It is a great pleasure to prepare an internship report on Jamuna Bank Ltd SME Loan. Vice President for allowing me to work at Jamuna Bank Limited, Motijheel Foreign Exchange Branch. I would like to express my gratitude to the SME Banking division of Jamuna Bank Ltd for providing valuable information, especially Ms.

Jamuna Bank Ltd is currently highly motivated to increase the bank's SME exposure.

List Of Tables

Chapter: 1

INTRODUCTION

- ORIGIN OF THE REPORT

- Objectives of the Report

- Significance of the Report

- Scope of the Report

- Methodology of the Report

- DATA REQUIREMENTS & ANALYSIS METHOD

- DATA SOURCES

The general objective of this report is-“To explore SME Banking in Jamuna Bank Ltd”. In this study, a conceptual study of the SME financing of Jamuna Bank Limited has been carried out. A survey has been conducted to find out the owners' views on the SME service provided by Jamuna Bank Ltd.

This study covers the aspect of SME credit management policy of Jamuna Bank Ltd and will try to find the performance of Jamuna Bank Ltd in the SME sector as compared to other banks.

Secondary Source

Limitation of the Report

Time constraint is also one of the main reasons, so more detailed study was not possible.

Chapter: 2 Literature Overview

- BANGLADESH-AN OVERVIEW

- CONTRIBUTION OF SME IN THE NATIONAL ECONOMY OF BANGLADESH The importance of SMEs in Bangladesh economy is precluded by non-availability of

- CHARACTERISTICS OF ENTREPRENEUR ON THE SUCCESS OF SME Characteristics of entrepreneur play an important role on ensuring the business success in

- DEMOGRAPHIC CHARACTERISTICS

- INDIVIDUAL CHARACTERISTICS

- PERSONAL TRAITS

- ENTREPRENEURIAL ORIENTATION

- KEY SUCCESS FACTORS & OBSTACLES IN SME

- REASONS FOR BANK'S RELUCTANCE IN SME FINANCING

- Fiscal and Financial Incentives Support for SME’s By Government

- Financing and Other Related Limitations to SME Development in Bangladesh

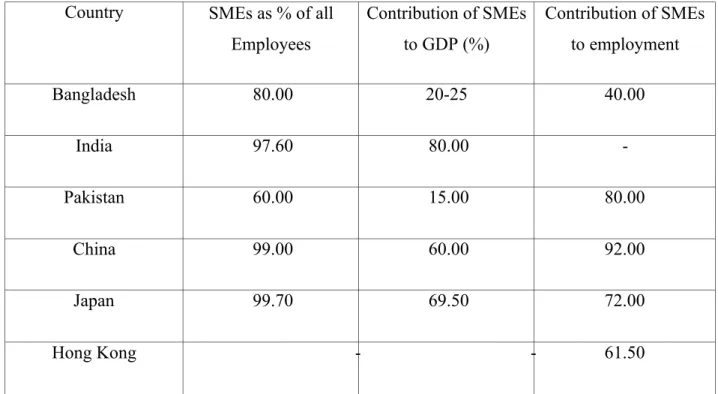

Consequently, the performance of SMEs is closely linked to the performance of the country. Some of the world's best-performing economies, especially Taiwan and Hong Kong, are heavily based on small businesses. Small business success is often classified into different categories, such as the individual characteristics of the owner, business characteristics, environmental characteristics, etc.

The sources that produce diversity lie in the variance of entrepreneurs' backgrounds, motives, and goals.

Resource Scarcity

In addition to institutional and policy support for finance, the government also provides a range of fiscal and financial support to the industrial sector including SMEs. Businesses that export 80% or more of goods or services qualify for duty-free importation of machinery and spare parts. Several financing and other related problems have been found which are the main barriers for the development of SMEs in Bangladesh.

High Employee Turnover

Absence of modern technology

Poor physical infrastructure

Financial Limitations

Lack of modern technology

Lack of Entrepreneurship Skills

Lack of information

Bureaucracy

Chapter: 3 ORGANIZATION OVERVIEW

- History of Jamuna Bank Ltd

- JBL’s Corporate Vision, Mission and Objectives

- Corporate Vision

- Corporate Mission

- Corporate Objectives

- ETHICAL PRACTICES

- STRATEGIES OF JBL

- Board of Directors

- SME Banking of Jamuna Bank Ltd

- Purpose of SME Loan i) Working capital

- SME Exposure Limit

The bank is managed and operated by a group of highly educated and professional teams with diverse experiences in finance and banking. A team of highly qualified and experienced professionals headed by the Bank's Managing Director, who has extensive banking experience runs the bank and is headed by an efficient Board of Directors for policy making. The sincere and hands-on involvement of the best management team in all tires of the Bank has brought out the best from the Bank.

The bank has already ranked at the top of the quality service providers and is known for its reputation. With a comprehensive range of financial products and services, the bank is committed to providing high quality financial services to its valued customers. In addition, considering its upcoming future, the bank's infrastructure is being upgraded whenever deemed necessary.

JBL's corporate vision is to become a leading banking institution and play a significant role in the development of the country. The bank is committed to satisfy the diverse needs of its customers through a collection of services at a competitive price by using appropriate technology and delivering on time so that sustainable growth, reasonable returns and contribution to the development of the country can be ensured with a motivated and professional workforce. To remain one of the best banks in Bangladesh in terms of profitability and asset quality.

Increase direct contact with customers to cultivate a closer relationship between the bank and the customer. The board of directors consists of 17 (seventeen) members and of which 16 members are elected by the shareholders and the remaining one is the Managing Director who is appointed the Chief Executive Officer of the bank.

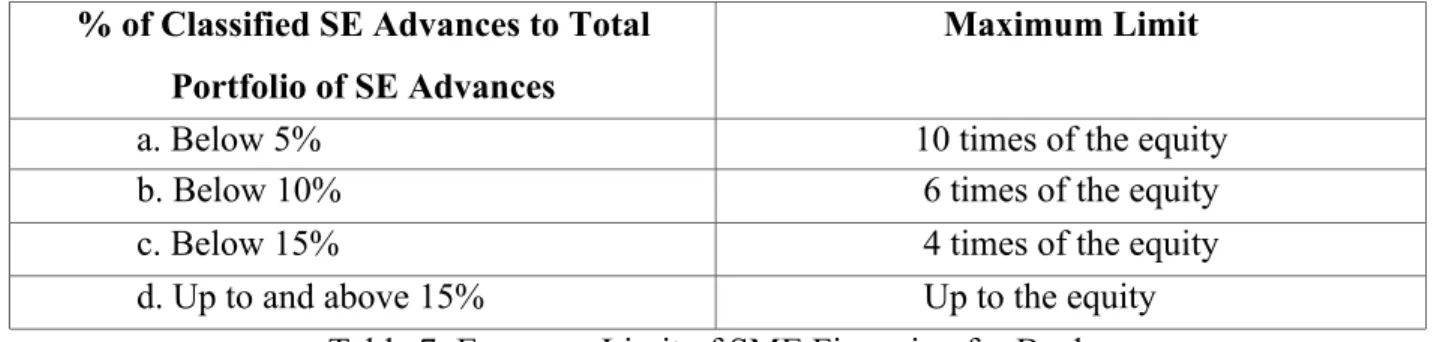

Maximum Exposure

Loan Pricing For small enterprises

Loan processing fee

For overdue: Penal interest shall be charged @ 3% on the overdue amount 3) Other fees & charges

- Period of Loan

- Mode of Repayment

- Security for the Loan Facility

- Documents Required for the Loan Facility

- Dedicated SME Branches in JBL

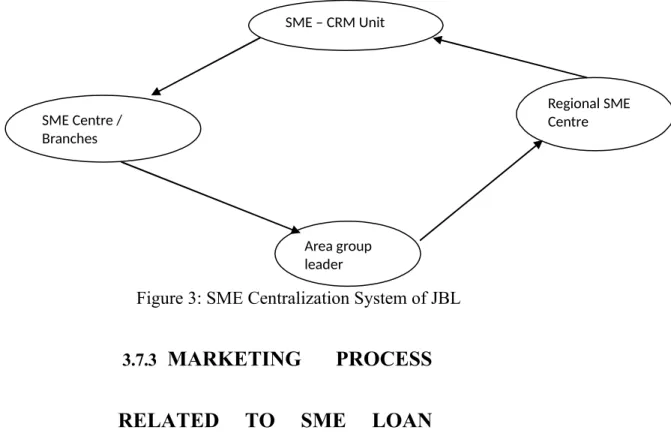

- Structure of SME Division

- TYPES OF SME LOAN IN JAMUNA BANK )LTD

- Criteria and Conditions of SME loan

- Selection Criteria of Potential Enterprise of SME Enterprise Selection Criteria

A written statement obtained from the borrower disclosing details of various facilities already obtained from other institutions. Copy of the memorandum and articles of association of the company including certificate of incorporation duly certified by the Registrar Joint Stock Companies (RJSC) and attested by the managing director accompanied by an up-to-date list of directors (if applicable). Copy of the company's board resolution to use credit facilities and authorization of the managing director/chairman/director to execute documents and operate the accounts (if relevant).

The business must be environmentally friendly (Ex: Not a drug or tobacco business) - The business must be legally registered, i.e. valid trade licence, income tax or VAT registration, wherever to be implemented. The business should ideally be located near the market and source of its raw materials/suppliers.

Entrepreneur Selection Criteria

Guarantor Selection Criteria

Processing and Screening of Loan Proposal

After sanctioning the proposal, the SME-CRM unit sends the loan file to the respective SME Center for disbursement. After completion of all the documentation formalities as per sanction, the center will disburse the loan through their respective branches after getting the disbursement authority from the Credit Administration Division (CAD) and reporting it to the “SME Banking Division” at Central Office.

- TARGET MARKETING

- MARKET POSITIONING

- DEVELOPING MARKETING MIX

Psychographic Segmentation: In terms of SME loan, customers are different in attitudes, interests and activity as some are time constrained and some are cash constrained. So the bank always tries to focus these things and then give the customers very carefully the loan. Behavioral segmentation: In terms of SME loan, there would be few customers who are highly educated such as graduates or postgraduates.

In the current scenario in Bangladesh, the highly educated people are not attracted to SME loans. There are too many different types of customers with too many different kinds of needs. Since the loan disbursement sectors are different, there are different pre- and post-loan disbursement strategies.

The marketing staff are very customer friendly and the loan processing system has been made as simple as possible. Rescheduling System - After taking SME loans, if a customer faces any problem in repaying the loan, then the rescheduling process is made for the convenience of the customer. Prompt Service - The main facility of SMEs is to provide prompt service to the customers.

Product: With a view to the SME loan, JBL has 2 types of loans: Short-term loan and medium-term loan. Price: In terms of SME loans, JBL receives a certain amount of processing fees and stamp fees for providing a loan to the customer.

Chapter: 4 DATA COLLECTION

AND ANALYSIS

- AGE LIMIT OF THE CLIENTS

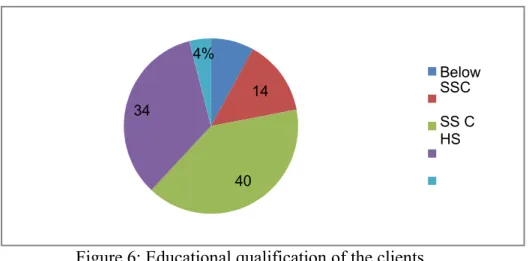

- EDUCATIONAL QUALIFICATION OF THE CLIENTS

- DIFFERENT CATEGORIES OF BUSINESS

- BUSINESS EXPERIENCE OF THE PROPRIETORS

- MAJOR USE OF THE SME LOAN

- MOST COMMON BUSINESS OBSTACLES

- MAIN REASONS BEHIND HIGH EMPLOYEE TURNOVER

For SME banks in Bangladesh, it would be risky to give loans to customers above 60 years of age and the JBL SME authority also discourages lending to owners above 60 years of age. In the survey, it was found that commercial concern is the main part of the interviewed SME owners. From the answers received, it can be seen that the loan is mainly used for the purchase of raw materials.

These options were predetermined and the owners were asked to choose one of these options. When reviewing the literature, it was found that SME concerns are characterized by high employee turnover due to low growth. We asked the owners about the main reason for frequent employee job changes and they answered the following 4 reasons: a.

48% of respondents stated that a higher salary is the main motivating factor for employees when changing jobs. 10% answered that employees change jobs due to a change in the working environment, and 18% answered that the main reason for changing jobs is problems with colleagues.

WAITING PERIOD BETWEEN LOAN APPLICATION AND SANCTION

- SATISFACTION LEVEL ON THE SERVICE OF JBL SME

- DETERMINATION OF PROBLEMS FACED BY BANK

- LOANS AND ADVANCE POSITION OF JAMUNA BANK LTD

- PERFORMANCE OF JAMUNA BANK LTD IN SME SECTOR

- PERCENTAGE OF SME LOAN TO TOTAL LOAN OF JBL

- PERFORMANCE COMPARISON OF JBL WITH , OTHER BANKS IN SME SECTOR

- YEARWISE SME DISBURSEMENT OF DIFFERENT BANKS

- ACHIEVEMENT OF SME TARGET GIVEN BY BANGLADESH BANK

- SWOT ANALYSIS OF SME DIVISION OF JAMUNA BANK LTD

Interviews with SME bankers revealed some problems or risks faced by the bank in the management of SMEs. Jamuna Bank Ltd (JBL) has been one of the best private banks in the financial sector. So it can be said that the Basic Bank has spent more money in the SME sector from their loan portfolio.

A large part of the loan in the SME sector is also given by private banks from the total loan amount. The private bank has also given a large share of credit to the SME sector out of their total loan amount. In all 3 years of this analysis, it is observed that the summary of disbursed credit to SMEs by 3 government banks (Sonali, Janata and Basic) is much more than private banks (Jamuna, Pubali and SCB).

The target amount of Pubali Bank was Tk 500 crore and their total disbursement was Tk 247 crore and their realization rate was 49.60%. Standard Charted Bank's target amount was tk 550 crore and their total disbursement was tk 496 crore and their achievement rate was 90%. The target amount of Pubali Bank was Tk 250 crore and their total disbursement was Tk 144.68 crore and their realization rate was 57.87%.

Standard Charted Bank's target amount was Tk 899.30 crore, their total disbursement was Tk 710.03 crore and their hit rate was 78.95%. Standard Charted Bank's target amount was Tk 899.30 crore and their total disbursement was Tk 515.03 crore and their achievement rate was 57.27%.

Strengths

Weakness

Opportunities

Threats

Chapter: 5 FINDINGS

From The data collection the following things are found

Chapter: 6 RECOMMENDATIONS

The SME interest rate should be made more competitive in order to expand the SME portfolio. The loan documentation process must be more effective to reduce collateral risk and loan default. The JBL authority should provide adequate training to their SME officers so that they can take on new SME clients and credit analysts should also be recruited to reduce the pressure on existing employees.

Chapter: 7 CONCLUSIONS

As a third generation private commercial bank, Jamuna Bank Ltd. a good opportunity to be a leading bank in Bangladesh economy. In recent years, their performance in the SME sector compared to other banks is not so much satisfactory, but they showed a regular growth from 2009 to 2011. This means that they have the opportunity to be one of the best banks in the SME sector -sector.

SMEs are a successful sector in Bangladesh which can be important for all banks in the near future. That is why, to keep up with other banks in Bangladesh, Jamuna Bank Ltd. JBL) should know the problems of the future customers of SMEs and try to find the best possible way which will create good connection with their new customers and achieve their goals.