42

Lampiran

Kurs USD

BI Rate

IHSG

Jan-07

9111,82

9,50%

1776,52

Feb-07

9112,85

9,25%

1772,35

Mar-07

9209,95

9,00%

1780,51

Apr-07

9142,90

9,00%

1948,46

Mei-07

8888,48

8,75%

2050,01

Jun-07

9028,55

8,50%

2119,17

Jul-07

9112,36

8,25%

2294,85

Agust-07

9413,55

8,25%

2152,85

Sep-07

9356,50

8,25%

2269,15

Okt-07

9152,71

8,25%

2556,94

Nop-07

9310,68

8,25%

2662,15

Des-07

9380,27

8,00%

2742,77

Jan-08

9453,3

8,00%

2640,93

Feb-08

9226,95

8,00%

2690,43

Mar-08

9230,83

8,00%

2475,91

Apr-08

9254,64

8,00%

2291,59

Mei-08

9337,3

8,25%

2425,98

Jun-08

9342,29

8,50%

2378,53

43

Agust-08

9195,1

9,00%

2134,43

Sep-08

9387,4

9,25%

1914,3

Okt-08

10098,65

9,50%

1376,22

Nop-08

11769,85

9,50%

1255,18

Des-08

11381,53

9,25%

1298,13

Jan-09

11223,11

8,75%

1367,83

Feb-09

11912,15

8,25%

1318,64

Mar-09

11908,8

7,75%

1343,93

Apr-09

11080,25

7,50%

1576,41

Mei-09

10449,11

7,25%

1837,88

Jun-09

10257,59

7,00%

2029,8

Jul-09

10161,86

6,75%

2133,45

Agust-09

10027,5

6,50%

2356,66

Sep-09

9950,39

6,50%

2394,59

Okt-09

9530

6,50%

2466,88

Nop-09

9517,2

6,50%

2424,32

Des-09

9504,85

6,50%

2492,65

Jan-10

9321,95

6,50%

2619,9

Feb-10

9395,11

6,50%

2548,58

Mar-10

9219,68

6,50%

2692,11

Apr-10

9072,33

6,50%

2895,43

44

Jun-10

9194

6,50%

2851,94

Jul-10

9094,45

6,50%

2977,06

Agust-10

9016,76

6,50%

3073,18

Sep-10

9020,84

6,50%

3335,58

Okt-10

8972,9

6,50%

3594,71

Nop-10

8983,29

6,50%

3670,61

Des-10

9067,62

6,50%

3667,8

Jan-11

9082,38

6,50%

3543,19

Feb-11

8957,11

6,75%

3449,74

Mar-11

8805,48

6,75%

3558,11

Apr-11

8694,3

6,75%

3749,2

Mei-11

8598,8

6,75%

3818,32

Jun-11

8607

6,75%

3805,4

Jul-11

8576,19

6,75%

4025,94

Agust-11

8574,79

6,75%

3936,35

Sep-11

8809,45

6,75%

3716,53

Okt-11

8939,67

6,50%

3600,4

Nop-11

9060,23

6,00%

3747,03

Des-11

8742,52

6,00%

3776,43

Jan-12

9154,76

6,00%

3930,84

Feb-12

9070,81

5,75%

3960,07

45

Apr-12

9221,5

5,75%

4162,22

Mei-12

9336,57

5,75%

4050,98

Jun-12

9498,14

5,75%

3850,55

Jul-12

9503,59

5,75%

4044,56

Agust-12

9547,16

5,75%

4114,76

Sep-12

9614,25

5,75%

4187,22

Okt-12

9645,14

5,75%

4309,68

Nop-12

9675,95

5,75%

4327,29

Des-12

9685,6

5,75%

4294,51

Jan-13

9735,57

5,75%

4403,12

Feb-13

9735,05

5,75%

4588,5

Mar-13

9758,11

5,75%

4823,16

Apr-13

9772,95

5,75%

4959,15

Mei-13

9809,91

5,75%

5100,44

Jun-13

9931

6,00%

4726,88

Jul-13

10123,7

6,50%

4631,38

Agust-13

10625,28

7,00%

4348,86

Sep-13

11402,95

7,25%

4353,64

Okt-13

11423,86

7,25%

4496,32

Nop-13

11652

7,50%

4359,72

46

Tabel pengujian Asumsi Klasik dan uji Hipotesis dengan program SPSS

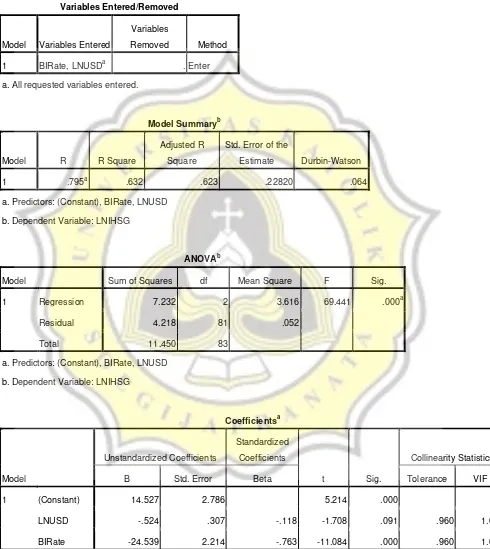

Variables Entered/Removed

Model Variables Entered

Variables

Removed Method

1 BIRate, LNUSDa . Enter

a. All requested variables entered.

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate Durbin-Watson

1 .795a .632 .623 .22820 .064

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: LNIHSG

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 7.232 2 3.616 69.441 .000a

Residual 4.218 81 .052

Total 11.450 83

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: LNIHSG

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig.

Collinearity Statistics

B Std. Error Beta Tolerance VIF

1 (Constant) 14.527 2.786 5.214 .000

LNUSD -.524 .307 -.118 -1.708 .091 .960 1.042

BIRate -24.539 2.214 -.763 -11.084 .000 .960 1.042

47

Coefficient Correlationsa

Model BIRate LNUSD

1 Correlations BIRate 1.000 -.200

LNUSD -.200 1.000

Covariances BIRate 4.901 -.136

LNUSD -.136 .094

a. Dependent Variable: LNIHSG

Collinearity Diagnosticsa

Model

Dimensi

on Eigenvalue Condition Index

Variance Proportions

(Constant) LNUSD BIRate

1 1 2.983 1.000 .00 .00 .00

2 .017 13.300 .00 .00 .97

3 3.958E-5 274.541 1.00 1.00 .03

a. Dependent Variable: LNIHSG

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value 7.2813 8.3381 7.9768 .29518 84

Residual -.50192 .60267 .00000 .22543 84

Std. Predicted Value -2.356 1.224 .000 1.000 84

Std. Residual -2.200 2.641 .000 .988 84

48

NPar Tests

One-Sample Kolmogorov-Smirnov Test

Unstandardized

Residual

N 84

Normal Parametersa,,b Mean .0000000

Std. Deviation .22543045

Most Extreme Differences Absolute .122

Positive .112

Negative -.122

Kolmogorov-Smirnov Z 1.117

Asymp. Sig. (2-tailed) .165

a. Test distribution is Normal.

b. Calculated from data.

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

Unstandardized Residual 84 -.50192 .60267 .0000000 .22543045

Valid N (listwise) 84

Variables Entered/Removed

Model Variables Entered

Variables

Removed Method

1 BIRate, LNUSDa . Enter

a. All requested variables entered.

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .760a .577 .567 .44515

a. Predictors: (Constant), BIRate, LNUSD

49

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 21.906 2 10.953 55.275 .000a

Residual 16.051 81 .198

Total 37.957 83

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: ABSZRES

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) -56.384 5.435 -10.375 .000

LNUSD 6.292 .599 .775 10.510 .000

BIRate -7.842 4.319 -.134 -1.816 .073

a. Dependent Variable: ABSZRES

Coefficient Correlationsa

Model BIRate LNUSD

1 Correlations BIRate 1.000 -.200

LNUSD -.200 1.000

Covariances BIRate 18.651 -.516

LNUSD -.516 .358

a. Dependent Variable: ABSZRES

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value .0676 2.2005 .7323 .51374 84

Residual -1.19521 .74524 .00000 .43975 84

Std. Predicted Value -1.294 2.858 .000 1.000 84

50

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value .0676 2.2005 .7323 .51374 84

Residual -1.19521 .74524 .00000 .43975 84

Std. Predicted Value -1.294 2.858 .000 1.000 84

Std. Residual -2.685 1.674 .000 .988 84

a. Dependent Variable: ABSZRES

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

Unstandardized Residual 84 -1.19521 .74524 .0000000 .43975232

Valid N (listwise) 84

Variables Entered/Removed

Model Variables Entered

Variables

Removed Method

1 BIRate, LNUSDa . Enter

a. All requested variables entered.

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .441a .195 .175 .47979

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: ABSZRES2

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 4.511 2 2.256 9.799 .000a

Residual 18.646 81 .230

Total 23.157 83

a. Predictors: (Constant), BIRate, LNUSD

51

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) -20.413 5.858 -3.485 .001

LNUSD 2.429 .645 .383 3.764 .000

BIRate -14.127 4.655 -.309 -3.035 .003

a. Dependent Variable: ABSZRES2

Coefficient Correlationsa

Model BIRate LNUSD

1 Correlations BIRate 1.000 -.200

LNUSD -.200 1.000

Covariances BIRate 21.666 -.600

LNUSD -.600 .416

a. Dependent Variable: ABSZRES2

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value .3861 1.3671 .8440 .23314 84

Residual -1.03701 1.71009 .00000 .47397 84

Std. Predicted Value -1.964 2.244 .000 1.000 84

Std. Residual -2.161 3.564 .000 .988 84

a. Dependent Variable: ABSZRES2

Variables Entered/Removed

Model Variables Entered

Variables

Removed Method

52

Variables Entered/Removed

Model Variables Entered

Variables

Removed Method

1 BIRate, LNUSDa . Enter

a. All requested variables entered.

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .441a .195 .175 .47979

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: ABSZRES2

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 4.511 2 2.256 9.799 .000a

Residual 18.646 81 .230

Total 23.157 83

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: ABSZRES2

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) -20.413 5.858 -3.485 .001

LNUSD 2.429 .645 .383 3.764 .000

BIRate -14.127 4.655 -.309 -3.035 .003

53

Coefficient Correlationsa

Model BIRate LNUSD

1 Correlations BIRate 1.000 -.200

LNUSD -.200 1.000

Covariances BIRate 21.666 -.600

LNUSD -.600 .416

a. Dependent Variable: ABSZRES2

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value .3861 1.3671 .8440 .23314 84

Residual -1.03701 1.71009 .00000 .47397 84

Std. Predicted Value -1.964 2.244 .000 1.000 84

Std. Residual -2.161 3.564 .000 .988 84

a. Dependent Variable: ABSZRES2

Variables Entered/Removed

Model Variables Entered

Variables

Removed Method

1 BIRate, LNUSDa . Enter

a. All requested variables entered.

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .314a .098 .076 .53915

a. Predictors: (Constant), BIRate, LNUSD

54

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 2.536 2 1.268 4.362 .016a

Residual 23.254 80 .291

Total 25.790 82

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: ABSZRES3

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) -6.472 6.798 -.952 .344

LNUSD .903 .747 .130 1.209 .230

BIRate -15.130 5.322 -.305 -2.843 .006

a. Dependent Variable: ABSZRES3

Coefficient Correlationsa

Model BIRate LNUSD

1 Correlations BIRate 1.000 -.146

LNUSD -.146 1.000

Covariances BIRate 28.326 -.582

LNUSD -.582 .558

a. Dependent Variable: ABSZRES3

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value .3210 .9550 .7297 .17586 83

Residual -.75783 1.45509 .00000 .53253 83

Std. Predicted Value -2.324 1.281 .000 1.000 83

Std. Residual -1.406 2.699 .000 .988 83

55

NPar Tests

One-Sample Kolmogorov-Smirnov Test

Unstandardized

Residual

N 83

Normal Parametersa,,b Mean .0000000

Std. Deviation .53253281

Most Extreme Differences Absolute .085

Positive .085

Negative -.077

Kolmogorov-Smirnov Z .779

Asymp. Sig. (2-tailed) .579

a. Test distribution is Normal.

b. Calculated from data.

Descriptives

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

Unstandardized Residual 83 -.75783 1.45509 .0000000 .53253281

Valid N (listwise) 83

Regression

Variables Entered/Removed

Model Variables Entered

Variables

Removed Method

1 BIRate, LNUSDa . Enter

56

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .267a .071 .048 .57798

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: ABSZRES4

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 2.044 2 1.022 3.059 .052a

Residual 26.725 80 .334

Total 28.769 82

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: ABSZRES4

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) -12.878 7.288 -1.767 .081

LNUSD 1.571 .801 .214 1.962 .053

BIRate -10.135 5.706 -.194 -1.776 .079

a. Dependent Variable: ABSZRES4

Coefficient Correlationsa

Model BIRate LNUSD

1 Correlations BIRate 1.000 -.146

LNUSD -.146 1.000

Covariances BIRate 32.554 -.669

LNUSD -.669 .641

57

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value .4818 1.1363 .8008 .15786 83

Residual -1.05542 2.06697 .00000 .57089 83

Std. Predicted Value -2.021 2.125 .000 1.000 83

Std. Residual -1.826 3.576 .000 .988 83

a. Dependent Variable: ABSZRES4

NPar Tests

One-Sample Kolmogorov-Smirnov Test

Unstandardized

Residual

N 83

Normal Parametersa,,b Mean .0000000

Std. Deviation .57089160

Most Extreme Differences Absolute .094

Positive .094

Negative -.057

Kolmogorov-Smirnov Z .859

Asymp. Sig. (2-tailed) .451

a. Test distribution is Normal.

b. Calculated from data.

Regression

Variables Entered/Removed

Model Variables Entered

Variables

Removed Method

1 BIRate, LNUSDa . Enter

58

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate Durbin-Watson

1 .267a .071 .048 .57798 1.456

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: ABSZRES4

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 2.044 2 1.022 3.059 .052a

Residual 26.725 80 .334

Total 28.769 82

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: ABSZRES4

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig.

Collinearity Statistics

B Std. Error Beta Tolerance VIF

1 (Constant) -12.878 7.288 -1.767 .081

LNUSD 1.571 .801 .214 1.962 .053 .979 1.022

BIRate -10.135 5.706 -.194 -1.776 .079 .979 1.022

a. Dependent Variable: ABSZRES4

Coefficient Correlationsa

Model BIRate LNUSD

1 Correlations BIRate 1.000 -.146

LNUSD -.146 1.000

Covariances BIRate 32.554 -.669

LNUSD -.669 .641

59

Collinearity Diagnosticsa

Model

Dimensi

on Eigenvalue Condition Index

Variance Proportions

(Constant) LNUSD BIRate

1 1 2.984 1.000 .00 .00 .00

2 .016 13.501 .00 .00 .98

3 3.767E-5 281.444 1.00 1.00 .01

a. Dependent Variable: ABSZRES4

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value .4818 1.1363 .8008 .15786 83

Residual -1.05542 2.06697 .00000 .57089 83

Std. Predicted Value -2.021 2.125 .000 1.000 83

Std. Residual -1.826 3.576 .000 .988 83

a. Dependent Variable: ABSZRES4

Regression

Variables Entered/Removed

Model Variables Entered

Variables

Removed Method

1 BIRate, LNUSDa . Enter

a. All requested variables entered.

Model Summary

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .795a .632 .623 .22820

60

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 7.232 2 3.616 69.441 .000a

Residual 4.218 81 .052

Total 11.450 83

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: LNIHSG

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) 14.527 2.786 5.214 .000

LNUSD -.524 .307 -.118 -1.708 .091

BIRate -24.539 2.214 -.763 -11.084 .000

a. Dependent Variable: LNIHSG

Coefficient Correlationsa

Model BIRate LNUSD

1 Correlations BIRate 1.000 -.200

LNUSD -.200 1.000

Covariances BIRate 4.901 -.136

LNUSD -.136 .094

a. Dependent Variable: LNIHSG

Regression

Variables Entered/Removed

Model Variables Entered

Variables

Removed Method

1 BIRate, LNUSDa . Enter

61

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate Durbin-Watson

1 .781a .609 .599 .22896 .065

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: LNIHSG

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 6.539 2 3.269 62.370 .000a

Residual 4.194 80 .052

Total 10.733 82

a. Predictors: (Constant), BIRate, LNUSD

b. Dependent Variable: LNIHSG

Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig.

Collinearity Statistics

B Std. Error Beta Tolerance VIF

1 (Constant) 14.035 2.887 4.861 .000

LNUSD -.473 .317 -.105 -1.490 .140 .979 1.022

BIRate -24.255 2.260 -.758 -10.731 .000 .979 1.022

a. Dependent Variable: LNIHSG

Coefficient Correlationsa

Model BIRate LNUSD

1 Correlations BIRate 1.000 -.146

LNUSD -.146 1.000

Covariances BIRate 5.108 -.105

LNUSD -.105 .101

62

Collinearity Diagnosticsa

Model

Dimensi

on Eigenvalue Condition Index

Variance Proportions

(Constant) LNUSD BIRate

1 1 2.984 1.000 .00 .00 .00

2 .016 13.501 .00 .00 .98

3 3.767E-5 281.444 1.00 1.00 .01

a. Dependent Variable: LNIHSG

Residuals Statisticsa

Minimum Maximum Mean Std. Deviation N

Predicted Value 7.3731 8.3334 7.9870 .28239 83

Residual -.51700 .58943 .00000 .22615 83

Std. Predicted Value -2.174 1.227 .000 1.000 83

Std. Residual -2.258 2.574 .000 .988 83

a. Dependent Variable: LNIHSG

Descriptives

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

LNUSD 83 9.06 9.40 9.1641 .08060

BIRate 83 .0575 .0950 .070783 .0113086

Valid N (listwise) 83

Descriptives

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

IHSG 84 1255 5100 3103.18 1044.915

Kurs USD 84 8574 12147 9606.05 846.975

BI Rate 84 .0575 .0950 .071071 .0115467