commit to user

ANTECEDENTS OF BUDGETARY PARTICIPATION:

ENHANCING EMPLOYEES’ JOB PERFORMANCE

THESIS

A thesis submitted in partial fulfillment of the requirement for the degree of Magister Sains

by :

FATMAWATI NIKMAH

NIM: S 4307067

FAKULTAS EKONOMI UNIVERSITAS SEBELAS MARET

commit to user

ANTECEDENTS OF BUDGETARY PARTICIPATION:

ENHANCING EMPLOYEES’ JOB PERFORMANCE

By:

commit to user

ANTECEDENTS OF BUDGETARY PARTICIPATION:

ENHANCING EMPLOYEES’ JOB PERFORMANCE

By:

commit to user

STATEMENT

Name : Fatmawati Nikmah

NIM : S4307067

Study Program : Master of Accounting

Main Interest : Public Sector Accounting

I declared truthfully that this thesis entitled “Antecedent Budgetary

Participation: Enhancing Employees’ Job Performance” is originally made by the researcher. The things related to other people’s works are signed as citation

commit to user

DEDICATION

My Parents,

Thank’s for the love and support... You give me strength and brave to face the world

My Brothers and Sister, Thank you for your support and suggestion...

All of my friends,

commit to user

MOTTO

· All our dreams can come true, if we have the courage to pursue them....

· Trust in God, everything will be okey...

commit to user

ACKNOWLEDGEMENT

Assalaamu’alaikum Wr. Wb.

Alhamdulillah, Researcher thanks to presence of ALLAH SWT for the

overflows of blesses, grants, and guides so that Researcher able to finish this

thesis well. This thesis is compiled to equip the duties and fulfill the preconditions

to get the Master of Science degree in Faculty of Economics, University of

Sebelas Maret Surakarta.

Researcher realizes that during the thesis process, there are many helps

from other parties, directly and indirectly. Herewith, Researcher says many thanks

to various the following parties:

1. Minister of National Education of Indonesian Republic, for the willingness to

give grants in the form of scholarship “Beasiswa Unggulan Diknas”, in order

to complete the study in Master of Accounting Study Program, Faculty of

Economic, University of Sebelas Maret Surakarta.

2. Prof. Dr. Bambang Sutopo, M.Com., Ak., as The Dean of Faculty of

Economics, University of Sebelas Maret Surakarta and also as the main

counselor, thank you for all the guidance, inspiration, help, motivation,

critique, and suggestion that help the researcher to achieve the best result.

3. Mr. Bandi, Dr., M.Si,Ak, as The Head of Master of Accounting Program,

Faculty of Economics, University of Sebelas Maret Surakarta. Thank you for

give me the chance to study in MAKSI. I am happy to be part of MAKSI’s

commit to user

4. Christiyaningsih Budiwati, S.E., M.Si, Ak, as the co-supervisor, for all the

guidance, help, motivation, critique, and suggestion that help the researcher to

finish this thesis. Thank you very much for your kindness and help. Without

your guidance, I can’t finish my thesis research.

5. Dra. Y. Anni Aryani, M. Prof. Acc., Ph.D., Ak and Drs. Muhammad Agung

Prabowo, M.Si.,Ph.D., Ak.as the examiners, thank you for the critique and

suggestions.

6. Drs. Hasan Fauzi, MBA. Ak, for opening the gate for me to study in this

faculty by accepting me in MAKSI International Class. I also want to say my

deeply thanks and appreciation for all your guidance, support, and motivation

during study in MAKSI.

7. Mr. Doddy Setiawan, S.E., M.Si., IMRI., Ak., Thank you for give me the

chance to study in MAKSI. I am happy to be part of MAKSI’s family.

8. The officials of Local Government of Surakarta who fill the questionnaires,

Thank you for the time, help, guidance and being my respondent.

9. Admission Staff, in Economics Faculty, University or Sebelas Maret

Surakarta thanks you for helping me to finish my study.

10. My family. Thank you for helping me doing my research and supporting me to

finish my study.

11. My best friends, Lisa, Mulia Dewi, Eny Ellyanora, thanks for the friendship.

commit to user

12. All of MAKSI’s students that I couldn’t write one by one. Hope this moment

will be our memorable moment for us. I love you all guys and I hope we can

walk together and still be Friendship.

Researcher realizes that this thesis is a long way off from perfection.

Hence, researcher expects all the constructive suggestion and criticism regarding

the content, grammar, or any other. Finally, researcher wants to apologize if there

are mistake and weakness in this thesis.

Wassalamu’alaikum. Wr. Wb.

Surakarta, May 2010

Regards,

commit to user

TABLE OF CONTENT

Page

APPROVAL PAGE ... ii

STATEMENT ... iv

DEDICATION PAGE... v

MOTTO PAGE ... vi

ACKNOWLEDGEMENT ... vii

TABLE OF CONTENT ... x

LIST OF TABLE ... xiii

LIST OF FIGURE... xiv

LIST OF APPENDIX ... xv

ABBREVIATIONS ... xvi

ABSTRACT... xvii

CHAPTER I. INTRODUCTION... 1

A. Research Background... 1

B. Problem Statement ... 5

C. Research Purpose ... 6

D. Research Benefits ... 6

CHAPTER II. LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT ... 7

A. Literature Review... 7

1. Budgeting Process in Local Government... 7

commit to user

3. Need For Achievement ... 13

4. Work Attitudes ... 17

5. Employees’ Job Performance... 21

6. Need for achievement, work attitude and job performance ... 23

B. Hypothesis Development ... 24

1. Need For Achievement and Budgetary Participation... 24

2. Work Attitudes and Budgetary Participation ... 26

3. Budgetary Participation and Employee’s Job Performance ... 27

C. Conceptual Schema ... 28

CHAPTER III. RESEARCH METHOD ... 30

A. Research Design... 30

B. Population, Sample, and Sampling Technique... 30

C. Data Collection... 31

D. Variables and Operasional Definitions ... 32

E. Analysis Technique ... 34

1. Descriptive Statistic ... 35

2. Validity and Reliability Test ... 35

3. Hypotheses testing ... 36

CHAPTER IV. DATA ANALYSIS AND DISCUSSION ... 39

A. Data Description... 39

1. Sample Selection... 39

commit to user

B. Reliability Test ... 41

C. Validity Test ... 42

D. Classic Assumption Analysis ... 43

E. Hypothesis Testing... 48

CHAPTER V. CONCLUSION AND RECOMMENDATION... 59

A. Conclusion... 59

B. Implications ... 60

C. Research Limitations... 60

D. Suggestions... 61

REFFERENCES ... 62

commit to user

LIST OF TABLE

page

Table 1 The amount of SKPD in Local Government of Surakarta... 31

Table 2 Questionnaire Description ... 40

Table 3 Descriptive Statistic of the Variables ... 41

Table 4 Reliability Result ... 42

Table 5 Validity Result ... 43

Table 6 Multicollinearity test result... 44

Table 7 Multicollinearity test result... 44

Table 8 Result of One-Sample Kolmogorov-Smirnov test... 47

Table 9 Result of One-Sample Kolmogorov-Smirnov test... 47

Table 10 Pearson correlation matrix ... 49

Table 11 Results of regression analysis using equation (1)... 50

(Dependent variable: Budgetary Participation) Table 12 Results of regression analysis using equation (2)... 51

commit to user

LIST OF FIGURE

Page

Figure 1 Local Government Budgeting Arrangement Cycle ... 10

Figure 2 Conceptual schema ... 29

Figure 3 Scatterplot Graphic ... 45

Figure 4 Scatterplot Graphic ... 46

commit to user

LIST OF APPENDIX

Page

APPENDIX I. Reliability test ... 67

APPENDIX II. Validity test ... 76

APPENDIX III. Multicolinearity test ... 86

APPENDIX IV. Heteroskedasticity ... 90

APPENDIX V. Normality test ... 96

APPENDIX VI. Regression test... 103

APPENDIX VII. Result of T-Test... 107

APPENDIX VIII. Regression Analysis for two sub samples ... 109

commit to user

ABBREVIATIONS

APBD : Anggaran Pendapatan dan Belanja Daerah

DPRD : Dewan Perwakilan Rakyat Daerah

KUA : Kebijakan Umum Anggaran

PPAS : Prioritas dan Plafon Anggaran Sementara

RAPBD : Rencana Anggaran Pendapatan dan Belanja Daerah

RKA : Rencana Kerja dan Anggaran

RPJPD : Rencana pembangunan Jangka Panjang Daerah

RPJMD : Rencana Pembangunan Jangka Menengah Daerah

RKPD : Rencana kerja Pemerintah Daerah

SKPD : Satuan Kerja Perangkat Daerah

commit to user

ABSTRACT

FATMAWATI NIKMAH NIM: S 4307067

ANTECEDENTS OF BUDGETARY PARTICIPATION: ENHANCING EMPLOYEES’ JOB PERFORMANCE

This research investigated the antecedent budgetary participation (need for achievement and work attitude), then assess the impact on employees’ job performance.

The data were obtained using questionnaires that distributed to respondents. Seventy two respondents were chosen as samples and path analysis was used as techniques to analyze the data.

The result of this research showed that need for achievement has significant positive association with budgetary participation. However, the result found that there is no significant association between work attitude and budgetary participation. Furthermore, the researcher found that budgetary participation had a significant positive association with job performance (e.i managerial performance). The researcher concludes that when employees have a higher need for achievement, they will tend to higher participation in budgetary process, and this condition will enhance employees’ job performance. Here, budgetary participation acted as mediating variable between need for achievement and job performance.

commit to user

Penelitian ini bertujuan untuk meneliti variabel anteseden dari partisipasi anggaran (kebutuhan berprestasi dan sikap kerja), kemudian menilai pengaruhnya terhadap kinerja pegawai.

Data pada penelitian ini didapatkan dari kuesioner yang telah disebarkan kepada responden. Tujuh puluh dua responden digunakan sebagai sampel dan analisis jalur (path analysis) digunakan untuk menganalisa data.

Hasil dari penelitian ini menunjukkan bahwa variabel kebutuhan berprestasi mempunyai hubungan positif yang signifikan terhadap partisipasi anggaran. Namun demikian, hasil penelitian menemukan tidak ada hubungan yang signifikan antara sikap kerja dengan partisipasi anggaran. Selanjutnya, peneliti menemukan bahwa partisipasi anggaran mempunyai hubungan positif yang signifikan terhadap kinerja pegawai (kinerja managerial). Peneliti menyimpulkan bahwa ketika mempunyai kebutuhan berprestasi yang tinggi, maka mereka cenderung mempunyai partisipasi yang tinggi dalam proses penganggaran, dan hal ini akan meningkatkan kinerja pergawai. Dalam hal ini, partisipasi anggaran sebagai variabel mediasi/perantara antara variabel kebutuhan berprestasi dengan kinerja pegawai.

commit to user

CHAPTER I

INTRODUCTION

A. Research Background

Budgeting in public sector organization is political process. Thus, budget

is an accountability instrument for public funding management and

implementation of programs which cost by public fund (Mardiasmo 2005). In

other words, public budgeting can be defined as financial condition of

organization that includes revenue, expenditure, and activities (Ompusunggu and

Bawono 2006).

Public sector budgeting is related with the process to decide the amount of

fund allocation for each program and activity in monetary unit, which using public

fund (Sardjito and Muthaher 2007). The stage of budgeting process is important,

because ineffective budget which is not performance-based oriented, will make

the predetermined planning can be failed. Budget is managerial plan for action to

facilitate the organization to achieve its goals (Rahayu, Ludigdo, and Affandi

2007).

Budget is a tool for government to direct the social-economy development,

to assure continuity, and improve the quality of society life (Mardiasmo 2005). In

order to obtain a good outcome of local government budget for society, the

participation of stakeholder in budgetary process is needed. Budgetary

participation in public sector occurred when among legislative, executive, and

commit to user

government which the proposal come from institution units that made by manager

unit. After thus, the draft of local government budget will be established by

executive with local government legislative (DPRD) based on the government

regulation (Halim 2007).

Local Government Budget (APBD) comes into arrangement relied on

performance approach, particularly pertained to a budget system focusing on

output achievement from pre-determined cost or input allocations. Regarding to

this performance approach, APBD must be targeted into objective achieved for

one budget year. Based on the Minister of Domestic Affair’s Regulation No.

13/2006 that covered the standard of local government budget draft formulation,

the proposal of local government budget arranged by executive budget team and

local government institution units (Satuan Kerja Perangkat Daerah/SKPD). Here,

the each manager unit (SKPD) has an important role for compiling the

program-related budget form their own unit as a part of the whole local government

budgeting (APBD). Thus, in performance-based budgeting process, each

institution unit should be involved in budgeting process; it means more employees

have allowed participating in budgetary activities.

Thompson as cited in Williams et al. (1990) challenged researchers to

examine budgetary behavior in such public sector organizations, as the budgetary

behavior may be different in these organizations compared to the behavior in

profit-making and less bureaucratic organizations. Similarly, Williams et al.

(1990) suggested that future budgetary participation and performance research in

commit to user

behavior factors which apply with equal facility to both sectors, but that particular

combinations dominate depending on the state of other organizational variables.

Moreover, the budgetary behavior in public sector organizations in the developed

countries might be different from what is observed in developing countries.

Furthermore, many of the prior studies on the budgetary participation and

performance relationship have produced conflicting results. Empirical evidence on

the relationship between budgetary participation and performance has been

offered by several researchers. Some studies have found a positive relationship

between budgetary participation and job performance (Nouri&Parker 1998;Yuen

2007;Yahya et al 2008). Other studies have suggested that there is a weak positive

relationship (Milani, 1975), or even a negative relationship (Kenis, 1979),

between the two factors. The other research conducted by Sardjito and Muthaher

(2007) showed that budget participation had direct effect on managerial

performance which there is positive relationship between budgetary participation

and manager performance in local government.

These mixed results indicate that no simple relationship exists between

budgetary participation and job performance, and suggest that there could be other

variables involved. Such inconsistent findings have prompted several researchers

to examine the antecedent variables that affect job performance indirectly during

budgetary participation. However, study of public-sector organizations remains

scanty. It is therefore necessary to extend the study of the complex relationship

between budgetary participation and performance to include an examination of the

commit to user

developing appropriate accounting-based planning and control systems that

facilitate effective budgetary development (Yuen 2007).

Shields and Shields (1998) have suggested that it is important not only to

understand the consequences of participative budgeting, but also to investigate its

antecedents. The current study has selected two factors as potential antecedent

variables: (1) need for achievement; and (2) work attitudes. However, previous

studies of budgeting and performance (Milani 1975; Steers 1975; Alam and Mia

2006) have identified job attitude among employees and need for achievement can

be represent as variables in the job performance.

According to Yuen (2007) who conducted the research about the

antecedent of budgetary participation in the context of public sector organization

in Macau, found that the two antecedent factors - a need for achievement and

work attitude - have a significant positive relationship with budgetary

participation, and concluded that indirect relationship exist between those two

antecedent factors and the dependent variable (job performance) with budgetary

participation as an intervening variable. From those result, this study wants to

adapt that research in public sector organization especially in the budgeting

process in Local Government’s Surakarta. As the recent public sector reforms

have also included a move towards decentralization to improve efficiency and

performance therefore budgetary processes in the local government have been

more participative. Since the autonomy regulation declared in 1999 and revised by

Law No.32/2004, each local government should be more independence including

commit to user

Government Budget (Anggaran Pendapatan dan Belanja Daerah/APBD) comes

into arrangement relied on performance approach, where each institution unit

(SKPD) should be involved in budgeting process. It explicitly in Minister of

Domestic Affair’s Regulation No.16/2006 which mandated that every SKPD must

arrange work program and budget (Rencana Kerja dan Anggaran/RKA).

This research examined the two antecedents factors (a need for

achievement and a work attitude) of participation in local government budgetary

activities and then to assess the impact of these two variables on job performance

in the context of managerial performance. So this research investigated budgetary

participation as intervening variable in the relation between the two antecedents

(need for achievement and work attitude) and managerial performance.

B.

PROBLEM STATEMENTS

The results from previous studies showed the relationship between

budgetary participation and job performance might be different under various

working conditions. As a result, the impact of budgetary participation on

performance in public sector also might be different from private sector, because

it has different working conditions. In addition, as governmental units, local

government is more hierarchical, bureaucratic and structured according to a

formal system of authority than privat sectors (Jermias and Setiawan 2007). Based

on the introduction explained previously, the research the problem statement can

be derived as follows: how are the relationship between need for achievement and

work attitude with the budgetary participation; and then through the budgetary

participation, how is the impact of these two variables on job performance in the

commit to user

C.

RESEARCH PURPOSE

According to the research problems, the purposes of this research are:

1. To examine the relationship between an employees’ need for achievement

and budgetary participation.

2. To examine the relationship between an employees’ work attitude and

budgetary participation.

3. To examine the relationship between budgetary participation and

employees’ job performance in local government as a public sector

organization.

D.

RESEARCH BENEFITS

The result of this research to be expected can give input, benefit for Local

government, about budgetary participation from each unit managers, and know

the influence of that participation in regional budget arrangement to performance.

And also show how is the antecedents’ factors such as positive job attitude and a

need for achievement influence the budgetary participation and then to assess the

impact of these two variables on job performance of local government officials as

budget actor according Law number 32/2004 about local government and Minister

of Domestic Affair’s Regulation No. 13/2006. The research result hopefully can

give contribution to academician to the development of public sector accountancy

literature especially in management accounting system development in public

commit to user

CHAPTER II

LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT

A. Literature Review

1. Budgeting Process in Local Government

Budget is a tool of accountability, management and economic policy. As

an instrument of economic policy, the budget function is created growth and

economic stability, also for even distribution of income, in order to achieve

government goals (Law No.17/2004). Local government budget (APBD) which

presented yearly by executive, give the detail information for legislative and

society about what programs that government planned to improve the quality of

life of the people, and how those programs will be funded. According to

Mardiasmo (2005), budgeting arrangement process has four purposes, such as:

a. Help government to achieve the fiscal goal and improve coordination inter

section/units in government surroundings.

b. Help to create the efficiency and fairness in providing public goods and

public service trough the priority making.

c. To make possible for government to fulfill the expenditure priority.

d. Improve the government responsibility and transparency to legislative and

commit to user

The appearance of local government autonomy system, since the declared

of Law no.32/2004 about local government and also Law no. 33/2004 about

financial balancing between central government and local government, brought

the fundamental change in the governance government and financial relationship,

also important change in local budgeting management. Local government budget

(APBD) arranged based on performance approach, that is a budgeting system

which give priority to the effort for performance achievement or output of the

fund allocation that was planned (Government Regulation No.58 / 2005).

Based on performance approach, APBD was arranged relied on a certain

target that will be achieved in one budget year. Preparing the local government

budget draft (RAPBD), local government and legislative (DPRD) arrange the

general policy of local government budget (APBD), which included guidance and

general determinations that will be agreed as guideline for local government

budget arrangement. The arrangement of general policy of APBD constitute the

effort for the achievement of vision, mission, goal, and target were determined in

Local government middle term development planning (Rencana Pembangunan

Jangka Menengah Daerah/RPJMD) for 5 (five) year period, and mayor program

which is arranged based on local government long term development planning

(Rencana pembangunan Jangka Panjang Daerah/RPJPD) that consider with the

national middle term development planning (Rencana Pembangunan Jangka

commit to user

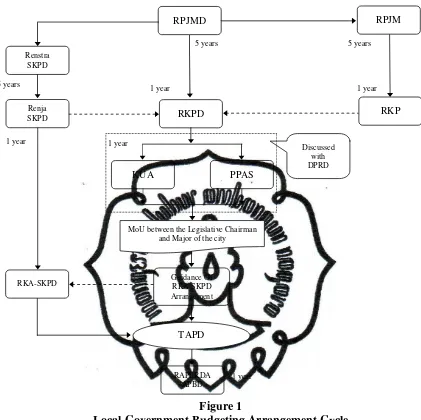

In addition, based on Minister of Domestic Affair’s Regulation

No.13/2006 about the standard of local government budget management, for local

government budgeting (APBD) arrangement, after there is agreement (MoU)

about general policy of budgeting (KUA PPAS) between the chief of local

government and legislative, every institution unit (SKPD) of local government

will arrange program planning and budget of institution unit (RKA-SKPD) with

use local government middle term expenditure frame-approach, harmony

budgeting, and performance-based budgeting. RKA-SKPD will be used by local

government budgeting team (Tim Anggaran Pemerintah Daerah/TAPD) as

material for arrange the local government budgeting draft (RAPBD). Finally,

RAPBD will be discussed together by TAPD and legislative budgeting team (Tim

Anggaran DPRD/Badan Anggaran DPRD), and after evaluated by governor,

those RAPBD will be established as APBD. The cycle of Local Government

commit to user

Figure 1

Local Government Budgeting Arrangement Cycle

(source: Kawedar, Rohman & Handayani 2008)

2. Budgetary participation

Budgetary participation refers to the extent to which manager participate in

preparing the budget and influence the budget goals of their responsibility center

(Kennis 1979). According to Brownell (1986), budgetary participation is defined

as a process whereby subordinates are given an opportunity to get involved in and

have influence on the budget setting process. Budgetary participation also can be

commit to user

refers to the budget process planning in which managers who are involved to

decision making from the information exchange in their organization (Shields and

Shields, 1998).

Participative budgeting gives an opportunity for managers to involve in

budget arrangement. Generally, the whole of budget goals should be

communicated to managers who will help to expand the budget to fulfill the goal.

In budget arrangement, programs were translated by manager responsibility in

conducting the program or part of the program. Basically, budget arrangement is a

decision process of the role of each manager in conducting the programs.

Budgetary participation in public sector occurred when among legislative,

executive, and society cooperate in budget formulation process. Budget made by

Chief of local government which the proposal come from institution units that

made by manager unit. Those, each institution unit of local government should be

involved in budgeting process. It means more employees have allowed

participating in budgetary activities.

Many authors have suggested that participation in setting budgetary goals

encourages managers to identify with the goals, accept them more fully and work

toward their achievement. It is argued that budgetary participation provides an

avenue for subordinates to communicate their private information to

organizational decision-makers and the opportunity to obtain job-relevant

commit to user

The degree of budget participation developed by Milani (1975) can be

measured from the 6 (six) perception of:

a. The portion of the budget the employee involved in setting;

b. The kind of reasoning provided to the employee by a superior when the

budget is revised;

c. The frequency of budget-related discussions initiated by the employee;

d. The amount of the influence the employee felt he has on the final budget;

e. The important of the employee’s contribution to the budget; and

f. The frequency of budget-related discussions initiated by the employee’s

superior when budget are being set.

Sord and Welsch in Sardjito and Muthaher (2007) suggests that the higher

participation would result higher good morality and initiative. Participation in

budgeting activities showed a positive significant influence to employees’

attitude, improve the production quantity and quality, and also improve the

coordination among managers.

While the issue of whether higher levels of budgetary participation

enhance managers’ performance has been widely studied in the accounting

literature, empirical findings to date have proved to be mixed (Wentzel 2002).

Some studies found that budgetary participation is related to job performance and

the relationship is positive (Nouri and Parker 1998; Yuen 2007). Some studies

link the intervening variables such as motivation (Brownell and McInnes, 1986),

budget adequacy and organizational commitment (Nouri and Parker, 1998) and

commit to user

and Muthaher 2007), managerial attitude and motivation (Mia 1988). The results

showed both a positive and negative relationship between budgetary participation

and job performance. Such inconsistent findings have prompted several

researchers to examine the antecedent variables that affect job performance

indirectly during budgetary participation (Yuen 2007). In this research will

examine the need for achievement and work attitude as antecedent factors of

budgetary participation.

3. Need for achievement

It may be stated that need theory as the theory of motivation that addresses

what people need or require to live a life of fulfilment, particularly with regard to

work. Need theory has a long-standing tradition is motivation research. There are

various need theories of motivation. One of the most widely mentioned theories of

motivation is the Hierarchy of Needs Theory put forward by psychologist

Abraham Maslow. Maslow views human motivation in terms of a hierarchy of

five needs, ranging from the most basic physiological needs to the highest needs

for self-actualization. According to Maslow, individuals will be motivated to fulfil

whichever need is the most powerful for them at a given time. Starting with the

physical needs, which are the most basic, each need must be satisfied before the

individual desires to satisfy a need at the next higher level. It is in the following

hierarchy of importance according to immediacy that Maslow places human

needs:

(a) Physiological needs: These are the basic needs for sustaining human life

commit to user

basic as needs that people will be motivated to fulfill them first through

whatever behavior achieves this end.

(b) Safety or security needs: They consist of the need for clothing, shelter,

and an environment with a predictable pattern such as job security,

pension, insurance etc. People are motivated to fulfill these needs only

when the physiological needs are mostly satisfied.

(c) Affiliation, acceptance, love or social needs: Since people are social

beings, they need to belong, to be accepted and loved by others.

(d) Esteem needs: They include the need for power, prestige, status,

achievement, and recognition from others. Satisfaction of the self-esteem

need leads to feelings of self-confidence, worth, capability, and adequacy,

of being useful and necessary in the world.

(e) Need for self-actualization: Maslow regards this as the highest need in his

hierarchy. This is the concept of fulfilling one’s potential and becoming

everything that one is capable of becoming.

Need for Achievement as the part of esteem needs can be referred as an

individual's desire for significant accomplishment, mastering of skills, control, or

high standards. People high in need for achievement are characterized by a

tendency to seek challenges and a high degree of independence. Their most

satisfying reward is the recognition of their achievements. Sources of high need

for achievement include:

a) Parents who encouraged independence in childhood;

commit to user

c) Association of achievement with positive feelings;

d) Association of achievement with one's own competence and effort,

not luck;

e) A desire to be effective or challenged;

f) Intrapersonal Strength. (www.wikipedia.com)

A need for achievement also can be defined as the personal striving of

individuals to attain goals within their social environment (Cassidy and Lynn

1989). The need for achievement is the employees' desire to perform to high

standards and to excel in their job. Individuals with a high need for achievement

like to set their own personal goals and are opposed to the organization setting

goals. These individuals also like goals in which they have a fifty percent chance

of achieving, because they do not want goals that are too easy to achieve.

Individuals with a high need for achievement want frequent, specific feedback and

to know how well they are performing their job. Individuals with a high need for

achievement also want to be in control of their workplace and work environment

and to be responsible for their productivity (Rayburn, Hammond, and Overby

2004). Individuals high in achievement needs have been characterized as

‘realistic’ and generally have occupational goals that are congruent with their

abilities. They are also found to be flexible in seeking detailed information and

feedback from a variety of sources to help in their pursuit of excellence

(Subramaniam 2002).

Persons with a high need for achievement are potentially useful members

commit to user

independent, and have an interest in excellence. They are also willing to take

personal responsibility for success and generally perceive themselves to have a

higher ability than the others (Yuen 2007).

According to Choi (2006), a high need for achievement is characterized by

the following:

1) a high interest in tasks which require a considerable level of skill and

problem solving ability,

2) a tendency to set moderately difficult goals,

3) a preference for concrete and quantitative feedback, and

4) a pursuit of satisfaction which is derived from the task itself and task

performance.

The need for achievement is an unconscious motive that drives individuals

to perform well or to improve their performance. Individuals with a high need for

achievement have a propensity to demonstrate their ability in overcoming difficult

tasks while maintaining consistently high standards. Such individuals consistently

seek feedback on their performance in order to learn from their mistakes and

prefer quantitative feedback. One reason why individuals with a high need for

achievement seek objective feedback is that their motivation is intrinsic more so

than extrinsic and therefore they prefer objective appraisal rather than approval or

acceptance based on the subjective appraisals of others (Loon and Casimir 2008).

According to Steers (1975) a high need for achievement subjects will tend

to place a higher valence on the attainment of their performance objectives than

commit to user

achievement- oriented behavior. Thus, when the tasks are of a challenging nature,

he argued that high need for achievement subjects will manifest high expectations

of task accomplishment and will exhibit a high level of effort and concomitant

involvement in their work. He found that individuals with strong higher order

needs demonstrate higher performance than individuals with weaker higher order

needs.

4. Work attitudes

Attitude is an important variable in human behavior. For better

understanding, it is important to discuss the meaning and definition of attitude.

There are six salient features, which contribute to the meaning of attitude

(Aswathappa in Jegadeesan 2007) such the followings:

a. attitudes refer to feelings and beliefs of individuals or group of

individuals;

b. the feelings and beliefs are directed towards other people, objects or ideas;

c. they tend to result in behavior or action;

d. they can fall anywhere along a continuum from very favorable to very

unfavorable;

e. they endure;

f. all people, irrespective of their status or intelligence, hold attitudes.

Individuals acquire attitudes from several sources but the point to be

stressed is that the attitudes are acquired but not inherited. The most important

sources of acquiring attitudes are direct experience with the object, association,

commit to user

Individuals possess hundreds of attitudes. But organizational behavior is

concerned with work-related attitudes, which are mainly three: job satisfaction,

job involvement and organizational commitment (Jegadeesan 2007).

Milani (1975) defined attitude in terms of employees’ feelings and

predispositions towards their jobs and employers in a budgetary context.

Following to Festinger’s theory of cognitive dissonance, it may argued employees

with positive work attitudes develop a cognitive dissonance (or psychological

uneasiness) during their participation in budget setting. To reduce this dissonance,

they try to improve their performance (Mia 1988; Yuen 2007).

Work attitude is important because committed executives are expected to

exemplify a willingness to work harder to achieve organizational goals.

Executives demonstrating this commitment have a greater desire to remain

employed with that organization. (Pool and Brian Pool 2007).

Milani (1975) divided working attitudes into job attitudes and organization

attitudes. He found that positive attitudes towards a job enhance an employee’s

identification with the organization’s goals, thus leading to an effective overall

performance for the organization. In most instances, attitudes towards the job have

been offered as an intervening factor that affects job performance when

participating in budget activities. Job related attitudes also play a major role in

shaping the work behaviors of managers in organizations (Jayan 2006).

Lynn in Jayan (2006) have developed a theoretical model to describe the

commit to user

and satisfaction) and Job attitudes (Job involvement and satisfaction) have with

several behavior intentions (turnover, absenteeism and performance).

The work attitudes investigated in this study included job satisfaction and

organizational commitment. In this present study, work attitude is related to job

satisfaction as attitude toward job and affective commitment as attitude toward

organization (Muse and Stamper 2007; Larson and Luthans 2006).

4.1. Job satisfaction as attitude toward job

This study used the global approach over the dimensions approach,

conceptualizing job satisfaction as the degree of positive emotions an employee

has toward a job. According to Shahnawaz and Jafri (2009) job satisfaction has

been defined as a pleasurable emotional state resulting from the appraisal of one’s

job - an affective reaction to one’s job and an attitude towards one’s job. Job

satisfaction also can be refers to one’s feelings towards one’s job. It can only be

inferred but not seen. Positive attitudes towards the job are conceptually

equivalent to job satisfaction and negative attitudes towards the job indicate job

dissatisfaction. If any employee likes his job intensely he will experience high job

satisfaction. If he dislikes his job intensely, he will experience job dissatisfaction

(Jegadeesan 2007).

The job satisfaction measurement that has been used for public sector

organization in previous study conducted by Baptiste (2008), focuses on

employees being satisfied with eight categories of their job: (1) sense of

commit to user

security, (6) training received, (7) the work they do, (8) involvement in decision

making.

4.2. Affective commitment as attitude toward organization

Organizational commitment reflects the extent an individual identifies

with an organization and committed to its organizational goals. (Pool and Brian

Pool 2007). Whereas satisfaction means positive emotions toward a particular job,

organizational commitment is the degree to which an employee feels loyalty to a

particular organization (Elanain 2009). Similar to previous study about

organizational commitment (Muse and Stamper 2007; Larson and Luthans 2006;

Elanain 2009) study, this research conceptualized organizational commitment as

an affective form of commitment based on feelings of loyalty toward the

organization (Allen and Meyer, 1990; 1991).

Affective (or attitudinal) commitment is defined as the willingness to

execute continuous effort for the success of the organization. It is characterized by

a strong belief in, and acceptance of, the organization’s goals and values (Yahya

et al 2008). As noted Parker and Kyj (2006), affective commitment is

characterized by: (1) strong belief in the goals and values of the organization, (2)

willingness to exert considerable effort to help the organization to reach its goals,

and (3) strong desire to maintain organizational membership. For individuals who

are committed to their organization, the desire to achieve organizational goals

extends beyond personal interests in acquiring tangible organizational rewards

commit to user

the organization even if direct reward is not contingent upon that aid. Committed

employees identify with organizational success (Parker and Kyj 2006).

5. Employees’ job performance

Job performance is a commonly used, yet poorly defined concept in

industrial and organizational psychology, the branch of psychology that deals with

the workplace. It most commonly refers to whether a person performs their job

well (www.wikipedia.com). Job performance is the degree of how an individual

manager perceives the resources to fulfill and support job requirement. The job

requirement some concerns the budget process to show the managers' decision

making to archived their job performance and job outcome (Agbejule and

Saarikoski 2006). In this study the employees’ job performance refers to the

managerial performance. It means job performance is the competences of

employees in conducting the managerial activity include planning, investigating,

coordinating, evaluating, supervising, staffing, negotiating and representing.

Effective managerial performance may be regarded as depending on competence

in the areas of managerial activity.

There are some indicators develop by Mahoney at all (1963) to measure

the managerial performance such as the followings (Frucot and White 2006;

Parker and Kyj 2006):

a. Planning

Determining goals, policies, and courses of action (e.g., work

commit to user b. Investigating

Collecting and preparing information for records, reports and accounts

(e.g., measuring output, record keeping, job analysis).

c. Coordinating

Exchanging information with people in other organizational units in

order to relate and adjust programs (e.g., advising other departments,

liaison with other managers, arranging meeting).

d. Evaluating

Assessment and appraisal of proposals or of reported or observed

performance (e.g., employee appraisals, judging output records,

judging financial reports, product inspection).

e. Supervising

Directing, leading and developing the subordinates (e.g., counseling,

training and explaining work rules to subordinates; assigning work and

handling complaints).

f. Staffing

Maintaining the work force of institution units (e.g., recruiting,

interviewing and selecting new employees; placing, promoting and

transferring employees).

g. Negotiating

Purchasing, selling or contracting for goods or services (e.g.,

contracting suppliers, dealing with sales representatives, collective

commit to user h. Representing

Advancing the general interest of the organization through speeches,

consultation, or contact with others outside the organization.

i. Overall Performance

Evaluation of the overall performance.

6. Need for achievement, work attitude and job performance

Some previous studies of organizational dynamics have identified positive

attitudes among employees and a need for achievement as being important

elements in lowering turnover and improving performance (Yuen 2007). Need for

achievement has long been recognized to influence job performance. A sense of

achievements promote good job performance. Better performance results from

employees’ passion for achievement (Alam and Mia 2006). Individuals with a

high need for achievement want frequent, specific feedback and to know how well

they are performing their job (Rayburn, Hammond, and Overby 2004).

They are also willing to take personal responsibility for success and

generally perceive themselves to have a higher ability than the others (Kukla,

1972). Klich and Feldman (1992) found that such managers care about their work,

and put more effort into it. This desire for success increases their feeling of

self-worth in an organization. These employees require more accurate feedback and

information from their superior to achieve a preset target.

As the need for achievement, work attitude also were examined by some

commit to user

Such as Milani (1975) suggested that attitude toward the job is offered as an

intervening factor which lead to better performance. He also suggested that good

attitude toward company or organization will lead a more effective overall

performance for the organization. Mia (1988) found that manager’s attitude

appear to be a contingent variable moderating the relationship between their

budget participation and performance. The result revealed that budget

participation by managers who had a more favorable attitude was associated with

improved performance while that budget participation by managers who had a less

favorable attitude was associated with hampered performance. In addition, Yuen

(2007) found that employees’ work attitudes and their need for a sense of

achievement are confirmed as significant influencing factors to job performance

during participation in budgetary activities. The present study examined the need

for achievement and work attitude as the antecedent of budgetary participation in

order to enhance job performance.

B. Hypothesis Development

1. Need for achievement and budgetary participation

A need for achievement has long been thought to influence job

performance. Locke in Alam and Mia (2006) suggested that a sense of

achievement promotes motivation and good job performance. The importance of a

sense of achievement lies in the belief that one should work hard to accomplish

commit to user

In terms of the budgeting process, these findings suggest that managers

with a greater need for achievement are likely to set more challenging, but

attainable, budget targets. They are also likely to seek greater control over their

working environment to maximize the probabilities of achieving or attaining their

goals, and the budgetary participation facilitates achievement such control. They

are more likely to express a willingness to accept more challenges and to take

extra responsibilities voluntarily (Yuen 2007). Given that budget participation is

an important organizational process through which managers may exchange

job-relevant information, it is possible that managers’ need for achievement may

affect their desire for participation in budget setting. The need for achievement

acts as a motivating factor for employees to participate in budget setting as it

facilitates their performance improvement (Alam and Mia 2006).

Steers (1975) also found that need for achievement does have an important

effect on the relationship between performance and job attitudes. Findings

concerning need for achievement are consistent with the argument advanced

earlier that high need for achievement subjects would exhibit a relatively strong

association between performance and satisfaction because superior performance

in itself often represents a form of intrinsic reward for such persons and often

leads to the receipt of positively extrinsic rewards from the organization.

Subramaniam (2002) stated that increasing participation in the budgetary

process becomes useful for managers with high need for achievement because

participation helps them gain appropriate job-relevant information and set more

commit to user

managers with high need for achievement would seek to have greater control over

their work environment in order to maximize the probability of achieving or

attaining their goals, and budgetary participation facilitates achieving such

control. So, it suggest that managers’ need for achievement may lead to (or act as

an antecedent of) their budget participation, which in turn may positively

influence their performance. As results of the above discussion, Hypothesis (H1)

can be stated as follows:

H1 : There is a direct and positive association between an employee’s need

for achievement and employee’s budgetary participation.

2. Work attitudes and budgetary participation

According to Muse and Stamper (2007), work attitude like job satisfaction

and affective commitment represent affective states or feelings employees may

have toward their job and work organization. In evaluating the effectiveness of

budgetary participation, researchers have commonly treated the construct of

“attitude” as an outcome variable. This is because it is commonly assumed that

participation should positively affect attitude as an outcome phenomenon.

However, improved budgetary participation can also be a result of positive work

attitudes among employees. Conversely, employees with negative work attitudes

might not care about achieving their budgeting goals during budgetary

participation (Yuen 2007).

An important reason for examining this variable in the present study is the

commit to user

effective overall performance through participative budgeting. The relationship

between budget participation and work attitudes (job satisfaction and affective

commitment) should therefore be tested. The research conducted by Yuen (2007)

reported that managers with a positive attitude are more likely to willing to

participate in budgetary activities. H2 can thus be formulated as follows:

H2 : There is a direct and positive association between an employee’s work

attitude and employee’s budgetary participation.

3. Budgetary participation and employees’ job performance

Budgetary participation should relate to the involvement of managers in

the budgetary process and their influence over the setting of budget targets

(Shields and Young 1993). The argument that managers’ participation in a budget

setting affects job performance is based on two arguments.

Firstly, psychological theory suggests that participation is related to

performance through self-identification and ego-involvement with budget goals.

Secondly, participation is seen to improve the flow of information between

subordinates and superiors, thus leading to improved cognition and enhanced

decision-making (Shields and Young, 1993). As a result, participation can

promote better performance through facilitation of learning and knowledge

acquisition.

The present study thus proposes that managers with a high need for

achievement and positive job attitudes are likely to seek greater control over their

commit to user

them with such control. The previous research result conducted by Yuen (2007)

found that there is a significant positive relationship between budgetary

participation and job performance. So, H3 is therefore postulated as follows:

H3 : There is a direct and positive association between an employee’s

budgetary participation and employee’s job performance.

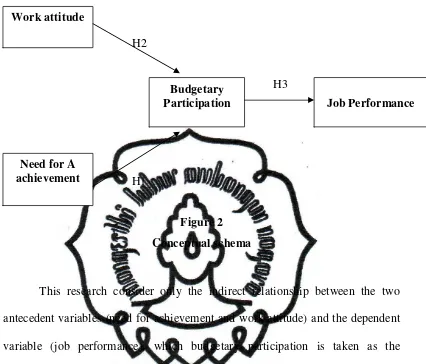

C. Conceptual Schema

Two variables were selected for examination in the present study as possible

antecedent variables of participative budgeting:

(1) managers’ need for achievement; and

(2) manager’s work attitudes.

These variables were chosen for examination because employees who have a need

for achievement and those who have a positive work attitude are likely to

demonstrate enhanced budgetary participation. Such employees are likely to

develop greater identification with, and involvement in, the organization. In turn,

their job performance is likely to be enhanced. These propositions, as shown in

commit to user H2

H3

H1

Figure 2 Conceptual schema

This research consider only the indirect relationship between the two

antecedent variables (need for achievement and work attitude) and the dependent

variable (job performance), which budgetary participation is taken as the

intervening variable in this indirect relationships. No hypothesis is developed for

the direct relationship between those two antecedent variables and job

performance.

Budgetary

Participation Job Performance

commit to user

CHAPTER III RESEARCH METHOD

A. Research Design

This research is quantitative study, and its type is a hypothesis testing.

Sekaran (2003) states that studies engage in hypothesis testing usually explain the

nature of certain relationships, or establish the differences among groups or the

independence of two or more factors in a situation.

B. Population, Sample, and Sampling Technique

Population refers to the entire group of people, events, or things of interest

that the researcher wishes to investigate (Sekaran 2003). The population in this

research is the employees who participate in the budget setting process of local

government Surakarta. In the process of local government budget setting,

participation from each of institution units (Satuan Kerja Perangkat Daerah

/SKPD) are needed, because they should be arranged the budget program planning

(Rencana Kegiatan Anggaran/RKA) for their units. Here, researcher chose the

managers of institution units (SKPD) of local government of Surakarta that

participate in the budget setting process of local government Surakarta, who has

commit to user

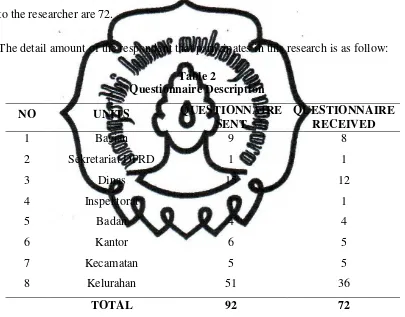

C. Data Collection

This research used survey method. The data obtained by listing question (questionnaire). The questionnaire spread directly (questionnaire was sent directly

to the respondent) for the each manager of institution units (Satuan Kerja

Perangkat Daerah/SKPD) as decision maker (Pengguna Anggaran/Kuasa Pengguna Anggaran) who responsible about the budget of their own institution.

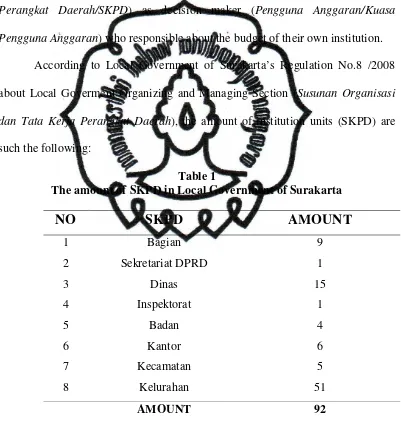

According to Local Government of Surakarta’s Regulation No.8 /2008

about Local Goverment Organizing and Managing Section (Susunan Organisasi

dan Tata Kerja Perangkat Daerah), the amount of institution units (SKPD) are such the following:

Table 1

The amount of SKPD in Local Government of Surakarta

NO

SKPD

AMOUNT

1 Bagian 9

2 Sekretariat DPRD 1

3 Dinas 15

4 Inspektorat 1

5 Badan 4

6 Kantor 6

7 Kecamatan 5

8 Kelurahan 51

AMOUNT 92

commit to user

D. Variables and Operational Definition

1. Independent variables

An independent variable according to Sekaran (2003) is one of the variables

that influence the dependent variable in either a positive or negative way. In

this research the indenpendent variables are:

a. Need for achievement

Need for achievement is the personal striving and employees' desire to

perform to high standards and to excel in their job. The present study

adopted the Manifest Needs Questionnaire to confirm that the

measurement was appropriate for assessing the need for achievement. A

modified five-item version of Steers and Braunstein’s (1976) Manifest

Needs Questionnaire was used to measure need for achievement. This

instrument has previously been used by Subramaniam et al. (2002).

Respondents were required to respond on a seven-point Likert-type

scale.

b. Work attitude

Work attitude is refers to the manager’s attitudes toward job and toward

their organization. In this study the work attitude measured by job

satisfaction and affective commitment. Job satisfaction was measured

by eight-item instrument developed by Nicole Renee Baptiste (2008).

The job satisfaction measurement has been used for public sector

organization that focuses on employees being satisfied with eight

commit to user

initiative, (3) influence over job, (4) pay, (5) job security, (6) training

received, (7) the work they do, (8) involvement in decision making.

Affective commitment was measured by eight-item instrument,

developed by Meyer and Allen (1991). This instrument has previously

been used by many studies (Ketchand and Strawser 1998; Muse and

Stamper 2007). Respondents were required to respond on a seven-point

Likert-type scale. The overall attitude (towards the job and towards the

organization) was assessed by the sum of the scores.

2. Intervening variable

The intervening variable surfaces as a function of the independent

variable operating in any situation, and helps to conceptualize and explain the

influence of the independent variable on the dependent variable (Sekaran

2003). The intervening variable in this research is budgetary participation.

Budgetary participation is the extent to which the employees or managers in

an organization have the opportunity to get involved in formulation of

budgets for which the employees are responsible to implement.

The Milani (1975) six-item, seven-point Likert-type scale instrument

was used to assess participation in budgeting. The instrument has been

extensively used in earlier studies and has provided high internal reliability

(Brownell, 1986; Frucot and White, 2006; Subramaniam et al 2002;Yuen

2007). Participants were asked to respond to each item on a seven-point scale

ranging from 1 (representing low participation) to 7 (representing high

commit to user 3. Dependent variable

The dependent variable in this research is job performance. Job

Performance is the competence of employees in conducting the managerial

activity includes planning, investigating, coordinating, evaluating,

supervising, staffing, negotiating and representing.

Job performance was measured with a self-evaluation questionnaire

developed by Mahoney et al. (1963). Respondents were asked to respond on a

nine-point Likert-type scale. They were required to rate their performance on

eight dimensions – planning, investigating, coordinating, evaluating,

supervising, staffing, negotiating and representing. They were also asked to

rate their overall performance. Although such self-evaluation might be

criticized as being a subjective measure, similar techniques have been widely

adopted in many studies (Brownell and Hirst 1986; Frucot at all 2006;Yuen

2007; Sardjito and Muthaher 2007).

E. Analysis Technique

The data analysis in this research conducted: descriptive statistic, validity and

reliability test and hypothesis testing. The computation of analysis technique is

commit to user 1. Descriptive statistic

Descriptive statistic consists of the measurement of mean, median,

standard deviation, maximum, and minimum value from each data sample. This

analysis means to give the picture of concerning distribution and the data sample

behavior.

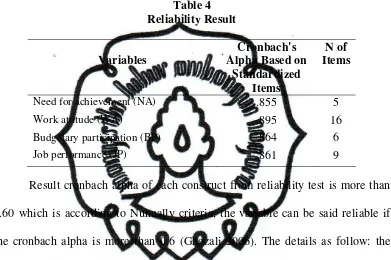

2. Validity and reliability test

Research variable measurement using questionnaire instrument must

use quality examination of data to obtain the test of validity and reliability. This

examination aims to know whether the instrument used is valid and reliable or

not. This is done since the truth of data analysis assesses the quality of research

result.

The aim of validity test is to measure the quality of instrument used and

to show the level of validity of the instrument, and also how well a concept can be

defined by a size of measurement (Ghozali 2006). Instrument can be categorized

as valid if instrument can measure what the researcher want and show the accurate

data. Examination conducted by using factor analysis. This research used

Confirmatory Factor Analysis (CFA) test to measure validity test. Confirmatory

Factor Analysis (CFA) test used to test whether the construct have

unidimentionality or the indicators can confirm the construct or variable. Data is

able to be conducted by factor analysis if the Kaiser’s MSA is above 0.5 (Ghozali

commit to user

Reliability test conducted by calculating Cronbach Alpha (ά) to test the

eligibility to consistency of all used scale. Instrument told reliable if owning

Cronbach Alpha (ά) more than 0.60 this is based on the Nunnally criteria (Ghozali

2006).

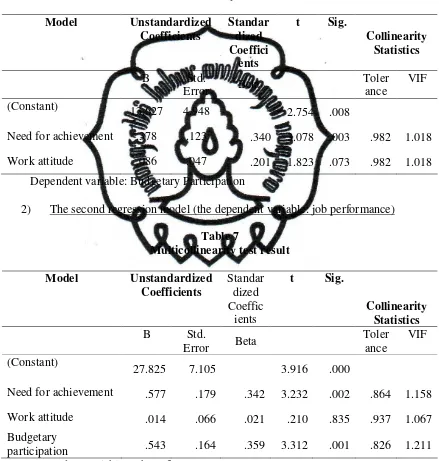

3. Hypotheses testing

Hypothesis will be tested by path model for the data analysis. Path

coefficients (representing the relationships between variables) were estimated by

standardizing the β regression coefficients (Yuen 2007). The relationship between

the variables in the path model can be stated as two equations, such as the follows:

BP = P31NA + P32 WA+ P3aRi... (1)

Where, BP : is the participative budgeting,

NA : the need for achievement,

WA : the work attitude,

P : the standardized partial regression coefficients (path coefficients),

Ri : the standardized residual

JP = P41NA + P42 WA+ P43 BP+P4bRi... (2)

Where, JP : is the job performance,

NA : the need for achievement,

WA : the work attitude,

BP : the participation in budgeting.

P : the standardized partial regression coefficients (path coefficients),

commit to user

Before the multiple regression test, the examination must use classical

assumption test to ensure the validity of research data, not bias, consistent, and

further it can estimate the efficient regression coefficient (Sekaran 2003).

a. Multicollinierity test

The goal of multicollinierity test is to test whether the regression

model found the correlation between the independent variables. The good

regression model must not have correlation between the independent

variables. If the independent variables have correlation, so the variables

are not orthogonal. To detect the multicollinierity, this research used the

tolerance value and the VIF (Variance Inflation Factors) value. To confirm

that multicollinierity not exist in the regression model, if the Tolerance

value is above 0.10 and the value of VIF is < 10 (Ghozali 2006).

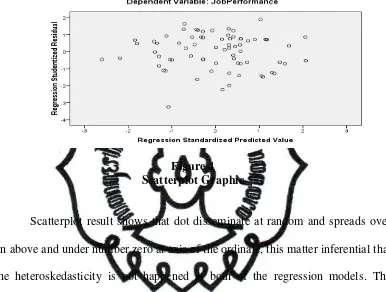

b. Heteroskedasticity test

The goal of heteroskedasticity test is to test whether in the

regression model there is inequality variance from residual of the certain

research to another. If there is fix variance of residual of the certain

research to another, it called homoskedasticity. The good regression model

is if there is homoskedasticity. If the graph scartterplots result show that

dot disseminate at random and also spread over on above and also under

number 0 (zero) at axis of the ordinate, this matter inferential that the

commit to user c. Normality test

The goal of Normality test is to test whether the regression model,

disturbing variable or residual normally distributed. Researcher uses the

analysis of statistic One-Sample Kolmogorov-Sminorv test with the

significant level 0.05, thus the data of residual is normally distributed. If

the Histogram and Normal P-P Plot of Regression Standardized Residual

shows that histogram graphic gives the normal pattern distribution and the

normal plot graphic shows that the dot spread around the diagonal line and

follow the diagonal line. It means that the histogram graphic show the

normal plot distribution thus the regression model is fulfill the normality