ACCOUNTING AND THE TIME VALUE OF MONEY

Teks penuh

Gambar

Garis besar

Dokumen terkait

Pada tujuan penggunaan time value of money adalah maximum utility terhadap barang sedangkan economic value of time tujuannya adalah maximum maslahah yang sesuai dengan

Konsep time value of money secara sederhana menjelaskan bahwa jika nilai guna uang pinjaman bagi yang dipinjamkan kepada peminjam adalah sama dengan nilai uang pada masa yang

Konsep time value of money secara sederhana menjelaskan bahwa jika nilai guna uang pinjaman bagi yang dipinjamkan kepada peminjam adalah sama dengan nilai uang pada masa yang

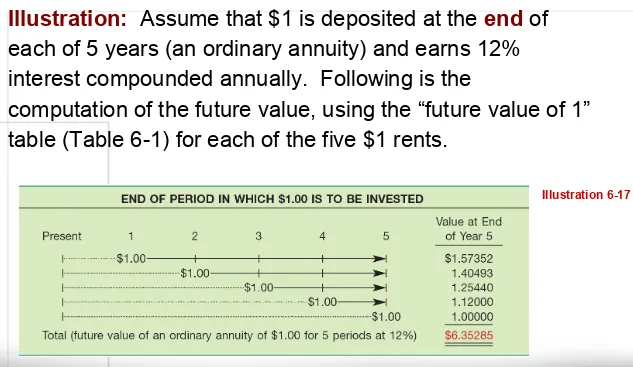

Jika Rina memutuskan untuk menabung di Bank setiap tahun dalam nominal yang sama (untuk konsep ANNUITY FUTURE VALUE). Penyelesaian

Pengakuan atas praktik time value of money dalam ekonomi konvensional pada akhirnya menimbulkan konsekuensi bahwa praktik ekonomi kon- vensional lebih dekat dengan praktik riba’

Konsep time value of money secara sederhana menjelaskan bahwa jika nilai guna uang pinjaman bagi yang dipinjamkan kepada peminjam adalah sama dengan nilai uang pada masa yang

Dalam praktik ekonomi konvensional dikenal konsep time value of money yaitu konsep yang diadopsi dari model biologi yang menganggap bahwa nilai uang di masa kini akan lebih

Future Value Anuity Nilai Anuitas Masa Mendatang Adalah suatu hal yang dimanfaatkan untuk mencari nilai dari suatu penjumlahan tahun yang akan datang dari jumlah yang diterima sekarang