This Financial System Stability Booklet represents part of Bank Indonesia»s aim to fulfill its mission ≈to achieve and maintain rupiah stability through the preservation of monetary and financial system stability to accomplish

sustainable long-term economic development∆.

Publisher: Bank Indonesia

Jl. MH Thamrin No 2, Jakarta Indonesia

The Financial System Stability Booklet is published as a means of socializing Financial System Stability to the general public.

Bank Indonesia

Directorate of Banking Research and Regulation Financial System Stability Bureau

Jl.MH Thamrin No.2, Jakarta, Indonesia Telepon : (+62-21) 381 7353, 381 8336 Fax : (+62-21) 2311672

Financial System Stability

Financial System Stability

Financial System Stability

Financial System Stability

Financial System Stability

Foreword iv

Introduction 1

What does Financial System Stability mean? 1

Supporting Factors of Financial System Stability 2

The Difference between Monetary Stability & Financial System 2

Stability

Why is Financial System Stability Important? 3

Parties Responsible for Financial System Stability 5

Role of the Central Bank in Financial System Stability 6

Two Approaches: Marcoprudential and Microprudential 9

Role of Bank Indonesia in Maintaining Financial System Stability 10

What has BI Accomplished? 15

Future Challenges 19

References 20

Glossary 21

FSS Related Sites 22

FOREWORD

In line with its title, the purpose of this booklet is to expand readers» understanding of financial system stability (FSS) as well as explain why FSS is important and how FSS is applied by the central bank. The booklet concisely defines FSS, differentiating it from monetary stability, and highlights factors that affect it, as well as outlining Bank Indonesia»s strategy to preserve FSS.

FSS is a public policy. Therefore, to maintain Indonesian financial system stability, effective coordination and cooperation are required, particularly with the Ministry of Finance, as the fiscal authority, and the Deposit Insurance Corporation. In addition, the public, especially institutions and financial market, as well as end users of financial services are expected to actively play a role and take responsibility. Stability is expected as a result of good corporate governance, effective risk management and market discipline.

Through the realization of two interrelated targets √ FSS and monetary stability √ rupiah stability can be realized, which is a prerequisite to galvanize continuous long-term domestic economic growth.

Jakarta, 23 May 2007 Deputy Governor

Bank Indonesia

The financial crisis that struck various parts of the world, including Indonesia, back in 1997 has taught us a very valuable lesson in the importance of maintaining stability of the financial system. Financial system instability poses terrible threats, namely the loss of public confidence as well as a slowdown in economic growth and a decline in income. In addition, the cost of economic recovery attributable to the crisis is extremely high, especially in the financial sector, while the recovery process itself rarely lives up to expectations. Therefore, financial system stability must be protected in the interest of the general public.

In the past few years post crisis, financial stability has become the primary agenda for both national and international policymakers. This has been marked by the growing number of publications, reviews, conferences and conventions regarding financial stability. Furthermore, there are an increasing number of central banks and financial organizations specifically forming special divisions or units to monitor and evaluate their domestic financial conditions. Moreover, such units publish financial stability reports. Meanwhile, international organizations are also undertaking similar procedures within the context of stability on a regional and international scale.

What does Financial System Stability mean?

The term Financial System Stability does not have universally accepted definition. Schinasi (2006a) defines financial stability as a situation in which the financial system is :

b. Assessing and managing financial risks.

c. Absorbing shocks.

In general, financial stability is financial system resilience against economic shocks, such that the intermediation function, payment system and risk distribution still perform accordingly.

Supporting Factors of Financial System Stability

There are four interrelated factors that support the establishment of financial system stability: (i) stable macro economy; (ii) well-managed financial institutions and efficient financial market; (iii) sound framework of prudential supervision; and (iv) safe and reliable payment system (see Diagram 1). Pressure on one factor may affect the others.

Diagram 1

Stable macroeconomic environment

Well-managed financial institutions and efficient financial market

Safe & robust payment system

Sound framework of prudential supervision Stable & Sound

Financial System

The Difference between Monetary Stability & Financial

System Stability

Why is Financial System Stability Important?

Having a stable financial system will prevent a recurrence of the 1997 Asia Crisis that triggered high fiscal expense, eventually borne by the general public. Even if a future crisis is unavoidable, the public will be more prepared given the faster recovery process.

There are three reasons why financial system stability is important:

A. Monetary stability can only be realized through financial stability,

since the financial system represents the transmission of monetary

policy.

Table 1

Monetary Stability Financial Stability

Definition/ objective Price stability to control inflation Institutional and financial market stability without pressures and price fluctuations that trigger economic volatility.

Instrument for control Yes, subject to lags Limited and difficult to adjust

Accountable Yes Hardly

Forecasting structure Central tendency of distribution Tails of distribution

Forecasting procedure Standard forecasts Simulation or stress test

Administrative procedure Simple Difficult

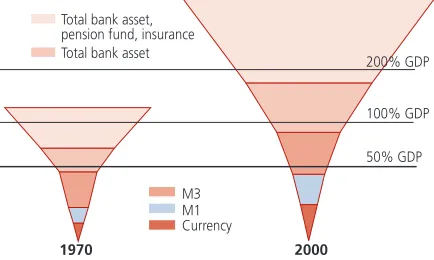

B. The following have the potential to intensify risk in an economy:

- Significant financial sector growth compared to economic

growth.

- Financial deepening which triggers changes in the composition

of the financial system, where the share of monetary assets

(aggregate) declines while the share of non-monetary assets

grows, such that the monetary base continues to rise (Figure 1).

- Globalization and cross-border integration fuels financial system

integration. This is reflected by the development of

conglomerates.

- Greater complexity in financial systems, particularly financial

instruments, products and activities, due to deregulation and

liberalization.

Diagram 2

The Relationship between Financial System Stability and Monetary Stability

Household - Liquidity Risk - Market Risk

International and Domestic : - Economic Factor - Non Economic Factor

Capital

C. A stable financial system will:

1. Create confidence and nurture a supportive environment for

depositors and investors to place their funds at financial

institutions, as well as fulfill the public»s requirements, especially

for smaller customers.

2. Stimulate an efficient intermediation function to induce

investment and boost economic growth.

3. Stimulate market operations and improve economic resource

allocation.

Parties Responsible for Financial System Stability

Financial System Stability is a public policy (Crockett, 1997), such that in general, all parties related to a financial system are responsible as follows:

Figure 1

Financial Sector Growth of G-8 Countries

Total bank asset, pension fund, insurance Total bank asset

M3 M1 Currency

200% GDP

50% GDP 100% GDP

- Financial authorities (government, central bank, deposit insurance

corporation, etc);

- Financial players (banks, capital market, non-bank financial

institutions); and

- The public, particularly the users of financial services.

However, financial system stability is created and maintained by the central bank. Why? Because a central bank can rapidly mitigate instability in the economy using available tools to suppress liquidity, as well as quickly restoring public confidence. Liquidity problems can be overcome through open market operations as well as lender of last resort or a discount window. Other measures that can be taken by a central bank include adjusting the minimum reserve requirements or interest rate policy to steer the economy back towards normal.

Role of the Central Bank in Financial System Stability

This new function of central banks is revealed implicitly and explicitly in their goals, mission and tasks.

On a global scale, several European central banks formed a non-profit organization: the Financial Stability Forum (www.fsforum.org) in April 1999, whose members comprise of almost all central banks, financial departments, and financial supervision authorities in the world. FSF is aimed at promoting financial stability on an international scale.

Meanwhile, the IMF along with World Bank launched the Financial System Assessment Program (www.imf.org/external/np/fsap/fsap.asp) in May 1999 which aims to evaluate a country»s financial system stability. Hitherto, almost 76 countries have participated in the program.

Table 2

1992 ERM exchange rate crisis in Italy and the United Kingdom

1994 Bond market turbulance in G10 countries 1994-95 Mexican crisis (tesobono)

Failure of Barings

1996 Bond market turbulance in United States 1997 U.S equity market correction

1997-98 Asian Crisis (Thailand, Indonesia, Republic of Korea) 1998 Russian default

Long-term Capital Management crisis and market turbulance 1999 Argentinean and Turkey crises

2000 Global bursting of equity price bubble

2001 Corporate governance problems: Enron, Marchoni, Global Crossing September 11th terrorist attack

2001-2 Argentina crisis and default Parmalat

Source: Schinasi (2006a)

Table 3

Financial Stability as the Explicit Aim of Central Banks in Several Countries

≈Regulate credit and currency in the best interest of the economic life of the nation, to control and protect the external value of the national monetary unity and to mitigate by its influence fluctuations in the general level of production, trade, prices and employment so far as may be possible within the scope of monetary action, and generally to promote the economic and financial welfare of Canada.∆

Bank of Canada

To maintain price stability and subject to that, to support the economic policy, including its goals for economic growth and employment. There is a MoU between the BoE and the government that delineates the Bank»s responsibility in the area of financial stability. It assigns the BoE responsibility in three broad areas including stability of monetary system; stability of financial system infrastructure particularly in the area of the payment system; and monitoring the financial system as a whole.

Bank of England (BOE)

≈To issue bank notes and to carry out currency and monetary control as well as to ensure smooth settlement of funds among banks and other financial institutions, thereby contributing to the maintenance of an orderly financial system.∆

Bank of Japan (BoJ)

≈To maintain price stability, to support the general economies policies in the Community, and to promote the smooth operation of the payment systems. The ECSB shall contribute to the smooth conduct of policies pursued by the competent authorities relating to the prudential supervision of credit institutions and the stability of the financial system.∆

European Central Bank (ECB)

≈To formulate and implement monetary policy directed to the economic objective of achieving and maintaining stability in the general level of prices.∆

Reserves Bank of New Zealand (RBNZ)

Figure 2

Publication of Financial Stability Review (Countries)

0 5 10 15 20 25 30 35 40 45 50

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

BI

BOE

To date, approximately 50 countries have already established their own function or unit to monitor the financial system. The results of such monitoring are compiled in a report known as the Financial Stability Review, which can be read at the websites of each respective central bank.

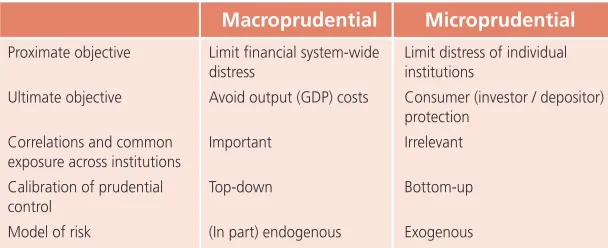

Two Approaches: Macroprudential and Microprudential

Fundamentally, the purpose of a financial system stability function is to analyze progress and assess risks, as well as recommend policies required to maintain financial stability.

Monitoring and evaluating financial system resilience is undertaken using two approaches: macroprudential and microprudential. The principle difference between the two is the purpose (see Table 4).

Role of Bank Indonesia in Maintaining Financial System

Stability

Bank Indonesia has been actively involved in creating and maintaining financial system stability in Indonesian since 2003, along with Bank Indonesia»s mission: ≈to achieve and maintain price stability by maintaining monetary stability and promoting financial system stability for sustainable national development.∆

To achieve financial system stability Bank Indonesia has adopted four strategies: (i) strengthening regulations and standards including fostering market discipline; (ii) intensifying research and surveillance on financial system; (iii) improving effective coordination and cooperation with relevant institution; and (iv) establishing financial safety nets and crisis resolution.

Bank Indonesia»s Framework of Financial System Stability is illustrated in Diagram 3.

Table 4

Macroprudential Microprudential

Proximate objective Limit financial system-wide Limit distress of individual

distress institutions

Ultimate objective Avoid output (GDP) costs Consumer (investor / depositor)

protection

Correlations and common Important Irrelevant

exposure across institutions

Calibration of prudential Top-down Bottom-up

control

Model of risk (In part) endogenous Exogenous

Strategy 1. Strengthening regulations, standards and market discipline. Strategy 1. Strengthening regulations, standards and market discipline. Strategy 1. Strengthening regulations, standards and market discipline. Strategy 1. Strengthening regulations, standards and market discipline. Strategy 1. Strengthening regulations, standards and market discipline.

In this case, the implementation of regulations and international

standards as well as consistent market discipline from market players

and supervisors has to form the foundation of all financial activity. Diagram 3

Framework of Financial System Stability

Diagram 4

12 Key Standards in the Financial Sector

An active involvement in creating and maintaining a sound and stable national financial system

≈Achieving and maintaining price stability by maintaining monetary stability and promoting financial system stability for sustainable

national development∆.

• Regulations & standards e.g Basle Core Principles, CPSIP, IAS, ISA, etc. • Market Discipline

Early Warning Systems • Macroprudential

indicators • Microprudential

indicators (aggregat) • Stress test

• Internal coordination

• External coordination

• Lender of last resort - Normal times - Systemic crisis • Deposit Insurance • Crisis resolution

Macroeconomic Policies & Data Transparency

Institutional & Market

Infrastructure Regulation & SupervisionPrudential Financial

•Principles of Corporate

Governance •Core Principles for

Systemically Important Payment System •Market Integrity (Financial

Action Task Force/FATF on Anti Money Laundering)

•Insolvency

•International Accounting

Standard (IAS)

•International Standard

on Auditing (ISA)

• Code of Good

Practice in Fiscal Transparency

• Data Dissemination

Standard

• Core Principles for Effective Banking Supervision • Principles of Securities

Regulation • Core Principles for

Strategy 2. Intensifying research and surveillance Strategy 2. Intensifying research and surveillanceStrategy 2. Intensifying research and surveillance Strategy 2. Intensifying research and surveillanceStrategy 2. Intensifying research and surveillance

Intensifying research and surveillance is aimed at identifying, evaluating

and monitoring risks that threaten financial stability.

In general, there are two research activities:

- Developing tools to assess FSS.

- Identifying problems that threaten FSS.

Output/ product of these activities : tools, working papers, articles

and policy recommendations.

Meanwhile surveillance is focused on two primary goals:

- Assessing and monitoring problems and risks that threaten FSS.

- Proffering recommendations and providing input for policy

formulation to maintain FSS.

Diagram 5 tional Risk

Liqu

idity

Risk - Bank

- Non Bank Capital Bank

Financial Institution & Markets

Payment System

Domestic Finance- Household

- Coorporate Inter

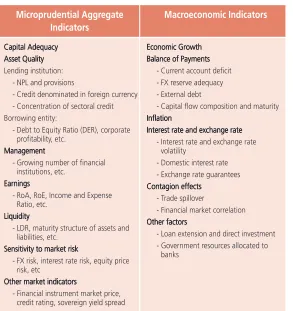

The instruments used to perform the surveillance function consist of

macroprudential and microprudential indicators, Financial Soundness

Indicators (FSI) and stress test.

Microprudential indicators are analyzed both aggregately and

individually for large banks with systemic effects. Besides,

macroeconomic conditions are the main concern in terms of

monitoring. Both aspects affect financial sector stability.

Table 5

Capital Adequacy Capital AdequacyCapital Adequacy Capital Adequacy Capital Adequacy Asset Quality Asset QualityAsset Quality Asset Quality Asset Quality Lending institution:

- NPL and provisions

- Credit denominated in foreign currency - Concentration of sectoral credit Borrowing entity:

- Debt to Equity Ratio (DER), corporate profitability, etc.

Management ManagementManagement Management Management

- Growing number of financial institutions, etc.

Earnings EarningsEarnings Earnings Earnings

- RoA, RoE, Income and Expense Ratio, etc.

Liquidity LiquidityLiquidity Liquidity Liquidity

- LDR, maturity structure of assets and liabilities, etc.

Sensitivity to market risk Sensitivity to market riskSensitivity to market risk Sensitivity to market risk Sensitivity to market risk

- FX risk, interest rate risk, equity price risk, etc

Other market indicators Other market indicatorsOther market indicators Other market indicators Other market indicators

- Financial instrument market price, credit rating, sovereign yield spread

Microprudential Aggregate Macroeconomic Indicators Indicators

Economic Growth Economic GrowthEconomic Growth Economic GrowthEconomic Growth Balance of Payments Balance of PaymentsBalance of Payments Balance of PaymentsBalance of Payments

- Current account deficit - FX reserve adequacy - External debt

- Capital flow composition and maturity Inflation

InflationInflation InflationInflation

Interest rate and exchange rate Interest rate and exchange rateInterest rate and exchange rate Interest rate and exchange rateInterest rate and exchange rate

- Interest rate and exchange rate volatility

- Domestic interest rate - Exchange rate guarantees Contagion effects

Contagion effectsContagion effects Contagion effectsContagion effects - Trade spillover

- Financial market correlation Other factors

Other factorsOther factors Other factorsOther factors

- Loan extension and direct investment - Government resources allocated to

Results of ongoing research and surveillance will be used as input to

determine future policy, namely prevention, correction and crisis

resolution.

The output from surveillance includes: weekly reports, material for

the monthly, quarterly and annual governors» board meetings and

the Financial Stability Review. In addition, several regular surveys are

conducted to support surveillance, for example a conglomerate

mapping survey, property surveys and a banking trust index survey

(in line with phasing out scheme).

Strategy 3. Improving coordination and cooperation. Strategy 3. Improving coordination and cooperation.Strategy 3. Improving coordination and cooperation. Strategy 3. Improving coordination and cooperation.Strategy 3. Improving coordination and cooperation.

This is accomplished through a Financial System Stability Forum (FSSF)

comprising of Bank Indonesia, the Ministry of Finance and the Deposit

Insurance Corporation. FSSF provides information and offers

recommendations to resolve issues related to financial system stability.

FSSF is a formal crisis management institution in Indonesia.

Startegy 4. Establishing financial safety net and crisis management. Startegy 4. Establishing financial safety net and crisis management.Startegy 4. Establishing financial safety net and crisis management. Startegy 4. Establishing financial safety net and crisis management.Startegy 4. Establishing financial safety net and crisis management.

In respect to this, there are two primary functions performed by the

central bank: crisis prevention and crisis resolution. A comprehensive

Financial Sector Safety Net (FSSN) consists of four elements: (i)

independent and effective supervision; (ii) lender of last resort; (iii) a

deposit insurance scheme; and (iv) effective crisis management.

Bank Indonesia, the Ministry of Finance and the Indonesian Deposit

Insurance Corporation have simultaneously developed FSSN to support

What has BI Accomplished?

2003

In 2003, a blueprint for Indonesian Financial System Stability was designed by the Banking Work stream unit from the Transformation Program Special Unit. The blueprint is favored by IMF and was approved by the Board of Governors for immediate implementation. The board also agreed to expand Bank Indonesia»s scope by promoting financial system stability in Indonesia. As a result, Bank Indonesia»s mission became ≈to achieve and maintain rupiah stability thorough the preservation of monetary and financial system stability to accomplish sustainable long-term economic development∆.

Implementation of the FSS function was performed by the Directorate of Banking Research and Regulation through the newly established Bureau of Financial System Stability (BFSS). BFSS was instituted using an organizational structure and flexible work pattern to ensure efficiency and effectiveness.

Diagram 6

Stable and Sound Financial System

Solid legal framework, clear definition of tasks and responsibilities as well as an effective coordination mechanism

Crisis Management

Policies

Ministry of Finance, BI,

IDIC Lender of

Last Resort

BI (LoLR) Oversight and

Supervision System

BI (as bank supervisor)

Deposit Insurance Corporation

Subsequently, semester surveillance results were published in the initial report known as Financial Stability Review No 1. In FSR 1, the importance of FSS to Indonesia is discussed as well as the performance and risks of the financial system. Additionally, strengthening financial system infrastructure to buffer pressure stemming from the financial system was reviewed. This includes human resource development, information systems, reviews and BFSS monitoring tools.

2004

At a developmental stage, BFSS issued a weekly report that routinely reviewed weekly FSS conditions, including a brief review of issues that could affect the financial system in the future.

Equally as important, beginning with the establishment of FSS, every three months the condition of FSS was reported at the board meeting, expanded to not merely cover bank conditions. The information format was also changed placing more emphasis on risk aspects.

Despite the limitation of human resources, BFSS also conducted research on FSS. The results were published in 2004 and are also available on Bank Indonesia»s website.

BFSS also recommended analyzing the systemic effects of the closure of several problematic banks.

To reinforce financial infrastructure, BFSS also compiles reviews on the Financial Sector Safety Net or FSSN, which include:

- An emergency funding facility (LoLR).

- The Deposit Insurance Corporation/IDIC, which can guarantee minor

not in line with best practices. BFSS also actively played a role in the

establishment of IDIC.

- Internal and external coordination centre related to FSS.

The Financial System Stability Committee (FSSC) was established, with a related task unit leader placed at BI to represent the coordination centre and information exchange for FSS.

In 2004, the Governor also requested BFSS to expand its tasks by examining ways to improve the banking intermediation function as a catalyst for real sector growth. In response, several primary products as well as products deemed below their maximum potential or avoided by banks were scrutinized. In addition, this was followed by Venture World Workshops held regularly in both urban and rural areas. The workshops facilitated meetings between the real sector, related government institutions and banks.

To improve surveillance tools, BFSS began mapping groups and conglomerates in Indonesia, considering they play a significant role in the financial system and economy.

BFSS also recommended GWM improvement based on banking LDR to absorb excess liquidity at banks. This would curb speculation and expand credit extension.

Surveillance results were published in the form of KSK 2 and 3, as well as weekly reports and several other reviews.

2005

BFSS also began compiling and published Bank Supervision Report (LPP) No 1, as part of BI»s role in supervising banks.

The previous year»s review, in terms of reinforcing financial infrastructure and collaborating with the government, had already begun to bare fruit, namely with the establishment of the Indonesian Deposit Insurance Corporation (IDIC) and the Financial System Stability Forum as the nerve centre for matters pertaining to Indonesian financial system stability. In 2005, Bank Indonesia was also active in international FSS forums, namely SEACEN, EMEAP and APEC.

A crucial measure was taken to strengthen the Financial Sector Safety Net where Bank Indonesia and the Ministry of Finance respectively issued a PBI and Finance Minister Decree (FMD) regarding an Emergency Funding Facility to overcome liquidity problems at banks with systemic effect.

2006

The year of 2006 witnessed the beginning of the Financial System Chartpack comprising of data and graphs of financial system performance. The Financial Stability Index was also examined, which could illustrate aggregate financial system conditions.

Weekly reports, RDG SSK, LPP No 2, KSK No 6 and KSK No 7 and LPP No 2 and several other results were improved and published during 2006.

Future Challenges

Financial sector globalization, compounded by technological advancement, has led to a more integrated financial system. Dynamic and diverse financial product innovation with higher complexity has exacerbated the triggers of financial system instability while also raising the difficulty of addressing such instabilities. In other words, the biggest challenge is to ensure that economic growth persists and crucial economic functions must continue to perform as normal despite mounting pressure.

Against this backdrop, it was agreed at the EMEAP Deputy»s Meeting to establish a Monetary and Financial Stability Committee to serve as a coordination and information exchange centre related to FSS issues at the regional level. Therefore, Bank Indonesia»s role in the region and beyond will become more significant yet challenging.

References

Aspachs,O, C.Goodhart, M.Segoviano, D.Tsomocos, L.Zicchino (2006),≈Searching for a Metric for Financial Stability∆, Special Paper No.167.

Batunanggar, S. (2006), ≈Financial Sector Safety Net: Literature Review And Practices in Indonesia∆, Financial Stability Review II-2006, No.8 March 2007, Bank Indonesia.

, (2003), ≈The Importance of Financial System Stability∆, Pengembangan Perbankan, Edition 99, March - April 2003.

Borio, C (2003), ≈Towards a Macroprudential Framework for Financial Supervision and Regulation∆, BIS Working Paper No 128.

Brealey, Richard A. et. al (2001), Financial Stability and Central Banks, Routledge and CCBS, Bank of England

Cihak, Martin (2006), ≈How Do Central Banks Write on Financial Stability?∆ IMF Working Paper (WP/06/163), June 2006.

Crocket, A (1997), ≈Why is Financial Stability a Goal of Public Policy?∆ Paper from the Maintaining Financial Stability in the Global Economy Symposium, 28-30 August, Federal Reserve Bank of Kansas City.

Evans et.al (2000), ≈Macroprudential Indicators of Financial System Soundness∆, IMF Occasional Paper No.192.

Fergusen Jr, R.W (2002), ≈Should Financial Stability be an Explicit Central Bank Objective?∆, Paper on Conference on Challenges to Central Banking from Globalized Financial System, IMF-Washington D.C, 16-17 September.

Houben, Aerdt, Jan Kakes, and Garry Schinasi (2004), ≈Towards a Framework for Safeguarding Financial Stability∆, IMF Working Paper (WP/04/101), June. McFarlane, I.J. (1999) ≈The Stability of the Financial System∆, Reserve Bank of Australia, Bulletin, August.

Mishkin, Frederick (2001), ≈Financial Policies and the Prevention of Financial Crises in Emerging Market Countries∆, NBER Working Paper No. 8087, January.

, (1997), ≈The Cause and Propagation of Financial Instability: Lessons for Policymakers∆, in Maintaining Financial Stability in a Global Economy: A symposium, U.S. Federal Reserve Bank of Kansas City.

Santoso,W. dan S.Batunanggar (2006), ≈Financial System Stability Framework∆, Bank Indonesia.

Glossary

Crisis management: Crisis management: Crisis management: Crisis management:

Crisis management: process which includes crisis identification, mitigation and resolution.

Crisis prevention: Crisis prevention: Crisis prevention: Crisis prevention:

Crisis prevention: the effort to prevent crisis through various policies including supervision and regulation (microprudential) of the financial markets and institutions, as well as mitigation (surveillance) for the financial system (macroprudential).

Crisis resolution: Crisis resolution: Crisis resolution: Crisis resolution:

Crisis resolution: the effort to overcome crisis when it occurs including restructuring and recapitalizing banks with systemic effect.

Cross-border integration: Cross-border integration: Cross-border integration: Cross-border integration:

Cross-border integration: financial integration that crosses international borders.

Discount window: Discount window: Discount window: Discount window:

Discount window: discounted credit provided by the central bank to another bank to overcome liquidity problems as a result of fund management mismatch.

Financial deepening Financial deepening Financial deepening Financial deepening

Financial deepening: the increased provision of financial services with a wider choice of services geared to all levels of society.

Lender of last resort: Lender of last resort: Lender of last resort: Lender of last resort:

Lender of last resort: the role of the central bank to provide loans to banks or other eligible institutions that are experiencing financial difficulty or are considered highly risky or near collapse.

Good Corporate Governance: Good Corporate Governance: Good Corporate Governance: Good Corporate Governance:

Good Corporate Governance: sound and healthy corporate governance

Monetary base: Monetary base: Monetary base: Monetary base:

Monetary base: the total amount of currency either circulated in the hands of the public or in the commercial bank deposits held in the central bank»s reserves.

Open market operations: Open market operations: Open market operations: Open market operations:

Open market operations: the buying and selling of government securities in the open market in order to expand or contract the amount of money in the banking system.

Reserve requirement: Reserve requirement: Reserve requirement: Reserve requirement:

Reserve requirement: requirements regarding the amount of funds that banks must hold in reserve against deposits made by their customers.

Risk mitigation: Risk mitigation: Risk mitigation: Risk mitigation:

Risk mitigation: efforts to reduce the possibility of risk occurrence. Stress testing:

Stress testing: Stress testing: Stress testing:

Stress testing: a simulation technique used on asset and liability portfolios to determine their reactions to different financial situations.

Surveillance: Surveillance: Surveillance: Surveillance:

FSS Related Sites

Badan Pengawasan Pasar Modal (Capital Market Supervisory Authority) www.bapepam.go.id

Bank Indonesia-Financial System Stability Bank Indonesia-Financial System StabilityBank Indonesia-Financial System Stability Bank Indonesia-Financial System StabilityBank Indonesia-Financial System Stability www.bi.go.id/web/id/SK001/SSK

Bank of England-Financial System Stability

www.bankofengland.co.uk/financialstability/index.htm Bank for International Settlements

www.bis.org/stability.htm Ministry of Finance www.depkeu.go.id Financial Stability Forum www.fsforum.org

International Monetary Fund (IMF)

- Financial System Assessment Program - Global Financial Stability Forum

www.imf.org/external/np/fsap/fsap.asp

International Organization of Securities Commissions www.iosco.org

Indonesian Deposit Insurance Corporation www.lps.go.id

Reserve Bank of Australia-Financial System Stability www.rba.gov.au/FinancialSystemStability/

World Bank