Full Terms & Conditions of access and use can be found at

http://www.tandfonline.com/action/journalInformation?journalCode=cbie20

Bulletin of Indonesian Economic Studies

ISSN: 0007-4918 (Print) 1472-7234 (Online) Journal homepage: http://www.tandfonline.com/loi/cbie20

Monetary Policy and the Exchange Rate During the

Crisis

Stephen Grenville

To cite this article:

Stephen Grenville (2000) Monetary Policy and the Exchange

Rate During the Crisis, Bulletin of Indonesian Economic Studies, 36:2, 43-60, DOI:

10.1080/00074910012331338883

To link to this article:

http://dx.doi.org/10.1080/00074910012331338883

Published online: 18 Aug 2006.

Submit your article to this journal

Article views: 58

View related articles

MONETARY POLICY AND THE EXCHANGE

RATE DURING THE CRISIS

Stephen Grenville

Reserve Bank of Australia

This paper examines monetary policy during the Indonesian crisis, looking in particular at what should have been the proper focus of policy. Both the exchange rate and money base have been suggested as appropriate policy objectives, but it is argued here that neither provides adequate policy guidance during a crisis.

Now that the dust has settled, somewhat, on the financial crisis of 1997, it may be possible and appropriate to attempt some evaluation of the crisis strategies. Here, the focus is on monetary policy. How should we evaluate monetary policy during the unfolding of the crisis? Many traditionalists would suggest that the proper measure for evaluating monetary policy should be base money (see, for example, McLeod 1997). Base money almost doubled between September 1997 and June 1998: in this traditional view, this is prima facie evidence that monetary policy was too loose. Others would argue that monetary policy should be evaluated in terms of the exchange rate—in this view, the 80% fall in the exchange rate (i.e. to one-fifth of its initial value) is the best evidence that monetary policy must have been too loose.

the implosion of the interbank money market. Any serious attempt to constrain the growth of base money, when the demand for its main component—currency—was rising so sharply, would have led to a serious shortage of liquidity in the payments system. To argue that the central bank should have denied these demands for base money is tantamount to advocating widespread failure-at-clearing of the banking system. As for the exchange rate, it was driven by forces that could not have been offset by higher interest rates.

If these approaches were faulty, what was the alternative? The third way, which we suggest might have been a more appropriate guide, is that monetary policy could have aimed at preventing domestic (i.e. non-traded) prices from rising much. This would not have been a soft option: it would have required high interest rates. But it had a chance of being successful (and of being seen to be successful), whereas money-base control or exchange-rate targeting were destined to fail, exacerbating the loss of confidence in policy making which was at the heart of the unprecedented collapse of the exchange rate.

THE OBJECTIVES OF MONETARY POLICY IN PRACTICE

There is little doubt that, in terms of the avowed objective, monetary policy in the period September 1997 to June 1998 was predominantly aimed at supporting the exchange rate. The exchange rate was the objective, and interest rates were the instrument. In the IMF’s post mortem on the Asian crisis (IMF 1999), we find this repeated again and again: ‘Although no targets were announced for exchange rates, the exchange rate was the central focus of monetary policy, and interest rates the operating target. … The exchange rate was the best available guide to policy, as no other nominal variable was immediately observable’ (p. 78). The mechanism is spelt out: ‘To provide a disincentive for the exit of capital, expected dollar returns would need at the very least to be positive’ (p. 42). The IMF’s regional chief, Hubert Neiss (1998), talks about the interest rate/exchange rate trade-off, stating that ‘the strategy was to raise short-term money market interest rates to stabilise the foreign exchange market’ (p. 1). Stanley Fischer (1998) put it this way: ‘We expected that currency stability would return to the economies in crisis, provided they ran tight monetary policies and defended their exchange rates’ (p. 3).

in April 1998, the monetary program was reformulated in terms of “firm control of NDA [net domestic assets] of Bank Indonesia”, which replaced base money as a performance criterion. The revised program was also intended to dig in heels sharply, by holding both base money and NDA broadly constant through end-1998’ (IMF 1999: 38).1

So we will attempt a judgment of monetary policy in terms of the two criteria: base money and the exchange rate.

BASE MONEY AS A GUIDE FOR MONETARY POLICY

The textbook model of base-money targeting envisages a world in which banks hold excess reserves and face an interest-elastic demand for borrowing. As the authorities expand base money, this adds to excess reserves and bids down interbank interest rates and the rest of the short end of the yield curve, so that the equilibrium lending quantity shifts down the interest-elastic demand-for-credit curve, to increase the volume of borrowing. In this world, money base is the instrument of policy and is also the measure against which policy is judged.

This model is an elegant expository device beloved of elementary economic texts, but it is no longer a good match with monetary policy implementation as it is practised by central banks in deregulated financial markets. The reasons for this are twofold. First, operationally, it is very difficult to tread the fine line between supplying enough base money to allow the payments system sufficient liquidity to carry out cheque clearances each day, while at the same time keeping a tight enough restraint on banks’ liquidity so as to constrain the growth in their balance sheets. Secondly, the empirical relationship between base money and the ultimate objectives—either inflation or the growth of nominal GDP—is, for most countries, not stable either in the short run or over a longer-term secular horizon. While some central banks have used money base control at certain periods (Switzerland did so until as recently as the 1980s), central banks have gravitated to systems that focus directly on a short-term interest rate. Central banks supply base money on demand, carrying out open market operations to keep bank liquidity close to the level desired by the banking system, and to influence the growth of banks’ balance sheets via the capacity that central banks have to set a short-term interest rate—the Fed funds rate in the United States or the cash rate in Australia. (This is set out in more detail in the appendix.)

crisis of the kind experienced by Indonesia in 1997 would make any attempt to implement monetary policy via control over base money irrelevant. There were enormous changes to both demand and supply of base money.

On the demand side there was a huge increase in the public’s demand for currency, largely motivated by loss of confidence in the banking system. Currency in circulation doubled in the year to mid 1998, accounting for 85% of the increase in base money. Further, because of the implosion of the interbank money market and general concerns about liquidity, banks’ desired liquidity levels rose very substantially.

At the same time, supply of base money was increasing even more dramatically. The closure of 16 private banks early in November dramatically reduced confidence in the banking system, causing runs on individual banks (Soedradjad 2000). The authorities were left with a stark choice—to allow these banks to fail at clearing (effectively closing their doors to depositors), or to support them via injections of central bank liquidity.

Given the chaotic circumstances of the time, multiple schemes and methodologies were used to provide this liquidity credit, and the funding was transferred at various stages between the central bank and the government. It is difficult to piece together, even now, an accurate detailed picture of the factors affecting base money. Starting with the central bank’s balance sheet, the base-money identity in terms of the factors that were important in this period is:

base money = currency + bank reserves = liquidity support – SBIs + foreign exchange reserves

Provision of bank liquidity support added to the supply of base money, and net issue of SBIs (Bank Indonesia Certificates) through open market operations contracted supply. To the extent that the central bank ran down its foreign exchange reserves (i.e. carried out foreign currency intervention), this too contracted base money supply. The net outcome of these supply factors determined the amount of base money held, either in the form of currency by the public, or as bank reserves.

money well in excess of the total base money at September 1997. As the IMF noted, there was little attempt to sterilise this through the issue of SBIs, at least in 1997 and the first months of 1998: ‘This support, intended to keep the payments system from breaking down, was provided quite indiscriminately, in part because of the difficulties of determining whether individual banks were facing liquidity or solvency problems, fears of contagion, and concern over the drying up of interbank lending reflecting uncertainty about which banks would survive. Such liquidity support, which the central bank made only limited efforts to sterilise, resulted in a massive increase in the NDA of the central bank’ (IMF 1999: 38). Beginning in March 1998, there were serious efforts to soak up the excess base money through the issue of SBIs and similar open market operations, taking out more than Rp 55 trillion of base money in the four months from March to June 1998. To some degree, the public (including the banks) were able to reduce the amount of base money in the system by purchasing foreign currency from the central bank, but only to the extent that the central bank was prepared to run down its reserves (i.e. intervene in the foreign exchange market). This amounted to $3 or $4 billion which, depending on the exchange rate, represents perhaps Rp 35 trillion.2

The development of base money during the crisis illustrates why it would have been futile to attempt to hold base money growth to the sorts of modest increases specified in the IMF’s conditionality.3 The public’s demand for extra cash (comprising two-thirds of the increase in base money during the three quarters under discussion) had to be met (the public’s cash holding is, always and everywhere, demand determined). It is possible that the banks’ cash and reserves at Bank Indonesia (the other component of base money) might have been rationed or reined in, but for what purpose? Those banks that were still solvent understandably wanted to hold more liquidity, in a world of uncertainty and with a non-functioning interbank money market.4

foreign exchange. This would not, in itself, have removed the surplus liquidity (unless the central bank was the seller of the foreign exchange), and so more SBI sales were called for.

What this says is that Bank Indonesia could have done a more effective job, in the latter part of 1997 and early months of 1998, in ensuring a closer correspondence between increases in supply of base money and demand. But for our purposes here, the question of selling more SBIs in late 1997/early 1998 is a side issue. The issue here is whether the growth of base money in these circumstances was a useful guide for monetary policy, providing some ex ante objectives and targets, and some ex post

method of evaluating whether monetary policy had been set correctly. The answer is ‘no’. The appropriate growth of base money was not knowable ex ante. To the extent that the growth of base money reflected increased demand for currency by the public, this clearly had to be met, and the same is probably true for the increase in bank reserves. This growth of base money was inevitable and unavoidable. The only practical response to these increased demands for currency and bank reserves was to meet them, while using open market SBI operations to sterilise any excess supply factors.

At a deeper level, of course, there was an important message for the central bank that confidence in the banking system had been lost—but this message called for measures to restore confidence in the banking system; it was not some message about restricting the growth of money base.

THE RELATIONSHIP BETWEEN INTEREST RATES AND EXCHANGE RATES

If base money was not a useful guide for monetary policy, was exchange rate stability a better objective? As the above quotes from the IMF show, monetary policy was directed towards the exchange rate, and although this failed (the exchange rate fell by more than 80%), there is little doubt that this was the basis of the often-heard judgments that interest rates should have been maintained at higher levels: if the exchange rate fell much more than was justified, then in this view, ipso facto monetary policy must have been too loose.

Even before the crisis, there was considerable evidence that defending an exchange rate by means of high interest rates was a strategy which failed at least as often as it succeeded. In 1994, Stanley Fischer (1994: 306) noted in relation to Mexico: ‘… as the European and especially the Swedish experiences show, there may be no interest rate high enough to prevent an outflow and a forced devaluation’. Since then, a number of cross-section country comparisons have tried to define this problem more precisely, with perhaps the most interesting being Goldfajn and Gupta (1998), who concluded that interest rates may help to defend an exchange rate except when the crisis involves a collapse of the financial sector. Again, the intuition is clear enough: if interest rate increases do substantial damage to the financial sector, the adverse consequences are large and outweigh any direct help interest rates might give to the exchange rate. An alternative causation has been suggested (noted by Furman and Stiglitz 1998: 118): that higher interest rates are effective in countries with poor inflation records (e.g. Latin America), as they are an important

signalling device to reassure investors that policy is rigorous. Elsewhere, higher interest rates do not support exchange rates.

From both intuition and experience, it was clear that very high interest rates would be needed to offset, in a mechanical way, the short-term

expectation of a depreciation. If the issue was one of confidence in policy and signalling, then a short sharp shock of higher interest rates might do the job of shifting expectations. But if the issue was seen in terms of

portfolio balance (i.e. expected return on a rupiah denominated investment had to be equal to the expected return on other financial assets, such as dollar securities), then what needed to be done was the equivalent of encouraging the audience to remain in a burning theatre by offering them a discount on their tickets. The strong expectation of even a 1% fall in the exchange rate tomorrow requires (using correct compounding) an annual interest rate of over 3,500% to balance the expected depreciation of the exchange rate. To make the same point another way, the average daily depreciation of the rupiah between 1 July 1997 and 30 January 1998 was 0.8%. A risk-neutral investor knowing this in advance would have required an annualised interest rate of 1,700%, maintained for this seven-month period, to offset that depreciation. Given that daily falls were sometimes as large as 18%, a risk-averse investor would have required a still higher interest rate.5 However this calculation is done, it is clear that extremely high interest rates are required to offset a near-term

convince the market, through raising interest rates, that they will succeed in holding the exchange rate, then high interest rates can quickly be lowered.

Many had drawn the conclusion from experience elsewhere that while high interest rates might be a worthwhile first-shot at defence of an exchange rate, this defence either worked quickly and was successful, or should be abandoned. This was one of the lessons of the 1992 (unsuccessful) defence of the English pound: markets did not believe that rates would be maintained at high levels, given the weak domestic economy (and they were proven correct). In Sweden in the same year, there was an initially successful defence using very high interest rates, but when the currency came under attack later in 1992 the defence was not repeated. Perhaps the only time an interest rate defence will succeed is when, for some reason, there has been a temporary loss of confidence reflected in the exchange rate, which can be restored by a sufficiently determined use of the interest rate instrument in a world where the exchange rate is not seen as fundamentally overvalued.

This did, indeed, seem to be the case in Indonesia in the latter part of 1997. Whatever argument might have been made that the exchange rate was overvalued in mid 1997, the amount of overvaluation was clearly quite small (and there were no obvious macro imbalances), so the initial move of the exchange rate from Rp 2,300 to 4,000/$ could be seen as

overcompensating for any initial overvaluation, leaving open the possibility of defending the new lower rate with a higher setting of interest rates.

So it made some sense, as an opening gambit, to raise interest rates sharply. Whether they were raised enough, and maintained at a sufficiently high level, cannot be judged with any precision. Some would argue that they should have been raised more. But in any case, this gambit—an attempt to demonstrate the rectitude and determination of policy by pushing hard on the interest rate lever—did not address the specific problems of Indonesia. The problem was not a lack of confidence in the macroeconomic policy framework, but was a phenomenon analogous to a bank run—an urgent (and rational) desire to get out ahead of others. These were binary (on/off) decisions, not easily reversed by the offer of a higher interest rate.

indirectly, be brought into question. Foreign creditors understandably became anxious about the creditworthiness of their debtors, and so had good reason to withdraw credit lines at the earliest opportunity. There was a ‘Catch-22’ here: the more credible the authorities were in a portfolio sense (in attracting investors by higher interest rates that were expected to be maintained), the more concerned creditors would be about the viability of borrowers. ‘Monetary policy in the Asian crisis programs faced a difficult task of balancing two objectives. On the one side was the desire to avoid a depreciation–inflation spiral. … On the other side were concerns that excessive monetary tightening could severely weaken economic activity’ (IMF 1999: 35).

There was a further problem with the interest rate defence. Much of the capital inflow was in the form of foreign currency denominated flows, with the interest rate received by the foreign creditors being a dollar (or yen) rate. Higher domestic (rupiah) interest rates did not compensate these creditors for the increased perceived risk, but rather made the risks worse. In these circumstances, higher interest rates did nothing to slow the capital outflow from this source.6

Looking at the Evidence

The references cited above were cross-country studies. This paper explores the same issue from the other end of the spectrum—by looking in detail at a particular country—Indonesia—to see whether the conjuncture of facts and events fits the model which would suggest that interest rates can effectively defend an exchange rate.

In trying to shed some light on this, we should look at which groups were most important in the capital outflow, and ask what flows might have been interest-elastic: where might higher interest rates have slowed the outflow, or created new inflows? In examining this, we would have to accept from the outset that there is not going to be a definitive answer— clearly higher interest rates would inhibit some outflows and create some

inflows.7 The task is to see whether the data reveal significant responses to interest rates.

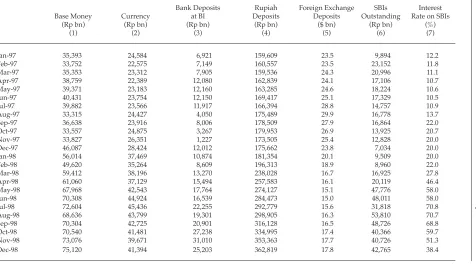

St

ep

hen G

renville

Bank Deposits Rupiah Foreign Exchange SBIs Interest Base Money Currency at BI Deposits Deposits Outstanding Rate on SBIs

(Rp bn) (Rp bn) (Rp bn) (Rp bn) ($ bn) (Rp bn) (%)

(1) (2) (3) (4) (5) (6) (7)

quite sharply in rupiah terms, they fell significantly in dollar terms—by around $10 billion between the middle of 1997 and mid 1998. Were these depositors concerned about the creditworthiness of their bank, and so shifted the funds to an overseas bank? Or were these depositors the ones who were most seriously strapped for cash in meeting foreign debt servicing? Whatever the explanation, higher interest rates on rupiah

deposits would not have directly influenced this choice.

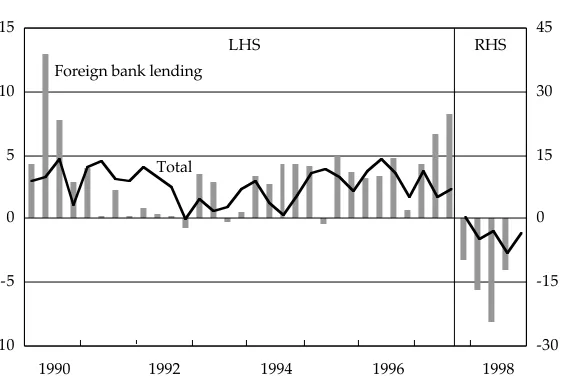

If the outflows were not, predominantly, Indonesians rearranging their own rupiah balance sheets to protect themselves from the devaluation, what were the predominant outflows? By far the most important single outflow related to foreign (overseas) bank transactions (figure 1). While the cutting of lines of credit provided by foreign overseas banks to domestic banks was important, foreign banks’ lending (presumably, again, lines of credit) to non-banks in Indonesia was also important, and this reversed very sharply. Foreign bank inflows, which had averaged around 5% of GDP before the crisis, turned into outflows equal to 15% of

FIGURE 1 Indonesian Capital Account (% of GDP)

Source: Bank of International Settlements (BIS).

-10 -5 0 5 10 15

-30 -15 0 15 30 45

1990 1992 1994 1996 1998

Foreign bank lending

Total

GDP in the year after the crisis. These lines of credit would have been foreign currency denominated, and again not susceptible to the inducement of higher rupiah denominated interest rates.

Information on whether higher interest rates attracted new inflows is harder to infer from the data. The most likely source was Singapore funds which, with a good knowledge of Indonesia, might have been attracted by higher rupiah interest rates at certain stages in the crisis. The most likely place for these funds to have flowed, directly or indirectly, was into SBIs—the high interest rate certificates issued by Bank Indonesia. Holdings of SBIs did, indeed, fall away in the second half of 1997, but came back very strongly in the first half of 1998. They fell from Rp 18 trillion in mid 1997 to Rp 7 trillion by year end, to recover the fall by March 1998 and reach Rp 60 trillion by mid year. Foreigners’ direct holdings were small and stable. Even if we include the SBIs held by foreign and joint-venture banks (which might be the indirect conduit for foreign inflows), that accounts for (at absolute maximum) around one-third of the increase, which represents only $2 billion—relatively modest compared with overall capital flows. More plausible is that the big rise in SBIs in the early months of 1998 was a manifestation of the process whereby the authorities propped up the banking system by providing liquidity to illiquid/insolvent banks, soaking up the addition to base money by issuing SBIs, held predominantly by other banks. So the big increase in SBIs does not seem to reflect large inflows of foreign capital responding to the high interest rates offered on these towards the middle of 1998.

CONCLUSION

There can be no simple evaluation of monetary policy during the crisis period, because policy was not applied consistently throughout the period. But with the exception of the latter months of 1997 and the early months of 1998 (where policy weakness can be seen in both interest rates and SBI operations), high interest rates were the central element in the strategy.

of 1998, given the seriousness of the political problems and general loss of confidence, it seems doubtful that there were many general investors who were brave enough to take the sort of risk that could be compensated by any realistic setting of interest rates. The exchange rate was no longer a useful target for policy, and an alternative focus of monetary policy might have been on maintaining domestic price stability, allowing the first-round effect of the exchange rate to flow through to traded goods, but trying to hold the price of non-traded goods and wages. It would still have been necessary to have quite tight monetary policy (in practice, probably somewhere near the settings that were achieved going into the middle part of 1998, i.e. somewhat higher than the end 1997 period).8 But with this objective, the rhetoric of monetary policy would have been profoundly different. Instead of the constant refrain that policy makers lacked resolve and monetary policy was too weak (with the debilitating effect that this had on confidence), it might have been accepted that monetary policy was doing just about all that could be expected of it, and if this had been generally acknowledged in the market, that would have been beneficial for the exchange rate. In the face of constant harping on the deficiencies of policy, most notably in a Washington Post article of 7 January 1998 (A01, A15 <http://www.washingtonpost.com>), the IMF turned an instrument designed to raise confidence in policy into an instrument that undermined it.

NOTES

2 This leaves a substantial remaining puzzle—having created Rp 150 trillion of base money via BLBI during these three quarters, and having removed only Rp 55 trillion of it via sterilisation with SBIs and Rp 35 billion via foreign reserve run-down, why did base money rise by only (!) Rp 33 trillion? The public took what cash it needed from the banks; the banks themselves were prepared to hold rather more liquidity than usual with Bank Indonesia, but in the end their choice was to hold only an additional Rp 33 trillion of base money, even though more than this was pumped into the system via BLBIs. The remaining unexplained factors in the base money formation picture are hidden in the elements called ‘Other’ in the Bank Indonesia and commercial bank balance sheets.

3 The initial Fund program set a performance criterion for growth of base money in the six months to March 1998 of less than 4%.

4 While banks did hold substantially more reserves, beginning late in 1997 (table 1, column 3), there are no signs that these were involuntary excess holdings, as banks maintained these higher levels after the crisis had ended.

5 Both these calculations are taken from Furman and Stiglitz (1998: 76). 6 In a textbook view of the world, there is a counter-argument to this last point.

While some creditors would have withdrawn their money, the higher interest rates would have attracted new foreign lenders, who would have responded to the higher rupiah interest rates. This textbook world, however, does not resonate with the reality of Indonesia. To see foreign capital inflows into Indonesia as a small fragment of the huge global financial market—with the implication of a fairly elastic supply of new capital in response to an interest rate increase—implies a degree of homogeneous integration that does not fit reality. Those who had invested in Indonesia during the boom years of the first half of the 1990s were a relatively small and compartmentalised sector of world financial markets—people who thought they knew something about these Asian markets, and who suddenly in 1997 realised the reality was different from their earlier perceptions. So the opportunity to offset the capital outflow from fleeing investors by attracting new investors with no initial position in Indonesia was not realistic.

7 There is not much doubt that higher interest rates combined with a feeling that the exchange rate had already fallen a fair bit did, at some stages, induce capital inflow: George Soros (1998) says that he invested in Indonesia late in 1997, when the exchange rate was at around Rp 4,000/$.

REFERENCES

Fischer, Stanley (1994), ‘Comments on Dornbusch and Werner’, Brookings Papers on Economic Activity 1: 304–9.

—— (1998), The Asian Crisis and Implications for Other Economies, Paper prepared for the seminar on The Brazilian and the World Economic Outlook, organised by Internews, Sao Paulo, Brazil, 19 June <http://www.imf.org/ external/np/speeches/1998/061998.HTM>.

Furman, J., and J.E. Stiglitz (1998), ‘Economic Crises: Evidence and Insights from East Asia’, Brookings Papers on Economic Activity 2: 1–135.

Goldfajn, I., and P. Gupta (1998), Overshootings and Reversals: The Role of Monetary Policy, Unpublished paper, International Monetary Fund, August. IMF (International Monetary Fund) (1999), ‘IMF-Supported Programs in Indonesia, Korea, and Thailand: A Preliminary Assessment’, Occasional Paper No. 178, Washington DC.

McLeod, R.H. (1997), ‘Explaining Chronic Inflation in Indonesia’, Journal of Development Studies 33 (3): 392–410.

Neiss, Hubert (1998), Lessons from the Asian Crisis, Paper prepared for the Cato Institute’s 16th Annual Monetary Conference, Washington DC, 22 October. Soedradjad (J. Soedradjad Djiwandono) (2000), ‘Bank Indonesia and the Recent

Crisis’, Bulletin of Indonesian Economic Studies 36 (1): 47–72.

APPENDIX

While the textbook exposition of monetary policy is generally in terms of base-money control, central banks in deregulated financial markets have, more or less universally, moved to a different system. The central bank’s open-market operations are used to ensure that there is adequate (but not excessive) liquidity to meet payments-system clearing requirements, and monetary policy is implemented, separately and more directly, by the announcement of interest rates. To understand why, we need to understand that:

• the elements of base money (on both sides of the central bank balance sheet) are quite volatile—some vary considerably from day to day (e.g. government receipts and payments) and others vary very significantly over a longer period (e.g. the seasonality of cash demand associated with holidays and festivals). As well, there are secular changes in the demand for base money, often responding to institutional change;

• the cheque-clearing system must clear: banks cannot be allowed to fail at clearance and still remain open. It is imperative that the central bank does not, under any circumstances, leave the system with insufficient funds to achieve payments-system clearance.

Any variation in the elements affecting base money will impinge, in a residual sense, on banks’ reserves with the central bank, i.e. on the balances they keep to meet payments-system clearing. If the authorities want to use base money as an operating instrument, they cannot influence (on a day-by-day basis) the public’s demand for currency, so they must focus on the residual balance of base money—bank reserves. They have to make sure these balances are large enough to achieve payments-system clearance, and—at the same time—are sufficiently constraining on banks so as to control the expansion of their balance sheets. Operationally, they have to control this small residual element of base money so as to steer between these two tight constraints. To try to achieve this twofold objective, there are two broad operational strategies.

financial world, as the required liquidity ratio ties up a significant part of banks’ balance sheets and makes them uncompetitive with other financial institutions.

The second (more common) strategy is for the central bank to ensure close control over the growth of bank liquidity, leaving enough (but not excessive amounts) so as to keep overnight interbank interest rates at positive and normal levels. Changes in the public’s demand for cash are offset by open market operations, as are other factors affecting base money. Variations on this theme were common a decade or two ago. The United States had in place such a system, under which monetary policy was administered through small changes to the growth of liquidity (achieved via lending to banks), intended more as a signalling device than as a method of direct control. The signals were often misunderstood, however, because day-by-day liquidity could not be controlled with precision. Central banks have tried various methods to ensure a non-disruptive development of base money, e.g. central bank rediscounting facilities, and the payment of interest on banks’ reserve deposits. But these facilities achieved one objective at the expense of another: rediscount facilities and remunerated reserves both require the authorities to set the rate of interest, which becomes the fulcrum rate of the short-term money market. This ran counter to the supposed rationale for these methods—that monetary policy was implemented via quantities, rather than price. As the focus on central bank independence brought with it a requirement for transparency and clear explanations of policy, these indirect systems (typified by terminology such as ‘snugging’) have been judged to be deficient.

This evolution was driven by deficiencies in base money as an

operating system, i.e. it could not be operated with the necessary degree of precision. Not only were these systems deficient in their ability to achieve the targeted rate of growth of base money, but at the same time the empirical evidence convincingly undermined the belief that there was a stable relationship between base money and the ultimate targets, such as nominal income or inflation. Even if the approach had been able to deliver a steady precise growth of base money, the earlier faith that this would achieve control over the ultimate objectives had been lost. This was the central issue, too, during the Indonesian crisis: even if it was

possible to control base money through the issue of SBIs, what, ex ante, was the correct rate of growth of base money?