on the security is expected to outperform the relevant market index by 5% or more over the next 12 months IN-LINE (IL) The total return on the security is not expected to outperform or underperform the relevant market index by 5% or more over the next

12 months

UNDERPERFORM (UP) The total return on the security is expected to underperform the relevant market index by 5% or more over the next 12 months SCB uses an investment horizon of 12 months for its price targets.

Additional information, including disclosures, with respect to any securities referred to herein will be available upon request. Requests should be sent to [email protected].

any particular person. Any investments discussed may not be suitable for all investors. Users of this document should seek professional advice regarding the appropriateness of investing in any securities, financial instruments or investment strategies referred to in this document and should understand that statements regarding future prospects may not be realised. Opinions, forecasts, assumptions, estimates, derived valuations, projections, and price target(s), if any, contained in this document are as of the date indicated and are subject to change at any time without prior notice. Our recommendations are under constant review. The value and income of any of the securities or financial instruments mentioned in this document can fall as well as rise and an investor may get back less than invested. Future returns are not guaranteed, and a loss of original capital may be incurred. Foreign-currency denominated securities and financial instruments are subject to fluctuation in exchange rates that could have a positive or adverse effect on the value, price or income of such securities and financial instruments. Past performance is not indicative of comparable future results and no representation or warranty is made regarding future performance. While we endeavour to update on a reasonable basis the information and opinions contained herein, there may be regulatory, compliance or other reasons that prevent us from doing so. Accordingly, information may be available to us which is not reflected in this material, and we may have acted upon or used the information prior to or immediately following its publication. SCB is not a legal or tax adviser, and is not purporting to provide legal or tax advice. Independent legal and/or tax advice should be sought for any queries relating to the legal or tax implications of any investment. SCB and/or its affiliates may have a position in any of the securities, instruments or currencies mentioned in this document. SCB and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document and on the SCB Research website or have a material interest in any such securities or related investments, or may be the only market maker in relation to such investments, or provide, or have provided advice, investment banking or other services, to issuers of such investments. SCB has in place policies and procedures and physical information walls between its Research Department and differing public and private business

functions to help ensure confidential information, including ‘inside’ information is not disclosed unless in line with its policies and procedures and the rules of its regulators. Data, opinions and other information appearing herein may have been obtained from public sources. SCB makes no representation or warranty as to the accuracy or completeness of such information obtained from public sources. SCB also makes no representation or warranty as to the accuracy nor responsible for

any information or data contains on any third party’s website. You are advised to make your own independent judgment (with the advice of your professional advisers as necessary) with respect to any matter contained herein and not rely on this document as the basis for making any trading, hedging or investment decision. SCB accepts no liability and will not be liable for any loss or damage arising directly or indirectly (including special, incidental, consequential, punitive or exemplary damages) from the use of this document, howsoever arising, and including any loss, damage or expense arising from, but not limited to, any defect, error, imperfection, fault, mistake or inaccuracy with this document, its contents or associated services, or due to any unavailability of the document or any part thereof or any contents or associated services. This material is for the use of intended recipients only and in any jurisdiction in which distribution to private/retail customers would require registration or licensing of the distributor which the distributor does not currently have, this document is intended solely for distribution to professional and institutional investors.

Country-Specific Disclosures - If you are receiving this document in any of the countries listed below, please note the following:

United Kingdom and European Economic Area: SCB is authorised in the United Kingdom by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. This communication is not directed at Retail Clients in the European Economic Area as defined by Directive 2004/39/EC. Nothing in this document constitutes a personal recommendation or investment advice as defined by Directive 2004/39/EC. Australia: The Australian Financial Services Licence for Standard Chartered Bank is Licence No: 246833 with the following Australian Registered Business Number (ARBN: 097571778). Australian investors should note that this communication was prepared for “wholesale clients” only and is not directed at persons who are “retail clients”

as those terms are defined in sections 761G and 761GA of the Corporations Act 2001 (Cth). Bangladesh: This research has not been produced in Bangladesh. The report has been prepared by the research analyst(s) in an autonomous and independent way, including in relation to SCB. THE SECURITIES MENTIONED IN THIS REPORT HAVE NOT BEEN AND WILL NOT BE REGISTERED IN BANGLADESH AND MAY NOT BE OFFERED OR SOLD IN BANGLADESH WITHOUT PRIOR APPROVAL OF THE REGULATORY AUTHORITIES IN BANGLADESH. Botswana: This document is being distributed in Botswana by, and is attributable to, Standard Chartered Bank Botswana Limited which is a financial institution licensed under the Section 6 of the Banking Act CAP 46.04 and is listed in the Botswana Stock Exchange. Brazil:SCB disclosures pursuant to the Securities and Exchange Commission of Brazil (“CVM”) Instruction 483/10: This research has not been produced in Brazil. The report has been prepared by the research analyst(s) in an autonomous and independent way, including in relation to SCB. THE SECURITIES MENTIONED IN THIS DOCUMENT HAVE NOT BEEN AND WILL NOT BE REGISTERED PURSUANT TO THE REQUIREMENTS OF THE SECURITIES AND EXCHANGE COMMISSION OF BRAZIL AND MAY NOT BE OFFERED OR SOLD IN BRAZIL EXCEPT PURSUANT TO AN APPLICABLE EXEMPTION FROM THE REGISTRATION REQUIREMENTS AND IN COMPLIANCE WITH THE SECURITIES LAWS OF BRAZIL. Germany: In Germany, this document is being distributed by Standard Chartered Bank Germany Branch which is also regulated by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin).

Hong Kong: This document, except for any portion advising on or facilitating any decision on futures contracts trading, is being distributed in Hong Kong by, and is attributable to, Standard Chartered Bank (Hong Kong) Limited 渣打銀行 香港 有限公司 which is regulated by the Hong Kong Monetary Authority. India: This document is being distributed in India by Standard Chartered Securities (India) Limited, which is a SEBI-registered broker and a member of the Bombay Stock Exchange Limited and The National Stock Exchange of India Limited. Registered Address: 2nd Floor, 23-25 M. G. Road, Fort, Mumbai - 400 001. India | Telephone No: 022 - 6135 5999 | Fax No: 022 - 6135 5900| http://www.standardcharteredtrade.co.in | Email: [email protected]. | CIN: U65990MH1994PLC079263.

Indonesia: The information in this document is provided for information purposes only. It does not constitute any offer, recommendation or solicitation to any person to enter into any transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of likely future movements in rates or prices or represent that any such future movements will not exceed those shown in any illustration. Kenya: Standard Chartered Bank Kenya Limited is regulated by the Central Bank of Kenya. This document is intended for use only by Professional Clients and should not be relied upon by or be distributed to Retail Clients. Korea: