Full Terms & Conditions of access and use can be found at

http://www.tandfonline.com/action/journalInformation?journalCode=vjeb20

Download by: [Universitas Maritim Raja Ali Haji], [UNIVERSITAS MARITIM RAJA ALI HAJI Date: 12 January 2016, At: 17:57

Journal of Education for Business

ISSN: 0883-2323 (Print) 1940-3356 (Online) Journal homepage: http://www.tandfonline.com/loi/vjeb20

Gender Imbalance in Accounting Academia: Past

and Present

Charles E. Jordan , Gwen R. Pate & Stanley J. Clark

To cite this article: Charles E. Jordan , Gwen R. Pate & Stanley J. Clark (2006) Gender Imbalance in Accounting Academia: Past and Present, Journal of Education for Business, 81:3, 165-169, DOI: 10.3200/JOEB.81.3.165-169

To link to this article: http://dx.doi.org/10.3200/JOEB.81.3.165-169

Published online: 07 Aug 2010.

Submit your article to this journal

Article views: 36

View related articles

ABSTRACT. Studies conducted in the

late 1980s and early 1990s reflected a

gen-der imbalance in the accounting academy

as the proportion of female professors fell

far below the percentage of women

accoun-tants in practice. For a sample of

doctoral-granting and nondoctoral-doctoral-granting

Associa-tion to Advance Collegiate Schools of

Business (AACSB) institutions, the authors

in this study examined changes in gender

ratios in accounting academia during the

period 1994 to 2004. Important findings

revealed that, relative to nondoctoral

grant-ing programs, terminally qualified female

accounting educators were no longer

under-represented at doctoral-granting

institu-tions. In addition, although far from

reflecting an appropriate gender balance,

the proportion of women in senior faculty

and administrative positions had improved

dramatically.

Copyright © 2006 Heldref Publications

mundson and Mann (1994) noted that women comprised only 14.1% of academic accountants in 1980; this percentage grew to 21.7% in 1988. These numbers include both tenure- and nontenure-track positions. Carolfi and Pillsbury (1996) reported that the proportion of female accounting faculty in tenure-track positions rose from 6.7% in 1979 to 19.8% in 1993. Even though their numbers rose mod-estly during this 15-year period, female accounting educators were poorly rep-resented in universities across the nation in 1993 because 37% of the institutions had no terminally qualified female accounting faculty members and anoth-er 32% employed only one woman. Thus, even though women comprised over half the workforce of practicing accountants in 1993, 69% of the univer-sities nationwide employed, at most, only one terminally qualified female accounting educator. Over a decade has passed since these studies were con-ducted. This led us to our first research question: What advancements have institutions made in employing termi-nally qualified female academic accountants in the past decade?

Several studies suggest that female accounting faculty have been more successful at attaining tenure-track employment at institutions not granting doctoral degrees in accounting than at schools granting such degrees (Carolfi &

Pillsbury, 1996; Collins, Parrish, & Collins, 1998; Collins, Reitenga, Collins, & Lane, 2000; Parker, 1995). Gender discrimination theory hypothe-sizes that because men still dominate accounting programs, especially doctor-al-granting ones, these male faculty will strongly influence the characteristics that candidates must possess (Collins et al., 2000). However, in a survey of female accounting educators, only 3% of the respondents felt that gender-related discrimination played a role in their hir-ing decision (Lanier & Tanner, 1999).

It may also be that terminally qualified female academic accountants self-select nondoctoral-granting institutions for employment over doctoral-granting ones. Dwyer (1994) noted that, relative to men, women may place more emphasis on teaching than on research, devote more time to family, and may be less commit-ted to their careers. These factors could cause women to seek employment at less research-oriented institutions. The data used in the prior studies on gender mix of accounting at doctoral-granting versus nondoctoral-granting institutions were several years old (Carolfi & Pillsbury, 1996; Collins et al., 1998; Collins et al., 2000; Parker, 1995), which led to our second research question: Relative to nondoctoral-granting institutions, do ter-minally qualified female academic accountants continue to be underrepre-sented at doctoral-granting institutions?

Gender Imbalance in Accounting Academia:

Past and Present

CHARLES E. JORDAN GWEN R. PATE STANLEY J. CLARK

UNIVERSITY OF SOUTHERN MISSISSIPPI HATTIESBURG, MISSISSIPPI

O

Another gender issue relates to the professorial rank that female accounting educators have achieved relative to their male counterparts. Using 1988 data, Norgaard (1989) found that the number of male accounting faculty in each of the three ranks (i.e., assistant, associate, and full professor) was approximately the same. However, consistent with their late entry into academia, terminal-ly qualified females were concentrated primarily at the assistant professor rank. Zuckerman (1987) concluded that, even in samples of male and female acade-mics with equivalent research records, men hold higher ranks than women do. In a similar study, Saftner (1988) pro-vided evidence that female academic accountants took longer than men to reach full professor status. Using data from the decade of the 1980s, Dwyer (1994) concluded that male accounting faculty were more likely than were females to reach the rank of full profes-sor, even after controlling for research activity.

Female accounting faculty members believe that published research, by far, represents the most important determi-nant in promotion decisions (Epps, 1991). In addition, Streuly and Maran-to (1994) demonstrated that female accounting faculty have performed at comparable levels with their male coun-terparts in terms of research quantity, quality, and impact (i.e., citations). Rama, Raghunandan, Logan, and Bark-man (1997) provided evidence that female accounting faculty promoted to associate professors at Association to Advance Collegiate Schools of Busi-ness (AACSB)-accredited nondoctoral-granting institutions actually outper-formed their promoted male counter-parts on a variety of research measures. The results of the aforementioned stud-ies based on data from the 1980s and early 1990s suggest that female accounting faculty are promoted more slowly than are male accounting faculty, even though women may be just as pro-ductive as men in terms of research. This led to the third, and final, research question in the current study: Given that significant numbers of female account-ing faculty have now been employed long enough to progress through the professorial ranks, have the proportions

of women at higher ranks (i.e., associate and full professor) improved in recent years?

METHOD

In this study, we attempted to answer the following three gender-related research questions regarding academic accountants:

1. In the past decade, have universi-ties made significant advancements in employing terminally qualified female accounting faculty?

2. Relative to nondoctoral-granting institutions, do female academic accountants continue to be underrepre-sented at doctoral-granting institutions? 3. Have the proportions of female academic accountants at higher ranks (i.e., associate and full professor) improved in recent years?

To answer these questions, we col-lected gender-related data on two dis-tinct groups of accounting faculty. One group contained faculty from doctoral-granting institutions, whereas the other group comprised faculty from AACSB-accredited nondoctoral-granting institu-tions. All institutions that had been granting accounting doctorates consis-tently since 1978 were included in the sample; 62 programs met this criterion. One hundred randomly selected AACSB-accredited nondoctoral-granting institu-tions were included as well. The prima-ry selection criterion for this group was that the programs had at least under-graduate AACSB business school accre-ditation in 1994 and maintained this accreditation through 2004. We omitted schools without AACSB accreditation from the study to provide more in-sam-ple homogeneity.

We collected data on the gender and rank of every tenure-track accounting faculty member in these two groups for 1994 and 2004. The 10-year gap allowed comparisons to be made between two different time periods. The earlier date (1994) was chosen because it is represen-tative of the time periods examined in most of the earlier research on account-ing faculty gender issues discussed previ-ously. We also collected gender-related data on the directors, chairs, or heads of the accounting programs and on the

deans of the respective colleges of busi-ness. We collected the data from Hassel-back’s Accounting Faculty Directory

(1994; 2004).

To ascertain the gender of each faculty member and administrator, we examined a subject’s first name and applied judg-ment based on common names of men and women. For names that appeared gender neutral, we took alternative steps to determine gender. These included con-sulting colleagues that might have per-sonal knowledge of the subjects, examin-ing accountexamin-ing program Web pages for pictures and biographies, and calling the accounting programs’ administrative assistants or faculty. Using this proce-dure, we determined the gender of every tenure-track faculty member and admin-istrator identified in the Hasselback

Accounting Faculty Directories for the sample institutions.

RESULTS

With the first research question, we simply sought to determine whether institutions had made significant improvement in employing terminally qualified female accounting faculty rela-tive to males. Table 1 shows summary data for total male and female accounting faculty holding tenure-track positions (not including administrators) at both nongranting and doctoral-granting institutions in 1994 and 2004. For the nondoctoral-granting institutions, the proportion of female faculty to total faculty increased from 22.8% in 1994 to 25.6% in 2004. Although this increase in proportion of women was not statistical-ly significant (α= .13234) between 1994

and 2004, examining the raw numbers indicated that women did gain ground during the period. To be more specific, the number of female accounting educa-tors increased by three during the period, whereas the number of males declined by 113.

For the doctoral-granting institutions, Table 1 reveals that women made a sta-tistically significant improvement (α =

.00796) during the period, going from 18% of the faculty in 1994 to 23.2% in 2004. In terms of sheer numbers, women gained 26 positions, whereas men dropped 114 slots. Taken as a whole, the institutions in the sample

made a statistically significant improve-ment (α= .01314) in increasing the

pro-portion of female accounting faculty, going from 20.6% in 1994 to 24.5% in 2004. The total number of male faculty dropped 14.3% during the period, from 1,588 in 1994 to 1,361 in 2004, while the total number of females increased 7% (from 413 to 442) during the same period. Although women obviously still lag behind their male counterparts in absolute numbers, significant improve-ment has occurred in the past decade to increase their representation in account-ing academia.

With the second research question, we sought to ascertain whether female accounting faculty continued to be underrepresented at doctoral-granting institutions relative to nondoctoral-granting schools. Table 1 shows that female accounting faculty comprised 22.8% of the total faculty for nondoc-toral-granting institutions in 1994. For the doctoral-granting institutions in 1994, the percentage of women was lower (18%). These proportions of female accounting faculty in 1994 at the two types of institutions differed at a statistically significant level (α =

.00790). This result is not surprising given the prior research (Carolfi & Pills-bury, 1996; Collins et al., 1998; Collins et al., 2000; Parker, 1995) suggesting that women have been more successful in securing employment at nongranting institutions than at doctoral-granting ones. A key issue in the current study is whether this discrepancy con-tinues today.

Table 1 reveals that women compri-sed 25.6% and 23.2% of the accoun-ting faculty positions in 2004 at nondoctoral-granting institutions and

doctoral-granting institutions, respec-tively. Although still lagging some-what behind the nondoctoral-granting schools, the doctoral-granting schools closed the gap that existed 10 years earlier, and, more important, the differ-ence in proportions is no longer statis-tically significant (α= .23198). Thus,

relying on overall faculty numbers, it appears that female academic accoun-tants at doctoral-granting institutions are no longer underrepresented relative to female academic accountants at nondoctoral-granting institutions.

A better yardstick for measuring trends in employing female accounting educators than the percentage of total faculty might be the percentage of assis-tant professors that are women. Assisassis-tant professors represent the pool of recently hired terminally qualified faculty, and it is the gender mix within this pool that would be most indicative of hiring differ-ences between nondoctoral-granting and doctoral-granting institutions. Table 2 shows information on the gender mix of accounting assistant professors at non-doctoral-granting and non-doctoral-granting universities in 1994 and 2004.

Table 2 reveals that almost 37% of the assistant professors at nondoctoral-granting institutions in 1994 were women whereas only 28.8% of the assistant professors at doctoral-granting schools at this time were women. These proportions differ significantly (α =

.02080) and indicate that, relative to nondoctoral-granting institutions, females were underrepresented at doc-toral-granting schools in 1994. Whether terminally qualified female academic accountants self-selected nondoctoral-granting institutions as employers or doctoral-granting institutions engaged

in gender discrimination in hiring is unknown. However, what is known is that female academic accountants were not employed in equal proportions at these two types of institutions in 1994.

Table 2 shows that, a decade later, this employment discrepancy was elim-inated. In particular, in 2004, women comprised about 37% of the total assis-tant professors at both nondoctoral-granting and doctoral-nondoctoral-granting institu-tions. This percentage approximates the proportion of accounting doctoral degrees awarded to women in the late 1990s and early 21st century. It appears that doctoral-granting institutions have made a conscious effort to increase their hiring of terminally qualified female academic accountants, and women are no longer underrepresented at these institutions, at least relative to nondoc-toral-granting schools.

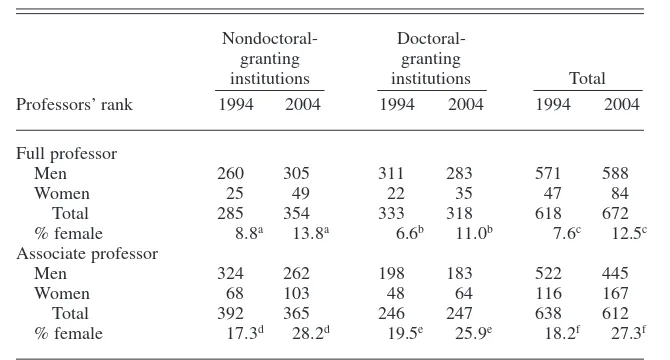

With the third and final research question, we did not seek to determine whether female accounting faculty are promoted faster or slower than their male counterparts are; we simply endeavored to ascertain if women comprised larger proportions of the higher professorial ranks than they did in the past. Table 3 shows the gender mix for nongranting, doctoral-granting, and all institutions in the sample for 1994 and 2004 for the senior ranks (i.e., associate and full professors). Table 3 shows that, for both nondoctoral-granting and doctor-al-granting institutions, women held higher proportions of both the associ-ate and full professor ranks in 2004 than they did in 1994. For both ranks and for both types of schools, the increased proportion of women during the 10-year period was statistically sig-TABLE 1. Gender Comparison of Tenure Track Accounting Faculty Between 1994 and 2004

1994 (n) 2004 (n)

Type of institution Men Women Total % female Men Women Total % female

Nondoctoral-grantinga 857 253 1110 22.8 744 256 1000 25.6

Doctoral-grantingb 731 160 891 18.0 617 186 803 23.2

Totalc 1588 413 2001 20.6 1361 442 1803 24.5

Note. The zvalues and αlevels are for two-sample proportions tests comparing the percentage of female faculty between 1994 and 2004. az= –1.50,α= .13. bz= –2.65,α= .01. cz= –2.48,α= .01.

nificant by traditional standards of sig-nificance (i.e., an αlevel of .10 or

bet-ter).

Again, the data in Table 3 do not imply that female academic accountants are now promoted faster than their male counterparts are. To make such an asser-tion would require detailed informaasser-tion about the time each faculty member spent in a particular rank prior to pro-motion. The data do, however, allow a generalization to be made that women academic accountants have made signif-icant improvements in attaining senior-level faculty positions in the past decade. In relation to the gender mix in accounting practice, women still have a long way to go before they achieve comparable gender levels to men in senior-level faculty positions. However, given the late entry of women into

accounting academia and the significant length of time required for anyone to become terminally qualified and progress through the professorial ranks, the improvements noted in Table 3 are encouraging.

Another analysis that could reveal women’s progress in academic stature would be an examination of the pro-portion of administrative positions held by women in 1994 compared with the same proportion in 2004. Table 4 shows the gender mix ratios for all institutions in the sample both for accounting program directors, chairs, or heads and for college of business deans for 1994 and 2004. The propor-tion of female accounting program administrators grew from 7.1% in 1994 to 16.7% in 2004, whereas the proportion of female deans increased

from 2.6% to 14.6% during this same time period. For both levels of admin-istrators, the growth in the percentage of women during the 10-year period was statistically significant.

The gains made by women in achiev-ing increased representation in the administrative positions may be one of the more revealing findings in the current study because it reflects an institutional mindset to improve the gender mix in accounting and business academia. Although there are obviously more senior female faculty available now to take the administrative reins than existed in the past, this is necessary but not sufficient to explain the gains women achieved in administrative positions. Even though affected somewhat by the judgment of tenure and promotion committees and administrators, faculty promotion in aca-demic rank is largely the result of indi-viduals meeting certain minimum stan-dards for teaching, research, and service. Administrative appointments to account-ing program director or business school dean are based on significant judgment by both personnel committees within the department or college and by higher level administrators, such as provosts and uni-versity presidents. The increased percent-age of female directors and deans in the past 10 years suggests an institutional awareness of the need for greater repre-sentation of women in the academic set-ting for accounset-ting and business and a belief in the academy that achieving a proper gender balance is appropriate.

DISCUSSION

The results of this study show that women have made important gains in the past decade in increasing their represen-TABLE 2. Gender Comparison of Assistant Accounting Professors in Nondoctoral- and

Doctoral-Granting Institutions

Nondoctoral-granting institutions Doctoral-granting institutions

Year/professors’ rank Men Women Total % female Men Women Total % female

1994 Assistant professorsa 273 160 433 36.9 222 90 312 28.8

2004 Assistant professorsb 177 104 281 37.0 151 87 238 36.6

Note. The zvalues and αlevels are for two-sample proportions tests comparing the percentage of female faculty between nondoctoral- and doctoral-grant-ing institutions.

az= 2.31,α= .02. bz= .11,α= .91.

TABLE 3. Gender Comparison of Accounting Faculty in Senior Ranks Between 1994 and 2004, by Type of Institution

Nondoctoral- Doctoral-granting granting

institutions institutions Total Professors’ rank 1994 2004 1994 2004 1994 2004

Full professor

Men 260 305 311 283 571 588

Women 25 49 22 35 47 84

Total 285 354 333 318 618 672

% female 8.8a 13.8a 6.6b 11.0b 7.6c 12.5c Associate professor

Men 324 262 198 183 522 445

Women 68 103 48 64 116 167

Total 392 365 246 247 638 612

% female 17.3d 28.2d 19.5e 25.9e 18.2f 27.3f

Note. The zvalues and αlevels are for two-sample proportions tests comparing the percentage of female faculty between 1994 and 2004.

az= –1.99,α= .05. bz= –1.96,α= .05. cz= –2.91,α= .00364. dz= –3.57,α= .00035. ez= –1.70, α= .09. fz= –3.85,α= .00012. .

tation in accounting academia. Signifi-cant improvement occurred in the pro-portion of women comprising senior fac-ulty and administrative positions. For the sample institutions in this study, between 1994 and 2004, the number of tenure-track accounting faculty positions fell by almost 10% as many universities faced tougher budget constraints and lower lev-els of accounting students than existed in the golden years of business education (i.e., the 1980s). The number of male accounting faculty declined by 14.3% during this period, yet the number of female academic accountants actually grew by 7% during these 10 years.

Relative to nondoctoral-granting institutions, the underrepresentation of female accounting faculty at doctoral-granting schools that occurred in 1994 and in the prior gender-related studies (Carolfi & Pillsbury, 1996; Collins et al., 1998; Collins et al., 2000; Parker, 1995) no longer exists because women comprised an equal percentage (37%) of the accounting assistant professors at both types of institutions in 2004. The results of this study by no means imply that gender equality currently flourishes in the accounting academy. Overall, for the institutions examined in this study, women comprised only 24.5% of the total tenure-track accounting faculty positions in 2004, which is far less than the more than 50% ratio of women to men that exists in the accounting prac-tice or with accounting students in the classroom.

However, our findings do suggest that gender-mix problems in account-ing academia are beaccount-ing addressed. Given that women had such a late start relative to men in pursuing careers as

academic accountants, complete eradi-cation of the gender imbalance within the professorate will be slow in com-ing. A key to eliminating this imbal-ance is the rate at which women receive doctorates in accounting. Although still somewhat of a minority compared with men, the percentage of women receiving doctorates in accounting continues to rise (Lanier & Tanner, 1999). This, of course, explains part of the improvements women made in the last decade in increasing their proportions within accounting academia; a larger pool of terminally qualified female candidates necessarily means that more female accounting faculty will be hired rela-tive to years past. It does not, howev-er, explain all of the improvements noted in this study (e.g., the change in gender employment ratios for doctor-al-granting institutions relative to non-doctoral-granting schools, the propen-sity to appoint more women as directors and deans). These factors suggest an institutional mindset that gender balance in the accounting acad-emy is important and that continued improvement will occur in the future.

NOTE

Correspondence concerning this article should be addressed to Charles E. Jordan, College of Business and Economic Development, University of Southern Mississippi, 118 College Drive #5178, Hattiesburg, MS 39406-0001. E-mail: Jordan@ cba.usm.edu

REFERENCES

Carolfi, I. A., & Pillsbury, C. M. (1996). The hir-ing of women in accounthir-ing academia. Journal of Education for Business,71, 151–156. Collins, A. B., Parrish, B. K., & Collins, D. L.

(1998). Gender and the tenure track: Some

sur-vey evidence. Issues in Accounting Education,

13(2), 277–299.

Collins, D. L., Reitenga, A., Collins, A. B., & Lane, S. (2000). Glass walls in academic accounting: The role of gender in initial employment position. Issues in Accounting Education,15(3), 371–390.

Dwyer, P. D. (1994). Gender differences in the scholarly activities of accounting academics: An empirical investigation. Issues in Account-ing Education,9(2), 231–246.

Epps, R. W. (1991). A profile of women with a PhD, DBA, or JD degree teaching academic accounting. Journal of Education for Business,

66, 136–139.

Hasselback, J. R. (1994). Accounting faculty directory. Englewood Cliffs, NJ: Prentice-Hall. Hasselback, J. R. (2004). Accounting faculty

direc-tory. Upper Saddle River, NJ: Prentice-Hall. Lanier, P. A., & Tanner, J. R. (1999). A report on

gender and gender-related issues in the accounting professorate. Journal of Education for Business,75, 76–82.

Nelson, I. T., Vendryzk, V. P., Quirin, J. J., & Allen, R. D. (2002). No, the sky is not falling: Evidence of accounting student characteristics at FSA schools, 1995–2000. Issues in Account-ing Education,17(3), 269–287.

Norgaard, C. T. (1989). A status report on acade-mic women accountants. Issues in Accounting Education,4(1), 11–28.

Omundson, J. S., & Mann, G. J. (1994). Publica-tion productivity and promoPublica-tion of accounting faculty: A comprehensive study. Journal of Education for Business,70, 17–24.

Parker, D. J. (1995). An examination of the distri-bution of female accounting academicians:

Evi-dence of regional and institutional bias.

Unpublished manuscript, Stephen F. Austin State University, Texas.

Rama, D. V., Raghunandan, K., Logan, L. B., & Barkman, B. V. (1997). Gender differences in publications by promoted faculty. Issues in Accounting Education,12(2), 353–365. Saftner, D. V. (1988). The promotion of academic

accountants. Journal of Accounting Education,

6(1), 55–66.

Streuly, C. A., & Maranto, C. L. (1994). Account-ing faculty research productivity and citations: Are there gender differences? Issues in Accounting Education,9(2), 247–258. Zuckerman, H. (1987). Persistence and change in

the careers of men and women scientists and engineers: A review of current research. In L. S. Dixon (Ed.),Women: Their underrepresentation and career differentials in science and engineer-ing. Washington, DC: National Academic Press.

TABLE 4. Gender Comparison of Accounting Directors and Business Deans Between 1994 and 2004

1994 2004

Professor Men Women Total % female Men Women Total % female

Accounting directorsa 144 11 155 7.1 130 26 156 16.7

Business deansb 152 4 156 2.6 135 23 158 14.6

Note. The zvalues and αlevels are for two-sample proportions tests comparing the percentage of female administrators between 1994 and 2004. az= –2.60,α= .009. bz= –3.79,α= .000.