Road Accident Fund for their support and time to enable me to complete this research study. To all my colleagues at the Western Cape Liquor Bureau for their support and motivation during this research study.

- Background to the research study

- Research problem statement

- Motivation/rationale for the study

- Contributions of this study

- Objectives of the study

- Research Design

- Research Questions

- Research limitations

- Structure of the Study

Identify existing possible ways to eradicate the common CG malpractices in SOEs in South Africa. What are the possible existing ways to eradicate the common CG malpractices in SOEs in South Africa.

Introduction

The title "The role of the internal auditor in improving corporate governance in state-owned enterprises in South Africa" was considered the most appropriate title for this study. Other sources that have supported this research are included in the references section of this research.

Overview of SOEs in South Africa

These influences include the differences of interests of different political parties and privatization for the restructuring and transformation of SOEs, as essential factors. OECD (2014) points out that SA economies have positioned SOEs at the core of their national improvement plans, following their dissatisfaction with their attempt to restructure and privatize SOEs in the 1990s due to a continued and increased support to SOEs to root out market failures and eliminate obstacles in the process of improvement and action of structural improvements.

Defining SOEs

According to Matsiliza, the government's intention in privatizing some state-owned enterprises was to upgrade their core business. 2011:11) explains that the government had to assess the performance of the SOEs as they were exposed to public scrutiny for failing to achieve its goals of sustaining its operations with adequate revenues and facilities available to its consumers. It is the researcher's understanding that SOEs are entities established by the government to meet the utility needs of society while exploring ways to financially sustain its SOEs and boost the SA economy.

Contributions of SOEs

Kim and Ali (2017:1) are of the opinion that SOEs enjoy more benefits compared to the private sector, as they often receive subsidies, bankruptcy protection, loans with very low interest rates and exemptions from debts owed to the government. . Kim and Ali (2017:1), however, also show that in exchange for these benefits, SOEs provide municipal services to the public at a cost that is much lower than the acceptable financial means needed to support them. during the provision of municipal services. 2015: iii) state that SOEs in SA are charged with various imperative tasks, namely increasing the competitiveness of the economy, investing in economic infrastructure, stimulating growth and fulfilling a number of industrial policy goals.

Legislation

Motivating reasons for this include the fact that the Companies Act (Act 71 of 2008) states that shareholders elect boards of directors that have a chief executive officer (CEO), while the government appoints CEOs within SOEs, resulting in the choice of the board of directors is powerless. The mandate of the PAC was to oversee the financial performance of state-owned enterprises using advisory committee reports in their role as watchdog and custodian of public funds (Makhado, 2016:5).

Theoretical framework

- Stakeholder theory

- Institutional theory

- The relevance of Stakeholder and Institutional theories to this study

The King 4 report on corporate governance (2016:5) explains that one of the benefits of understanding stakeholders' expectations is that management can develop a better stakeholder strategy. These social perceptions, standards and directions contribute to building and shaping the organization within.

Corporate Governance

- Defining Corporate Governance

- The history of Corporate Governance

- Corporate Governance challenges in SOEs in South Africa

Other CG quality indicators include the World Governance Indicators (WGI), the Ibrahim Index of African Governance (IIAG) and the African Integrity Indicators (Global Integrity) (Kanyane & Sausi 2015:30). The King Report 4 on Corporate Governance (2016:21) indicates that the code applies to all organizations, regardless of the manner and form of incorporation or establishment or whether in the public or private sector.

The Internal Audit Function (IAF)

- Mandatory guidance

- Recommended guidance

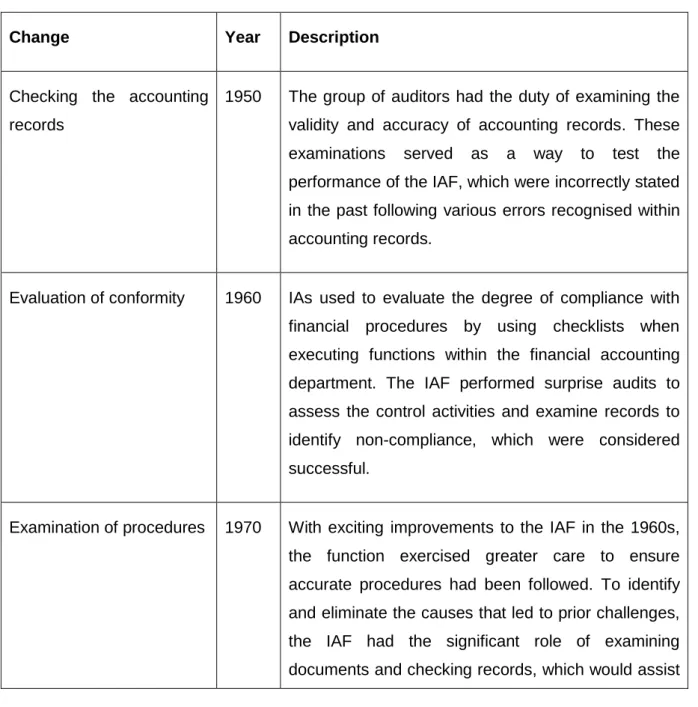

- The history of internal auditing

- The Internal Audit Function within SOEs

- The IAFs role towards corporate governance

These assessments are made to determine whether the IAF has performed its duties within the guidelines of the internal audit process. The IAF status refers to the position of the IAF and is determined by the demand for the function in support of various activities.

Combined assurance

To ensure the duties of the combined statement model are carried out effectively, the King 4 Corporate Governance Report (2016:68) states that the audit committee should take responsibility for ensuring that measures are in place and operating as intended to achieve the objectives about strengthening an effective internal control setting in the organization. While it is clear that IAs have the daunting task of ensuring that appropriate governance frameworks are regularly examined and monitoring tested, it is a fundamental responsibility of the IAF which, if regularly evaluated, would improve the governance frameworks necessary for to improve and sustain SOEs.

Risk management and SOEs

Most risks originate from the operational areas of the organization. Yaraghi and Langhe argue that the success of risk management depends on the existence and effectiveness of a governance framework that understands and promotes the risk management process throughout the organization.

Conclusion

Matsiliza (2017:40) believes that the risk assessment of SA SOEs is mistakenly focused on individual risks rather than the collaboration of various risks with the potential to address risks affecting CG. According to Bromiley et al., enterprise risk management emphasizes the importance of organizations to comprehensively and articulately address risks by aligning the risk management process between CG and the organizations' strategy.

Introduction

Purpose of study, research questions and objectives

- Purpose of the study

- Research Questions

- Objectives of the research study

It also indicates the roles the IAF plays in ensuring the achievement of ethical CG within SOEs. If CG practices deteriorate, this may pose greater challenges to the performance of the IAF in SOEs.

Research design

- Exploratory and descriptive

Research setting and delineation

Population

Sampling

In this study, the researcher chose purposive sampling based on the specific sample respondents identified who could answer the research questions and problem statement, which are part of the population discussed earlier in this chapter. The identified CG elements were purposeful because the researcher created questions from them with the aim of getting answers from this specific group of sample respondents, which the researcher was positive about, for them to answer.

Data collection tool

The content of the questionnaire was copied by the researcher, and the questionnaire was then created as an online electronic survey, with the content pasted into the survey. With the questionnaire created, the researcher could ask questions that would address the main research questions of the study, and ultimately, address the research objective.

Dependent and Independent Variables

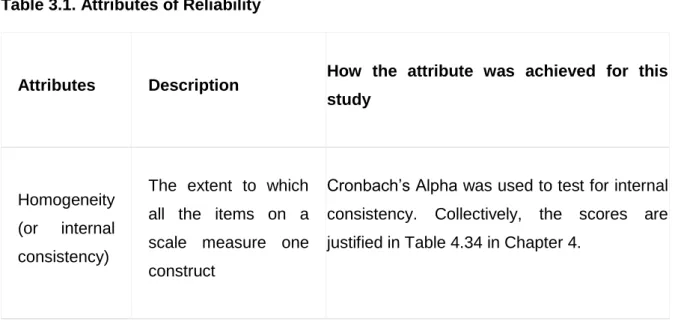

Reliability and Validity

- Reliability

- Validity

Harm to participants: The researcher ensured that this study will not result in any harm or damage to the research participants and their related companies. Violation of privacy: The researcher ensured that no private information was used for the study unless the participants gave their consent.

Data analysis

This study is therefore for academic purposes only, and although no harm can be foreseen, the researcher will not be held responsible for unforeseen circumstances that may result in harm. Besides this, the researcher did not use the collected data for personal benefit of the researcher.

Conclusion

Limitations of this research included the difficulty of accessing state-owned enterprises, particularly when striving to communicate with the target audience. In this context, several telephone calls were made to contacts with professionals in the IAFs in SOEs.

Introduction

Data collection

- Profile of the respondents

- Race and age analysis of the sample respondents

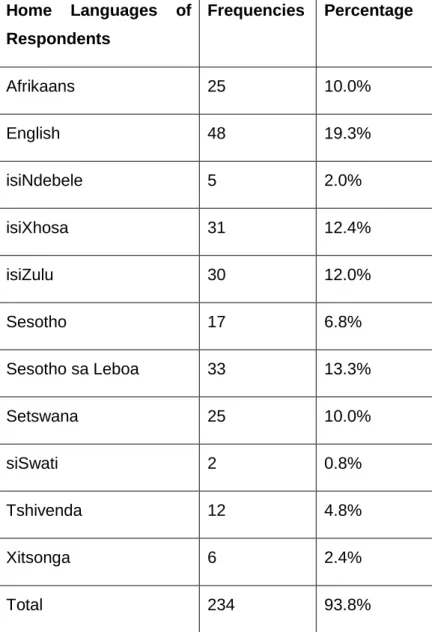

- Languages of respondents

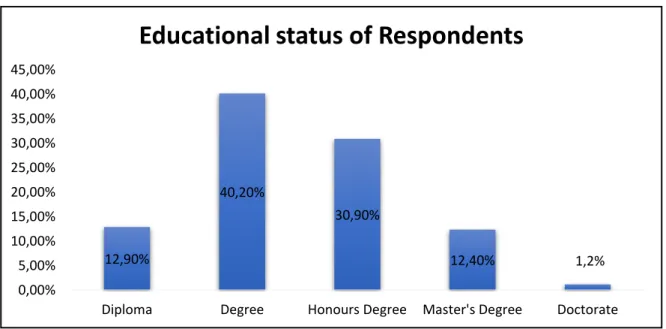

- Educational status of respondents

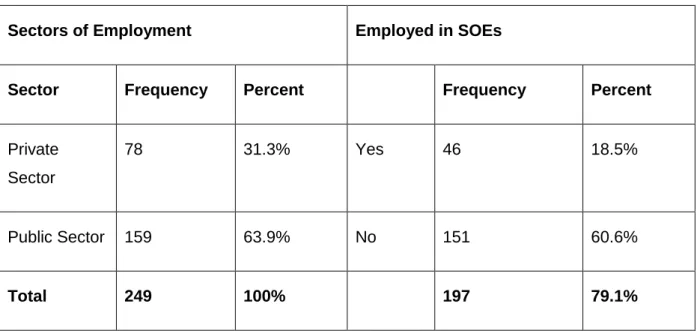

- Sector employment of respondents and those employed within SOEs

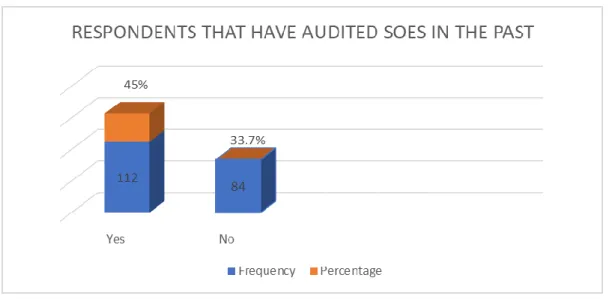

- Respondents that have audited SOEs in the past

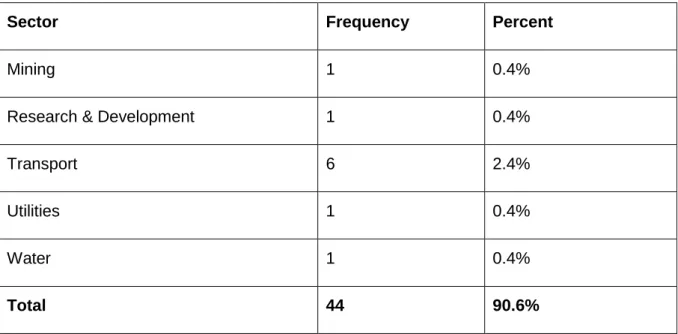

- Sectors in which the SOEs currently operate

- Staff complements of SOEs

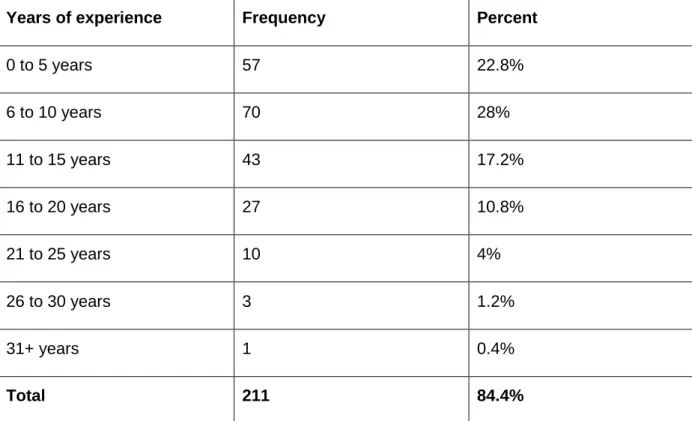

- Years of experience in the Internal Audit environment

- Respondents' professional memberships held

- Provinces where respondents perform(ed) audits

By analyzing the sample in relation to age groups, this can also serve as an indicator of exposure/level of experience within the IAF. Continued skill enhancement will only raise performance standards within the IAF, as skill along with experience will contribute to the required efficiency and effectiveness of the IAF in SOEs.

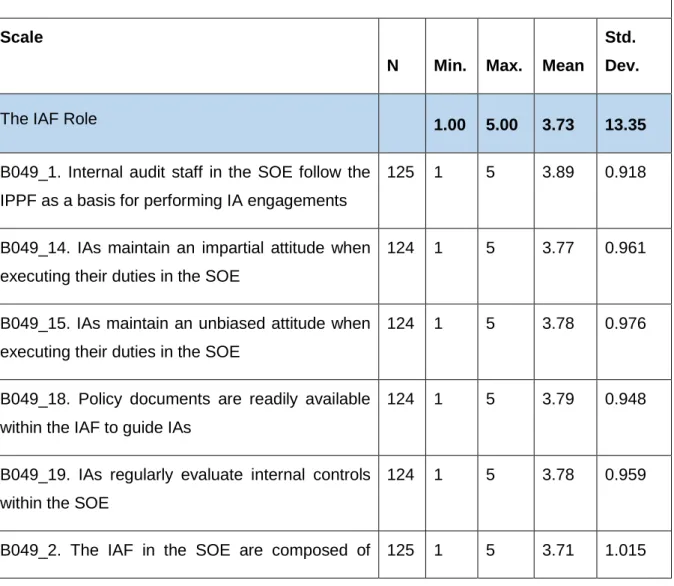

Descriptive statistics – Mean of a sample

The largest standard deviation was 1.108, also on the element of intra-company IAF reviews that take place within prescribed time frames. The highest mean score was 3.42 (n = 124), reflecting that the IAF in the SOE is well positioned to provide high quality professional assurance.

The effects of demographic variables on themes

- Compliance irregularities (dependent variable)

- Utility services (dependent variable)

- Attitude toward IAF (dependent variable)

- Mann-Whitney test performed between sector of employment and all dependent

- Mann-Whitney test performed between corporate governance mal-practices on

- Mann-Whitney test performed between, have you audited an SOE in the past, on

- Mann-Whitney test performed between, professional memberships held by

- Kruskal-Wallis H test performed between, the impact of Home Languages on

- Kruskal-Wallis H tests performed between Academic Qualifications and

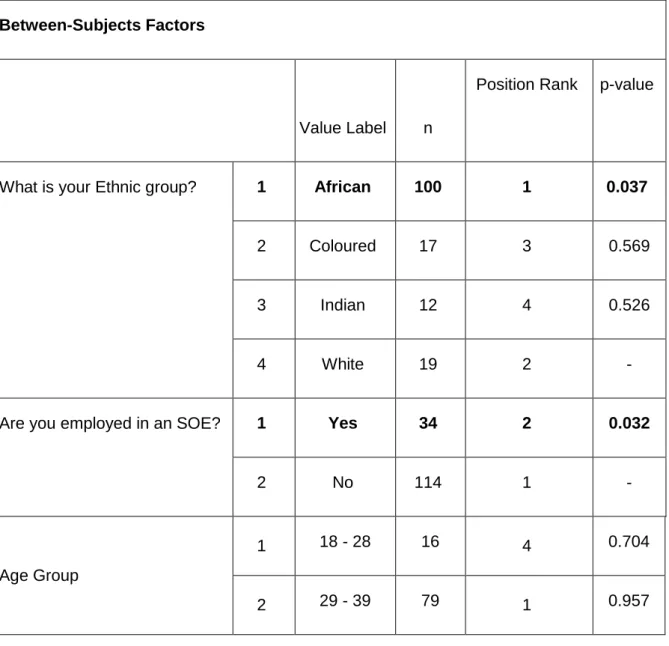

The statistical indicator (p-value) for the independent variable Have you audited an SOE in the past, as shown in Table 4.24, shows that the independent variable had no effect on any of the main CG determinants/themes. As can be seen from Table 4.26, the effect of Home Languages did not have a significant effect on the various dependent variables shown above.

Reliability and Validity analysis

- Reliability analysis

- Validity analysis

The nature of board leadership theme had no correlation with compliance irregularities and risk themes. The relationship between compliance irregularities and risks falls under the framework of a weak relationship, while the relationship of compliance irregularities with the theme of IAF resources is considered very weak.

Conclusion

Introduction

The research problem revisited

110. within each topic), namely the role of the IAF, the nature of the board's leadership, compliance irregularities, risks, IAF leadership, IAF resources, utilities and attitudes towards the IAF.

Primary research question and objective

The IAF recommends ways to management to address the CG challenges facing the SOE (mean = 3.77). With the above reflected average score, it is clear that this function is fulfilled by the IAF in SOEs.

Secondary questions and objectives

- Secondary question 1

- Secondary question 2

- Secondary question 3

The IAF in the SOE is adequately positioned to provide high quality professional assurance (mean = 3.42). The IAF in the SOE has adequate resources to provide high quality professional security (mean = 3.26).

Kruskal-Wallis H Tests, Mann-Whitney Tests and Test between-subjects conducted

This may be a sign that the IAF board does not take it seriously and maintains an ignorant attitude towards the IAF. IAF reviews are not conducted on a regular basis, which is critical to improving IAF in SOEs.

Discussion

Mann-Whitney tests were performed on the pooled data and no dependent variable had a significant effect on the gender (male/female) variable. Dependent Variable – The role of IAF had a p-value of 0.014 and had a significant effect on the employment sector, while the role of IAF and Nature of Board Leadership (dependent variables) had a significant effect with p-values of 0.010 and 0.005. on the independent variable Employment in state-owned enterprises.

Recommendations

This would enable the IAF to identify the gaps in the standards currently being followed that should be filled/amended. This would enable the IAF to identify the gaps in the standards currently being followed that should be filled/amended.

Areas for further research

The audit committee, with their extensive experience, may be able to perform these reviews if independent reviews cannot be performed regularly. An independent study on the effect of the audit committee within SOEs should be conducted to understand the strength of the audit committee and the role it fulfills within the SOE.

Conclusion

The IAF recommends to management ways to address the corporate governance challenges facing the SOE.] For each of the following statements, please indicate whether you agree or disagree using. IAs continuously assess whether all risk information is communicated in a timely manner to relevant areas within the SOE.] For each of the following statements, indicate whether you agree or disagree using