Full Terms & Conditions of access and use can be found at

http://www.tandfonline.com/action/journalInformation?journalCode=vjeb20

Journal of Education for Business

ISSN: 0883-2323 (Print) 1940-3356 (Online) Journal homepage: http://www.tandfonline.com/loi/vjeb20

Students' Approaches to Study in Introductory

Accounting Courses

Rafik Z. Elias

To cite this article: Rafik Z. Elias (2005) Students' Approaches to Study in Introductory Accounting Courses, Journal of Education for Business, 80:4, 194-199, DOI: 10.3200/ JOEB.80.4.194-199

To link to this article: http://dx.doi.org/10.3200/JOEB.80.4.194-199

Published online: 07 Aug 2010.

Submit your article to this journal

Article views: 84

View related articles

ducation researchers have examined the study approaches of university students. Specifically, their research has focused on what happens in the time between receipt of the information from the instructor and assessment. The stu-dent’s approach to study is an important determinant of learning (Biggs, 1987). Research findings generally have identi-fied two approaches to studying: deep and surface. On the one hand, a student using the deep approach has an intrinsic interest in the subject matter. The stu-dent relates ideas and conclusions to understand the subject matter thorough-ly. On the other hand, a student employ-ing a surface approach merely memo-rizes information to pass an exam (Biggs, 1978). Ramsden (1988) argued that students can change their study approach depending on many factors, such as the teaching style and the nature of the discipline under study.

My purpose in this study was to exam-ine the way in which students approach studying in introductory accounting courses. These courses are required of all business majors and some nonbusiness majors. Because the courses represent the first, and sometimes the last, expo-sure that many students have to account-ing, it is useful to examine how they approach their study in this discipline. I also examine how different demographic characteristics such as GPA, expected

level processing concentrated more on the meaning of the article compared with those using surface-level process-ing, who memorized key words. Biggs (1987) further examined the two study approaches and identified their distinc-tive characteristics. On the one hand, he found that students who used a deep approach to studying have an intrinsic interest in the material, and their objec-tive is to develop competence in the subject matter. In doing so, they relate ideas to other contexts and discover meaning by reading widely. On the other hand, Biggs found that students using a surface approach simply want to meet the minimum course expecta-tions. To avoid working more than nec-essary, they limit their studying to memorizing key concepts and key words to pass an examination.

Study Approaches and Learning

Researchers have investigated whether study approaches and learning are related. The general conclusion is that deep approaches are consistent with enhanced learning. Trigwell and Posser (1991) studied the relationship between study approaches and qualitative learn-ing outcomes. The results indicated that students using the deep approach achieved higher learning outcomes than did those using a surface approach.

E

ABSTRACT. Significant education research has focused on the study approaches of students. Two study approaches have been clearly identi-fied: deep and surface. In this study, the author examined the way in which students approach studying introduc-tory accounting courses. In general, he found that GPA and expected course grade were correlated positively with using the deep approach to studying. Compared with other business majors, accounting and nonbusiness majors used more deep and fewer surface approaches to studying. In addition, women and students who were more mature and senior employed the deep approach more often than did other students. The results have implications for the accounting instructor in these critical introductory courses.

class grade, gender, and age affect approaches to study. Identifying subsets of students who use deep strategies will be useful to the accounting instructor in structuring the class.

Approaches to Study

The concept of study approaches was originally introduced by Marton and Saljo (1976). They presented stu-dents with reading passages along with comprehension questions and found that comprehension of the major con-cepts was dependent upon whether a student used deep-level or surface-level processing. Students who used

deep-Students’ Approaches to Study in

Introductory Accounting Courses

RAFIK Z. ELIAS

California State University, Los Angeles Los Angeles, California

Kember, Charlesworth, Davies, McKay, and Scott (1997) presented students with cases and defined successful cases as those that increased students’ deep approach to studying. Ramsden (1992) and Marton and Saljo (1997) concluded that analytical skills are enhanced through the use of a deep-study approach. Biggs (1993) asserted that the use of a surface approach is inadequate because its purpose is to avoid failure. Similarly to previous researchers, in the present study I assume that a deep approach to studying is preferable to a surface approach because the former encourages learning.

Accounting Education and Study Approaches

The findings of education research have shown that study approaches dif-fer, depending on the discipline under study. Entwistle and Ramsden (1983) examined differences in study ap-proaches based on discipline. The results indicated that the deep approach was more evident in the arts and social sciences, whereas the examination of evidence was more characteristic of sci-entific disciplines. Ramsden (1988) also argued that study approach was a func-tion of the discipline and asserted that a student can adapt his or her study approach to fit the discipline. To test for discipline differences, Eley (1992) used a within-subjects design to measure whether a student changed study approach according to discipline. The tendency to use a surface approach was higher in accounting courses, whereas English classes fostered a deeper approach to learning.

More than a decade ago, the Account-ing Education Change Commission (AECC) issued its recommendations regarding accounting education in gen-eral and the introductory accounting course specifically. The commission overwhelmingly emphasized the need for the students to develop analytical and conceptual skills, rather than mem-orizing professional standards (AECC, 1990). The commission also empha-sized the importance of the first accounting courses for all business majors and advocated that these courses should teach the students to learn on

their own to give an accurate view of the accounting profession to all students (AECC, 1992). Sharma (1997) noted that fostering a deep approach to learn-ing among accountlearn-ing students was essential in implementing the commis-sion’s recommendations.

Factors Affecting Study Approaches

Researchers have obtained mixed results in their examinations of the rela-tionship between study approaches and GPA. Rose, Hall, Bolen, and Webster (1996) found no significant correlation between the deep or surface approaches and overall GPA for American psycholo-gy students. Davidson (2002) reached similar conclusions when examining American accounting students. However, Booth, Luckett, and Mladenovic (1999) found a significant correlation between the use of the surface approach and GPA among British accounting students. Holschuh (2000) investigated the rela-tionship between grades in an introducto-ry biology course and study approaches. The results indicated that students who performed better used more deep approaches and fewer surface approach-es compared with students who did not perform as well. I used these mixed results to formulate the following hypothesis in the null form:

H1: There is no significant correla-tion between overall GPA and class grade in Introductory Accounting and the surface and deep approaches to studying.

A significant amount of research has focused on whether demographic fac-tors influence study approaches. Studies regarding gender provided mixed results. For example, Wilson, Smart, and Watson (1996) found no differences in study approaches between male and female Australian accounting students. Rose et al. (1996) reached similar con-clusions in an examination of a sample of U.S. psychology students. However, Hassall and Joyce (1998), investigating U.K. accounting students, found differ-ences only with respect to the surface approach to studying. The men general-ly used surface approaches more often than did the women.

Age and maturity also have been

examined as possible predictors of study approaches. Richardson (1995) and Devlin (1996) concluded that nontradi-tional (older) students—those over 25 years of age—used the deep approach more often than did traditional (younger) students. Trueman and Hartley (1996) attributed these differences to better management of time by mature students compared with traditional students.

Auyeung and Sands (1994) examined whether high school accounting educa-tion predicted study approaches at the university level. Their results indicated a significant correlation between previ-ous accounting knowledge and the sur-face approach to studying in college, but they found no significant correlation with the deep approach.

Some researchers have investigated the learning approaches of accounting students and compared them with those of other majors. Gow, Kember, and Cooper (1994) examined changes in study approaches of Hong Kong accounting students over time. Their results revealed that students used fewer deep strategies in their 2nd year compared with their 1st. However, deep strategies increased in their 3rd and 4th years of study. Sharma (1997) exam-ined Australian accounting students’ study approaches and found that study approaches were generally in the “gray area” between surface and deep. How-ever, the students were more interested in acquiring necessary professional skills. Booth et al. (1999) also exam-ined Australian accounting students and compared them with students majoring in the arts, education, and the sciences. Their results showed that, compared with students in other majors, account-ing students used more surface and fewer deep learning approaches. Very little research has focused on differ-ences between accounting and other business majors in their study approaches.

The inconclusive results presented in previous research led me to formulate the following hypothesis in the null form:

H2: There are no differences between deep and surface approaches to learning based on gender, age, grade level, major, and prior accounting education among introductory accounting students.

Method

The sample for this study consisted of introductory accounting students in two accredited universities (one public and one private). I administered surveys dur-ing the last week of a semester to all sec-tions of Introduction to Financial Accounting and Introduction to Manage-rial Accounting. After disregarding incomplete surveys, I had data from a sample of 480 students in 14 different sections taught by eight different instruc-tors. There were no common exams in either university. The exams generally consisted of a combination of multiple-choice questions, exercises, and essays.

Nist and Diehl (1994) examined suc-cessful study strategies among college students. Using their conclusions, Holschuh (2000) developed an instru-ment to measure deep and surface study approaches and applied it in an investi-gation of the study approaches of intro-ductory biology students. The instru-ment consists of 45 questions about the use of textbooks, taking notes, studying, and use of available support. Twenty-eight questions measured deep study-ing, and 17 questions measured surface studying. Each respondent recorded the amount of the deep and surface study methods that he or she used during the semester.

The results of previous research have indicated that study approaches are situation-specific (Eley, 1992; Rams-den, 1988). Previous research in study approaches has relied on the Study Process Questionnaire (SPQ) developed by Biggs (1987). The SPQ originally consisted of three factors: deep, surface, and achieving, but research uncovered significant deficiencies in the instru-ment. Biggs, Kember, and Leung (2001) revised the instrument to include only two factors: deep and surface. However, the instrument is not intended for mea-suring study approaches in specific dis-ciplines. Rather, it measures study approaches in the student’s course of choice (Biggs et al.).

The instrument developed by Holschuh (2000) was designed specifi-cally for use in introductory biology courses. Every statement relating to study approach directs the student’s attention to the current discipline under

study. Because study approaches are domain and content specific (Garner, 1988), I modified the instrument by replacing “biology” with “accounting.” No other changes were made to the instrument.

Results

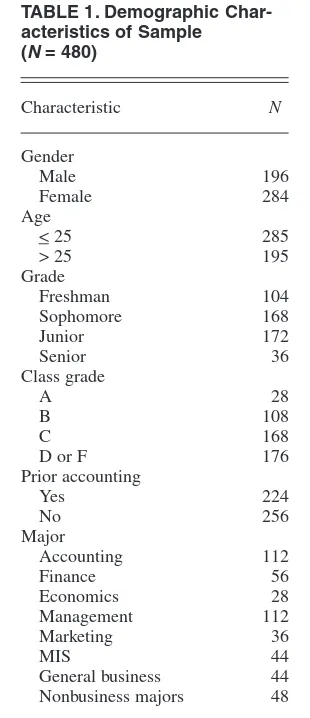

The first step in my data analysis was to test for any differences between the students at the two universities. A com-parison of the mean scores of deep and surface approaches revealed no signifi-cant differences. I therefore combined the two samples in the ensuing tests. In Table 1, I present the demographic char-acteristics of the sample.

Demographic characteristics reveal that the majority of the students were women, less than 25 years old, and accounting and management majors. In addition, about 45% of the students had learned accounting before taking the introduction to accounting classes, and most of the students expected to achieve a

C or a D in the introductory accounting courses.

To examine the relationship between overall GPA and study approach, I used correlation analysis between deep and surface approaches and overall GPA. The results indicated a significant positive correlation between the deep approach and GPA (r= .21,p< .001) and a nega-tive correlation between the surface approach and GPA (r= –.22,p< .001).

I used students’ self-reported expect-ed grades instead of actual grades for two reasons. First, I administered the survey 1 week before the end of the semester in many of the introductory accounting classes. Some of the instructors indicated that they had assigned voluntary extra-credit home-work to some students for submission after the survey. Some instructors also had comprehensive final exams, and others did not. Therefore, to account for different grading criteria and the possibility that some students’ grades could change significantly in the ensu-ing week compared with their current grades, I judged expected grades to be more accurate measures of perfor-mance. The use of expected class grades is also grounded in education and psychology research. Expected class grades have been used extensive-ly in research regarding teaching eval-uations (Greenwald & Gillmore, 1997). Goldman (1985) found that expected grades had a positive rela-tionship with instructor rating and overall value of the course. In addition, the social psychological theory of attri-bution holds that successful outcomes for one’s own behavior lead to positive beliefs about one’s abilities, and vice versa (Greenwald, 1980). Following this theory, Marks (2000) stated that expected grades were positively related to perceived learning. Expected grades, therefore, have theoretical and practi-cal advantages over actual grades in measuring students’ perceptions of learning. However, expected grades suffer from the possibility of overly optimistic expectations (Garavalia & Gredler, 2002). This disadvantage is a limitation of the present study. I used correlation analysis to investigate the relationship between study approach and expected class grade. My results

TABLE 1. Demographic Char-acteristics of Sample (N= 480)

showed a positive correlation between the deep-study approach and expected class grade (r = .25, p < .001) and a negative correlation between the sur-face approach and expected class grade (r= –.25,p< .001).

Correlation analysis also revealed a weak positive statistical correlation between the deep and surface approaches to studying (r= .07,p< .09). This result is consistent with the findings of Kember and Gow (1989), who concluded that stu-dents may sometimes employ both meth-ods in their studying, depending on the circumstances and required tasks. Rose et al. (1996) also found the same overlap between the deep and surface approaches and concluded that this finding indicated the ability of students to adapt to specific situations.

My next series of tests involved demographic differences. I used an analysis of variance (ANOVA) to exam-ine the effect of each factor on the deep and surface approaches, separately. I followed the ANOVA with t tests to compare the means of the significant factors. I present the ANOVA results and mean comparisons in Table 2.

All factors except for prior accounting knowledge were significant with regard to the deep-study approach. In general, female and nontraditional students used the deep approach more often compared with men and traditional students. Also, freshman students used the deep approach more often than did sopho-mores and juniors, but use of the deep approach increased again among seniors. There were significant differ-ences based on selected major. Account-ing and nonbusiness majors used the deep approach the most, whereas eco-nomics and general business majors used it the least.

In regard to the surface approach to studying, women and nontraditional students used it the least. Senior stu-dents used this approach the least, whereas freshmen and juniors used it the most. Students with prior account-ing education used the surface approach more often compared with those who were introduced to accounting in col-lege. I also found that economics, mar-keting, and general business majors used the surface approach more often compared with other majors.

Conclusions and Implications

My purpose in this study was to exam-ine the study approaches of undergradu-ate students in the introduction to accounting courses. My results generally

revealed that the deep approach to studying was positively correlated with expected course grade in these critical classes and with overall GPA. These results are positive from the instructor’s perspective. Because there were no

TABLE 2. Factors Affecting Deep and Surface Studying

ANOVA factor F M

Panel A. Deep approach

Gender 8.59**

Male 11.16**

Female 12.38**

Age 3.10*

< 25 11.58* > 25 12.31*

Grade 8.69**

Freshman 13.00** Sophomore 11.33** Junior 11.18** Senior 14.55** Accounting 2.30

Yes 12.21 No 11.59

Major 6.34**

Accounting 14.00** Finance 10.64** Economics 9.00** Management 11.92** Marketing 12.46** MIS 12.81** General business 9.54** Nonbusiness 13.25**

Panel B. Surface approach

Gender 9.91**

Male 5.30**

Female 4.65**

Age 17.15**

< 25 5.39** > 25 4.52** Grade 14.85**

Freshman 5.34** Sophomore 5.09** Junior 5.30** Senior 2.66** Accounting 11.33**

Yes 5.41** No 4.71**

Major 1.77*

Accounting 4.78* Finance 4.57* Economics 5.28* Management 5.25* Marketing 5.66* MIS 4.54* General business 5.54* Nonbusiness 5.08*

*Significant at the .10 level. **Significant at the .001 level.

common exams and eight different instructors were involved in teaching these courses, it seems that the exami-nations and other assessment methods required a deep understanding of the subject matter rather than memorizing key words. A future study could investi-gate more closely the relationship between study approaches and specific examination types. For example, Scouller (1998) found that multiple-choice questions typically encouraged Australian education students to use a surface approach to studying, whereas essay questions required a deeper approach. A similar study could be con-ducted in accounting. In the present study, I also found a slight correlation between the two approaches to study. This correlation means that a student can use a combination of surface and deep methods in a particular discipline (Marton & Saljo, 1997).

My results generally revealed that demographic factors were important determinants of study approach. Women used more deep strategies and fewer sur-face strategies, compared with men. These findings correspond with those of Hassall and Joyce (1998), who examined British accounting students. I also found that, compared with traditional students, nontraditional students used more deep and fewer surface strategies, a result sim-ilar to that of Devlin (1996), who attrib-uted it to better time management skills among nontraditional students. Also, in a finding similar to that of Gow et al. (1994), freshmen and seniors in my study used more deep approaches, com-pared with sophomores and juniors. Gow et al. attributed these results to the burnout effect and the fact that many 2nd- and 3-year students take more courses than they can handle. However, the results of the present study should be interpreted with caution because I did not conduct a longitudinal analysis.

It is interesting to note that students who learned accounting before taking these introductory courses used more surface strategies compared with those who were first exposed to accounting in college. A possible explanation is that the material was redundant for those who had already studied accounting, so they felt that they needed only to mem-orize keywords to pass the exams.

Further investigation of this variable is warranted, especially given that the accounting profession is attempting to attract qualified students from high school. My analysis of major differ-ences provided comforting results. Accounting majors used a deeper approach to studying compared with other business majors. The accounting instructor should emphasize to other majors the importance of accounting in their chosen fields. It is possible that these students did not value accounting in their career and therefore did not attempt to study it deeply.

Although the results of this study did not show that introductory accounting courses foster a deeper understanding of accounting, instructors should make more effort to foster this understanding among traditional students and other business majors. This emphasis is impor-tant in light of the major challenges fac-ing the accountfac-ing profession and the cri-sis of confidence in corporate reporting.

REFERENCES

Accounting Education Change Commission (AECC). (1990). Objectives of education for accountants: Position statement number one.

Issues in Accounting Education, 5,307–312. Accounting Education Change Commission

(AECC). (1992). The first course in accounting: Position statement number two. Issues in Accounting Education, 7,249–251.

Auyeung, P. K., & Sands, D. F. (1994). Predicting success in first-year university accounting using gender-based learning analysis. Accounting Education: An International Journal, 3,

259–272.

Biggs, J. B. (1978). Individual and group differ-ences in study processes. British Journal of Educational Psychology, 48, 266–279. Biggs, J. B. (1987). Students’ approaches to

learn-ing and studylearn-ing. Hawthorn, Vic.: Australian Council for Educational Research.

Biggs, J. B. (1993). From theory to practice: A cognitive systems approach. Higher Education Research and Development,12,73–85. Biggs, J. B., Kember, D., & Leung, D. Y. (2001).

The revised two-actor study process question-naire: R-SPQ-2F. British Journal of Education-al Psychology, 71,133–149.

Booth, P., Luckett, P., & Mladenovic, R. (1999). The quality of learning in accounting educa-tion: The impact of approaches to learning on academic performance. Accounting Education: An International Journal, 8,277–300. Davidson, R. A. (2002). Relationship of study

approach and exam performance. Journal of Accounting Education, 20,29–44.

Devlin, M. (1996). Older and wiser? A compari-son of the learning and study strategies of mature age and younger teacher education stu-dents. Higher Education Research and Devel-opment, 15,51–60.

Eley, M. G. (1992). Differential adoption of study

approaches within individual students. Higher Education, 23,231–254.

Entwistle, N. J., & Ramsden, P. (1983). Under-standing student learning. London: Croom Helm. Garavalia, L. S., & Gredler, M. E. (2002). An exploratory study of academic goal setting, achievement calibration and self-regulated learning. Journal of Instructional Psychology, 29,221–230.

Garner, R. (1988). Verbal-report data on cognitive and metacognitive strategies. In C. E. Wein-stein, E. T. Goetz, & P. A. Alexander (Eds.),

Learning and study strategies: Issues in assess-ment, instruction, and evaluation. San Diego, CA: Academic Press.

Goldman, L. (1985). The betrayal of the gate-keepers: Grade inflation. Journal of General Education, 37,97–121.

Gow, L., Kember, D., & Cooper, B. (1994). The teaching context and approaches to study of accountancy students. Issues in Accounting Education, 9,118–130.

Greenwald, A. (1980). The totalitarian ego: Fabri-cation and revision of personal history. Ameri-can Psychologist, 35,603–618.

Greenwald, A., & Gillmore, G. M. (1997). Grad-ing leniency is a removable contaminant of stu-dent ratings. American Psychologist, 52,

1,209–1,217.

Hassall, T., & Joyce, J. (1998). Floating on the surface or in the deep end? Management Accounting, 76,46–50.

Holschuh, J. P. (2000). Do as I say, not as I do: High, average, and low-performing students’ strategy use in biology. Journal of College Reading and Learning, 31,94–108.

Kember, D., Charlesworth, M., Davies, H., McKay, J., & Scott, V. (1997). Evaluating the effectiveness of educational innovations: Using the study process questionnaire to show that meaningful learning occurs. Studies in Educa-tional Evaluation, 23,141–157.

Kember, D., & Gow, L. (1989). A model of stu-dents, approaches to learning encompassing ways to influence and change approaches.

Instructional Science, 18,263–288.

Marks, R. B. (2000). Determinants of student evaluations of global measures of instructor and course value. Journal of Marketing Education, 22,108–119.

Marton, F., & Saljo, R. (1976). On qualitative dif-ferences in learning: I. Outcome and process.

British Journal of Educational Psychology, 46,

4–11.

Marton, F., & Saljo, R. (1997). Approaches to learning. In F. Marton, D. Hounsell, & N. Entwistle (Eds.),The experience of learning: Implications for teaching and studying in high-er education. Edinburgh: Scottish Academic Press.

Nist, S. L., & Diehl, W. (1994). Developing text-book thinking (3rd ed.). Lexington, MA: Heath. Ramsden, P. (1988). Context and strategy: Situa-tional influences on learning. In R. E. Schmeck (Ed.),Learning strategies and learning styles.

New York, NY: Plenum Press.

Ramsden, P. (1992). Learning to teach in higher education. London: Routledge.

Richardson, J. T. (1995). Mature students in high-er education: II. An investigation of approaches to studying and academic performance. Studies in Higher Education, 20,5–17.

Rose, R. J., Hall, C. W., Bolen, L. M., & Webster, R. E. (1996). Locus of control and college stu-dents’ approaches to learning. Psychological Reports, 79,163–171.

Scouller, K. (1998). The influence of assessment

method on students’ learning approaches: Multi-ple choice question examination versus assign-ment essay. Higher Education, 35,453–472. Sharma, D. S. (1997). Accounting students’

learn-ing conceptions, approaches to learnlearn-ing, and the influence of the learning-teaching context on approaches to learning. Accounting

Educa-tion: An International Journal, 6,125–146. Trigwell, K., & Posser, M. (1991). Relating

approaches to study and quality of learning out-comes at the course level. British Journal of Educational Psychology,61,265–275. Trueman, M., & Hartley, J. (1996). A

compari-son between the time-management skills and

academic performance of mature and tradi-tional-entry university students. Higher Edu-cation, 32,199–215.

Wilson, K. L., Smart, R. M., & Watson, R. J. (1996). Gender differences in approaches to learning in first-year psychology students. British Journal of Educational Psychology, 66,59–71.