CORPORATE OWNERSHIP & CONTROL

Postal Address:

Postal Box 36 Sumy 40014 Ukraine

Tel: +380-542-698125 Fax: +380-542-698125

e-mail: [email protected] www.virtusinterpress.org

Journal Corporate Ownership & Control is published four times a year, in September-November, December-February, March-May and June-August, by Publishing House ―Virtus Interpress‖, Kirova Str. 146/1, office 20, Sumy, 40021, Ukraine.

Information for subscribers: New orders requests should be addressed to the Editor by e-mail. See the section "Subscription details".

Back issues: Single issues are available from the Editor. Details, including prices, are available upon request.

Advertising: For details, please, contact the Editor of the journal.

Copyright: All rights reserved. No part of this publication may be reproduced, stored or transmitted in any form or by any means without the prior permission in writing of the Publisher.

Corporate Ownership & Control

ISSN 1727-9232 (printed version) 1810-0368 (CD version) 1810-3057 (online version) Certificate № 7881

CORPORATE OWNERSHIP & CONTROL

VOLUME 13, ISSUE 1, AUTUMN 2015,

С

ONTINUED

–

3

CONTENTS

THE COMPARISONS OF BANK FINANCIAL PERFORMANCE

BETWEEN GOVERNMENT OWNED AND LISTED BANK IN INDONESIA 345

Djoko Suhardjanto, Yohana Sylvi Putri Ayu, Nurharjanto, Iwan Setiadi

A TAUTOLOGY OF ANCIENT LEADERSHIP INTELLIGENCE:

AN INTERPRETIVE AUTO-ETHNOGRAPHIC RESEARCH 351

Sivave Mashingaidze

ASYMMETRY BETWEEN THE COST OF MEDICAL LITIGATIONS

AND THE NUMBER OF MEDICAL LITIGATIONS 356

Moshibudi J. Selatole, Collins C. Ngwakwe

PRODUCTIVITY EFFICIENCY OF THE SYSTEMIC BANKS:

EVIDENCE FROM GREECE 362

Kyriazopoulos George

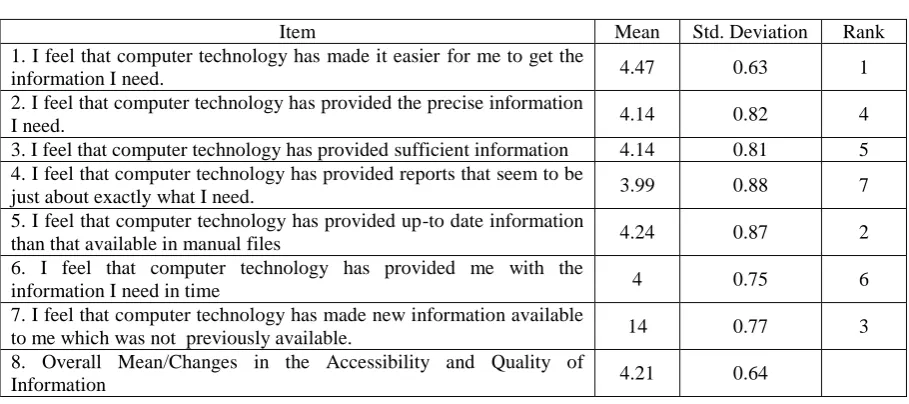

THE DECISION MAKERS' PERCEPTIONS TOWARD THE ADOPTION OF INFORMATION TECHNOLOGY BY GOVERNMENT INSTITUTIONS IN JORDAN AND ITS AFFECT ON INFORMATION ACCESSIBILITY,

AND DECISION MAKING QUALITY 370

Rami Tbaishat, Saleh Khasawneh, Abdullah Mohammad Taamneh

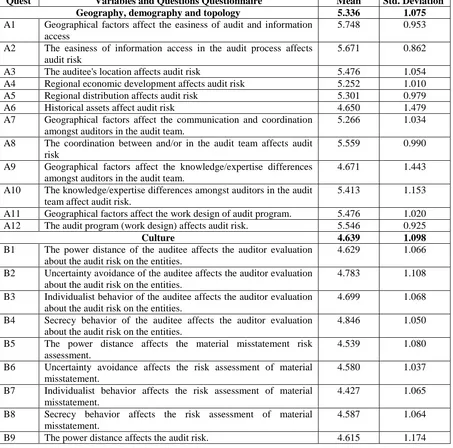

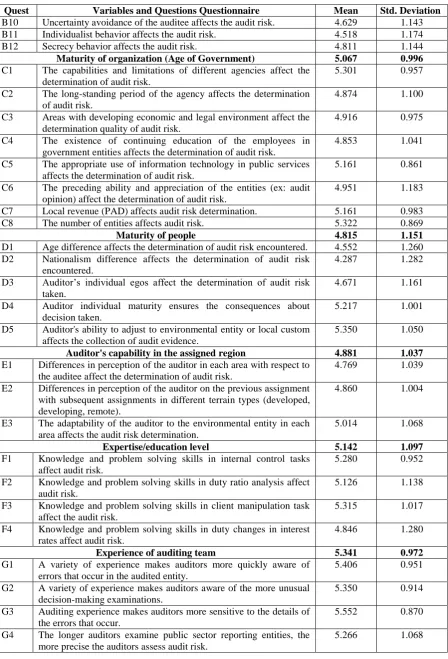

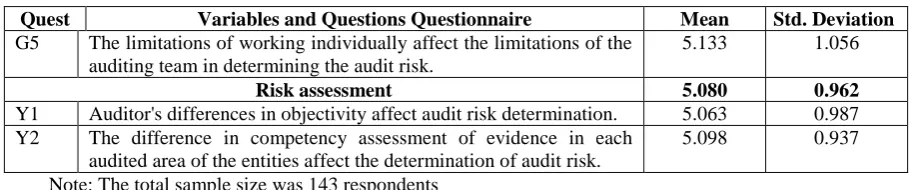

DETERMINANTS OF AUDIT RISK ASSESSMENT FOR GOVERNMENTAL AUDITS IN INDONESIA: A STUDY OF THE NATIONAL AUDIT

BOARD OF THE REPUBLIC OF INDONESIA 379

Agung Nur Probohudono, Payamta Payamta, Sri Hantoro

DOES SIZE AFFECT LOAN PORTFOLIO STRUCTURE AND

PERFORMANCE OF DOMESTIC-OWNED BANKS IN INDONESIA? 389

Apriani D.R Atahau, Tom Cronje

THE COMPANY SECRETARY’S ROLE IN CG: PRIVATE AND PUBLIC

OWNED SOUTH AFRICAN COMPANIES 401

THE COMPARISONS OF BANK FINANCIAL PERFORMANCE

BETWEEN GOVERNMENT OWNED AND LISTED

BANK IN INDONESIA

Djoko Suhardjanto*, Yohana Sylvi Putri Ayu**, Nurharjanto***, Iwan Setiadi***

Abstract

This study aims to examine the differences of bank financial performance based on listing status and government ownership. The population of this study is 120 banks in Indonesia in 2011-2013, both listing and non listing bank. Sample used in this study consist of 75 listing banks and non listing banks, not including Islamic Bank and District Development Bank (Bank Pembangunan Daerah-BPD). The data is analyzed using independent sample test. The results show that (1) Non Performing Loan (NPL) rate in non government ownership bank is lower than NPL rate of government owned bank, and (2)NPL rate of listed bank is lower than NPL rate of non listed bank.

Keywords: Financial Performance, Non Performing Loan, Listing Status, Government Ownership

*Universitas Sebelas Maret, Jl. Ir Sutami 36A, Kentingan, Surakarta, 57126, Indonesia

**Akademi Pariwisata Mandala Bhakti, Jl. Letjen. Suprapto No. 16, Sumber, Surakarta, 57138, Indonesia ***Universitas Sebelas Maret, Jl. Ir Sutami 36A, Kentingan, Surakarta, 57126, Indonesia

1 Introduction

The aim of this study is to examine the differences of financial performance (non performing loan-NPL) betweeenthe government ownership and non government ownership banks, and the differences of financial performance between listed and non listed banks.

NPL is the failure in credit. The high ratio of NPL faces by a bank will cause difficulties for the bank to develop loan portfolio and financing a new profitable loan. The high ratio of NPL can weaken and reduce the chance of growth in the economic sector, private sector, as well as job creation (United States Agency International Development, 2011). NPL acts as an indicator used to assess a bank‘s failure in credit distribution and the implication of corporate governance (CG) application.

Government ownership of the bank contains social purposes such as prioritize public interest and support the financing activity of less promising business sector that aggravates bank financial performance (Cornett et al., 2009). The government ownership that supposed to motivate the banking growth, cause the inefficiencies in bank financing performance (Berger et al., 2005). The prior study indicates that the government ownership of a certain bank cause a credit risk owned by the bank higher, especially for the countries affted by the Asia (Cheng et al., 2013). Government ownership also causes a decline in bank performance. It is because government motives contains social purposes such as prioritize public interest and support the financing

activity of less promising business sector that burden the bank financial performance (Cornett et al., 2009).

In the bank operation there is a conflict of interest between the director and the comissioner, stakeholder or the affiliated party of the director, commissioner or shareholders who might harm the bank (Guidance of Good Corporate Governance/GCG in Banking, 2012). The conflict of interest affects the policies implementation or GCG implementation in the bank (Komite Nasional Kebijakan Governance-national Committee of Governance Policy/KNKG, 2012). The conflict of interest can be controlled with intern and extern mechanism (Babatunde and Olaniran, 2009).

The study conducted by Ahmad and Campus (2013) concluded that private bank positively affect the NPL. Cheng et al. (2013) stated that bank ownership structure and listing status of a bank affect bank financial performance. Cornet, Guo, Khaksari, and Tehranian (2009) concluded that state owned bank have a lower profitability, small amount of core capital, and have a higher credit risk compare to private bank. Indonesia bank industry is a highly regulated industry along with a strict regulation of financial management and CG application. Thus the CG application on non listed bank industry of Indonesia is important to be examined.

There are differences of this study and the prior study. This study examines the differences of the government ownership and non government ownership on NPL performance of Indonesia‘s listed and non listed bank in 2012-2013.

differences of financial performance in the bank with government ownership and the bank without government ownership? (2) Are there any differences of financial performance in the bank status (listed bank and non listed bank)?

2 Literature review

Jensen and Meckling (1976) defined agency relationship as a contract involving one or more people (principals) who ask another person (the agent) to organize the company, resulting in the delegation of decision-making authority from the principal to the agent. If both parties maximizing their own interests, then the agent will not provide the best performance for the principal benefit, while the principal may restrict the possibility of applying incentives for agents in accordance with their performance. Thus, the company needs to provide cost to ensure the agents will make a right decision in accordance with the principal‘s perception. It is explained that the agency cost will occurs when the principal and agent itself have some conflict of interest and when the principal face some difficulties in controlling the agent.

As the corporate organizer, manager tends to have more internal information and understand company future prospect better than the stakeholder, thus the manager needs to inform the current condition of the company to the owner. Sometimes the information are not significant with the real condition, these kind of informations are named information asymmetric (Ujiyantho and Pramuka, 2007). The asymmetric information can be a conflict trigger of stakeholder and manager.

The manipulation conducted by manager which started by conflict of interest can be minimized with certain monitoring mechanism to align the current interests. The alignment mechanism can be done by widening the managerial ownership (Jensen dan Meckling, 1976), company stocks owned by institutional investors (Colpan et al., 2007), and the monitoring process perform by board of directors (Ujiyantho and Pramuka, 2007).

Managerial ownership aims to surpress the conflicts between managers and external stakeholders (Adnan et al., 2011). Institutional ownership take some roles in company monitoring along with these kind of reasons: (1) institutional ownership own the majority of company stocks, (2) the high rate of investation profit potential, (3) institutional ownership has less ability in financing stocks without affecting its price, (4) has the strong impact for the management, (5) has the fiducia responsibility to the company owner, and (6) has the ability to monitor the executive performance. Board of director take some roles in company operation by control the top management activities and controlling company resources and operational activity (Pandya, 2011). The relationship of stakeholder and manager is the real definition of agency relationship, thus the issue

“separation of ownership and control” can be stated as the common issue of agency problem (Jensen and Meckling, 1976), thus it can be concluded that agency cost can develop the ownership structure of the company.

There are other perspectives of ownership structure based on company stakeholder numbers, they block ownership and dispersed ownership (Adnan et al., 2011). Block ownership is the condition when the party owned company stocks more than five percent (dispersed ownership). Block owners tend to put more attention on company performance than individuals who own stocks less than 5% (dispersed ownership). Dispersed ownership owned fewer portions of the stocks, thus they have a lower motivation to monitor the company than the block owners did. The block holder will monitors manager‘s performance more thoroughly and hold a power to affect board decision taking process. Thus, the existence of block holder can positively affect company performance that realized through the achievement of low capital cost and monitoring effectiveness (Dwivedi and Jain, 2005).

This study focuses on institutional ownership by examining the differences of bank financial performance in government owned bank and public bank, as well as the differnces of financial performance in listed bank and non listed bank.

2.1 Corporate governance

CG is defined as an environment developed by trust, ethics, and moral value that represent synergic effort from related parties (Crowther and Seifi, 2011). According to the simple finance model concept, or commonly knowned as agency theory, the main problem of CG is constructing the regulations and incentives in order to effectively align agent‘s behavior according to principal‘s interest. It is assumed that agent (manager) is an untrusted person, have their own interest and opportunistic behavior, thus CG that can protect principal‘s interest and control the agent‘s behavior is needed (Jensen and Meckling, 1976).

mechanisms are developed by national or international instituton in the best practice (disclosure quality, audit and accounting standard, employee regulation, standard environment, industry product standard, and listing requirement).

CG mechanism used in this study are (a) internal mechanism, in this case ownership structure. Ownership structure is the structure of company ownership sharing focused on the broad role of stockholders, thus they can control company management (Chen, 2001). The proxy used to measure the ownership structure is government ownership. Government ownership is government involvement in the business sector realized with the company ownership for a certain purposes, among others is privatization interest to restructure and ensure the viability of an institution (Ghozali, 2013). (b) the external mechanism is a bank listing status. Go Public is a bank effort in socializing their company by accepting the public funds inclusion, whether in ownership term or establishment of company management policy. The capital market has an important role in extern mechanism. The capital market is continuously monitoring and put an objective value for the company or even for the company management. The company stock performance is a transparency value of public perception on company value for manager and owner. The measurement can be used by the stockholders to assess manager‘s performance and as a consideration in providing incentives for managers

Bank with government ownership is less monitored by their owner because the owner believes that the bank will be strictly monitored by the government. Less supervision performed by the owner leads the bank to face more risk and likely to be bailed out by the government when a crisis take place. It is then become a cause for the manager to put less effort in improving the bank performance. (Cheng et al., 2013). Berger et al., (2005) stated that government owned banks tend to have low efficiency and high rate of NPL because government ownership will reduce the credit access, reducing financial development system, and restraining the economic growth. Cornett et al. (2009) stated that state-owned bank has low profitability, less main capital, and higher credit risk compared with non-state owned bank. The differences of government ownership can affect bank performance (Berger et al., 2005; Cornett et al., 2009; Cheng et al., 2013). Thus, the first hypothesis can be formulated as:

H1: There are differences in financial performance of bank with government ownership and bank without government ownership.

The bank listing status can improve the asset quality and capital adequacy ratio. The bank listing can affect the risk taking process of the bank because the listing bank will have more strict regulation compare to non listing bank. The bank listing status is also able to realize the bank capital that can be reached with lower costs (Cheng et al., 2013). Listed bank can developed faster, using less financial leverage, investing less in intangible assets, and generate smaller returns compare to non listed bank (Capasso, Rossi, and Simonetti, 2006). The differences in the level of risk taking in turn affects the difference in the bank financial performance (Capasso et al., 2006; Claessens and Tzioumis, 2006; Petranov, 2006; Cheng et al., 2013). Thus, the second hypothesis can be formulated as:

H2: There are differences in financial performance of listed bank and non listed bank. 3 Research method

This study population is all banks in Indonesia in 2011-2013, both listed and non listed bank. The total number of banks in Indonesia is 120 banks; consist of 36 listed banks and 84 non listed banks. The sample used in this study is 225 banks (consist of 75 listed banks and non listed banks in 2011-2013) selected using purposive sampling technique. The purposive sampling technique is a non probability sampling with a certain criteria (Sekaran and Bougie, 2013). The selected sample criterias are a: (1) non Islamic banks dan non district development banks operated in Indonesia in 2011-2013, (2) the banks issued annual report of 2011 to 2013 which can be accessed by authors, (3) there are ownership structure and bank listing status related data that becomes main focus of this study, either in the annual report or other publicity reports.

This study used independent sample test analysis. Data used in this study is a secondary data taken from company annual report in 2011-2013.

4 Analysis result

The first hypothesis examines whether there are financial performance differences of bank with government ownership and bank without government ownership. The hypothesis testing results can be seen below:

Table 1. T-test of Government Owned Bank-Non Government Owned Bank-1

Government Ownership Notation N Mean

NPL of Government Ownership Bank NPL of Non Government Ownership Bank

1 0

22 201

-0.032 -0.016 Notes: 1 = Government ownership bank

According to the Table 1, it can be seen that the average NPL of government ownership bank is -0.032, meanwhile the average NPL of non government ownership bank is -0.016, the value

indicates that the NPL of government owned bank is different with the NPL of non government owned bank. The results of independent sample t test can be shown as:

Table 2. T-test of Government Owned-Non Government Owned-2

Notes

Levene‘s Test for Equality of Variances

t-test for Equality of Means

F Sig. t Sig. (2-tailed)

NPL Equal variances assumed 0.982 0.323 -4.44 0.000

According to the Table 2, it can be seen that F count of Levene's Test is 0.982 with the probability of 0.323 (>0.05%). It indicates that both of the banks share a same variance. Then, seen from the output of equal variance assumed which showed the t value in the amount of -4.44 with the significance probability of 0.000 (<0.05), the value showed that NPL of government owned banks are different with NPL of non government owned banks (H1 is accepted).

The t-test results in Table 1 and 2 show that the average value of NPL of government owned banks are greater than the average value of NPL of non

government owned banks, with the significance rate at the amount of 0.000 (0%). It shows that government owned banks have worse financial performance compared to non government owned banks. This condition indicates that the government owned banks have a high NPL rate. It shows that the government owned banks have a higher credit distribution failure rate compared to the non government owned banks.

The second hypothesis examines whether there are differences of financial performance of listed bank and non listed bank. Below is the result of the second hypothesis testing:

Table 3. T-test of Listed Bank-Non Listed- Bank 1

Government Ownership Notasi N Mean

NPL Listed Bank NPL Non Listed Bank

1 0

106 117

-0.021 -0.014 Notes: 1 = Listed bank

0 = Non listed bank

According to the group statistics table above, it can be seen that the average NPL of listed bank is 0.021, while the average NPL of non listedbanks is

-0.014, the values indicate that the NPL of listed banks and non listed banks are different. However, the independent sample t test is still needed.

Table 4. T test of Listed Bank - Non Listed Bank-2

Notes

Levene‘s Test for Equality of Variances

t-test for Equality of Means

F Sig. t Sig. (2-tailed)

NPL Equal variances assumed 1.418 0.235 -3.366 0.001

Independent samples t test table showed that F count of Levene‘s Test is 1.418 with the probability in the amount of 0.235 (>0.05%). It is shown that both of the banks share the same variance. It can be seen from the output of equal variance assumed t value is -3.366 with the significance probability at 0.001 (<0.05). The value means that the NPL of listed banks and non listed banks are different (H2 is accepted).

According to the t test result it can be seen that the average NPL of listed banks is smaller than the average NPL of non listed banks with the significance level of 0.001 (0.1%), thus it can be concluded that the performance of listed banks (NPL= -0.021) are better than the performance of non listed banks (NPL= -0.014). This condition usually takes place in listed banks owned by block holder/block ownership.

Block ownership controls company performance more than dispersed ownership, because the dispersed ownership is lack of motivation in monitoring the managers (Jensen and Meckling, 1976). Block holder in the listed banks will perform more control to the company, thus company performance can be improved.

5 Discussion

put less effort in improving the bank performance. (Cheng et al., 2013). As the result, the performance of government owned bank is worse than the performance of non government owned bank.

This statement is supported by Ianotta et al. (2012). They stated that the failure risk of government owned bank is lower than the failure risk of non government owned bank. However the failure risk does not indicate that the operational risk will be low. The operational risk also can not reflect a good economic and financial condition of the bank. It is caused by government support in the form of protection mechanism.

The mechanism is a benefit for state owned bank because it provides a lower cost of capital. However the protection does not affect market order and provide an opportunity for the market to improve the risk taking. Thus, while having a low risk of failure, government ownership pose a high operational risk, as an illustration, the economic and financial conditions are worse than the non government ownership bank.

The analysis result is in a line with the study conducted by Ahmad and Campus (2013). They stated that dispersed ownership can reduce bank performance and improve the bank risk. Bank with listing status, dispersed ownership, and less managerial control from the owner, will lead to the assymetric information and conflict of interest between the owner and managers. (Jensen and Meckling, 1976). It leads to the decision taken will be more benefiting for the managers. Lack of supervision and managerial control can lead managers to take high risks in the loan portfolio with the aim of improving the efficiency of short-term costs through lending to low quality debitors, which can increase the future NPL rate. This analysis result supports the statement that listed bank performance (with block ownership composition) is better than non listed bank performance (with dispersed ownership composition).

6 Conclusion

This study aims to explain the differences of bank financial performance in government owned banks and non government owned banks, and also the differences of bank financial performances in listed status banks and non listed status banks in Indonesia. The study results indicate that:

1. NPL rate of non government owned bank is lower than the NPL rate of government owned bank. It means that the bank financial performance of non government owned bank is better than the bank financial performance of government owned bank. It is because the government ownership of the bank is followed by political interest, thus the government program will not provide benefit for the bank.

2. NPL rate of listed bank is lower than the NPL rate of non listed bank, it indicates that the bank financial performance of listed bank is better than the bank financial performance of non listed bank. It

indicates that block holder ownership in the listed bank has positive effect to the bank financial performance.

7 Suggestions

According to the research result, below are the suggestions that can be given:

1. The research result showed that the bank financial performance of non government owned bank is better than the bank financial performance of government owned bank. This results indicates the need to review the government ownership in the bank to reduce government involvement in the bank operations, that leads to the poor performance of bank.

2. The needs to divide the stock ownership into some block holder ownerships in order to avoid dispersed ownership, which leads to less supervision and monitoring of bank management. As the result, bank performance faces an inefficiencies.

3. The main suggestion that can be given are to develop a supervision regulation related to ownership structure, perform a more strict monitoring of credit allocation process, thus the common guidance of risk management can be gained, for example risk governance.

8 Research limitation

The limitations of this study are:

1. This study is conducted in a short period (2011-2013). Thus, the analysis result that can be given is not precise enough.

2. The variabels used in this study are only ownership structure and bank listing status. In the future, other studies can develop the research with other variabels, such as capital structure or managerial remuneration, in order to examine the result consistency of bank financial performance.

9 Research result impication

9.1 Theoritical implication

The result can improve the understanding of ownership structure of bank management in Indonesia. The result is supporting the statement which stated that the bank financial performance of non government owned banks and listed banks are better than the bank financial performance of government owned bank and non listed bank.

9.2 Managerial implication

opportunity is pretty high. Thus it will attract more investor to invest in Indonesian bank. This condition will support the bank function of financial intermediation organization that will prop other industrial sectors. In the end bank industry will support the national economic.

References

1. Adnan, M. A., Htay, S. N. N., Rashid, H. M. A., and Meera, A. K. M. (2011), ―A Panel Data Analysis on the Relationship between Corporate Governance and Bank Efficiency‖, Journal of Accounting, Finance and Economics, Vol.1, No. 1, pp. 1-15.

2. Ahmad, F, and Campus, P. (2013), ―Ownership Structure and Non-Performing Loans: Evidence from Pakistan‖, Asian Journal of Finance & Accounting, Vol. 5, No. 2, pp. 268-288.

3. Akpan, E. S., and Riman, H. B. (2012), ―Does Corporate Governance affect Bank Profitability? Evidence from Nigeria‖, American International Journal of Contemporary Research, Vol. 2, No. 7, pp. 135-145.

4. Babatunde, M. A. and Olaniran, Q. (2009), ―The Effects of Internal and External Mechanism on Governance and Performance of Corporate Firms in Nigeria‖, Corporate Ownership & Control, Vol. 7, No. 2, pp. 330-344.

5. Berger, A. N., Imbierowicz, B., and Rauch, C. (2012), ―The Roles of Corporate Governance in Bank Failures during the Recent Financial Crisis‖, The Southern Finance Association Annual Meeting 2012.

6. Berger, A. N., Clarke, G. R. G., Cull, R., Klapper, L., and Udell, G. F. (2005), ―Corporate Governance and Bank Performance: A Joint Analysis of the Static, Selection, and Dynamic Effects of Domestic, Foreign, and State Ownership‖, World Bank Policy Research Working Paper 3632.

7. Chen, J. (2001), ―Ownership Structure as Corporate Governance Mechanism: Evidence from Chinese Listed Companies‖, Economics of Planning, Vol. 34, No. 1, pp. 53-72.

8. Cheng, M., Zhao, H. and Zhang, J. (2013), ―The Effects of Ownership Structure And Listed Status On Bank Risk In China‖, The Journal of Applied Business Research, Vol. 29, No. 3, pp. 695-710.

9. Cornett, M. M., Guo, L., Khaksari, S., and Tehranian, H. (2009), ―The Impact of State Ownership on Performance Differences in Privately-Owned versus State-Owned Banks: An International Comparison‖, Journal of Financial ntermediation, Vol. 10, No. 1, pp. 1-21.

10. Crowther and Seifi. 2011. Corporate Governance and International Business. bookboon.com.

11. Departemen Keuangan Republik Indonesia (Badan Pengawas Pasar Modal dan Lembaga Keuangan), (2008), Identifikasi Pemodal Asing di Pasar Modal Indonesia. Jakarta: Badan Pengawas Pasar Modal dan Lembaga Keuangan.

12. Dwivedi, N. and Jain, A. K. (2005), ―Corporate Governance and Performance of Indian Firms: The Effect of Board Size and Ownershhip‖, Employee Responsibilities and Rights Journal, Vol. 17, No. 3, pp. 161-172.

13. Ghozali, Imam. (2013). Aplikasi Analisis Multivariate dengan Program SPSS. Semarang: Badan Penerbit FE Universitas Diponegoro.

14. Hasan, I. and Xie, R. (2012), ―A note on foreign bank entry and bank corporate governance in China‖, BOFIT Discussion Paper, Vol. 8, No. 1, pp. 1-23. 15. Jensen, M. C. and Meckling, W. H. (1976). Theory of

the Firm: Managerial Behavior, Agency Cost and Ownership Structure. Journal of Financial Economic, Vol. 3, No. 4, pp. 305-360.

16. Komite Nasional Kebijakan Governance. 2006. Pedoman Umum Good Corporate Governance di Indonesia. Jakarta: KNKG.

17. Niawati, P. (2011), Analisis Pengaruh Penerapan Corporate Governance, Kepemilikan, dan Ukuran (Size) Bank terhadap Kinerja Bank. Tesis Fakultas Ekonomi Program Magister Manajemen Universitas Indonesia. Jakarta: FEUI.

18. Organisation for Economic Co-operation and Development (OECD), (2006), Corporate Governance of Non-Listed Companies in Emerging Markets. Paris: OECD.

19. Pandya, H. (2011), ―Corporate Governance Structures and Financial Performance of Selected Indian Banks‖. Journal of Management and Public Policy, Vol. 2, No. 2, pp. 4-21.

20. Peraturan Bank Indonesia Nomor 8/4/PBI/2006 tentang Pelaksanaan Good Corporate Governance bagi Bank Umum.

21. Poudel, R. P. S. and Hovey, M. (2013), ―Corporate Governance and Efficiency in Nepalese Commercial Banks‖, International Review of Business Research Papers, Vol. 9, No. 4, pp. 53-64.

22. Sekaran, U and Bougie. (2013), Research Method for Business: A Skill Building Approach. Chichester: Wiley.

23. Uadiale, O. M. (2010), ―The Impact of Board Structure on Corporate Financial Performance in Nigeria‖, International Journal of Business and Management, Vol. 5, No. 10, pp. 155-166.

A TAUTOLOGY OF ANCIENT LEADERSHIP INTELLIGENCE:

AN INTERPRETIVE AUTO-ETHNOGRAPHIC RESEARCH

Sivave Mashingaidze*

Abstract

The main purpose of the article was to look into how business and management could extract from ancient data base of leadership intelligence for solutions. The article cherry picked a few great historical leaders who won wars using their leadership intelligence. An Interpretive auto-ethnography methodology was used and strategic intelligence qualities such as Changing the mood, Boldness of vision, Doing the planning, Leading from the front, Bringing people with you and finally Likeability Factor was explored from these leaders. The results was that all the above mentioned strategic intelligence qualities were quintessential for these historical leaders to achieve their objectives hence business and management today can learn and tap from these qualities for a competitive strategy.

Keyword: Leadership Intelligence, Tautology, Interpretive

*College of Economic and Management Sciences, Department of Business Management, University of South Africa Tel: +2763 0095605

1 Introduction

According to a 2000 study by Yale University and the Center for Socialization and development-Berlin, ―people, unlike animals, gain success not by being aggressive but by being nice. The research found that most successful leaders, from CEOs to PTA presidents, who treated their subordinates with respect and made genuine attempts to be liked. Their approach garnered support and led to greater success.‖ There is more to intelligence than getting a high score in an aptitude test or solving enigmas others are unable to solve. Intelligence comes in many forms; it‘s just not limited to mental capacity. There are other ‗intellectual‘ factors perhaps more important at work in a leader‘s life. Intelligence is the ability of the mind to comprehend, use thought and reasoning for problem solving – the ability to acquire knowledge and use it practically. The 4 Intelligences of a Leader; they are wisdom, character, social and spiritual intelligence. According to Sternberg, (2003) Wisdom Intelligence is a form of intelligence, needed in today‘s world and is having a deep understanding of the reality of people, things, events or situations, resulting in the ability to choose or act accordingly to produce optimum results. On the other hand Webb, (1915) defined character intelligence as pursuing and developing moral excellence, which leads to self-mastery.

For instance, skilled workers using the hammer and chisel crafted ancient statues very methodically and patiently, shaping some of the most renowned pieces of art we admire today. Within time, an onlooker could see a face or an image emerge from the granite rock. This process also happens with

people. During our childhood, we are similar to a marble slab, which, over time, through choice, action and self correction, you and I create the right actions and new outcomes, which form a new character. Social intelligence is a term coined by Daniel Goleman in his best seller bearing the same name. According to Goleman (2006), social intelligence possesses two components. The first component is what he calls social awareness that is what we sense about others. The second is social faculty, which is what we do with that awareness. In other words, social intelligence is how we read others and approach them to gain the best possible connection. The last part of intelligence is spiritual intelligence which is the ability to build and sustain a relationship with God where you attract His unrelenting favor, to the point it begins to overflow into your life. Favor can be defined in many ways. Cicero coined its original meaning; ―to show kindness to someone‖ or a ―gift given as a mark of favor (Zohar, 2012).

2 Research methodology: an interpretive auto-ethnography

official and personal -, diaries, memorials, epistles, videos, photos) and techniques (triangulation of information and in-depth analysis of the sources) (Abrahão, 2008a). This understanding can also be found in Pineau (2010). According to Ellis and Bochner (2006) auto-ethnography is a research method that uses ―stories to do the work of analysis and theorizing‖ (p. 436). Holman Jones (2005) writes that auto-ethnography is ―setting a scene, telling a story, weaving intricate connections among life and art, experience and theory, evocation and explanation . . . and then letting go, hoping for readers who will bring the same careful attention to your words in the context of their own lives.

3 Likeability factor in the ancient leaders

According to Sanders (2006), the Likeability Factor defines likeability as ―an ability to create positive attitudes in other people through the delivery of emotional and physical benefits.‖ People with high L -factors generate positive feelings in others and, in doing so, improve their own lives. Author Tim Sanders posited that, the more likeable a person is, the better the chance that person has of receiving a positive outcome when faced with decisions that are out of his or her control. Sanders stress four characteristics that are critical to boosting L-factors:

1) friendliness, or the ability to communicate liking and openness to others;

2) relevance – the capacity to connect with others;

3) empathy – the ability to recognize, acknowledge, and experience other people‘s feelings; and

4) Realness, or integrity and authenticity.

3.1 Strategic intelligence qualities

Gifford, J. (2010) summarized the concept of Strategic Intelligence and likeability factor based on studying successful leaders of change. These leaders shared these seven qualities:

1. Changing the Mood 2. Boldness of Vision 3. Doing the Planning 4. Leading from the Front 5. Bringing People with You

3.2 Changing the mood

Nelson Mandela changed the mood of South Africa to an extent that seems unbelievable, even with hindsight (Gifford, 2010). For decades, black and white South Africans had been embattled in an increasingly bitter conflict. Nelson Mandela himself was regarded as a violent terrorist leader, in league with foreign powers, determined to overthrow the government of South Africa. To understand Mandela‘s achievement it is necessary to remember that during the apartheid

period and the civil unrest that it created, Nelson Mandela was clearly perceived to be a terrorist and a communist, apparently in league with foreign powers, determined to bring down the South African state and install a black communist regime that would be implacably hostile to whites. Mandela‘s Truth and Reconciliation Commission took much of the poison out of the bitter recriminations that both sides had stored up against the other, but in a real sense it was simply the personality of Mandela himself that provided the cure; calm, smiling, dignified, inclusive (Mandela, 2008).

3.3 Boldness of vision

According to Andrews, (1988), leaders are often judged by the vision that they bring to their organization. A great vision for any organization is simple and, well, bold, but it need not be grand. At this more understandable, more mundane level, it becomes clear that every leader does indeed need a vision. The leaders from history in this section were able to offer their nations a truly momentous vision, a vision that changed the course of history. What is interesting is that they had not been born, as it were, with this vision. They had not been carrying it around, waiting to proclaim it to the right audience. They found themselves in a particular set of circumstances; with a particular set of issues—and suddenly it all became clear. In order to lead their country forward, they were able to articulate what everybody needed to hear.

3.3.1 Abraham Lincoln (1809–1865)

3.4 Doing the planning

One of the most underrated accomplishments of any manager is planning. Not in the obvious sense in which planning is one of the key functions of every managerial job specification (many managers‘ jobs consist of very little else than planning, that is ensuring that a certain result has been delivered by a particular deadline) but rather in planning the broad outline of what it is that you intend to achieve in your current role. It is dauntingly easy to get bogged down in the details of any job. It is dauntingly easy to get bogged down in the details of any job. Sometimes simply keeping things running on a day-to-day basis seems like a pretty big achievement. In fact, that always feels like a pretty big achievement, because it is. But every manager needs also to find the time to plan exactly how they intend to achieve their broader objectives on the timescale that they have allowed themselves. The really great planners are the ones who seem able to hold huge amounts of information in their heads, who never for one moment lose sight of the objectives, or of the precise order in which they should be achieved. As a result, such managers seem to pull off a succession of miraculous successes. They are not, of course, miraculous; they are the product of meticulous planning.

3.4.1 Napoleon Bonaparte (1769–1821)

Napoleon is known as one of the great military commanders of all time – possibly the greatest (Semmel, 2004). His leadership skills were based on a wide range of personal characteristics and strengths. He had a remarkable memory, able to store and recall huge amounts of information in great detail. He could focus on any issue for very long periods of time without losing concentration; his keen intelligence and his shrewd grasp of the key issues of the day gave him a commanding air of authority. He was personally brave, to the point of a kind of fatalism (―the bullet has not yet been made that has my name on it‖); he had the ability to inspire others, and to drive them very hard. He had great breadth of vision; huge self-belief; and considerable personal charm when necessary. Napoleon‘s agile mind was always turning things over, investigating the options, thinking of alternatives. He had a mind like a filing cabinet, but he also used some important tools to help his memory. He used a system of record books of key governmental and military information, constantly updated by clerks and all presented in precisely the same format. The internal organization of these books could not be changed without Napoleon‘s agreement; he knew exactly where he could find the information that he wanted. He described his own mind as being like a cabinet, with information stored behind certain doors. If he wanted to think about a certain topic, he opened the relevant drawer in his mind – and there it was. When he wanted to sleep, he closed all of the

doors and he slept. This astonishing mental resource meant that Napoleon was able to plan, not only in broad brush strokes, but in detail. When he conceived of a grand plan, he also supplied the logistics to deliver that plan, down to the last detail. Napoleons astonishing victories owed little to luck (though there is always fortune in battle, both good and bad). His victories – his success in many fields – owed almost everything to his meticulous planning.

3.5 Leading from the front

Nothing is more impressive in a manager than to lead from affront. This can take many forms, the most obvious of which is the ―traditional tarnished golden rule concept‖ of not asking anybody else to do what you wouldn‘t do yourself – of exposing yourself to danger along with your troops (Topel, 1998).. The military analogy is not so far-fetched: it is inspiring when a manager picks up the phone to talk to a key client if there is a problem; when they step in to mediate a dispute; when they stick their neck out to make the case to senior management for the needs of their own team or division; when they take on a difficult interview with the media; when they are seen to be out and about promoting the organization to the outside world.

3.5.1 Horatio Nelson (1758–1805)

point where they began to think like him – to the extent that, in a sudden, unplanned engagement, they could be hoped to react exactly as he would himself. Like any great leader, Nelson had much strength. Perhaps his most defining characteristic, one which he demonstrated throughout his career, was his outstanding personal bravery and his habit of leading from the front. Nelson was always in thick of it. He had lost an arm and an eye on separate occasions leading attacks on the enemy on shore. He never asked his crew to do anything that he would not do himself and, as a result, he could be certain that they would follow him.

3.6 Bringing people with you

Bringing people with you is not one skill, but a set of skills. Some managers bring people with them because they are good speakers. They may or may not be good at motivating people face to face, but if you put them on a podium, or behind a microphone, then they are able to inspire an audience to follow them to the ends of the earth. Others achieve the same ends, more painstakingly, through their actions. They keep on doing the right thing, consistently, until people can see the intention that runs through their actions. In the wider context within which an organization works, managers must also try to bring along their various constituencies – customers and suppliers; the local community; the media; the industry – without them having bought into the plan in the same way. These constituencies may be brought with you by a combination of factors, including appeals to self-interest and common self-interest. They may come with you, but only because there is something in it for them.

3.6.1 George Washington (1732–1799)

George Washington, the first President of the United States, led the revolutionary army that was to defeat the British Empire, and turned the 13 east-coast colonies – from Massachusetts and New Hampshire in the north to South Carolina and Georgia in the south – into the 13 ―United States‖ of America (Ellis, 2005). A man of commanding personal presence, Washington came to personify the struggle against the British. As commander-in-chief of the Continental Army, as it was known, he fought a dogged war for eight long years, suffering some heavy defeats but also some occasional victories of great psychological significance. Washington seemed to hold his army together by sheer willpower and force of personality. Washington at first declined a salary ($25,000 per annum) on the grounds that his was a public service that should not be rewarded, but then accepted the salary so that the future presidency should not become a rich man‘s preserve. He opposed the idea of party politics. He reluctantly accepted the second term of office to which he was elected in 1792, and then

refused a third, establishing the practice that would become law when the 22nd amendment was passed in 1947.

3.7 Making things happen

One of the most basic things that a manager has to do is to make things happen. As a junior manager, even a middle manager, it will do you no harm at all to be seen rolling up your sleeves and sorting out whatever mess you may have inherited: whether it be completely revamping the training program, overhauling the bonus system.

3.7.1 George S. Patton (1885–1945)

Patton once said, “―I don‘t want to get any messages saying, ‗I am holding my position.‘ We‘re not holding a goddamned thing. We are advancing constantly and we are not interested in holding onto anything, except the enemy's balls. We are going to twist his balls and kick the living shit out of him all of the time. Our basic plan of operation is to advance and to keep on advancing regardless of whether we have to go over, under, or through the enemy. We are going to go through him like crap through a goose; like shit through a tin horn! From time to time there will be some complaints that we are pushing our people too hard. I don‘t give a good goddamn about such complaints. I believe in the old and sound rule that an ounce of sweat will save a gallon of blood. The harder we push, the more Germans we will kill. The more Germans we kill, the fewer of our men will be killed. Pushing means fewer casualties. I want you all to remember that‖ (Forty, 1996). George S. Patton was in command of the US Third Army in the lead-up to the Allied invasion of northern Europe in 1944, as the final effort to defeat Nazi Germany got under way. Patton believed above all things in training and discipline, in being prepared to meet the enemy. ―If men do not obey orders in small things, they are incapable of being led in battle. I will have discipline – to do otherwise is to commit murder.‖62 Patton trained his men hard and insisted on tight discipline: sloppiness, lack of alertness, and waiting in foxholes for the enemy to come to you – these were what got you killed.

3.8 Creating opportunities

use of their individual skills and playing at the top of their game, then opportunities start, as if by magic, to appear. The individual skills of one player create the opportunity for the next player. The cumulative effect of a number of small opportunities suddenly becomes one big opportunity. A coach can set out the general strategy for a team like this, and encourage them to play a certain sort of game, but even the best coach cannot plan for the precise opportunity that will win the game. Opportunities can be created in many ways. Building the right team is essential: highly talented individuals will bring opportunities to a manager‘s doorstep. Developing a really outstanding marketing idea can do the same thing: suddenly a particular image or a slogan incorporates the organization‘s goals so well that other things start to fall into place; apparently unrelated bits of activity suddenly make more sense from this new perspective; different departments suddenly come up with new ideas that fit neatly into the new perspective. Entering a new market or entering a market at a particularly well-judged time can do the same thing: suddenly opportunities are falling at a team‘s feet.

4 Conclusion

Ancient leaders with Strategic Intelligence moved their followers to become willing collaborators. These collaborators tended to feel that they were participating in the creation of their relationship to their work. Erich Fromm (1947) emphasizes the connection between productive work and happiness. Effective leaders provided the opportunity for people to connect their work to their values. To do this they worked with both intellectual and emotional issues, knowledge of both the head and the heart. It took both head and heart to develop a philosophy of leadership and a philosophy of life. In short, it took leadership Intelligence to become a leader who is needed to win.

References

1. Andrews, A. (1988). Management of change requires

leaders with boldness and vision. Human Resource

Management, 4(4), 12-15.

2. Bruner, E. M. (1994). Abraham Lincoln as authentic

reproduction: A critique of postmodernism. American

Anthropologist, 96(2), 397-415.

3. Ellis, J. J. (2005). His Excellency: George

Washington. Vintage.

4. Ngunjiri, F. W., Hernandez, K. A. C., & Chang, H.

(2010). Living autoethnography: Connecting life and

research. Journal of Research Practice,6(1), 1.

5. Ellis, C., Adams, T. E., & Bochner, A. P. (2011).

Autoethnography: an overview. Historical Social

Research/Historische Sozialforschung, 273-290.

6. Forty, G. (1996). The Armies of George S. Patton.

Arms and Armour.

7. Gifford, J. (2010). 100 Great Leadership Ideas: From

successful leaders and managers around the world. Marshall Cavendish International Asia Pte Ltd. 8. Goleman, D. (2006). The socially

intelligent. Educational leadership, 64(1), 76-81.

9. Hesselbein, F., & Goldsmith, M. (2006). The leader of

the future 2. Soundview Executive Summaries, 28

(12).

10. Knight, R. J. B. (2005). The pursuit of victory: the life

and achievement of Horatio Nelson. Basic Books. 11. Maccoby, M. (2007). Narcissistic leaders. Boston:

Harvard Business School Press.

12. Mandela, N. (2008). Long walk to freedom: The

autobiography of Nelson Mandela. Little, Brown 13. Sanders, T. (2006). The likeability factor: How to

boost your L-Factor and achieve your life's dreams. Three Rivers Press (CA).

14. Semmel, S. (2004). Napoleon and the British. Yale

University Press.

15. Sternberg, R. J. (2003). Wisdom, intelligence, and creativity synthesized. Cambridge University Press.

16. Topel, J. (1998). The tarnished Golden Rule (Luke 6:

31): The inescapable radicalness of Christain

ethics. Theological Studies, 59(3), 475.

17. Webb, E. (1915). Character and intelligence: An attempt at an exact study of character. University Press.

ASYMMETRY BETWEEN THE COST OF MEDICAL

LITIGATIONS AND THE NUMBER OF MEDICAL

LITIGATIONS

Moshibudi J. Selatole*, Collins C. Ngwakwe*

Abstract

The impact that rising costs of litigations has had on many countries has seen society deprived of good quality health care and a substantial extra-expenditure in health budgets. The financial and societal costs of medical malpractice litigations have also been a growing cause for concern in the developing country of South Africa. This paper attempted to contribute to the knowledge of this problem in the South African setting by examining settlement costs of medical litigations in one province of the country over a 6 year period, and examining the relationship between these costs and the number of litigations. No correlation was found between the number of litigations and the costs of litigations, this indicates that, aside from the number of litigations, other factors are responsible for rising costs of litigation. The paper recommends that the department should continue monitoring the environmental costs of litigations for budgetary and management purposes; and the need to introduce an electronic integrated medical litigations reporting system, as well as tort reforms to curb the costs of the litigations. This work also calls for substantial further research in terms of what disciplines, what medical errors, and what circumstances greatly influence litigation outcomes.

Keywords: medical litigations, litigation costs, medical malpractice, environmental costs, tort reforms, medical costs

*Turfloop Graduate School of Leadership, Faculty of Management & Law, University of Limpopo, South Africa

Introduction

The recent years have seen the local press being inundated with reports of expanding litigation costs against the health care sector, particularly the private sector, corroborated by a medical indemnity insurance in South Africa, the Medical Protection Society (MPS). The public sector seems to be catching up, with large litigation pay-outs to individuals by the state being reported. South Africa‘s health system has for many years lagged behind developed countries, e.g. USA, in suffering a great deal of financial loss due to medical malpractice. These spiralling litigation cases have however, led many to believe South Africa is on the verge of a litigation storm.

In the context of the ongoing suboptimal economic climate, and the already ailing state of the public health care system, this added expanding extraordinary expenditure is of great financial and quality assurance concern. It is acknowledged that costs of litigations, which can be regarded as environmental costs, range from non-financial to financial, and include direct (compensation pay-out and legal fees) and indirect costs such as defensive medicine costs (Kessler et al., 2006), risk management expenses, and others (Mello et al., 2010).

In the light of the highlighted increasing litigation costs in South Africa (Seggie, 2013; Pepper and Slabbert, 2011), despite literature search and as far as the author is aware, no studies examining the cost of litigations against public health sector have been conducted. There are notions of unpredictability of the size of the settlement costs in relation to any litigation (Sohn & Bal, 2012), however the direct statistical determination of the relationship between the costs and the number of the litigations is hardly offered in the literature. Therefore, the objective of this is to examine whether any relationship exists between the costs and the number of litigations.

The paper is organised in the following manner: section 1 discusses related literature; section 2 summarises the research methodology; section 3 looks at data analysis and results and section 4 at the discussion of the results; lastly section 5 concludes and submits recommendations

1 Related literature

Cavitz, 2013,), the implications and consequences (Seggie, 2013; Medical Chronicle, 2012; Baker, 2011; Kessler, 2014), as well as factors that may help mitigate risks against litigations (Boothman et al, 2009; Medical Protection Society, 2011; Berlinger, 2007; Mazor et al., 2004). Pepper and Slabbert (2011) made recommendations by suggesting ways that may assist to dampen the rate at which society sues the health institutions, and the manner in which pay-outs are made, citing several studies that also looked at legal reforms pertaining to litigations. Several papers have looked at the specific disciplines in the eye of the storm: the field of obstetrics and gynaecology and surgery (Alsaadique, 2004; Jenna, 2011; East and Snyckers, 2011; Matsaseng and Moodley, 2005), as well as medical conditions that carry high risks (Vukmir, 2008). Locally, one just has to look at local newspapers to see what litigation is costing the South African government (City Press, 2013).

Rising medical litigation costs is not unique to South Africa; Phillips et al. (2004) cite that in 2000 there were just over 16 000 paid claims against [private] medical healthcare providers in the United States of America with total payments of nearly $4 billion. Roberts and Hoch (2009) examined the relationship between medical malpractice litigations and medical costs in the USA and found them to be positively and significantly related, with estimates indicating that malpractice litigation costs account for 2%-10% of medical expenditures. Mello et al. (2010) estimated that the USA medical liability system costs, including defensive medicine costs, amounted to 55.6 billion dollars, and 2.4% of the US total health care spending. In 1999 the NHS Litigation Authority in England closed 3 254 claims at a cost of £386 million. In 2004, Finland incurred total costs of paid compensation of €24.2 million under their no-fault compensation system, with 88% of the claims arising against their public health and 12% from the private sector (Hirvensalo, 2006).

Explanatory factors included technological advances (that are expensive) and improved life expectancy, which meant increased cost of care (Bown, 2012); the medical discipline involved (McAbee et al., 2008); the severity of the disability (cited in Bhatt et al., 2013); as well as legal mechanisms of managing litigations in a country (Hambali & Khodapanahandeh, 2014; Sohn & Bal, 2012), leading to the notion of unpredictability in the

payment size related to any litigation. This has resulted in high medical indemnity insurance premiums (Medical Chronicle, 2012) and a general impediment of patient access to quality healthcare because of practitioners neglecting risky fields (Cline & Pepine, 2004). However following placing a cap on compensation of medical litigations (one tort reform model), some US states saw a decline in defensive medicine costs and a remarkable return of medical practitioners who had left and a reduction in medical malpractice indemnity insurance, as well as a better distribution of funds between lawyers and their plaintiff clients (Legant, 2006).

2 Method, analysis and results

This study is a quantitative survey of all medical litigation cases from all districts of a province in South Africa between the financial years 2008/2009 – 2013/2014. The research applied purposive sampling to target only those litigations brought for the 6 years, in order to give an estimate of the amount of expenditure from litigations for that period. The total sample was comprised of 372 cases. Data were collected from the department of health and treasury records. Approval was granted for access only to details of the closed (settled litigations).

The number of all the litigation cases and the costs of all the settled cases year by year, as well as annual budgets and expenditures of the department of health over the 6 year period were recorded. Data were analysed by descriptive statistical and correlation analysis using a Microsoft Excel electronic spreadsheet and the SPSS software.

The main objective is to ascertain possible correlation between cost of litigation and the number of litigation; furthermore, the analysis also examined possible relationship between the number of lost litigations and the settlement costs (cost of litigations). This is with a view to determining if other causative factors may (aside from number of litigations), contribute to the rising cost of litigation. The correlation analysis showed that there is no relationship between the number of the total litigations and the settlement costs of the litigations. Neither is there any relationship between lost litigations and the settlement costs of the litigations.

The analyses are shown in tables 1 – 4 and Figures 2 - 3.

Table 1. Parametric Correlations (Number of Litigation and Cost of Litigation)

No.of.Litigation Cost.of.Litigation

No.of.Litigation Pearson Correlation 1 -.074

Sig. (2-tailed) .890

N 6 6

Cost.of.Litigation Pearson Correlation -.074 1

Sig. (2-tailed) .890

Table 2. Nonparametric Correlations (Number of Litigation and Cost of Litigation)

No.of.Litigation Cost.of.Litigation Kendall's tau_b No.of.Litigation Correlation Coefficient 1.000 .000

Sig. (2-tailed) . 1.000

N 6 6

Cost.of.Litigation Correlation Coefficient .000 1.000

Sig. (2-tailed) 1.000 .

N 6 6

Spearman's rho No.of.Litigation Correlation Coefficient 1.000 -.116

Sig. (2-tailed) . .827

N 6 6

Cost.of.Litigation Correlation Coefficient -.116 1.000

Sig. (2-tailed) .827 .

N 6 6

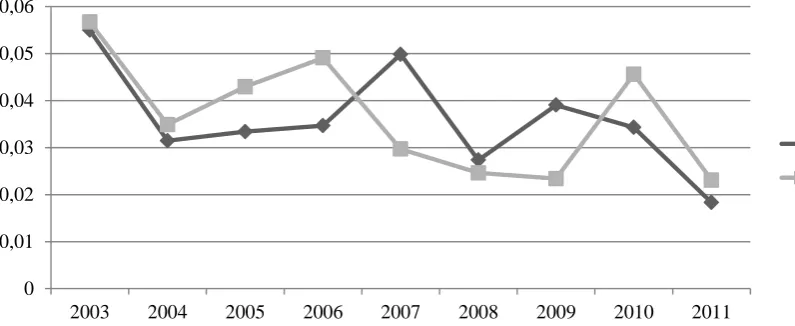

Figure 1. Number of Litigation and Cost of Litigation

Table 3. Parametric Correlations (Lost Litigation and Cost of Litigation)

No.of.Lost.Litigation Cost.of.Litigation

No.of.Lost.Litigation Pearson Correlation 1 .715

Sig. (2-tailed) .110

N 6 6

Cost.of.Litigation Pearson Correlation .715 1

Sig. (2-tailed) .110

Table 4. Nonparametric Correlations (Lost Litigation and Cost of Litigation)

No.of.Lost.Litigation Cost.of.Litigation Kendall's tau_b No.of.Lost.Litigation Correlation Coefficient 1.000 .414

Sig. (2-tailed) . .251

N 6 6

Cost.of.Litigation Correlation Coefficient .414 1.000

Sig. (2-tailed) .251 .

N 6 6

Spearman's rho No.of.Lost.Litigation Correlation Coefficient 1.000 .551

Sig. (2-tailed) . .257

N 6 6

Cost.of.Litigation Correlation Coefficient .551 1.000

Sig. (2-tailed) .257 .

N 6 6

Figure 2. Lost Litigation and Cost of Litigation

3 Discussion of results and findings

The study found that over the 6-year period, the department an average of 0.06% of the total expenditures in the department in litigation settlement costs. This is way less than the amounts reported to have been paid in other provinces (City Press, 2013), and certainly a drop in the ocean compared to the billions of dollars and hundreds of millions of pounds paid out in medical litigations in the US and UK respectively. Mello et al. (2010) and Roberts & Hoch (2009) reported that in the US, costs of litigations, although including some other costs other than settlement costs, amounted to 2%-10% of health expenditure. Monitoring these costs of litigation (environmental contingency costs) has implications for future healthcare budgeting wherein it can be

noted that less than 0.5% can be budgeted for medical litigation risk.

According to the Public Finance Management Act of the country, these costs, although they will have to be budgeted for in the medium and long term, can be regarded as fruitless and wasteful expenditure. This refers to expenditure that could have been avoided had reasonable care been exercised (South Africa, 1999).

a significant role in the rising cost of medical litigation.

This finding supports literature findings that other issues are at play in terms of the rapidly rising costs of litigations. The type of case involved plays a significant role. It has been stated that certain medical disciplines such as obstetrics and paediatrics attract very high litigation settlement costs. Within these disciplines there are certain types of errors or error outcomes or severity of disability (Bhatt et al., 2013), such as obstetric errors giving rise to cerebral palsy in the child, that attract high costs. This study did not involve looking at which disciplines and what kind of errors were involved, however this is likely to have been the case.

As inflation increases and cost of living, particularly cost of health care and equipment, has become too high, so must have litigation settlement costs. The traditional system of dealing with medical litigation in South Africa must also have played a role, assuming that there is currently competence of legal representatives and judges on medico-legal issues. Some countries that have reformed their legal Tort systems are able to put caps on the settlement cost, thus reducing these costs (Sohn & Bal, 2012). However, the implication of the lack of relationship between lost litigations and the settlement amounts is that every case will still need to be scrutinised and decided on its merit, and tort reforms such as a no-fault system may not be applicable to all cases.

4 Conclusions and recommendations

The impact that rising costs of medical litigations has had on many countries has seen society being deprived of good quality health care and a substantial extra-expenditure in health care budgets. In an attempt to address this problem, calls have been made to put emphasis on patient safety, and most rigorously on law reforms to reduce costs and to encourage the notion that best medical care is not substantiated by a lack of medical errors. It is ironical that patients may not be patient anymore; it is also a reality that medical errors will occur, and that only where it is warranted compensation should be paid out to the injured.

The financial and societal costs of medical malpractice litigations are also a growing cause for concern in the developing country of South Africa faced with deteriorating economic conditions and an ailing public health care sector. This study attempted to contribute to the knowledge of this problem in the South African setting by investigating this phenomenon in one province of the country. Although there were some limitations in terms of data completeness, estimations were still made possible.

Litigations expenditures for the province amounted to an average of 0.06% of the department‘s expenditure over the 6 year period. It may not be a storm yet, but the province is definitely experiencing turbulence in terms of medical litigations. Of special

interest, no correlation or relationship was found between the number of litigations and the cost of litigations using the correlation analysis, implying that the type of the claim involved, amongst a few other factors, may be of paramount importance.

The study submits the following recommendations: In accordance with activity based costing accounting framework, the societal costs of litigations need to be closely monitored and allocated accordingly. To facilitate knowledge dissemination and learning, access to closed litigation cases and outcomes should be readily available to healthcare institutions and practitioners through an integrated database system at the medical professions governing body, the HPCSA. The state should look into tort reforms such as putting caps on settlement costs. This work also calls for substantial further research in terms of what disciplines, what medical errors, and what circumstances greatly influence relational and litigation outcomes. To paint a clearer picture of South Africa, research need to be undertaken in all the provinces of the country.

References

1. Alsaadique, A., 2004. Medical liability: The dilemma of litigations. Saudi Medical Journal, 25(7), pp. 901-906.

2. Baker, T., 2011. The Medical Malpractice Myth (Large Print 16pt). [Online]. Chicago: University of Chicago. Available at: http://www.readhowyouwant.com . [Accessed: 19th March 2014].

3. Berlinger, N., 2007. After Harm: Medical Error and the Ethics of Forgiveness. Baltimore: John Hopkins University Press.

4. Bhatt, A., Safdar, A., Chaudhari, D., Clark, D., Pollak, A., Majid, A. & Kassab, M., 2013. Medicolegal considerations with intravenous tissue plasminogen activator in stroke: A systematic review. Stroke Research and Treatment [Online] Available at: http://dx.doi.org/10.1155/2013/562564. [Accessed: 30th June 2014].

5. Boothman, R. N., Blackwell, A. C., Campbell, D. A. Jnr., Commiskey, E. & Anderson S., 2009. A better approach to medical malpractice claims? The University of Michigan experience. Journal of Health and Life Sciences Law, 2(2), pp. 125-159.

6. Bown, S., 2012. Counting the litigation cost. MPS Casebook, 20(1), pp. 9-11.

7. Cavitz, A., 2013. Medical Malpractice: Liberty Exists In Proportion To Wholesome Restraint. [Online] Available at: http://www.josephs.co.za. [Accessed: 19th March 2014].

8. City Press Newspaper., 2014. [Online] Available at: http://www.citypress.co.za/news. [Accessed: 19th February 2014].

11. Hambali, S. N. &. Khodapanahandeh, S., 2014. A review of medical malpractice issues in Malaysia under Tort litigation system. Global Journal Of Health Science, 6(4), pp. 76-83.

12. Hamasaki, T., Takehara, T. and Hagehara, A., 2008. Physicians‘ communication skills with patients and legal liability in decided medical malpractice litigation cases in Japan. BMC Family Practice. [Online] 9(1). Available at: http://www.biomedcentral.com/1471-2296/9/43. [Accessed: 26th March 2014].

13. Hirvensalo, E., 2006. Legislation covering medical malpractice in Finland. Journal of Bone & Joint Surgery, British Volume, 88(Supp I), pp. 13-14. 14. Holohan, T. V., Colestro, J., Grippi, J., Converse, J. &

Hughes, M., 2005. Analysis of diagnostic error in paid malpractice claims with substandard care in a large health care system. Southern Medical Journal, 98(11), pp.1083-1087.

15. Je