HOW LATTER LIFE SATISFACTION INFLUENCES was submitted to the College of Management, Mahidol University. In this study, retirement planning and retirement preparation are investigated in terms of when and how the individual initiated the plan, how different the reality of retirement life was from the expectation, how they prepared for late life , what were the challenges they experienced in preparation. , and how they adapted to the change. Previous studies in the literature on retirement preparation and factors influencing retirement planning are reviewed.

Qualitative research is conducted by conducting in-depth interviews with 8 Thais aged 60 and over who are in late life and have experienced the journey of retirement planning. The purpose of this study is to understand the journey to retirement life and explore the perspective of how retirement planning affects an individual's life after retirement. Knowing the difference in the retirement gap could be useful in educating the younger generation to prepare for the future and show them the importance of retirement planning.

Then, conduct in-depth interviews with the group of people over 60 to understand their retirement planning journey, as well as find a recommendation from those who have experienced retirement life that they would like to share with the young generation.

Preparation for retirement

Retirement is a stage of life for those who have completed their working life, free from work obligations, transitioning to a new era that allows them to pursue activities of their own choosing that they want to do before (Mishra, 2019). According to the Consumer Financial Protection Bureau (2015), economic well-being plays an important role in enjoying retirement. They have good financial control, can support current and unforeseen financial problems, help them achieve financial freedom that allows them to live the life they want.

To prepare retirement savings, one must estimate the amount of money needed to live over a lifetime at the expected standard of living (Reiss & Watson, 2019). Furthermore, Cheung; Mooney's quantitative studies (as cited in Palaci et al., 2018) support that perspective taking influences one's behavior toward goal achievement.

Influence factors on retirement planning

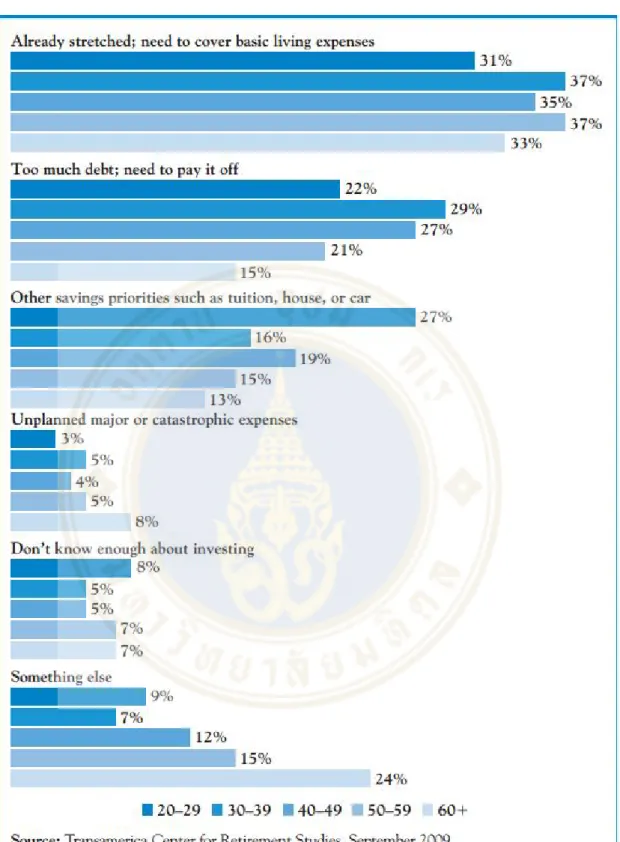

Therefore, as time goes on, they have less time to save, and most workers admit that even if they work until the age of 65, they still do not have enough savings for retirement. Additionally, people are living longer these days, so more retirement savings are needed (Reiss & Watson, 2019). Still, worryingly, most workers, especially those in their 20s and 30s, don't know much about investing for retirement because they have other financial priorities to take care of first (Figure 2.1), such as basic living expenses. expenses, house and/or car expenses, and debt to pay (Transamerica Center for Retirement Studies, 2010).

Some said they have to spend on major car repairs, major home repairs, illness or injury (self/partner), or loss of wages, where these events affect their savings (Pew Charitable Foundations, 2015). Without sufficient retirement savings, Reiss & Watson (2019) reveal two possible alternatives, either they accept that they will run out of money and try to live with what they have at hand, or they will have to work many more years to catch up. failure to maintain their expected standard of living in retirement.

Health-related spending

Retirement savings must take into account an unexpected factor that could affect savings, such as inflation, future healthcare costs and returns on investments (Max, 2018). When it comes to inflation, the same amount of money in another period may not have the same value as its current value because it affects the cost of living in the future (Reiss & Watson, 2019). Therefore, one way to beat inflation is to invest in high-yield investments such as bond yields, stock markets and money market funds, and also avoid investing in a low-yield market where this could lead to a depreciation of the monetary value .

However, Jefferson's (2007) qualitative research project found that some participants decide to invest in real estate where it is sometimes difficult to convert the asset into cash. It is counted as their wealth, but it is not what they can use for consumer spending. Healthcare costs in later life are very high, so if a person does not have health insurance, they may face financial difficulties during the recovery process (Saha, 2019).

Moreover, it has been found that many low- and middle-income Indian households are pushed into poverty situations due to healthcare-related obligations.

Dissaving by elderly

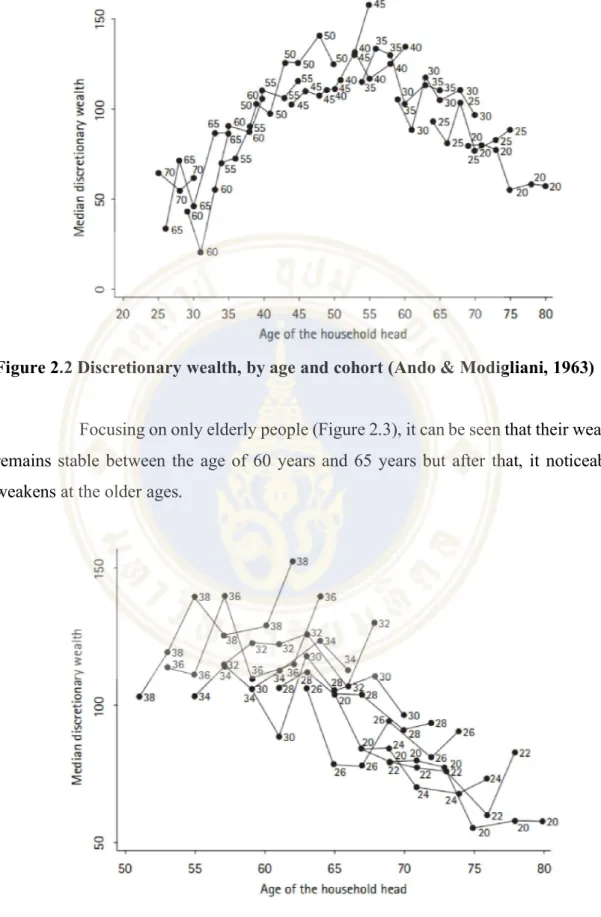

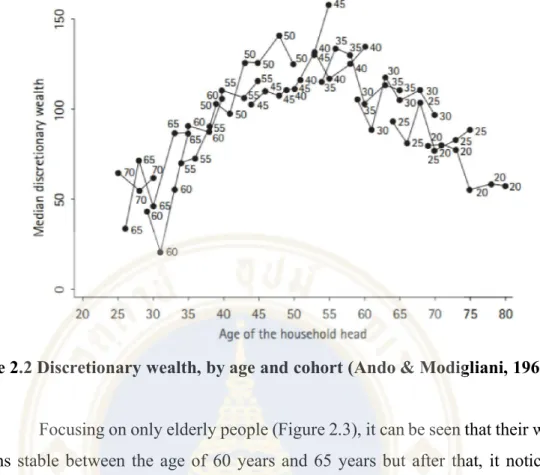

While annual medical expenses for people aged 65 years are about $11,752, the expenses rise to $31.99 of those who are 85 years old, which is about 170% increase. By focusing only on the elderly (Figure 2.3), it can be seen that their wealth remains stable between the ages of 60 years and 65 years, but after that it weakens noticeably at the older ages. In addition to normal consumption such as household costs, food and supply costs, the additional spending of the elderly over early and mid-life are these 4 major costs as follows (McKearn, 2018);

Home maintenance and living situation costs – Changing their home is necessary, change the circumstances in a way that suits their ages, increase safety. Transport costs – Depletion of bodily functions such as sight, hearing or body movement affects the ability to drive. Personal care costs – As mentioned earlier, frailty limits the elderly's ability to live on their own, and therefore they need someone to help them with daily life.

Health care costs - With chronic diseases and exhaustion of body systems, this causes higher medical expenses.

Financial preparation

Organize your income and expenses into “buckets” – Divide your savings into many accounts for any purpose, such as basic living, lifestyle expenses, emergency or healthcare expenses, etc. Consider professional advice – Let them help you create the big picture of a long-term goal, planning for future expenses and optimizing taxes. In summary, the literature review shows that most people want to have a comfortable life and can live the way they want, but for this they need a healthy financial income.

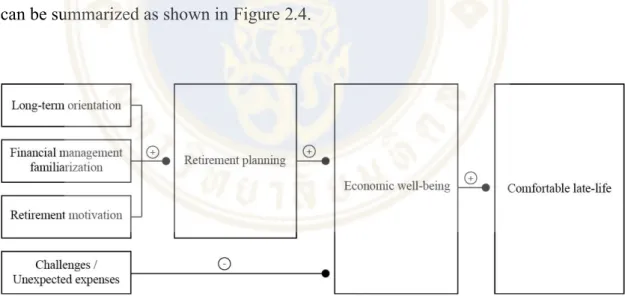

It can be concluded that those people with a long-term orientation, financial knowledge and retirement motivation appear to have a greater financial curriculum, which leads to greater financial well-being. In contrast, the impact of unexpected expenses, such as health-related costs, can result in a declining individual's wealth. All in all, the factors found from the literature review, both positive and negative factors, can be summarized as shown in figure 2.4.

METHODOLOGY

Primary data collection method

Interview method

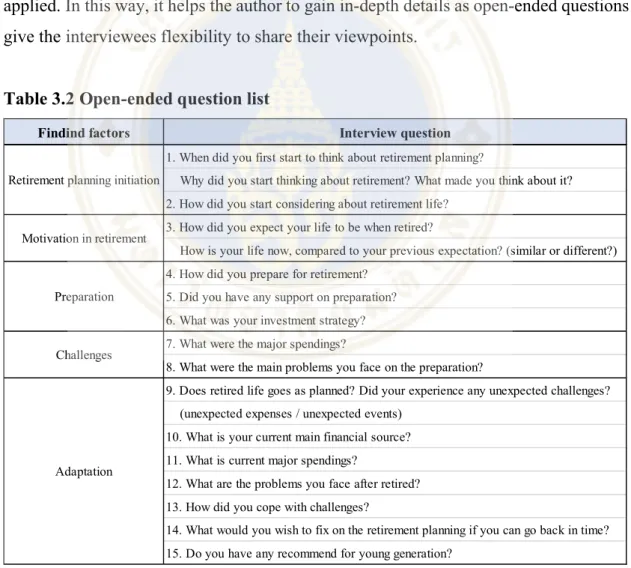

Open-ended question: To understand each participant's journey and perspective, a two-way communication interview with open-ended questions will be employed. In this way, it helps the author to obtain in-depth details as open-ended questions give interviewees the flexibility to share their views. What would you like to do in terms of retirement planning if you could go back in time?

This technique is not only used to verify data, but also helps encourage participants to share more about their stories so that the author can delve into their perspective. Interview: Interviews are conducted using a one-on-one interactive video call interview. The interviews took place in the free time of the interviewees in a chosen environment where they feel comfortable and relaxed.

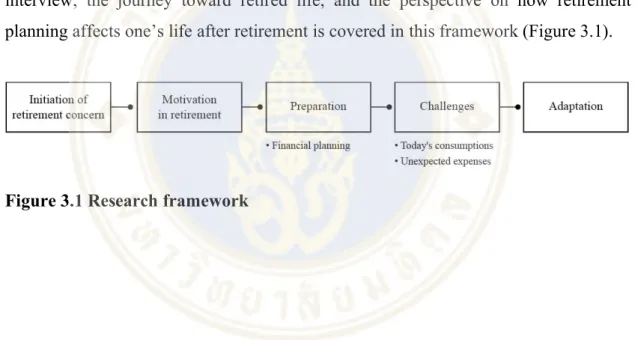

In addition to what they explained, the body language, gesture and facial expression of the interviewees will be observed. Research Framework: Using the primary data collected from the in-depth interview, the journey to retired life and the perspective on how retirement planning affects one's life after retirement is addressed in this framework (Figure 3.1).

RESEARCH FINDINGS

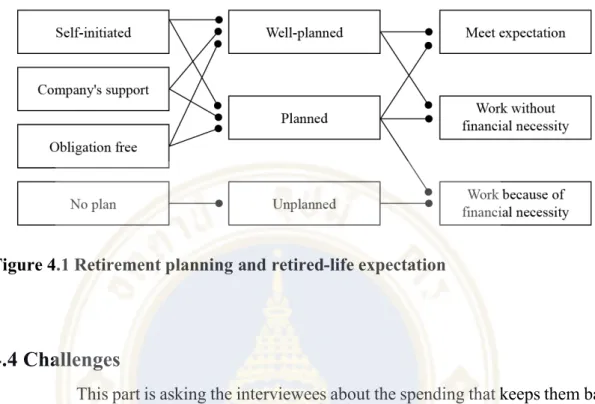

- Initiation of retirement concern

- Retired life: Expectation versus Reality

- Retirement preparation

- Adaptation

- Life lessons

- Conclusion

- Recommendations

The actual time they can think about the future is when they finish paying off their debt (home loans and car leases) and when their children have graduated from college. She was a baker who was not familiar with financial planning or preparing for the future. Some of the supporters simply give advice on how to invest and recommend a high-yield investment, but some of them will help plan the investment strategy and manage all the savings for the interviewees.

All interviewees invest in all 3 forms of investments, especially in the form of savings and funds in which it is the easiest way to save money. G had invested in these assets saying that the price has been increasing and they tend to appreciate more in the future. It expected the rental income to cover its price, while holding the right to assets that it could sell in the future.

B also bought savings insurance, thinking it would provide him with a steady income in the future. At the beginning of their working life, their wages are barely enough to live on, so it is quite difficult to save for the future. She continues to cook the bakery, trying to sell a lot and aiming to own a bakery in the future.

But he also recommends that they invest in real estate if they cannot invest in the form of savings, because they are easy to spend. This is one way to create discipline that prevents overspending, but can pay back in the future. Some get support from their company in the form of an old-age pension, and some have to generate their own monthly income, passive income.

Based on the conclusion we drew from the findings and the interviewees' suggestion for the young generation, the recommendations for Thais to prepare for their retirement can be summarized as follows; As they grow older, they will realize that it is not a necessary expense, where they could convert it into savings, allowing them to have a better quality of life in the future.