PT Reasuransi MAIPARK Indonesia

Dengan Hormat,

Sesuai dengan tujuan pendirian MAIPARK,

MAIPARK selalu berupaya untuk memberikan

pelayanan yang terbaik bagi Industri Asuransi

Umum di Indonesia khususnya mengenai

statistik dan pengetahuan risiko gempa bumi.

Dukungan dari seluruh perusahaan asuransi

umum sangat berarti bagi kami dalam upaya

pengembangan Laporan Statistik ini.

Kami berharap Laporan Statistik ini dapat

memberikan manfaat tidak hanya bagi

perusahaan yang menangani asuransi gempa

bumi, namun juga bagi industri asuransi umum

di Indonesia.

Hormat kami,

Dear Sir / Madam,

In line with the purpose of MAIPARK

establishment, MAIPARK always strive to

provide the best service for General Insurance

Industry in Indonesia particularly regarding

statistic and knowledge of Earthquake risks.

Support from the General Insurance Industry will

be meaningful to us in order to improve this

Statistic Report.

We hope this Statistic Report will be beneficial

not only to the insurance companies which write

earthquake insurance but also to the whole

general insurance industry in Indonesia.

Sincerely,

Kata Pengantar

Foreword

Yasril Y. Rasyid

President Director

Hal.

Kata Pengantar ... i

Daftar Isi ... ii

Informasi Statistik ... vii

Ikhtisar Statistik Asuransi Gempa Bumi

Indonesia Juni 2015 ...

A. Umum ... 1

B. Struktur Pasar ... 1

C. Premi Bruto ... 1

D. Jumlah Risiko ... 3

E. Incurred Claim ... 5

Exposure Asuransi Gempa Bumi Indonesia ...

Tabel 2.1. Exposure Per Cresta Zone ... 10

Tabel 2.2. Exposure Per Okupasi ... 12

Tabel 2.3. Exposure Per Interest... 14

Tabel 2.4. Exposure Per Provinsi ... 16

Tabel 2.5. Exposure Per Kelas Konstruksi ... 17

Premi Bruto Asuransi Gempa Bumi Indonesia

... ….

Tabel 3.1. Gross Premium Per Cresta Zone .. 19

Tabel 3.2. Gross Premium Per Okupasi ... 21

Tabel 3.3. Gross Premium Per Provinsi ... 23

Tabel 3.5. Gross Premium Per Kelas Konstruksi

... 24

Jumlah Risiko Asuransi Gempa Bumi Indonesia

...

Tabel 4.1. Jumlah Risiko Per Cresta Zone ... 26

Tabel 4.2. Jumlah Risiko Per Okupasi ... 28

Tabel 4.3. Jumlah Risiko Per Kelas Konstruksi

... 30

Klaim Asuransi Gempa Bumi Indonesia ...

Tabel 5.1. Klaim Frekwensi Per Cresta Zone.. 32

Tabel 5.2. Klaim Frekwensi Per Okupasi ... 34

Page

Foreword ... i

Contents ... ii

Statistic Information ... vii

Statistic Overview of Indonesian Earthquake

Insurance June 2015 ...

A. General ... 1

B. Market Structure ... 1

C. Gross Premium ... 1

D. Number of Risk ... 3

E. Incurred Claim ... 5

Indonesian Earthquake Insurance Exposure ...

Table 2.1. Exposure By Cresta Zone ... 10

Table 2.2. Exposure By Occupation ... 12

Table 2.3. Exposure By Interest ... 14

Table 2.4. Exposure By Province ... 16

Tabel 2.5. Exposure By Construction Class .... 17

Indonesian Earthquake Insurance Gross

Premium ...

Table 3.1. Gross Premium By Cresta Zone ... 19

Table 3.2. Gross Premium By Occupation .... 21

Table 3.3. Gross Premium By Province ... 23

Table 3.5. Gross Premium By Construction Class

... 24

Indonesian Earthquake Insurance Number of

Risks ...

Table 4.1. Number of Risk By Cresta Zone ... 26

Table 4.2. Number of Risk By Occupation .... 28

Table 4.3. Number of Risk By Construction Class

... 30

Indonesian Earthquake Insurance Claim ...

Table 5.1. Claim Frequency By Cresta Zone .. 32

Table 5.2. Claim Frequency By Occupation….34

Daftar Isi

Content

Tabel 5.4.. Klaim Per Cresta Zone ... 36

Tabel

5.5.

Klaim

Per

Okupasi

... ………...38

Profil Risiko dan Klaim ...

Underwriting Year 2011 - 2015,

Seluruh Okupasi ... 40

Underwriting Year 2015, Seluruh Okupasi ... 41

Underwriting Year 2014, Seluruh Okupasi ... 42

Underwriting Year 2013, Seluruh Okupasi ... 43

Underwriting Year 2012, Seluruh Okupasi ... 44

Underwriting Year 2011, Seluruh Okupasi ... 45

Profil Risiko dan Klaim

Underwriting Year

2015

Per Okupasi ...

Okupasi Agrikultural ... 46

Okupasi Komersial ... 47

Okupasi Industrial ... 48

Okupasi Residensial ... 49

Profil Risiko dan Klaim

Underwriting Year

2014

Per Okupasi ...

Okupasi Agrikultural ... 50

Okupasi Komersial ... 51

Okupasi Industrial ... 52

Okupasi Residensial ... 53

Profil Risiko dan Klaim

Underwriting Year

2013

Per Okupasi ...

Okupasi Agrikultural ... 54

Okupasi Komersial ... 55

Okupasi Industrial ... 56

Okupasi Residensial ... 57

Table 5.4. Claim By Cresta Zone . ... …….36

Table 5.5 Claim By Occupation ... …..38

Risk and Loss Profile ...

Underwriting

Year

2011

-

2015,

All Occupation ... 40

Underwriting Year 2015, All Occupation ... 41

Underwriting Year 2014, All Occupation ... 42

Underwriting Year 2013, All Occupation ... 43

Underwriting Year 2012, All Occupation ... 44

Underwriting Year 2011, All Occupation ... 45

Risk and Loss Profile Underwriting Year 2015

By Occupation …. ...

Agricultural Occupation ... 46

Commercial Occupation ... 47

Industrial Occupation ... 48

Residential Occupation ... 49

Risk and Loss Profile Underwriting Year 2014

By Occupation …. ...

Agricultural Occupation ... 50

Commercial Occupation ... 51

Industrial Occupation ... 52

Residential Occupation ... 53

Risk and Loss Profile Underwriting Year 2013

By Occupation …. ...

Agricultural Occupation ... 54

Commercial Occupation ... 55

Industrial Occupation ... 56

Profil Risiko dan Klaim

Underwriting Year

2012

Per Okupasi ...

Okupasi Agrikultural ... 58

Okupasi Komersial ... 59

Okupasi Industrial ... 60

Okupasi Residensial

... 61

Profil Risiko dan Klaim

Underwriting Year

2011

Per Okupasi ...

Okupasi Agrikultural ... 62

Okupasi Komersial... 63

Okupasi Industrial ... 64

Okupasi Residential ... 65

Exposure, Premi Bruto, Jumlah Risiko dan Klaim

Asuransi Gempa Bumi Indonesia ...

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Cresta Zone, Underwriting Year 2011 .... 66

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Cresta Zone, Underwriting Year 2012 ... 67

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Cresta Zone, Underwriting Year 2013 ... 68

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Cresta Zone, Underwriting Year 2014

... 69

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Cresta Zone, Underwriting Year 2015

... 70

Exposure, Premi Bruto, Jumlah Risiko dan Klaim

Asuransi Gempa Bumi Indonesia ...

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Okupasi, Underwriting Year 2011 ... 71

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Okupasi, Underwriting Year 2012 ... 72

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Okupasi, Underwriting Year 2013 ... 73

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Okupasi, Underwriting Year 2014

... 74

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Okupasi, Underwriting Year 2015

... 75

Risk and Loss Profile Underwriting Year 2012

By Occupation …. ...

Agricultural Occupation ... 58

Commercial Occupation ... 59

Industrial Occupation ... 60

Residential Occupation ... 61

Risk and Loss Profile Underwriting Year 2011

By Occupation ...

Agricultural Occupation ... 62

Commercial Occupation ... 63

Industrial Occupation ... 64

Residential Occupation ... 65

Indonesian Earthquake Insurance Exposure,

Gross Premium, Number of Risks and Claim ...

Exposure, Gross Premium, Number of Risks &

Claim by Cresta Zone, UY 2011 ……….66

Exposure, Gross Premium, Number of Risks &

Claim by Cresta Zone, UY 2012 ... 67

Exposure, Gross Premium, Number of Risks &

Claim by Cresta Zone, UY 2013 ... 68

Exposure, Gross Premium, Number of Risks &

Claim by Cresta Zone, UY 2014 ... 69

Exposure, Gross Premium, Number of Risks &

Claim by Cresta Zone, UY 2015 ... 70

Indonesian Earthquake Insurance Exposure,

Gross Premium, Number of Risks and Claim ...

Exposure, Gross Premium, Number of Risks &

Claim by Occupation, UY 2011 ………..71

Exposure, Gross Premium, Number of Risks &

Claim by Occupation, UY 2012 ... 72

Exposure, Gross Premium, Number of Risks &

Claim by Occupation, UY 2013 ... 73

Exposure, Gross Premium, Number of Risks &

Claim by Occupation,

UY

2014

... 74

Exposure, Gross Premium, Number of Risks &

Claim by Occupation,

UY

2015

... 75

Exposure, Premi Bruto, Jumlah Risiko dan Klaim

Asuransi Gempa Bumi Indonesia ...

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi, Underwriting Year 2011 ... 76

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi, Underwriting Year 2012 ... 77

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi, Underwriting Year 2013 ... 78

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi, Underwriting Year 2014

... 79

Exposure, Premi Bruto, Jumlah Risiko & Klaim

per Provinsi, Underwriting Year 2015

... 80

Peta

Distribusi Exposure Gempa Bumi Indonesia per

Provinsi,

Underwriting Year

2015, per 30 Juni

2015 …….. ... 81

Distribusi Gempa Bumi Indonesia M > 5 dan

Claim Incurred

2015 …… ... 82

Distribusi Exposure Gempa Bumi Indonesia per

Provinsi, Underwriting Year 2015, per 30 Juni

2015, Distribusi Gempa Bumi Indonesia M > 5

dan

Claim

Incurred

UY

2015………..83

Ulasan Aktuaria

……….…………84

Lampiran

1.

Daftar Istilah ... 93

2.

Tarif Asuransi Gempa Bumi Indonesia ….

... 95

3.

Skala First Loss ... 97

4.

Tabel jangka Waktu Pertanggungan

Kurang Dari Satu Tahun ... 98

5.

Skala Indemnity Period ... 99

6.

Tabel Cresta Zone dan Zona ……….100

Indonesian Earthquake Insurance Exposure,

Gross Premium, Number of Risks and Claim ...

Exposure, Gross Premium, Number of Risks &

Claim by Province, UY 2011 ……….76

Exposure, Gross Premium, Number of Risks &

Claim by Province, UY 2012 ... 77

Exposure, Gross Premium, Number of Risks &

Claim by Province, UY 2013 ... 78

Exposure, Gross Premium, Number of Risks &

Claim by Province,

UY

2014

... 79

Exposure, Gross Premium, Number of Risks &

Claim by Province,

UY

2015

... 80

Map

Indonesian Earthquake Exposure Distribution

By Province, Underwriting Year 2015, as at 30

June 2015 ... 81

Indonesian Earthquake Distribution M > 5 and

Claim Incurred 2015 ………..……….

... 82

Indonesian Earthquake Exposure Distribution

By Province, Underwriting Year 2015, as at 30

June 2015, Indonesian Earthquake Distribution

M > 5 and Claim Incurred 2015.. ... 83

Actuarial

Commentary ……..

……….…………84

Attachments

1.

Glossaries ... 93

2.

Indonesian Earthquake Insurance Tariff ..

... 95

3.

First Loss Scale ... ………97

4.

Short Period Table Less Than One Year

Period……….98

5.

Indemnity Period Scale………99

6.

Cresta Zone and Zone Table………100

Referensi

1.

Otoritas Jasa Keuangan (OJK).

2.

Badan Pusat Statistik (BPS).

*)

Laporan Statistik ini dapat diperoleh di website

PT Reasuransi MAIPARK Indonesia

www.maipark.com

Reference

1.

Financial Services Authority (OJK).

2.

Central of Statistics Bureau (BPS).

*)

Statistic Report is available on PT Reasuransi

MAIPARK Indonesia‘s Website

1.

Statistik dibuat berdasarkan Underwriting

Year yang tercatat sampai dengan posisi

30 Juni2015.

2.

Sesi Limit

2.1.

Limit Sesi atas setiap risiko (any

one risk) untuk gabungan kerugian

fisik dan gangguan usaha adalah

sebagai berikut:

2.1.1 Untuk daerah Jawa Barat,

Banten dan DKI:

5% (lima prosen) dari

jumlah

seluruh

pertanggungan (total

sum

insured)

maksimum

USD

2.500.000,00 (dua juta

lima ratus ribu Dollar

Amerika) atas setiap

risiko,

setiap

perusahaan asuransi

atau penerbit polis

untuk

Underwriting

Year 2010, 2011 dan

2012.

5% (lima prosen) dari

jumlah

seluruh

pertanggungan (total

sum

insured)

maksimum

Rp.

25.000.000.000,00

(dua puluh lima miliar

Rupiah) atau yang

setara dengan USD

2.631.578,00 (dua juta

enam ratus tiga puluh

satu lima ratus tujuh

puluh delapan Dollar

Amerika) atas setiap

risiko,

setiap

perusahaan asuransi

atau penerbit polis

1.

Statistic Report is based on Underwriting

Year basis, which is recorded as at 30

June 2015.

2.

Cession Limit

2.1.

Cession Limit of any one risk for the

combined material damage and

business interruption are as follows:

2.1.1

For West Java, Banten and

DKI:

5% (five percent) of the

total sum insured,

being a maximum of

USD

2,500,000.00

(two

million

five

hundred thousand U.S.

Dollars) for any one

risk, each insurance

company or policy

issuer for Underwriting

Year 2010, 2011 and

2012.

5% (five percent) of the

total sum insured,

being a maximum of

Rp.25,000,000,000.00

(twenty five billion

Indonesian Rupiahs)

or equal to USD

2,631,578.00

(two

million six hundred

thirty one thousand five

hundred seventy eight

U.S. Dollars) for any

one

risk,

each

insurance company or

policy

issuer

for

Underwriting

Year

2013.

Informasi Statistik

Untuk

Underwriting

Year 2013.

2.1.2

Untuk daerah Indonesia

lainnya:

25% (dua puluh lima

prosen) dari jumlah

seluruh

pertanggungan (total

sum

insured)

maksimum

USD

2.500.000,00 (dua juta

lima ratus ribu Dollar

Amerika) atas setiap

risiko,

setiap

perusahaan asuransi

atau penerbit polis

untuk

Underwriting

Year 2010, 2011 dan

2012.

25% (dua puluh lima

prosen) dari jumlah

seluruh

pertanggungan (total

sum

insured)

maksimum

Rp.

25.000.000.000,00

(dua puluh lima miliar

Rupiah) atau yang

setara dengan USD

2.631.578,00 (dua juta

enam ratus tiga puluh

satu lima ratus tujuh

puluh delapan Dollar

Amerika) atas setiap

risiko,

setiap

perusahaan asuransi

atau penerbit polis

untuk

Underwriting

Year 2013.

2.1.3

Terhitung sejak 1 Januari

2014 Limit Sesi atas setiap

risiko (any one risk) untuk

gabungan kerugian fisik

dan gangguan usaha

adalah:

15%

(lima

belas

prosen) dari jumlah

seluruh

2.1.2.

For other Indonesia areas:

25%

(twenty

five

percent) of the total

sum insured, being a

maximum of USD

2,500,000.00

(two

million five hundred

thousand U.S. Dollars)

for any one risk, each

insurance company or

policy

issuer

for

Underwriting

Year

2010, 2011 and 2012.

25%

(twenty

five

percent) of the total

sum insured, being a

maximum

of

Rp.25,000,000,000.00

(twenty five billion

Indonesian Rupiahs)

or equal to USD

2,631,578.00

(two

million six hundred

thirty one thousand five

hundred seventy eight

U.S. Dollars) for any

one

risk,

each

insurance company or

policy

issuer

for

Underwriting

Year

2013.

2.1.3.

Since January 1, 2014,

Cession Limit of any one

risk for the combined

material damage and

business interruption is :

15% (fifteen percent)

of the total sum

pertanggungan (total

sum

insured)

maksimum

USD

3.500.000,00 (tiga juta

lima ratus ribu Dollar

Amerika) atas setiap

risiko,

setiap

perusahaan asuransi

atau penerbit polis

untuk

Underwriting

Year 2014.

15%

(lima

belas

prosen) dari jumlah

seluruh

pertanggungan (total

sum

insured)

maksimum

Rp.

35.000.000.000,00

(tiga puluh lima miliar

Rupiah) atau yang

setara dengan USD

3.043.478,26 (tiga juta

empat puluh tiga ribu

empat ratus tujuh

puluh delapan koma

dua puluh enam Dollar

Amerika) atas setiap

risiko,

setiap

perusahaan asuransi

atau penerbit polis

untuk

Underwriting

Year 2015.

2.2.

Yang dimaksud dengan setiap

risiko (anyone risk) adalah

akumulasi (aggregate) jumlah

harga pertanggungan seluruh risiko

pada lokasi yang sama untuk

masing-masing

perusahaan

asuransi. Definisi setiap risiko atau

setiap lokasi ditentukan oleh

perusahaan

asuransi

dalam

underwriting polis kebakaran.

insured,

being

a

maximum of USD

3,500,000.00

(three

million five hundred

thousand U.S. Dollars)

for any one risk, each

insurance company or

policy

issuer

for

Underwriting

Year

2014.

15%

(twenty

five

percent) of the total

sum insured, being a

maximum

of

Rp.35,000,000,000.00

(thirty

five

billion

Indonesian Rupiahs)

or equal to USD

3,043,478.26

(three

million fourty three

thousand four hundred

seventy eight point

twenty six U.S. Dollars)

for any one risk, each

insurance company or

policy

issuer

for

Underwriting

Year

2015.

2.2.

Anyone risk is the accumulation

(aggregate) of total sum insured of

all risks at the same location for each

insurance company. The definition of

anyone risk or any location is

specified by the insurer or policy

issuer in accordance with the fire

underwriting policy.

2.3

Dalam hal penutupan secara

First

Loss Basis / Sub-limit, jumlah yang

disesikan sebagaimana diatur

dalam butir 2.1 diatas, dikalikan

prosentase First Loss Scale.

2.4

Untuk risiko yang ditutup secara

ko-asuransi, jumlah maksimum sesi

dari semua anggota ko-asuransi

adalah sesuai dengan ketentuan

yang diatur dalam 2.1 diatas. Sesi

masing-masing perusahaan adalah

proporsional sebanding sahamnya

dalam ko-asuransi.

Dalam hal terdapat penutupan lain

selain polis ko-asuransi tersebut

pada obyek pertanggungan yang

sama, perusahaan asuransi tetap

dapat mensesikan risiko dimaksud,

dengan catatan jumlah seluruh sesi

perusahaan

asuransi

bersangkutan

tidak

melebihi

ketentuan yang diatur pada butir

2.1.

2.3

In First Loss Basis / Sub Limit

policies, the amount ceded is

stipulated in point 2.1 above, then

multiplied by the percentage of First

Loss Scale.

2.4

For risks which are covered by

co-insurance, the maximum cession

from all members of coinsurance is

stipulated in point 2.1 above. Each

ceding

company

cedes

proportionally depending on its

co-insurance share.

If there are policies other than

co-insurance policy on the same

insured object, the insurer is still able

to cede such risk subject to total

insurance company’s

cession not

exceeding the provision in point 2.1.

3.

Tarif Premi Asuransi Gempa Bumi

Indonesia

3.1. Penutupan

Full Value Basis

mengaplikasikan

Tarif

Premi

Standar Gempa Bumi Indonesia

(lampiran 2).

3.2. Penutupan

First Loss / Sub Limit

Basis mengaplikasikan standar

First Loss Scale (lampiran 3).

3.3. Perhitungan

premi

untuk

penutupan kurang dari 12 (dua

belas) bulan diberlakukan skala

premi jangka pendek (lampiran 4)

3.4. Untuk perhitungan premi Business

Interruption diberlakukan Indemnity

Period Scale (lampiran 5).

4.

Obyek Pertanggungan

4.1 Obyek pertanggungan yang dapat

disesikan

adalah

obyek

pertanggungan asuransi kebakaran

berupa:

4.1.1. Kerusakan Fisik:

Bangunan

Pondasi

Penggalian dan

Sejenisnya

Persediaan Barang

Lain-lain

4.1.2 Gangguan Usaha:

Keuntungan Bruto

Upah

Kenaikan

Biaya

Operasional

Lain-lain

4.2 Penutupan sebagaimana dimaksud

pada butir 4.1. adalah yang ditutup

secara langsung (direct business)

termasuk ko-asuransi. Penutupan

tidak langsung (indirect business /

reasuransi) tidak dapat disesikan.

3.

Indonesian

Standard

Earthquake

Premium Tariff

3.1.

For the coverage of Full Value

Basis, apply Indonesian Standard

Earthquake

Premium

Tariff

(attachment 2).

3.2.

For the First Loss / Sub Limit Basis

coverage apply standard First Loss

Scale (attachment 3).

3.3.

Premium calculation for short

period coverage is based on Short

Period Scale (attachment 4).

3.4.

Premium calculation for business

interruption is based on Indemnity

Period Scale (attachment 5).

4.

Insured Object

4.1.

Insured object which can be ceded

is fire insurance object such as:

4.1.1.

Material damage:

Building

Foundation

Excavation and

the like

Stock

Others

4.1.2.

Business Interruption

Gross Profit

Wages

Increase in cost of

working

Others

4.2.

Insured object referred in point 4.1

is direct business, including

coinsurance. Indirect business /

reinsurance cannot be ceded.

5.

Pelaporan Bordero

Pelaporan bordero dilakukan setiap

bulannya untuk semua risiko yang ditutup

pada bulan yang bersangkutan dan sudah

harus diterima selambat-lambatnya pada

akhir bulan berikutnya

5.

Bordereaux Submission

Bordereaux submission is on a monthly

basis for all risks underwritten in the

month concerned and should be received

by the end of the following month at the

latest.

A.

Umum

Berdasarkan data Badan Pusat Statistik,

Perekonomian Indonesia pada triwulan II-2015

sebagaimana diukur dari Produk Domestik

Bruto (PDB), tumbuh sebesar 3,78 %

dibandingkan triwulan I-2015 (q-to-q). Nilai

Produk Domestik Bruto (PDB) Indonesia atas

dasar harga konstan 2010 pada triwulan II-2015

mencapai Rp. 2.239,3 triliun sedangkan pada

triwulan I-2015 sebesar Rp.2.157,8 triliun. Bila

dilihat berdasarkan harga berlaku, PDB triwulan

II-2015 adalah sebesar Rp. 2.866,9 triliun

sedangkan triwulan I-2015 adalah Rp. 2.728,8

triliun.

B. Struktur Pasar

Berdasarkan data Otoritas Jasa Keuangan

pada buku Direktori Perasuransian Indonesia

2014: Industri Keuangan Non Bank

Perasuransian, terdapat 82 perusahaan

asuransi umum yang memiliki izin beroperasi di

Indonesia.

C. Premi Bruto

Sampai dengan 30 Juni 2015, premi bruto

asuransi gempa bumi

Underwriting Year 2011

adalah sebesar Rp.

2.821,3

miliar. Premi bruto

untuk Underwriting Year 2012 tercatat

A. General

Based on Central of Statistics Bureau Data,

Indonesian economic in second quarter 2015 as

measured by Gross Domestic Product (GDP)

increased by 3.78 % compared with first quarter

2015 (q-to-q). Gross Domestic Product (GDP)

based on Constant Price 2010 in second quarter

2015 reached the amount of Rp. 2,239.3 trillion

while in first quarter 2015 was Rp. 2,157.8

trillion. If it is based on Current Market Price,

GDP in second quarter 2015 was Rp. 2,866.9

trillion while in first quarter 2015 was Rp. 2,728.8

trillion.

B. Market Structure

Based on Financial Services Authority data

in the book of Indonesian Insurance Directory

2014: Non Bank Financial Institution Insurance,

there are 82 general insurers having operating

licenses in Indonesia.

C. Gross Premium

As at 30 June 2015, earthquake gross

premium for Underwriting Year 2011 was Rp.

2,821.3 billion. Gross premium for Underwriting

Year 2012 was recorded

Ikhtisar Statistik Asuransi Gempa Bumi Indonesia Juni 2015

Statistic Overview of Indonesia Earthquake Insurance June 2015

Rp. 2.645,4 miliar, sedangkan untuk

Underwriting Year 2013 adalah Rp. 4.251,8

miliar. Untuk Underwriting Year 2014 dan 2015

adalah Rp. 4.242,6 miliar dan Rp. 749,7 miliar.

Angka

– angka ini akan terus bergerak naik

terutama untuk

Underwriting Year 2014 dan

2015.

Tabel 1.1 di bawah ini menyajikan rincian

premi bruto berdasarkan jenis okupasi dari

Underwriting Year 2011 hingga

Underwriting

Year 2015. Prosentase okupasi Industrial selalu

berada pada posisi pendapatan tertinggi

dibanding 3 (tiga) okupasi lainnya (Agrikultural,

Komersial, Residensial), yaitu di atas 47% dari

total premi.

Meskipun okupasi Komersial, Residensial

dan Agrikultural tidak memberikan kontribusi

premi sebesar okupasi Industrial, namun ketiga

okupasi tersebut memperlihatkan pertumbuhan

premi yang cukup signifikan. Hal ini terlihat

terutama pada premi okupasi Komersial pada

Underwriting Year 2013 yang meningkat

sebesar 165,3% dari Rp. 646.139,75 juta di

Underwriting Year 2012

menjadi Rp.

1.714.074,27 juta.

Rp. 2,645.4 billion, while for Underwriting Year

2013 was Rp. 4,251.8 billion. For Underwriting

Year 2014 and 2015 were Rp. 4,242.6

billion

and Rp. 749.7

billion.

These figures would

certainly increase especially for Underwriting

Year 2014 and 2015.

The table 1.1 below shows the details of

gross premium based on occupation from

Underwriting Year 2011 to Underwriting Year

2015. Industrial occupation always has the

biggest percentage income compared to 3

(three) remaining occupations (Agricultural,

Commercial, Residential), that is above 47 %

from premium total.

Although occupation of Commercial,

Residential and Agricultural do not contribute

premium as much as Industrial occupation,

those three occupation show significant

premium growth. In this case, the premium

under Commercial occupation in Underwriting

Year 2013 increased by 165.3% from Rp.

646,139.75 million in Underwriting Year 2012 to

Rp. 1,714,074.27 million.

Dalam Jutaan Rupiah

In Million Rupiah 2011 23,897.32 0.85% 758,200.03 26.87% 1,696,811.05 60.14% 342,414.01 12.14% 2,821,322.40 2012 29,419.23 1.11% 646,139.75 24.43% 1,623,908.96 61.39% 345,921.69 13.08% 2,645,389.64 2013 34,917.83 0.82% 1,714,074.27 40.31% 2,028,735.96 47.71% 474,108.51 11.15% 4,251,836.57 2014 24,913.07 0.59% 918,279.91 21.64% 2,679,945.46 63.17% 619,512.25 14.60% 4,242,650.69 2015 2,213.84 0.30% 211,342.54 28.19% 409,408.22 54.61% 126,734.87 16.90% 749,699.47

Tabel 1.1 Premi Bruto dan Rasio Berdasarkan Okupasi per 30 Juni 2015

Table 1.1 Gross Premium and Ratio By Occupation as at 30 June 2015

Underwriting

Year

Okupasi

Total

D. Jumlah Risiko

Tabel 1.2 di bawah ini menyajikan jumlah

risiko pada

Underwriting Year 2011 hingga

Underwriting Year 2015 yang tercatat sampai

dengan 30 Juni 2015.

D. Number of Risks

Table 1.2 below shows the number of risks

from Underwriting Year 2011 to Underwriting

Year 2015 recorded until 30 June 2015.

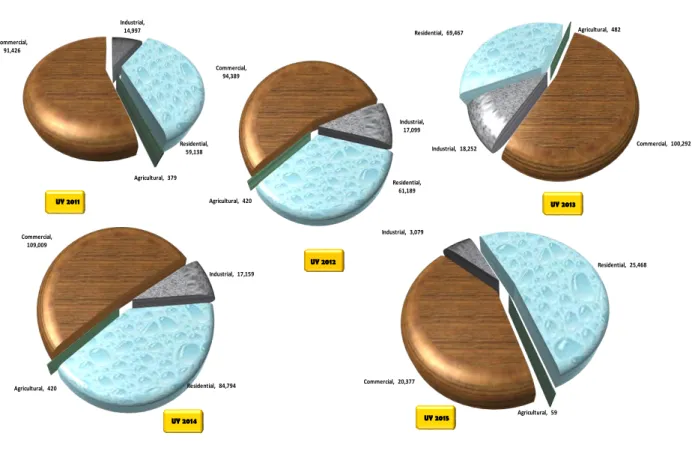

Agricultural, 482 Commercial, 100,292 Industrial, 18,252 Residential, 69,467 Agricultural, 420 Commercial, 109,009 Industrial, 17,159 Residential, 84,794 Agricultural, 59 Commercial, 20,377 Industrial, 3,079 Residential, 25,468

Number of Risk By Occupation

As at 30 Jun 2015

Agricultural, 379 Commercial, 91,426 Industrial, 14,997 Residential, 59,138 Agricultural, 420 Commercial, 94,389 Industrial, 17,099 Residential, 61,189 UY 2011 UY 2014 UY 2015 UY 2012 UY 2013Tabel 1.2 Jumlah Risiko Berdasarkan Okupasi per 30 Juni2015

Table 1.2 Number of Risk By Occupation as at 30 June 2015

Jumlah /

Total

%

Jumlah /

Total

%

Jumlah /

Total

%

Jumlah /

Total

%

Jumlah /

Total

%

Agricultural / Agricultural A 379 0.23 420 0.24 482 0.26 420 0.20 59 0.12 Komersial / Commercial C 91,426 55.10 94,389 54.53 100,292 53.21 109,009 51.57 20,377 41.60 Industrial / Industrial I 14,997 9.04 17,099 9.88 18,252 9.68 17,159 8.12 3,079 6.29 Residensial / Residential R 59,138 35.64 61,189 35.35 69,467 36.85 84,794 40.11 25,468 51.99 165,940 100.00 173,097 100.00 188,493 100.00 211,382 100.00 48,983 100.00

Occupation

Jumlah / TotalJumlah risiko terbesar untuk setiap

Underwriting Year, dalam hal ini dari

Underwriting Year 2011 sampai dengan

Underwriting Year 2015 ada pada okupasi

Komersial, yaitu selalu berada pada rasio di atas

41% dari total risiko. Kemudian diikuti oleh

okupasi Residensial dengan rasio di atas 35%.

Jika terdapat asosiasi antara kontribusi

premi dengan banyaknya risiko maka belum

tentu asosiasi tersebut berbentuk linear dan

positif. Hal ini dibuktikan dengan apabila melihat

dari premi bruto tertinggi berada di okupasi

industrial sedangkan banyak risiko tertinggi

berada pada okupasi komersial.

Berdasarkan data okupasi, okupasi

Komersial terdiri dari beberapa kode okupasi.

Jumlah risiko terbesar berdasarkan kode

okupasi di

Underwriting Year 2011

– 2015

adalah sebagai berikut:

Okupasi Residensial terdiri dari beberapa kode

okupasi. Jumlah risiko terbesar berdasarkan

kode okupasi di Underwriting Year 2011 – 2015

adalah sebagai berikut:

The highest number of risks for each

Underwriting Year, in this case from

Underwriting Year 2011 to Underwriting Year

2015, is under Commercial occupation, which is

always on the ratio above 41% from the total

risk. Then, it is followed by Residential

occupation with ratio above 35%.

If there is any association between the

premium contribution and the number of risks

then the association is not necessarily linear nor

positive. This is proved which the highest gross

premium is on the industrial occupation while the

highest total risk is under commercial

occupation.

Based on occupation data, Commercial

occupation consist of several occupation codes.

The highest number of risks by occupation code

in Underwriting Year 2011

–

2015 are as follows:

Residential occupation consist of several

occupation codes. The highest number of risks

by occupation code in Underwriting Year 2011

–

2015 are as follows:

U/Y 2011 U/Y 2012 U/Y 2013 U/Y 2014 U/Y 2015

Jumlah / Total Jumlah / Total Jumlah / Total Jumlah / Total Jumlah / Total

Shops 2934 0 0 0 25,737 5,096

Shops - Subject to Waranty A 29341 22,158 22,998 15,962 0 0

Private Warehouses and Storehouses - Subject to Warranty A

29371 12,800 12,980 14,291 0 0

Veem and Bonded Warehouses -

Subject to Warranty A 293941 1 2 3 0 0

34,959 35,980 30,256 25,737 5,096

Description & Occupation Code

Jumlah / Total

Deskripsi & Kode Okupasi

Jumlah Risiko Terbesar pada Okupasi Komersial Berdasarkan Kode Okupasi per 30 Juni 2015

The Highest Number Of Risk in Commercial Occupation as at 30 June 2015 by Occupation Code

U/Y 2011

U/Y 2012

U/Y 2013

U/Y 2014

U/Y 2015

Jumlah /

Total

Jumlah /

Total

Jumlah /

Total

Jumlah /

Total

Jumlah /

Total

Private Warehouses and

Storehouses - Subject to

Warranty A

2976

35,956

35,385

34,065

46,956

14,530

Jumlah Risiko Terbesar pada Okupasi Residensial Berdasarkan Kode Okupasi per 30 Juni 2015

The Highest Number Of Risk in Residential Occupation as at 30 June 2015 by Occupation Code

Deskripsi & Kode Okupasi

Description & Occupation Code

E. Incurred Claim

Berdasarkan tabel 1.3 di bawah ini,

frekuensi klaim gempa bumi paling banyak

terjadi di Underwriting Year 2011 yaitu sebanyak

87 klaim dan didominasi okupasi Komersial

sebanyak 62 klaim. Hal ini disebabkan oleh

kejadian gempa bumi di 2011 yaitu Gempa Bumi

Nusa Dua pada tanggal 13 Oktober 2011

dengan kekuatan 6,8 S.R dan Gempa Bumi

Sibolga pada tanggal 6 November 2011 dengan

kekuatan 6,7 S.R.

E. Incurred Claim

Based on table 1.3 below,

the highest

earthquake claim frequency occurred in

Underwriting Year 2011 was 87 claims and it

dominated by Commercial occupation of 62

claims. It was caused by Earthquakes in 2011

namely Nusa Dua Earthquake on 13 October

2011 with a magnitude of 6.8 S.R and Sibolga

Earthquake on 6 November

2011

with a

magnitude of 6.7 S.R.

2011

2012

2013

2014

2015

Agrikultural /

Agricultural

A

0

0

0

0

0

Komersial /

Commercial

C

62

14

45

7

0

Industrial /

Industrial

I

0

0

5

0

0

Residensial /

Residential

R

25

1

7

2

0

87

15

57

9

0

Tabel 1.3 Frekwensi Klaim Berdasarkan Okupasi per 30 Juni 2015

Table 1.3 Claim Frequency By Occupation as at 30 June 2015

Occupation

Jumlah /

Total

Underwriting Year

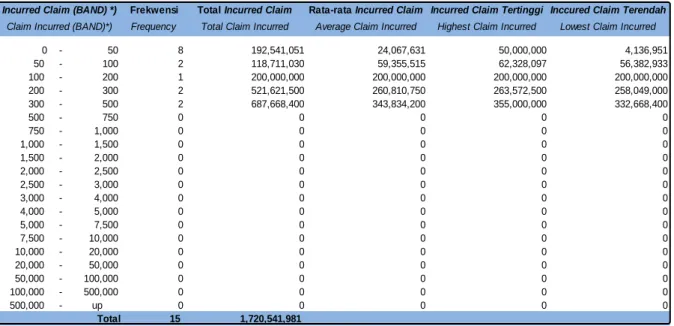

Berdasarkan Tabel 1.4 dan grafik di bawah

ini terlihat bahwa untuk frekwensi klaim tinggi

berada pada Total Incurred Claim yang relative

kecil, sedangkan untuk frekwensi klaim kecil

berada pada Total Incurred Claim yang relative

besar.

Based on table 1.4 and graph below it can

be seen that the high frequency claims lies in

relatively small Total Claim Incurred, while low

frequency claims lies in relatively big Total Claim

Incurred.

*) Dalam Rupiah

*) In Rupiah

Frekwensi

Total

Incurred Claim

Rata-rata

Incurred Claim Incurred Claim Tertinggi Inccured Claim Terendah

Frequency

Total Claim Incurred

Average Claim Incurred

Highest Claim Incurred

Lowest Claim Incurred

0

-

50

8

192,541,051

24,067,631

50,000,000

4,136,951

50

-

100

2

118,711,030

59,355,515

62,328,097

56,382,933

100

-

200

1

200,000,000

200,000,000

200,000,000

200,000,000

200

-

300

2

521,621,500

260,810,750

263,572,500

258,049,000

300

-

500

2

687,668,400

343,834,200

355,000,000

332,668,400

500

-

750

0

0

0

0

0

750

-

1,000

0

0

0

0

0

1,000

-

1,500

0

0

0

0

0

1,500

-

2,000

0

0

0

0

0

2,000

-

2,500

0

0

0

0

0

2,500

-

3,000

0

0

0

0

0

3,000

-

4,000

0

0

0

0

0

4,000

-

5,000

0

0

0

0

0

5,000

-

7,500

0

0

0

0

0

7,500

-

10,000

0

0

0

0

0

10,000

-

20,000

0

0

0

0

0

20,000

-

50,000

0

0

0

0

0

50,000

-

100,000

0

0

0

0

0

100,000

-

500,000

0

0

0

0

0

500,000

-

up

0

0

0

0

0

15

1,720,541,981

Claim Incurred (BAND)*)

Incurred Claim (BAND) *)

Total

Tabel 1.4 Frekwensi I

ncurred Claim Underwriting Year

2012 Per 30 Juni 2015

Table 1.4 Frequency Incurred Claim Underwriting Year 2012 as at 30 June 2015

Dengan melihat tabel 1.5 tampak bahwa

jumlah klaim terbesar berada pada Underwriting

Year 2013. Klaim yang terbesar adalah pada

okupasi Komersial, yaitu 99,40% dari total klaim

di

Underwriting Year 2013 atau sebesar Rp.

306,2 miliar.

Tabel 1.6 di bawah ini menyajikan kejadian

Gempa Bumi Tahun 2015 dan

Incurred Claim

sampai dengan 30 Juni 2015.

Looking at table 1.5 below, it shows that the

largest claim is in the Underwriting Year 2013.

The largest claim is under Commercial

occupation that is 99.40% of the total claim in

Underwriting Year 2013 or Rp. 306.2 billion.

Table 1.6 below shows earthquake events

occurred in 2015 and the corresponding

incurred claims as at 30 June 2015.

Table 1.5 Claim Amount By Occupation as at 30 June 2015

Dalam Rupiah

In Rupiah

2011

2012

2013

Jumlah /

Amount

%

Jumlah /

Amount

%

Jumlah /

Amount

%

Jumlah /

Amount

%

Jumlah /

Amount

%

Agrikultural / Agricultural A 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 Komersial / Commercial C 6,375,313,072.29 95.80 1,670,541,980.54 97.09 306,212,972,292.31 99.40 1,228,599,676.05 94.69 0.00 0.00 Industrial / Industrial I 0.00 0.00 0.00 0.00 1,750,356,290.96 0.57 0.00 0.00 0.00 0.00 Residensial / Residential R 279,739,660.04 4.20 50,000,000.00 2.91 99,244,211.73 0.03 68,916,625.00 5.31 0.00 0.00 6,655,052,732.33 100.00 1,720,541,980.54 100.00 308,062,572,795.00 100.00 1,297,516,301.05 100.00 0.00 0.00

2015

Jumlah /

Total

Underwriting Year

Tabel 1.5 Jumlah Klaim Berdasarkan Okupasi per 30 Juni 2015

2014

Okupasi

Tabel 1.7 di bawah ini menyajikan klaim

untuk event Manado perjenis okupasi.

Tabel di bawah ini adalah daftar klaim

terbesar sampai dengan tanggal 30 Juni 2015.

Table 1.7 shows Manado event by

occupation.

The table below is a list of the largest claims

as at 30 June 2015.

Dalam Rupiah

In Rupiah

No.

Kejadian

Tanggal Kejadian

Kekuatan Gempa (S.R)

Klaim

Event

Date of Loss

Magnitude (S.R)

Claim

1

ACEH

26-12-2004

9

782,649,961,586.18

2

YOGYA

27-05-2006

5.9

268,635,542,386.91

3

PADANG

06-03-2007

5.8

22,224,113,241.32

4

BENGKULU

12-09-2007

7.9

49,044,007,333.60

5

PADANG

16-08-2009

6.9

42,782,942,555.00

6

TASIKMALAYA

02-09-2009

7.3

24,400,937,277.87

7

PARIAMAN

30-09-2009

7.6

1,082,395,841,788.55

8

BIMA

09-11-2009

6.7

43,046,593,135.48

9

MERAPI

25-10-2010

*)

27,499,741,856.40

10

KELUD

13-02-2014

*)

113,296,619,876.55

*) Pe nye ba b terka i t l e tus a n gunung be ra pi Ca us e d by vol ca ni c e rupti on

Daftar Klaim - Klaim Terbesar Posisi 30 Juni 2015

List of The Largest Claims as at 30 June 2015

Tabel 1.7 Kejadian Gempa Bumi Tahun 2015 dan Klaim per Okupasi per 30 Juni 2015

Table 1.7 Earthquake Event in 2015 and Claim per Occupation as at 30 June 2015

Event

Date of Loss

Agrikultural / Komersial /

Industrial /

Residensial /

Agricultural

Commercial

Industrial

Residential

Manado

19-Mar-15

0

1

0

0

0.00

367,160,000.00

0.00

0.00

Residensial /

Residential

Agrikultural /

Agricultural

Komersial /

Commercial

Industrial /

Industrial

Kejadian

Tanggal Kejadian

Okupasi

Occupation

Frekwensi

Frequency

Jumlah (Dalam Rupiah)

Amount (In Rupiah)

Tabel 1.6 Kejadian Gempa Bumi Tahun 2015 dan Klaim per 30 Juni 2015

Table 1.6 Earthquak e Event in 2015 and Claim as at 30 June 2015

Dalam Rupiah

In Rupiah

Kejadian

Tanggal Kejadian

Kekuatan Gempa (S.R)

Event

Date of Loss

Magnitude (S.R)

Manado

19-Mar-15

5.2 SR

367,160,000.00

Klaim

Tabel 1.8 menyajikan data jumlah polis dan

loss ratio per 30 Juni 2015. Tabel tersebut

menunjukkan bahwa loss ratio tertinggi berada

pada

Underwriting Year 2013 sebesar 7,25%.

Hal ini dipengaruhi oleh nilai klaim yang cukup

tinggi yang mayoritas disebabkan dari Erupsi

Gunung Kelud tahun 2014.

Tabel 1.9 menyajikan Premi dan

Exposure

per 30 Juni 2015.

Table 1.8 shows number of policies, and

loss ratio as at 30 June 2015. The table show

that the biggest loss ratio was at Underwriting

Year 2013 i.e. 7.25%. It was influenced by large

amount of claim that majority resulting from

Kelud Eruption in 2014.

Table 1.9 shows Premium and Exposure as

at 30 June 2015.

Tabel 1.8 Jumlah Polis dan Loss Ratio per 30 Juni 2015

Table 1.8 Number of Policies and Loss Ratio as at 30 June 2015

Underwriting

Jumlah Polis

Premi *)

Frekwensi Klaim

Jumlah Klaim *)

Year

Number of Policies

Premium *)

Claim Frequency

Incurred Claim *)

2011

117,060

2,821,322,404,542.47

87

6,655,052,732.33

0.24%

2012

111,505

2,645,389,635,380.59

15

1,720,541,980.54

0.07%

2013

115,678

4,251,836,566,234.02

57

308,062,572,795.00

7.25%

2014

125,596

4,242,650,688,164.07

9

1,297,516,301.05

0.03%

2015

34,745

749,699,474,583.64

0

0.00

0.00%

Keterangan :

*) Dalam Rupiah In RupiahLoss Ratio

Dalam Jutaan Rupiah

In Million Rupiah

Premi

Exposure

Prem ium

Exposure

2011

2,821,322.40

2,154,508,565.60

2012

2,645,389.64

1,931,209,404.23

2013

4,251,836.57

2,605,650,673.28

2014

4,242,650.69

2,688,065,075.39

2015

749,699.47

501,167,234.30

T O T A L

14,710,898.77

9,880,600,952.80

Tabel 1.9 Premi dan Exposure per 30 Juni 2015

Table 1.9 Premium and Exposure as at 30 June 2015

Tab le 2.1

in IDR

Amount

%

Amount

%

Amount

%

Amount

%

Amount

%

BANDA ACEH

1.1

4,799,061,565,236.65

0.22

3,853,109,114,587.20

0.20

4,584,417,825,419.94

0.18

6,358,619,953,498.16

0.24

455,976,230,003.88

0.09

MEDAN

1.2

46,652,172,698,019.40

2.17

39,461,037,801,624.10

2.04

47,542,841,695,945.20

1.82

52,960,197,728,466.80

1.97

15,266,930,733,632.30

3.05

OTHERS

1.3

98,732,449,809,919.40

4.58

40,046,371,005,873.30

2.07

49,388,292,913,159.30

1.90

50,050,764,200,763.80

1.86

5,459,716,930,089.16

1.09

NORTH SUMATERA

1

150,183,684,073,175.00

6.97

83,360,517,922,084.60

4.32

101,515,552,434,525.00

3.90

109,369,581,882,729.00

4.07

21,182,623,893,725.40

4.23

PADANG

2.1

16,558,741,293,262.30

0.77

18,866,092,244,302.70

0.98

27,019,846,969,932.80

1.04

29,477,769,570,121.90

1.10

4,343,731,570,576.07

0.87

PALEMBANG

2.2

15,670,152,211,490.50

0.73

18,924,640,233,255.90

0.98

22,991,302,055,908.20

0.88

18,812,054,223,542.00

0.70

2,704,718,148,459.90

0.54

OTHERS

2.3

123,060,615,053,710.00

5.71

134,125,533,745,810.00

6.95

150,261,108,880,271.00

5.77

181,058,254,439,927.00

6.74

29,600,541,769,976.90

5.91

SOUTH SUMATERA

2

155,289,508,558,463.00

7.21

171,916,266,223,368.00

8.90

200,272,257,906,112.00

7.69

229,348,078,233,590.00

8.53

36,648,991,489,012.90

7.31

JAKARTA

3.1

464,501,709,083,112.00

21.56

399,151,129,341,981.00

20.67

429,924,032,664,141.00

16.50

531,708,345,423,764.00

19.78

114,243,160,461,085.00

22.80

BANDUNG

3.2

6,881,910,055,825.06

0.32

10,941,392,878,987.80

0.57

10,455,800,182,858.20

0.40

9,865,031,172,512.33

0.37

3,383,533,867,786.94

0.68

OTHERS

3.3

607,607,677,895,557.00

28.20

655,965,204,624,330.00

33.97

974,495,125,173,158.00

37.40

884,594,173,548,510.00

32.91

175,486,957,797,968.00

35.02

WEST JAVA

3

1,078,991,297,034,490.00

50.08

1,066,057,726,845,300.00

55.20

1,414,874,958,020,160.00

54.30

1,426,167,550,144,790.00

53.06

293,113,652,126,839.00

58.49

SEMARANG

4.1

6,547,169,388,280.43

0.30

7,032,671,423,369.66

0.36

8,708,673,384,952.73

0.33

6,094,897,525,335.40

0.23

872,040,937,538.39

0.17

YOGYAKARTA

4.2

10,227,924,407,900.00

0.47

9,213,654,452,599.54

0.48

8,527,858,959,520.06

0.33

13,606,090,868,674.60

0.51

2,202,243,172,949.89

0.44

OTHERS

4.3

116,804,919,938,213.00

5.42

102,486,294,341,901.00

5.31

136,192,546,432,047.00

5.23

139,412,503,264,086.00

5.19

35,491,815,108,839.00

7.08

CENTRAL JAVA

4

133,580,013,734,394.00

6.20

118,732,620,217,870.00

6.15

153,429,078,776,519.00

5.89

159,113,491,658,096.00

5.92

38,566,099,219,327.30

7.70

SURABAYA

5.1

87,137,349,483,550.50

4.04

50,352,975,158,199.70

2.61

37,296,159,313,449.70

1.43

77,159,355,434,089.90

2.87

17,350,016,361,654.30

3.46

OTHERS

5.2

300,813,831,856,445.00

13.96

210,015,661,096,202.00

10.87

200,084,798,977,104.00

7.68

350,891,208,794,371.00

13.05

33,500,806,604,704.10

6.68

EAST JAVA

5

387,951,181,339,995.00

18.01

260,368,636,254,402.00

13.48

237,380,958,290,554.00

9.11

428,050,564,228,461.00

15.92

50,850,822,966,358.40

10.15

KALIMANTAN

6

123,120,604,752,261.00

5.71

101,269,813,257,791.00

5.24

128,063,585,552,569.00

4.91

104,335,917,881,702.00

3.88

19,654,791,173,810.90

3.92

UJUNG PANDANG

7.1

10,441,385,729,218.00

0.48

10,366,655,119,882.30

0.54

14,056,704,460,026.80

0.54

21,486,486,598,491.00

0.80

3,108,512,496,701.43

0.62

OTHERS

7.2

59,644,593,333,905.30

2.77

53,890,334,194,031.10

2.79

39,155,028,523,482.00

1.50

110,822,471,621,368.00

4.12

10,501,222,198,359.10

2.10

SULAWESI

7

70,085,979,063,123.30

3.25

64,256,989,313,913.30

3.33

53,211,732,983,508.80

2.04

132,308,958,219,859.00

4.92

13,609,734,695,060.50

2.72

OTHER ISLANDS

8

55,306,297,043,097.90

2.57

65,246,834,197,369.70

3.38

316,902,549,313,180.00

12.16

99,370,933,137,622.20

3.70

27,540,518,738,916.40

5.50

2,154,508,565,599,000.00

100.00

1,931,209,404,232,100.00

100.00

2,605,650,673,277,120.00

100.00

2,688,065,075,386,850.00

100.00

501,167,234,303,051.00

100.00

U/Y 2015

As At 30/06/2015

National Aggregate Exposure By Cresta Zone

T O T A L

U/Y 2014

Cresta Zone

U/Y 2013

U/Y 2011

U/Y 2012

101,515,552.43 200,272,257.91 1,414,874,958.02 153,429,078.78 237,380,958.29 128,063,585.55 53,211,732.98 316,902,549.31 109,369,581.88 229,348,078.23 1,426,167,550.14 159,113,491.66 428,050,564.23 104,335,917.88 132,308,958.22 99,370,933.14 21,182,623.89 36,648,991.49 293,113,652.13 38,566,099.22 50,850,822.97 19,654,791.17 13,609,734.70 27,540,518.74

National Aggregate Exposure By Cresta Zone

As at 30 Jun 2015

(In Billion IDR)

150,183,684.07 155,289,508.56 1,078,991,297.03 133,580,013.73 387,951,181.34 123,120,604.75 70,085,979.06 55,306,297.04 83,360,517.92 171,916,266.22 1,066,057,726.85 118,732,620.22 260,368,636.25 101,269,813.26 64,256,989.31 65,246,834.20 UY 2011 UY 2012 UY 2013 UY 2014 UY 2015