Full Terms & Conditions of access and use can be found at

http://www.tandfonline.com/action/journalInformation?journalCode=vjeb20

Download by: [Universitas Maritim Raja Ali Haji] Date: 11 January 2016, At: 21:02

Journal of Education for Business

ISSN: 0883-2323 (Print) 1940-3356 (Online) Journal homepage: http://www.tandfonline.com/loi/vjeb20

Lower Level Prerequisites and Student

Performance in Intermediate Business Courses:

Does It Matter Where Students Take Their

Principles Courses?

Clifton T. Jones , Mikhail S. Kouliavtsev & Jack R. Ethridge Jr.

To cite this article: Clifton T. Jones , Mikhail S. Kouliavtsev & Jack R. Ethridge Jr. (2013) Lower Level Prerequisites and Student Performance in Intermediate Business Courses: Does It Matter Where Students Take Their Principles Courses?, Journal of Education for Business, 88:4, 238-245, DOI: 10.1080/08832323.2012.688777

To link to this article: http://dx.doi.org/10.1080/08832323.2012.688777

Published online: 20 Apr 2013.

Submit your article to this journal

Article views: 98

View related articles

ISSN: 0883-2323 print / 1940-3356 online DOI: 10.1080/08832323.2012.688777

Lower Level Prerequisites and Student Performance

in Intermediate Business Courses: Does It Matter

Where Students Take Their Principles Courses?

Clifton T. Jones, Mikhail S. Kouliavtsev, and Jack R. Ethridge, Jr.

Stephen F. Austin State University, Nacogdoches, Texas, USAAnecdotal evidence suggests that those students who take their lower level business principles courses at junior or community colleges are less prepared for success in intermediate business courses than their classmates who take them at a 4-year institution. Using data on student performance in four typical intermediate business courses—Intermediate Microeconomics, Intermediate Macroeconomics, Intermediate Business Statistics, and Intermediate Financial Accounting I—the authors found that average student performance in these courses is essen-tially completely determined by the underlying academic quality of the student, as measured by grade point average. Where they take their lower level prerequisite courses, and what letter grade they earn in those courses, do not generally play a significant role.

Keywords: accounting, economics, intermediate, principles, statistics, student performance, transfer

The growing national concern over the rapid rise in under-graduate tuition rates at four-year higher education insti-tutions in the United States in recent years has led some observers to encourage students to attend less expensive two-year junior or community colleges for completion of their lower level courses before transferring to a senior college or university for completion of their bachelor’s degree. The Obama Administration has been a very vocal advocate of greater enrollment in community colleges for both termi-nal vocatiotermi-nal training as well as a cheaper stepping stone to an eventual bachelor’s degree.1 However, many faculty

teaching intermediate business courses may have seen anec-dotal evidence that students who choose to take their lower level business prerequisites at two-year colleges are often less well prepared as compared to their classmates who take those same lower level courses at a four-year institution. As faculty in an Association to Advance Collegiate Schools of Business (AACSB)–accredited college of business, we have even heard some of our business students who took their

Correspondence should be addressed to Clifton T. Jones, Stephen F. Austin State University, Department of Economics & Finance, P.O. Box 13009, SFA Station, Nacogdoches, TX 75962-3009, USA. E-mail: [email protected]

lower level business courses at a two-year college say that they did not learn as much as did their peers who took those courses at our university. These students often acknowledge that while the courses taken at the two-year college were less expensive, they may not have provided them with the same foundation for success in their upper level business courses. One of our accounting students who took her principles of ac-counting courses at a local junior college opined that perhaps she had simply “gotten what she paid for,” and was thereby forced to work harder to catch up with her classmates in her intermediate accounting courses.

Using actual student data, rather than just anecdotal exam-ples, this study attempts to quantitatively determine the extent to which students who take certain of their lower level pre-requisites at a two-year college tend to perform more poorly in intermediate business courses than those who took their lower level prerequisites at a four-year institution. If there is a systematic difference in student performance between these two groups, then it may be wise to encourage those junior college students who plan on earning a bachelor’s degree in business to wait and take their lower level business prereq-uisites after they have transferred to a four-year institution. On the other hand, if there is no systematic difference, then taking one’s lower level prerequisites at a two-year college could be an attractive option for some business students.

PREREQUISITES AND PERFORMANCE IN INTERMEDIATE COURSES 239

REVIEW OF LITERATURE

There exists a vast literature on those factors that enhance stu-dent success in undergraduate business courses. These stud-ies often seek to identify pedagogical strategstud-ies for improv-ing student success, while recognizimprov-ing differences in student demographic characteristics such as age, gender, ethnicity, and major, among other things. In this review we focus on only those previous studies which relate directly to the issue addressed in our analysis.

Colley, Volkan, Drucker, and Segal (1996) published one of the only empirical studies that directly tested the differen-tial impact on student performance in an intermediate busi-ness course of taking lower level prerequisites at a two-year college versus a four-year institution. They regressed student letter grade performance in Intermediate Financial Account-ing I on the student’s average letter grade across the two prin-ciples of accounting courses, running separate regressions on transfer students (those who took both principles courses at a junior college) and nontransfer students (those who took both principles courses at the same university where they took Intermediate Financial Accounting I). Students who took only one of the principles courses at a junior college were excluded from the analysis, as well as those who took either principles course more than once. Using data from three different universities, they found that the nontransfer students’ average letter grade in principles did have a statis-tically significant impact on their letter grade in Intermediate Financial Accounting I at all three universities; the estimated impacts implied an increase of 0.71 to 0.90 letter grades for each one letter grade increase in the average principles grade. However, the same analysis for transfer students only found a significant impact at one of the three universities. Comparing this estimated impact for transfer students to that for nontransfer students at the same university implied that nontransfer students would perform between one half to one full letter grade higher in Intermediate Financial Accounting I, assuming the same average letter grade in their principles courses. It is to be noted that this regression analysis did not include any other explanatory variables beyond the average principles grade and a constant term.

Von Allmen (1996) examined the link between student performance in lower level prerequisite courses in economics and calculus and subsequent performance in intermediate microeconomics. He found that a student’s performance in the Principles of Economics course (combined micro/macro) and the calculus course had a significant impact on their performance in intermediate microeconomics, along with their grade point average (GPA) and class rank. Zanakis and Valenzi (1997) looked at student performance in an under-graduate business statistics course and found that the stu-dents’ anxiety about statistics and mathematics in general influenced their performance, as well as their prior GPA. Borde (1998) analyzed student performance in an introduc-tory marketing course (typically taught as an upper level

course) and found that a students’ GPA was the single most important factor in determining their performance.

Huang, O’Shaughnessy, and Wagner (2005) studied stu-dent performance in Intermediate Financial Accounting I relative to a prerequisite change that required students to take a third, one-hour introductory accounting course or pass a pretest, both of which were focused on the accounting cycle. This prerequisite change was introduced in response to the American Accounting Association Accounting Ed-ucation Change Commission (1992) position statement that encouraged a shift in focus in the traditional accounting prin-ciples courses from a preparer’s approach to that of a user’s approach. Their results suggested that a student’s grades in the two user-focused accounting principles courses may not be a very effective measure of their potential for success in Intermediate Financial Accounting I, especially if many of the students take their accounting principles courses at a two-year college.

The exhaustive reviews of the accounting education lit-erature conducted periodically by Watson, Apostolou, Has-sell, and Webber (2007) and Apostolou, HasHas-sell, Rebele, and Watson (2010) listed several recent empirical analyses that are related to the present study. Turetsky and Weinstein (2003) studied the impact of students’ grades in account-ing principles courses on their performance in an upper level financial management course. Their regression analysis mod-eled the finance course grade as a function of SAT score, gender, grades in the accounting principles and mathematics courses, and transfer status. They found that the students’ grades in the accounting prerequisites were positively cor-related with their grade in the finance course. Springer and Borthick (2007) looked at student performance in Interme-diate Financial Accounting I as a function of the students’ grades in two different kinds of accounting principles courses (a traditional course versus a course with cognitive conflict tasks), as well as GPA, age, gender, and transfer status. They found that only a higher GPA and taking principles courses that include cognitive conflict tasks were related to improved performance in the intermediate course. Sanders and Willis (2009) found that requiring an accounting principles compe-tency exam—beyond just successful completion of the ac-counting principles courses—improved student performance in Intermediate Financial Accounting I.

Pomykalski, Dion, and Brock (2008) built a statisti-cal model of a business student’s senior cumulative GPA based on the student’s performance in certain freshman-level business foundation courses, which included principles of macroeconomics and introduction to statistics. They found that students’ grades in these two key business principles courses were strong predictors of their senior-level GPA, and concluded that “a student’s performance in freshman core courses may be highly predictive of the student’s over-all performance in the business major” (p. 162). Attempts at including measures of the student’s underlying academic aptitude, as measured by their SAT scores and high school

GPA, as well as gender in their model revealed that none of these factors played a statistically significant role in deter-mining senior GPA. We note that their analysis only included those business students who actually completed their degree requirements and graduated, and did not focus on student performance in specific intermediate business courses, but on overall performance across all subjects—business and nonbusiness—required for the business degree.

Although not directly related to student performance in in-termediate business courses, Christensen, Nance, and White (2012) found that MBA students who lacked undergraduate business prerequisites actually outperformed those who had completed those same business prerequisites, and that under-graduate GPA predicted success in an MBA program. This implies that student academic quality—as measured by un-dergraduate GPA—is more important in determining MBA student success than is successful completion of certain busi-ness undergraduate prerequisites.

Finally, Watson et al. (2007) lamented that,

Most published accounting education articles deal with is-sues related to curriculum or pedagogy...these articles are

mostly descriptive or short-term studies offering no empirical evidence of effectiveness. Accounting education needs more empirical studies...to evaluate the educational effectiveness

of different curriculum models and instructional approaches. (p. 22)

We agree with Watson et al. and hope to make a positive contribution to the business education literature with this empirical study of the impact on students of taking their business prerequisites at a two-year junior college.

DATA AND ANALYSIS

We obtained data from various semesters between 2005 and 2011 on student performance in four typical upper level business courses at a comprehensive, regional public uni-versity (variable names appear in capitals): Intermediate Mi-croeconomics, Intermediate MaMi-croeconomics, Intermediate Business Statistics, and Intermediate Financial Accounting I. Intermediate Microeconomics and Intermediate Macroe-conomics are required of all eMacroe-conomics majors; the prereq-uisites are Microeconomic Principles and Macroeconomic Principles, respectively. Students may take the economics principles courses in any order, and do not have to complete both in order to register for either of the intermediate eco-nomics courses. Intermediate Business Statistics is required of all business majors; the prerequisite is an Introduction to Probability and Statistics, which is taught by the math depart-ment. Intermediate Financial Accounting I is required of all accounting majors; the prerequisites are Principles of Finan-cial Accounting and Principles of Managerial Accounting. Students must complete Principles of Financial Accounting

before they are allowed to take Principles of Managerial Accounting.

For each student who took one of these courses we col-lected the following data: final course average for the in-termediate business course, final course letter grade for the lower level prerequisite(s), location for the lower level pre-requisite (two years vs. four years), gender, ethnicity, race, cumulative GPA, major, and class at the time they took the intermediate business course. Following Huang et al. (2005), we used only the first final course average for those students who attempted the intermediate course multiple times, and we used the highest letter grade for those who took the lower level prerequisite course more than once. Unlike Colley et al. (1996), we did not exclude those students who only trans-ferred one of their principles classes from a junior college.

The variable names are the following:

For the final course averages: Intermediate Microeconomics (MICRO), Intermediate Macroeconomics (MACRO), Intermediate Business Statistics (BSTAT), Intermediate Financial Accounting I (FACCT).

For the prerequisite letter grades (coded as 1, 2, 3, 4): Principles of Microeconomics (PMICRO), Principles of Macroeconomics (PMACRO), Introduction to Probabil-ity and Statistics (PSTAT), Principles of Financial counting (PFACC), and Principles of Managerial Ac-counting (PMACC).

For cumulative GPA at the time the intermediate course was taken (GPA).

For the remaining variables, all of which are expressed as binary dummy variables, if the prerequisite course was transferred from a two-year college (JUCO), class rank if other than a junior (SOPH or SENIOR), sex (GENDER=1 if female), ethnicity (ETHNIC =1 if Hispanic) and race (RACE=1 if African American), and if the student was majoring in the discipline covered by the intermediate course (ECON or BUS or ACCT).

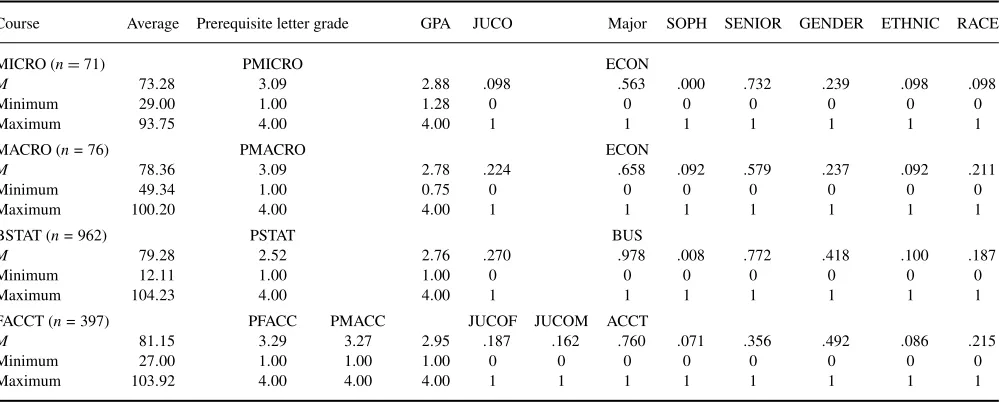

Descriptive statistics for all model variables for each of the previous four intermediate business courses are presented in Table 1.

For each of the four intermediate courses we ran a linear regression model of the final course average on a constant term, the letter grade for the relevant prerequisite(s), GPA, JUCO, SOPH, SENIOR, GENDER, ETHNIC, RACE, and major (ECON or BUS or ACCT).

EMPIRICAL RESULTS

Intermediate Microeconomics

Column (a) in Table 2 presents ordinary least squares es-timates of the previous full regression model for MICRO (Model I). While the model demonstrates good explanatory power (the adjustedR2is .637), the only independent variable

PREREQUISITES AND PERFORMANCE IN INTERMEDIATE COURSES 241

TABLE 1

Descriptive Statistics for Model Variables

Course Average Prerequisite letter grade GPA JUCO Major SOPH SENIOR GENDER ETHNIC RACE

MICRO (n=71) PMICRO ECON

M 73.28 3.09 2.88 .098 .563 .000 .732 .239 .098 .098

Minimum 29.00 1.00 1.28 0 0 0 0 0 0 0

Maximum 93.75 4.00 4.00 1 1 1 1 1 1 1

MACRO (n =76) PMACRO ECON

M 78.36 3.09 2.78 .224 .658 .092 .579 .237 .092 .211

Minimum 49.34 1.00 0.75 0 0 0 0 0 0 0

Maximum 100.20 4.00 4.00 1 1 1 1 1 1 1

BSTAT (n =962) PSTAT BUS

M 79.28 2.52 2.76 .270 .978 .008 .772 .418 .100 .187

Minimum 12.11 1.00 1.00 0 0 0 0 0 0 0

Maximum 104.23 4.00 4.00 1 1 1 1 1 1 1

FACCT (n =397) PFACC PMACC JUCOF JUCOM ACCT

M 81.15 3.29 3.27 2.95 .187 .162 .760 .071 .356 .492 .086 .215

Minimum 27.00 1.00 1.00 1.00 0 0 0 0 0 0 0 0

Maximum 103.92 4.00 4.00 4.00 1 1 1 1 1 1 1 1

Note.Data for MICRO were collected from four semesters between spring 2006 and fall 2010; data for MACRO were collected from five semesters between spring 2005 and spring 2011; these two classes are only taught every third long semester. Data for BSTAT included every semester from summer 2007 through summer 2011. Data for FACCT included every semester from spring 2008 through fall 2011.

that turns out to be significant is GPA, which serves as a mea-sure of student academic quality. Each one-unit increase in a student’s cumulative GPA is estimated to yield an increase in the final course average in MICRO of over 20 percentage points. Surprisingly, the letter grade earned in the prerequi-site course (PMICRO) is not a significant factor, nor is the fact that the prerequisite course was taken at a two-year col-lege (JUCO). Similarly, none of the demographic variables is significant. Although not presented here, dropping all of the dummy variables except for JUCO does not change this basic result, nor does dropping everything but GPA and a constant term, making our finding robust.

Another anecdotal observation often made by faculty is that stronger students tend to take their prerequisites at the

TABLE 2

Regression Model Results for MICRO

a. Model I b. Model II c. Model III

Coefficient p Coefficient Coefficient p

Constant 9.151 .213 41.862 .000 43.096 .000

PMICRO 0.359 .853 10.139 .000 10.239 .000

GPA 20.473 .000 — —

JUCO −3.482 .419 — –15.669 .000

GENDER 0.095 .974 — —

RACE 1.755 .669 — —

ETHNIC 3.874 .374 — —

ECON 2.498 .311 — —

SENIOR 3.289 .281 — —

Note.For Model 1, adjustedR2=.637 (SE=9.687); for Model II, adjustedR2=.264 (SE=13.793); for Model III, adjustedR2=.341 (SE= 13.049).

four-year university, while weaker students are more likely to take them at a two-year college. It seems intuitive that this would be the case, as stronger students are more likely to be admitted into the university directly from high school, and more likely to receive freshman scholarships, while weaker students may have to start their studies at a two-year college if they are denied freshman admission to the university or do not qualify for a freshman scholarship. Indeed, this observation is borne out in our sample, wherein only 5.7% of Intermediate Microeconomics students with GPAs above the sample mean of 2.88 took Microeconomic Principles at a two-year college, while 13.9% of Intermediate Microeconomics students with below-average GPAs did. However, our results from Model I clearly show that differences in student performance in Intermediate Microeconomics can be attributed to their GPA, rather than where they took Microeconomic Principles or what letter grade they earned in the prerequisite.

Column (b) in Table 2 shows what happens if we follow Colley et al. (1996) and estimate a simpler model with only a constant term and PMICRO as independent variables (Model II). In Model II the adjustedR2fell to .264, but the estimated

slope coefficient on PMICRO jumped to 10.14 and becomes statistically significant. This result seems to confirm Colley et al.’s previous findings and suggests that every one letter grade increase in the prerequisite course will lead to a one letter grade increase in intermediate microeconomics (i.e., 10 percentage points equal one letter grade). In column (c) of Table 2 (Model III) we see that if we add the JUCO dummy variable to Model II we find that JUCO becomes statistically significant, the estimated slope coefficient for PMICRO is not affected, and the adjustedR2increases to .341. According to the results from Model III, the estimated impact of taking

the prerequisite course at a two-year college is to reduce the average student’s grade in intermediate microeconomics by 15.7 percentage points, or one and one half letter grades, which is indeed considerable. Both of these results seem quite reasonable and agree nicely with the anecdotal evidence.

Of course, the results from Model I tell us that the coeffi-cient estimates from Models II and III are badly biased due to omission of the important GPA variable, and are therefore unreliable. This suggests that the results reported by Colley et al. (1996) may also be biased. However, these biased results may provide a possible explanation for the anecdotal evidence that some faculty have perceived: students who take the prerequisite course at a two-year college, or make a lower grade on the prerequisite, often do not do as well on the intermediate course. Without taking into account the student’s underlying academic quality—which may not be readily observable to the faculty member – this may appear to be true. But once we accounted for student academic quality, we discovered that where the student took the prerequisite, and what grade they achieved on the prerequisite, simply did not matter in determining their performance in intermediate microeconomics. Good students find a way to be successful, and weaker students continue their weak performance.

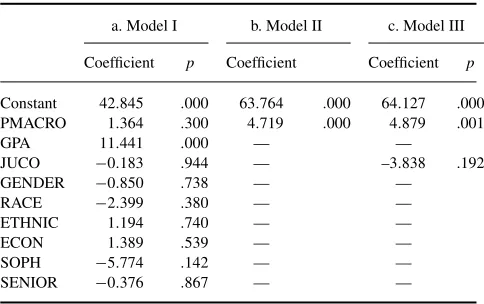

Intermediate Macroeconomics

Column (a) in Table 3 presents the results from estimating Model I for MACRO. Once again, the only variable which is found to be statistically significant is GPA, but the esti-mated effect is almost half the size it was for Intermediate Microeconomics: 11.44 versus 20.47. The overall explana-tory power of the model was somewhat weaker as well, but the basic conclusions remain unchanged: student academic quality, as measured by GPA, was the only significant factor in determining student performance in intermediate macroe-conomics. Re-estimation of the model without any of the

in-TABLE 3

Regression Model Results for MACRO

a. Model I b. Model II c. Model III

Coefficient p Coefficient Coefficient p

Constant 42.845 .000 63.764 .000 64.127 .000

significant variables does not change our findings, confirming the robustness of these estimates. We note that intermediate macroeconomics students with above-average GPAs in our sample were less likely to take their prerequisite at a two-year college than were their classmates with below-average GPAs by a difference of 15.1% to 27.9%, which is similar to what we found for intermediate microeconomics students.

In Table 3 we also show the results of estimating the two simple models with only a constant term and PMACRO (Model II in column (b)), and a constant term, PMACRO, and the JUCO dummy variable (Model III in column [c]). Each of these two simple models yield a statistically signif-icant estimated coefficient on PMACRO of just under 5.0, which is about half as large as we found for Models II and III of MICRO in Table 2. Unlike in Table 2, we did not find a significant effect from adding JUCO to Model III in column (c). The results from Models II and III of MACRO again show that a naive analysis of student performance as a function of prerequisite grade and location alone can lead to biased conclusions. Furthermore, these results strengthen our previous conclusion for intermediate microeconomics that student quality trumps both location and grade in the prerequisite course in determining student performance in the intermediate business course.

Intermediate Business Statistics

Table 4 presents the results from estimating Model I for BSTAT. These results differ markedly from those reported previously for Intermediate Microeconomics and Interme-diate Macroeconomics. In the full model, we find that the prerequisite grade (PSTAT), GPA, and the JUCO dummy are all statistically significant. However, GPA continues to play the largest role in determining student performance in the intermediate course, while PSTAT and JUCO play much smaller roles. Every one-unit increase in GPA increases the

TABLE 4

Regression Model Results for BSTAT

a. Model I b. Model II c. Model III

Coefficient p Coefficient Coefficient p

Constant 41.172 .000 67.232 .000 67.539 .000

PREREQUISITES AND PERFORMANCE IN INTERMEDIATE COURSES 243

final course average in intermediate business statistics by about 13 percentage points, slightly more than we found for intermediate macroeconomics (11.44), but less than we found for intermediate microeconomics (20.47). Unlike in-termediate microeconomics and macroeconomics students, intermediate business statistics students with above-average GPAs in our sample were just as likely to take the lower level prerequisite at a two-year college as were their classmates with below-average GPAs: 27.0% versus 27.1%. Neverthe-less, GPA still plays the deciding factor in student perfor-mance in the intermediate business statistics course.

The impacts from the prerequisite grade, while statisti-cally significant, are very small: each letter grade increase in PSTAT only increases BSTAT by 1.22 percentage points. Similarly, taking the prerequisite math course at a two-year college has a small, but significant effect of reducing BSTAT by 2.37 percentage points. These results essentially imply that taking the introductory statistics course at a two-year college is equivalent to a two letter grade reduction in the prerequisite course (i.e., an A at the two-year college is equivalent to a C at the university). Nevertheless, this nega-tive impact from taking the prerequisite at a two-year college is not too troublesome because of its small magnitude; as with intermediate microeconomics and macroeconomics, the student’s GPA remains the primary determinant in his or her performance in the intermediate course.

Dropping the insignificant dummy variables from Model I does not change the results reported above for BSTAT. Columns (b) and (c) in Table 4 reveal that Models II and III for BSTAT gave much lower measures of goodness-of-fit compared to Model I, just as was found for MICRO and MACRO. Because PSTAT and JUCO were already found to be significant in Model I, the omission of GPA in Models II and III serves primarily to increase the estimated coefficients on PSTAT and JUCO (i.e., bias them upward). In Model II it now appears that each one letter grade improvement in PSTAT increases BSTAT by about 5 percentage points, or four times larger than we found in Model I. In Model III, the impact of taking the introductory statistics course at a two-year college appears less pronounced, so that an A at the two-year college is equivalent to a B at the university. Of course, these biased results are unreliable and serve mostly as another reminder that some measure of student academic quality should be included in the model.

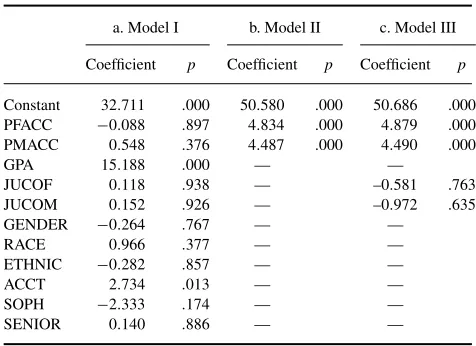

Intermediate Financial Accounting I

Finally, Table 5 presents the results from estimating Mod-els I, II, and III for FACCT. Because there were two sepa-rate prerequisite courses for Intermediate Financial Account-ing I—Principles of Financial AccountAccount-ing and Principles of Managerial Accounting—we included two separate dummy variables to indicate whether those courses were taken at a two-year college—JUCOF and JUCOM, respectively. The results for Intermediate Financial Accounting I are

remark-TABLE 5

Regression Model Results for FACCT

a. Model I b. Model II c. Model III

Coefficient p Coefficient p Coefficient p

Constant 32.711 .000 50.580 .000 50.686 .000

ably similar to those obtained for the other three intermediate business courses: the single most important determinant of student performance is GPA. Each one-unit increase in GPA implies an increase in FACCT of over 15 percentage points, which is in the center of the previous estimates for the other three intermediate courses. Intermediate Financial Account-ing I students with above-average GPAs were only slightly less likely to have taken their accounting principles at a two-year college: 17.6% versus 19.8% for financial principles and 16.1% versus 16.2% for managerial principles.

As before, the grades earned in the prerequisite courses (PFACC and PMACC) do not matter, nor does the fact they were taken at a two-year college (JUCOF, JUCOM). In this sense our results are consistent with those of Huang et al. (2005), who found that students’ grades in user-focused ac-counting principles courses did not significantly influence their performance in Intermediate Financial Accounting I. However, in this case we also found that accounting majors (ACCT) outperform their nonaccounting major classmates by an average of almost three grade points; none of the other demographic variables was statistically significant. This re-sult is most likely due to the fact that a grade of C or better in intermediate financial accounting I is a prerequisite for intermediate financial accounting II, which is also required of all accounting majors. In addition, accounting majors re-alize that their initial employment prospects in accounting are significantly affected by their accounting GPA, as well as their overall GPA, and so may be somewhat more motivated to earn a higher grade in intermediate financial accounting I than are non-accounting majors. Re-estimation of the model with only the constant term, GPA, and ACCT did not change our results, slightly raising the adjustedR2to .541.

Columns (b) and (c) show us once again of the dangers of estimating simpler models containing only the prerequisite

grades PFACC and PMACC (Model II), plus the associated two-year college dummy variables (Model III). The fit of these models drops off dramatically from that of Model I, and we see that the estimated coefficients on the principles grades are about 4.50 to 5.00 and appear to be significant, very similar to what we found for BSTAT and MACRO. This time the two-year dummy variables were not significant, as we also found with MACRO. Adding the significant ACCT variable to either Model II or III does not change the results.

DISCUSSION AND CONCLUSIONS

A rigorous analysis of student data from a regional com-prehensive public university has shown that, contrary to anecdotal evidence, where business students complete their lower level prerequisite courses is simply not that im-portant. Student success in four typical intermediate busi-ness courses—Intermediate Microeconomics, Intermediate Macroeconomics, Intermediate Business Statistics, and In-termediate Financial Accounting I—is essentially com-pletely determined by the underlying academic quality of the student, as measured by his or her GPA. Each one unit increase in a student’s GPA leads to an increase in their per-formance in the intermediate course of anywhere from 11 to 20 percentage points, or about 1–2 letter grades. For some intermediate business courses, students with above-average GPAs are more likely to take their principles courses at a four-year university, but that fact alone does not lead to bet-ter student performance. Stronger students rise to the top and outperform their peers regardless of where they took their prerequisites. Weaker students are not handicapped by tak-ing their prerequisites at a two-year college, and receive no real advantage by waiting and taking their principles courses at a four-year university.

The significance of the student’s underlying academic quality (as measured by his or her GPA when taking the course) in determining the performance in a specific course or set of courses was noted in several of the previous stud-ies cited previously, such as Von Allmen (1996; intermedi-ate microeconomics); Zanakis and Valenzi (1997; business statistics); Borde (1998; marketing); Turetsky and Weinstein (2003; finance); Springer and Borthick (2007;intermediate financial accounting); and Christensen et al. (2012; MBA program). But our finding that a student’s letter grade in the lower level prerequisite course does not determine his or her performance in the upper-level course—with the excep-tion of intermediate business statistics, where the effect was quite small, a little more than one percentage point—is less expected, and seems to contradict our casual observation.

One possible explanation why students’ performance in the lower level courses does not significantly affect their performance in the follow-up on the intermediate course may be that the structure of most intermediate business courses usually involves a certain amount of review of the prerequisite

material at the start of the course. The extent of this review may differ from course to course, or even from instructor to instructor, but over time an attentive instructor may perceive that the intermediate students need some additional review, and so add that content to their course. With enough review of the lower level material, students are able to perform in the intermediate course at the level that is typical for them in other courses (i.e., consistent with their GPA), regardless of how strong their foundation is from the principles courses.

This explanation may have become even more compelling for the intermediate financial accounting I courses after most accounting principles courses were changed to a user’s per-spective, rather than a preparer’s perspective in the mid-1990s. Those faculty teaching Intermediate Financial Ac-counting I might have found it necessary to augment their syllabi with much of the lower level content that had previ-ously been covered in the accounting principles courses. This is basically what Huang et al. (2005) and Sanders and Willis (2009) found. If so, this would suggest that the amount of truly upper level content in Intermediate Financial Account-ing I courses has shrunk over the years since this change. However, with the move of many accounting major degree programs to a five-year, 150-hr curriculum there is probably enough time to make up for weaker intermediate courses by adding advanced content in subsequent accounting courses. Of course, those nonaccounting majors who only take the intermediate accounting courses and do not go on to the more advanced accounting courses would not be receiving the same accounting preparation as before.

It is important to note that our findings do not imply that the lower level prerequisite courses are not necessary for stu-dent success in the intermediate business courses. To make such a statement would require us to have a substantial num-ber of observations for students who took the intermediate courses without having first completed the lower level pre-requisites. Because we rigorously enforce the lower level prerequisites for our intermediate courses, no such data are available.

NOTE

1. See, for example, “Obama Addresses White House Summit On Community Colleges,” Huffington Post, http://www.huffingtonpost.com/2010/10/05/communi ty-college-summit- n 750402.html

REFERENCES

American Accounting Association, Accounting Education Change Com-mission. (1992). The first course in accounting: Position statement no. two.Issues in Accounting Education,7(2), 249–251.

Apostolou, B., Hassell, J. M., Rebele, J. E., & Watson, S. F. (2010). Ac-counting education literature review (2006–2009).Journal of Accounting Education,28, 145–197.

Borde, S. F. (1998). Predictors of student academic performance in the introductory marketing course.Journal of Education for Business,73, 302–306.

PREREQUISITES AND PERFORMANCE IN INTERMEDIATE COURSES 245

Christensen, D. G., Nance, W. R., & White, D. W. (2012). Academic per-formance in MBA programs: do prerequisites really matter?Journal of Education for Business,87, 42–47.

Colley, J. R., Volkan, A. G., Drucker, M. & Segal, M. A. (1996). Evaluating the quality of transfer versus nontransfer accounting principles grades. Journal of Education for Business,71, 359–362.

Huang, J., O’Shaughnessy, J. & Wagner, R. (2005). Prerequisite change and its effect on intermediate accounting performance.Journal of Education for Business,80, 283–288.

Pomykalski, J. J., Dion, P., & Brock, J. L. (2008). A structural equation model for predicting business student performance.Journal of Education for Business,83, 159–164.

Sanders, D. E., & Willis, V. F. (2009). Setting the P.A.C.E. for student success in intermediate accounting.Issues in Accounting Education,24, 319–337.

Springer, C. W., & Borthick, A. F. (2007). Improving performance in ac-counting: evidence for insisting on cognitive conflict tasks.Issues in Accounting Education,22, 1–19.

Turetsky, H., & Weinstein, G. (2003). Validity check on the accounting prerequisites within the business curriculum.Advances in Accounting Education,5, 165–180.

Von Allmen, P. (1996). The effect of quantitative prerequisites on perfor-mance in intermediate microeconomics.Journal of Education for Busi-ness,72, 18–22.

Watson, S. F., Apostolou, B., Hassell, J. M., & Webber, S. A. (2007). Ac-counting education literature review (2003–2005).Journal of Accounting Education,25, 1–58.

Zanakis, S. H. & Valenzi, E. R. (1997). Student anxiety and attitudes in business statistics. Journal of Education for Business, 73, 10– 16.