Factor Analysis Supporting Implementation SIMDA and Its Effect on Quality of Financial Statements In SKPD (Research on SKPD Local Governments Tegal)

Yeni Priatna Sari, Mohammad Alfian, Bahri Kamal Lecturers in 3rd Diploma of Accounting Study Program

of Polytechnic Harapan Bersama Tegal Jl. Mataram No. 9 Tegal

Telp (0283) 352000, Fax (0283) 353355, Hp. 081932251090 [email protected] ;[email protected]

ABSTRACT

This study aims to identify the factors supporting the implementation SIMDA SKPD and the influence on the quality of implementation SIMDA financial statements at Tegal district governments.This study was conducted based on the condition on SIMDA implementation, it is evidenced by the low quality of accounting information. The low quality of accounting information can be found on the Local Government Finance Report (LKPD) that received an unqualified opinion (WTP) of the results of an audit conducted by the BPK. The population in this study is the Local Government sectors in Tegal regency. The sample in this study were taken by purposive sampling method. The questionnaire can be further processed by 54 pieces. The hypothesis was analyzed using Structural Equation Model (SEM) with SmartPLS 2.0M3.The results of this research is the support of top management, data quality and knowledge level of human resources SIMDA has positive effect on the implementation of the SKPD in Tegal regency. Based on the research conducted is also known that the implementation SIMDA at SKPD in kabupaten Tegal has positive effect on the quality of financial reporting.

Keywords: implementation SIMDA, SKPD, quality of financial statements

INTRODUCTION

Generally the Public sector organizations in Indonesia have lack of the quality of

accounting information.Poor information can not be relied upon as consideration to

make a decision after the reporting period (Bastian, 2010). The low quality of

accounting information generated by local governments proved by the local government

obtain unqualified opinion (WTP) of the results of the audit of the Local Government

Finance Report (LKPD) conducted by BPK. This can be seen from the summary of the

information that is only 12% and 25% kabupaten city or as many as 36 counties and 21

cities of 313 counties and 85 cities in LKPD audited by BPK obtain WTP

opinion.According BPKP not obtaining the WTP opinion beberpa caused by factors,

such factor is the weakness of the internal control system, un organized asset in

countries / regions, financial statements disclosure are not in accordance with

Government Accounting Standards (SAP), the weaknesses in the system of preparation

of financial statements, and inadequate competence of human resources in the financial

management of local governments.LPKD is a combination of the financial statements

produced by SKPD - SKPD that exist in the region, in other words if LKPD less good

quality it is a reflection of the lack of good quality SKPD lapororan kuangan produced

in the area.The government and its related parties are trying to improve the quality of

the resulting financial statements, it is reflected by the issuance of PP 71 in 2010 to

replace PP 24 in 2005 to transform the base into the accrual basis of accounting in order

to improve the quality of accounting information contained in the financial statements.

Accounting information system is a tool used by management in the organization to

provide the added value that generate competitive advantage and as a control device

that generates internal information.Rostami and Mongadam (2010) states that

information technology can be used as an excellent support for the organization in

carrying out the strategy that has been set. At the moment SIA integrated with TI used

by organizations in the existing data processing is not going well can

produce output which can weaken the performance of the organization. Devi (2013)

states that the success of an enterprise information system depends on how the system is

run, the system convenience for the wearer, and the utilization of the technology used.

The application of accounting information system at the local government stipulated

in the Regulation of the Minister of Internal Affairs No. 13 of 2006 on Regional

Financial Management Guidelines.Regulation of the Minister of Internal Affairs No. 13

of 2006 has the objective which is to improve the information generated. BPKP in this

SIMDA (Local Financial Management Information System), which was introduced on

29 August 2006. This application was developed by BPKP to assist financial

management both at SKPKD (as entities reporting) as well as at the level of SKPD

(accounting entities).This application program is expected to provide more benefits to

the local government in implementing the financial management area. However, based

upon initial observations conducted by researchers in the environment SKPD in Tegal

district government found that:

a. SIMDA not fully used optimally, which led to the adoption SIMDA by SKPD can not

help maximal to achieve the goals organization governments.

b. The lack of preparation of SKPD on applicating the integrated financial softwaresuch

as SIMDA to do accounting procedures.

c. There is no certainty about the software that is used as the standard (default

software) in accounting procedures, which led to still diverse forms of financial statements

produced by SKPD, it is obviously difficult for users of the financial statements in decision

making.

d. The ability to master the operation of SIMDA uneven in each SKPD,

this softwarerequires users not only well versed in accounting but also in the use of

computers.

e. There are still many SKPD employees who prefer to use the manual paper work or

with Ms.Excell to complete its work which is considered easier than using SIMDA.

Based on this background, researchers interested in conducting research with the

title “Factors Analysis Supporting Implementation SIMDA and The Effect on

Quality of Financial Statements in SKPD (Research on SKPD in Local Governments Tegal)”

SIMDA implementation of the local government as a public sector organization is

expected to improve the quality of the accounting information contained in the financial

statements in the local government environment. With the increasing quality of financial

reporting is expected that the accounting information can be used as decision making and

as a form of management accountability for the use of the resources available in the

organization.Based on the background of the problem, we propose the following

research problem:

1. How significant is the quality of human resources effecting on the SIMDA

implementation?

2. How significant is the data quality effecting on the implementation SIMDA?

3. How significant is the management support effecting on the implementation

SIMDA?

4. How significant is the implementation SIMDA effecting on the quality of

financial reporting at SKPD?

BENEFITS OF RESEARCH

Researchers conducted this study with the aim to provide the benefits: To determine

the factors supporting the implementation SIMDA SKPD and examine their effect on the

implementation SIMDA Tegal regency administration to the quality of the resulting

financial statement on the local government Tegal.

LITERATURE AND DEVELOPMENT HYPOTHESIS

1. The Effect of Human Resources Toward Quality Implementation SIMDA.

According to Devi (2013) based on its findings stated that the successful use

addition to the training activities could build the confidence of the user so as to

anticipate the onset of anxiety and rejection from the user to the new system.

User understanding of information technology determines the success of an

information system, otherwise ignorance or anxiety new user to the system that could

lead to failures in the use of information technology. Improved understanding of the

users of information systems also affect success in utilizing information technology

(Sunarti and Nur, 1998). Hargo research results (2001) states that the level of

understanding of information technology to significantly affect the implementation

of information technology. Devi (2013) states that the level of user understanding

affect the successful implementation of accounting information systems. Thus the

proposed hypothesis is:

H 1: Human Resources has the Positive Impact Against Implementation SIMDA.

2. The Effect of Data Quality Toward Implementation influence SIMDA.

The whole process of generating data (collection, storage, and use of data) should

be done fine so that the quality of the data used can be properly processed. Lee and

Strong in Al-Hiyari, et al (2013) states that the data production process must run

properly in order to achieve quality results, in line with that Rahayu (2012) states that

quality data can affect the output of the SIA.Xu (2009) stated that the quality of

the output SIA relies on the existing input.Thus the proposed hypothesis is:

H 2: The Quality of Data has the Positive Impact Of Implementation SIMDA.

3. The Effect of Top Management Support Toward The Implementation SIMDA. According to Cooper (2006) a management commitment is the involved and

maintain behavioral management in the achievement of organizational

goals. Improved management commitment to the development of accounting systems

will have a direct impact on the quality of the implementation of the SIA, Thong, et

may not be involved in aspects of the implementation of the SIA as (in response to

the recommendation of consultants, or SIA monitor the development project), they

found that increasing the effectiveness of management's commitment information

system because they provide the resources needed for development projects

SIA.Rahayu (2012) examined the effect of management's commitment to quality

data and SIA, he found that management commitment and quality data together have

a sufficient effect on Accounting Information Systems, although the contribution of

management commitment to quality data that needs to be improved, he also found a

lack of top management support for training and funding for the development of the

resource. Thus the proposed hypothesis is:

H 3: Top Management Support has the Positive Impact Of Implementation

SIMDA.

4. The Effect of Implementation SIMDA Toward the Quality of Financial Statements

According to Grande, et al. (2011) SIA is defined as a tool when put in the field of

information technology and systems (IT) designed to assist in the management and

control topics related to economics-finance companies. In line with this, Salehi et

al. (2010) stated accounting information systems improve individual performance in

producing quality financial statements. Xu (2003) stated that the quality of the

information contained in the financial statements that bad can have adverse effects on

decision-making, such as errors in the information on the inventory may lead to

wrong decision making by managers so that excess inventory or supplies that have a

severe impact on the company profitability and customer satisfaction. Quality of the

information contained in the financial statements can be evaluated by four attributes

accuracy, timeliness, completeness and consistency, in line with Mc Leodet

of relevance, accuracy, timeliness and completeness. Thus the proposed hypothesis

is:

H 4: Implementation SIMDA has the Positive Impact on the Quality of Financial

Statements. RESEARCH METHODS

1. Data Types

Source of data in this study are primary data and secondary data

sources. According to Hartono (2013) states the primary data source is a data source

that directly provide data to data collectors, and secondary data are data sources that

do not directly provide the data to the data collector. Primary data in this study in the

form of opinions and information obtained from the respondents by providing

questionnaires that had been developed to the respondent. Questionnaires will be

given directly to the respondent so that researchers can explain the research to be

done and how to fill out the questionnaire. The bustle of the respondents caused the

respondents require a short time to do filling the questionnaire.

2. Population Research

Population studied in this research is the Local Government SKPD in Tegal

Regency that uses SIMDA in the preparation of financial statements. The

determination of this population is expected to represent a larger population, so the

results of this study can be generalized well. Another factor affecting the

determination of the population in this study is limited time owned by the researcher.

3. Sempel Research

Samples taken by the Judgment purposive sampling method. Criteria - criteria in

selecting sample namely:

2. SKPD in the local government Tegal who have financial or accounting

section.

3. SKPD in the local government Tegal which implementing SIMDA in

the preparation of financial statements.

4. Data Collection Technique

Data collection techniques used in this research is the survey method, the method

of data collection and analysis in the form of opinions from the studied subjects

(respondents) through a question-and-answer (Hartono, 2013).

5. Data Analysis

Latan and Ghozali (2012) stated that the analysis of research data is a part of the

testing process the data after the selection phase and data collection study. Analysis

of the data in this study using Partial Least Square (PLS). PLS can be used on any

kind of scale of data (nominal, ordinal, interval, ratio) and the assumption that a more

flexible terms. PLS is also used to measure the relationship of each indicator with

konstruknya. Additionally, the PLS can test the structural model

of bootstrapping against nature outer and inner models models. Because in this study

using indicators to measure each konstruknya, and also measurement model is

structural, it was decided to use PLS.

RESULTS AND DISCUSSION

1. Return Questionnaire

Questionnaires were returned is as much as 54 questionnaires from 54

questionnaires distributed.From questionnaires that have been returned, the entire

questionnaire can be used as the questionnaire completed by the

2. Data Analyst

a. Designing Model Measurements (Outer Model)

This stage is used to determine the validity and reliability of connecting

indicators with latent variables.Indicators in this study was reflective as

indicators of latent variables affecting the indicator for that use 3-phase

measurement according to Latan and Ghozali (2012), namely:

1. Discriminant Validity

Evaluation in this research was to see at the square root of average

variance extracted (AVE). Model measurements assessed by measurement of

cross loading the constructs. If the correlation constructs with each indicator is

larger than the size of the other constructs, then the latent constructs predict

better indicator than the other constructs.

If the value is higher than the value of correlation between constructs, then

good discriminant validity TERC apai.According to the 2012 Latan and

Ghozali highly recommended if AVE greater than 0.5.

Here is the formula for calculating the AVE:

AVE= Σλi

measurements can be used to measure the reliability and the results are more

conservative than the composite value reliabity (pc).

Based on the results of data processing is done with the help of software

for all constructs of> 0.50. So as to meet the requirements of convergent

validity.

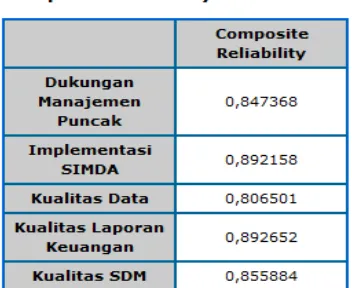

2. Composite Reliability

To determine composite reliability, if the value of composite reliability

pc > 0.8 can be said that the construct has a high reliability or reliable and>

0.6 be quite reliable (Chin in southern and Ghozali 2012).Here's the formula

for calculating the composite reliability ():

ρc=

(

Σλi)

of Composite Reliability for all constructs of > 0.70. It can be concluded that

all indicators of the construct is reliable or in other words meet the reliability

test.

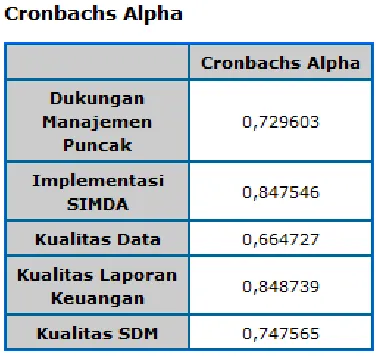

3. Cronbach Alpha

In PLS, reliability testing is reinforced by the Cronbach alpha where every

answer tested consistency, Cronbach's alpha in said well if the 0.5 and 0.3 if

said enough.

Insert Table 3

Cronbach alpha valuesgenerated all very well construct such > 0.7 So that it

can be concluded that all indicators reflective construct is reliable or meet the

reliability test. However, according to the southern and Ghozali

(2012) Cronbach alpha generated by the PLS bit of an underestimate so it is

b. Designing a Structural Model (Iner Model)

Structural models were evaluated using the R-square (R²) to construct the

dependent, Stone-Geisser Q-square test for predictive relevane and t test and

the significance of the coefficient parameters of structural lines. R² can be used

to assess the effect of latent variables independent of the dependent latent

variable does have a substantive effect.

Insert Table 4

From Table 4 it can be seen the value of R-Square for SIMDA variables show

results 0.786115 This means support of top management, data quality, and the

level of human knowledge SIMDA affect the implementation of 78.61 percent, it

shows that 21.39 percent factor or other variables that support the implementation

of SIMPDA at SKPD in TEGAL district government. While the R-square value

for the variable quality of the Financial Statements of .679233 it shows that

SIMDA affect the financial statements amounted to 67.92 percent, so that there

are 32.08 percent of the variables or other factors that affect quality of financial

statements.

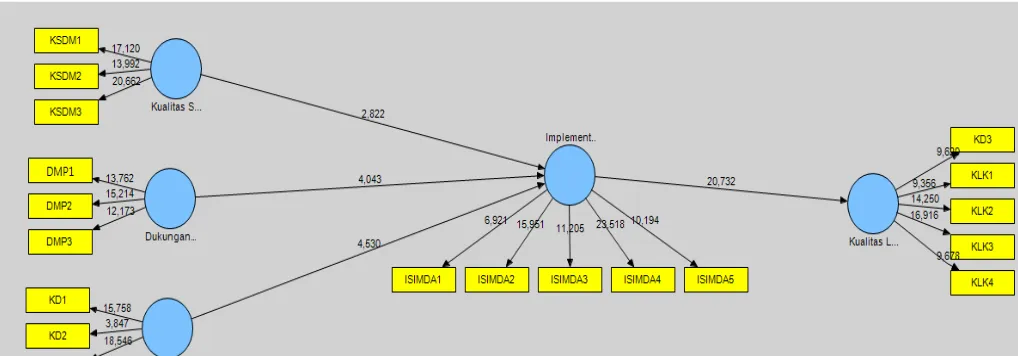

c. Construction Line Diagram

Insert Figure 1

d. Conversion Chart Path to Equation System

a. Iner Model

Inner Model specification specifies the relationship between latent

constructs with other latent constructs.

Inner Equation Model:

η 2 = β 1 η 1 +

ς

2Description:

η: endogenous latent variables.

γ:

Coefficient of influence of exogenous variables on endogenousvariables.

ξ: latent exogenous variables.

β: Coefficient influence endogenous variables on endogenous variables.

ς:

Error models.b. Outer Model

Outer Model specification specifies the relationship between latent constructs

and indicators.

Outer Equation Model:

x=Λxξ+εx

y=Λyξ+εy

Where:

x and y = matrix of manifest variables associated with the latent exogenous

and endogenous.

and =coefficient matrix.

and =matrix of outer models residue.

e. Hypothesis Testing (Resampling bootstrapping)

Based on the goals of the research, the design hypothesis test that can be made is the

design hypothesis testing in this study are presented based on the research

inaccuracies limit of () = 5 per cent = 0.05. And produce t-table value at 1.98

(southern and Ghozali, 2012).

So according to (Latan and Ghozali 2012):

If the value of t-statistic is smaller than t-table [t-statistic <1.98],

soHo accepted andHa rejected.

If the value of t-statistic greater than or equal to the t-table [t-statistic>

1.98], then Ho is rejected and Ha accepted.

Insert Table 5

Based on the above path coefficients can be seen that only the top management

support no significant effect on SIMDA, while the quality of input data and the level

of knowledge menegenai SIMDA positive effect on the implementation SIMDA.

T-statistics from the influence of top management support to the implementation of

SIMDA 4.043497> 1.98 , it means that the management support positive effect on the

implementation of the SKPD in lingkunagan SIMDA Tegal district government. The

results are consistent with Cooper (2006);Rahayu (2012); Al-Hiyari (2013).

T-statistics from the influence of the quality of data on the implementation of SIMDA

4.530046> 1.98, it means that the quality of data input positive effect on the

implementation SIMDA. The results are consistent with Xu (2009);Rahayu

(2012); Al-Hiyari (2013). T-statistics of the effect of the level of knowledge of the

implementation SIMDA users 2.822337> 1.98, it means that the level of knowledge

about the users SIMDA positive effect on the implementation SIMDA. The results are

consistent with Hargo (2001); Devi (2013). T-statistics of influence SIMDA

Implementation of the Quality of Financial Statements 20.731692> 1.98, it means that

the implementation SIMDA positive effect on the quality of financial statements or

LKPD generated by SKPD. The results are consistent with Rahayu (2012);Al-Hiyari

(2013).

1. Conclusion

Good top management support to the implementation of SIMDA is needed

in order to improve the quality of implementation SIMDA due. This study

proves that top management support affect the implementation SIMDA.

Data quality affected to the quality of implementation SIMDA because if

the quality of the data used as input data is less good, it will affect the quality of

implementation SIMDA.This study also proved that data quality has positive

influence on implementation SIMDA.

The quality of human resources greatly affect the implementation SIMDA

because if the quality of human resources that operate SIMDA not qualified then

it will be bad for the implementation SIMDA vice versa.This study proves that

the positive effect on the quality of human resources SIMDA implementation.

Implementation of good SIMDA will produce better quality financial

statements, but if the implementation is not good done SIMDA will produce

quality financial reports that are less well too.This study proves that the

implementation SIMDA affect the quality of financial reporting.

Based on the research results it can be concluded that in order to obtain

good quality reports required keangan good SIMDA dikarenaka implementation

process of preparing financial statements using SIMDA and that the

implementation SIMDA can work well it needs the support of top management,

data quality and good quality of human resources.

2. Limitations Research

Researchers realized that this study has some limitations, which include:

1. The research sample taken by the researcher as a research object only on the

obtained are less able to represent civil servants (PNS), which works on environmental SKPD

other Regional Government , Researchers restricted sampling areas because of the limited

time and energy.

2. Samples taken by the researchers is a public sector organization, so that the

conclusions of this study are not necessarily the same if the research conducted at

organizations in other sectors.

3. Measurement of all variables of this research is based on the perception of

respondents, which can cause problems if the perception of the respondents did not

correspond to the real situation. This can lead to response bias.

1. Suggestion

Suggestions given researchers expected to be used for the development of further research.Future studies are expected to not limit the sampling areas

only on one area only, so as to represent the wider population.In addition, the

sample should not be confined to the public sector organizations alone, but

expanded so as to include organizations in other sectors.

Many factors in the implementation of other information systems that can

affect the quality of the financial statements, but is not used and researched in

this study.Future studies are expected to incorporate these factors to be studied,

such as age, sex, pegaruh working environment, the benefits of information

systems, as well as other factors.

Researchers also suggest not only based on the research variables measuring

perceptions of respondents.Collecting data in future studies are expected not

only limited to the questionnaire alone, but can also be done through

interviews.The presence of investigators at the time of filling the questionnaire

respondents should also be done.This will avoidresponse bias, since

BIBLIOGRAPHY

Al-Hiyari, Ahmad., Al-Mashregy, MHH, Mat, NKN, and Alekam, JM 2013. Factors that Affect Accounting Information System Implementation and Accounting Information Quality: A Survey in Northern University of

Malaysia. American Journal of Economics, 2013, 3 ( 1): 27-31

Cooper, D. 2006. The Impact of Management's Commitment on Employee Behavior: A Field Study. American society of engineers safely.

Devi, Virsia, FP 2013. Effect of Accounting Information System Implementation of the Performance of Local Government Organisation (Research on SKPD Regional Governments Kulon Progo). Thesis. Yogyakarta: Yogyakarta Muhammadiyah University.

Endraswari, Rizki.M. 2006. Factors Affecting Applications Infoemasi Technology and Its Effect on Company Performance (Studies in SMEs Crafts Bantul, Yogyakarta). Thesis.Semarang: Diponegoro University.

Grande, EU, Estébanez, R. P, and Colomina, C. M. 2011. The impact of Accounting Information Systems (AIS) on Performance Measures: Empirical Evidence in Spanish SMEs. The International Journal of Digital Accounting

Research, Vol. 11.

Hargo, Utomo.Exploration Study2001.About Deployment IT For Small and Medium Enterprises. Journal of Economics and Business,

Indonesia Vol.16 No.2 pp.153-163.

Hartono, Jogiyanto.2013. Business Research Methodology misguided and experiences, Fifth Edition. BPFE.Faculty of Economics and Business UGM. Yogyakarta.

Indra Bastian.2010. The Public Sector Accounting An Introduction, Third Edition.Jakarta: publisher.

Southern, Heng and Ghozali, Imam. 2012. Partial Least Squares Concepts, Techniques and

Applications Using Program SmartPLS 2.0 M3, Diponegoro University

Publishers Agency.Semarang.

Mc. Leod, Raymond and Schell, George P. 2007. Management Information Systems, Tenth Edition. Upper Saddle River New Jersey 07458: Pearson / Prentice Hall. Regulation of the Minister of the Interior No. 13 Year 2006 on Regional Financial

Management Guidelines.

Government Regulation No. 58 Year 2005 on Management of Local Government.

Government Regulation No. 71 Year 2010 regarding the Government Accounting Standards. Rahayu, SK, 2012. The Factors That Support The Implementation of Accounting Information

Systems: A Survey in Bandung and Jakarta's Taxpayer Offices. Journal of Global Management.

Sajady, H., Dastgir, M., Nejad, H, H. 2008. Evaluation of effectiveness of accounting information systems. International Journal of Information Science and Technology.

Salehi, Mahdi, Rostami, Vahab, and Abdolkarim Mogadam 2010. Usefulness of Accounting Information System in Emerging Economy: Empirical Evidence of Iran. International Journal of Economics and Finance, Vol.2, No.2; May 2010.

Annual Congress of the European Accounting Association.April 20 to 22, 2011.

Sunarti, Setianingsih and Nur, Indriantoro. 1998. Effect of Top Management Support and Communications User-Developer of the User Satisfaction Relations and Participation in Information Systems Development. Indonesian

Journal of Accounting Research, Vol. 1 No. July 2 pp. 193-207

Thong, JL, Chee-Sing, Y., and Raman, K. S. 1996.Top Management Support, External Expertise and Information Systems Implementation in Small Businesses. Information Systems Research, 7 (2), 248-267. Law No. 17 Year 2003 on State Finance.

Law No. 1 of 2004 concerning State Treasury.

Xu, H., 2003. Critical Success Factors for Accounting Information Systems Data Quality, Dissertation, University of Southern Queensland.

Attachment

Table 1

Table AVE

Results Olah data by SmartPLS 2.0

Table 2

Results Olah data by SmartPLS 2.0 Table 3

Table Cronbachs Alpha

Results Olah data by SmartPLS 2.0

Table 4

Suber: Results Olah data by SmartPLS 2.0

Table 5

Table Path Coefficients (Mean, STDEV, T-Values

Suber: Results Olah data by SmartPLS 2.0

Figure 1