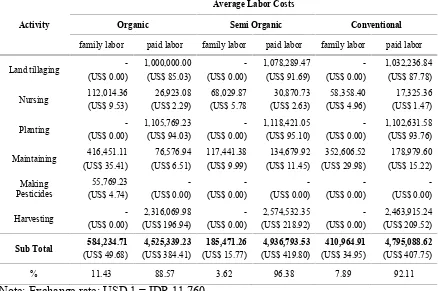

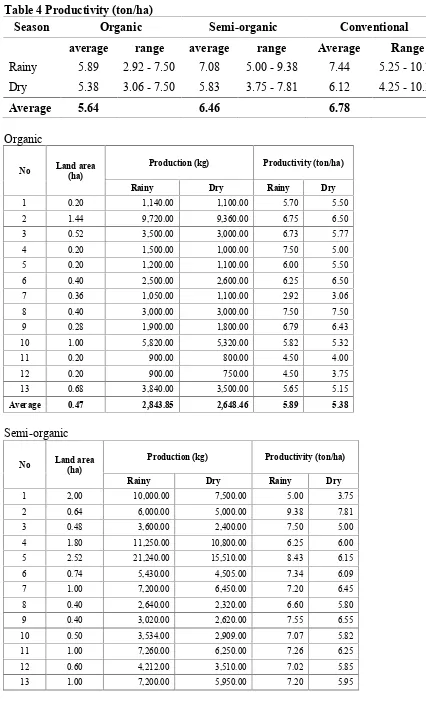

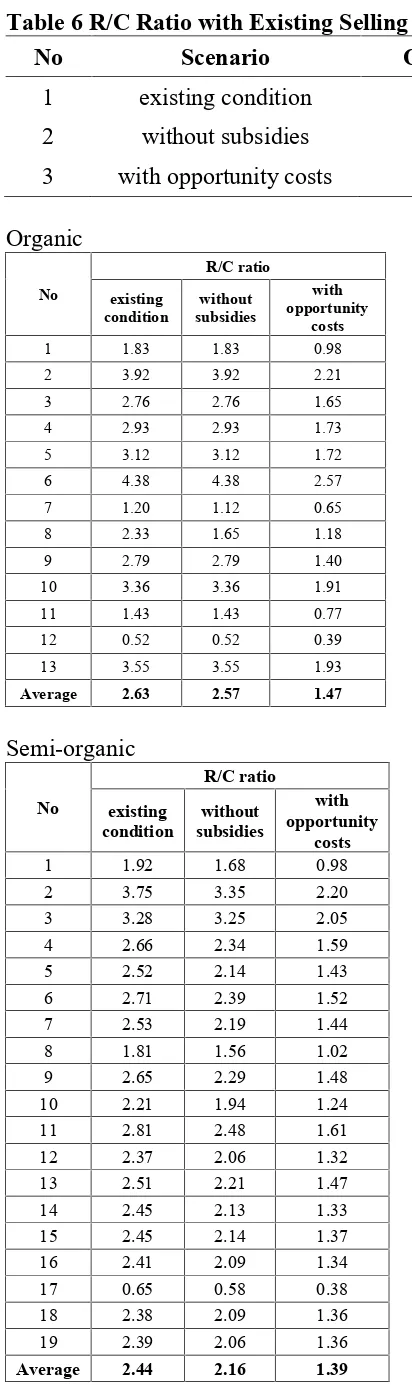

Organic Farming as an Alternative in Improving the Economic Viability and Sustainability of Rice Farms (Study case in North Sumatra, Indonesia) Diana Chalil

Teks penuh

Gambar

Dokumen terkait

55 An Introduction to Asset-Backed Securities 54 An Introduction to Asset-Backed Securities New EOC questions 56 Understanding Fixed-Income Risk and Return 55

metode ruang vektor, dapat mempermudah dalam proses pencarian informasi.. yang

Berdasarkan observasi yang dilakukan oleh peneliti di kelas X Teknologi Pengolahan Hasil pertanian (TPHP) 1 SMK N 1 Pandak diperoleh bahwa pembelajaran mata diklat

masyarakat lingkungan sekitar Masjid. Pasalnya, kader-kader pemberdayaan perempuan memang dilatih dengan keahlian pendidikan mengajar dan pendidikan kesehatan yang

bersangkutan dan manajemennya atau peserta perorangan tidak dalam pengawasan pengadilan, tidak pailit, kegiatan usahanya tidak sedang dihentikan dan/atau direksi yang bertindak

Dengan demikian para mahasiswa yang memiliki pengetahuan tentang penelitian cenderung akan meningkatkan semangat belajarnya agar dapat mencapai cita-citanya dan

Peranan fauna tanah terhadap sifat fisik tanah yaitu membantu dalam pembentukan agregat, memperbaiki struktur tanah, aerasi dan drainase; terhadap sifat kimia tanah yaitu

Hasil penelitian menunjukkan bahwa implementasi Pembiayaan Pemilikan Rumah (PPR) Syariah Griya Ar-Roya menggunakan akad istis}na’ yang bebas dari bunga, denda dan lebih