ASSESING OF POST ADAPTATION IFRS ACCOUNTING RELEVANCE IN

BANKING COMPANY

Elly Astuti1, Titin Eka Ardiana2

1

Accounting Education Department, Universitas PGRI Madiun E-mail: ellyastuti@unipma.ac.id

2

Accounting Department, Universitas Muhamadiyah Ponorogo E-mail: titineka31@gmail.com

ABSTRACT

IFRS convergence is a topic of financial accounting research in various countries since the establishment of the standard into a set of international accounting standards globally. This research trend also happened in Indonesia. The main impression of IFRS convergence is the quality of accounting information. The quality of information in the financial statements is proxied with the level of earnings management, the relevance value of accounting information and stock prices.

This study will focus on the relevance of the value of accounting information because in some of the previous studies that already exist, penastrophes are focused on manufacturing companies. It is rare that research reveals the relevance of the value of accounting information to banking companies and other financial sector firms. Therefore, this study is aimed to reveal the impact of IFRS convergence on the relevance of the value of accounting information to banking companies.

The population of this study is banking companies in 2007-2016. The period 2007-2008 was chosen as the period prior to IFRS, 2012-2013 as the first full adoption period and 2015-2016 as the second full adoption period. Sampling technique using purposive sampling. Analsis technique using multiple linear regression with advanced test using chow test. Result of analysis of increase of Adjusted R2 in period of pre IFRS, Full Adoption Tahp I and Full Adoption Phase II. This shows that during the period of convergence there is an increase in the quality of accounting information proxied with the relevance of accounting value.

Keywords: IFRS convergence, value relevance of accounting information, banking companies

I. INTRODUCTION

IFRS is a set of global accounting standards decided upon for adaptation in Indonesia since 2008. IFRS is a high quality trusted accounting standard to enhance transparency, accounting quality and global comparability. IFRS is a very market-oriented standard.

IFRS convergence supported by government legal institution system is assumed able to improve the quality of presentation of accounting information that can be used as material consideration of society in placing its deposit fund. Thus, the quality of information is very important to protect the community as a major operational funding source. This is especially to prevent misplaced public funds that cause distrust in the banking institutions as happened in Indonesia that is Centuri Bank.

(Drago, Mazzuca and Colonel, 2013; Liu and Liu, 2007 and Kargin, 2013). However, the results of research conducted by Van der Meulen (2007), Cahyonowati and Ratmono (2012), and Karampinis and Hevas (2011) show that after the IFRS convergence there is no increase in the relevance of the value of information on the company's financial statements. This suggests that IFRS's impact on value relevance remains inconsistent.

Several studies have been conducted related to the impact of IFRS on value relevance in Indonesia, have been documented in manufacturing companies and LQ-45. Financial and banking companies are often excluded from the sample due to their particular characteristics. In addition, IFRS convergence process in Indonesia has unique characteristics. Adaptation is done in Indonesia gradually. This allows a significant difference in the value relevance captured by investors from the company's financial statements in the period before and after the IFRS convergence. Therefore, this research is aimed to reveal the relevance of accounting value in banking companies.

II. LITERATURE REVIEW

Accountancy relevance is how well accounting measurements can reflect the information needed and used by investors to make economic decisions. A review of the relevance of accounting values is generally used as a consideration for improvements to applicable accounting standards.

IFRS is a set of global accounting standards that has been gradually adapted in Indonesia since 2008. This is Indonesia's commitment as agreed by the G-20 meeting in London. However, the impact of IFRS adaptation has not been studied in depth across all corporate sectors in Indonesia. Several studies have been conducted to reveal the relevance of accounting value in Indonesia in general documented to manufacturing companies and LQ 45 in the limited period. The unique characteristics of each of the different industry sectors allow different results.

Alkali, Zuru and Kegudu (2017) documented that the value of post-adaptation IFRS accountancy relevance has had a different impact on developing countries. IFRS adaptation will further undermine the relevance of accounting information in developing countries because some estimation models are used when some assets are not actively traded. In line with this, Hung (2001) discloses that the use of accrual accounting will result in a weak relevance value in countries with less protection to investors.

Indonesia is one of the developing countries with a legal system linking code law. Kouki (2015) documented several countries adhering to the legal code law system of Belgium, France and Germany showing an increased value of accountancy relevance that increased post-adaptation of IFRS. Based on these assumptions, the adaptation of local accounting standards to IFRS supported by the legal system of government institutions is believed to improve the quality of the presentation of accounting information that can be used as a material consideration of the community in placing its deposit funds. This is in line with the research of Agustino, Drago and Silipo (2011) which stated that IFRS convergence makes banks more transparent so that people can know the level of uncertainty and risks that banks have. Increased banking transparency will certainly have an impact on the growing public confidence to save money in the bank. Based on these assumptions, the hypothesis of this study is

III. RESEARCH METHODS

This study uses secondary data from the annual report of manufacturing companies listed on the BEI 2007-2008 (for samples prior to IFRS adoption), 2012-2013 (for samples after first stage IFRS convergence) and 2015-2016 (for samples after IFRS convergence the second stage). The year 2013 and 2016 are taken in this study as the period after assuming the company takes 1 year to implement all policies that have been fully adapted according to IFRS. Selection of 2013 and 2015 due to full adaptation has been set in 2012 for the first phase and 2015 for the second phase.

Sampling technique using purposive sampling with several criteria as follows:

1. Companies listing on IDX from 2007 to 2016 and have never experienced delisting 2. The company keeps its financial statements consistently

3. The financial statements are presented in rupiah

4. Data - data required for research variables that include stock prices, book value shares, earnings per share, debt level and total assets tetsedia in full.

After applying some of these, a total sample of 21 companies was established with a total of 126 firm observations. however there is data outlier in the period before convergence ie in the year 2007-2008 sehinnga issued one company sample in that period. Total final observations of 124 companies. Hypothesis testing of value relevance using the price model developed by Ohlson (1995) as follows:

Pit+1 = β0 + β1BVEPSit + β2EPSit + εit (1) Explanation:

Pit+1 = share price as of March 31 in t+1,

BVEPSit = book value of equity per share in year t,

EPSit = earnings pershare in t,

Ε = Error.

The above model is estimated by multiple linear regression for period data before and after separate IFRS adoption. The value relevance test uses the value of Adjusted R2 obtained from the estimate. If the value of Adjusted R2 is significantly greater for the period data after IFRS adoption then indicates an increase in the relevance of the value of accounting information. Conversely, if there is no significant increase or decrease in Adjusted R2 then this shows no change in the relevance of the value of accounting information before and after the adoption of IFRS.

Further testing is done by providing several control variables in the test model. The several variables that may have an effect on the relevance of accounting value is the size of the company proxied by total assets, price eraning ratio and the level of debt owned by the company.

Further analysis using chow-test. This statistical technique is chosen because it can test the structural change of the relationship between the dependent variable and some independent variables over a period of time (Ghozali, 2012: 181). The occurrence of structural changes indicates that the parameter values of accounting information variables may become unequal during the period 2007 to 2016 due to the IFRS adoption event. Chow test can be used to test equality of coefficients in time series data by classifying observation groups into "before" and "after". The equality of coefficient test with chowtest uses residuals sum of squares (RSS) with the following formula:

F =

(

𝑅𝑅𝑆𝑆𝑆𝑆𝑟𝑟 −𝑅𝑅𝑆𝑆𝑆𝑆𝑢𝑢𝑟𝑟

)/

𝑘𝑘

RSSr is derived from the regression estimation of a number of k parameters for all observations. RSSUR is RSS1 + RSS2 obtained from the results of regression estimation for "before" and "after" periods with the number of observations each of n1 and n2 (Ghozali, 2012: 182).

IV. RESULTS AND DISCUSSION

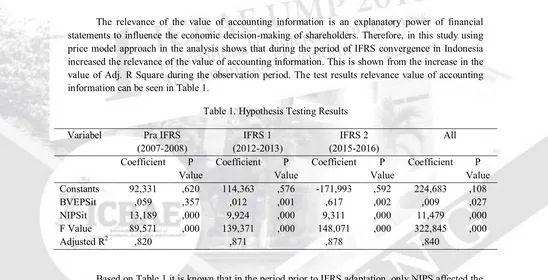

The relevance of the value of accounting information is an explanatory power of financial statements to influence the economic decision-making of shareholders. Therefore, in this study using price model approach in the analysis shows that during the period of IFRS convergence in Indonesia increased the relevance of the value of accounting information. This is shown from the increase in the value of Adj. R Square during the observation period. The test results relevance value of accounting information can be seen in Table 1.

Table 1. Hypothesis Testing Results

Variabel Pra IFRS (2007-2008)

IFRS 1 (2012-2013)

IFRS 2 (2015-2016)

All

Coefficient P Value

Coefficient P Value

Coefficient P Value

Coefficient P Value Constants 92,331 ,620 114,363 ,576 -171,993 ,592 224,683 ,108

BVEPSit ,059 ,357 ,012 ,001 ,617 ,002 ,009 ,027

NIPSit 13,189 ,000 9,924 ,000 9,311 ,000 11,479 ,000 F Value 89,571 ,000 139,371 ,000 148,071 ,000 322,845 ,000

Adjusted R2 ,820 ,871 ,878 ,840

Based on Table 1 it is known that in the period prior to IFRS adaptation, only NIPS affected the stock price. This indicates that the company's valuation of the firm's equity is based more on profitability estimation (NIPSit). The book value of equity (BVEPSit) was not significant in the period prior to IFRS adaptation. This indicates that in that period, the accounting information presented in the financial statements is underutilized by investors to conduct corporate valuation. Agostino, Drago and Silipo (2011) state that in countries with major funding sources derived from debt, or in countries with legal code law systems, investors have broader private information. Such information is information that is not publicly published.

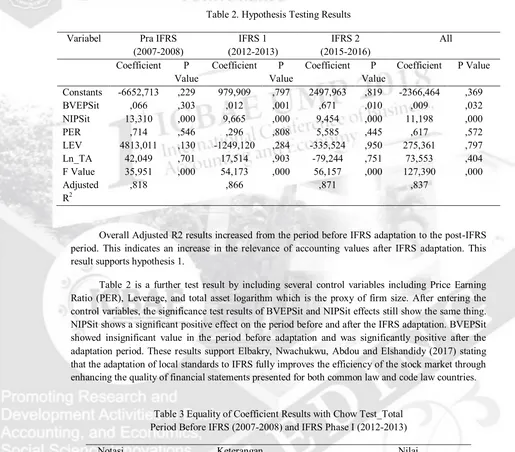

Table 2. Hypothesis Testing Results

Overall Adjusted R2 results increased from the period before IFRS adaptation to the post-IFRS period. This indicates an increase in the relevance of accounting values after IFRS adaptation. This result supports hypothesis 1.

Table 2 is a further test result by including several control variables including Price Earning Ratio (PER), Leverage, and total asset logarithm which is the proxy of firm size. After entering the control variables, the significance test results of BVEPSit and NIPSit effects still show the same thing. NIPSit shows a significant positive effect on the period before and after the IFRS adaptation. BVEPSit showed insignificant value in the period before adaptation and was significantly positive after the adaptation period. These results support Elbakry, Nwachukwu, Abdou and Elshandidy (2017) stating that the adaptation of local standards to IFRS fully improves the efficiency of the stock market through enhancing the quality of financial statements presented for both common law and code law countries.

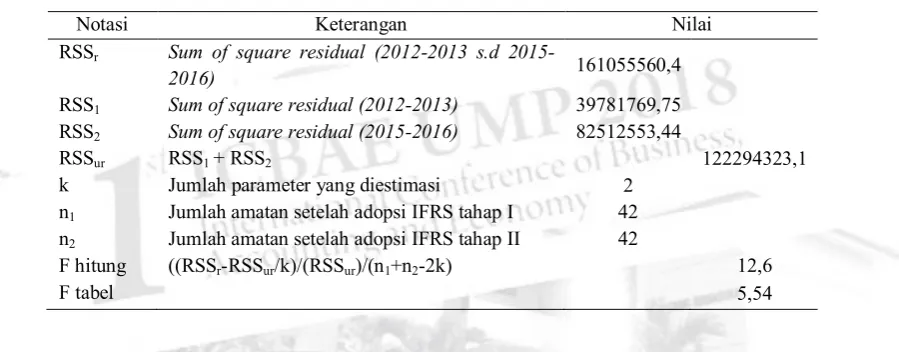

Table 3 Equality of Coefficient Results with Chow Test_Total Period Before IFRS (2007-2008) and IFRS Phase I (2012-2013)

Notasi Keterangan Nilai

RSSr Sum of square residual (2007-2008 s.d

2012-2013) 80643813,83

RSS1 Sum of square residual (2007-2008) 29216682,63

RSS2 Sum of square residual (2012-2013) 39781769,75

RSSur RSS1 + RSS2 68998452,38

k Jumlah parameter yang diestimasi 2

n1 Jumlah amatan sebelum adopsi IFRS 40 n2 Jumlah amatan setelah adopsi IFRS 42

F hitung ((RSSr-RSSur/k)/(RSSur)/(n1+n2-2k) 6,5

F tabel 5,54

Table 4 Equality of Coefficient Results with Chow Test_Total

Period and IFRS Phase I (2012-2013) and IFRS Phase II (2015-2016)

Notasi Keterangan Nilai

RSSr Sum of square residual (2012-2013 s.d

2015-2016) 161055560,4

RSS1 Sum of square residual (2012-2013) 39781769,75

RSS2 Sum of square residual (2015-2016) 82512553,44

RSSur RSS1 + RSS2 122294323,1

k Jumlah parameter yang diestimasi 2

n1 Jumlah amatan setelah adopsi IFRS tahap I 42 n2 Jumlah amatan setelah adopsi IFRS tahap II 42

F hitung ((RSSr-RSSur/k)/(RSSur)/(n1+n2-2k) 12,6

F tabel 5,54

The results of the analysis support Hung's (2001) statement which reveals that accounting relevance is the proportion of accounting information that the market can capture through stock price changes. IFRS adaptation conditions that must be implemented by companies listing on the BEI increasingly support the improvement of the relevance value value of accounting. Kouki (2015) documented that when a company adaptes its financial statements to IFRS voluntarily, it will not increase the relevance of the overall accounting value. However, after IFRS adaptation is mandatory, the quality of the value of accounting information increases significantly.

V. CONCLUSION, SUGGESTION, AND LIMITATION

The main purpose of accounting is to present quality information to interested parties for economic decision making. To meet the quality information criteria, accounting must reflect 3 main indicators that include; earnings management, timely delivery of possible losses and value relevance. Value reevaluation is how strong accounting information can affect the main economic decision for investors. This is reflected in how the information presented affects the movement of stock prices.

The value relevance can be measured using two main approaches: the price model developed by Ohlson (1995) and the return model developed by Easton and Harris (1991). In some previous studies more relevance assessments were based on the Ohlson model with a more focused research focus on

assessing investors.

The rapid development of global business, allowing investors to invest in a wider scope. Investors can invest funds in cross-country by conducting stock or bond portfolios. To improve the comparability, transparency, quality of information, the international accounting standards body has decided to establish an internationally accepted set of standards (IFRS).

Research on the impact of IFRS on improving the quality of information, has been done a lot. Nevertheless, the results of this study may differ if they see the unique characteristics of Indonesia that do adaptation gradually. The results of the analysis show during the adaptation of several periods of visible increase in the quality of accounting information. This result is in line with Kouki (2015) which states that the relevance of post-convergence accounting values shows an increase.

condition such as inflation rate, GDP growth, dividend payout ratio, company accrual rate not included as a control variable.

References

Agostino, M., Drago, D., dan Silipo, D.B, 2011. The value relevance of IFRS in the European banking industry. Rev Quant Finan Acc 36:437–457

Alkali, M. Y., Zuru, N.L, dan Kegudu, D.S. 2018. Book Value, Earnings, Dividends, and Audit Quality on the Value Relevance of Accounting Information Among Nigerian Listed Firms. Accounting Vol 4 Hal 73-82.

Barth, M.E, Beaver, W.H dan Landsman. 1992. The market Valuation Implication of Net Periodic Pension Cost Components. Journal of Accounting and Economics. Vol 15 hal 27-62

Cahyonowati, N., dan Ratmono, D. 2012. Adopsi IFRS dan Relevansi Nilai Informasi Akuntansi. Jurnal Akuntansi dan Keuangan, 14( 2), 105-115

Drago, D., Mazzuca, M., dan Colonel, R.C., Do Loans Fair Value Affect Market Value? Evidence from European Banks. Journal of Financial Regulation and Compliance, 21 (2), 108-120

Elbakry, A.E, Nwachukwu, J.C, dan Abdou, H.S, dan Elshandidy, T. 2017. Comparative Evidence on The Value Relevance of IFRS Based Accounting Information in Germany and the UK. Journal of International Accounting Auditing and taxation. Vol 28 Hal 10-30

Hung, M. 2001. Accounting Standards and Value Relevance of Financial Statements: An International Analysis. Journal of Accounting and Economics Vol. 30 Hal 401-420

Karampinis, N. & Hevas, D. 2011. Mandating IFRS in an Unfavorable Environment: The Greek Experience. The International Journal of Accounting, 46, 304-332.

Kargin, S. 2013. The Impact of IFRS on The Value Relevance of Accounting Information: Evidence from Turkish Firms. International Journal of Economics and Finance, 5, 71-80.

Kouki, A. 2015. IFRS and Value relevance: A Comparison Approach Before and After IFRS Conversion in the European Countries. Journal of Applied Accounting Research.

Liu, J., & Liu, C. 2007. Value Relevance Of Accounting Information In Different Stock Market Segments: The Case of Chinese A-, Band H-shares. Journal of International Accounting Research, 6, 55–81.

Olowolaju, P. S., dan Ogunsan, J. O., 2016. Value Relevance of Accounting Information in The Determination of Shares Prices of Quoted Nigerian Deposit Money Bank. International journal of Economis, Commerce and Management. Vol. 6 No 10 hal 128-147.

Suprihatin, S. dan Tresnaningsih, E. 2013. Dampak Konvergensi International Financial Reporting Standards Terhadap Nilai Relevan Informasi Akuntansi. Jurnal Akuntansi dan Keuangan Indonesia, 10(2), 171-183.