The Impact of Domestic Debt on Economic Growth in Malawi

A Dissertation presented to

The Development Finance Centre (DEFIC) Graduate School of Business

University of Cape Town

In partial fulfilment

of the requirements for the degree of Master of Commerce in Development Finance

by

Felix Chitera CHTFEL002

December 2020

Supervisor Assoc. Prof. Abdul Latif Alhassan

University

of Cape

Town

The copyright of this thesis vests in the author. No quotation from it or information derived from it is to be published without full acknowledgement of the source.

The thesis is to be used for private study or non- commercial research purposes only.

Published by the University of Cape Town (UCT) in terms of the non-exclusive license granted to UCT by the author.

University

of Cape

Town

ii Plagiarism Declaration

1. I certify that I have read and understand the Commerce Faculty Ethics in Research Policy.

http://www.commerce.uct.ac.za/Pages/ComFac-Downloads

2. I certify that I have read the General Rules and Policies Handbook (Handbook 3) regarding Student Rules of Academic Conduct: RCS1.1 to RCS3.2 and Rules Relating to examinations G20.1 to G22.2.

3. I certify that I have read and understand the document, “Avoiding Plagiarism: A Guide for students”.

4. This work has not been previously submitted in whole, or in part, for the award of any degree in this or any other university. It is my own work. Each significant contribution to, and quotation in, this dissertation from the work, or works of other people has been attributed, and has been cited and referenced.

5. I authorize the University of Cape Town to reproduce for the purpose of research either the whole or any portion of contents in any manner whatsoever.

Student number CHTFEL002

Student name

FELIX ABRECK CHITERA Signature of Student

Date:

DECEMBER, 2020

Abstract

Domestic debt has over recent years increasingly grown to be a significant portion of the financing budget for the government of Malawi. As such, this study investigated the impact that domestic debt has on economic growth in Malawi. The research employed classical time series estimations techniques covering unit root and cointegration analysis based on annual data from 1984 to 2015 to examine the long-run and short-run relationship between domestic debt and economic growth in Malawi.

The findings of the study show that in the long-run domestic debt has a positive impact on economic growth in Malawi, while a negative long-run relationship was established between inflation and economic growth. High inflation was found to stifle economic growth. In addition, the study established that government consumption expenditure and population growth also have a negative impact on economic growth. The study therefore recommends that the government needs to use domestic debt in moderation for as long as it positively impacts economic growth and that an effective monetary policy exists that reins in inflation. Furthermore, the study recommends that government needs to control government expenditure and take acceptable steps that will manage population growth.

iv Table of Contents

Plagiarism Declaration ... ii

Abstract ... iii

Table of Contents ... iv

List of tables ... vii

List of figures ... viii

Glossary of Terms ... ix

Acknowledgement ... x

Chapter 1 : Introduction ... 1

1.1 Background of the study ... 1

1.2 Problem statement ... 3

1.3 Research Objectives and hypothesis ... 4

1.4 Limitations ... 5

1.5 Scope and Justification of the Study ... 5

1.6 Organisation of the Study ... 6

Chapter 2 : Literature Review ... 7

2.1 Introduction ... 7

2.2 Economic context of Malawi ... 7

2.3 Overview of Public debt in Malawi ... 7

2.4 Conventional View of Public Debt ... 10

2.5 Economic Growth theories ... 11

2.5.1 The Theory of Stages of Economic Growth ... 12

2.5.2 Solow Neo-classical Growth Model ... 13

2.6 Empirical Literature on Debt and Economic Growth Relationship ... 13

2.6.1 Non-linear relationship between public debt and economic growth ... 14

2.6.2 Neutral Relationship of Public Debt on Economic Growth ... 15

2.6.3 Positive Impact of Public Debt on Economic Growth ... 16

2.6.4 Negative Impact of Public Debt on Economic Growth ... 18

2.7 Chapter Summary ... 20

Chapter 3 : Research Methodology... 22

3.1 Introduction ... 22

3.2 Research approach... 22

3.3 Data source and sample period... 23

3.3.1 Model Specification ... 23

3.4 Variable description and measurement ... 24

3.4.1 Economic Growth ... 24

3.4.2 Government Domestic Debt (GOVD) ... 25

3.4.3 Government Expenditure (GOVE) ... 25

3.4.4 Inflation (INF) ... 26

3.4.5 Population Growth (PoPG) ... 27

3.5 Estimation Approach ... 28

3.5.1 Unit Root Test ... 28

3.5.2 Co-integration ... 29

3.5.3 Long-run and Short-run effects ... 29

Chapter 4 : Research Findings and Discussion ... 31

4.1 Introduction ... 31

4.2 Descriptive statistics and model Diagnostics ... 31

4.2.1 Descriptive statistics ... 31

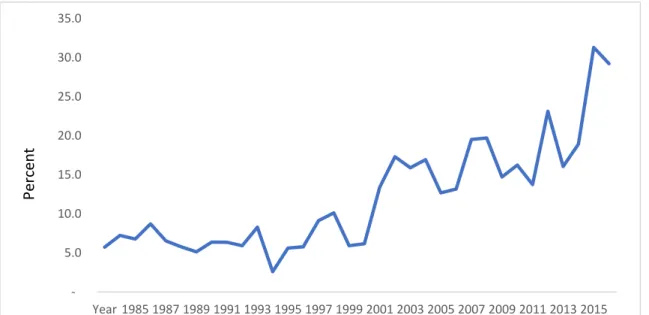

4.2.2 GDP Per Capita Growth Rate ... 32

4.2.3 Population growth... 33

4.2.4 Inflation ... 34

4.2.5 Expenditure ... 35

4.2.6 Debt ... 36

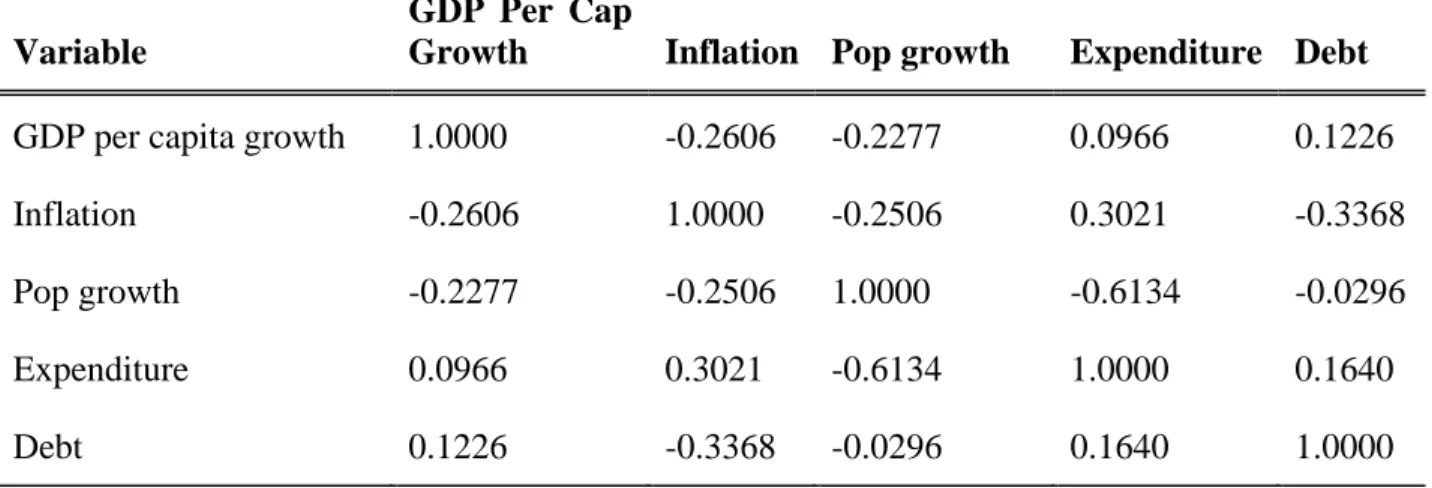

4.3 Correlation Analysis ... 36

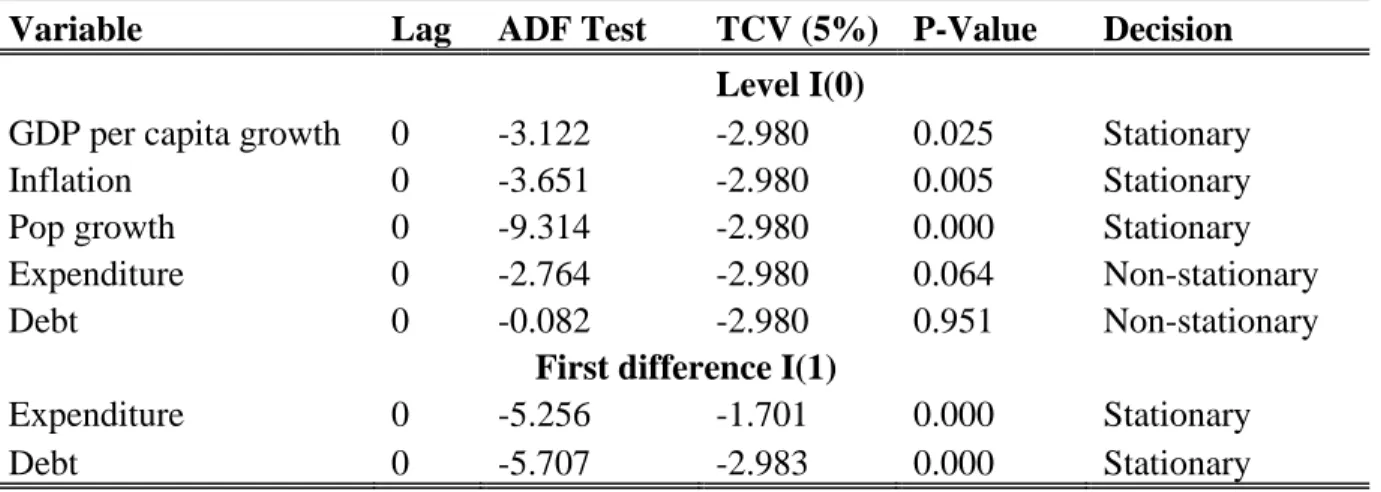

4.4 Unit Root Test Results ... 38

4.5 Autoregressive Distribution Lag (ARDL) Model Estimation ... 38

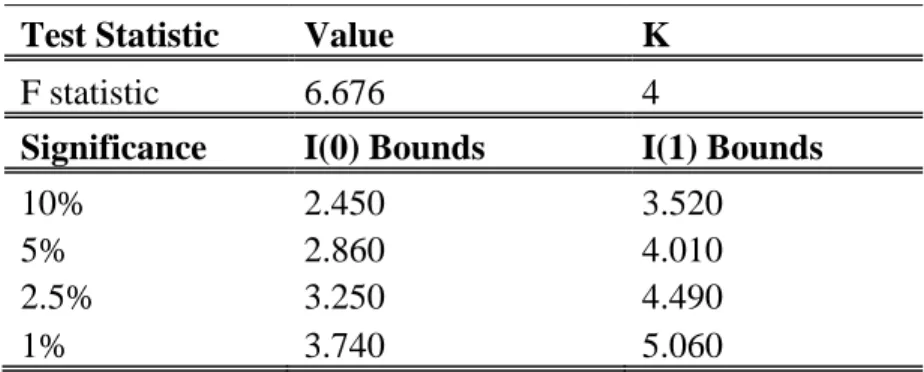

4.6 ARDL Bounds test for co-integration. ... 39

4.7 Long Run Results ... 39

4.8 Short Run Estimates ... 43

vi

4.9 Residual Diagnostic Results ... 45

4.10 Stability Diagnostic Tests... 46

4.10.1 Cusum Test (Cumulative sum of squares) ... 46

Chapter 5 : Conclusion and Recommendations ... 48

5.1 Introduction ... 48

5.2 Summary of Study and Conclusions ... 48

5.3 Recommendations ... 49

5.4 Further research ... 49

References ... 51

Appendix 1: Research data ... 59

Appendix 2: GDP Per capita Growth rate ... 60

List of tables

Table 3-1: Variables in the regression model ... 27

Table 4-1: Descriptive Statistic ... 32

Table 4-2: Correlation of variables ... 37

Table 4-3: Unit Root Test Results ... 38

Table 4-4: ARDL Bounds Test Results ... 39

Table 4-5: Long run results ... 41

Table 4-6: Short-Run Estimates ... 44

Table 4-7: Model Diagnostics Test ... 46

viii List of figures

Figure 2-1: Total Public Debt—SSA PRGT Eligible Countries (Percent of GDP): ………..9

Figure 2-2: Total Public and Publicly Guaranteed Debt and Interest Expense: ……….10

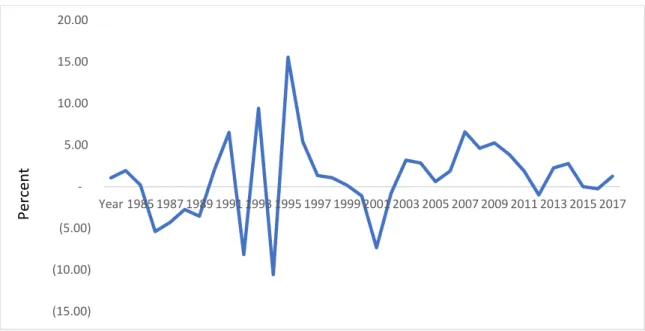

Figure 4-1: Graph for GDP Per Capita Growth Rate ... 33

Figure 4-2: Graph for population growth... 34

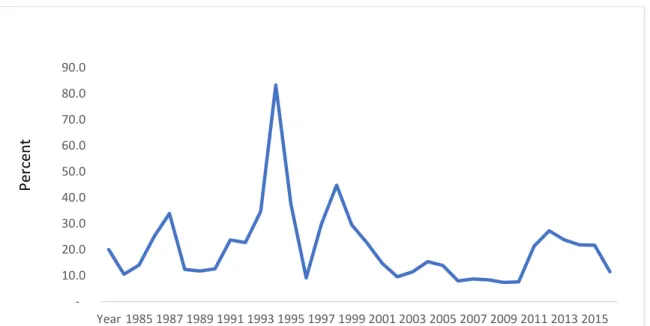

Figure 4-3: Graph for inflation. ... 35

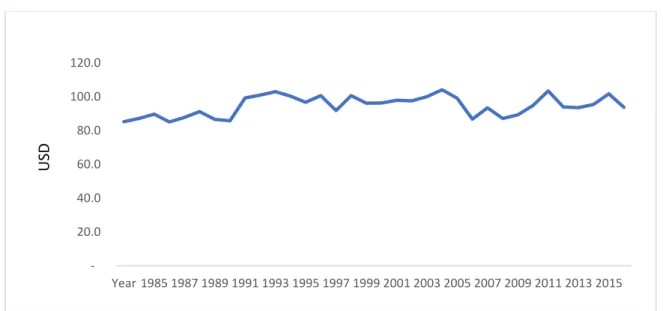

Figure 4-4: Graph for Expenditure ... 35

Figure 4-5: Graph for Debt ... 36

Figure 4-6: CUSUMQ Plot ... 47

Figure 4-7: CUSUMQ... 47

Glossary of Terms

EAC East Africa Community GDP

GDI

Gross Domestic Product Gross Domestic Investment GOVD Government Domestic Debt

GOVE Government Consumption Expenditure HIPC Highly Indebted Poor Countries

IMF International Monetary Fund INF Inflation

OECD Organisation for Economic Cooperation and Development OLS Ordinary Least Squares

PoPG Population Growth ECM Error Correction Model SSA Sub Saharan Africa USA United States of America VECM Vector Error Correction Model

x Acknowledgement

First and foremost, I would like to thank God for the opportunity and grace that was given to me throughout this academic journey.

I would like to appreciate the hard-working staff at the University of Cape Town Graduate School of Business – Development Finance Centre for their invaluable effort and support and contribution in many ways to this academic journey.

I specifically would like to acknowledge and express profound gratitude to Assoc. Prof. Abdul Latif Alhassan from the University of Cape Town - Graduate School of Business for the invaluable support and guidance. You showed resilience and untiring effort to provide timely advice and guidance throughout the entire study.

I would like to appreciate the Economic Policy Research department of the Reserve Bank of Malawi for facilitating access to some important data which was useful in the study.

Lastly but not least, I would like to appreciate my wife Nancy and my son Lawrence for the support, patience and encouragement during this study.

In conclusion, I would like to advise that none of the above-mentioned individuals share errors or omissions that may be identified in this work. I take full responsibility for this work.

Chapter 1 : Introduction

1.1 Background of the study

Economic growth is an important macroeconomic variable because it does have a reflection on the wellbeing of the citizens of any country. A country characterised by high rates of economic growth would be considered much better placed to provide a higher level of standard of living than a country with a lower level of economic growth, ceteris paribus. Faster-growing countries have the potential of trickling down the effects to its citizens which itself should increase the levels of living standards. This will also increase job opportunities leading to lower levels of poverty.

It is expected that consistent high economic growth rates determine the attractiveness of a country as an investment destination, since investors envisage that their resources will be put to profitable use (World Bank, 2011) and this includes foreign direct investment and local private investment.

The reason is that an economy with an expected high economic growth rate is considered a good place as it can provide the necessary labour force, over and above there being a conducive environment for market access to goods and services (World Bank, 2011) leading to increased revenue collection by government. This is expected to translate to investment in social infrastructures such as road networks, high quality schools and health services.

A growing economy is more likely to be characterised by increased production of raw materials and processed goods and services, which may be exported and earn foreign exchange. This in turn has the effect of stabilising the currency. The local currency may even appreciate against major trading currencies such as the South African Rand and the US dollar as a result of the extra foreign exchange earnings. It therefore follows that economic growth is important for the stabilisation of the macroeconomic environment.

Economic growth is also important in that growing economies require more labour force – both skilled and unskilled – which automatically increases employment rates and leads to a desirable state of the economy because higher demand due to lower unemployment is squared with a higher supply of goods and services. It follows that a growing economy will have more jobs available for its population, which is good for poverty alleviation efforts. It can further be argued that economic growth can result in increased tax revenue, which would be a direct consequence of a broadened tax base from the expanded private sector and payroll tax.

2 It is therefore important to undertake an empirical investigation of the factors that have an effect on economic growth for any country. This study focuses on domestic debt as one of the important macroeconomic variables which have a bearing on economic growth in Malawi.

On the other hand, public debt is increasingly becoming a feature of financing the recurrent and non-recurrent expenditure budget of the government of Malawi (World Bank, 2019). It is noted for instance that foreign financing which was at 2.5% in 20/17 progressively went down to 1.3%

in 2019/2020 but is projected to rise again to 3.7% of GDP financial year 2020/2021 (World bank, 2020). Domestic borrowing steadily progressed over the six-year period from 0.9% of GDP in 2016.17 to GDP ratio of 7.3% in 2019/2020 (World Bank, 2020). This is further projected to increase to 8.7% of GDP in 2020 (World Bank 2020). It is further noted that Malawi is at high risk of overall debt distress due to high levels of domestic debt contracted at high interest rates and moderate risk of external debt distress. The debt servicing costs have stand at 35% of revenue and grants in financial year 2019/2020 (World Bank, 2020). In a study that examined the features of domestic markets in Africa, including Malawi, Christensen (2005) found that most countries had domestic debt which was growing considerably. For instance, the study noted that in 1980 most countries had a debt to GDP ratio of 11% compared to 15% in the 1990s. In terms of the domestic debt to broad money, the ratio was constant at 40% even though some countries such as Ghana, Gambia, and Malawi had a ratio of 100%. The implication is that further expansion of domestic borrowing by government might affect private sector borrowing from commercial banks.

The increasing dependence on public debt by developing economies could be attributed to inadequate revenue being generated from tax, largely because of the low tax base of these economies and sometimes inefficient tax administration. Naturally, governments resort to internal and external borrowing in order to manage the deficits in their budgets as they seek to improve the socio-economic conditions of their citizens.

In its report of the Malawi Economic Monitor, the World Bank (2019, 9th Edition) reported that Malawi’s public debt has sharply increased since the time the country benefited from the Highly Indebted Poor Country relief (HIPC, 2006, p.15). The report noted that high fiscal deficits have mostly been financed through high-cost domestic borrowing (World Bank, 2019). This domestic debt accumulation is indicative of the increasing significance of domestic debt in Malawi. The World Bank report observes that the ratio of domestic debt to Gross Domestic Product (GDP) has

grown by more than double since 2011 and it stood at 60% in 2018. It would therefore be interesting to examine if this domestic debt expansion has yielded any impact on economic growth.

Public debt is, therefore, a direct consequence of a deficit in government budget due to insufficient revenue collected internally and which fails to meet the immediate needs to finance the national budget. Government then has the option of turning to borrowing, which can be from both external and/or internal sources. A debt is internal if it is sourced from the domestic market, regardless of currency, hence in this paper it is being referred to as domestic debt. If the debt is sourced from foreign markets, then it will be referred to as foreign borrowing.

Reinhart and Rogoff (2011) argued that domestic debt, while in most cases forgotten, is in fact large. In their study they establish that for the 64 countries considered in their study, domestic debt accounted for nearly two-thirds of total public debt. It is for this reason that Reinhart and Rogoff (2011) posit that studying domestic debt and recognising its existence may be a significant step to help explain why governments default on external debt.

These activities and manoeuvres by government have the potential of affecting the trajectory of economic growth in the country. It is specifically envisaged that these activities by government in increasing internal borrowing have the potential of impacting private sector credit and this may affect private investment and capital formation.

1.2 Problem statement

It is increasingly evident that public debt in Malawi has been steadily growing as the government has resorted to domestic debt to fund part of its budget (World Bank, 2019). Kumbatira (2008) observes that domestic debt has been a significant source of funding since the 1990s. Kumbatira (2008) notes that in the 1980’s Malawi depended on external borrowing for budgetary support.

This is no longer the case as the government now depends on both domestic and external borrowing such that government has resorted to balance its budget by borrowing from the private sector in form of issuing government bonds and treasury bills (World Bank, 2019). This has meant that in the end banks and major private sector players have been competing to place their funds with the central bank by investing in treasury bills.

This observation has also become a major concern for the World Bank, as reported in the Malawi Economic Monitor (World Bank, 2019). The World Bank explains that since 2013, the government

4 has been making high interest payments on domestic debt and this is calculated as high as 20% of government revenue (World Bank, 2019). This payment, the World Bank argues, is leaving less room for the government to apply the funds to growth-enhancing expenditures. In terms of GDP ratio, Malawi’s external debt has expanded rapidly to 37.3% of external debt to GDP ratio in 2015 from an external debt to GDP ratio of 20.1% in 2012 (Rasmussen, 2018). Similarly, domestic debt has also increased significantly from domestic debt to GDP ratio of 13.8% in 2012 to a ratio of 22.6% in 2017(Ramussen, 2018). This has resulted to an overall debt to GDP ratio of 55.1% in 2017 (Ramussen, 2018). World Bank (2019) has observed that Malawi has more than doubled its debt stock since 2011 to a debt to GDP ratio of 60% in 2018 with most of the fiscal deficits expected to be financed from domestic borrowing. This trend was the same in 2020 as World Bank (2020) reported an increase of public debt from 59.4% 64.6% of GDP between 2019 and 2020.

During the same time external debt decreased from 29.7% to 28.1% of GDP whilst domestic debt rose from 29.7% to 36.5% of GDP in 2020 (World Bank, 2020).

A focus on domestic debt is particularly important as this is increasingly becoming a way of financing budget deficits for the government (World Bank, 2019). This is especially true when indications by the World Bank show that it expects the government to present a budget for the 2019/20 financial year that will show even a wider deficit of 5.8% of Gross Domestic Product that is 2 percentage points higher than what was initially projected at 3.8%. The budget deficit will most likely be financed from domestic borrowing (World Bank, 2019).

The problem, therefore, is that economic growth appears to be affected by the activities of governments such as domestic borrowing, suggesting that national economies can take a negative or positive trajectory depending on the policy direction of governments on domestic debt. In that case it is important that an understanding of the impact of domestic debt on economic growth is analysed. The finding of this research would help the government to make informed policy decisions when taking on domestic debt.

1.3 Research Objectives and hypothesis

Therefore, from the foregoing problem statement, this paper sets out to analyse the impact of domestic debt on economic growth in Malawi. The specific objective of the study is:

• To examine the impact of domestic debt on economic growth in Malawi.

The hypothesis is set out as below:

Null hypothesis: Domestic debt has no impact on economic growth in Malawi Alternative hypothesis: Domestic debt has an impact on economic growth in Malawi 1.4 Limitations

The study spans a long period of time with many variables in an effort to assess if there is any effect of domestic debt on economic growth in Malawi. This may result in some of the data for the chosen period being unavailable. Efforts will be made to identify and use only those variables which have data readily available to be used in the regression model.

1.5 Scope and Justification of the Study

This study will look at data that informs economic growth for the sampled period. Therefore, the study is considered important because whilst similar studies have previously been undertaken, the focus of the studies has tended more towards the relationship between external debt and economic growth (Sekhampu & Tchereni , 2013); Phiri & Tchereni,2013) or in some cases the relationship between foreign aid and economic growth, but not on the impact of domestic debt on economic growth in Malawi. Further, the understanding of the impact of domestic debt on economic growth in the case of Malawi is important as the finding could help inform fiscal policy formulation at a time when the Malawian government is borrowing in increasing measure from the domestic and external markets. As indicated in the introduction, domestic borrowing is growing and it is only proper that policy makers have an informed understanding as to whether the increased domestic debt is having the intended effect on economic growth and, if anything, what other policy recommendations can be made for effective debt application.

Given the background that few empirical studies exist which have a specific focus on the relationship of domestic debt and economic growth in Malawi, this study will therefore contribute to this body of literature. The study is necessitated by the growing public debt and the need for policy makers in Malawi to understand the impact of domestic debt on economic growth. This study has, therefore, significant impact on practice, policy and academic literature.

Further, the study is expected to contribute to the existing body of research on public debt and economic growth. It is expected to provide some guidance for domestic debt management in

6 Malawi. Its findings are also expected to contribute to policy and practice for the Malawian Government in the formulation of policy and its implementation.

1.6 Organisation of the Study

The organization of this dissertation will take the form as detailed in this section. Chapter one has covered the introduction of the research including the problem statement, main and specific objectives, research hypothesis and justification of the study.

Chapter two discusses literature review covering work already done by other studies in similar research areas. Chapter three presents the research methodology. In this chapter research design and data collection methods are discussed. Chapter four discusses the findings of the research as collected from the data collection methods. Chapter five presents the findings and offers an interpretation of the findings. Finally, the chapter will give the conclusion of the research.

Chapter 2 : Literature Review

2.1 Introduction

This chapter discusses the empirical and theoretical literature on factors of economic growth.

Theoretical literature focuses on selected theories of economic growth.

2.2 Economic context of Malawi

Malawi is a landlocked country in south eastern Africa with a GDP of USD7.667 billion. GDP per capita for Malawi was USD411.55 as of 2019 with an annual growth rate change in GDP of 4.4%.

Its Gross National Income is reported at 20.13 billion PPP dollars. The country has an estimated population of 18.6m in 2019 which is expected to double by 2038 (World Bank, 2020). According to African Development Bank Country Strategy Paper for 2013 -2017, Malawi ‘s economy is narrowly based with Agriculture sector being the main source of growth and exports. AFDB (2013 -2017) reports that the sector represents approximately 37% of GDP and that it employs nearly 80% of the labour force. AfDB (2013-2017) also reports that the sector accounts for 82.5% of foreign exchange. The other sectors that significantly contribute to GDP are wholesale and retail trade which includes hotel industry and restaurants. This sector collectively contributes 24% to GDP indicating the significant contribution of tourism to Malawi economic growth (AFDB, 2013- 2017). World Bank (2020) projects a contraction in real GDP per capita growth at 1% due to the pandemic. Population growth is estimated at 3% and as a result the real GDP per capita will further contract. The education sector is usually the highest funded sector in recent years at about 17.6%

of the budget. This is closely followed by agriculture which earns 16.2% of the budget. Other sectors of the economy that are receiving considerable budgetary allocations include healthcare which gets 9.3%, transport and ICT at 6.9% and energy at 6.2% (World Bank, 2020)

2.3 Overview of Public debt in Malawi

Domestic debt has been issued in Malawi since the 80’s but the debt exposure started to deteriorate between 2001 and 2004 (Kumbatira, 2008). In the study to propose debt sustainability strategies, Kumbatira notes that the increased indebtedness has resulted in a high interest regime which has negatively affected the government’s ability to sustainably allocate resources for critical poverty alleviation expenditure. The International Monetary Fund (IMF) (2017) indicated that Malawi

8 faced a moderate risk of debt distress based on the assessment of external debt with heightened vulnerabilities related to domestic debt.

Kumbatira (2008: p12) defines domestic public debt is as “borrowings in local currency (Malawi Kwacha) from domestic or foreign sources.” From this definition, Kumbatira therefore explains that domestic debt comprises borrowings from the local banks, such as the Reserve Bank of Malawi, commercial banks, non-bank financial institutions, corporate sector, foreign investors and individuals contracted in form of “issuance of marketable and non-marketable instruments with the major proportion being in marketable securities such as treasury bills. Kumbatira (2008) further points out other instruments can be used to contract debt. These instruments include Local Registered Stocks, which are split between treasury bonds and treasury notes; Ways and Means, arrears; and contingent liabilities among others (Kumbatira, 2008, p. 12)

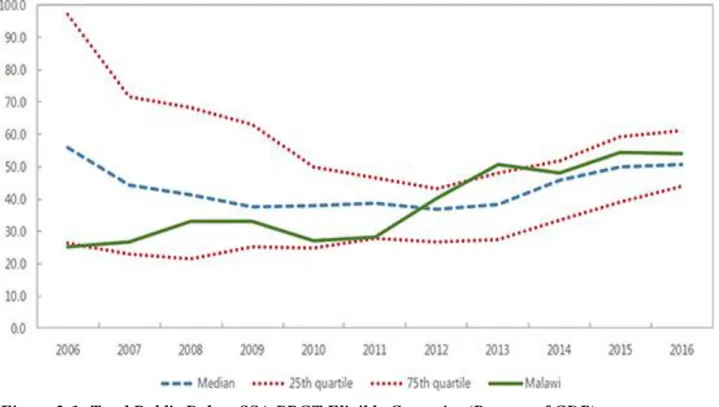

The IMF (2017) reports that over the recent years Malawi had accumulated debt more rapidly than before 2017, to the extent that its debt levels are higher compared to those of other Sub-Saharan Africa countries. It is further observed that the debt levels have more than doubled to around 54%

of GDP in 2017 from around 28% of GDP in 2007 resulting in the country’s debt standing above SSA median debt levels (IMF, 2017) of the Poverty Reduction Growth Trust eligible countries.

Figure 2.1 below graphically demonstrates that Malawi public debt levels have been growing at levels that are far above the Sub-Saharan median and this may be cause for a careful analysis of public debt levels in Malawi.

Figure 2-1: Total Public Debt—SSA PRGT Eligible Countries (Percent of GDP), (Source: WEO data and IMF staff calculation.)

The IMF (2017) reported that the composition of Malawi’s debt shows a progressive shift from borrowing externally to domestic borrowing. The IMF (2017) report argues that the shift is largely due to three things including the growing fiscal deficits during the period 2013 to 2017, the securitisation of domestic arrears, and the withdrawal of funding by different donors. The graphs in Figure 2.2 show the shift in the composition of debt with domestic debt beginning to grow proportionately over the period represented in the graphs. In addition, the graphs clearly indicate that domestic debt is expensive when compared to external debt based on the interest expense that is payable.

10 Figure 2-2: Total Public and Publicly Guaranteed Debt and Interest Expense:

(Sources: Malawian authorities and IMF staff calculation.)

2.4 Conventional View of Public Debt

Elmendorf and Mankiw (1999) state that Conventional view of public debt holds the view that in the short-run output is determined by demand. As a result, Elmendorf et al. (1999) asserts there is therefore a positive effect created by fiscal deficits or higher public debts on disposable income, aggregate demand and output. Elmendorf et al. (1999) reason that this positive, short-run effect of budget deficit is markedly noticeable if the output is below capacity.

In the long run, the effects of increase in public debt changes. Cochrane (2011) as quoted by Gómez-Puig and Sosvilla-Rivero (2017) argues that in the long-run the view is different if the decrease in public savings resulting from a higher budget deficit is not fully compensated by an increase in private savings. Cochrane (2011) as quoted by Gómez-Puig et al. (2017) argues that this results in a decrease of national savings, which translates in lower total investment. Therefore, asserts Cochrane (2011) as quoted by Gómez-Puiq et al. (2017) that the decrease in national savings will inevitably have a negative effect on GDP since low investment will lead to small capital stock, higher interest rates and lower productivity and wages. The resulting negative effect

on public debt is therefore further magnified by distortionary taxes which may be employed as a form of fiscal adjustment to rein on the debt.

The Ricardian equivalence on the other hand is a type of neutrality position that states that assuming a particular government policy does not have any important effect (Mankiw et al., 1999).

According to Elmendorf and Mankiw (1999) the Ricardian equivalence takes a different view from the conventional view of debt. It essentially argues that whilst conventional view would take the viewpoint that a fiscal stance that reduces taxes without reducing government expenditure today or in the future should stimulate consumption, reduce national savings and capital accumulation in the process depressing long-term economic growth. This effect changes when the Ricardian equivalence theory is considered. The government policy is not expected to have any effect if Ricardian equivalence theory holds (Mankiw et al., 1999: p32).

The view by Traum and Yang (2010) gives another perspective on the finding. Traum and Yang (2010) estimate a new Keynesian model with a detailed specification. In this model an account is made for the dynamics between fiscal and monetary policy interactions and fiscal adjustments induced by debt accumulation. It is found that most fiscal instruments respond to debt systematically. For instance, they argue that government is seen to reduce its purchases and transfers whilst increasing taxes when government debt-to-output ratio rises as a way of reining on debt growth.

Furthermore, Traum and Yang (2010) posit that there is no systematic reduced- form relationship between government debt and real interest rates, arguing that any crowding out effect resulting from government debt depends on the magnitude of the policy innovations brought about by the debt growth. The effect would depend on the distortionary fiscal financing and monetary policy in response to debt accumulation. For instance, they argue that increases in future capital and labour taxes, which are necessary to offset debt accumulation, have a negative impact on investment. In addition, responses of the real interest rates and investment may be influenced by how aggressively the central bank stabilises inflation and output.

2.5 Economic Growth theories

Economic growth is a matter that attracts a lot of discussion given the interest that every government has in economic growth. Over the years economic growth has been studied and several

12 theories have been promulgated. The principal theories that have been discussed are the Stages of Economic Growth theory whose major contributors include the Harrod-Domar growth model, the Solow neo-classical growth model (Todaro & Smith, 2015) and also the theory of debt and economic growth.

2.5.1 The Theory of Stages of Economic Growth

The theory of Stages of Economic Growth was first advanced by Rostow (1959) who postulated that a country goes through a series of stages on its way to economic development, ranging from take-off to self-sustaining (Todaro & Smith, 2015). The theory argues that for any economy to take off it needs to mobilise domestic and foreign savings which would capacitate it to generate enough investment to accelerate growth (Todaro & Smith (2015), p120). This thinking links closely to the Harrod-Domar growth model which theorises that for any economy to grow it must save a proportion of its national income (Todaro & Smith, 2015). These savings would help the country to replace impaired capital goods. If this view holds, then it is necessary that there should be net addition to the capital stock in order to grow an economy. It can be seen from the discussion, therefore, that the Harrod-Domar economic growth model makes the following assumptions (Todaro & Smith, 2015):

1. The first assumption is that Savings leads to investment and this is represented mathematically as S=I where S is the Savings ratio and I is the Investment, (Todaro & Smith, 2015, p.123) 2. The second assumption is that Investment in turn leads to changes in capital stock represented

mathematically as I=∆𝐾 (Todaro & Smith, 2015, p.123)

3. The third assumption is that there is a constant capital-output ratio which implies that for every amount of capital in a given country there is a corresponding output whose ratio to capital is constant. This is represented mathematically as r =Δk

Δ𝑦 (Todaro & Smith, 2015, p.123)

From the foregoing, therefore, the Harrod-Domar economic growth model derives the following economic growth model:

∆𝑦 = Δ𝑠

Δ𝑟

where y is the gross domestic product, s is the savings amount and r is the capital output ratio.

2.5.2 Solow Neo-classical Growth Model

Closely linked to the theory as espoused by the Harrod-Domar growth model is the Solow neo- classical growth model (Todaro & Smith, 2015). This theory was first espoused by Nobel laureate Robert Solow who added labour force and technology to the economic growth model. The crux of the Solow growth model is that economies must end up to the same level of income if their savings ratio, depreciation, labour force growth, and productivity are the same (Todaro & Smith, p120).

The Solow theory of economic growth differs from the Harrod-Domar growth model in that this model makes allowance for substitution between capital and labour (Todaro & Smith, 2015).

Prescott (1998) citing Solow (1970) in the review of the Solow neo-classical growth model explained that Solow models mimicked the basic growth fundamentals which infer that on average real output per worker would normally grow at roughly constantly rate, and the growth of tangible capital stock tends to grow at the same rate as well. This, as a result, leads to the rate of capital/output ratio being constant. In this case, Prescott (1998) citing Solow (1970), notes that the capital’s share of income is also constant and so is the growth of output per worker and real wages.

The varying theories of economic growth indicate that there are possibly many factors that impact economic growth in a given country and that the impact varies depending on the country’s economic fundamentals. This is the reason that this study will set out to investigate the impact of domestic debt on economic growth in Malawi.

2.6 Empirical Literature on Debt and Economic Growth Relationship

Saungweme & Odhiambo (2018) conducted an extensive study of the body of literature on the impact of public debt on economic growth. Their analysis found that literature has generally advanced four theories of public debt and economic growth relationship. There are those studies that conclude that there is a neutral relationship between public debt and economic growth;

effectively arguing that public debt has no impact on economic growth and is called the Ricardian Equivalence Hypothesis. Secondly, there are those studies that argue there is a negative impact of public debt on economic growth. Thirdly, there are studies that argue for the positive impact of public debt on economic growth. Finally, other studies assert that there is a non-linear relationship between public debt and economic growth. This literature is further discussed in detail in the following sections.

14 2.6.1 Non-linear relationship between public debt and economic growth

In the study that sought to examine the effect of public debt on growth whilst controlling for institutional environment in which the debt is incurred, Kutivadze (2011) had an interesting finding on the impact of external and domestic financing. The study grouped countries by income levels for the period covering 1990 to 2007. It was established that regression outcomes pointed to the existence of a non-linear relationship between total public debt and economic growth in the subsets of middle- and low-income countries. It was also established that this non-linear relationship mainly arose as a result of the external debt other than the domestic debt component. It was therefore concluded that high levels of external debt are associated with low rates of GDP growth per capita. The study posited that this relationship was not established with domestic debt, as in this case, high levels of domestic debt were not necessarily associated with low levels of economic growth.

Kutivadze (2011) also brings another noteworthy insight which argues that there is a strong link between financial development and growth across a subset of middle-income countries. This finding highlights the fact that debt structure is relevant to growth, thus noting the importance of the development of the domestic bond markets in order to promote long-lasting economic growth.

Kumar and Woo (2010) also attest to the existence of a non-linear relationship between public debt and economic growth. They argue that there is some evidence of non-linearity with only debt levels of as high as above 90% of GDP having a negative effect on growth. The effect is largely attributable to the slowdown in labour productivity due to reduction in investment and reduced growth of the capital stock per worker.

Doğan and Bilgili (2014) employing the Markov Regime-Switching model in analysing external debt for Turkey, covering the period 1974 to 2009, rejects the null hypotheses at 1% significance level, which suggests that the two alternative models are linear. This leads to the conclusion that the relationship between economic growth and debt is non-linear. This is also a view supported by Fosu (1996) who found that the impact of debt on growth in the long-term is non-monotonic. It was established that in Sub-Saharan Africa the relationship is positive at low levels of investment.

However, that relationship shifts to negative after a GDI/GDP threshold of about 16%. This finding points to the complicated relationship between debt and growth and the fact that this relationship is not linear. Adam and Bevan (2001) argue that for a given debt, the impact of the deficits is non-

linear and ambiguous. The findings suggest a non-linearity in the relationship between growth and fiscal deficits for a sample of developing countries. These non-linearities may emerge from interactions between the size of the deficit and growth, and the interactions between deficit and public debt. Casares (2015) demonstrated analytically that there is a non-linear relationship between public debt and economic growth. It was found that there was a positive impact on the tradable sector following an increase in the external public debt to GDP ratio (Casares, 2015).

Thus Casares (2015) attributes this finding to the fact that the depreciation of the real exchange rate resulted in the increase in the fraction of labour employed in the tradable sector and he therefore explains that this results in the reduction of the proportion of non-tradable capital thereby increasing the tradable capital. Furthermore, Casares (2015) demonstrated the existence of an inverted U-shaped relationship between public debt and economic growth and described that the non-linearity between public debt and economic growth was explained by two opposite effects on the growth rate of the economy. Therefore, Casares (2015) argues that the first effect – which explains the positive relationship – is that the increase of external public debt results in the decrease of relative prices of non-tradable goods. This results in the tradable sector attracting more resources and this benefits growth rate since the tradable sector is a technological leader. The second opposite effect according to Casares (2015) that explains the negative effect is that, when the external public debt increases, the country risk premium increases, and interest payments on the private and public debt increase. Casares (2015) goes on to argue that this results in the decrease of the household disposable income and the savings to GDP ratio, which also results in the reduction of resources for capital accumulation. Consequently, the growth rate declines.

2.6.2 Neutral Relationship of Public Debt on Economic Growth

As indicated earlier, other studies argue that there is a neutral relationship between public debt and economic growth. For instance, studies by Ahlborn and Schweickert (2015) find that there is a neutral growth effect for low public debt. However, the study also establishes that this relationship tends to negative once debt levels reach around 60% of GDP. Dar and Amirkhalkhali (2014) agree with this finding in their paper in which they attempted to empirically investigate the impact of public debt on economic growth for a group of 23 industrialised countries within a production function framework. It was found that whilst the public debt coefficient was negative this was statistically insignificant making a case for a neutral relationship for debt levels below a certain

16 2.6.3 Positive Impact of Public Debt on Economic Growth

Chiu and Lee (2017) further found that increase in public debt has the impact of stimulating economic growth for countries with high- and low-income levels with varying degrees of sensitivity. The sensitivity of impact on economic growth for additional public debt is high for low income countries suggesting that, in terms of policy, countries should borrow appropriately in line with their income levels. Da Veiga, Ferreira-Lopes, & Sequeira, (2016) agree with this finding as they conclude that economies in Africa generally grow more when public debt is within the 30- 60% limit of GDP, therefore exhibiting an inverted U relationship between economic growth and debt. Da Veiga et al., (2016) however, observed an opposing trend when evaluating the relationship between debt levels and inflation. Their study concludes that a high level of indebtedness is associated with high inflation rates. Chiu and Lee (2017) also concur with this finding as their study found that government debt has the effect of reducing economic growth of the country if it is taken above a certain threshold in high risk environments. Chiu and Lee (2007) also explain that public debt stimulates economic growth if it is taken by low risk countries. From this study, the authors make a recommendation that governments which seek to finance their budgets through increased uptake of debt, with a view to stimulating economic growth, should ensure that they have put in place measures that reduce political risk, and have the capacity to finance their debts to reduce their country’s risk.

It is important to note that the views espoused by Da Veiga et al., (2016) are supported by the debt Laffer Curve theory which states that there is a non-linear relationship between debt and economic growth (Megersa, 2015). In this theory, it is espoused that at certain levels domestic debt will initially accelerate economic growth because it mobilises resources, which are then used to finance budget deficits. The theory, however, posits that an economy slides into a debt overhang as stock of domestic debt increases and this results in a decline in levels of economic growth. This is an obvious result of high debt servicing costs which reduces resources that should otherwise have been directed to productive investments. Further, the high debt tends to crowd out private investment, and issuance of debt may trigger a rise in interest rates, which will also have a negative effect on investment funding. Ndoricimpa (2017) confirms the presence of nonlinearities on the impact of debt on economic growth noting, however, that the estimations reflect the impact of debt on economic growth as significant if natural resources are included, regardless of whether the debt

regime is below or above threshold in general. Ndoricimpa (2017) asserts that low debt is neutral or growth enhancing, whilst high debt is found to be consistently detrimental to economic growth.

Megersa (2015) focussed on low-income Sub-Saharan African countries and specifically tested for the presence of the Laffer Curve theory. The study concluded that there was indeed robust evidence that supported the view that lower levels of public debt contributed positively to economic growth and higher levels of debt are associated with negative economic growth. Babu, Kiprop, Kalio and Gisore (2015), using data covering the period 1990-2010, empirically examined the effect of domestic debt on economic growth in the East Africa Community (EAC). The study by Babu et al. (2015) revealed that expansion of domestic debt has a positive effect on economic growth of the EAC member countries, whilst establishing in the same study that terms of trade volatility could negatively affect the economic growth of the region.

Fincke and Greiner, (2015) investigated the relationship between economic growth and public debt by focusing on eight emerging economies. Unlike many studies that have found a negative relationship between these variables, or an inverted U-shaped relationship, it was concluded in their study that there is a significant positive correlation that exists between public debt to GDP ratio and eventually economic growth. It is possible that one of the reasons could be that the sample countries had not accumulated enough debt to reach the tipping point and begin to experience a U- shaped relationship, since the focus was on emerging economies. Indeed Fincke and Greiner (2015) noted in their paper that comparatively the GDP/Debt ratios of the eight countries studied was lower on average than those where the U-shaped relationship had been observed. In a similar study, Tchereni, Sekhampu, and Ndovi (2013) examined the relationship between external debt and economic growth in Malawi using time series data for the period 1975 to 2003. They found that there is a negative relationship between economic growth and external debt, even though this was found to be statistically insignificant. As a result, the study concluded that, as a policy recommendation, the government should not place heavy reliance on foreign debt.

Ferreira (2009) confirms that there is a Granger causality relationship between the growth of the real Gross Domestic Product (GDP) per capita and the public debt. This was represented in the study by the ratio of the current primary surplus/GDP and the ratio of the gross Government debt/GDP (Ferreira, 2009, p10). In this study Ferreira (2009) further concludes that this relationship is bi-directional. This finding is supported by Patillo et al. (2002 & 2004) in their study

18 which concludes that at low levels economic growth is positively affected by external debt whilst the relationship is negative at high levels. On the other hand, Presbitero (2005) finds an outright clear negative relationship between debt and economic growth at any level.

Mbate (2013) further found results consistent with the Laffer Curve theory. In his study, he found that it was confirmed that a non-linear relationship exists between domestic debt and economic growth. The study noted that an increase in domestic debt resulted in an accelerated economic growth, but this growth began to stagnate when debt levels surpassed certain thresholds. This view is supported by Reinhart and Rogoth (2010) who argued that domestic debt results in economic growth but only within certain thresholds.

Putunoi and Mutuku (2019) on the other hand, in a study on the impact of domestic debt on economic growth in Kenya, observed that domestic debt expansion has a positive, significant effect on economic growth. The same study further observed that this debt, when it reaches excessive levels, can be inflationary and have a crowding out effect on private sector borrowing. Owusu- Nantwi and Erickson (2016) employing Vector error correction and Johansen cointegration analysis, examined the relationship between public debt and economic growth in Ghana and the results indicated that public debt significantly positively impacted on economic growth in the short and long term.

2.6.4 Negative Impact of Public Debt on Economic Growth

Studies by Schaclarek (2004) on the other hand concluded that based on the results of 59 developing countries and industrialised countries there is always a negative and significant relationship between total external debt and economic growth for developing countries. This robust relationship was not evident in the industrialised countries suggesting that for developed countries higher public debt levels are not necessarily associated with lower GDP growth rates. Further to this view, Egert (2013) sought to test further the finding by Reinhardt and Rogoth on the debt threshold beyond which the economy starts to experience negative growth. In this study Egert (2013) employed non-linear methods and found that some evidence exists in favour of a negative relationship between debt and growth, and further noted that these results were sensitive to the time dimension, country coverage considered, data frequency and assumptions on the minimum number of observations in each nonlinear regime. Egert (2013) further showed that whilst previous empirical studies have validated the 90% public debt ceiling as argued by Reinhart–Rogoth beyond

which economic growth slows down, the number 90% is not a magic number. Negative economic effects can take effect at public debt to GDP ratio at levels as low as 20% - 60%. In concluding his study, therefore, Mbate (2013) challenges governments to develop country specific domestic debt management strategies that integrate debt ceilings in order to limit domestic borrowing.

Furthermore, Adofu and Abula (2010), in their study of the relationship between economic growth and domestic debt in Nigeria for the 1986-2005 period, concluded that domestic debt had a negative effect on the economic growth. These findings are supported by studies by Panizza and Presbitero (2012) which utilised the instrument variable approach when analysing the effect of debt on the growth of the economy for a number of Organisation for Economic Cooperation and Development nations. In their study Panizza and Presbitero (2012) posited that a negative connection was established between public debt and economic growth. As a result, Adofu and Abula (2010) recommended that domestic debt needed to be discouraged and the authorities should focus instead on broadening the tax revenue base.

Saungweme and Odhiambo (2018) therefore posited that, given all these conflicting views in the vast body of literature, the impact of public debt on economic growth is not that straightforward and the assertion that public debt is bad for economic growth is founded on prima facie evidence and should be taken with caution. This theoretical background is also supported by studies conducted by Mergesa and Cassimon (2014) who observed that whilst the concern over the sustainability of public debt and its negative effects on economic growth is based on sound theoretical background, it should be emphasised that effects on different countries will not be the same. Specifically, Mergersa et al. (2014) noted that it is misleading to expect that rising levels of public debt will have similar impacts on economic growth across developing countries which have strong and weak public sector management quality respectively. Mergesa et al. (2014) finds the same pattern of negative relationship between public debt and economic growth when the data set does not consider cross-country differences in public sector management. However, when public sector management quality is considered, then public debt displays a negative relationship in weak countries with weak institutions whilst a positive relationship is displayed in countries with strong public sector management systems. In the same study, it was also found that there is evidence of a significant non-linear relationship between public debt and economic growth if the whole data set is considered. This is not the case when public sector management quality is considered. The

20 relationship displays a higher debt sustainability threshold for countries with strong public sector management.

Abbas and Christensen (2010) suggest that the contribution of domestic debt to growth seems more evident at domestic debt to deposit ratio of 35% and asserts that a ratio higher than that will strangle economic growth. This finding gives credence to the argument that domestic debt crowds out the lending to the private sector whilst at the same time preferring an argument that domestic debt is beneficial at certain optimal levels.

Furthermore, Abbas and Christensen (2010) explain that the optimal size is dependent on quality and sensitive to its quality, arguing that high levels of domestic debt can lead to economic growth if the debt is issued in the form of marketable securities which bear positive interest, and is also issued to non-banking investors. The issuing to non-banking investors supports competition in the financial sector.

Interestingly, Christensen (2005) also found that financing domestic debt was far more expensive when compared to external borrowing. He cited countries like Malawi, Ghana, Kenya among others that had set aside as much as 15% of their revenues in order to service domestic debt.

Akram (2018) in a study on the relationship of debt to investment in Pakistan observed that domestic debt had a negative and significant relationship with investment. This finding suggested that domestic debt had the effect of crowding out private sector investment. The same study, however, noted that domestic debt did not have a significant relationship with per capita GDP.

2.7 Chapter Summary

It can be broadly surmised from the literature that there are divergent views and a broad range of empirical on the impact of domestic debt on economic growth. It can also be surmised that whilst it is generally agreed by others that domestic debt is beneficial to the growth of the economy, there is also empirical evidence that suggests this this benefit is only applicable when the debt levels are within a certain threshold. This nonlinear relationship is exhibited in the response of growth to varying levels of debt with a marked negative growth at higher debt levels. When debt grows beyond certain limits it is reminiscent of the debt intolerance phenomenon as explained in Reinhart, Rogoff, and Savastano (2003). This essentially says that market interest rates rise significantly when debt reaches debt tolerance ceilings, and this may have an effect on economic

growth. There is also other empirical evidence that suggests that domestic debt can be beneficial only if certain country specific structures are in place. Zaidi (1997) for instance, argues for the productive use of domestic debt or foreign debt as long as the real rate of economic growth exceeds the real rate of interest on the government debt. It is for this reason that this paper, using time series data, will seek to investigate the impact of domestic debt on economic growth in Malawi.

It is also evident from the numerous empirical studies that a number of these studies employed the research methodology that included econometric techniques such as regression analysis and unit root analysis. This study will adopt some of these models and this is explained in the following chapter on research methodology.

22

Chapter 3 : Research Methodology

3.1 Introduction

This chapter presents the research methodology that was adopted in this study to guide the data collection, analysis of data and its findings. The first section introduces the research approach giving clarity on the focus of the study and the type of data that will be collected. The second section discusses the source of data, the population and the sample period. Thus, the research approach is discussed in section 3.2. This is followed by section 3.3 which presents the population and sample period with subsection 3.3.1 discussing data collection. Section 3.4 presents the measurement and discussion of the variables which have been adopted in the research. Finally, section 3.5 details the estimation approach which reviews the integration of the variables using unit root tests, followed by an analysis of the co-integration of the variables and thirdly the analysis concludes with a review of the short- and long-run effects.

3.2 Research approach

According to Saunders, Lewis, and Thornhill. (2007) research can generally assume three approaches, which are qualitative, quantitative and mixed methods. Qualitative research makes use of non-numerical data or data which cannot be quantified. Quantitative research makes use of numerical data or data which can be quantified, while the Mixed Methods approach makes use of both qualitative and quantitative approaches. This research has adopted a quantitative research design based on the research questions and problem of this study. The research question for this study seeks to determine the impact of domestic debt on economic growth in Malawi. The variables of the study are therefore domestic debt and economic growth and both measures are quantifiable.

It is therefore possible that a causal relationship between these variables can be determined statistically. It should be noted, however, that the qualitative method could have been used to examine the impact of domestic debt on economic growth, but this is not considered the most appropriate method in this context because the qualitative method is most effective for data that are based on meaning, expressed through words, where results are collected in non-standardised data requiring classification into categories and analysis conducted through use of themes and conceptualisation (Saunders, Lewis & Thornhill, 2007)

3.3 Data source and sample period

Secondary economic data sourced from World Bank and Reserve Bank of Malawi is used. This data spans the period 1984-2015. For the central limit theorem to hold in order to pass the normality test, the observations must not be less than 30, otherwise there will be a loss of degrees of freedom (Gujrati, 2004). The World Bank, Reserve Bank of Malawi and National Statistical Office all collect and periodically compile time series macroeconomic data. These data are tested and verified by their statistics and research departments before being published for other uses. The economic data specifically focuses on variables such as domestic debt, gross domestic product, population growth, inflation, investment and private credit, government consumption expenditure and capital formation.

3.3.1 Model Specification

This study relies on secondary time series data for the period 1984-2015 obtained from International Monetary Funds, Reserve Bank of Malawi and National Statistics Office in Malawi.

The data is then subjected to correlation analysis in order to do a preliminary review of direction of relationship of the variables. The preliminary review helps in identifying expected signs for regression method and which are formed at the correlation coefficient analysis stage. The data is initially subjected to descriptive statistics in order to understand patterns and relationships.

Following this, a growth model attempting to collate the impact of some of the key macroeconomic variables on economic growth in Malawi is formulated leading to a multiple regression model as posited by Phiri and Tchereni (2013) as well as Tchereni and Sekhampu (2013) as follows:

𝐺𝐷𝑃𝑡 = 𝛼 + 𝛽1𝐺𝑂𝑉𝐷 𝑡+ 𝛽2𝐺𝑂𝑉𝐸𝑡+ 𝛽3𝐼𝑁𝐹𝐿𝑡+ +𝛽4𝑃𝑜𝑃𝐺𝑡 + 𝜇𝑡

In the model, GDPt is the economic growth rate in year t which is a dependent variable and is the subject of this study. In the model coefficient 𝛼 is the y-intercept whilst the coefficients to be estimated are denoted as 𝛽1 to𝛽4. Section 3.4 discusses the variables that have been employed in the model in greater detail.

24 3.4 Variable description and measurement

3.4.1 Economic Growth

Economic growth can take a number of forms depending on the context of the discussion.

However, Rao (2003) defines economic development as a comprehensive process which includes improvements in all sections of society in areas such as the wellbeing of the total population on a sustainable basis whilst simultaneously minimising abject poverty and economic deprivation of society. The Organisation for Economic Cooperation and Development (OECD) on the other hand is more specific in its definition of economic growth. OECD (2016) defines economic growth as a subset of economic development with a focus on improvement on Gross Domestic Product (GDP) from one period to another period. Burda and Wyplosz (2009) defines real GDP as the final market value of goods and services within a given year when valued at constant prices. An assessment of GDP growth is measured as the annual percentage growth rate of GDP at market prices on constant local prices. Callen (2018) takes the view that another measure preferred by policy makers is the real GDP growth rate. This is the GDP that considers the total value of economic output adjusted for inflation. It is argued that this is preferred because it gives more accurate comparisons of economic growth over time. Callen (2018) asserts that if inflation is not adjusted for, nominal GDP would tend to rise over time even though the level of economic activity may have remained flat. Alternatively, Congressional Research Service (2019) argues that real GDP per capita which is calculated as a country’s GDP divided by its population is used as a measure of economic growth for comparison over time across countries because it accounts for differences in population. Ivic (2015) defines economic growth as a consistently increasing volume of production in a country or an increase in GDP. Such growth, according to Ivic (2015), can also be measured as GDP per capita and that this is expressed as economic growth in economic theory.

In agreement with this definition is Haller (2015), who defined economic growth as increase in national income per capita. Haller (2015) therefore defines economic growth as the process of increasing sizes on national economies, measured through macro-economic indicators especially GDP per capita. This study therefore adopts the definition of economic growth as measured by GDP per capita growth rate.

3.4.2 Government Domestic Debt (GOVD)

GOVD is the government domestic debt and empirical research shows varying relationships to economic growth with other studies finding that there is no effect on economic growth which results from government debt. In other studies, it has been established that government debt actually has negative effect on economic growth, whilst still others have established that a positive relationship exists between government debt and economic growth. Government domestic debt is defined as borrowings in local currency (Malawi Kwacha) from domestic or foreign sources (Kumbatira, 2008). Spilioti and Vamvoukas (2015) in their study of the Greek economy on the relationships between debt and economic growth concluded that there is a statistically significant relationship between the two variables and that this relationship is positive for debt to GDP levels at about 110%. It is for this reason that there is an increased accumulation of interest payments as debt increases and which eventually leaves the country with fewer resources for investment in the productive sectors of the economy. It is based on this understanding that this study hypothesises a negative relationship between Gross domestic debt beyond certain levels to economic growth.

3.4.3 Government Expenditure (GOVE)

GOVE is government expenditure which is expected to be positively correlated as government spending is expected to spur investment. Shim (2003) defines government expenditure as the acquisition of goods and services for current or future use. It can be argued that increased government expenditure helps to create jobs which means more disposable income for people. The disposable income will either be channelled into savings which will increase the savings ratio for the country or more goods and services will be demanded, which in turn spurs the need for increased production and provision of services. Government expenditure is a derivative of the revenue generated by the government principally from taxes. If the government does not balance its budget and runs on a deficit it means that its revenue sources are insufficient to cover its capital and recurrent expenditure. This puts pressure on the government to borrow thereby directly affecting the level of development. Wagner’s theory argued that increased government expenditure in selected areas such as health and education may spur economic growth resulting high labour productivity. The increased labour productivity, it can be assumed, provides a productivity factor necessary for economic growth. Alsharhaani and Alsadiq (2014) argue that government expenditure may positively impact private domestic investment and public spending resulting in

26 (2014) reason that government expenditure is dictated by the size of the government. However, the relationship between government expenditure and economic growth can also sometimes be negative as this public expenditure has to be financed and this funding is either sourced from debt or taxes. This results in a policy dilemma as governments have to grapple with policy decisions on the most efficient way of spending, which would translate into economic growth. Mitchell (2005) in a study designed to investigate the impact of government spending on economic performance had, interestingly, concluded that a large and growing government may actually not be a conducive factor for economic growth. Mitchell (2005) noted that there are indeed circumstances in which lower levels of government expenditure would result in higher economic growth in the same way as higher levels of spending have in certain circumstances led to economic growth. Indeed, studies by Easterly and Levine (2001) have posited that there is actually a negative relationship between government spending and economic growth. This study hypothesises a positive relationship between government expenditure and economic growth.

3.4.4 Inflation (INF)

INF has tended to command significant attention from central banks in recent times. Inflation is the annual percentage change in the cost of goods and services measured over a period of time.

Most banks have placed emphasis on price stability. It is noted that monetary policy, whether applied in form of interest rates or growth of monetary aggregates, has tended to focus on the achievement of a low and stable inflationary environment. This is presumably because central banks have generally viewed inflation as costly. It is thought that businesses and households perform poorly in unpredictable and high inflation environments. Barro (1996) finds that the estimated effect on economic growth is significantly negative when some plausible instruments are used in the statistical procedures. This leads to drawing conclusions that the relations reflect causation from higher inflation to reduced economic growth. Studies by Thilrwall (1994) suggest that inflation levels of between 5% to 8% might be the reasonable threshold for economies to achieve positive economic growth. It is very tempting for governments following an inflation target regime to benchmark against this metric. It would also be interesting to see what happens to economic growth and debt patterns in different inflationary environments. Fischer (1993) identified a positive non-linear relationship between low inflation rates and economic growth. This finding is supported by Bruno and Easterly (1998) as their study established that a negative relationship exists between high inflation rates and economic growth. The study did not, however,