1. General Review

The Indonesian economy is forging ahead with accelerated growth underpinned by macroeconomic stability. This accelerated performance is being fuelled by strengthening consumption, exports and investment. Consumption is climbing on the back of buoyant consumer confidence, availability of consumer financing and low import prices. Alongside this, more robust export activity is being spurred by vibrant demand from China and India. The resurgent domestic and international demand has brought renewed growth in investment. In 2010, the Indonesian economy is forecasted to grow by 6.0%-6.3%, with growth in 2011 climbing to 6.0%-6.5%. In analysis of prices, inflation mounted significantly during Q3/2010. Price increases were recorded mainly in the volatile foods category, and particularly for seasonings and vegetables. Nevertheless, inflationary pressure from core items and administered prices stayed low. Bank Indonesia is keeping a close watch on this potential for inflationary pressure and is strengthening policy coordination with the Government at both central and regional levels. Bank Indonesia will respond with the necessary policy mix to keep inflation on track with the established target at 5%±1% in 2010.

The global economy remains on the path of growth, albeit at varying levels. The larger economies, notably the US, Japan and China, have entered a slowdown. The drop in US economic growth comes in response to pressure bearing down on consumption from high unemployment and the credit crunch, while in Japan, the economic slowdown is explained by appreciation in the yen that has dented export competitiveness. China, where the economy had advanced at a rapid pace, has been compelled to apply brakes to avoid overheating. On the other hand, Europe and particularly Germany and France have charted better than expected growth. This improvement has resulted in part from rising exports and results of stress testing of European banks that exceeded expectations, thus rekindling optimism among economic actors. Alongside this, emerging market economies continue to chart solid growth. Sustained expansion in global manufacturing and steadily rising volume of world trade helped the world economy to maintain growth during Q3/2010, although a more moderate level than in Q2/2010.

The Indonesian economy is expected to post more robust growth for Q3/2010 compared to the preceding quarter. Growth in the domestic economy for the quarter is estimated at 6.3% (yoy). Key to this growth is buoyant household consumption, with estimated growth holding above 5% (yoy). The brisk pace of consumption is being fuelled by consumer optimism and higher incomes bolstered by export earnings. Export growth in Q3/2010 is estimated at 11.4%. Exports have climbed as a result of the steady improvement in world economic growth, led by China and India, and the growing diversity of export destinations. Investment growth is projected at 9.9% (yoy) for Q3/2010, and comes in response to rising demand and improvement in the investment climate. This condition also augurs for renewed growth in imports. In disaggregation by sector, growth in non-tradable sectors forged ahead of the tradable sectors.

properties. Regarding exports, the rise in manufactured exports is contributed mainly by the Jabalnustra region and Jakarta. In contrast, expansion in resource-based exports has taken place in the Kalimantan, Sulampua and Sumatra regions despite crop losses from anomalous weather conditions.

Regarding prices, inflation mounted steadily in Q3/2010, largely from pressure in the volatile foods category. The persistently high volatile foods inflation has been caused by anomalous weather conditions that have disrupted production and distribution as well as from a hike in household electricity billing rates. Added sources of inflationary pressure are hikes in tuition fees coinciding with the start of the new academic year and surging demand related to the religious festive season. Nevertheless, inflationary pressure in September 2010 eased to 0.44% (mtm) from 0.76% (mtm) one month earlier. Taken together, CPI inflation in Q3/2010 widened to 2.79% (qtq) or 5.80% (yoy) from the previous quarter inflation at 1.41% (qtq) or 5.05% (yoy). Despite this, administered prices had little impact on CPI inflation due to the absence of strategic government decisions regarding prices in September 2010.

In preliminary figures for Q3/2010, Indonesia's balance of payments surplus exceeded earlier forecasts. Key to this is significant improvement in the capital and financial account surplus. The steep rise in the capital and financial account surplus has been driven by improving international perceptions of the Indonesian economy, marked by upgrading of Indonesia's credit rating, upward trend in returns on rupiah investments and excess global liquidity. On the other hand, the current account is expected to post a reduced surplus in the wake of high import growth as domestic economic activity gathers momentum. Nevertheless, the dominance of imported raw materials and capital goods signals that the accelerated imports will continue to benefit domestic economic activity. Taken together, international reserves at the end of September 2010 stood at 86.55 billion US dollars, equivalent to 6.5 months of imports and servicing of official external debt.

The rupiah has appreciated further in keeping with the still sizeable current account surplus, heavy foreign capital inflows and prudently managed risks. Rupiah gains have been bolstered by positive global sentiment and growing strength of domestic fundamentals. Measured in comparison to Q2/2010, the rupiah appreciated by an average of 1.2% (qtq) to Rp 9,001 to the US dollar. The third quarter appreciation was accompanied by reduced volatility, down from 0.5% in Q2/2010 to 0.2% in Q3/2010. At end-Q3/2010, the rupiah closed at Rp 8,924 per US dollar, up 1.2% (ptp) from Q2/2010. The stable value of the rupiah offers support for importing the necessary raw materials for domestic production, while on the other hand, the rupiah appreciation has not borne down significantly on exporters because of continued strong international demand.

Financial market conditions showed improved stability during Q3/2010. The Indonesian government securities market and capital market saw further improvement, reflected in the gains in the Jakarta Composite Index (JCI) and lower yields on government securities. This improvement in the two markets during Q3/2010 was bolstered by improvement in the economic outlook. On the interbank money market, liquidity conditions maintained an upward trend. Monetary policy transmission also operated smoothly during Q3/2010, as reflected in movement in the overnight interbank rate at about the level of the BI Rate, more robust credit expansion led by working capital credit and an all-time high in the JCI.

In response to these developments, credit growth for 2010 overall is forecasted at 22%-24%, in line with the business plans prepared by banks. Key to the credit expansion is more robust confidence among economic actors in the outlook for the economy.

On 5 October 2010, the Meeting of the Bank Indonesia Board of Governors, after considering this assessment and the outlook for the economy, decided to hold the BI Rate at 6.5% with an interest rate corridor at ±100 bps. Key to this decision was the

2. Latest Macroeconomic Indicators

The continued progress in global economic recovery has also bolstered the performance of the domestic economy. In emerging market nations, economic recovery moved at a brisk pace, while recovery in advanced industrial nations was generally stable. These conditions have had a positive impact on developments in the Indonesian economy. Indonesia's economic growth is estimated higher in Q3/2010 compared to the preceding quarter due to the effect of more vigorous household consumption, strengthening investment performance and high external demand. Exports are forecasted to maintain brisk growth in line with the improvement in the global economy and support from increased production capacity. This combination of domestic and external demand resulted in high volume during Q3/2010. On the supply-side, growth mounted higher in estimates for the manufacturing, trade, hotels and restaurants, financial services and construction sectors as economic conditions continue to improve. The mining sector has maintained stable growth in estimates, bolstered by steady performance in crude oil lifting. However, the agriculture sector charted lower estimated growth with the passing of the rice harvest. The electricity, gas and water utilities sector reports stable estimated growth in the absence of efforts to bring significant added production on stream in this sector.

DEVELOPMENTS IN WORLD ECONOMY

Global economic growth continued to forge ahead in estimates for Q3/2010, despite uneven distribution of the growth. Recovery was particularly strong in emerging market nations compared to more moderate recovery in advanced industrial economies. On one hand, the US economy is constrained by pressures bearing down on consumption, such as weak support from the financial sector (access to credit) and high levels of unemployment despite progressive improvement in the labour market. In Japan, economic recovery is also hampered by the appreciation of the yen that has impacted exports. On the other hand, European economies are reported to be regaining momentum, fuelled by higher exports from the core eurozone nations (Germany and France) in keeping with the depreciating trend in the euro. In the developing world and particularly Asia, economic activity has been affected by the economic stabilisation process under way in China.

The US economy maintained positive growth in Q3/2010 estimates, despite slowing in comparison to earlier forecasts.1 Indications of a US economic slowdown are

evident in the downward revision in the US GDP for Q2/2010 to 1.7% (qtq annual) from 2.4% (qtq annual). In the latest developments, the US manufacturing sector is regaining momentum, reflected in improvement in the production index and capacity utilisation, despite predictions of future decline. Signs of this are visible in leading manufacturing indicators, such as the Purchasing Manager Index (PMI), manufacturing surveys (Chicago and Philadelphia) and the Beige Book report in August that reported falling business activity in 12 districts. On the consumption side, economic recovery is continuing at a moderate pace. Household consumption strengthened overall as reflected in the positive trend in retail sales during July and August. However, the modest growth in consumption indicates that consumption is still under pressure from slow credit expansion, rising consumer pessimism in the future outlook for the economy and high unemployment at 9.6% in August 2010.2

Estimates point to sustained positive growth in Europe. During Q2/2010, European economies grew by 1.0% (qtq) or 1.9% (yoy) with the depreciating trend in the euro currency delivering a positive boost to exports. The improving condition of the European economy was

1

In the figures for Q3/2010, growth is estimated to have reached 3.4% (yoy) or 2.3% (qtq) (August CF) before dropping to 3% yoy or 1.8% qtq (September CF).

driven primarily by economic growth in Germany and France, while growth in other nations on the European periphery, such as Greece, Portugal and Spain, has slowed due to the imposition of austerity programmes. European consumption (data for July) maintains positive growth although dogged by high unemployment figures at 10.0%. Activity has begun to slow in the manufacturing sector, as indicated by the downward trend in the PMI for manufacturers and the production index.

Alongside this, economic recovery in Japan has been hampered by falling export performance. This decline has impacted manufacturing activity in Japan, as evident from the manufacturing PMI at 53.6 (June 2010) and 50.1 (August 2010). Domestic consumption has also come under pressure as a result of rising unemployment and weak consumer confidence.

In Asia, economic growth is forecasted to carry forward although at a more moderate pace as China stabilises the economy. Export performance and brisk domestic demand are the main factors driving economic growth in Asia. This trend is supported by the economies of China and India, the engines of growth in Asia, which have maintained a positive trend even though at a more moderate pace. In related developments, the normalisation of policy by monetary authorities in the Asian region and the withdrawal of the fiscal stimulus by raising electricity billing rates and fuel process will affect household consumption in Asia. In the Consensus Forecast, the economies of China and India are expected to chart growth at 9.3% (yoy) and 8.0% (yoy) for Q3/2010.

Global financial markets have resumed bullish activity following downward pressure in August 2010. The improvement in economic indicators for the US and China at end-Q3/2010 has lifted concerns over the pace of global economic recovery, which weakened during August. Negative sentiment towards Europe is easing, although confidence is not yet solid. The renewed risk appetite among investors for assets sold by the PIIGS countries is visible in the market absorption of debt instruments floated by Portugal, Greece, Spain and Ireland. Responding to these positive developments, the European Commission revised upwards the 2010 economic growth forecast for Europe to 1.7% (yoy) on 13 September from the earlier 0.9% (yoy) announced in May. Rising market optimism is also reflected in the movement in stock indices and improving perceptions of global risks.

World inflation remained generally stable during Q3/2010 due to the continued weak economic activity in advanced nations. According to composite data on inflation outcomes, global inflationary pressures were largely unchanged from the preceding quarter. During August 2010, inflation ran no higher than 2.9% (yoy) due to poor consumption growth mainly in developed economies.

those nations. In emerging market regions, some central banks have also embarked on normalising monetary policy while introducing liquidity management and macroprudential policy in the financial system. Among the Asian central banks that have lifted rates are Thailand (+50 bps), Korea (+25 bps), Malaysia (+25 bps) and India (+125 bps - reverse repo; +75 bps - repo rate). In Latin America, rate increases have been announced by central banks in Brazil (+50 bps), Chile (+50 bps) and Peru (+75 bps).

ECONOMIC GROWTH

Aggregate Demand

GDP growth in Q3/2010 is estimated higher than in the previous quarter. On the demand side, economic growth during the quarter was bolstered primarily by rising household consumption with added support from stronger investment and high external demand (Table 2.1). Growth in household consumption is estimated up from Q2/2010 in keeping with steadily rising public purchasing power, sustained consumer optimism for the condition of the economy and the strengthening of the rupiah that has held down prices for imports. Investment activity gathered momentum in Q3/2010 in response to improving market perceptions of investment conditions, new policies promoting investment activity, accelerated progress on infrastructure projects, the rupiah appreciation that has kept import prices low and abundant financing support from banks, the capital market and capital inflows. In regard to externals, estimates point to continued robust export performance in keeping with the improvement in the global economy and increased production capacity. This combination of domestic and external demand resulted in high volume during Q3/2010.

Table 2.1

GDP Growth – Demand Side

Household consumption mounted higher in estimated figures for Q3/2010. Supporting this are developments in leading household consumption indicators that suggest that household consumption growth is in the expansionary stage of the cycle (Graph 2.1). Household consumption is climbing in keeping with the rise in public purchasing power, low loan interest rates, consumer optimism in the condition of the economy and the strength of the rupiah that has held down import prices. Household consumption has mounted on rising consumption of non-food items. Halfway through Q3/2010, continued strong sales of cars and motorcycles provided a key indication of the high levels of non-food consumption. Positive developments are also evident in sales of electronic products (Graph 2.2).As happens every year on the eve of the fasting month and religious festive season, the findings of the retail survey for non-automotive and non-electronic goods point to a significant jump in public consumption.In preliminary survey results, the real sales index for August 2010 reached 267.5, having climbed 11.0% (mtm), while in annual terms the index mounted 36.9%. In a similar vein, imports of consumption goods also climbed during Q3/2010. The steady improvement in the trade, hotels and restaurants sector since the beginning of the year also boost provided a lift to household consumption tendencies in

%YoY, Tahun Dasar 2000

I II III IV I II III IV I II III

Total Konsumsi 4.9 5.5 5.5 6.3 6.4 5.9 7.3 6.3 5.4 5.9 6.2 2.5 3.1 6.4

Konsumsi Swasta 5.0 5.7 5.5 5.3 4.8 5.3 6.0 4.8 4.7 4.0 4.9 3.9 5.0 5.4

Konsumsi Pemerintah 3.9 3.6 5.3 14.1 16.4 10.4 19.2 17.0 10.3 17.0 15.7 -8.8 -9.0 13.1

Pembentukan Modal Tetap Domestik Bruto 9.4 13.9 12.2 12.3 9.4 11.9 3.5 2.4 3.2 4.2 3.3 7.9 8.0 9.9

Ekspor Barang dan Jasa 8.5 13.6 12.4 10.6 2.0 9.5 -18.7 -15.5 -7.8 3.7 -9.7 19.6 14.6 11.4

Impor Barang dan Jasa 9.0 18.0 16.1 11.1 -3.7 10.0 -24.4 -21.0 -14.7 1.6 -15.0 22.6 17.7 15.1

PDB 6.3 6.2 6.3 6.2 5.3 6.0 4.5 4.1 4.2 5.4 4.5 5.7 6.2 6.3

= Angka Proyeksi

2009 2007

Q3/2010.

The sustained acceleration in household consumption growth during Q3/2010 was bolstered by availability of financing. The rise in household consumption financing is reflected in the brisk growth in consumer financing extended by multifinance companies and adequate levels of consumption credit extended by banks as of mid-Q3/2010. Positive indications of continued strong public purchasing power were also evident in improved farmer terms of trade and stable wages for farm labour at the end of the quarter as prices mounted for food crop, animal and fisheries commodities. Early Q3/2010 also saw renewed growth in credit card and debit card transactions at 14% (yoy) and 21% (yoy).

Graph 2.1

Private Consumption Leading Indicator

Graph 2.2 Sales of Electronic Goods

Investment growth is estimated to have mounted further in Q3/2010. Indications of revamped investment growth are visible in leading indicators for investment that point to an ongoing expansionary phase (Graph 2.3), high volume of imported capital goods, heightened growth in FDI and investments under the domestic investment scheme, ambitious plans by foreign investors for relocation and expansion in production capacity. Supporting this is the increased use of investment credit and leasing, sizeable plans for floating stocks and corporate bonds to finance investment activity, stronger FDI growth and increased drawdown of private foreign borrowings. Support for stronger investment activity has come from improving market perceptions of investment conditions, the appreciation in the rupiah that has lowered prices for imported goods and introduction of various policies. In addition, inventories are also expected to provide a positive contribution.

Graph 2.3

Investment Leading Indicator

Graph 2.4

Gross Fixed Capital Formation - Machinery

The upsurge in investment has been matched by higher quality of investment. In the first half of 2010, this was reflected in the levels of investment targeting goods of a more productive nature, primarily machines. Numbers for realised investment point to improvement in

97.5

2005 2006 2007 2008 2009 2010 2011

Indikator Penuntun Konsumsi (lead : 8 bulan dr Juni 2010)

gPDBKonsRT CLI Konsumsi RT (rhs)

Impor Barang Konsumsi, M1 Riil, CPI avg fase kontraksi : 19,3 bulan avg fase ekspansi : 22,8 bulan

-40

TV Lemari es Mesin Cuci AC

% yoy

2005 2006 2007 2008 2009 2010

Indikator Penuntun Investasi (lead : 4 bulan dr Juni 2010)

PMTB CLI PMTB

IPI, Sales Commercial Car, IPI Machinery and Equipment, Cement Consumption

avg fase kontraksi : 16,5 bulan avg fase ekspansi : 13,7 bulan

-10 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 yoy Mesin IPI Machinery and Equipments M Suku Cadang & Perlengkapan Barang Modal (s/d Agust) M Barang Modal Kecuali Alat Angkutan (s/d Agust)

gross fixed capital formation from 3.3% in 2009 to an average of 7.9% during the first half of 2010. Leading in investment growth was investment in machinery, which has mounted since Q4/2009 (Graph 2.4). This growth is estimated to have carried over into Q3/2010, as reflected in developments in the monitoring of various leading indicators. Machinery imports were up in July 2010, led by machinery used in telecommunications, transportation and production. Growth in production machinery imports surpassed even that of telecommunications imports. At the same time, growth in construction investment was stable (Graph 2.5) and heavy equipment investment slowed during Q2/2010. Data for July-August 2010 indicates brisk growth in cement consumption alongside rising imports of construction materials in early Q3/2010. Realised investment in startups and companies holding operating licences (FDI and domestic investment scheme) also continued to climb (Graph 2.6). In Q2/2010, realised FDI reached 60% of target, while realised domestic investment came to 52.6% of target. In assessing outcomes for the first half of 2010, the Investment Coordinating Board (BKPM) estimates that the Rp 118.4 trillion and Rp 41.6 trillion targets for FDI and domestic investment can be reached.

Graph 2.5

Building and NonBuilding Investment

Graph 2.6

Realization of Foreign and Domestic Investment (BKPM)

Exports in Q3/2010 are projected to be growing at a brisk pace. Factors driving buoyant exports include stable oil production, reasonably good economic conditions in trading partner nations, consumer and business confidence at the global level, rising export commodity prices and expansion in production capacity. Real export growth in July 2010 reached 30.7% (yoy), up from the June figure of 28.2% (yoy), but below the growth achieved in Q2/2010 at 31.2% (yoy) (Graph 2.7). This downturn is explained by flagging exports of mining products and notably copper and nickel, alongside diminishing exports of wood and shrimps. Exports of non-resource based products were up in comparison to Q2/2010. Leading performers were palm oil, plastic products, machinery and mechanical tools. The high export growth projection is also supported by the ongoing process of global economic recovery. Reflecting this recovery is the continued expansion in volume of world trade, mounting prices for mining exports and gains in production indices in some major export destinations including India and China. Concerning oil and natural gas, the improved lifting of oil expected to carry forward into Q3/2010 will influence oil and gas developments for the entire quarter.

-5 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

PMTB (rhs) Alat Angkutan Mesin Bangunan (rhs)

Graph 2.7

Total Export, Oil&Gas and Non Oil&Gas Export (Real Value)

Graph 2.8 Import Leading Indicator

Imports in Q3/2010 are expected to chart rapid growth. Factors driving this condition include sustained high levels of domestic and external demand and the appreciation in the rupiah that has held down prices for imports.The persistent high level of imports is consistent with movement in leading import indicators, which suggest that import growth is in the expansionary phase (Graph 2.8). This projection is supported by a renewed increase in import VAT revenues during August 2010. However, in real terms, import growth in July 2010 reached 24.9% (yoy), down from the June figure of 33.5% (yoy) and the Q2/2010 level of 48.9% (yoy). Imports have slowed across the board, including oil and natural gas imports and non-oil and gas imports. In the oil and gas sector, imports have eased due to declining oil consumption and prices for imported oil and gas.

Government Financial Operations

Higher revenues and slowed Government spending have combined to produce a national budget surplus for the first eight months of 2010. State revenues until August 2010 stood at 60.8% of the Revised Budget target, ahead of the equivalent 57.2% figure in 2009. However, state expenditure absorption reached only 49.4% of the Revised Budget target, down from the previous year's level of 51.9% of the Revised Budget target. As a result, the budget has posted a surplus of Rp 46.6 trillion, or 0.7% of GDP. The budget surplus has been achieved even in spite of a third quarter deficit at Rp 1.3 trillion (data for July and August 2010).

The rise in state revenues is bolstered by the performance in non-tax revenues. All components of non-tax revenues have gained over the preceding year. In 2009, these revenues reached just 50.7% of the Revised Budget target, but the January-August period of 2010 has marked significant improvement at 62.5% of target. The largest contribution to increased non-tax revenues is from natural resources revenues on oil and gas in line with the higher prices for crude oil. Other Non-Tax Revenues are also up significantly from a number of factors: (i) new regulations governing categories of non-tax revenues and applicable rates in some line ministries and government agencies; (ii) optimised and improved administration of non-tax revenues in line ministries and government agencies; and (iii) higher receipts from service revenues.

Taxation performance has also improved in most components. Realised tax revenues in August 2010 reached 60.3% of the Revised Budget target, up slightly from the 2009 level of 59.4%. This is driven in particular by the improving condition of the international and domestic economy demonstrated by mounting revenues from non oil and gas income tax, VAT and taxes on international trade. Excise revenues will also benefit from the decision to raise

-40%

Total Non-Oil & Gas Oil & Gas (rhs)

% yoy % yoy

2005 2006 2007 2008 2009 2010

Indikator Penuntun Impor (lead : 10 bulan dr Maret 2010)

pdb_imp CLI_impor

fase kontraksi fase kontraksi

Industrial Production Index, Volume Listrik Industri, Produksi Kendaraan, IP Industri Pengolahan Japan, IP Kertas dan Produk dari Kertas, IP Pakaian dan Perlengkapannya, PSI Korea, Rp to USD, Rp to JPY, Kredit Kons Riil, M1 Riil

tobacco excise by an average of 21.7%, effective in early 2010.3

3 Stipulated in Minister of Finance Regulation No. 181/PMK.011/2009 concerning Tobacco Products Excise.

The low level of government expenditures has been brought about mainly by central government spending. Reflecting this condition are realised central government expenditures, which in August 2010 stood at no more than 44.6% of the Revised Budget target. This compares to the 48.1% expenditure level for the same period in 2009. The low rate of central government expenditure is explained by lower than expected growth in line ministry and government agency expenditures. Of the five components of line ministry/government agency expenditures, only Social Aid reported an improved expenditure outcome over the preceding period. Alongside this, absorption of Capital Expenditures and Other Expenditures has slipped below the historical trend since 2007. Subsidy spending, however, mounted significantly due to rising volume in consumption of subsidised fuels.

Budget financing is adequately funded from issuances of Indonesian government securities.In September 2010, gross value of issued Indonesian government securities reached Rp 144.9 trillion (81.4% of the Revised Budget target), ahead of the Rp 127 trillion booked one year earlier (87.7% of the Revised Budget target). The higher issuance of government securities is commensurate with the keen investor interest in these instruments. Interest was particularly strong among foreign investors.

Aggregate Supply

Table 2.2

GDP Growth – Supply Side

Manufacturing sector growth is estimated slightly higher in Q3/2010 on the strength of continued high domestic and external demand. This is supported by leading indicators for the manufacturing sector pointing to upbeat developments during the coming quarter. In early Q3/2010, the production and capacity utilisation indices in the BI Production Survey showed an upward trend.Concerning use of production inputs, slightly increased growth in electricity consumption was reported for end-Q2/2010. Further indications of improving fortunes in manufacturing are evident in the high volume of machinery and tool imports in August 2010, driven by investment in this sector. Confirming this was accelerated expansion in gross fixed capital formation in domestic and foreign machinery during Q2/2010, reported at 5.4% (yoy) and 16.4% (yoy).In the Business Tendency Survey conducted by the Central Statistics Agency (BPS), optimism among business actors in industry climbed to 106.7 in Q3/2010, compared to the Q2/2010 level of 102.3. If analysed by the underlying variables, the more favourable business conditions in Q3/2010 were driven by expectations of improvement in domestic orders, foreign orders, selling prices and orders of inputs. Concerning financing, bank lending to the manufacturing sector steadily climbed for the period ending July 2010.

The trade, hotels and restaurants sector posted higher estimated growth for Q3/2010. Stronger performance in manufacturing has contributed to an increase in the volume of traded goods. In addition, the factor of the religious festive season is also expected to boost trade sector growth, as indicated by retail index gains during August 2010. In addition, mounting economic activity and high imports led to further expansion in trade sector activity during Q3/2010. Import VAT registered significant growth in August 2010 at 30.9% (yoy). Imports are predicted to maintain high growth, due to the brisk pace of automotive sales. The more vigorous growth in the trade subsector was also followed by brisk expansion in the hotels and restaurants subsector in figures for mid-Q3/2010. Hotel occupancy and foreign tourist arrivals, the key indicators for this subsector, both showed gains in July 2010. Trade sector growth was also supported by higher levels of bank financing in figures reported for early Q3/2010.

The agriculture sector is expected to register slower growth for Q3/2010. Flagging growth in this sector is explained by slowing performance in the foodstuffs subsector in the aftermath of the main rice harvest. The ARAM II forecast figures released by BPS for 2010 predicts that overall rice production will expand at a slower rate due to diminishing harvested area and tapering productivity growth. Rainfall steadily increased in September as a result of the La Nina phenomenon. This will essentially have a positive impact by expanding the area of arable land. However, the heavy rainfall also poses negative implications for plants sensitive to heavy rainfall, such as chilli peppers, cocoa and tobacco and may increase the population of crop pests and the risk of flooding. Even so, the fisheries, agriculture and forestry subsectors all show positive

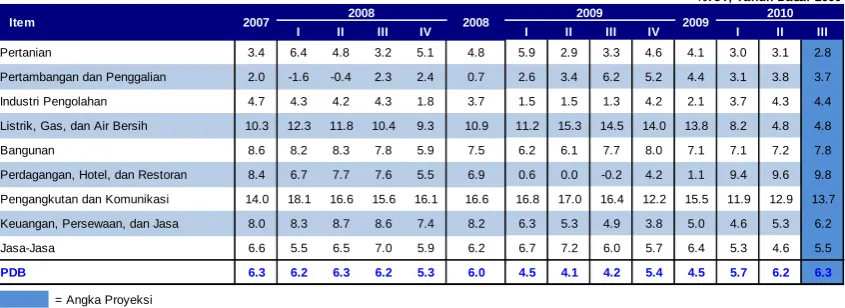

%YoY, Tahun Dasar 2000

I II III IV I II III IV I II III

Pertanian 3.4 6.4 4.8 3.2 5.1 4.8 5.9 2.9 3.3 4.6 4.1 3.0 3.1 2.8

Pertambangan dan Penggalian 2.0 -1.6 -0.4 2.3 2.4 0.7 2.6 3.4 6.2 5.2 4.4 3.1 3.8 3.7

Industri Pengolahan 4.7 4.3 4.2 4.3 1.8 3.7 1.5 1.5 1.3 4.2 2.1 3.7 4.3 4.4

Listrik, Gas, dan Air Bersih 10.3 12.3 11.8 10.4 9.3 10.9 11.2 15.3 14.5 14.0 13.8 8.2 4.8 4.8

Bangunan 8.6 8.2 8.3 7.8 5.9 7.5 6.2 6.1 7.7 8.0 7.1 7.1 7.2 7.8

Perdagangan, Hotel, dan Restoran 8.4 6.7 7.7 7.6 5.5 6.9 0.6 0.0 -0.2 4.2 1.1 9.4 9.6 9.8

Pengangkutan dan Komunikasi 14.0 18.1 16.6 15.6 16.1 16.6 16.8 17.0 16.4 12.2 15.5 11.9 12.9 13.7

Keuangan, Persewaan, dan Jasa 8.0 8.3 8.7 8.6 7.4 8.2 6.3 5.3 4.9 3.8 5.0 4.6 5.3 6.2

Jasa-Jasa 6.6 5.5 6.5 7.0 5.9 6.2 6.7 7.2 6.0 5.7 6.4 5.3 4.6 5.5

PDB 6.3 6.2 6.3 6.2 5.3 6.0 4.5 4.1 4.2 5.4 4.5 5.7 6.2 6.3

= Angka Proyeksi

2010 2009

indications that may prevent further slowing in the agricultural sector. Estates and fisheries exports recorded in early Q3/2010 again reflected buoyant growth. As regards financing, the agricultural sector was marked by increased lending activity as of July 2010.

The mining sector underwent stable growth in estimates for Q3/2010, bolstered mainly by steady performance in crude oil lifting as of August 2010. July 2010 production in the non-oil and gas mining subsector also pointed to a stable trend. Positive indications were also visible in growing exports of non-oil and gas commodities reported for July 2010, such as aluminium and iron ore. Mining sector performance has followed the same trend as the brisk expansion in bank lending support for the mining sector as of early Q3/2010.

More robust growth is estimated for the transport and communications sector during the quarter under review. In the communications subsector, the factor of the religious festive season is expected to boost performance in telecommunications. According to data from the Indonesian Telecommunications Regulation Agency (BRTI), telecommunications traffic during the recent Eid-ul-Fitr festivities was up 35% over usual levels. Growth picked up in both customers and frequency of telecommunications use during Q3/2010, following a slowing trend in preceding quarters. This has been driven by high growth in internet and data communications, which has outpaced growth in cellular phone use. Indicators for the transportation subsector also point in positive direction. Air passenger numbers for July 2010 reflected a sustained pattern of rapid growth. Similarly, rail passenger traffic reported higher growth in figures for July 2010. The annual homegoing for the Eid-ul-Fitr festivities is also estimated to have boosted passenger numbers and volume of cargo. The buoyant growth in the transportation subsector appears to have prompted a response in higher imports of transportation equipment as of August 2010 to anticipate mounting passenger numbers and cargo volume. In contrast, banks reported diminished lending growth to this sector in figures for early Q3/2010.

The construction sector recorded stronger estimated growth in Q3/2010. The upswing in construction sector performance is indicated by movement in production indices for domestic construction materials, i.e. the cement production index and the base metals production index. Heavy equipment sales for construction were also up significantly during the first half of 2010 compared to the same period one year before. Work on government projects commencing in Q3 and Q4/2010 and indications of strengthening investment in the second half of 2010 are among the factors driving performance in the construction sector. Cement consumption and imports of construction materials, both indicators of construction sector activity, maintained brisk levels of growth in August 2010. As regards financing, banks reported increased levels of credit expansion for the construction sector in figures for early Q3/2010.

Regional Economic Performance

Regional economic growth offers confirmation for the upbeat developments in the national economy. The region of Sumatra, Maluku and Papua (Sulampua) reported stronger economic growth from improving estates and mining performance mainly in response to mounting prices. Similarly, high economic growth is projected for the Jakarta, Java, Bali and Nusa Tenggara (Jabalnustra) and Kalimantan regions, bolstered by upbeat performance in the manufacturing and construction sectors.

accelerated disbursement and increased levels of state budget expenditures compared to 2009. Improvement in regional budget outcomes was observed mainly in the Jabalnustra and Jakarta regions, with outcomes averaging above 50%. Strong consumption in the regions was also supported by above 17% growth in consumption credit extended by banks. Similarly, the consumer confidence index for September 2010 indicates more robust consumer confidence in all regions. Estimates point to growing construction and non-construction investment in some regions, led by Jakarta and Jabalnustra. In Sumatra, investment growth is focused more on construction. Indications of improving investment was visible in leading investment indicators, with cement consumption (Graph 2.10), findings of the Bank Indonesia residential survey and imports of capital goods up in all regions.

On the supply side, manufacturing growth in the Jabalnustra region is projected to forge ahead, driven by domestic and external demand. The rise in manufacturing activity has been accompanied by an upward trend in credit to the manufacturing sector in almost all regions. However, agricultural sector activity is expected to slow in some regions. This comes as the result of falling crop productivity caused by a surge in pest attacks in some centres of agricultural production in West Java, East Java and Bali. While output has eased following the end of the harvest season, production has also suffered from heavy rains.

Graph 2.9

Regional Farmers’ Terms of Trade

Graph 2.10

Regional Cement Consumption

CPI inflation has mounted in all regions. In some areas, inflation in Q3/2010 was spurred by disrupted food supplies and high freight costs. Inflation in most areas peaked in July as a result of tightened supply from centres of agricultural production. Limited production of seasonings and vegetables in some regions outside Java, led by Sumatra, led to direct buying in the agricultural centres in Java, thus reducing the available supply of these centres to Jakarta. Administered prices inflation in the regions was spurred by increases in electricity billing rates and annual vehicle registration fees. In addition, the increase in cargo rates at the Tanjung Perak port, effective from 1 August 2010, has been a key factor spurring inflation in the Balustra and Kali-Sulampua regions.

Graph 2.11

Sumatera Jabalnustra Jakarta Kali-Sulampua Nasional

BALANCE OF PAYMENTS (BOP)

Indonesia's positive external condition was key to the solid balance of payments performance during Q3/2010. During the quarter, the balance of payments posted an estimated surplus bolstered by the high surplus in the capital and financial account. The improvement in the capital and financial account took place mainly in portfolio investments (PI) and direct investment (DI). Improving international perceptions of the Indonesian economy, upward trend in returns on rupiah investments and excess global liquidity all contributed to the heavy inflows of foreign capital for portfolio investments. Positive perceptions of the domestic economy also prompted higher inflows of funds for foreign direct investment. However, the current account is projected to chart a reduced surplus for Q3/2010 due to the effect of strong imports and the widening income account deficit. The high level of imports is consistent with the accelerating pace of economic activity during the quarter under review. Alongside this, exports have maintained respectable performance, buoyed by the upward trend in commodity prices. Although developed nations have entered a slowdown, this poses little threat to exports. In the outcome of these developments, the Q3/2010 balance of payments is expected to chart a surplus.

Current Account

The current account is forecasted to chart a surplus, albeit down from the preceding quarter. Rapidly expanding imports are closing the gap with exports, particularly in the non-oil and gas sector. An added factor in the reduced current account surplus is the enlarged income account deficit.

Exports are projected to maintain robust expansion in Q3/2010, buoyed by solid performance in non-oil and gas exports and oil exports. Figures for January-July 2010 show non-oil and gas on a upward trend. Exports to developed markets, such as Europe and Japan, have stagnated slightly, but renewed growth in exports to the US was visible near the end of the period. Alongside this, exports to emerging markets like China and India continue to forge ahead. The more robust export performance in Q3/2010 is also supported by the ongoing climb in commodity prices. Recent developments in prices for Indonesia's export commodities, which began mounting in September, may boost exports further. Non-oil and gas commodity prices have risen in monthly figures (2.1%, mtm) and in comparison to the past year (19.3%, yoy). Prices have climbed in nearly all sectors. Imports recorded brisk expansion in Q3/2010, in keeping with the accelerating pace of domestic economic activity and stable appreciation in the rupiah. The January-July 2010 period was marked by a rising trend in imports, led by raw materials and consumption goods. Nevertheless, there is confidence that high volume of imports is supporting domestic economic activity. The rise in imports of raw materials is consistent with the manufacturing sector response to mounting domestic and export demand. In another area of the current account, the income account recorded an enlarged deficit, mainly from higher dividend and interest payments on investments and placements in Indonesia. This is consistent with the estimated heavy capital inflows in the capital and financial account, particularly in the portfolio investment category.

Capital and Financial Account

the economic outlook prompted higher inflows of FDI into Indonesia during the quarter. These consist mainly of more robust inflows of equity investments and a higher rate of reinvested earnings by parent companies, particularly in non-oil and gas sectors. Positive perceptions of the domestic economy have sustained a strong risk appetite among global investors that has encouraged investment in Indonesia. The steady improvement in returns has strengthened the incentive for investors to channel funds into Indonesia.

International Reserves

3. Monetary Policy and Indicators Q3 2010

In Indonesia, economic performance is steadily improving despite the slowdown

in some advanced nations that is affecting global economic recovery. The conducive trend

in the domestic economy has spurred appreciation in the exchange rate alongside improvement in risk indicators and attractive returns on rupiah placements. During Q3/2010, the rupiah charted further gains. GDP data indicating buoyant growth and healthy performance in the balance of payments influence movement in the rupiah to produce an average 1.2% appreciation to Rp 8,998 to the US dollar. This gain in the exchange rate was also accompanied by reduced volatility

compared to one quarter earlier. Concerning prices, inflationary pressure in Q3/2010 was up

significantly from the preceding quarter. Measured annually, CPI inflation in Q3/2010 reached

5.80% (yoy), up from the Q1/2010 level of 5.05% (yoy). This rise is prompted mainly by growing inflationary pressure from non-fundamentals, in particular volatile foods and administered prices. In contrast, inflationary pressure from fundamentals, illustrated by core inflation, is only minimal but has begun to climb in response to strengthening demand.

Monetary policy transmission continued to operate through various channels. Monetary policy policy transmission through the interest rate channel is functioning well. Short-term interest rates, reflected in rates on the interbank market, have held at conducive levels as indicated by stable movement in the overnight rate near the BI Rate level throughout Q3/2010. In addition, deposit and lending rates continue to ease. In the credit channel, monetary policy transmission saw progress improvement during Q3/2010. Credit expansion mounted to 19.3% (yoy) in August 2010, ahead of the preceding quarter's expansion at 18.0% (yoy). In other developments, monetary policy transmission on the capital market, government securities market and mutual funds market is also positive. The stock market saw the Jakarta Composite Index (JCI) climb to a historical peak of 3,501. On the government securities market, yields were down in almost all tenors. Similarly, the mutual funds market reported positive developments in line with the performance of underlying assets.

RUPIAH EXCHANGE RATE

During Q3/2010, the rupiah charted further gains. Measured as an average, the rupiah appreciated 1.2% during Q3/2010 to Rp 8,998 to the US dollar (Graph 3.1). At end-Q3/2010, the rupiah closed at Rp 8,925 to the US dollar, having climbed 1.5% (ptp) over the preceding quarter. Rupiah appreciation was accompanied by a reduction in volatility during Q2/2010 to 0.2% from 0.5% in the preceding quarter (Graph 3.2).

Global economic recovery in Q3/2010 was overshadowed by concerns over slowdown in some major economies, led by the US and Japan. Indications point to US and Japanese growth slipping below predicted levels, while European economies may surpass earlier forecasts. Growth in Asian economies has also dropped slightly, although continuing at a brisk pace. Global conditions are still flush with excess liquidity as developed economies continue with an accommodative monetary policy stance to bolster economic recovery. In contrast, emerging market economies have taken further steps to normalise policy in response to rising inflationary pressure. These external conditions have produced a sustained appreciating trend in currencies across Asia, including Indonesia.

Domestically, solid economic fundamentals have been a key factor in the performance of the rupiah. In Q2/2010, Indonesia's GDP growth reached 6.2% (yoy), an indication of strengthening economic resilience. In addition, the expected surplus in the balance of payments has sustained positive expectations among global investors regarding the Indonesian economy.

Foreign investor confident steadily mounted in line with improving perceptions of domestic risks and stronger expectations that Indonesia would make investment grade. The Credit Default Swap (CDS) indicator for Indonesia remained low and stable, consistent with the decline in another risk indicator, namely the yield spread between Indonesian government bonds and US T-Notes (Graph 3.3). At the same time, the swap premium (an indicator of the expected direction of movement in the rupiah) remained stable in all tenors (Graph 3.4).

Graph 3.3

Risk Perception Indicators

Graph 3.4

Swap Premium in Various Tenors

The rupiah maintained positive attraction. Uncovered interest parity (UIP), an indicator of returns on the rupiah, was recorded at 6.22%, more than for any other country in Asia (Graph 3.5). After factoring improvement in risk premia, the rupiah gained even more attractiveness. This was indicated by Covered Interest Parity (CIP), which maintained an upward trend during 2010. At end-September 2010, the CIP stood at 4.44%, ahead of Korea, the Philippines and Malaysia (Graph 3.6).

1.0

Graph 3.5

UIP for Countries in the Region

Graph 3.6

CIP for Countries in the Region

INFLATION

The period of Q3/2010 was marked by a significant rise in inflationary pressure. The quarterly measure of CPI inflation in Q3/2010 mounted to 2.79% (qtq), up from 1.41% (qtq) in the previous quarter. The rise in inflationary pressure during Q3/2010 is explained primarily by the non-fundamentals of volatile foods and administered prices. On the other hand, signs pointed to the onset of increasing pressure from fundamentals, reflected in initial escalation of public expectations of inflation. Nevertheless, the monthly and annual inflation figures for September 2010 eased slightly in comparison to the preceding month to 0.44% (mtm) or 5.80% (yoy) from the previous 0.76% (mtm) or 6.44% (yoy) (Graph 3.7).

In disaggregation by expenditure category, inflationary pressure in Q3/2010 came largely from foodstuffs. The inflationary surge in this category is explained by adverse weather conditions in early Q3/2010 that disrupted production and distribution of some foodstuff commodities, led by miscellaneous seasonings and vegetables (Graph 3.8).

Graph 3.7 Inflation

Graph 3.8

Inflation by Category (%qtq)

DISSAGGREGATION OF INFLATION

Graph 3.9

Inflation of Trading Partner Countries and Exchange Rate

Graph 3.10

Imported Commodities Inflation, Core Inflation, and WPI Imports

Inflation expectations mounted higher. The rise in inflation expectations was observed mainly in short-term expectations. This was borne out in the findings of the Consensus Forecast (SF) survey in September 2010, which pointed to an upward trend in inflation expectations for 2010 and 2011 (Graph 3.11). The Consumer Survey also offered indication of mounting consumer expectations (Graph 3.12).

Graph 3.11

Inflation Expectation – Consensus Forecast

Graph 3.12.

Consumers‘ Inflation Expectation (Bank Indonesia Consumers Survey)

Graph 3.13 Real Sales Growth

Graph 3.14

Manufacturing Production Index and Capacity Utilization (Bank Indonesia Production Survey)

In early Q3/2010, the main source of upward pressure on prices was volatile foods. Anomalous weather conditions that hit production and distribution of a range of food commodities, and particularly seasonings and vegetables, led to significant increases in prices. Furthermore, the celebration of religious festivities amid conditions of limited supply contributed to even more rapid price hikes. Nevertheless, harvesting of seasonings near the end of the period paved the way for gradual decline in volatile foods inflation. In response to these developments, the quarterly and annual measures of volatile foods inflation mounted to 6.22% (qtq) and 12.41% (yoy) from the previous quarter's levels of 4.64% (qtq) and 11.51% (yoy).

Rice prices were again a leading contributor to volatile foods inflation in Q3/2010, partly because of factors constraining output but also attempts by merchants to boost margins amid rising prices for other food commodities. Higher rice prices were driven partly by escalating costs of production (costs of post-harvest drying) due to the intensity of recent heavy rains. Meat commodities also generated significant inflationary pressure due to tight supply amid soaring demand related to the Ramadan fasting month and the Eid-ul-Fitr festive season. Nevertheless, major seasonings underwent price correction at the end of the period, thus easing the inflationary pressure generated by price increases for rice and other food items throughout the quarter. While demand mounted in advance of Eid-ul-Fitr, the harvesting of crops and added supply from imports of various seasonings (red chilli peppers, shallots and garlic) helped bring down the level of volatile foods inflation.

In the administered prices category, inflation climbed significantly during Q3/2010. Government-announced price increases, with electricity billing rates raised on 1 July 2010 followed by higher annual vehicle registration fees, had significant impact on administered prices inflation. However, household fuels (kerosene and bottled LPG) had only minimal effect on Q3 inflation, due to the absence of supply shortages during the conversion programme. Taken together, administered prices inflation in Q3/2010 was recorded at 3.54% (qtq), having climbed sharply from 0.57% (qtq) in the previous quarter.

MONETARY POLICY

Interest Rates

festivities. In related developments, perceptions of counterparty risk on the overnight interbank market remained subdued during Q3/2010. Indicating this was the average spread between high and low interest rates at 33 bps, still stable when compared to the 27 bps spread one quarter earlier. In 2010, counterparty risk perceptions on the overnight interbank market have remained stable at 27 bps.

Interbank rates in longer tenors also maintained stable movement throughout Q3/2010. The average interbank rates in longer tenors moved within a range of 2-5 bps compared to the preceding quarter. Interbank rates in the 27-30 day tenor and above 30 day tenors showed more volatile movement compared to other tenors due to the light frequency of transactions. Taken together, the interest rate structure at the end of Q3/2010 was marked by progressive improvement.4 However, a steep interest rate differential persisted in above 27-day tenors, due to

the thin level of transactions in these tenors (Graph 3.16).

Graph 3.15

Interbank O/N Rate & Monetary Instrument

Graph 3.16

Interbank Rate in Various Tenors

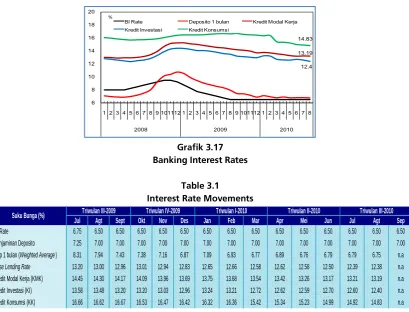

Further developments took place in monetary policy transmission through the bank interest rate channel. During Q3/2010 (data for August 2010), the average 1-month deposit rate eased by 4 bps, in contrast to the 2 bps rise in the preceding quarter. However, the average deposit rate across all tenors in fact mounted by 4 bps. This was prompted by the higher rates on 24-month deposits, reflecting the banking strategy of securing longer-term funding. However, 1, 3 and 6-month deposit rates were stable in comparison to one quarter earlier. In the outcome of these developments, the average deposit rate remained on the high side at 7.38%, albeit slightly lower than 7.52% in the previous quarter. On the other hand, the average loan interest rate in Q3/2010 came down 15 bps, a more modest decline compared to 27 bps in the earlier quarter. Loan interest rates were lowered mainly for investment credit and consumption credit. During Q3/2010, rates for these loans eased 30 bps and 16 bps to 12.40% and 14.83%. In contrast, working capital credit mounted 2 bps to 13.19% (Graph 3.17).

In disaggregation by category of bank, one-month deposit rates were lowered mainly by private banks, with the rate cut averaging 8 bps. However, the steepest reductions in loan interest rates took place at state banks, where rates came down 26 bps.

4 Longer tenors also carried higher interest rates. 5.4

BI Rate rPUAB O/N (average) FASBI O/N SBI Repo

%

O/N 2-6 Hari 7 Hari 8-26 Hari 27-30 Hari > 30 Hari

Grafik 3.17 Banking Interest Rates

Table 3.1

Interest Rate Movements

Funds, Credit, and Money Supply

Growth in depositor funds during Q3/2010 was down from the preceding quarter. In Q3/2010 (data for August 2010), depositor funds recorded 13.3% (yoy) growth, down from the earlier quarter's level of 14.9% (Graph 3.18). Accordingly, depositor funds slipped by Rp 3.3 trillion from the previous quarter to Rp 2,092.8 trillion. This downturn in funding is explained in part by public demand for cash in preparation for the Eid-ul-Fitr festivities.

When analysed by component, the slowing growth in depositor funds is explained by the thin increase in demand deposits, a development related to the slow rate of government expenditures compared to the preceding year. At the end of Q3/2010 (data as of August 2010), demand deposit growth had dropped to 6.3% (yoy) from the preceding quarter's growth of 16.8% (yoy). Alongside this, growth in savings deposits and time deposits, the other funding components, mounted to 22.0% and 11.9% (yoy) from the previous quarter's levels of 18.6% and 11.7% (yoy).

Policy transmission steadily improved in the credit channel. During Q3/2010, lending growth (including channelling) reached 19.3% (yoy), up from 18.0% (yoy) at the end of the preceding quarter (Graph 3.18). As a result, the expansion in credit outstanding from the beginning of the year to mid-Q3/2010 (August 2010) reached Rp 199.8 trillion (13.6%, ytd). This lending growth is markedly higher than the expansion recorded for the same period in 2009 (3.2%, ytd), but remains below the aggressive credit expansion of 2008 (19.2%, ytd). In preliminary figures for September, credit expansion mounted further to 21.3% (yoy).

In disaggregation by category of use, the contribution of working capital credit is steadily rising. In August 2010, growth in working capital credit was the main factor invigorating credit expansion. Working capital credit recorded expansion at 20.1% (yoy), up significantly from the previous period that recorded only 12.7% (yoy). In contrast, growth in investment credit and consumption credit fell to 16.2% (yoy) and 22.7% (yoy) from the previous quarter's levels of 25.2% (yoy) and 25.0% (yoy) (Graph 3.19). The expanding contribution of

13.19

BI Rate Deposito 1 bulan Kredit Modal Kerja

Kredit Investasi Kredit Konsumsi %

% %

Jul Agt Sept Okt Nov Des Jan Feb Mar Apr Mei Jun Jul Agt Sep

BI Rate 6.75 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50

Penjaminan Deposito 7.25 7.00 7,00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00

Dep 1 bulan (Weighted Average) 8.31 7.94 7.43 7.38 7.16 6.87 7.09 6.93 6.77 6.89 6.76 6.79 6.79 6.75 n.a

Base Lending Rate 13.20 13.00 12.96 13.01 12.94 12.83 12.65 12.66 12.58 12.62 12.58 12.50 12.39 12.38 n.a

Kredit Modal Kerja (KMK) 14.45 14.30 14.17 14.09 13.96 13.69 13.75 13.68 13.54 13.42 13.26 13.17 13.21 13.19 n.a

Kredit Investasi (KI) 13.58 13.48 13.20 13.20 13.03 12.96 13.24 13.21 12.72 12.62 12.59 12.70 12.60 12.40 n.a

Kredit Konsumsi (KK) 16.66 16.62 16.67 16.53 16.47 16.42 16.32 16.36 15.42 15.34 15.23 14.99 14.92 14.83 n.a

Triwulan III-2010

working capital credit also points to improvement in credit quality. Only 14 months previously (since June 2009), credit growth had consistently been fuelled by consumption credit.

In disaggregation by sector, credit growth was again bolstered by miscellaneous sectors. In Q3/2010 (data for August 2010), lending in miscellaneous sectors widened by 34.2% (yoy). Nevertheless, lending in other strategic sectors and particularly social services, trade, manufacturing and agriculture gathered additional momentum during the quarter under review. In disaggregation by currency, foreign currency loans widened by 9.3% (yoy) during Q3/2010 (data as of August 2010), which compares to only 5.0% (yoy) one quarter earlier. If a fixed exchange rate (Rp 9,000.-) is applied, growth in foreign currency lending reached 20.5% (yoy), compared to 17.6% (yoy) in the preceding quarter. The more rapid pace of foreign currency lending is related to the high level of import activity, led by capital goods. In contrast, rupiah-denominated credit expansion edged upwards to 22.1% (yoy) from the previous quarter's growth of 21.5% (yoy).

Graph 3.18

Funding, Credit Growth, and BI Rate

Graph 3.19 Credit Growth by Usage

Base money maintained stable expansion amid mounting economic activity. In Q3/2010, average monthly growth in base money was largely steady at 12.3% (yoy), compared to the previous quarter's expansion at 13.5% (yoy). This growth has taken place against a background of mounting economic activity reflected in the rise in average monthly expansion of cash outside banks to 14.2% (yoy) in Q3/2010 compared to 10.5% (yoy) one quarter earlier.

Nevertheless, expansion took place in M1 and M2 economic liquidity. In Q3/2010 (figures for August 2010), average growth in M1 economic liquidity mounted to 13.6% (yoy) from 11.1% (yoy) in the previous quarter. Like for M1, average M2 growth in Q3/2010 climbed to 14.9% (yoy) from 13.1% (yoy) in the preceding quarter (Graph 3.20). The stronger M1 growth is commensurate with growth in the GDP, and thus offers an early indication of improvement in economic conditions.

The improving trend in M1 was supported mainly by added provision of cash. M1 widened by Rp 10.0 trillion in Q3/2010 (data as of August 2010) to Rp 564.5 trillion. This resulted mainly from escalating demand for cash by the public, as is the customary seasonal trend with the Eid-ul-Fitr festivities, as well as from lower positions of demand deposits due to the slower pace of government expenditures compared to the previous year. For this reason, economic growth is also predicted to follow a positive trend. Improvement in M2 is also consistent with developments in M1 and quasi-money. At end Q3/2010 (data as of August 2010), M2 had risen by Rp 21.0 trillion to Rp 2,274 trillion. Regarding components, key support for M2 growth came from time deposits and savings deposits (quasi-money), while M1 also maintained stronger expansion.

Graph 3.20

Nominal Growth of M1 and M2

Financial Markets

Stock market developments were upbeat during Q3/2010. The JCI has made significant gains, especially with the global economic recovery that began in late 2008. The JCI has gained 38% compared to the beginning of 2010. This steep climb took the JCI to an all-time high at 3,501.3 by the end of the period. The gains in the JCI matched share performance on global markets, nearly all of which charted gains. This performance points to significantly improved investor perceptions of the process of world economic recovery in the aftermath of the global financial crisis of 2008.

The sharp rise in the JCI has been driven more by the rush of capital inflows. In Q3/2010, foreign investors booked a net purchase averaging Rp 225 billion per day, up significantly from the previous quarter's net purchase at only Rp 60 billion per day. The surging capital inflows are indicative of the strong confidence that foreign investors have in the outlook for the Indonesian economy.

Index gains were evenly spread across all sectors, with basic industry, multifarious industry and consumer goods in the lead. Rising share prices in these sectors reflect the high level of investor confidence in the future business outlook amid improvement in macroeconomic fundamentals. The basic industries sector is closely linked to production inputs, such as cement, base metals and chemicals. The consumption sector, however, consists of the food and beverages sector and the pharmaceuticals sector.

JCI gains have also been followed by significantly increased volume of share trading. The liquidity of the stock market has mounted in line with JCI gains. Daily turnover during Q3/2010 came to Rp 2.3 trillion, down from the Rp 2.8 trillion recorded one quarter earlier. However, daily volume of share trading during the period under review reached 4.6 billion shares, stable when compared to the preceding quarter.

Graph 3.21

2005 2006 2007 2008 2009 2010

M1 M2 M2 Rp

Performance has improved on the government securities market, buoyed by the economic outlook and positive perceptions of external risk. Average yield on government securities narrowed in all tenors, with the steepest drop in yield recorded for the above 10-year tenor at more than 100 bps (Graph 3.23). From a macroeconomic perspective, the factors behind the redoubled performance of government securities are the stable exchange rate and the positive outlook for economic growth. Externally, the improved performance in government securities is related to diminished perceptions of risk reflected in the downward trend in CDS for Indonesia and the yield on Indo Global Bonds (Graphs 3.24 and 3.25). In addition, performance of government securities was also bolstered by the limited scope of fiscal risks and prudently managed fiscal sustainability.

Graph 3.23 Yield SUN and BI Rate

Graph 3.24 Yield SUN and CDS Graph 3.25 Yield SUN and EMBIG Spread

In developments similar to the stock market, rising capital inflows during Q3/2010 strengthened the performance of government securities. The government securities market moved in tandem with the stock market, with average yield narrowing significantly in comparison to early 2009. This resulted from heavy capital inflows as indicated by expanding foreign investor positions in government securities. In turn, the lower yield on government securities was followed by more active trading on the secondary market (Graph 3.26).

Graph 3.26 Yield SBN and Daily Trading Volume

Mutual funds recorded gains in Net Asset Value (NAV), driven mainly by performance of fixed income funds. NAV for fixed income funds mounted by 7.5% over the preceding period. However, the steep gains in the JCI during Q3/2010 were not fully reflected in the NAV performance of mutual funds. Also important to note is that the rise in mutual funds NAV has been driven more by increased holdings of units, not any overall increase in asset value. This indicates less than optimum performance in the fund placements held in mutual fund units (Graph 3.27).

Graph 3.27 Mixed Mutual Funds Index, Fixed Income, and Stock

0 2 4 6 8 10

1 2 3 4 56 7 8 910 11 121 2 3 45 6 7 8 910 11 12 12 34 5 6 7 8

2008 2009 2010

5 10 15 20 Daily Average-Trading Volum e Govt Bond

Average Yield (RHS)

Rp, Triliun

%

0 50 100 150 200

0 50 100 150 200 250

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8

2007 2008 2009 2010

Spread Indeks NAB-NAB/Unit

Indeks NAB

4. The Indonesian Economic Outlook

In 2010, the Indonesian economy is forecasted to chart 6.0%-6.3% growth,

ahead of earlier forecasts. This upbeat outlook is supported by buoyant domestic and external

performance and is bolstered by steady improvement in macroeconomic stability. On the domestic front, robust consumer confidence and optimism for the future condition of the economy has led to a rapid surge in household consumption. At the same time, the investment climate is expected to improve as business responds by building added production capacity. Externally, export growth is forecasted to remain strong in keeping with the steadily improving process of global economic

recovery. In 2011, Indonesia's economic growth is predicted to reach 6.0%-6.5% as

domestic demand accelerates further and global exports forge ahead. Household consumption is predicted to climb in various regions of Indonesia. The improvement in domestic conditions will be reinforced by investment growth, which is forecasted to gain momentum. The acceleration in investment is expected with the upgrading of Indonesia's sovereign rating at the global level that will position Indonesia as one of the leading venues for investment. These positive conditions provide a robust foundation for Indonesia's macroeconomic conditions in order to promote sustainable and equitable growth in future years.

Inflation is predicted to mount further in 2010, while potential exists for slight

reduction in 2011. CPI inflation in 2010 is expected to be biased upwards of the 5%±1%

inflation targeting range. In 2011, CPI inflation is also expected to biased above the 5±1% range as

a result of strengthening domestic economic activity, rising imported inflation driven by higher commodity prices and inflation expectations. On the non-fundamentals side, heightened inflationary pressure is expected from hikes in some strategic administered prices. Added to this, volatile foods inflation is forecasted to remain high, although below the levels reached in 2010.

ASSUMPTIONS AND SCENARIOS

Assumptions for the International Economy

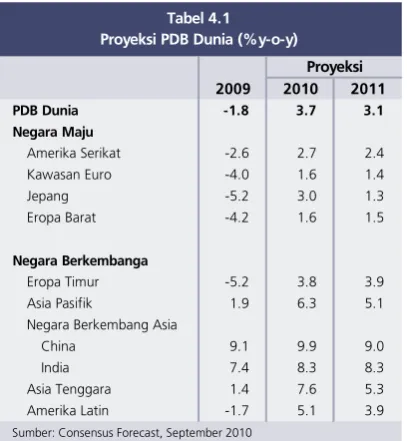

The global economic recovery is predicted to maintain momentum, bolstered by vigorous recovery in emerging market economies. According to the Consensus Forecast, Asia-Pacific nations could potentially grow 6.3% in 2010 and 5.1% in 2011. This is remarkably high growth when compared to the 2009 level of 1.9% (Table 4.1). At the same time, forecasts for the United States and Japan suggest more constrained economic expansion due to the impact of high unemployment and weak support from the financial sector. In the Eurozone, economic forecasts remain fraught with uncertainty.

With global economic recovery moving forward, world trade volume is predicted to expand in 2010 and 2011. The ongoing expansion in the manufacturing sector driven by the rapid recovery in Asian economies underpins the forecast for high growth in volume of world trade. In data published by the CPB Netherlands Bureau for Economic Policy Analysis, as of July 2010 growth achieved in world trade had reached 18.5% (ytd).

Fiscal Policy Assumptions

The deficit in the Revised 2010 budget, as approved by the Indonesian Parliament at end-May 2010, is set at 2.1% of GDP. However, in view of recent developments, the Government predicts that in 2010, the actual deficit will come to only 1.5%. The below-target deficit outcome is based on the low level of budget expenditure absorption by line ministries/government agencies during the first half of 2010.

Beyond this, the Financial Notes for the Draft 2011 Budget project the deficit at 1.7% of GDP. This deficit relies on measures to optimise sources of revenue, with focus on broadening the tax base and intensifying tax collection and support from reforms in tax administration. Beyond taxation policy, the government taking actions to boost resource-based production in order to boost non-tax revenues from oil and gas and non-oil and gas sources.

On the expenditures side, central government allocations will be targeted at improving the welfare of state officials and retirees, implementation of administrative reform, infrastructure construction, allocation of better targeted subsidies, social safety nets and community block grants. To close the deficit in 2011, the Government is prioritising domestic financing sources and cutting back on external financing sources while progressively easing the debt-to-GDP ratio in order to maintain fiscal sustainability.

ECONOMIC GROWTH OUTLOOK

Indonesia's economic growth in 2010 is forecasted at 6.0%-6.3%, buoyed by robust domestic and external performance and steady improvement in macroeconomic stability. In the domestic economy, strong growth is forecasted for household consumption in line with robust consumer confidence and optimism over future economic conditions. The investment climate is predicted to improve further as business responds by expanding production capacity. Similarly, export growth is forecasted to remain strong in keeping with the steadily improving process of global economic recovery.

In 2011, Indonesia's economic growth is predicted to reach 6.0%-6.5% in keeping with continued acceleration in domestic demand. Rising household consumption is predicted across many regions in Indonesia, from Sumatra to Java and the eastern part of the archipelago. Investment growth is also predicted to take off with the various improvements in Indonesia's sovereign rating at the global level that will position Indonesia as one of the leading venues for investment.