Manajemen | Fakultas Ekonomi Universitas Maritim Raja Ali Haji jbes%2E2009%2E08105

Teks penuh

Gambar

Dokumen terkait

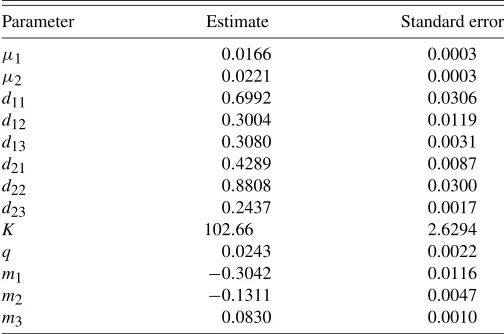

Because the latter assumption is not needed for identification of the shocks in the present mixed normal setup, the zero restriction in ( 2.3 ) which specifies that the second shock

KEY WORDS: Backtesting; Basel Accord; Conditional quantile; Estimation risk; Fixed, rolling, and recursive forecasting scheme; Forecast evaluation; Risk management;

To investigate whether minority workers face an economy- wide glass ceiling or sticky floor, we estimate wage gaps at sev- eral quantiles of the conditional wage

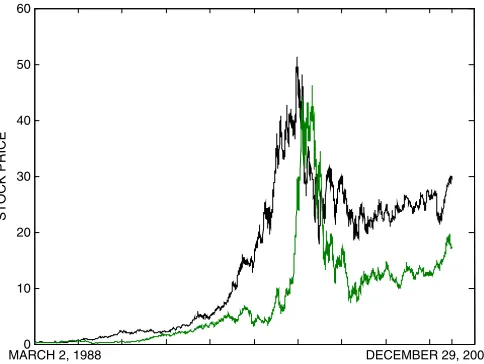

In Panel (A) we show the filtered time series for both the model with the factor loadings parameter added to the state (DNS–TVL, dotted line) and the model with both the

The bottom line from this experiment is that the welfare weights can matter in the cost of living, the second-order part of the approximation (which captures substitution effects)

Since all models have the same individual volatility dynamics, with the sole exception being the flexible multivariate GARCH model, any difference in the goodness of fit for

Todorov and Tauchen (2006) showed how to simulate CARMA ( 2 , 1 ) stochastic volatility processes using a particu- lar family of driving Lévy processes and Todorov (2009) used a CARMA

Compared with models with constant variances, mod- els with stochastic volatility have significantly more accurate interval forecasts (coverage rates), normalized forecast