In the thematic article “News Event Surprise on Currency Exchange: Clear from GBP-AUD”, I would first like to express my sincere thanks to my assistant. In this article, we investigate the impact of news announcements on currency exchange using event study methodology. The currency exchange data was collected for the past eight years (January 2007 to September 2015) with a one-minute time frame.

Second, although our result shows that economic news has an impact on currency exchange, we cannot be specific whether single or multiple news announcements have more impact on currency exchange than each other. Currently, there are various investment products that offer high returns to investors and one of them is currency exchange, "Forex" Forex refers to the foreign exchange market. Currency exchange is always volatile due to economic or governmental factors between two tradable currencies (Égert and Kočenda (2014), Kearns and Manners (2006)).

Several papers have used high-frequency data to examine the reaction of foreign exchange to macroeconomic news and monetary decisions.

LITERATURE REVIEWS

Theories

Alternative models for the normal return include the CAPM model, or more simplistic approaches such as average returns Mackinlay (1997). In terms of equity, the Company's activities such as dividend payout, earnings announcement, share split, etc. So, a signal to the investor to be aware of the situation of the company which will later reflect the change in share price.

Empirical Studies

- Impact from Monetary policy change

- Impact from sterilized intervention

- GARCH & EGARCH model to identify an increase in volatility of currency exchange

Similar to currency exchange, any news involving the country's economy or political situation will eventually affect the currency exchange of those countries (Investopedia). This finding on intervention affects the currency exchange in the short term, consists of the related work of Cotte, Galli and Rebecchini (1994) and Humpage (1999) and the time series based study of Dominguez and Frankel (1993). Frenkel, Stadtmann and Pierdzioch (2001) detect high volatility during an intervention in the currency exchange data using the GARCH model.

As shown in Frenkel et al. 2001), the effect of high volatility was only small and tended to be reversed the day after the intervention. Similar to Omrane, Bauwens and Giot (2005), who used the EGARCH model to find the impact of nine categories of planned and unplanned news announcements on EUR/USD. The result suggested an increase in volatility just before the release of both planned and unplanned news.

DATA AND METHODOLOGY

Data

- Hypothesis

- Data Sources

Later, on any given day, we may have either a single news release or multiple news releases. For every news release in forexfactory.com, there are 3 types of data specified: past, actual and consensus. Indicating good news means that the actual value of the news release is greater than the previous value of the news release on the specific economic news.

In contrast to good news, bad news means that the actual value of the news release is less than the previous news release value of the particular economic news. Therefore, several news releases can be mixed between good and bad news releases in one day. A good news release is considered to be more news if there is more good news than bad news.

For example, there are three single news announcements in a day, two of them are good news and one more is bad news.

Methodology

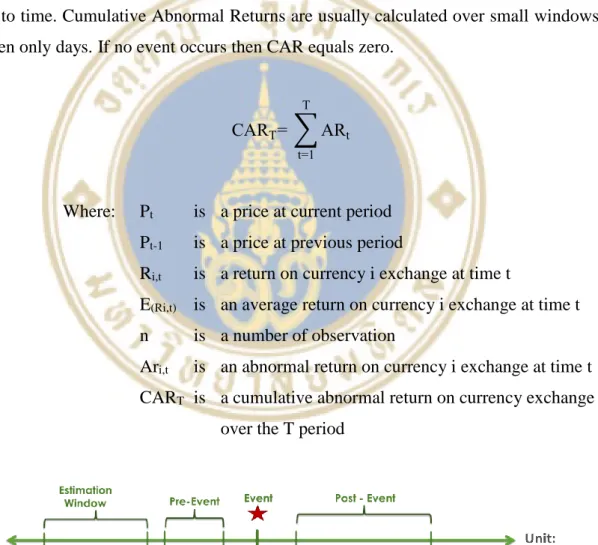

We then use standard event research methodology to estimate the impact of news announcement via currency exchange. Based on trial and error, we arrive at the best estimate period, ranging from 90 minutes to 31 minutes before the news announcement. Where: CAR[-a,+a] is a cumulative abnormal return on currency exchange from one minute before the news announcement to one minute after the news announcement.

For the last hypothesis, we take the news announcement that has an impact on the currency from the first hypothesis as an input. The result for this hypothesis would represent the pre- and post-event of each news announcement by trial and error. Hence, the entry position is an abnormal return, at that minute(s), that deviates the most from the average value of abnormal return during 120 minutes before news announcement.

And the exit position is the minute(s) that the abnormal return deviates the most from the mean value of the abnormal return during the 240 minutes after the news announcement.

EMPIRICAL RESULTS

Hypothesis 1: Specific news announcement shows a significant impact to the studied currency exchange

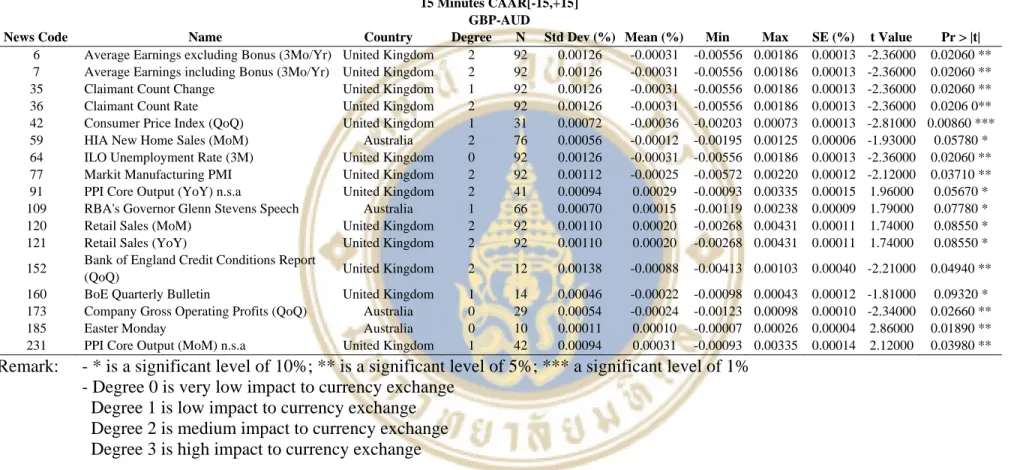

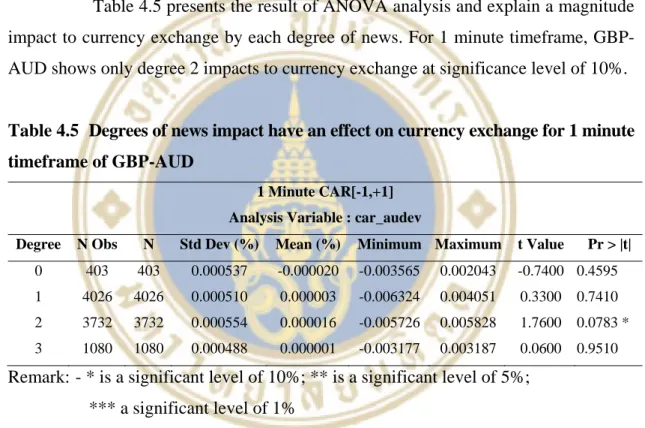

For a 5-minute time frame, as shown in Table 2, it shows the specific news announcements that have a significant impact on the currency exchange. For a 15-minute time frame, as shown in Table 3, the specific news announcements that have a significant impact on the currency exchange are shown. For a 30-minute time frame, as shown in Table 4, the specific news announcements that have a significant impact on the currency exchange are shown.

In summary, there are 65 numbers of events that have a significant impact on GBP-AUD. For 1 minute time frame there are 10 number of events; in 5 minute time frame there are 17 number of events; In 15 minute time frame there are 17 number of events; In a 30 minute time frame there are 21 events.

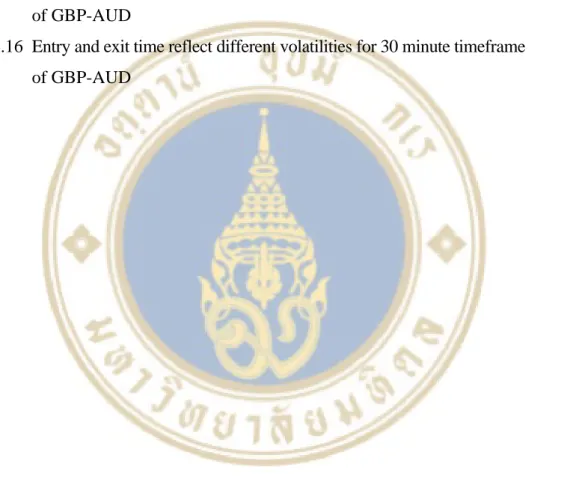

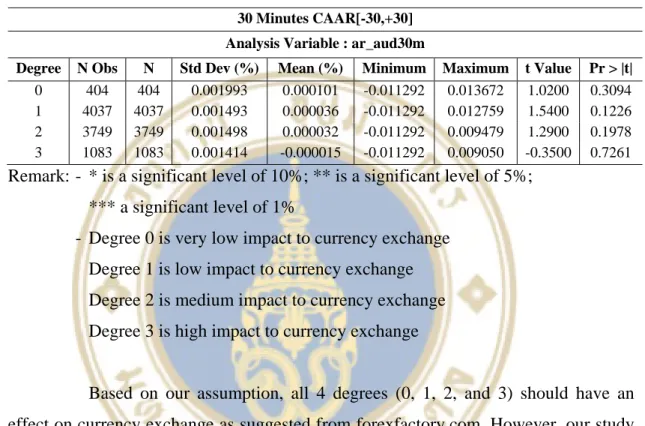

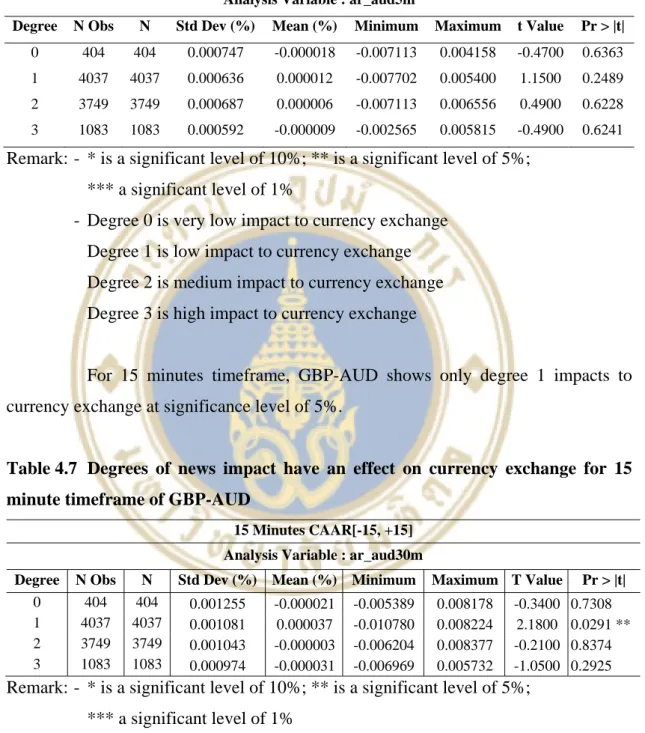

Hypothesis 2: Degrees of news impact have an effect on currency exchange

For a time frame of 15 minutes, GBP-AUD shows only degree 1 impacts on the currency exchange at the 5% significance level. For a 30-minute time frame, GBP-AUD shows an acceptance of the null hypothesis that news impact rates have an effect on the currency exchange. Based on our assumption, all 4 degrees (0, 1, 2 and 3) should have an effect on the currency exchange, as suggested by forexfactory.com.

However, our study found that degrees have no effect on currency exchange. Although a degree of 2 or 3 should have more impact on the currency exchange than a degree of 0 or 1, some of the news announcements are already absorbed by the investor before the announcement occurs. For GBP-AUD, there is a significant impact on the 1-minute timeframe on a scale of 2 and a significant impact on the 15-minute timeframe on a scale of 1.

Hypothesis 3: Multiple news announcements have greater magnitude impact than single news announcement

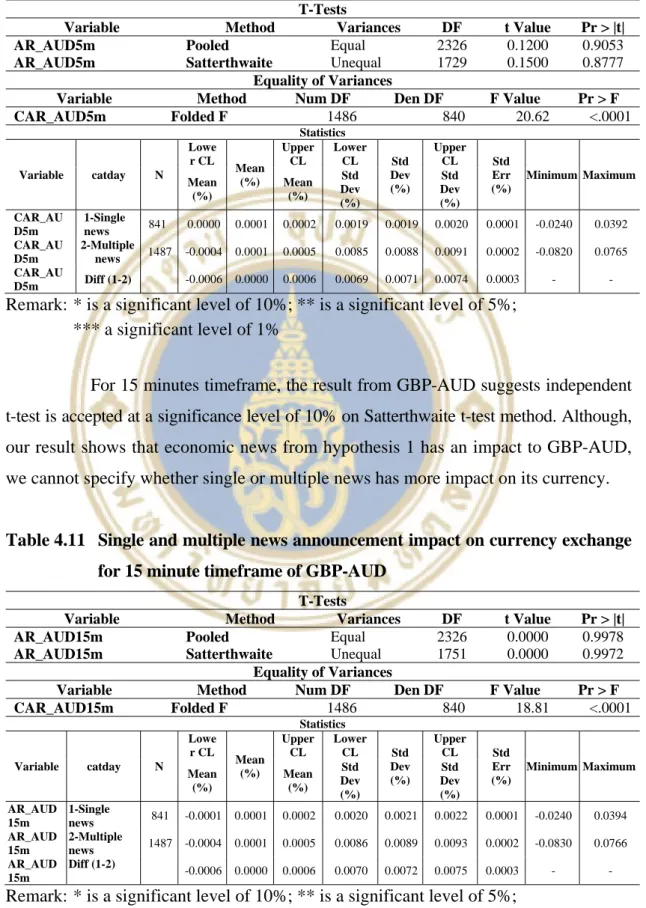

For the 1-minute timeframe, the result from GBP-AUD suggests that the independent t-test is accepted at a 10% significance level in Satterthwaite's t-test method. Although, our result shows that economic news from hypothesis 1 has an impact on GBP-AUD, we cannot specify whether a single or multiple news has more impact on its currency.

Tests

- Hypothesis 4: Various entry and exit time reflect different volatilities Time interval for considering entry and exit in this study will cover 120

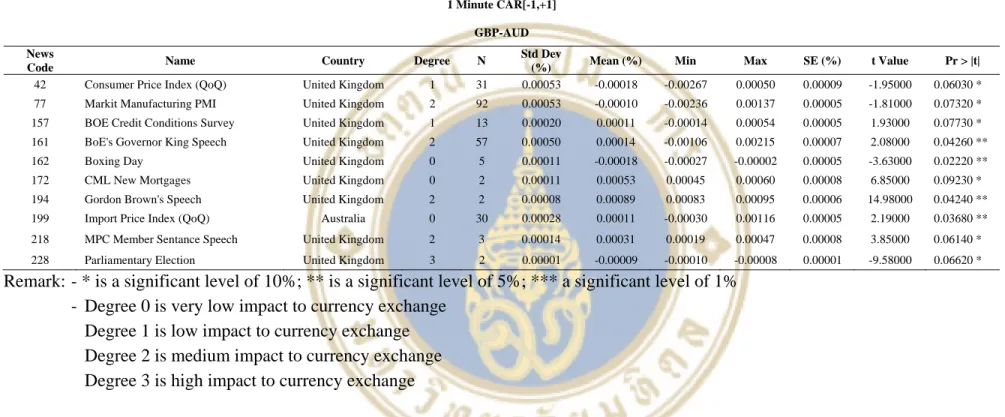

CPI is UK news level 1, our conclusion found entry 11 minutes before news release and exit time 240 minutes after news release. Markit Manufacturing PMI is UK news Level 2, our close found an entry 86 minutes before the news release and an exit time of 240 minutes after the news release. Boxing Day is UK news, level 0, our close found an entry 88 minutes before the news and an exit time of 37 minutes after the news.

CML New Mortgages is a UK news, rate 0, our conclusion found an entry at 7 minutes before the news release and exit time at 135 minutes after the news release. Gordon Brown's speech is UK news, level 2, our conclusion found an entry at 20 minutes before the news announcement and an exit time at 156 minutes after the news announcement. MPC Member Sentence Speech is UK news, rate 0, our conclusion found an entry 5 minutes before the news announcement and an exit time at 58 minutes after the news announcement.

Average Earnings Excluding Bonus (3m/y) is a UK news grade 2, our conclusion found an entry 90 minutes before news release and exit time 240 minutes after news release. Average earnings including bonus (3mth/year) is a UK news, grade 2, our conclusion found an entry 90 minutes before news release and exit time 240 minutes after news release. Claimant Count Change is UK news grade 2, our conclusion found an entry 90 minutes before news release and exit time 240 minutes after news release.

Claimant Count Rate is UK news grade 2, our conclusion found an entry 90 minutes before news release and exit time 240 minutes after news release. ILO Unemployment Rate (3M) is UK news, grade 0, our conclusion found an entry 90 minutes before news release and exit time 240 minutes after news release. Markit Manufacturing PMI is UK news, grade 2, our conclusion found an entry 35 minutes before news release and exit time 240 minutes after news release.

Good Friday is UK news, rate 0, our conclusion found an entry at 15 minutes before the news release and an exit time of 5 minutes before the news release. Claimant count change is UK news, level 1, our conclusion found an entry at 90 minutes before the news announcement and an exit time at 240 minutes after the news announcement. The BoE Quarterly Bulletin is a UK news, scale 1, our conclusion found an entry at 90 minutes before the news release and an exit time at 240 minutes after the news release.

Markit Manufacturing PMI is a UK news, scale 2, our conclusion found an entry at 90 minutes before the news release and exit time at 240 minutes after the news release.

CONCLUSION

Fourth, the specification of the computer to run the currency exchange result should be recommended with higher specification than the average home computer user. Finally, in addition to the selected data (Price High, Low, Open, Close), we can further improve the quality of the data by adding a volume variable to run the result more accurately.

Using high, low, open and close prices to estimate the effects of cash settlement on futures prices. Estimating the volatility of stock prices: a comparison of methods using high and low prices.

APPENDICES

Appendix A: Define News Announcement Code

124 Retail Sales ex-Fuel (MoM) UK 2 125 Retail Sales ex-Fuel (YoY) UK 2 127 Scottish Independence Referendum UK 3 128 Total Business Investment (QoQ) UK 2 129 Total Business Investment (YoY) UK 0. 163 BRC Retail Sales Monitor - All ( YoY) Great Britain 2 164 BRC Shop Price Index (MoM) Great Britain 0 168 CB Leading Economic Index Great Britain 2 169 CBI Industrial Trends Survey - Orders (MoM) Great Britain 1 171 CML Gross Mortgage lending s.a. 196 Halifax house prices (3m/YoY) UK 1 197 Halifax house prices (MoM) UK 1 198 Hometrack house prices s.a (MoM) UK 0.

PPI Core Output (YoY) n.s.a United Kingdom 2 Producer Price Index - Output (MoM) n.s.a United Kingdom 2 Producer Price Index - Output (YoY) n.s.a United Kingdom 0.