Dengan Hormat,

Dengan mengucap Puji Syukur Kehadirat Tuhan

Yang Maha Esa, buku “Laporan Statistik

Asuransi Gempa Bumi Indonesia (LSAGBI)

Desember 2015” telah selesai disusun.

Penyusunan LSAGBI ini selaras dengan salah

satu Visi MAIPARK yaitu menjadi “Center Of

Excellence” dan sebagai upaya dalam

memberikan pelayanan yang terbaik bagi

Industri Asuransi Umum di Indonesia khususnya

mengenai statistik serta pengetahuan risiko

gempa bumi.

Sebagai salah satu publikasi rutin, LSAGBI ini

memuat hasil kajian risiko-risiko gempa bumi

terkait data

exposure

, premi nasional, jumlah

risiko dan perkembangan risiko gempa bumi. Di

dalam laporan ini kami juga menyajikan ulasan

aktuaria dan risiko

exposure

dari sudut pandang

asuransi gempa bumi

Dukungan dari seluruh perusahaan asuransi

umum sangat berarti bagi kami dalam upaya

pengembangan laporan statistik ini. Kami

menyadari kebutuhan penyempurnaan buku ini

sangat tinggi sehingga kritik maupun saran

sangat kami harapkan.

Akhir kata, semoga laporan ini dapat menjadi

referensi

yang

berkualitas

dan

dapat

memberikan manfaat tidak hanya bagi

perusahaan yang menangani asuransi gempa

bumi, namun juga bagi Industri Asuransi Umum

di Indonesia. Kami mohon maaf apabila masih

ditemukan kesalahan data dan informasi yang

disajikan dalam buku ini.

Dear Sir / Madam,

Our gratitude to God Almighty, the “Indonesian

Earthquake Insurance Statistic Report as at

December 2015” is ready to publish. This report

publication i

s aligned with MAIPARK’s vision,

which is to be a "Center of Excellence” and also

to provide the best service for the General

Insurance Industry in Indonesia, especially

statistic and earthquake risks knowledge.

As a regular publication, it contains earthquake

risks study related to the national Exposure,

premium, number of risks and development of

the earthquake risks management. We also

include actuarial and Exposure risks reviews

from earthquake insurance point of view.

Support from the General Insurance Industry

will be meaningful to us in order to improve this

Statistic Report. We realize the need for

improvement of this report is very high so that

critics and suggestions are appreciate.

Finally, we hope that this report could be used

as a qualified reference and will be beneficial for

all general insurance industries in Indonesia.

We apologize for any possible data and

information errorspresented in this report.

Hormat Kami,

Sincerely,

Hal.

Page

Kata pengantar………

...

……i

Daftar Isi

……….iii

Content……

..

……….i

Foreword………..iii

A.

Umum

………

1

B.

Struktur Pasar

……….2

C.

Premi Bruto dan

Exposure

……….2

D.

Jumlah Risiko

………..

3

E.

Incurred Claim

………...

..

6

F.

Ulasan Aktuaria: Pengaruh Deductible

pada Distribusi Frekuensi Klaim dan Besar

Klaim

………..

.13

G.

Ulasan Asuransi: Gempabumi yang

mengubah..

………

....22

A.

General

………...1

B.

Market Structure

………2

C.

Gross Premium and Exposure

………2

D.

Number of Risk

………..

3

E.

Incurred Claim

………

6

F.

Actuary Commentary:

The

Effect of

Deductibles on Claims Frequency and Claims

Severity Distributions

………

...13

G.

Insurance Commentary: Earthquake that

Change………..………

22

Distribusi

Exposure

Gempa Bumi Indonesia

per Provinsi,

Underwriting Year

2016, per 30

Juni 2016

………...

27

Distribusi Gempa Bumi Indonesia M > 5 dan

Claim Incurred

2016

………

28

Distribusi

Exposure

Gempa Bumi Indonesia

per Provinsi,

Underwriting Year

2015, per 30

Juni 2016, Distribusi Gempa Bumi Indonesia M

>

5

dan

Claim

Incurred

UY

2016

………...

.29

Indonesian Earthquake Exposure Distribution by

Province, Underwriting Year 2016, as at 30 June

2016

……….

27

Indonesian Earthquake Distribution M > 5 and

Claim Incurred 2016

………...

28

Indonesian Earthquake Exposure Distribution by

Province, Underwriting Year 2016, per 30 June

Tabel 2.5.

Exposure

Per Kelas Konstruksi...37

Table 2.1. Exposure By Cresta Zone ... 30

Table 2.2. Exposure By Occupation ... 32

Table 2.3. Exposure By Interest ... 34

Table 2.4. Exposure By Province

…………

...36

Table 2.5. Exposure By Class of Construction..37

Iktisar Statistik Asuransi Gempa Bumi

Indonesia Juni 2016

Statistic

Overview

of

Indonesian

Earthquake Insurance June 2016

Exposure

Asuransi Gempa Bumi

Indonesia

Indonesian Earthquake Insurance

Exposure

Peta

Map

Tabel 3.1. Premi Bruto Per Cresta Zone

……

.39

Tabel 3.2. Premi Bruto Per Okupasi

…………

41

Tabel 3.3. Premi Bruto Per

Interest………...

43

Tabel

3.4.

Premi

Bruto

Per

Provinsi

………...

...

…

45

Tabel 3.5. Premi Bruto Per Kelas Konstruksi

... 46

Table 3.1. Gross Premium by Cresta Zone

……39

Table 3.2. Gross Premium by Occupation...41

Table 3.3. Gross Premium by Interest...43

Table 3.4. Gross Premium by Province

……..…

45

Table 3.5. Gross Premium by Class of

Construction

………

46

Tabel 4.1. Jumlah Risiko Per Cresta

Zone

.. 48

Tabel 4.2. Jumlah Risiko Per Okupasi ... 50

Table 4.3. Jumlah Risiko Per Kelas Konstruksi

... 52

Table 4.4. Jumlah Risiko Per Provinsi...

...…

54

Table 4.1. Number of Risk By Cresta Zone ... 48

Table 4.2. Number of Risk By Occupation ... 50

Table 4.3. Number of Risk By Construction Class

………

...52

Table 4.4. Number of Risk By Province ...

….

54

Tabel 5.1. Frekuensi Klaim Per Cresta Zone.55

Tabel 5.2. Frekuensi Klaim Per Okupasi

……

57

Tabel 5.3. Frekuensi Klaim Per Provinsi

……

59

Tabel 5.4. Klaim Per Cresta Zone

………

60

Tabel 5.5. Klaim Per Okupasi

………..

62

Tabel 5.6. Klaim Per Provinsi

………..

64

Table 5.1. Claim Frequency By Cresta Zone

…..

55

Table 5.2. Claim Frequency By Occupation

……

57

Table 5.3. Claim Frequency By Province

………

59

Table 5.4. Claim By Cresta Zone

……….

60

Table 5.5. Claim By Occupation

………...

62

Table 5.6. Claim By Province

………..

64

Underwriting Year

2012 - 2016, Seluruh

Okupasi

……….

65

Underwriting Year

2016, Seluruh Okupasi

…

66

Underwriting Year

2015, Seluruh Okupasi

…

67

Underwriting Year

2014, Seluruh Okupasi

…

68

Underwriting Year

2013, Seluruh Okupasi

…

69

Underwriting Year

2012, Seluruh Okupasi

…

70

Underwriting

Year

2012

-

2016,

All

Occupation……….

.65

Underwriting Year 2016, All Occupation

……….

66

Underwriting Year 2015, All Occupation

……….

67

Underwriting Year 2014, All Occupation

……….

68

Underwriting Year 2013, All Occupation

………

69

Underwriting Year 2012, All Occupation

……….7

0

Premi Bruto Asuransi Gempa Bumi

Indonesia

Indonesian Earthquake Insurance Gross

premium

Jumlah Risiko Asuransi Gempa Bumi

Indonesia

Indonesian Earthquake Insurance Number

of Risk

Klaim Asuransi Gempa Bumi

Indonesia

Indonesian Earthquake Insurance Claim

Okupasi Agrikultural

……….

71

Okupasi Komersial

………..

72

Okupasi Industrial

………

73

Okupasi Residensial

………

74

Occupation Agricultural

……….

71

Occupation Commercial

………...

72

Occupation Industrial

………

73

Occupation Residential

……….

74

Okupasi Agrikultural

……….

75

Okupasi Komersial

………..

76

Okupasi Industrial

………

77

Okupasi Residensial

………

78

Occupation Agricultural

……….

75

Occupation Commercial

………...

76

Occupation Industrial

………

77

Occupation Residential

……….

78

Okupasi Agrikultural

……….

79

Okupasi Komersial

………..

80

Okupasi Industrial

………8

1

Okupasi Residensial

………8

2

Occupation Agricultural

……….

79

Occupation Commercial

………...

80

Occupation Industrial

………8

1

Occupation Residential

……….82

Okupasi Agrikultural

……….

83

Okupasi Komersial

………..

84

Okupasi Industrial

………

85

Okupasi Residensial

……….………..

86

Occupation Agricultural

……….

83

Occupation Commercial

………...

84

Occupation Industrial

………

85

Occupation Residential

………

86

Okupasi Agrikultural

……….

87

Okupasi Komersial

………...

...88

Okupasi Industrial

……….

89

Okupasi Residensial..

………...

..90

Occupation Agricultural

……….

87

Occupation Commercial

………

...88

Occupation Industrial

………89

Occupation Residential

……….9

0

Profil Risiko dan Klaim

Underwriting

Year

Per Okupasi 2016

Risk and Profile Claim Underwriting Year

2016 By Occupation

Profil Risiko dan Klaim

Underwriting

Year

Per Okupasi 2015

Risk and Profile Claim Underwriting Year

2015 By Occupation

Profil Risiko dan Klaim

Underwriting

Year

Per Okupasi 2014

Risk and Profile Claim Underwriting Year

2014 By Occupation

Profil Risiko dan Klaim

Underwriting

Year

Per Okupasi 2013

Risk and Profile Claim Underwriting Year

2013 By Occupation

Profil Risiko dan Klaim

Underwriting

Year

Per Okupasi 2012

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per

Cresta

Zone,

Underwriting

Year

2016

………91

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per

Cresta

Zone,

Underwriting

Year

2015

………9

2

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per

Cresta

Zone,

Underwriting

Year

2014

………93

Exposure

, Premi Bruto, Jumlah Risiko &

Klaim per Cresta Zone,

Underwriting Year

2013

………94

Exposure

, Premi Bruto, Jumlah Risiko &

Klaim per Cresta Zone,

Underwriting Year

2012

………95

Exposure, Gross Premium, Number of Risk &

Claim by Cresta Zone, Underwriting Year

2013

……….94

Exposure, Gross Premium, Number of Risk &

Claim by Cresta Zone, Underwriting Year

2012

………

.95

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per

Okupasi,

Underwriting

Year

2016

………96

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per

Okupasi,

Underwriting

Year

2015

………97

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per

Okupasi,

Underwriting

Year

2014

………98

Exposure

, Premi Bruto, Jumlah Risiko &

Klaim per Okupasi,

Underwriting Year

2013

………99

Exposure

, Premi Bruto, Jumlah Risiko &

Klaim per Okupasi,

Underwriting Year

2012

………..10

0

Exposure, Gross Premium, Number of Risk &

Claim by Occupation, Underwriting Year

2016

………

.96

Exposure, Gross Premium, Number of Risk &

Claim by Occupation, Underwriting Year

2015

………

.97

Exposure, Gross Premium, Number of Risk &

Claim by Occupation, Underwriting Year

2014

………

.98

Exposure, Gross Premium, Number of Risk &

Claim by Occupation, Underwriting Year

2013

………

.99

Exposure, Gross Premium, Number of Risk &

Claim by Occupation, Underwriting Year

2012

………10

0

Exposure,

Premi Bruto, Jumlah Risko

dan Klaim Asuransi Gempa Bumi

Indonesia Per Cresta Zone

Indonesian Earthquake Insurance Exposure,

Gross Premium, Number of Risk and Claim

By Cresta Zone

Exposure,

Premi Bruto, Jumlah Risko

dan Klaim Asuransi Gempa Bumi

Indonesia Per Okupasi

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi,

Underwriting Year

2016

…….. 10

1

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi,

Underwriting Year

2015

……...

102

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi,

Underwriting Year

2014

……...

103

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi,

Underwriting Year

2013

………

104

Exposure

, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi,

Underwriting Year

2012

………105

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per

Provinsi,

Underwriting

Year

2016

………..

101

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi, Underwriting Year 2015

………...10

2

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi, Underwriting Year 2014

………...

103

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi, Underwriting Year

2013

………

..104

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi, Underwriting Year

2012

………..

105

Lampiran

1.

Daftar Istilah…….………

106

2.Tarif

asuransi

Gempa

Bumi

Indonesia

…….……….………...

...108

3. Zona Asu

ransi Gempa Bumi Indonesia………11

2

4. Cr

esta Zone Indonesia………12

2

5.

Skala

First Loss

………

129

6. Tabel

Short Periode

kurang dari 1

tahun

…..………

..

………

..130

7. Skala

Indemnity Period

………

...131

Attachment

1.

Glossaries………..…..106

2.

Indonesian

Earthquake

Insurance

Tariff………..108

3. Cresta Zone and Zone Table………112

4. Indonesia Cresta Zone ……….122

5. First Loss Scale …..………129

6. Short Period Table Less Than One Year

Period………130

7. Indemnity Period Scale………..…131

Referensi

Reference

1. Otoritas Jasa Keuangan (OJK).

2. Badan Pusat Statistik (BPS).

1. Financial Service Authority (OJK).

2. Central of Statistic Bureau (BPS).

*)

Laporan Statistik ini dapat diperoleh di website

PT Reasuransi MAIPARK Indonesia

Indonesia Per Provinsi

Ikhtisar Statistik Asuransi Gempa Bumi Indonesia Juni 2016

S

tatistic Overview of Indonesia Earthquake Insurance June 2016

A. Umum

A. General

Berdasarkan data Badan Pusat Statistik,

pertumbuhan ekonomi Indonesia berdasarkan

Produk Domestik Bruto (Harga Berlaku) triwulan

II terhadap triwulan sebelumnya naik sebesar

4,02% (Rp2.942,00 triliun menjadi Rp.3.086,60

triliun).

Dari sisi Industri Asuransi Umum, menurut

Asosiasi Asuransi Umum Indonesia, dapat

dilihat bahwa Premi Bruto untuk kelas bisnis

harta benda (triwulan II tahun 2015 ke triwulan II

2016) mengalami kenaikan sebesar 9,6%

(Rp.7.942,93 miliar menjadi Rp.8.704,58 miliar)

Based on Central of Statistics Bureau data,

Indonesia economic growth by Gross Domestic

Bruto (Current Price) second quarter compare

to

previous

quarter

increased

4.02%

(IDR2,942.00 trillion to IDR.3,086.60 trillion)

From the General Insurance Industry, based on

General Insurance Indonesia Assosiation, can

be seen that Gross Premium for property class

of business (second quarter 2015 compare to

second

quarter

2016)

increase

9.6%

(IDR.7,942.93 billion to IDR.8,704.58 billion)

Produk Domestik Bruto atas dasar Harga Berlaku dan Harga Konstan 2010 - Kuartal II 2016

Gross Domestic Product by Current Price and Constant Price 2010 - second quarter 2016

Triw ulan I-2016 /

Quarter 1- 2016

Triw ulan II-2016 /

Quarter 2 - 2016

Triw ulan I-2016 /

Quarter 1 - 2016

Triw ulan II-2016 /

Quarter 2 - 2016

Produk Dom estik Bruto

(Gross Dom estic Product)

2,942.00

3,086.60

2,262.30

2,353.20

dalam triliun rupiah

in trillion rupiah

Harga Berlaku (Current price)

Harga Konstan 2010/ Constant price 2010

Premi dan Klaim Bruto Kelas Bisnis Harta Benda - Kuartal II 2016

Gross Premium and Claim Property class of business - Second Quarter 2016

Kelas Bisnis

Class of Business

Triwulan I-2015

Triwulan I-2016

Triwulan I-2015 Triwulan I-2016

Harta Benda

7,942.93

8,704.58

3,431.57

3,400.25

dalam miliar rupiah

in billion rupiah

dan Klaim Bruto turun -0,9% (Rp.3.431,57 miliar

menjadi Rp.3.400,25 miliar ).

and Gross Claim decrease -0.9% (IDR.

3.431,57 billion to IDR.3,400.25 billion).

B. Struktur Pasar

B. Market Structure

.

C. Premi Bruto

C. Gross Premium

Tabel 1.1 menyajikan rincian premi bruto

berdasarkan jenis okupasi dari

Underwriting

Year

2012 hingga

Underwriting Year

2016.

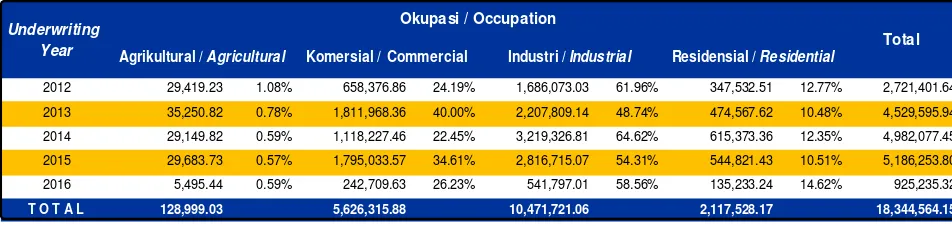

Berdasarkan data tersebut dapat kita lihat

bahwa untuk Okupasi Industrial dan Residensial

pada

Underwriting Year

2012-2014 mengalami

trend kenaikan, namun dua okupasi lainnya

menurun di

Underwriting Year

2014. Penurunan

pada Okupasi Agrikultural ini diakibatkan adanya

penurunan penutupan di Provinsi Jawa Barat

khususnya di Kab. Karawang. Selain itu

penurunan ini juga disebabkan adanya

penurunan penutupan di Provinsi Bali dan Jawa

Barat, masing-masing adalah Kab. Karangasem

dan Kab. Bandung.

The table 1.1 shows the details of gross

premium

based

on

occupation

from

Underwriting Year 2011 to Underwriting Year

2015.

We could see based to Industrial and

Residential Occupation data have increase

trend, but other two occupation in Underwriting

Year 2012-2014 have decrease in Underwriting

Year 2014. The decrease in Agriculture

Occupation because of decrease cover in East

Java Province especially City of Karawang. The

decrease also caused by decreasing cover in

Bali Province and East Java i.e. Karangasem

and Bandung District respectively.

Struktur Pasar Industri Asuransi Umum Indonesia

Mark et Structure of the Indonesia General Insurance Industry

Kategori

Jumlah

Perusahaan Asuransi Umum

76

Perusahaan Reasuransi

6

Asuransi Sosial

2

Perusahaan Asuransi Wajib

3

Sumber: buku Direktori 2015: Industri Keuangan Non Bank

D. Jumlah Risiko

D

.

Number of Risk

Dari Tabel 1.2 dapat kita peroleh informasi

bahwa jumlah risiko Okupasi Komersial terbesar

ada di

Underwriting Year

2014 yaitu 124.558.

Sedangkan jumlah risiko Okupasi Komersial di

Underwriting Year

2016 adalah 25.085 atau

sebesar 20,14% atau seperlima dari jumlah

risiko Okupasi Komersial di

Underwriting Year

2014. Jika pola pensesian dan proses validasi

bordero tidak berubah, maka jumlah risiko

Okupasi Komersial di

Underwriting Year

2016

masih akan meningkat.

Jumlah Risiko pada Okupasi Agrikultural di

Underwriting Year

2015 dibandingkan dengan

Underwriting Year

2014 baru mencapai

51.79%(390 dibanding 753), berbeda dengan 3

okupasi lainnya yang rata-rata diatas 90%. Hal

ini diakibatkan karena adanya penurunan jumlah

risiko penutupan sebagian besar di Provinsi

Sumatera Utara dan Kalimantan Timur.

Penurunan yang relative signifikan terjadi di

Provinsi Sumatera Utara adalah di Kab.

Simalungun, Kab. Tapanuli Selatan dan Kab.

From Table 1.2 we can find information that

the biggest number of risks for Commercial

Occupation was in Underwriting Year 2014 i.e

124,558

.

While number of risks

for

Commercial

Occupation in Underwriting Year 2016 was

25,085 i.e. 20.14% or fifth of the number of risks

Commercial Occupancy in Underwriting Year

2014. If the cession and bordereoux validation

processing pattern unchanged, then number of

risks for the Commercial Occupation in

Underwriting Year 2016 still increased.

Number of risks in Agriculture Occupation

in Underwriting Year 2015 compared to

Underwriting Year 2015 reached 51.79% (390

compare to 753), different to other three

occupation that average above 90%. This is

because of the decrease number of risks cover

mostly in North Sumatra and East Kalimantan

Province. Relatively significant decrease was in

North Sumatra Province i.e. Simalungun,

Tapanuli Selatan dan Asahan District. While in

Dalam Jutaan Rupiah

In Million Rupiah

2012

29,419.23

1.08%

658,376.86

24.19%

1,686,073.03

61.96%

347,532.51

12.77%

2,721,401.64

2013

35,250.82

0.78%

1,811,968.36

40.00%

2,207,809.14

48.74%

474,567.62

10.48%

4,529,595.94

2014

29,149.82

0.59%

1,118,227.46

22.45%

3,219,326.81

64.62%

615,373.36

12.35%

4,982,077.45

2015

29,683.73

0.57%

1,795,033.57

34.61%

2,816,715.07

54.31%

544,821.43

10.51%

5,186,253.80

2016

5,495.44

0.59%

242,709.63

26.23%

541,797.01

58.56%

135,233.24

14.62%

925,235.32

T O T A L

128,999.03

5,626,315.88

10,471,721.06

2,117,528.17

18,344,564.15

Tabel 1.1 Premi Bruto dan Rasio Berdasarkan Okupasi per 30 Juni 2016

Table 1.1 Gross Premium and Ratio By Occupation as at 30 June 2016

Underwriting

Year

Okupasi / Occupation

Total

Asahan. Sedangkan di Provinsi Kalimantan

Timur, penurunan jumlah risiko penutupan yang

relative signifikan ada di Kota Balikpapan.

East Kalimantan, relatively significant decrease

in number of risks cover was in Balikpapan city.

Jika terdapat asosiasi antara kontribusi

premi dengan banyaknya risiko maka belum

tentu asosiasi tersebut berbentuk linear dan

If there is any association between the

premium contribution and the number of risks then

the association is not necessarily linear nor

Tabel 1.2 Jumlah Risiko Berdasarkan Okupasi per 30 Juni 2016

Table 1.2 Number of Risk By Occupation as at 30 June 2016

Jumlah /

Total

%

Jumlah /

Total

%

Jumlah /

Total

%

Jumlah /

Total

%

Jumlah /

Total

%

Agricultural / Agricultural A 420 0.24 535 0.28 753 0.32 390 0.17 189 0.35

Komersial / Commercial C 94,595 54.42 100,683 53.12 124,558 52.94 123,845 54.78 25,085 46.31

Industrial / Industrial I 17,199 9.89 18,433 9.73 18,903 8.03 17,165 7.59 4,236 7.82

Residensial / Residential R 61,613 35.45 69,873 36.87 91,061 38.70 84,669 37.45 24,661 45.52 173,827 100.00 189,524 100.00 235,275 100.00 226,069 100.00 54,171 100.00

Occupation

Jumlah / Total

Okupasi

U/Y 2012

U/Y 2013

U/Y 2014

U/Y 2015

U/Y 2016

Number of Risk By Occupation

As at 30 June 2016

UY 2012

UY 2013

UY 2014

UY 2015

UY 2016

Agricultural

UY 2012

UY 2013

UY 2014

UY 2015

UY 2016

Commercial

UY 2012

UY 2013

UY 2014

UY 2015

UY 2016

Industrial

UY 2012

UY 2013

UY 2014

UY 2015

UY 2016

positif. Hal ini dibuktikan dengan apabila

melihat dari premi bruto tertinggi berada di

okupasi industrial sedangkan banyak risiko

tertinggi berada pada okupasi komersial.

positive. This is proved which the highest gross

premium is on the industrial occupation while the

highest total risk is under commercial occupation.

Berdasarkan data okupasi, okupasi

Komersial terdiri dari beberapa kode okupasi.

Jumlah risiko terbesar berdasarkan kode

okupasi di

Underwriting Year

2012

–

2016

adalah sebagai berikut:

Based on occupation data, Commercial

occupation consist of several occupation codes.

The highest number of risks by occupation code

in Underwriting Year 2012

–

2016 are as follows:

Okupasi Residensial terdiri dari beberapa

kode okupasi. Jumlah risiko terbesar

berdasarkan kode okupasi di

Underwriting

Year

2012

–

2016 adalah sebagai berikut:

Residential occupation consist of several

occupation codes. The highest number of risks by

occupation code in Underwriting Year 2012

–

2016 are as follows:

Jumlah Risiko Terbesar pada Okupasi Residensial Berdasarkan Kode Okupasi per 30 Juni 2016

The Highest Number Of Risk in Residential Occupation as at 30 June 2016 by Occupation Code

U/Y 2012

U/Y 2013

U/Y 2014

U/Y 2015

U/Y 2016

Total

Total

Total

Total

Total

Dwelling Houses, not classified

as Shop-Houses (Ruko), not

exceeding 3 storeys.

2976

35,736

34,338

48,485

44,746

14,226

35,736

34,338

48,485

44,746

14,226

Description & Occupation Code

Total

Jumlah Risiko Terbesar pada Okupasi Komersial Berdasarkan Kode Okupasi per 30 Juni 2016

The Highest Number Of Risk in Commercial Occupation as at 30 June 2016 by Occupation Code

U/Y 2012

U/Y 2013

U/Y 2014

U/Y 2015

U/Y 2016

Total

Total

Total

Total

Total

Shops

2934

0

0

33,421

33,483

6,768

Shops - Subject to Waranty A

29341

23,045

16,013

0

0

0

Private Warehouses and

Storehouses - Subject to

Warranty A

29371

13,080

14,355

0

0

0

Veem and Bonded Warehouses -

Subject to Warranty A

293941

2

3

0

0

0

36,127

30,371

33,421

33,483

6,768

Description & Occupation Code

E.

Incurred Claim

E. Incurred Claim

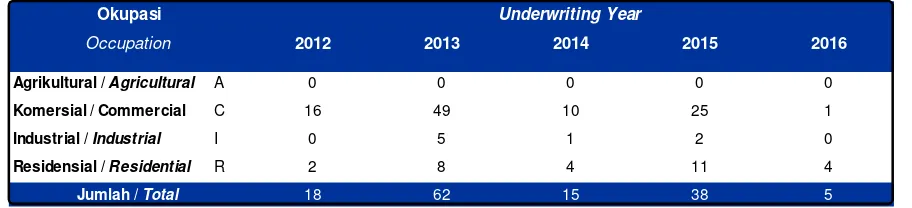

Berdasarkan tabel 1.3, frekuensi klaim

gempa bumi paling banyak terjadi di

Underwriting Year

2013 yaitu sebanyak 62

klaim dan didominasi okupasi Komersial

sebanyak 49 klaim. Hal ini disebabkan oleh

kejadian Erupsi Gunung Kelud, 13 Februari

2014. Klaim akibat Erupsi ini sebagian besar

berasal dari Provinsi Jawa Timur khususnya

Kota & Kab. Kediri, Kab. Malang dan Kota

Surabaya.

Based on table 1.3, the highest earthquake

claim frequency occurred in Underwriting Year

2013 was 62 claims and it dominated by

Commercial occupation of 49 claims. It was

caused by Kelud Eruption, on 13 February 2014.

This claim due to Eruption was mostly come from

East Java Province especially City and District of

Kediri, Malang District and Surabaya city.

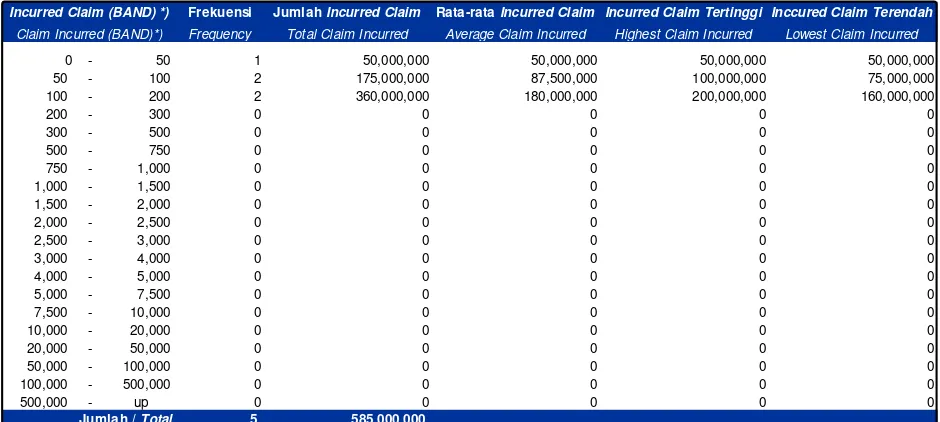

Berdasarkan Tabel 1.4 dan grafik terlihat

bahwa untuk frekuensi klaim tinggi berada

pada Total

Incurred Claim

yang relatife kecil,

sedangkan untuk frekuensi klaim kecil berada

pada Total Incurred Claim yang relative besar.

Gambaran tersebut adalah untuk Underwriting

Year 2016 selama 6 bulan terakhir dimana

masih memungkinkan terjadi perubahan jika

terjadi event ke depan.

Based on table 1.4 and graph below it can be

seen that the high frequency claims lies in

relatively small Total Claim Incurred, while low

frequency claims lies in relatively big Total Claim

Incurred. The picture was for Underwriting Year

2016 during the last six month which probably any

changes if an event occurs in the future.

2012

2013

2014

2015

2016

Agrikultural / Agricultural

A

0

0

0

0

0

Komersial / Commercial

C

16

49

10

25

1

Industrial / Industrial

I

0

5

1

2

0

Residensial / Residential

R

2

8

4

11

4

18

62

15

38

5

Tabel 1.3 Frekwensi Klaim Berdasarkan Okupasi per 30 Juni 2016

Occupation

Jumlah /

Total

Table 1.3 Claim Frequency By Occupation as at 30 June 2016

Underwriting Year

*) Dalam Rupiah *) In IDR

Frekuensi

Jumlah Incurred Claim

Rata-rata Incurred Claim Incurred Claim Tertinggi Inccured Claim Terendah

Frequency

Total Claim Incurred

Average Claim Incurred

Highest Claim Incurred

Lowest Claim Incurred

0

-

50

1

50,000,000

50,000,000

50,000,000

50,000,000

Table 1.4 Frequency Incurred Claim Underwriting Year 2016 as at 30 June 2016

Claim Incurred (BAND)*)

Incurred Claim (BAND) *)

Jumlah / Total

Dari tabel 1.5 tampak bahwa jumlah klaim

terbesar berada pada

Underwriting Year

2013.

Klaim yang terbesar adalah pada okupasi

Komersial, yaitu 99.63% dari total klaim di

Underwriting Year

2013 atau sebesar

Rp.271,3 miliar.

From the table 1.5 below, it shows that the

largest claim is in the Underwriting Year 2013. The

largest claim is under Commercial occupation that

is 99.63% of the total claim in Underwriting Year

2013 or

Rp.

271.3 billion.

Tabel 1.6 menyajikan kejadian Gempa

Bumi Tahun 2016 dan

Incurred Claim

sampai

dengan 30 Juni 2016.

Table 1.6 shows earthquake events occurred

in 2016 and the corresponding incurred claims as

at 30 June 2016.

Table 1.5 Claim Amount By Occupation as at 30 June 2016

Dalam RupiahIn IDR

2012

2013

2014

Jumlah / Total % Jumlah / Total % Jumlah / Total % Jumlah / Total % Jumlah / Total % Agrikultural / Agricultural A 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 Komersial / Commercial C 1,636,685,520.49 92.33 271,246,520,180.70 99.63 624,550,950.05 67.66 5,959,405,013.50 38.45 200,000,000.00 0.00 Industrial / Industrial I 0.00 0.00 890,057,888.00 0.33 200,000,000.00 21.67 7,680,965,985.00 49.56 0.00 0.00 Residensial / Residential R 135,984,751.35 7.67 104,486,089.00 0.04 98,536,193.51 10.67 1,857,064,680.00 11.98 385,000,000.00 0.00 1,772,670,271.84 100.00 272,241,064,157.70 100.00 923,087,143.56 100.00 15,497,435,678.50 100.00 585,000,000.00 0.00

2016

Jumlah / Total

Underwriting Year

Tabel 1.5 Jumlah Klaim Berdasarkan Okupasi per 30 Juni 2016

2015

Okupasi / Occupation

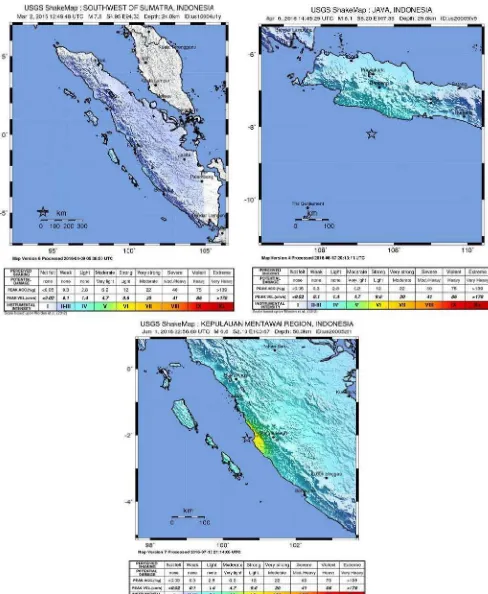

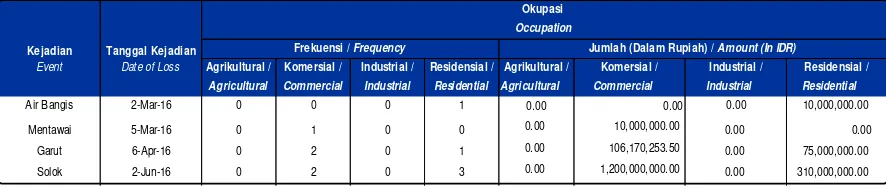

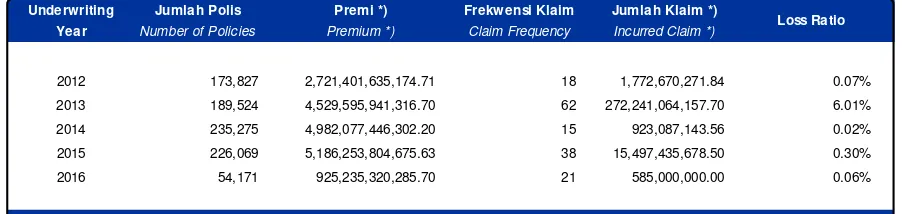

Tabel 1.6 Kejadian Gempa Bumi Tahun 2016 dan Klaim per 30 Juni 2016

Table 1.6 Earthquak e Event in 2016 and Claim as at 30 June 2016

Dalam Rupiah

In IDR

Kejadian

Tanggal Kejadian

Kekuatan Gempa (S.R)

Event

Date of Loss

Magnitude (S.R)

Air Bangis

2-Mar-16

7.8 SR

10,000,000.00

Mentawai

5-Mar-16

5.3 SR

10,000,000.00

Garut

6-Apr-16

6.1 SR

181,170,253.50

Solok

2-Jun-16

6.5 SR

1,510,000,000.00

Claim

Gambar 3. Peta Intensitas dan ShakeMap Gempa Air Bangis, Garut dan Solok setelah kejadian (sumber peta intensitas:

http://www.earthquake.usgs.gov

).

Tabel 1.7 menyajikan klaim untuk

event

Air

Bangis, Mentawai, Garut dan Solok perjenis

okupasi. Dapat dilihat bahwa okupasi yang

terdampak pada beberapa event tersebut adalah

Komersial dan Residensial. Hal ini dimungkinkan

masih sedikit/belum adanya penutupan pada

Okupasi Industrial dan Agrikultural sehingga

dampak ke Okupasi tersebut belum ada atau

mungkin laporan klaim untuk kedua Okupasi

tersebut belum masuk.

Table 1.7 shows Air Bangis, Mentawai,

Garut and Solok event by occupation. It can be

seen that Commercial and Residential

Occupation

affected

with

some event

mentioned. This is probably a little/there is not

yet cover in Industrial and Agricultural

Occupation so the impact to the occupation

does not exist or may the claim report was not

received yet (Incurred But Not Reported

).

Tabel di bawah ini adalah daftar klaim

terbesar sampai dengan tanggal 30 Juni 2016.

Event Pariaman merupakan event dengan besar

klaim terbesar dalam kurun waktu 5 tahun pasca

event Aceh.

The table below is a list of the largest claims

as at 30 June 2016. Pariaman event was the

biggest claim in the period of 5 years since the

Aceh event.

Tabel 1.7 Kejadian Gempa Bumi Tahun 2016 dan Klaim per Okupasi per 30 Juni 2016 Table 1.7 Earthquak e Event in 2016 and Claim per Occupation as at 30 June 2016

Event Date of Loss Agrikultural / Komersial / Industrial / Residensial /

Agricultural Commercial Industrial Residential Agricultural Commercial Industrial Residential

Air Bangis 2-Mar-16 0 0 0 1 10,000,000.00

Mentawai 5-Mar-16 0 1 0 0 0.00

Garut 6-Apr-16 0 2 0 1 75,000,000.00

Solok 2-Jun-16 0 2 0 3 310,000,000.00

Occupation

Residensial / Agrikultural / Komersial / Industrial /

Kejadian Tanggal Kejadian

Okupasi

Frekuensi / Frequency Jumlah (Dalam Rupiah) / Amount (In IDR)

Tabel 1.8 menyajikan data jumlah polis dan

loss ratio per 30 Juni 2016. Tabel tersebut

menunjukkan loss ratio

Underwriting Year

2016

masih lebih kecil dari 5

Underwriting Year

.

Sedangkan loss ratio tertinggi berada pada

Underwriting Year

2013 sebesar 6.01%. Hal ini

dipengaruhi oleh nilai klaim yang cukup tinggi yang

mayoritas disebabkan dari Erupsi Gunung Kelud

tahun 2014.

Table 1.8 shows number of policies, and

loss ratio as at 30 June 2016. The table show

that the biggest loss ratio was at Underwriting

Year 2013 i.e. 6.01%. It was influenced by

large amount of claim that resulting majority

from Kelud Eruption in 2014.

Dalam Rupiah

In IDR

No.

Kejadian

Tanggal Kejadian

Kekuatan Gempa (S.R)

Klaim

Event

Date of Loss

Magnitude (S.R)

Claim

1

ACEH

26-12-2004

9

781,709,354,691.64

2

YOGYA

27-05-2006

5.9

286,314,259,635.72

3

PADANG

06-03-2007

5.8

22,445,090,553.18

4

BENGKULU

12-09-2007

7.9

48,880,150,344.02

5

PADANG

16-08-2009

6.9

42,782,942,555.00

6

TASIKMALAYA

02-09-2009

7.3

24,305,724,396.26

7

PARIAMAN

30-09-2009

7.6

1,083,648,012,851.01

8

BIMA

09-11-2009

6.7

43,046,593,135.48

9

MERAPI

25-10-2010

*)

27,499,741,856.40

10

KELUD

13-02-2014

*)

322,962,107,319.64

*) Penyeba b terka i t l etus a n gunung bera pi

*) Caused by volcanic eruption

Daftar Klaim - Klaim Terbesar Posisi 30 Juni 2016

List of The Largest Claims as at 30 June 2016

Tabel 1.8 Jumlah Polis dan Loss Ratio per 30 June 2016

Table 1.8 Number of Policies and Loss Ratio as at 30 June 2016

Underwriting

Jumlah Polis

Premi *)

Frekwensi Klaim

Jumlah Klaim *)

Year

Number of Policies

Premium *)

Claim Frequency

Incurred Claim *)

2012

173,827

2,721,401,635,174.71

18

1,772,670,271.84

0.07%

2013

189,524

4,529,595,941,316.70

62

272,241,064,157.70

6.01%

2014

235,275

4,982,077,446,302.20

15

923,087,143.56

0.02%

2015

226,069

5,186,253,804,675.63

38

15,497,435,678.50

0.30%

2016

54,171

925,235,320,285.70

21

585,000,000.00

0.06%

Keterangan :

*) Dalam Rupiah*) In IDR