Full Terms & Conditions of access and use can be found at

http://www.tandfonline.com/action/journalInformation?journalCode=vjeb20

Journal of Education for Business

ISSN: 0883-2323 (Print) 1940-3356 (Online) Journal homepage: http://www.tandfonline.com/loi/vjeb20

Student Readership of Supplemental, In-Chapter

Material in Introductory Accounting Textbooks

Michael C. Toerner

To cite this article: Michael C. Toerner (2006) Student Readership of Supplemental, In-Chapter Material in Introductory Accounting Textbooks, Journal of Education for Business, 82:2,

112-117, DOI: 10.3200/JOEB.82.2.112-117

To link to this article: http://dx.doi.org/10.3200/JOEB.82.2.112-117

Published online: 07 Aug 2010.

Submit your article to this journal

Article views: 10

View related articles

ABSTRACT. In this study, the author

explored the extent to which students read the supplemental, in-chapter material con-tained in introductory accounting textbooks. A total of 668 students enrolled in 2002 spring and fall semesters at 3 universities in the southern United States participated in the study. The results showed that the par-ticipants considered elaborations on chapter topics to be the most important material they encountered. However, 55%–70% of the participants ignored all the materials involving Internet links, international accounting issues, and Microsoft Excel applications.

Key words: accounting curricula, education, textbooks

Copyright © 2006 Heldref Publications

Student Readership of Supplemental,

In-Chapter Material in

Introductory Accounting Textbooks

MICHAEL C. TOERNER SOUTHERN UNIVERSITY BATON ROUGE, LOUISIANA

ver the past decade, calls for changes in accounting education have come from a variety of sources. However, despite the source, the mes-sage has basically been the same: accounting educators have to (a) pre-sent accounting concepts in an interest-ing way, and (b) show students the real-world relevance of accounting as a profession.

The authors and publishers of intro-ductory accounting textbooks have responded to these challenges by including within the body of individual chapters material such as: (a) chapter-opening stories that deal with real-world accounting and business issues, (b) descriptions of how real companies use accounting information, (c) elaborations on or clarifications of topics discussed in the chapter, (d) discussions of inter-national accounting issues, (e) links to Internet resources designed to increase students’ understanding of chapter top-ics, and (f) activities intended to enhance students’ proficiency with Microsoft Excel. Although this material appears within the body of the chapter, it is supplemental in the sense that it is separate from and in addition to the chapter’s main narrative. This separate-ness is evident from either the material’s placement (generally in the margin) or the manner in which it is presented (usually in a sidebar). This supplemen-tal material is intended to enhance

stu-dents’ understanding of accounting, but are students actually reading it? In this article, I provide a preliminary answer to this question.

METHOD

During the spring and fall of 2002, students enrolled in the introductory accounting course at three universities completed a questionnaire concerning their readership of the supplemental material contained in their textbooks. The course in which the students were enrolled was the first of a two-course sequence that is generally taken by all business majors. The course is also a required or a recommended elective in certain nonbusiness fields.

Selection of Universities

Each university in the study was a public institution located in the southern United States. I selected the universities because the instructors at these schools agreed to participate in the study. The universities that participated in the study used the following textbooks: (a) Financial Accounting: Tools for Busi-ness Decision Making (2nd ed.) by Kimmel, Weygandt, and Kieso (2000); (b) Fundamental Financial Accounting Concepts (4th ed.) by Edmonds, McNair, Milam, and Olds (2003); and Financial Accounting: A Bridge to Decision Making (4th ed.) by Ingram

O

and Baldwin (2001). Table 1 shows the supplemental material contained in these textbooks.

Administration of Questionnaire

Instructors at university 1 adminis-tered questionnaires to students at uni-versity 1 in spring 2002. Students at the other two universities completed their questionnaires in fall 2002. Students completed the questionnaires near the end of the term, after the deadline for dropping classes had passed, for two reasons. First, it gave students an oppor-tunity to read all or most of the supple-mental material in their textbooks. Sec-ond, it prevented the study results from possibly being skewed by students who knew that they were eventually going to drop the class because they were per-forming poorly. Such students might

have devoted only a minimal amount of time to their accounting studies and, thus, might have read the supplemental material to a lesser extent than students

who were committed to completing the course.

Construction of Questionnaire

Questionnaires were specific to each university and contained one section for each of the supplemental items found in the textbook used by that university. Within each section of the question-naire, students indicated the extent to which they had read the supplemental item described in that section as fol-lows: (a) I read all of the items (e.g., I read every chapter-opening story in the textbook), (b) I read most of the items, (c) I read some of the items, and (d) I read none of the items.

Participants in the Survey

As shown in Table 2, 668 students participated in the study. At university 1, 12 different instructors taught 27 sec-tions of introductory accounting in

TABLE 1. Supplemental, In-Chapter Material Contained in University Accounting Textbooks

Material included

Type of material University 1 University 2 University 3 Chapter-opening stories Yes Yes No Descriptions of how real companies

use accounting information Yes Yes Yes Elaborations upon chapter topics Yes No Yes Discussions of international

accounting issues Yes Yes No Links to internet resources No No Yes Microsoft Excel activities No No Yes

Note. The textbooks used by the universities in the study were Financial Accounting: Tools for Business Decision Making(2nd ed.) by P. D. Kimmel, J. J. Weygandt, and D. E. Kieso (2000); Fundamental Financial Accounting Concepts(4th ed.) by T. P. Edmonds, F. M. McNair, E. E. Milam, and P. R. Olds (2003); and Financial Accounting: A Bridge to Decision Making(4th ed.) by R. W. Ingram and B. A. Baldwin (2001).

TABLE 2. Characteristics of Study Participants (N= 668)

Characteristic % of students Gender

TABLE 3. Summary of Supplemental Accounting Textbook Material Read by Students

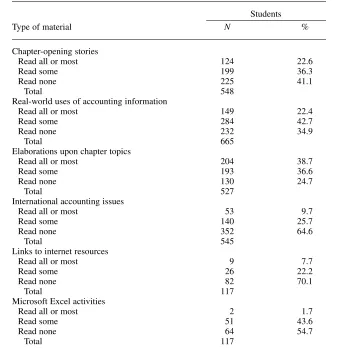

Students Type of material N % Chapter-opening stories

Read all or most 124 22.6 Read some 199 36.3 Read none 225 41.1

Total 548

Real-world uses of accounting information

Read all or most 149 22.4 Read some 284 42.7 Read none 232 34.9

Total 665

Elaborations upon chapter topics

Read all or most 204 38.7 Read some 193 36.6 Read none 130 24.7

Total 527

International accounting issues

Read all or most 53 9.7 Read some 140 25.7 Read none 352 64.6

Total 545

Links to internet resources

Read all or most 9 7.7 Read some 26 22.2 Read none 82 70.1

Total 117

Microsoft Excel activities

Read all or most 2 1.7 Read some 51 43.6 Read none 64 54.7

Total 117

spring 2002. I used a random number table to select 12 sections (one for each instructor) for inclusion in the study. University 2 offered 5 sections of intro-ductory accounting in fall 2002. I included all of these in the study. Uni-versity 3 had 13 sections of introductory accounting during the fall 2002. The on-site survey coordinator at university 3 was only able to administer question-naires in 6 of these sections.

RESULTS

Table 3 presents an overview of the study results and provides the basis for the following observations. First (and perhaps most noteworthy given the purpose of the study), with the excep-tion of material that clarified or elabo-rated on in-chapter topics, between approximately 35% and 70% of the

participants ignored all of the supple-mental material they encountered. The highest nonreadership rates were for supplemental material involving links to Internet resources (70.1%), interna-tional accounting issues (64.6%), and Microsoft Excel applications (54.7%).

Second, 38.7% of the participants read all or most of the supplemental material that elaborated on topics that were discussed in the body of the chap-ter. This was about 16% higher than the percentage of students who read all or most of (a) the chapter-opening stories (22.6%) and (b) the descriptions of real-world uses of accounting information (22.4%).

Third, 43.6% of the students who were exposed to the Microsoft Excel activities and 42.7% of the students who encountered material that described real-world uses of accounting information

read some (but not all or most) of the material. These rates were roughly 6% higher than the rates at which students read some of the chapter-opening stories (36.3%) and some of the material that clarified in-chapter concepts (36.6%).

Table 3 presents aggregate readership statistics for the supplemental items described therein. However, it is possi-ble a student’s college major, gender, or grade point average (GPA) might have influenced that readership.

Effect of Demographic Factors on Readership Rates

College Major

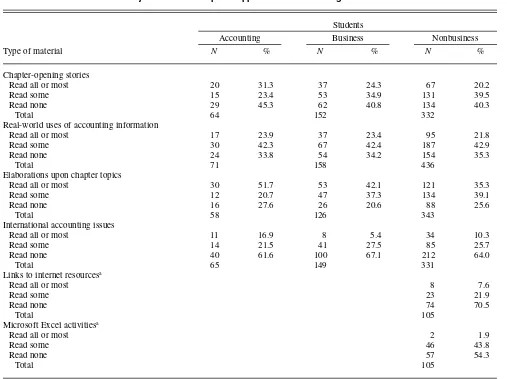

Table 4 shows the extent to which the readership of supplemental material was affected by a student’s major. The table indicates that, in general, accounting majors read all or most of a given type

TABLE 4. Effect of Students’ Major on Readership of Supplemental Accounting Textbook Material

Students

Accounting Business Nonbusiness Type of material N % N % N % Chapter-opening stories

Read all or most 20 31.3 37 24.3 67 20.2 Read some 15 23.4 53 34.9 131 39.5 Read none 29 45.3 62 40.8 134 40.3

Total 64 152 332

Real-world uses of accounting information

Read all or most 17 23.9 37 23.4 95 21.8 Read some 30 42.3 67 42.4 187 42.9 Read none 24 33.8 54 34.2 154 35.3

Total 71 158 436

Elaborations upon chapter topics

Read all or most 30 51.7 53 42.1 121 35.3 Read some 12 20.7 47 37.3 134 39.1 Read none 16 27.6 26 20.6 88 25.6

Total 58 126 343

International accounting issues

Read all or most 11 16.9 8 5.4 34 10.3 Read some 14 21.5 41 27.5 85 25.7 Read none 40 61.6 100 67.1 212 64.0

Total 65 149 331

Links to internet resourcesa

Read all or most 8 7.6

Read some 23 21.9

Read none 74 70.5

Total 105

Microsoft Excel activitiesa

Read all or most 2 1.9

Read some 46 43.8

Read none 57 54.3

Total 105

aAn extremely low number of accounting majors and business majors prevented the calculation of meaningful readership statistics for these categories.

of supplemental material more fre-quently than business majors, who, in turn, read all or most of an item more often than nonbusiness majors.

Second, Table 4 reveals that the per-centage of students who read all or most of the material that elaborated on chap-ter topics was higher than the corre-sponding rates for all other types of sup-plemental material. This was true for all students, regardless of major.

Third, for a given type of supplemen-tal item, a student’s major generally had little effect on the percentage of stu-dents who did not read any of the items.

Gender

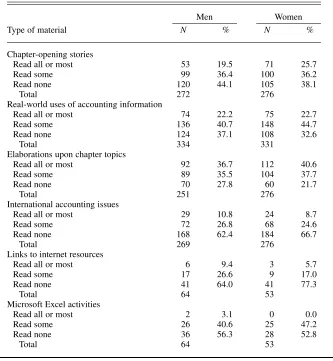

Table 5 shows the impact that gender had on student readership rates. The table indicates that women read all or most of the following material more often than men: (a) chapter-opening sto-ries, (b) discussions of how accounting information is used in business, and (c)

material that elaborated on chapter top-ics. The reverse was true for internation-al accounting issues, Internet links, and Microsoft Excel applications.

Second, the percentages of both men and women who read all or most of the material that elaborated on chapter top-ics were much higher than the corre-sponding percentages for the other types of supplemental material.

Third, Table 5 demonstrates that, with the exception of Internet links, gender did not greatly influence the extent to which students ignored a given type of supplemental material. For Internet links, the nonreadership rate for female students was 13% higher than for men.

Grade Point Average

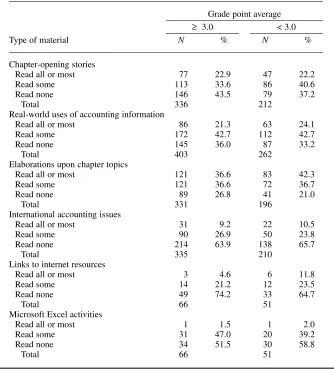

Table 6 shows the relationship between students’ GPA and readership of supplemental material. For the most part, the percentage of students with a

GPA below 3.0 who read all or most of a given type of supplemental material was greater than the percentage of stu-dents with at least a 3.0 GPA who read the same material.

Second, students, regardless of GPA, read all or most of the material that elaborated on chapter topics to a greater extent than they read the other types of supplemental material.

Third, students with at least a 3.0 GPA tended to ignore the supplemental material more than students whose GPA was below 3.0. The main exception to this tendency was material that involved Microsoft Excel activities.

DISCUSSION

Textbook authors write their books with a variety of goals in mind. They choose particular words and examples and arrange material in a certain way because they believe that doing so will best accomplish their goals.

In a similar way, students approach a class and, by necessity, the textbook that accompanies the class with a set of goals. As a result, it seems reasonable to assume that the extent to which a stu-dent will interact with a given type of textbook material is determined, at least in part, by the student’s perception of the degree to which the material, if stud-ied or otherwise acted on, will help the student achieve his or her goals. Mater-ial that is perceived as helpful in meet-ing a goal will receive more time and attention than material that is deemed to be of little help. Material that receives a substantial amount (how that term is defined is not relevant to this discus-sion) of a student’s time can be said to be important whereas material that receives little or no time can be said to be unimportant.

I did not ask students to indicate the amount of time they spent studying a particular type of supplemental material. However, they were asked to describe, on a 4-point scale ranging from read all to read none, their involvement with the material. In doing so, the study provides evidence (albeit indirect) about stu-dents’ perceptions of the importance of the supplemental material they encoun-tered. Students who read all or most of a given type of material considered it

TABLE 5. Effect of Students’ Gender on Readership of Supplemental Accounting Textbook Material

Men Women Type of material N % N % Chapter-opening stories

Read all or most 53 19.5 71 25.7 Read some 99 36.4 100 36.2 Read none 120 44.1 105 38.1

Total 272 276 Real-world uses of accounting information

Read all or most 74 22.2 75 22.7 Read some 136 40.7 148 44.7 Read none 124 37.1 108 32.6

Total 334 331 Elaborations upon chapter topics

Read all or most 92 36.7 112 40.6 Read some 89 35.5 104 37.7 Read none 70 27.8 60 21.7

Total 251 276 International accounting issues

Read all or most 29 10.8 24 8.7 Read some 72 26.8 68 24.6 Read none 168 62.4 184 66.7

Total 269 276 Links to internet resources

Read all or most 6 9.4 3 5.7 Read some 17 26.6 9 17.0 Read none 41 64.0 41 77.3

Total 64 53

Microsoft Excel activities

Read all or most 2 3.1 0 0.0 Read some 26 40.6 25 47.2 Read none 36 56.3 28 52.8

Total 64 53

important. Material that was not read at all was regarded as unimportant. Read-ership levels between these extremes signified that the material was some-what important.

In light of the aforementioned, then, the findings reported in Tables 3–6 may be interpreted as follows. First, the participants in the study (regardless of major, gender, or GPA) considered elaborations on and clarifications of chapter topics to be the most important type of supplemental material they encountered.

Second, between 35% and 70% of the participants thought that 5 of the 6 types of supplemental material to which they were exposed were unim-portant. The items deemed unimportant and the percentage of students who felt this way were as follows: (a) links to Internet resources (70%), (b) discus-sions of international accounting issues

(65%), (c) Microsoft Excel applica-tions (55%), (d) chapter-opening sto-ries (41%), and (e) descriptions of real-world uses of accounting information (35%).

Third, accounting majors read all or most of a given type of supplemental material more frequently than business majors, who, in general, read all or most of an item more often than nonbusiness majors.

Fourth, the effect of gender on read-ership was mixed. For three types of supplemental items (see Table 5), women read all or most of the materials more frequently than men. The reverse was true for three other types of materi-als. Finally, as far as the effect of GPA on readership was concerned, students with a GPA below 3.0 generally read all or most of the supplemental material more often than students whose GPA was at least 3.0.

Implications

The findings and conclusions dis-cussed above have several implications for the authors of future introductory accounting textbooks. First, textbook authors should consider incorporating into the body of the chapter elaborative material that is currently supplemental in nature. The students in this study believed that this material was the most important supplemental material they encountered. Nevertheless, about 25% of the participants ignored it altogether and about 37% read only some of it. Relocating the supplemental, elabora-tive material to the body of the chapter might increase the likelihood that it will be read by all or most of the students who are exposed to it.

Second, textbook authors should con-sider eliminating supplemental material that (a) involves links to Internet resources, (b) describes international accounting issues, and (c) requires stu-dents to use Microsoft Excel. A large portion of the students in the study (70%, 65%, and 55%, respectively) regarded this material as unimportant, as evidenced by the fact that they did not read any of it.

Removing this material from text-books would not adversely affect a stu-dent’s learning experience in introduc-tory financial accounting. Indeed, as a result of their lifestyles or their expo-sure to computer software, most of today’s students probably already have a working knowledge of both the Inter-net and Microsoft Excel. In addition, because one does not have to be famil-iar with international accounting issues to understand basic accounting princi-ples, deleting the international material would in no way hinder students’ efforts to learn introductory accounting.

Third, as evidenced by the percent-age of students who read at least some of the material, the chapter-opening stories and the descriptions of how accounting information is used in the business world were clearly of interest to the participants. Despite this fact, both types of material were totally ignored by over one-third of the dents in the study. To capitalize on stu-dents’ interest in this material, textbook authors should consider working it into

TABLE 6. Effect of Grade Point Average on Readership of Supplemental Accounting Textbook Material

Grade point average

≥ 3.0 < 3.0 Type of material N % N % Chapter-opening stories

Read all or most 77 22.9 47 22.2 Read some 113 33.6 86 40.6 Read none 146 43.5 79 37.2

Total 336 212 Real-world uses of accounting information

Read all or most 86 21.3 63 24.1 Read some 172 42.7 112 42.7 Read none 145 36.0 87 33.2

Total 403 262 Elaborations upon chapter topics

Read all or most 121 36.6 83 42.3 Read some 121 36.6 72 36.7 Read none 89 26.8 41 21.0

Total 331 196 International accounting issues

Read all or most 31 9.2 22 10.5 Read some 90 26.9 50 23.8 Read none 214 63.9 138 65.7

Total 335 210 Links to internet resources

Read all or most 3 4.6 6 11.8 Read some 14 21.2 12 23.5 Read none 49 74.2 33 64.7

Total 66 51

Microsoft Excel activities

Read all or most 1 1.5 1 2.0 Read some 31 47.0 20 39.2 Read none 34 51.5 30 58.8

Total 66 51

the body of the chapter. Once it is no longer offset on a textbook page, stu-dents might read all or most of the material with greater frequency.

Future Research

This study was limited to three univer-sities in the southern United States. Addi-tional studies are needed to determine the extent to which the present study’s find-ings are representative of all students enrolled in introductory accounting courses. In addition, future researchers should consider quantifying student

readership (e.g., “I read less than 25% of the indicated item”) rather than relying on subjective terms such as some and most. Making this change would provide a more accurate picture of the extent to which students read the supplemental, in-chapter material found in introductory accounting textbooks.

NOTE

The author acknowledges the help of Anne Wheat Cox, who assisted in coding the data on which this article is based. The author also acknowl-edges the comments of two anonymous reviewers, whose remarks helped strengthen this article.

Correspondence concerning this article should be addressed to Dr. Michael C. Toerner, Southern University, School of Accountancy, 218 T. T. Allain Hall, Baton Rouge, LA 70813

E-mail: drmike749@aol.com

REFERENCES

Edmonds, T. P., McNair, F. M., Milam, E. E., & Olds, P. R. (2003). Fundamental financial accounting concepts (4th ed.). New York: McGraw-Hill Irwin.

Ingram, R. W., & Baldwin, B. A. (2001). Finan-cial accounting: A bridge to decision making (4th ed.). Cincinnati, OH: South-Western Col-lege Publishing.

Kimmel, P. D., Weygandt, J. J., & Kieso, D. E. (2000). Financial accounting: Tools for business decision making(2nd ed.). New York: Wiley.