Piyapas Tharavanij for his insight and knowledge to improve understanding on valuation along with adoption of business knowledge. Also, to all my professors at CMMU for all knowledge in any related filed. Kritsakorn, my best partner for all time during my academic years, for his support and sharing not only about the lesson but also for being a profession in my career.

Finally, I would like to thank all my friends, especially Mr. Voratach and Mr. Veeravith for their support, encouragement and joy, and for sharing a lot of life experience during the time as a master's student. This thematic article showed how to value the stock price of The Global Power Synergy Public Company Limited (GPSC), applying the concept of the Free Cash Flow to Firm (FCFF) model. The free cash flow to the company represents the value of the company's operations resulting from the square root of the company's value, derived from future earnings.

VALUATION

Highlights

- New capacity to drive revenue growth

- Opportunity from investment in associate and joint-venture Company diversified its investment to 3 countries, USA, Laos and Japan

- Economic growth creates growing opportunity

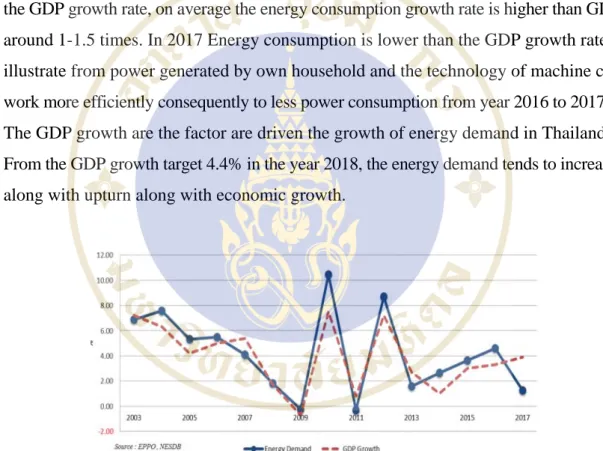

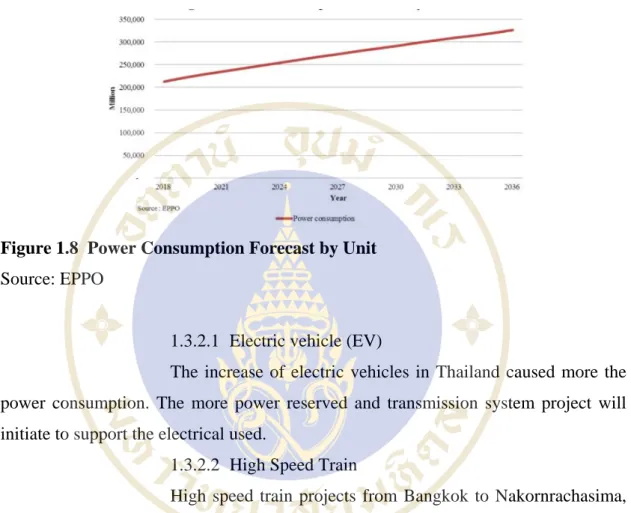

In addition, the company invests in the expansion of the plant in Rayong province, to support the expansion of the economy from the Eastern Economic Corridor (EEC) and also to support the business growth of the PTT Group. With Thailand's expected GDP in 2018 and 2019 at 4.4% and 4.2%, energy consumption is expected to grow at 1.5 times higher than GDP, from the correlation between GDP and energy demand consumption in Thailand . Furthermore, government policy supports more demand growth in many projects; Electric vehicles, high-speed rail and the Eastern Economic Corridor (EEC).

Business Description

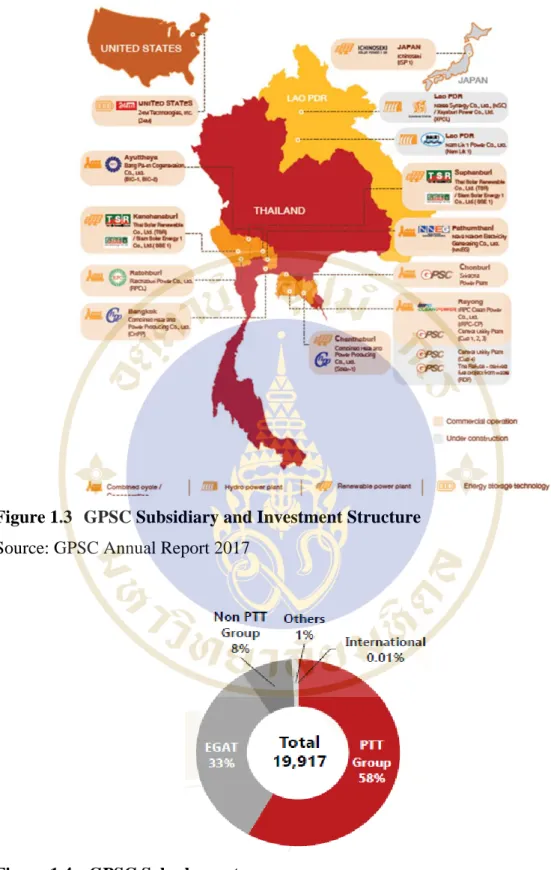

- Subsidiaries and Capacity

- Merger & Acquisition

By 2020, 4 more power plants (Rayong Power Plant CUP4, Navanakorn Power Generation Expansion Phrase, Xayaburi Power and Nam Lak 1 Power) will be fully operational. In 2018, PTT signed the contract to purchase the shares of Glow Energy Plc, the second largest asset size in Thailand's energy industry, the SET-listed company with major shares owned by Engie SA, the French utility giant electric that operates in many nationalities. The agreement is to buy all 69.11% of the shares from Engie SA and to buy the remaining part by tender offer.

After the merger, GPSC's power generation capacity will be the third largest in the industry with an approximately three-fold increase from committed electricity from 1,940 MW to 4,835 MW also with higher steam capacity from 1,585 ton/hour to 2,791 ton/hour. However, the deal is under review by the Energy Regulatory Commission, with concerns over the impact of the merger where GPSC may become a monopoly power producer in Rayong province.

Macro-Economic Analysis

- Macro outlook support industry growth

- Forecast of power consumption growth

- Natural gas outlook

- Renewable situation outlook

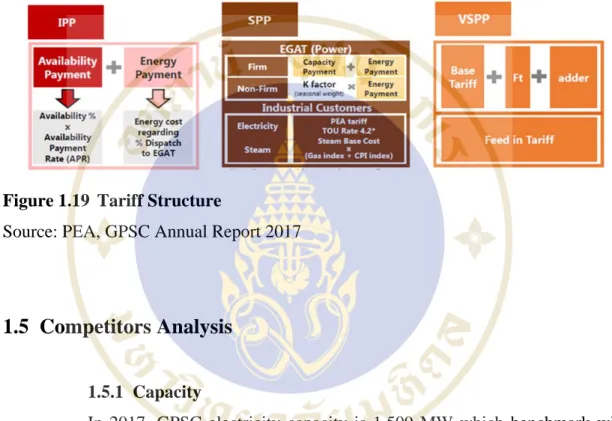

- Tariff Structure

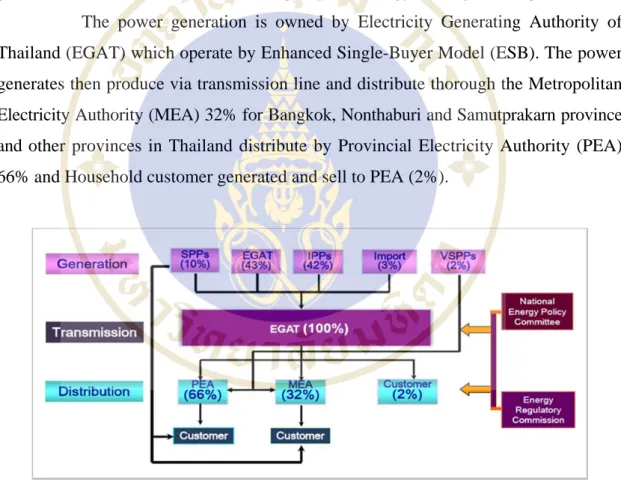

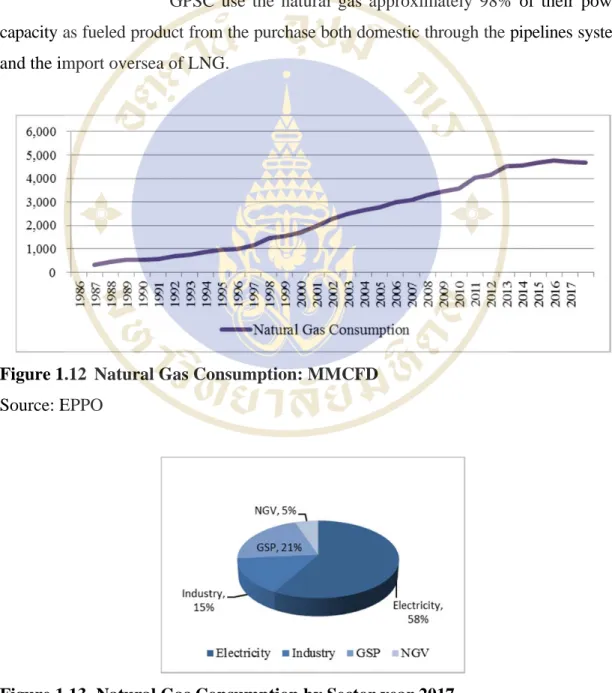

From the energy consumption by sector from the year 2017 (Figure 1.6 Electricity consumption by sector, 2017), the largest electricity consumption from the industrial sector in 48%, the second is business 25% and the residential sector 24% in total. Thailand's electricity generation classified by fuel type Natural gas is the most used power source in the country for 60% (Figure 1.7 Power consumption classified by fuel type) from gas-fired power plants from natural gas came from the Gulf of Thailand. In the short term, the natural gas from the Gulf of Thailand will go out of business in the next 4-5 years.

Imports of natural gas from Myanmar will be used to offset the electricity generated. The domestic gas was distributed through the pipeline system and transported abroad and then stored in the form of liquefied natural gas (LNG). The increase was driven by escalating global oil prices and government subsidies for the use of natural gas vehicles (NGVs) also include household use of liquefied natural gas (LNG).

The source of natural gas was separated between domestic supply from production in the Gulf of Thailand (73%) and the Andaman Sea. GPSC uses natural gas for approximately 98% of their power capacity as a fuel product from purchasing both domestically through the pipeline system and overseas imports of LNG.

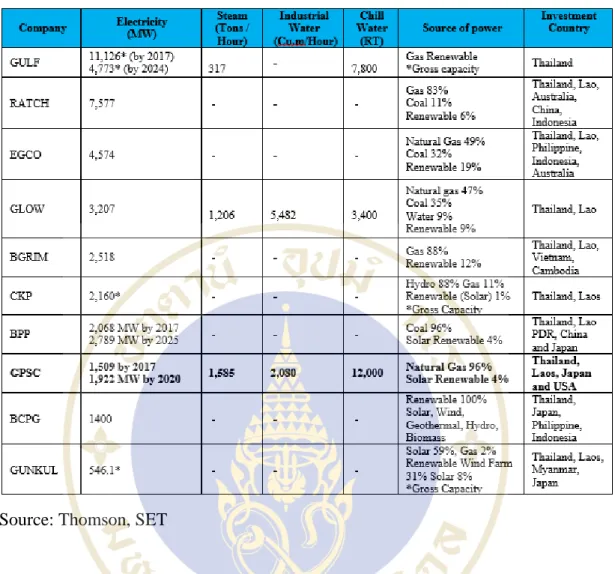

Competitors Analysis

- Capacity

- Diversify Asset portfolio (Source of power, Renewable Power Plant) GPSC invested overseas to diversify assets portfolio. GPSC major operation

- Profit & Return on Investment

GPSC's main business is in Thailand with the natural gas resources of PTT (its parent company). For renewable energy, which is expected to have high growth in the future, GPSC has currently invested in 3 factories in Thailand and 1 in Japan. US investment is in other business such as battery research and development in anticipation of better performance and advantage over others in the industry.

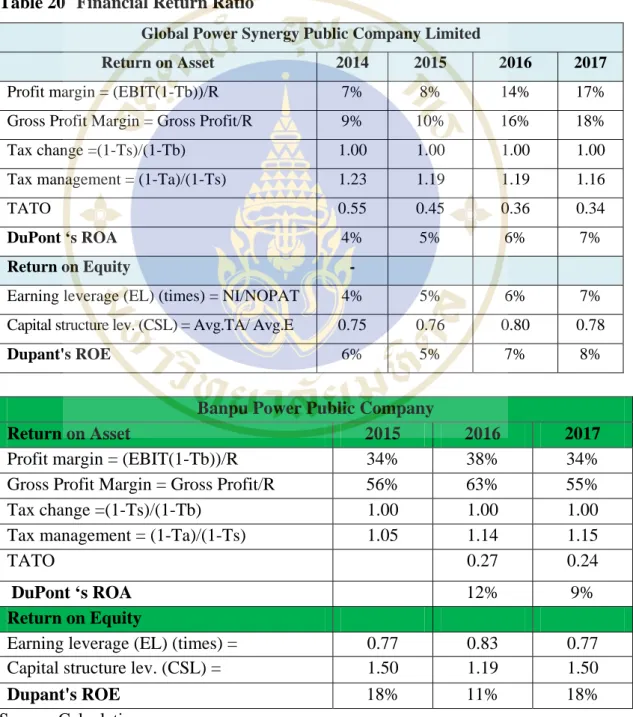

Similar to GPSC, other companies in the segment are invested in foreign country (Lao, Japan, Vietnam, Cambodia, PDR, Philippines, Indonesia and Myanmar) with the exception of Gulf based only in Thailand. BCPG company has the highest net profit margin than other firms with 45.93% from their use of 100% renewable energy as their energy source. From the financial performance the highest earnings per share is EGCO 22.45 compared to other companies in the industry are in the range between 0.09 and 0.62.

Return on Equity (ROE), Glow, Gulf and BGRIMM have the highest range in the segment with an average ROE of 12, while GPSC is on the lower end compared to a below average ROE ratio of 8.9. In terms of debt-to-equity ratio, BPP has the lowest among peers, while GPSC and RATCH have low D/E due to lower leverage.

Discounted Cash Flow Valuation (DCF)

- Investment Summary

- Free Cash Flow to Firm (FCFF) Table 1.15 Free Cash Flow to Firm 2018 (F)

- Value of non-operating assets

- Value of GPSC Share

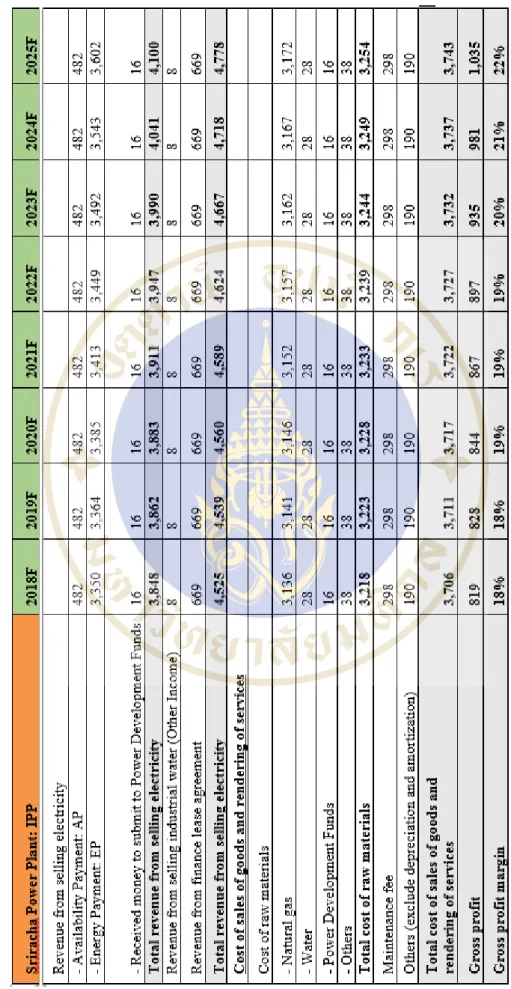

The remaining years of GPSC's solid project life are 4 Sriracha Power (SPP), Rayong Central Utility Plant (CUP1-4), IRPC Clean Power (IRPC) and Combine Heat and Power Producing Company Limited (CHPP). Sriracha Power Plant is an IPP: the power plant can only distribute EGAT (subject to PPA). A plant currently selling chilled water at 30% capacity will then be used as an assumption.

The dividend income in 2017 is selected based on its minimum income received during the period 2015-2017. Other income is expected with 1% ratio to revenue from sales and service delivery, based on historical income statement usual size ratio. The company gets tax incentive benefit from its investment by getting promotion certificate from Thailand Board of Investment (BOI). We project based on 1) historical income tax rate for the past 3 years 2) the company will have effective tax rate as Table 1.11 GPSC Corporate Income Tax.

Property, plant and equipment is charged at a 4% or 25-year depreciation period because major assets are plant and equipment that have a 25-year useful life. The projection is using an assumption of 4 years of average AR days, inventory days and AP days. Rayong Utilities Power CUP4 is expected to be completed within 2019, so the remaining investment needs must be included within the 2019 period.

Assuming we can maintain market share in the industry, we expect to grow at the same pace. We credit the spread to the firm's debt rating to reflect the cost of borrowing the firm's financial risk. As of September 30, 2018, the value of the company's non-operating assets is THB 4,760 million, cash and cash equivalents of THB 4,754 million and the current investment amount is THB 6 million.

The company has terminal growth as the expectation of capacity growth of the Thailand industry CAGR 2.2%, the value will be 57.23 THB per share.

Financial Analysis

- Market and Financial Risk

- Reputation Risk

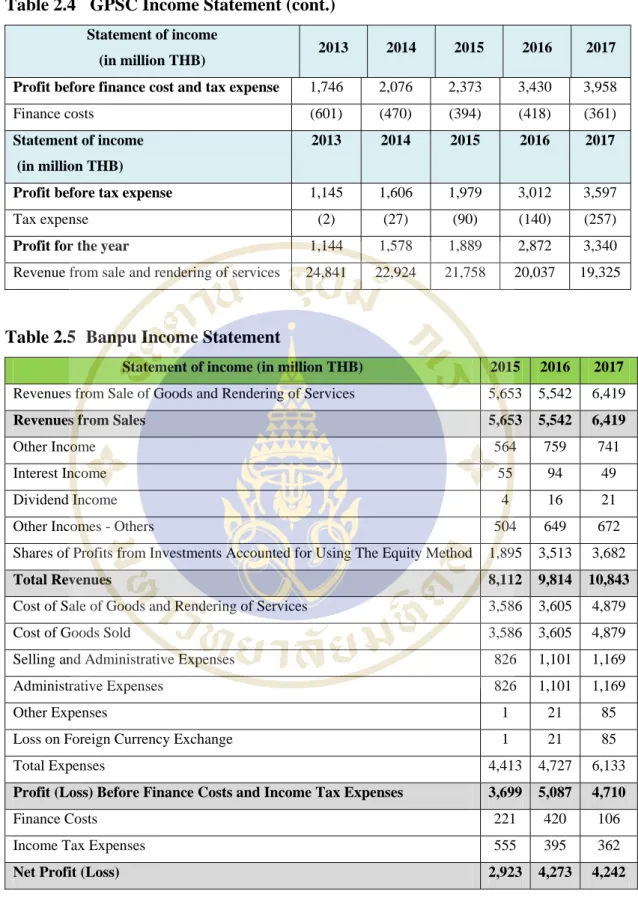

Short-term liabilities amount to 7% and long-term liabilities to 26%, a significant total volume of long-term borrowing 16% and debentures 8%. Compared to BPP, the total size of equity capital is equal to 83.4% majority from share capital 65.1% and retained earnings 11.6%. Trend analysis, in GPSC's income statement, sales growth revenue grew 78% lower than competitor BPP which grew 114% in 2017, but GPSC's net profit has higher growth at 292%% compared to BPP at 145% due to BPP. has a high share of cost of goods sold and PSA costs.

The trend analysis of the balance sheet, asset side, GPSC shows an increase in cash and cash equivalents up to 62% and trade receivables increase up to 73%. BPP has an increase in cash and cash equal to 97.377%, of long-term debt and trade receivables to 103%. The fixed asset GPSC has increased the tangible fixed assets to 150% and the investments in associates to 354%, respectively from their new power plant and the investment in Associates Company.

The BPP has also increased tangible fixed assets to 203% and investments in associates and joint ventures to 209%. The BPP has increased short-term borrowings to 517% and other short-term liabilities increased to 105%. For financial risk ratio, GPSC has higher liquidity from the current ratio equal to 2.43 times compared to BPP equal to 0.84 times.

In terms of Cash Conversion Cycle (CCC), GPSC has 34.94 days which is slightly lower than BPP 37.46 days. In terms of solvency risk, debt to equity ratio BPP has lower debt to equity equivalent to 0.20 times compared to GPSC has 0.39 times respectively from part of long-term borrowing. The operation has risk in the process, while product or waste must be handled systematically.

For IU, customers have a long-term purchase agreement, but upon expiry there is a risk that it will not be renewed. Under many rules that must be adhered to, actions not adhered to will be suspected as legally unlawful. The specific function of the unit is to supervise all functions in the group to ensure strict compliance with applicable rules and regulations.

GPSC Organization Chart

GPSC Business Portfolio

GPSC Value Chain

History Natural Gas Pool Price

GPSC Revenue Share

Financial Analysis

- Income Statement

Net of current portion of long-term liabilities Long-term loans from financial institutions net of current portion of postal employee benefit.

Common Size Analysis

- Income Statement Common size Analysis

- Common Size of Financial Position Statement

Forecast Financial Statement .1 Income Statement