1

Impediments in Competitive Electricity Market Establishment

in Java Bali Power System

I Made Ro Sakya Sinthya Roesly*)

PLN Java Bali Transmission & Load Dispatch Center Krukur Limo Cinere – PO Box 159 CNR Telp/Fax. +62-21-754 2646 / +62-21-754 3661

Jakarta 16514 - Indonesia

E-mail: [email protected], [email protected]

ABSTRACT

New Indonesia Electricity Law replacing the Law No. 15 of the year 1985 has been enacted on late September 2002. This will bring fundamental change to the way the industry operates. More open and transparent mechanism based on clear procedures and rules is expected to be in place. Centralistic industry governed by the Government which is common in the industry for long period will gradually be transferred into a more de-centralistic and market oriented framework.

The Government ultimate goal is the establishment of a fully-competitive electricity market that encourages competition in electricity production and supply. The competitive structure will consist of many generation companies, distribution companies, retail companies, retail agents, one transmission company, system operator and market operator. Generation companies will compete each other in selling their electricity. Sales can be conducted via a wholesale market power pool or directly to retailers or large customers through bilateral contracts.

There are 8 prerequisites of the market implementation stated in the new Law, i.e.: i) the retail tariff is at its economic level, ii) competition in primary energy, iii) establishment of Regulatory Body, iv) rules supporting the competition, v) readiness of infrastructure including hardware and software, vi) power system condition enabling competition, vii) level playing field, and viii) other preconditions set-up by Regulatory Body. By September 2003, the Regulatory Body should be established, and within 5 years from 2002, limited generation competition should be implemented. Afterwards, once the system is ready, competition at retail side will follow.

This paper will look at the readiness of Java Bali system for competitive electricity market implementation as required by the new Law, particularly with regard to system operations aspect. This includes capacity balance, transmission constraints, as well as operational rules and regulation. It will cover description on various issues such as actual and projected generation capacity for the following 5 years to catch demand growth, contractual limits on dispatch flexibility such as take-or-pay gas and geothermal contracts, existence of many independent power producers (IPPs) whose contracts do not fit easily into a competitive market, the presence of multiple transmission constraints, as well as availability of various operational codes required for market implementation, e.g. Grid Code, Distribution Code, Transmission Pricing, Planning and Competitive Tendering Code, Tariff Code and the Market Rules.

Key words: Java-Bali, competition, electricity market.

1.

Introduction

New Indonesia Electricity Law No. 20/2002 replacing the Law No. 15 of the year 1985 has been enacted on late September 2002. This will bring fundamental change to the way the industry operates. More open and transparent mechanism based on clear procedures and rules is expected to be in place. Centralistic industry governed by the Government which is common in the industry for long period will gradually be transferred into a more de-centralistic and market oriented framework.

The Government ultimate goal is the establishment of a fully-competitive electricity market that encourages competition in electricity production and supply. The competitive structure will consist of many generation companies, distribution companies, retail companies, retail agents, one transmission company, system operator and market operator. Generation companies will compete each other in selling their electricity. Sales can be conducted via a wholesale market power pool or directly to retailers or medium voltage (MV) or high voltage (HV) customers through bilateral contracts.

The market implementation will be in two stages. Stage 1 is the competition limited to generation and stage 2 is retail competition at medium and high voltage. Five year time frame from the law enactment is given for the implementation of competition. There will be a Market Supervisory Agency (MSA) who will function as regulator in the competitive region.

In the Blue Print for the Development of National Electricity Industry 2003-2020, the Government designates two systems that would be prepared for operation under competitive market. The two systems are Batam island and Java-Bali-Madura., or in this paper we simply refer to Java Bali system.

This paper will briefly describe the challenges of the market implementation in Java Bali power system, particularly with regard to the operational aspects of eigth prerequisites mentioned above. It will look at the overview of the power system condition in the next 5 years which includes capacity balance, transmission system and other operational infrastructures required for enabling the market.

2.

Electricity Market as in the Law [1]

The new law requires the break-up of electricity ventures into separate business entities for generation, HV/MV retail, the so-called Retail Agent, transmission, distribution, and low voltage (LV) retail, namely Supply Business. The first two will be opened for competition, while the last three will be left as regulated industries. Apart from those five ventures, the law also recognizes the two other functions in the industry, namely System Operator (SO) and Market Operator (MO).

Detail design of the market is not mentioned in the Law. Supply Business sells electricity to LV customers in a certain region. It can buy electricity from the market (pool) and/or directly from the generator which does not participate in the market. Retail Agent sells electricity to HV/MV customers. However, with the consent from MSA and based on the inqiry from customers to get specific quality and service, it can sell electricity to LV customers. Similar to Supply Business, Retail Agent dan buy electricity from the market and/or directly from generator which does not participate in the market.

MO’s function is to match bids and offers of electricity in accordance with the Market Rules which drives efficiency, economics and healthy competitive environment. The responsibility of the MO includes: (i) coordination with SO in electricity delivery, (ii) determination of electricity market price and the quantity to deliver, (iii) providing transaction information to all market participants, (iv) settlement of all electricity market transaction, (v) dispute resolution on the market transactions, (vi) reporting of the market transactions to MSA, serta (vii) performing other duties with regard to market operations assigned by the MSA.

SO’s function id to manage power system operation which is secure, reliable and provides quality electricity in accordance with the Grid Code. The responsibility of SO includes: (i) developing power system expansion plan, (ii) maintaining the level of security, quality and reliability of the power system in accordance with the applicable standard, (iii) demand forcasting and developing generating unit loading schedule based on information from MO, (iv) coordination of generation and transmission maintenance scheduling dan jaringan transmisi tenaga listrik, (v) providing dispatch instruction to generator and switchiing instruction to transmission operator, (vi) providing information to MO for electricity transaction settlement purposes, (vii) ensure short term continuity of supply, and (viii) performing other duties with regard to power system operations assigned by the MSA.

In the competitive market, generators will compete in selling their electricity produced. They will offer the selling price to the MO and MO will sellect the generators and determine the market clearing price of the electricity. The results of the market clearing process will be given to the SO who then will operate the system. SO has the right to deviate from MO decisions if so required by the system.

Detail market design will be determined by the MSA, for example whether the market will use centralised unit commitment, adopt one price system, with gross or net pool, etc.

3. Market Establishment Challenges

Establishment of competitive electricity market as stipulated in the Law poses several operational challenges. The following paagraphs will describe such challenges.

3.1.

Power System Condition

3.1.1. Java Bali Power System – Current Condition

Java Bali power system is the biggest interconnection system in Indonesia (see Figure-1 in the Appendix). This system constitutes approximately 80% of electricity produced in Indonesia and … million customers out of …… total PLN (Indonesia State-Owned Electricity Corporation) customers. The operations of the system is divided into four regional transmission operator (Region), and the customers are managed by 5 distribution units of PLN.

Demand

Electricity consumption in the past 5 years has increased about …% per year, while the annual system peak has increased …% in average. The highest system peak demand was 13. 682 MW (23rd

October 2003).

Looking at the geographical demand distribution, the center of the demand in the system is the western part of the Java island. This creates the electricity flow from eastern part of the system to the west. Tabel-1 shows composition of peak demand of typical working day in each region in Java Bali system.

3 customers of ….GWH annual electricity consumption connected to MV system and the rests are LV customers. HV and LV customers are mostly the industrial and commercial customers category which absorb about 60% of electricity in Java Bali.

Those HV customers have about 2000 MVA contracted power and the rate of annual energy consumption increase at approximately 12%. MV customers ……

Supply

Electricity supply in Java Bali is sourced from various primary energy, i.e hydro, coal, natural gas, geothermal, and oil.

Tabel –2

Capacity Balance of Java Bali System in 2003

Electricity in Java Bali system is transferred using 500 kV, 150 kV and 70 kV transmission lines. 500 kV lines function as interconnector of East, central and west Java regions. 150 kV and 70 kV lines serve to transfer eelctricity from supply point or interconnection point through 500 kV extra high voltage substation to demand centers around Java Bali system.

There are several weak points in the current transmission system. Some parts of networks are still constrained by bottlenecks, overloading and lack of adequacy of security level. For example:

Central region to western region transfer is constrained by voltage stability limit. Maximum transfer is allowed at ……MW at …. lines. This condition is overcome once the ……lines has been operated.

High interbus transformer loading with more than 60% nominal rating resulting in unfulfillment of N-1 criteria. Serious condition appears at central Java region in which everyday expensive generating units have to be started up (must-run units).

Bali system also has contraint caused by limited transfer capability of submarine cable from Java to Bali. This creates the situation in which Bali has to start up expensive generating units.

3.1.2. Java Bali Power System – Projection in 5 Years

Demand and Supply

Demand forecast of the Jawa Bali power sustem shows that average peak load growth … % per year, thus forecasted peak load in 2008 will be … MW. Table .. depict forecasted peak load for each year.

The low growth of peak load is due to low additional capacity of the power plant. The load growth is controlled through a

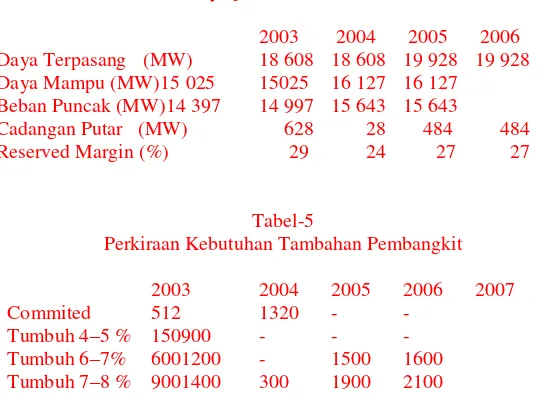

Kebutuhan pasokan sistem Jawa-Bali sangat tergantung pada pertumbuhan beban. Dengan mempertimbangkan beberapa pembangkit yang saat ini sudah dalam proses pembangunan, maka hingga tahun 2007 akan terdapat tambahan kapasitas pembangkit sebesar 1.830 MW. Pembangkit-pembangkit tersebut antara lain adalah PLTG Grati, PLTP Dieng, PLTG Cikarang dan PLTU Tanjung Jati. Penambahan pembangkit tersebut hanya dapat menampung pertumbuhan beban sekitar 4.5% hingga tahun 2005, dan beban yang tumbuh secara natural setelah tahun 2006.

Untuk menampung pertumbuhan beban yang lebih tinggi dengan tetap mempertahankan reserve margin minimal 30% diperlukan tambahan pembangkit yang lebih besar lagi. Tabel-4 menunjukkan perkiraan neraca daya pada skenario Terbatas hingga tahun 2006. Tabel-5 menunjukkan perkiraan kebutuhan tambahan pembangkit pada pertumbuhan beban tertentu.

Tabel –4

Melihat tingkat kebutuhan pasokan tersebut, maka untuk dapat melayani beban, terlebih lagi jika ingin menerapkan kompetisi, diperlukan usaha peningkatan kemampuan pasokan sesegera mungkin mengingat waktu yang dibutuhkan untuk membangun pembangkit baru adalah sekitar 4 hingga 5 tahun. Usaha-usaha yang dapat dilakukan antara lain adalah peningkatan kapasitas pembangkit yang sudah beroperasi melalui repowering dan upaya agar kesiapan pembangkit lebih tinggi.

Langkah lain yang dapat ditempuh adalah dengan melakukan kerjasama dengan pihak ketiga yang saat ini mempunyai pembangkit yang sudah terinterkoneksi dengan PLN tetapi hanya digunakan untuk kebutuhan sendiri, atau biasa disebut sebagai Pembangkit Captive (captive power).

Sesuai ketentuan RUUK, kompetisi dalam bidang pembangkitan paling lambat dilaksanakan 5 tahun setelah berlakunya UU. Dengan mempertimbangkan kesetimbangan pasokan dan beban tenaga listrik, tanpa adanya penambahan kapasitas pembangkit yang relatif besar ruang kompetisi di sisi pembangkitan pada masa 5 tahun dari sekarang tampak masih akan terbatas.

Transmission System

Additional t/l : Southern Route

5

Penambahan kapasitas penyaluran yang saat ini sudah dalam tahap pembangunan diharapkan akan dapat mengurangi kendala operasi penyaluran di sistem Jawa-Bali. Penyelesaian salah satu jalur SUTET (Saluran Udara Tegangan Ekstra Tinggi) yang sangat penting yaitu SUTET jalur selatan yang memanjang dari Paiton–Kediri–Pedan–Tasik–Depok beserta GITET dan GI terkaitnya akan mampu mengurangi kendala penyaluran. Pada saat ini SUTET Paiton–Pedan sudah beroperasi dua sirkit dan akan diikuti oleh beroperasinya sirkit kedua tahun 2003. Selanjutnya SUTET Pedan–Tasik–Depok beserta GI terkait diharapkan selesai pada tahun 2005. Dengan selesainya proyek ini, maka pembangkitan dari sisi timur Jawa dapat disalurkan seluruhnya ke sisi barat Jawa.

Meskipun kondisi ini akan dapat mendukung terlaksananya kompetisi, beroperasinya SUTET tersebut diatas tentunya belum sepenuhnya akan menghilangkan seluruh kendala transmisi yang ada di sistem Jawa-Bali. Kendala transmisi lainnya yang diperkirakan masih ada antara lain :

Pasokan dari sisi 500 kV yang sudah tidak memenuhi N-1, Tingginya pembebanan penyaluran di jaringan 150 kV dan 70 kV Mutu tegangan di beberapa pusat beban yang sudah di bawah standar.

Permasalahan diatas memerlukan tambahan kapasitas penyaluran yang secara bertahap perlu diantisipasi dari saat ini jika ingin menerapkan kompetisi. Mengingat bahwa akan tidak ekonomis untuk menghilangkan semua kendala transmisi, maka diperlukan suatu pengaturan komersial yang memungkinkan bekerjanya pasar di tengah kendala transmisi yang ada.

3.2.

Primary Energy Market

The only primary energy market which is already competitive so far is for the coal. The oil market is under the process of deregulation. It is expected that by the year …. the market is already in place. The current monopoly of state owned enterprise of oil distribution and its regulated price mechanism will be replaced by market mechanism with various players. The gas market is very restricted. The gas transmission infrastructure (pipeline) is the major constraint for the gas market development. The infrastructure is not expected to be in place before the year ….. The hydro is somewhat special. It is in limited quantity and its usage is optimised for various purposes, i.e. irrigation, household consumption, and electricity.

Power procurement & market system

3.3.

Infrastructure Readiness

3.3.1. Rules & Regulation

As recognized by te Law, the new market structure will require totally different set of rules and regulation from what we have today.The Government has started to develop a number of draft government regulations (DGR) for example DGR on Electricity Business License, DGR on Designation of Areas Implementing Competition and Prohibition of Market Domination, DGR on Electricity Price, etc.

With regard to the market implementation, several technical and operational rules are required, i.e. Market Rules, Grid Code, Distribution Code, procedures for Planning and Competitive Tendering and Tariff Code for non-competitive/regulated businesses. The Government has already had draft of these rules which have been developed since 1998. Some adjustments to such rules, however, are required to cater for the latest development and make them in line with the new Electricity Law.

In addition to those regulations, the existence of the Regulator or the so-called Electricity Market Supervisory Board is also important. Presidential Decree on the EMSB has been issued and now the Government is in the process of candidate selection.

3.3.2. Software & Hardware

Metering

Market implementation requires the existence of electronic meter to enable settlement for half hourly or hourly transactions. Currently, at the generation side interconnections there have been equipped with electonic meters. While at the distribution side, only half of the interconnection points are installed with electronic meter. It is expected that the whole points is covered by electronic meters by the end of this year.

Market Operation System(MOS)

MOS functions normally include market players’ bid/offer management, dispatch/scheduling module, clearing price determination, settlement and invoicing. MOS interacts with metering system, SCADA/EMS, and requires IT hardware such as computers, application software and communication system.

Currently, there have not yet any concrete plan to develop and install the MOS at the Java Bali system.

Communication Infrastructure

6 Settlement

Once the market exist, there is a requirement for a more sophisticated settlement system. Not only the system should be developed to cater all the transactions in accordance with the market rules, it should also have the capability to interface with the financial institutions which manage the fund flows.

Currently the settlement system is quite simple since most of the transactions are based on similar model of power purchase agreement (PPA). Simple database or spread sheets calculations can cover the whole transactions.

The Government has started to study the financial settlement system functional specification and is going to assess further its software specification. Indonesia. In addition to its status as the the state-owned enterprise, it is still has the privilege to electrify the rural areas around the country. The new Law has automatically invoke the privilege status of PLN to manage the electricity business in the whole nation, however the inexistence of the detail rules regarding the implementation of such provision makes other new players difficult to enter the business. In addition, current retail tariff which is claimed not yet at its economic level, has made the industry not attractive enough for the new players.

Market Power: HHI and RSI

The following tables show the market power of various players in Java Bali system using the Herfindahl Hirschman Index (HHI) Residual Supply Index (RSI) in the next five years, with the assumption of no network constraints, no take-or-pay, and hydro generators participate in the market.

From the table above we see that in the year 2007 system HHI is 2657. There is no absolut threshold for the HHI to ensure the market can work well. However, generally the value between 1500-2500 is used as acceptable reference [3].

7

RSI indicates the percentage of available supply if one generator supply is revoked from the system. The higher the RSI than than 100% is better. From the above table, we can see that there are two generators, i.e. Indonesia Power dan PJB who have RSI of less than 100%.

Although the HHI and RSI cannot really represent the actual condition of market dynamics, they are still be able to be used as an initial precautions of the market power.

Apart form the market power of the players in the market, it must also be recognized that the Java-Bali market is relatively small, with one plant, Suralaya coal-fired plant (3400 MW) is able to meet about one-third of current maximum system demand.

3.5.

Other Challenges

3.5.1. Market Participants Readiness

With the market in place, market participants are required to actively find the most economic ways to sell or buy electricity from various channels in the market. Not only knowledge on buying and selling electricity is required, but also the knowledge on the various risk mitigating tools that help minimizing the risks resulting from the volatile electricity price in the market. Market participants, particularly the Distribution/Retail side which historically have operated under regulated environment will have to switch their paradigm into the new competitive one. Time will be needed for the market participants to gather the necessary knowledge to be in the market.

3.5.2. Transitional Arrangement & Stranded Costs

Another issue that is important to consider in the competitive market implementation is the integration of the existing PLN PPA with IPPs into the market. Some of the PPAs have contractual limits on dispatch flexibility resulting from take-or-pay gas contracts and geothermal contracts, and there are an increasing number of IPPs whose contracts do not fit easily into a competitive market.

This condition also relate to the stranded costs of such PPA. Although the new electricity law recognizes stranded costs issue, so far there have not been so obvious of how such costss are going to be calculated and reimbursed.

3.5.3. Subsidy / Rural Electrification

As important as all the above issues are the subsidy and rural electrification. The new electricity law does mention about the separation of commercial operations of electricity supply from social obligation to underprivileged communities. However, detail guidelines for implementation has not been defined.

4. Conclusions

There are various obstacles in the current system that make implementation of rapid industry change into a competitive electricity industry become difficult. On the generation side, fuel markets have not yet been liberalized. There are contractual limits on dispatch flexibility from take-or-pay gas contracts and geothermal contracts, and there are an increasing number of IPPs whose contracts do not fit easily into a competitive market. It must also be recognized that the Java-Bali market is relatively small, with one plant, Suralaya coal-fired plant, able to meet one-third of maximum system demand.

East-West transfer of power is constrained in Java, and will continue to be constrained until the completion of the 500 kV Southern Loop in around 2004. There are also many local constraints. The presence of these multiple transmission constraints reduces the potential for competition by limiting flexibility in dispatch and thereby increasing market power.

On the distribution side, PLN’s distribution units have no experience in acting as separate companies, let alone in purchasing power from a pool. They have no track-record and their creditworthiness will be weak.

Coincidentally, neither has an independent regulatory body (EMSB) been formed, although the Directorate of Electricity Business Supervision within DGEEU currently has responsibility for regulatory activities.

5. Recommendation

A gradual transition to full competition is therefore required. The transition structure is intended to provide smooth change of the industry and to give the opportunity for all parties to prepare themselves, as well as to be able to get learning experience during the transition phase.

During the transition phase, all players are expected to interact through clear contracts mechanism which can support the establishment of an efficient electricity sector. Such contracts can be made with simplifications in calculation and suitable with the infrastructure capability exist in the transition period.

Reference:

[1] Electricity Law No. 20 Year 2002.

[2] PASA 2004-2008 ???.

[3] Making Competition Work in Electricity, Sally Hunt, 2002

Biography:

Ir. I Made Ro Sakya, MEngSc. dilahirkan di Solo, Jawa Tengah. Menyelesaikan studi S1 di Jurusan Teknik Elektro Institut Teknologi Bandung dan S2 di Melbourne University, Australia. Saat ini bekerja di PLN P3B sebagai Manager Unit Bidding & Operasi Sistem (UBOS). Email: [email protected]

9