The Ind on esian Journal o f A cco u n tin g and B usiness S ociety 57

The Impact of Approved Accounting Standard AASB 1024

“Consolidated Accounts ” on the Information Included in

Consolidated Financial Statements

Bambang Agus Pramuka

D e p a rtm e n t o f A c c o u n ta n c yF a c u lty o f E c o n o m ic s, G e n e ral S o e d irm a n U n iv e rsity P u rw o k e rto , In d o n esia

Abstract

T h e in te n t o f c o n s o lid a te d f in a n c ia l s ta te m e n ts is to p r o v id e

m e a n in g f u l, r e le v a n t, u s e fu l, a n d r e lia b le in f o r m a tio n a b o u t th e o p e r a tio n s o f a g r o u p o f c o m p a n ie s . In c o m p lia n c e w ith A A S B 1 0 2 4 ’C o n s o lid a te d

A c c o u n t s ’, a n d A A S 2 4 C o n s o lid a te d F in a n c ia l R e p o r t s ’,a p a r e n t e n tity n o w h a s to in c lu d e in its c o n s o lid a te d f in a n c ia l s ta te m e n ts all c o n tr o lle d e n titie s , r e g a r d le s s o f th e ir le g a l fo rm o r th e o w n e r s h ip in te r e s t h e ld . T h e n e w S ta n d a r d a ls o p r o v id e s a n e w s ty le o f c o n s o lid a te d f in a n c ia l s ta te m e n ts f o rm a t, w h ic h r e q u ir e s a n in c r e a s e d d is c lo s u r e o f o u ts id e e q u ity in te r e s t ( O E I , f o r m e r ly m in o r ity in te r e s t) , e s p e c ia lly in th e B a la n c e S h e e t.

T h e p u r p o s e o f th is s tu d y is to d e te r m in e th e im p a c t o f A A S B 1 0 2 4 o n th e c o n s o lid a te d f in a n c ia l s ta te m e n ts o f e f f e c te d c o m p a n ie s . E x a m in a tio n o f th e f in a n c ia l s ta te m e n ts o f 5 2 c o m p a n ie s r e v e a ls th a t: ( 1 ) th e a d o p tio n o f A A S B 1 0 2 4 ( a n d A A S 2 4 ) d id s ig n if ic a n tly a lte r th e s tr u c tu r e a n d f o r m a t

o f th e b a s ic f in a n c ia l s ta te m e n ts , e s p e c ia lly th e B a la n c e S h e e t in te r m s o f d is c lo s in g th e O E I; a n d (2 ) th e a d o p tio n o f A A S B 1 0 2 4 ( a n d A A S 2 4 ) h a d n o s ig n i f ic a n t im p a c t o n th e c o n s o lid a te d f in a n c ia l fig u re s .

1. Introduction

In 1991, th e re w as an a m e n d m e n t to th e C o rp o ra tio n A c t to a d o p t d e fin itio n s u sed in th e 'A p p ro v e d A c c o u n tin g S ta n d a rd ' p re p a re d b y th e A u stra lia n

A c c o u n tin g S ta n d a rd s B o ard (A A S B ). In S e p te m b e r 1991, fo llo w in g th is a m e n d m e n t, A A S 24 w a s rev ise d an d reissu ed u n d e r A A S 24 “ C o n s o lid a te d F in a n c ia l R e p o rts ” , an d th e A A S B a lso rele ase d an A p p ro v e d A c c o u n tin g S ta n d ard A A S B 1024 “ C o n s o lid a te d A c c o u n ts ” , e ffe c tiv e fo r th e fin a n c ia l y e a r e n d e d o n o r a fte r 31 D e c e m b e r 1991. B o th S ta n d ard s a p p ly to a p a re n t e n tity w h ic h is a re p o rtin g e n tity ; h o w e v e r, w h ile A A S B 1024 a p p lie s to c o m p a n ie s , A A S 2 4 a p p lie s to all e n titie s o th e r th an c o m p a n ie s.

B a se d on c o m p a ris o n o f in fo rm a tio n c o n ta in e d in: (1 ) c o n s o lid a te d fin a n c ia l s ta te m e n ts p re p a re d fo r th e last fin a n c ia l y e a r b e fo re 31 D e c e m b e r 1991

5 8 T h e Im p act o f A p p ro v ed A cco u n tin g S tandard A A S B 1024 .

( th e re fo re in flu e n c e d b y p ro v is io n s o f “ o ld ” C o m p a n ie s C o d e /C o rp o ra tio n s A c t); (2 ) c o n s o lid a te d fin a n c ia l sta te m e n ts in (1 ) a b o v e re sta te d a c c o rd in g to A A S B 1024 a n d th e “ n e w ” C o rp o ra tio n s A ct; an d (3 ) c o n s o lid a te d a c c o u n ts p re p a re d fo r th e firs t fin a n c ia l y e a r e n d in g o n o r a fte r 31 D e c e m b e r 1991 (th e re fo re in flu e n c e d by p ro v is io n s o f A A S B 1024 a n d th e “ n e w ” C o rp o ra tio n s A c t); th e s tu d y e x a m in e s th e im p a c t th e A c c o u n tin g S ta n d ard on: (i ) in fo rm a tio n d is c lo s e d in fin a n c ia l s ta te m e n ts ; a n d (ii) re p o rte d fin a n c ia l fig u re s.

2. Literature review

B e fo re 31 D e c e m b e r 1991, th e re w a s n o a p p ro v e d a c c o u n tin g s ta n d a rd ' fo r c o n s o lid a tio n . T h e p re p a ra tio n o f fin a n c ia l s ta te m e n ts fo r g ro u p s c o m p a n ie s w a s g o v e rn e d b y th e p ro v is io n s o f th e

Companies A ct & Codes

a n d S c h e d u le 7 o f th e R e g u la tio n s to th e C o m p a n ie s C o d e . T h e se w e re th en re p la c e d b y th eCorporations

Law,

w h ic h b e c o m e o p e ra tiv e o n 1 Ja n u a ry 1991, an d S c h e d u le 5 o f th e C o rp o ra tio n R e g u la tio n s re sp e c tiv e ly .U n d e r s e c tio n 295 o f th e C o rp o ra tio n s L aw , th e D ire c to rs o f a (g ro u p ) h o ld in g c o m p a n y w e re re q u ire d to h a v e m ad e o u t, a t th e en d o f a fin a n c ia l y e a r, b e fo re th e d e a d lin e (th e d a te w h e re th e fin a n c ia l sta te m e n ts sh o u ld b e s ig n e d b y th e D ire c to rs ) o f th a t fin a n c ia l y e a r, 'g r o u p a c c o u n ts ' th at:

“ (a ) d e a l w ith :

(i) th e g r o u p ’s p ro fit o r lo ss fo r, and

(ii) th e g r o u p ’s sta te o f a ffa irs as a t th e en d of;

th a t fin a n c ia l y e a r o f th e c o m p a n y an d th e c o rre s p o n d in g fin a n c ia l y e a rs o f th e o th e r b o d ies c o rp o ra te in th e g ro u p ; and

(b ) g iv e a tru e a n d fa ir v ie w o f th e p ro fit o r lo ss an d state o f a ffa irs so far as th e y c o n c ern m e m b e rs o f th e c o m p a n y ” .

S u ch g ro u p a c c o u n ts a re in a d d itio n to th e a c c o u n ts o f th e h o ld in g c o m p a n y itself.

S e c tio n 74 o f th e C o rp o ra tio n s L aw , h o w e v e r, p ro v id e d r e lie f to w h o lly o w n e d 'A u s tr a lia ' h o ld in g c o m p a n ie s th a t w e re in co rp o ra te d in a n y S ta te o r T e rrito ry o f A u s tra lia , fro m th e re q u ire m e n t s to p rep a re g ro u p a c c o u n ts.

h o w e v e r, th e C o rp o ra tio n s L aw a llo w e d o n ly s u b s id ia rie s to be c o n s o lid a te d , a n d su b s id ia rie s w e re e ffe c tiv e ly d e fin e d as

companies

in w h ic h a g re a te r th a n 5 0 % sh a re h o ld in g w a s h eld . (S h a n a h a n 1989, p. 7 5 ) T h is p ro v isio n o p e n e d th e w a y to leav e a s se ts a n d lia b ilitie s o f f th e c o n s o lid a te d b a la n c e sh e e t b y k e e p in g th e m in (a) c o m p a n ie s in w h ic h o n ly 5 0 % o r less s h a re h o ld in g w a s h e ld , o r in (b ) n o n -c o rp o ra te b o d ie s su ch as tru s ts, p a rtn e rsh ip , a s so c ia tio n s a n d th e like.T he Indonesian Journ al o f A cco u n tin g an d B usiness Society 59

T h e C o rp o ra tio n s law a lso a llo w e d fo u r a lte rn a tiv e s re la tin g to 'g r o u p a c c o u n ts ': fu ll c o n s o lid a tio n , tw o o r m o re sets o r c o n s o lid a te d a c c o u n ts , in d iv id u a l a c c o u n ts , o r a c o m b in a tio n o f o n e o r m o re sets o f c o n s o lid a te d a c c o u n ts a n d o n e o r m o re se ts o f in d iv id u a l a c c o u n ts. E v en th o u g h S c h e d u le 5 re c o m m e n d e d a 'f u ll c o n s o lid a tio n ', th e a lte rn a tiv e s p ro v id e d h ad th e p o te n tia l to lead to d is s im ila ritie s in p ra c tic e .

M o re o v e r, th e law d id n o t c la rify th e c rite ria a n d c o n c e p t u s e d in c o n s o lid a tin g F in a n c ia l s ta te m e n ts. T h is led to c o n fu sio n in p ra c tic e , p a rtic u la rly in tre a tin g th e 'm in o r ity in te re s t' a n d 'in te r -e n tity tra n s a c tio n s .' (S h a n a h a n 1989 )

In late 1991, th e C o rp o ra tio n s L a w w a s a m e n d e d a n d A A S 2 4 /A A S B 1024 re issu e d a n d a p p ro v e d . U n d e r th e n e w S ta n d ard s a n d n e w le g isla tio n , c o n s o lid a te d a c c o u n ts a re n o w c o m p u ls o ry . T h e p re p a ra tio n o f o n e se t o f c o n s o lid a te d a c c o u n ts is th e o n ly fo rm a llo w e d fo r an e c o n o m ic e n tity w h ic h is a re p o rtin g e n tity . T h e

c h o ic e s p re v io u s ly g iv en b y th e L aw w ith re s p e c t to a lte rn a tiv e fo rm a ts o f th e g ro u p fin a n c ia l s ta te m e n ts h a v e n o w b een d e le ted .

F u th e rm o re , c o n tro l ra th e r th an o w n e rsh ip , is th e c rite ria w h ic h sh o u ld b e u se d to s h o w th e re la tio n s h ip b e tw e en a p a re n t e n tity a n d its su b s id ia rie s. A d e c is io n m u st b e m a d e as to W h e th e r e n titie s a re c o n tro lle d b e fo re b rin g in g th em in to th e c o n s o lid a tio n p ro c e ss. H o w e v er, s u b je c tiv ity in th e d e fin itio n o f c o n tro l m a y r e s u lt in d iffe re n t o p in io n s a b o u t a g iv en situ a tio n . I f less th a n 5 0 % o w n e rs h ip e x is ts a n d c o n tro l is said to e x ist, th e re a so n fo r d e c isio n m u st b e d is c lo s e d in th e a c c o u n ts . C o n v e rs e ly , i f m o re th an 5 0 % o w n e rs h ip e x ists a n d c o n tro l is sa id n o t to e x ist, th e re a so n m u st a lso be d isc lo se d . (C o m m e n ta ry , p a ra .(x ix ))

U n d e r th e n e w sta n d a rd s an d n ew le g isla tio n , c o n s o lid a te d a c c o u n ts fo r th e p a re n t c o m p a n y m u s t n o w in clu d e th e a sse ts, lia b ilitie s an d e q u itie s a n d e q u itie s o f a n y leg a l e n tity th a t th e c o m p a n y c o n tro ls, in c lu d in g tru s ts, p a rtn e rs h ip s o r o th e r e n titie s . T h e u se o f w h o lly o w n e d tru s ts to k e e p p ro je c ts o f f th e b a la n c e s h e e t is n o lo n g e r e ffe c tiv e . (C o rp o ra tio n s L aw , Sec. 2 9 4 A (5 ); S w in d e lls 19 91)

H o w e v e r, so m e e n titie s w h ic h w e re p re v io u s ly re q u ire d to p re p a re g ro u p a c c o u n ts a re n o lo n g e r re q u ire d to d o so. it is th e e x is te n c e o f u se rs d e p e n d e n t u p o n th e g e n e ra l p u rp o se fin a n c ia l re p o rts w h ic h c o n s titu te s a re p o rtin g e n tity . I f th e re a re n o su c h u se rs, th e re is n o re p o rtin g e n tity , an d n o re q u ire m e n t to c o n s o lid a te . T h is w ill b e th e c a se fo r m a n y e x e m p t p ro p rie ta ry h o ld in g c o m p a n ie s . (S w in d e lls

1991, p 7 )

60 T he Im pact o f A p p ro v ed A cco u n tin g S tandard A A S B 1024

3. Method

3 .1 . S a m p le

C o m p a n ie s in c lu d e d in th e rese a rc h a re th o se th a t w e re c la s s ifie d as th e 1991 to p 100 c o m p a n ie s ra n k e d b y th e B u sin e ss R e v ie w W e e k ly (B R W ) m a g a z in e . T h e B R W ( O c to b e r 18, 199 1) h as ran k e d th ese A u stra lia n c o m p a n ie s a c c o rd in g to th e ir re v e n e u s . T h e c h o ic e o f th e s e c o m p a n ie s as th e re se a rc h sa m p le is b a s e d on th e b e lie f th a t th e y a re larg e c o m p a n ie s w h ic h c a n be e x p e c te d to h a v e s u b s id ia rie s, su ch th a t th e y h a v e to p re p a re c o n so lid a te d fin a n c ia l sta te m e n ts.

3 .2 . T im e P e rio d

T h e tim e p e rio d c h o se n fo r th e rese a rc h w as th e last p e rio d to w h ic h th e 'o l d ' le g is la tiv e re q u ire m e n ts a p p lie d , an d th e firs t p e rio d th e A A S B 1024 a n d th e 'n e w ' le g is la tiv e re q u ire m e n ts b e c o m e o b lig a to ry . T h e 'o l d ' le g isla tiv e re q u ire m e n ts a p p lie d u n til 3 0 D e c e m b e r 1991, an d w e re th e n re p la c e d b y th e n e w r e q u ire m e n t a p p lic a b le fro m 31 D e c e m b e r 1991. T h e re fo re , th e fin a n c ia l s ta te m e n ts fo r th e s e tw o p e rio d s w e re req u ired .

3 .3 . A n a ly s is

T o fu lfill th e firs t o b je c tiv e o f th e stu d y , th e fin a n c ia l s ta te m e n ts w e re a n a ly s e d in te rm s o f th e ir c o n fo rm ity w ith th e 'o l d ' le g isla tiv e re q u ire m e n t (fo r p re- A A S B fin a n c ia l s ta te m e n ts ), an d A A S B 1024 an d 'n e w ' le g isla tiv e re q u ire m e n ts (fo r th e p o s t- A A S B 1024 fin a n c ia l sta te m e n ts). In p a rtic u la r, th e a n a ly s is fo c u se d o n th e c o n s e q u e n c e s o f th e m a in d iffe re n c e s b e tw e e n th e tw o re q u ire m e n ts .

A A S B 1024 a n d th e C o rp o ra tio n L a w d o n o t a p p ly to m o st e n titie s w ith in th e p u b lic se cto r. H o w e v e r, R e q u ire m e n ts re g a rd in g c o n s o lid a te d a c c o u n ts fo r p u b lic s e c to r e n titie s a re v e ry s im ila r to th o se fo r p riv a te s e c to r e n titie s (c o rp o ra tio n ), as p ro v id e d in A c c o u n tin g S ta n d ard A A S 2 4 an d re s p e c tiv e le g is la tiv e re q u ire m e n ts . F o r c o m p a ris o n p u rp o se s , th e p u b lic s e c to r o rg a n iz a tio n w e re a ls o a n a ly se d .

T o F u lfill th e s e c o n d o b je c tiv e o f th e stu d y , th e a n a ly s is w a s c o n d u c te d b y c o m p a rin g fin a n c ia l fig u re s o f c h o se n c o m p a n ie s as re p o rte d a t th e ir last p re -A A S B 10 24 fin a n c ia l re p o rt, w ith th e ir e q u iv a le n t fig u re s as re p o rte d in th e ir firs t p o st- A A S B 1024 fin a n c ia l re p o rt. F o r m o s t c o m p a n ie s, th e s e fig u re s h ad a lre a d y b een re s ta te d to c o m p ly w ith th e re q u ire m e n t o f A A S B 1024 fo r c o m p a ris o n p u rp o se w ith th e c u rre n t y e a r fig u re s. S o m e o f th e m , h o w e v e r, d id n o t re s ta te th e ir la st p re- A A S B 1024 fin a n c ia l fig u re s a c c o rd in g to A A S B re q u ire m e n ts . I f th is a d d itio n a l

Th e In donesian Journal o f A cco u n tin g and B usiness S ociety 61

in fo rm a tio n fo r th e s e e n titie s w as n o t a v a ila b le , th e y w e re e x c lu d e d fro m th e a n a ly sis.

T h e p u rp o se o f th is a n a ly sis is to e x a m in e th e c h a n g e s in fin a n c ia l fig u re s d u e to a p p lic a tio n o f A A S B 1024. F u rth e rm o re , to m e a su re th e s ig n ific a n c e o f th e c h a n g e s , a sta tis tic a l te s t w a s a p p lie d u sin g T -T est.

3 .4 . H y p o th e s e s

Null Hypothesis (Ho):

T h e a p p lic a tio n o f A A S B 1024 (an d A A S 2 4 ) an d n e w le g isla tiv e re q u ire m e n ts w o u ld n o t s ig n ific a n tly a ffe c t th e fin a n c ia l fig u re s re p o rte d in th e c o n so lid a te d fin a n c ia l sta te m e n t.

Alternate Hypothesis (Hi):

T h e a p p lic a tio n o f A A S B 1024 (a n d A A S 2 4 ) an d n e w le g isla tiv e re q u ire m e n ts w o u ld s ig n ific a n tly a ffe c t th e fin a n c ia l fig u re s re p o rte d in th e c o n s o lid a te d fin a n c ia l s ta te m e n ts.

4. Findings-1

4 .1 . C h a ra c te ris tic s o f th e sa m p le

O f th e to p 100 c o m p a n ie s in A u stra lia , 48 c o m p a n ie s h a v e b e e n e x c lu d e d fro m th e a n a ly s is. T h e re a so n s a re th a t 17 d id n o t re sp o n d an d fin a n c ia l s ta te m e n ts w e re

n o t a v a ila b le , w h ile th e re m a in in g 31 c o m p a n ie s, b ra n c h e s o r n o n -p a re n t e n titie s (6 c o m p a n ie s ); n o n -p a re n t e n tity p u b lic c o m p a n ie s (11 c o m p a n ie s ); n e w o r re o rg a n iz e d c o m p a n ie s (3 c o m p a n ie s ); an d 12 c o m p a n ie s w h ich h av e n o t p u b lish e d th e ir p o st- A A S B 10 24 fin a n c ia l sta te m e n ts. T h e c o m p a n ie s in clu d e d in th e a n a ly sis w ere, th e re fo re , 52 c o m p a n ie s ; b e in g 4 6 c o m p a n ie s w h ic h a re p riv a te se c to r c o rp o ra tio n an d 6 w h ic h a re p u b lic s e c to r en titie s.

4 .2 . S u b sid ia rie s

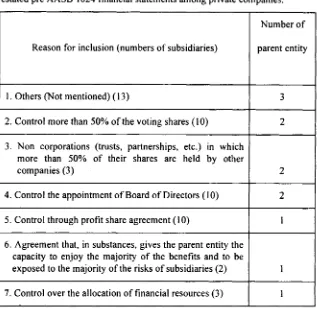

A n a ly s is th e tw o p o te n tia l d iffe re n c e s in th is a rea, th e re a re 14 e n titie s s p e c ific a lly a ffe c te d b y th e c h a n g e d d e fin itio n in A A S B 1024 an d n e w le g isla tio n re q u ire m e n ts , o f w h ic h o n e is a p u b lic se c to r e n tity . T h e s e c o m p a n ie s , 13 p riv a te c o m p a n ie s a n d o n e p u b lic c o m p a n ie s, h ad to in clu d e so m e su b sid ia rie s e x c lu d e d in th e ir o rig in a l p re -A A S B 1024 fin a n c ia l s ta te m e n ts in th e ir re s ta te d p re -A A S B 1024 fin a n c ia l sta te m e n ts , as m a n y as 41 e n titie s fo r th e p riv a te se c to r c o m p a n ie s a n d 81

62

T h e Im pact o f A p p ro v ed A c co u n tin g Standard A A S B 1024e n titie s fo r th e p u b lic s e c to r e n titie s. T h e re a so n s fo r in c lu sio n o f th e s e s u b s id ia rie s fo r th e p riv a te c o m p a n ie s a re sh o w n in th e T a b le 1:

Table 1. Reasons for including originally excluded subsidiaries in the

restated pre AASB 1024 financial statements among private companies.

Reason for inclusion (numbers o f subsidiaries)

N um ber o f

parent entity

1. Others (Not m entioned) (13) 3

2. Control m ore than 50% o f the voting shares (10) 2

3. Non corporations (trusts, partnerships, etc.) in which more than 50% o f their shares are held by other

companies (3) 2

4. Control the appointment o f Board o f Directors (10) 2

5. Control through profit share agreement (10) 1

6. Agreem ent that, in substances, gives the parent entity the capacity to enjoy the m ajority o f the benefits and to be

exposed to the majority o f the risks o f subsidiaries (2) 1

7. Control over the allocation o f financial resources (3) 1

T h re e o f th e s e 13 p riv a te se c to r c o m p a n ie s, an d a lso th e o n e p u b lic se c to r e n tity , d id n o t m e n tio n th e re a so n s fo r in clu d in g th e ir o rig in a lly e x c lu d e d s u b s id ia rie s fro m th e ir p re -A A S B 1024 (o r p re -A A S 2 4 fo r th e p u b lic c o m p a n y ) fin a n c ia l sta te m e n ts . T h is d o e s n o t c o m p ly w ith o n e o f th e d isc lo s u re re q u ire m e n ts o f A A S B 1024 a n d A A S 2 4 , th a t is, “th e id e n tity o f a n y s u b s id ia ry in w h ic h th e p a re n t e n tity h o ld an o w n e rs h ip [ in te re st a n d /o r v o tin g rig h ts o f 50 p e r c e n t o r less, to g e th e r w ith an e x p la n a tio n o f h o w c o n tro l e x is ts .” [e m p h a sis a d d e d ].

In a d d itio n , o n e p riv a te s e c to r c o m p a n y h e ld m o re th a n 5 0 % o w n e rs h ip in te re s t in a s u b s id ia ry w ith o u t h a v in g a n y c o n tro l o v e r th a t su b sid ia ry . T h e rea so n is th a t th e p a re n t e n tity c a n n o t e x e rc ise a m a jo rity o f th e v o tin g rig h ts a t m e e tin g s o f m e m b e rs o r d ire c to rs . A n o th e r p riv a te s e c to r c o m p a n y , o n th e o th e r h a n d , h a s

T he Indonesian Jou rnal o f A cco u n tin g and B usiness S ociety 63

c o n tro l o v e r 9 e n titie s th o u g h th e rig h t to a p p o in t th e B o a rd o f D ire c to rs, ev en th o u g h it d id n o t h o ld a n y o w n e rs h ip in te re st in th e c o n tro lle d e n titie s.

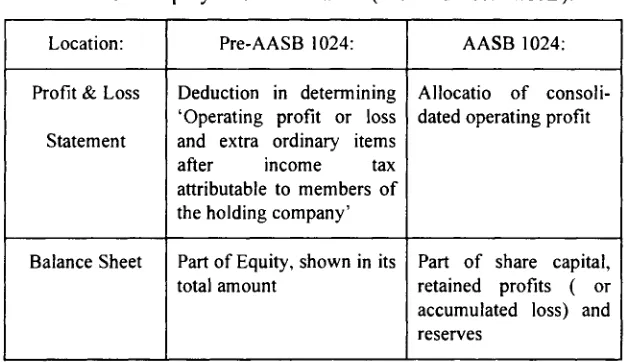

4 .3 . O u ts id e E q u ity In te re s t

(OEI)

T h e re a re tw o m ain p o in ts to be c o n s id e re d in re la tio n to d isc lo s u re re q u ire m e n ts fo r O E I: th e n a tu re o f d isc lo s u re in th e P ro fit a n d L o ss S ta te m e n t, an d in th e B a la n c e S h eet. T h e P re -A A S B 1024 b asic fo rm a t fo r fin a n c ia l s ta te m e n ts w e re p ro v id e d in S c h e d u le 5 to th e C o rp o ra tio n R e g u la tio n s, an d a ls o A A S B 1018: P ro fit a n d L o ss A c c o u n t. T h e fin a n c ia l s ta te m e n ts fo rm a t a c c o rd in g to A A S B 1024 is p ro v id e d in A p p e n d ix 3 o f th e sta n d a rd . H o w e v er, th e b a sic fo rm a t a c c o rd in g to S c h e d u le 5 an d A A S B 1018 h a v e n o t y e t b een a m e n d e d , ev en th o u g h th e S ta n d a rd s h a v e c o m e in to e ffe c t. S u m m a ry o f th e tw o re q u ire m e n ts re g a rd in g th is issu e is sh o w n in T a b le 2

T a b le 2. O u ts id e E q u ity In te re s t L o c a tio n (P re - an d P o st-A A S B ).

L o c a tio n : P r e - A A S B 1 0 2 4 : A A S B 1 0 2 4 :

P r o f it & L o s s

S ta te m e n t

D e d u c tio n in d e te r m in in g ‘O p e r a t in g p r o f it o r lo s s a n d e x tr a o r d in a r y ite m s

a f te r in c o m e ta x a t tr ib u ta b le to m e m b e r s o f th e h o ld in g c o m p a n y ’

A llo c a tio o f c o n s o li d a te d o p e r a tin g p r o f it

B a la n c e S h e e t P a r t o f E q u ity , s h o w n in its to ta l a m o u n t

P a r t o f s h a r e c a p ita l, r e ta in e d p r o f it s ( o r a c c u m u la t e d lo s s ) a n d r e s e r v e s

A n a ly s in g th e s e tw o m ain p o in ts, th e fin d in g s h a v e b e e n su m m a ris e d as sh o w n in T a b le 3. In o rd e r to fu lfil b o th S c h e d u le 5 an d A A S B 1024 re q u ire m e n ts , so m e c o m p a n ie s c o m b in e d th e s e tw o d iffe re n t fo rm a t re q u ire m e n ts — sh o w in g to ta l a m o u n t in th e B a la n c e S h e e t an P ro fit an L o ss S ta te m e n t, an d p ro v id e th e d e ta il in fro m o f N o te s.

64

Th e Im pact o f A p p ro v ed A cco u n tin g S tandard A A SB 1024 ...Table 3. Outside Equity Interests Location Distribution - Private Companies

. . _ g . —

Location o f Outside Equity Interest in:

Number o f companies

Pre-AASB

Reports

Post-AASB

Reports

Balance Sheet:

1. Does not appear. 12 10

2. Total amount (Schedule 5) 27 6

3. Total amount and Notes 7 24

4. Detail (AASB 1024 ) 0 6

Total 46 46

Profit & Loss Statem ent:

1. Does not appear 11 11

2. Deduction (Schedule 5) 34 34

3. Allocation (AASB 1024) 0 0

Total 46 46

In a d d itio n to th e in fo rm a tio n g iv en in T a b le 3, in th e p riv a te s e c to r s a m p le fo u r c o m p a n ie s h ad ‘w h o lly o w n e d s u b sid ia rie s a n d h e n c e th e y d id n o t sh o w a n y O E I in th e ir fin a n c ia l sta te m e n ts. T h e R e m a in in g tw o c o m p a n ie s sh o w O E I in th e ir P ro fit a n d L o ss A c c o u n t on a o n e lin e b a sis, W ith o u t g iv in g an y a d d itio n a l n o tes. H o w e v e r, th e y sh o w O E I in d e ta ile d a m o u n t a c c o rd in g to th e A A S 2 4 fo rm a t re q u ire m e n ts in th e ir B a la n c e S heet.

4 .4 . E lim in a tio n s

T h e ‘O ld ’ le g isla tio n d id n o t in d ic a te w h e th e r all th e a ffe c ts o f in te r-e n tity tra n s a c tio n s h o u ld b e e lim in a te d p a rtia lly o r to ta lly . A A S B 1024, h o w e v e r, c le a rly re q u ire s th a t all e ffe c ts o f in te r-e n tity tra n s a c tio n s b e e lim in a te d fu lly . A n a ly s is o f b o th p re -a n d p o s t-A A S B 1024 fin a n c ia l s ta te m e n ts, in b o th p riv a te an d p u b lic c o m p a n ie s , lea d s to th e c o n c lu sio n th a t all c o m p a n ie s e lim in a te d th e e ffe c t o f in te r e n tity tra n s a c tio n to ta lly .

Th e Indon esian Journal o f A ccountin g and B usiness S ociety 65

5. Findmgs-2:

T h is s e c tio n d isc u sse s th e c o m p a riso n o f th e 1991 p re -A A S B 1024 c o n s o lid a te d fin a n c ia l fig u re s w ith th e p o st-A A S B 1024 re sta te d c o n s o lid a te d fig u re s to d e te rm in e w h e th e r th e a p p lic a tio n o f A A S B 1024 an d th e n e w le g isla tiv e re q u ire m e n ts h ad a s ig n ific a n t im p act on th e rep o rted fin a n c ia l fig u re s.T h e fin a n c ia l

fig u re s in th e B a la n c e S h e e ts a n a ly se d w ere: C u rre n t A sse ts, T o tal A sse ts, C u rre n t L ia b ilitie s, T o tal L ia b ilitie s, and N e t A ssets. F in a n cia l fig u re s fro m th e P ro fit and L o ss S ta te m e n ts u sed fo r th e a n a ly sis w ere R e v e n u e s an d O p e ra tin g P ro fit A fte r T a x (O P A T ). T a b le 4., s u m m a rise s th e fin a n c ia l fig u re s as re p o rte d in th e B a la n ce S h e e ts an d P ro fit & L o ss S ta te m e n ts.

Table 4. Financial Figures in Balance Sheets and Profit & Loss Statements ($ 000)

No D e s c r ip tio n

P r iv a te

C o m p a n ie s P u b lic E n titie s

Descriptions MEAN STDEV MEAN STDEV

1 C urrent Assets

Original 1,088.555 899,455 1,283,630 1,165,675

Restated 1.088.456 899,559 1,283,630 1,165,675

2 Total Assets

Original 7,222.878 16,536,090 24,471,624 32,797,026

Restated 7,219,013 16,592,371 24,471.344 32,797,056

3 C urrent Liabilities

Original 1.191,027 1,431.881 1,860,040 1,494,150

Restated 1,186,601 1,428,579 1,860,040 1,494,150

4 Total Liabilities

Original 4,390,024 13,638,200 22,654,322 30,551,048

Restated 4,419.081 13,738,897 22,660,212 30,550,494

5 N et Assets

66 T he Im pact o f A pp ro v ed A ccountin g Stand ard A A S B 1024

Original 2,881.725 8.045.681 1.817,304 2,409,584

Restated 2,799.931 7.937,788 1.811,135 2,409,584

6 Revenues

Original 3,745.848 3.793.962 2,834,784 925,550

Restated 3,735,876 3.789.183 2,831.739 921,531

7 OPAT

Originial 51,516 533.024 275.922 448.029

Restated 49,264 527.104 273.215 449,922

A p p ly in g a T -T e st, th e T -v a lu e an d P -v a lu e fo r e ach e le m e n ts o f th e B a la n c e S h e e t an d P ro fit & L o ss S ta te m e n t a re rep o rte d in T a b le 5. T h e resu lt m e a n s th a t th e re is n o sig n ific a n t d iffe re n c e b e tw e en p re-A A S B an d re sta te d p o st- A A S B fin a n c ia l fig u re s rep o rte d in th e c o n so lid a te d fin a n c ia l sta te m e n ts.

T a b le 5. T - T e s t R e s u lt f o r C h a n g e s in B a la n c e S h e e t a n d P ro f it & L o s s S ta te m e n ts F ig u re s .

N o C h a n g e s in:

P riv a te C o m p a n ie s P u b lic E n titie s

T V a lu e P -V a lu e T V a lu e P -V a lu e

1. C u r r e n t A s s e ts 0 .0 8 0 .9 3 ** **

2 . T o ta l A s s e ts 0 .2 2 0 .8 3 1.00 0 .3 6

3. C u r r e n t L ia b ’s 1 .5 6 0 .1 3 ** **

4 . T o ta l L ia b ilitie s - 1 .2 0 0 .2 4 -1.00 0 .3 6

5. N e t A s s e ts 1.01 0 .3 2 1.00 0 .3 6

6. R e v e n u e s 1 .3 7 0 .1 8 1.23 0 .2 7

7. O p a t 0 .3 2 0 .3 2 1.00 0 .3 6

** N o C h a n g e s - - n o T - te s t

The Indon esian Jou rnal o f A cco u n tin g and B usiness Society 67

Attorney General Department. 1991. A ustralian C orporation & S ecurities Legislation: C orporation Law. 2nd Edition. Sydney: CCH Australia.