Refer to Important disclosures in the last page of this report

Stock DataTarget price (Rp) Rp3,500

Prior TP (Rp) n.a.

Shareprice (Rp) Rp3,050

Upside/downside (%) +14.8

Sharesoutstanding (m) 10,688 Marketcap. (US$ m) 2,258

Axiata Investments (Indonesia) Sdn.

Bhd. 66.4%

PT Indo Premier Sekuritas [email protected] +62 21 5793 1168

Pursuing growth in outer Java

More optimism on healthier industry competition.

4G expansion in outer Java to drive growth.

Lowest risk from voice and SMS decline among Big 3 Telcos.

Re-initiate with TP Rp3,500 – BUY, 10% discount to 7-yr mean.

Outer Java = Key to further growth.

XL plans to invest c.55% of 2018 capex

in outer Java to reach 4G coverage of 85% of Indonesia’s population by end of

1H19 (vs. currently 65-70%), esp. in Kalimantan, Sumatra, and Sulawesi. We

view this as positive strategy as it will enable XL to grab opportunity from rising

smartphone penetration in outer Java. We expect stable EBITDA margin during

expansion phase to outer Java (2018F/19F at 37%) and then to slightly expand

gradually thereafter. For comparison, XL’s normalized EBITDA margin was 41% in

4Q17, post-acquisition of Axis.

Better data pricing in 2H18F to aid performance.

XL said it has raised data

pricing for certain Axis data packages in May and for XL packages before Lebaran

2018. XL also mentioned its intention to gradually improve data pricing further

after Lebaran based on market’s response. Therefore, we expect revenue growth

to accelerate to +7%YoY in 2019F from flat YoY in 2018F (2H18F +6%HoH),

slightly outpacing our est. for Telkomsel at -2%YoY,

due to short-term pressure of

SIM Card re-registration and relatively competitive 1H18 vs. 2H18F.

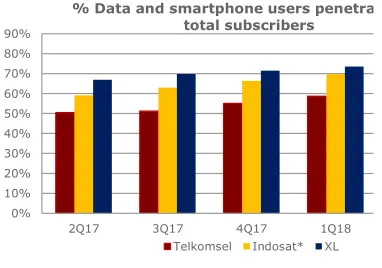

Potential opportunity from subscribers’ transition to data.

We think XL

might get slightly better chance to penetrate outer Java in data service compared

to voice and SMS considering that interconnection cost does not apply in data and

less dependency to one mobile phone number to use data. Furthermore, XL also

benefited from being a more data-centric company (based on data user

penetration and data revenue contribution as shown in Figure 1-2) among Big 3

Telcos. We expect 2018F/19F strong data traffic growth of 76/69%YoY (vs.

Telkomsel 77/49%YoY) and increase in mobile data revenue contribution to

68/76% (above Telkomsel 48/56%).

Re-initiate at BUY with TP of Rp3,500.

We rolled over our valuation to 2019.

Our DCF-based TP assumed WACC of 12.5% (Fig 8). Our target 2019 EV/EBITDA

for XL is 5.5x, 10% discount to 7-year mean and 25% discount to TLKM (adj. for

% ownership in Telkomsel). XL trades at 2019EV/EBITDA of 5x, at -1STD below

its 7-yr mean and 32% discount to TLKM. We expect XL to achieve core profit

breakeven when its outer Java expansion makes its full-year impact in 2020. Our

TP translates to 2020EV/EBITDA of 5x, similar to EXCL’s -1STD below 7-yr mean.

Downside risk: Time lag until more certainty in growth outlook after tightening of

starter pack registration.

Source: EXCL, IndoPremier Share Price Closing as of :8-August-2018

2

Refer to Important disclosures in the last page of this report

Fig. 1: Big 3 Telcos’ Data and smartphone portion of total subs.

Fig. 2: Big 3 Telcos’ Data revenue portion to total revenue

0%

% Data and smartphone users penetra total subscribers

Telkomsel Indosat* XL

*) 2Q18 smartphone and data user penetration of Telkomsel and XL were 63% and 77% respectively.

2Q17 3Q17 4Q17 1Q18 2Q18

Data contribution to total net-revenue

Telkomsel* Indosat** XL

*) Telkomsel’s data revenue contribution to total Telkomsel’s revenue

Source: Companies, IndoPremier Source: Companies, IndoPremier

Fig. 3: XL’s data revenue and effective yield Fig. 4: XL fw-hist. EV/EBITDA (3 Aug Jul 2018: 4.5x)

0

Data revenue (LHS) Effective yield (RHS)

3

Fw-EV/EBITDA Fw-EV/EBITDA avg Fw-EV/EBITDA + 1 STD Fw-EV/EBITDA -1 STD Fw-EV/EBITDA - 2 STD Fw-EV/EBITDA + 2 STD

-2STD 4.0 -1STD 5.1 Avg 6.1 +1STD 7.2 +2STD 8.3

3

Refer to Important disclosures in the last page of this report

Fig. 5: Xtream smartphone package*Type

*) Terms and Conditions Applied

**) All with RAM 1GB / ROM 8GB specification.

***) FUP (Fair Usage Policy) 5GB/day according to Tribun News. Different FUP might apply in different area and/or time of observation. ^ (Smartphone price/12month + monthly top up Rp 25K) / (30x 5GB + 1GB)

Note:

Evercoss previously (Apr 2018) said the result was above expectation as three weeks after launched, Xtream 1 and 1 Plus (sales) reached 50K units (mostly reached via Evercoss channel), 2.5x initial target of 20K units. Evercoss targets Oct’18 sales volume for those 2 series at 300K units.

Source: Company, IndoPremier, Merdeka.com, Tribun News

Strategy to grow early adopter of 4G

XL’s “Xtream” smartphone bundled package is resulted from cooperation between

XL, “Evercoss” (smartphone brand), and YouTube. This bundled package (requires

monthly top-up for 1 year) was launched in Apr 2018. The cheapest smartphone

package priced Rp669K (c.16% of avg. monthly 2017 GDP per capita).

Based on the XL’s product description, Xtream smartphone is available in stores

and 6 popular e-commerce channels: Tokopedia, Lazada, Bukalapak, Blibli,

MatahariMall, and Shopee. We found cheaper price for Xtream 1 in one of sellers in

BukaLapak e-commerce (c. 16% cheaper than price mentioned in Figure 5) which

also allows 0% instalment for 12 month at Rp47K/month, relatively affordable

enough to trigger wider penetration of 4G users in Indonesia, in our view.

4

Refer to Important disclosures in the last page of this report

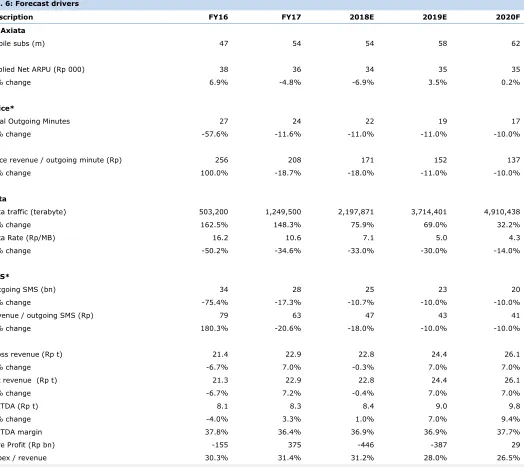

Fig. 6: Forecast driversDescription FY16 FY17 2018E 2019E 2020F

XL Axiata

Mobile subs (m) 47 54 54 58 62

Implied Net ARPU (Rp 000) 38 36 34 35 35

% change 6.9% -4.8% -6.9% 3.5% 0.2%

Voice*

Total Outgoing Minutes 27 24 22 19 17

% change -57.6% -11.6% -11.0% -11.0% -10.0%

Voice revenue / outgoing minute (Rp) 256 208 171 152 137

% change 100.0% -18.7% -18.0% -11.0% -10.0%

Data

Data traffic (terabyte) 503,200 1,249,500 2,197,871 3,714,401 4,910,438

% change 162.5% 148.3% 75.9% 69.0% 32.2%

Data Rate (Rp/MB) 16.2 10.6 7.1 5.0 4.3

% change -50.2% -34.6% -33.0% -30.0% -14.0%

SMS*

Outgoing SMS (bn) 34 28 25 23 20

% change -75.4% -17.3% -10.7% -10.0% -10.0%

Revenue / outgoing SMS (Rp) 79 63 47 43 41

% change 180.3% -20.6% -18.0% -10.0% -10.0%

Gross revenue (Rp t) 21.4 22.9 22.8 24.4 26.1

% change -6.7% 7.0% -0.3% 7.0% 7.0%

Net revenue (Rp t) 21.3 22.9 22.8 24.4 26.1

% change -6.7% 7.2% -0.4% 7.0% 7.0%

EBITDA (Rp t) 8.1 8.3 8.4 9.0 9.8

% change -4.0% 3.3% 1.0% 7.0% 9.4%

EBITDA margin 37.8% 36.4% 36.9% 36.9% 37.7%

Core Profit (Rp bn) -155 375 -446 -387 29

Capex / revenue 30.3% 31.4% 31.2% 28.0% 26.5%

*) Voice and SMS figures are estimate. Starting 2Q16, voice and SMS traffic were not disclosed by company. **) Our 2H18F effective data yield is Rp6.8/MB (lower than 1H17 Rp7.5/MB, but similar to 2Q18).

5

Refer to Important disclosures in the last page of this report

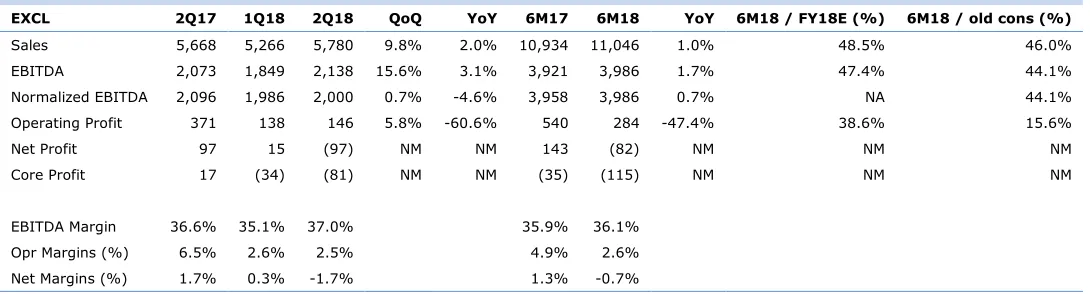

Fig. 7: 2Q18 resultsEXCL 2Q17 1Q18 2Q18 QoQ YoY 6M17 6M18 YoY 6M18 / FY18E (%) 6M18 / old cons (%)

Fig. 8: Risk-free-rate and terminal EV/EBITDA assumption

Risk-Free rate 7.5%

Equity market risk premium 6.0%

Beta 1.3 2-year Beta

Cost of equity 15.4%

Post-tax cost of debt 7.9%

Debt/Capital ratio 38%

WACC 12.5%

Terminal EV/EBITDA 5.6

Source: Company, IndoPremier, Bloomberg

Potential acceleration in long-term EBITDA growth.

There might be short-term pressure in share price as we conservatively estimate

2018/19 EBITDA at below cons. However, we assume investors will eventually

focus on higher EBITDA growth trajectory in the future from: 1) Growing data

demand in Indonesia; 2) Lower uncertainties post-SIM card registration; 3) Growth

opportunity in outer Java. Moreover, consensus’ est. might be less dependable for

now considering relatively substantial variance between cons’ 18F/19F EBITDA low

end (14/23% above) to high end.

Risks

Upside risk:

Stronger than expected data demand, faster than expected return

from investment in data network (and/or core profit turnaround), significantly

stronger trend in Rupiah vs. USD, further potential upside considering XL’s highest

share price last year (before market gradually pricing in intense price competition

in 3Q17 and SIM card registration) was Rp4,020, c.32% above current share price.

Downside risk

: Short-term forex risk, unsustainable improvement in data yield.

XL’s USD debt accounted 31% of total debt as of 2Q18, with maturity in 2019. The

company hedged USD debt (for principal) at c.Rp14.6k/USD based on 2Q18

disclosure.

6

Refer to Important disclosures in the last page of this report

Year To 31 Dec (RpBn) 2016A 2017A 2018F 2019F 2020F

Income Statement

Net Revenue 21,341 22,876 22,778 24,372 26,084

Cost of Sales 0 0 0 0 0

Gross Profit 21,341 22,876 22,778 24,372 26,084 SG&A Expenses (21,329) (21,505) (22,042) (23,488) (24,777) Operating Profit 12 1,370 735 883 1,308 Net Interest (1,533) (1,295) (1,330) (1,399) (1,270) Forex Gain (Loss) 351 (30) 0 0 0 Others-Net 1,355 176 587 587 457 Pre-Tax Income 186 221 (8) 71 495

Income Tax 190 154 2 (18) (124)

Minorities 0 0 0 0 0

Net Income 375 375 (6) 53 371

Balance Sheet

Cash & Equivalent 1,400 2,455 1,068 1,245 1,341

Receivable 663 809 802 865 913

Inventory 161 143 157 164 173

Other Current Assets 4,583 3,773 4,305 4,451 4,733 Total Current Assets 6,807 7,181 6,332 6,726 7,160

Fixed Assets - Net 33,183 34,934 33,315 30,914 28,211 Goodwill 6,681 6,681 6,681 6,681 6,681 Non Current Assets 8,056 7,525 8,541 9,473 9,568 Total Assets 54,896 56,321 54,869 53,795 51,621

ST Loans 0 0 0 0 0

Payable 6,503 7,476 0 7,695 8,236

Other Payables 4,329 3,979 3,244 2,939 3,109 Current Portion of LT Loans 3,645 3,771 4,140 4,575 0

Total Current Liab. 14,477 15,227 14,576 15,210 11,345

Long Term Loans 11,026 10,980 10,238 8,663 9,863 Other LT Liab. 8,184 8,484 8,431 8,129 8,259 Total Liabilities 33,687 34,691 33,245 32,001 29,467

Equity 13,208 13,226 13,226 13,226 13,226 Retained Earnings 8,002 8,405 8,399 8,568 8,927

Minority Interest 0 0 0 0 0

Total SHE + Minority Int. 21,209 21,631 21,625 21,794 22,153 Total Liabilities & Equity 54,896 56,321 54,869 53,795 51,621

7

Refer to Important disclosures in the last page of this report

Year to 31 Dec 2016A 2017A 2018F 2019F 2020F

Cash Flow

Net Income (Excl.Extraordinary&Min.Int) 375 375 (6) 53 371

Depr. & Amortization 7,064 6,167 6,871 7,298 7,637 Changes in Working Capital 1,178 1,147 (503) 363 312

Others 868 833 1,265 552 990

Cash Flow From Operating 9,486 8,522 7,626 8,266 9,309 Capital Expenditure (6,401) (7,387) (6,267) (5,829) (5,029)

Others 201 413 189 81 94

Cash Flow From Investing (6,200) (6,974) (6,078) (5,748) (4,935) Loans (5,385) 80 (373) (1,140) (3,375)

Equity 6,721 18 0 0 0

Dividends 0 0 0 116 (11)

Others (6,251) (1,119) (1,760) (1,816) (1,344) Cash Flow From Financing (4,915) (1,021) (2,134) (2,840) (4,730) Changes in Cash (1,630) 527 (585) (322) (355)

Financial Ratios

Gross Margin (%) 100.0 100.0 100.0 100.0 100.0 Operating Margin (%) 0.1 6.0 3.2 3.6 5.0 Pre-Tax Margin (%) 0.9 1.0 0.0 0.3 1.9

Net Margin (%) 1.8 1.6 0.0 0.2 1.4

ROA (%) 0.7 0.7 0.0 0.1 0.7

ROE (%) 2.1 1.8 0.0 0.2 1.7

ROIC (%) 1.8 1.7 0.5 0.4 1.4

Acct. Receivables TO (days) 13.5 10.3 10.4 10.3 10.2 Acct. Receivables - Other TO (days) 3.1 2.8 2.5 2.2 2.3 Inventory TO (days) 0.0 0.0 0.0 0.0 0.0 Payable TO (days) 0.0 0.0 0.0 0.0 0.0 Acct. Payables - Other TO (days) 0.0 0.0 0.0 0.0 0.0

Debt to Equity (%) 69.2 68.2 66.5 60.7 44.5 Interest Coverage Ratio (x) 147.0 1.1 2.1 1.7 1.0 Net Gearing (%) 62.6 56.8 61.5 55.0 38.5

Head Office

PT INDO PREMIER SEKURITAS

Wisma GKBI 7/F Suite 718

Jl. Jend. Sudirman No.28

Jakarta 10210 - Indonesia

p +62.21.5793.1168

f +62.21.5793.1167

INVESTMENT RATINGS

BUY : Expected total return of 10% or more within a 12-month period

HOLD : Expected total return between -10% and 10% within a 12-month period

SELL : Expected total return of -10% or worse within a 12-month period

ANALYSTS CERTIFICATION.

The views expressed in this research report accurately reflect the analysts personal views about any and all of the subject securities or issuers; and no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in the report.

DISCLAIMERS