Full Terms & Conditions of access and use can be found at

http://www.tandfonline.com/action/journalInformation?journalCode=vjeb20

Download by: [Universitas Maritim Raja Ali Haji], [UNIVERSITAS MARITIM RAJA ALI HAJI

TANJUNGPINANG, KEPULAUAN RIAU] Date: 13 January 2016, At: 17:50

Journal of Education for Business

ISSN: 0883-2323 (Print) 1940-3356 (Online) Journal homepage: http://www.tandfonline.com/loi/vjeb20

Assessing Students' Accounting Knowledge: A

Structural Approach

Margaret N. Boldt

To cite this article: Margaret N. Boldt (2001) Assessing Students' Accounting Knowledge: A Structural Approach, Journal of Education for Business, 76:5, 262-269, DOI:

10.1080/08832320109599646

To link to this article: http://dx.doi.org/10.1080/08832320109599646

Published online: 31 Mar 2010.

Submit your article to this journal

Article views: 20

View related articles

Assessing Students’ Accounting

Knowledge:

A

Structural Approach

MARGARET N. BOLDT

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Murray State University

Murray, Kentucky

n recent years, formal outcomes

I

assessment of student learning has become increasingly important for accounting programs. It is no longer sufficient to evaluate student learning as measured by the subjective experience of the instructor in the classroom or even by student performance on class- room examinations. Rather, most insti- tutions and accounting programs are required to have a formal outcomes assessment program. For example, any school desiring accreditation by the American Assembly of Collegiate Schools of Business-The International Association for Management Education (AACSB) must comply with this orga- nization’s requirement for outcomes assessment.In a recent article, Barbara Apostolou

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

(1999) discussed four common outcome

measurements: standardized tests, per- formance assessment, alumni surveys, and employer surveys. Certainly, all of these measures provide accounting pro- grams with valuable data about student preparedness for employment, satisfac- tion with their education, ability to “per- form” on standardized tests, and so forth. However, none of these measures adequately addresses the question of whether students possess the necessary accounting knowledge to become accounting experts. Of course, account- ing knowledge is only one capability of

262

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Journal of Education forzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

BusinessABSTRACT. This study explored a structural approach to assessing stu- dents’ accounting knowledge. An “expertise” knowledge structure of basic financial accounting concepts was constructed, and students’ knowl- edge structures of the same concepts were then compared with the “exper- tise” knowledge structure. Data were collected from respondents at a large public university to demonstrate the procedure and method of analysis. The procedure has the potential for providing accounting programs with valuable information regarding their students’ knowledge after completing a course or program of study.

several mentioned by the Accounting Education Change Commission ( 1 990).

Importantly, accounting knowledge is the one capability that accounting pro- grams must address internally. Other aspects of the collegiate experience are unlikely to make significant contribu- tions to students’ accounting knowl- edge. Hence, the onus is on accounting programs to assess whether students have the necessary knowledge when completing courses or programs.

In the present study, I assessed stu- dents’ accounting knowledge by using an “expertise,” or benchmark, knowl- edge structure that can be compared with students’ knowledge structures. The procedure may provide accounting programs with important information concerning students’ knowledge gaps.

Furthermore, the approach is relatively easy to implement and can be used to assess knowledge in various areas of accounting (e.g., auditing, taxation).

Assessing Knowledge Structures

Goldsmith, Johnson, and Acton

(1991) outlined a three-step process for

implementing a structural approach to capturing knowledge in a specific domain. The first step in this process is knowledge elicitation, essentially the accessing of participants’ organization of memory for a set of concepts rele- vant to the domain being investigated. Although there are several models for memory structures in the literature (e.g., network models, feature models), all of them rely on the idea that concepts vary along some continuum of psycho- logical proximity, or relatedness, in memory (Schvaneveldt, Durso, Gold- smith, et al., 1985). For the present

study, I used participants’ pairwise rat- ings of relatedness among concepts in financial accounting to access partici- pants’ memory structures.

The second step in the structural approach is defining a representation for the knowledge elicited from participants (Goldsmith et al., 1991). There are sever-

al procedures available for representing knowledge elicited in the form of pair- wise relatedness ratings. Network mod-

els depict local relationships by connect- ing nodes (representing concepts) with weighted links (representing relation- ships between concepts; Schvanaveldt et al., 1985). Importantly, network models do not limit the relationships that can be represented, The present study focused primarily on identifying the necessary relationships between financial statement items that are necessary for expertise and the extent to which two student groups have these relationships in their organi- zation of memory. As a result, elicited knowledge is via linkweighted network models.

The final step in Goldsmith and col- leagues’ (1991) structural approach is evaluating the knowledge representa- tions relative to some standard. Hence, students’ knowledge structures are eval- uated relative to an “expertise” struc- ture. Additionally, concepts that are not well defined are classified as being over-, under-, or misdefined based on the presence or absence of idiosyncratic

and critical links.

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

I

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Knowledge Representations for Teachers and Students

Seven accounting teachers at a large public university in the southwestern

United States served as experts. ’ h o

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

ofthese participants had no practical expe- rience in either public accounting or private industry. However, both of them had over 15 years of teaching experience at the college level and had presumably spent several thousand hours solving accounting problems. These two partic- ipants, then, could be considered experts at accounting problem solving even though they lacked practitioner experience. The remaining five educa- tors all had some practical experience.

Eleven students enrolled in the cap- stone course for the master’s of accoun- tancy degree served as one group of stu- dent participants. None of these students had ever been employed as an accountant, but all had completed the courses required in an undergraduate accounting major. The final group of

participants consisted of

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

8 students whohad completed an introductory financial accounting course satisfactorily (i.e., received a grade of C or better).

I reviewed examples of financial

statements to select 20 concepts that would be familiar to all groups of par- ticipants. Participants rated the 20 con-

cepts by judging the degree of “related- ness” between two items in a given pair

on a scale of 1 (not related) to 9

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

(veryrelated). Each participant completed all

possible painvise ratings for the 20 con- cepts, totaling 190 pairs. (See Table 1 for a list of the 20 items.) Application of the Pathfinder’ algorithm to respon- dents’ painvise ratings produced link- weighted network models.

Results and Discussion

Pearson product-moment correlations were computed for each participant’s ratings with every other participant’s rat-

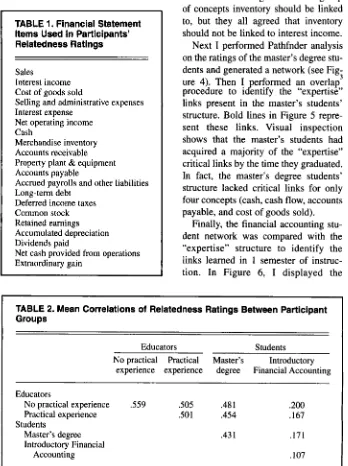

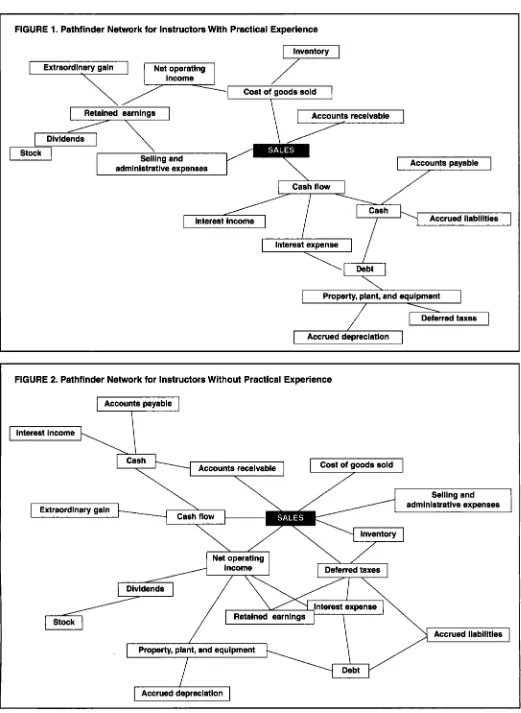

TABLE 1. Financial Statement Items Used in Participants’ Relatedness Ratings

Sales

Interest income

Cost of goods sold

Selling and administrative expenses Interest expense

Net operating income Cash

Merchandise inventory Accounts receivable Property plant & equipment Accounts payable

Accrued payrolls and other liabilities Long-term debt

Deferred income taxes

Common stock

Retained earnings

Accumulated depreciation Dividends paid

Net cash provided from operations Extraordinary gain

ings. The mean correlations of the ratings are shown in Table 2. These results show that the master’s degree students had a relatively high level of agreement with teachers, whereas the financial account- ing students disagreed with both advanced students and teachers.

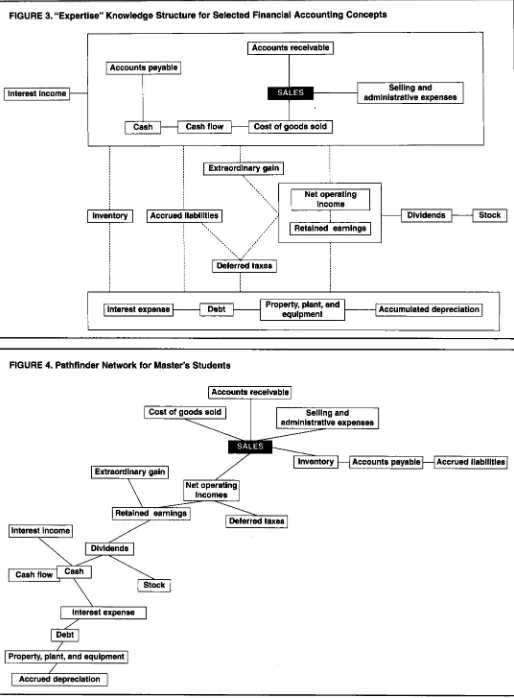

[image:3.612.223.571.269.735.2]I performed Pathfinder analyses on the educators’ networks to identify sep- arately the links for educators with prac- tical experience and the links for those without practical experience. The resulting networks are displayed in Fig- ures 1 and 2. A composite “expertise” knowledge structure was then compiled by overlaying the two networks (see Figure 3).* The dashed lines in Figure 3

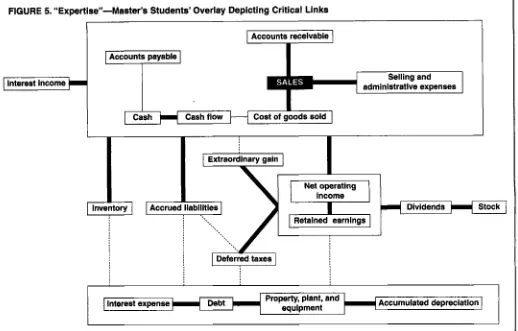

represent “flexible” links. For example, educators did not agree on which group of concepts inventory should be linked to, but they all agreed that inventory should not be linked to interest income. Next I performed Pathfnder analysis on the ratings of the master’s degree stu- dents and generated a network (see Fig-

ure

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

4).

Then I erformed an overlap procedure to igntify the “expertise”links present in the master’s students’

structure. Bold lines in Figure

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

5 repre-sent these links. Visual inspection shows that the master’s students had acquired a majority of the “expertise” critical links by the time they graduated. In fact, the master’s degree students’ structure lacked critical links for only four concepts (cash, cash flow, accounts payable, and cost of goods sold).

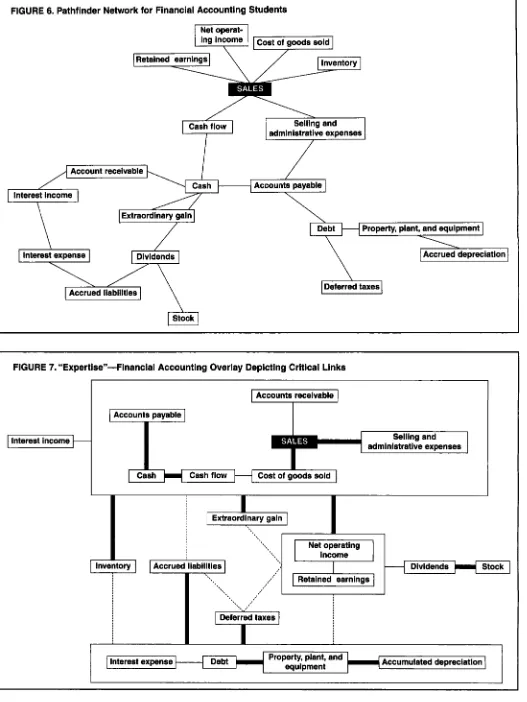

Finally, the financial accounting stu- dent network was compared with the “expertise” structure to identify the links learned in 1 semester of instruc- tion. In Figure 6, I displayed the 3

TABLE 2. Mean Correlations of Relatedness Ratings Between Participant Groups

Educators Students

No practical Practical Master’s Introductory experience experience degree Financial Accounting

Educators

No practical experience

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

3 9 .so5 .48 1 .200Practical experience .so1 .454 .167

Master’s degree .43 1 ,171

Introductory Financial Students

Accounting ,107

May/June 2001 263

FIGURE 1. Pathfinder Network for Instructors With Practical Experience

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Extraordinary gain Net operating

I

inventoryI

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

7-

Accounts payable administrative expenses

Cash flow

interest income Accrued liabilities interest expense

-4,

Property, plant, and equipment

/

/

I

Accrued depreciationI

FIGURE 2. Pathfinder Network for Instructors Without Practical Experience

Accounts receivable Accounts receivable

\ \ /

Selling and administrative expenses

inventory

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

1

HLz-

Net operatingDeferred taxes Dividends

interest expense Retained earnings

Stock

Accrued liabilities

I

/ I

Property, plant, and equipment

Debt Accrued depreciation

264

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

JournalzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

of Education for Business [image:4.612.49.570.31.744.2]FIGURE 3. “Expertise” Knowledge Structure for Selected Financial Accounting Concepts

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

I

. .

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

I II

I

Interest income fI

Accounts receivableI

Selling and administrative expenses

I

Cash flow

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

t--l

Cost of goods soldI

j

I

Extraordinary gainI

1

Accrued’liabliitiesI

j

...

,.’1

+,

,,,*’ Retained earnings

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

4

- -

Dividends StockI

I 1

I I

{Accumulated depreciation

1

1

Property, plant, andeaulment Debt

FIGURE 4. Pathfinder Network for Master’s Students

I Accounts receivable I

Cost of goods sold Selling and administrative expenses

Inventory

H

Accounts payableH

Accrued liabilities Net operatingI

I

incomesI

1

Retained earningsI

Deferred taxes interest incomeDividends

[

Cash flowI

CashI

\

I

Interest expenseI

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

I

I

Property, plant, and equipmentI

&

Accrued depreciationzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

May/June

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

2001 265FIGURE 5. “Expertise”-Master’s Students’ Overlay Depicting Critical Links

Accounts receivable

Accounts payable

Selling and

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

I

Interest income administrative expensesCash Cash flow Cost of goods sold

I

Debt Accumulated depreciation

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Pathfinder network for the financial accounting students’ ratings, and in Fig- ure 7 I show the overlap with the “expertise” structure. The results demonstrate that the financial account- ing students had not acquired many of the critical links necessary for expert- level problem solving. In fact, critical links were absent for nine of the items. However, one of the critical links that was missing in the master’s students’ network was present in the financial accounting students’ network, implying that that relationship somehow degrades and/or decays with time.

To quantify the similarity and identi- fy the specific differences between the student structures and the “expertise” structure, I analyzed and classified each concept as either well-defined, misde- fined, overdefined, or underdefined. This classification was based on the presence or absence of idiosyncratic links (i.e,, links present only in the stu- dent structure) and the presence or absence in the student structure of all critical links (i.e., links present in the “expertise” structure). Items with all of

266

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Journal ofzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Education for Businessthe critical links and no spurious links are well-defined. Misdefined items do not have all of the critical links but do have some idiosyncratic links. Overde- fined concepts have extraneous links but also have all of the critical links, where- as underdefined concepts lack spurious links but also are missing some critical

links. The data in Table

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

3 show the clas-sification for each of the items by group. The results are consistent with the mean correlations presented earlier. As expected, the master’s students had many well-defined concepts and only a few mis-, over-, and underdefined items. The financial accounting students, on the other hand, had very few well- defined items compared with the mas- ter’s students.

A closer examination of the specific items that were not well defined by the master’s students yields some interest- ing insights. First, it is perhaps not sur- prising that cash was a misdefined item. Knowledge of the subtle interrelation- ships that cash has with other accounts probably may be acquired only through solving many problems involving sever-

al periods. That is, routinized knowl- edge for this item may come from expe- rience with complete cash cycles, rather than through isolated transactions. Although master’s students would cer- tainly have been exposed to some multi- period problems, the vast majority of problems in accounting courses deal with only one effect on cash at a time.

Two of the underdefined items (accounts payable and cost of goods sold) deal explicitly with the product cycle. A possible explanation for this result is that students generally take rel- atively few (only two) courses that deal with product costing and the manufac- turing cycle. The overdefined items, in contrast, are both related to financing activities and receive a great deal of exposure over many courses. However, the coverage is generally indirect in that these accounts are related to the items actually being taught (e.g., debt and stock). Additionally, the related accounts are covered frequently because of the complexity involved in accounting for transactions affecting these accounts. Possibly, the master’s students have

FIGURE 6. Pathfinder Network for Financial Accounting Students

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Interest expense Dividends

I

Cost of goods soldI

Accrued depreciation

I

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

\ /

inventory

\

/

Retained earnings

1

Accrued liabilities Dividends Stock

7

1

administrative exDenses

.*.

. ,

. ,

** I, [image:7.612.48.575.50.752.2]Deferred taxes

FIGURE 7. “Expertise”-Financial Accounting Overlay Depicting Critical Links

I Interest income I

Accounts receivable

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

I

I

Accounts payableI

I . - I

I

I JI

Accumulated depreciation Property, plant, and

equipment interest expense Debt

I

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

May/June

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

2001 267 [image:7.612.45.564.56.405.2]TABLE 3. Item Classifications for Financial Statement Items

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Item Introductory Financial classification Master’s degree students Accounting students Well-defined Sales

Interest income

Selling and administrative expenses Net income Inventory Accounts receivable Property Accrued liabilities Debt Deferred taxes Stock Retained earnings Accumulated depreciation Extraordinary gain Misdefined Cash

Overdefined Interest expense Dividends Underdefined Accounts payable

Costs of goods sold Cash flow Inventory Property Debt Deferred taxes Stock Accumulated depreciation Extraordinary gain Sales Cash flow Interest income Interest expense Accounts receivable Dividends Debt

Selling and administrative Accounts payable Cash

Accrued liabilities Costs of goods sold Net income Retained earnings

expenses

erroneously attributed the complexity of accounting for related items to the overdefined items. Last, cash flow is underdefined. Discussions with teachers at the institution revealed that cash flow is generally covered at the end of cours- es in a somewhat cursory fashion.

Unlike the master’s students’ classifi- cations, the results of the financial accounting students did not seem to have underlying themes related to the type of activity. Rather, six of the seven well- defined items were located on one finan- cial statement, the balance sheet. The seventh item, extraordinary gain, usually was related to transactions that affect the

balance sheet. The other

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

13 items thatwere not well defined all were related to one of two types of transactions: infre- quent transactions and accruals. Items related with infrequent transactions (div- idends and debt) have many rules asso- ciated with them and probably require

268

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

JournalzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

ofzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Education for Business more than 1 semester of experience totransfer into routinized knowledge. The remaining 11 mis-, under-, and overde- fined items all relate in some way to accrual accounting. Obviously, introduc- tory students do not have a good under- standing of accrual-basis accounting after 1 semester of instruction.

General Discussion and Concluding Remarks

In this study, I explored the use of a

structural approach for assessing stu- dents’ knowledge structures for finan- cial accounting concepts. This approach provides a more complete picture of the knowledge gained from a course or pro- gram of study. That is, the structural approach simultaneously provides information about the concepts or rela- tionships that students do not under- stand and those they do understand.

Importantly, this approach provides lit-

tle information about what students can do with the knowledge (i.e., practical skills) and would be used most effec- tively in conjunction with other assess- ment procedures.

This exploratory study’s results indi- cate that beginning students at the par- ticular institution under investigation are not obtaining a complete understanding of accrual-basis accounting, a primary goal of the course. Additional research is needed to determine exactly how this knowledge gap can be filled earlier in the degree program. A possible starting point for this research might be the use of a pre- and posttest procedure to iden- tify precisely which relationships cur- rently are being acquired in the course. This study also provides encouraging feedback regarding graduating students, who seem to have acquired most of the essential links for expertise.

Finally, this study had several limita- tions that could be addressed in future research. First, results could be more generalizable with participants from several institutions. Additionally, a lon- gitudinal study in which participants provide ratings after several courses would help identify when and how “expertise” knowledge is acquired.

NOTES

1. The information provided on Pathfinder relies heavily on Schvanaveldt, Durso, and Dearholt (1989). For further information on Pathfinder, consult that article or the documenta- tion available with the software (KNOT PC soft- ware).

2. I adapted this procedure from the analysis in

Schvanaveldt et al. (1985) to arrive at the “right

stuff’ for expertise.

3. This overlap procedure differs from the overlay in that it identifies only the links shared between the two structures. In contrast, the over- lay procedure depicts the links that are in either structure.

ACKNOWLEDGMENT

This article benefited greatly from comments provided by Stephen Butler, Francis Durso, and participants of the University of Tulsa Accounting

Research Symposium and the Sixth Annual Meet- ing of the American Society of Business and Behavioral Sciences.

REFERENCES

Accounting Education Change Commission (AECC). (1990, Fall). Objectives of education for accountants: Position Statement No. I .

Issues in Accounting Education. 307-3 12. Apostolou, B. (1999). Outcomes assessment.

[image:8.612.50.381.73.449.2]Issues in Accounting Education,

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

14( I ) ,zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

edge network organizingzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

toolfor IBM PC corn- Schvanaveldt, R.. Durso, E, Goldsmith, T., Breen, 177-197. T., Cooke, N., Tucker, R.,zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

& De Maio, J. Goldsmith, T., Johnson, P., & Acton, W. (1991). (1985). Measuring the structure of expertise.Assessing structural knowledge. Journal of International Journal

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

of Man-MachinezyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Studies, patibles. Las Cruces, NM: Interlink, Inc.Schvanaveldt, R., Durso, F., & Dearholt, D. (1989). Network structures in proximity data.

Educational Psychology, 83,88-96. The Psychology of Learning and Motivation, 23,699-728. 24,249-284.

KNOT PC Software. (1990). KNOT-PC: Knowl-

JOURNAL OF

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

EDUCATION

FOR

BUSINESS

...

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

.W. ..B . B W...

.B.... .

YES!

I would like to order a one-year subscription to the Journal of Education.

.

.

ORDER FORM W

for Business published bi-monthly. I understand payment can be made to Heldref

Publications or charged to my VISAh4asterCard (circle one).

$41 .00 Individuals

m

$70.00 InstitutionsACCOUNT # EXPIRATION DATE

SIGNATURE

NAMEllNSTlTUTlON

.

.

ADDRESS

.

CITY/STATE/ZI P COUNTRY

W

ADD $15.00 FOR POSTAGE OUTSIDE THE U S . ALLOW 6 WEEKS FOR DELIVERY OF FIRST ISSUE.

SEND ORDER FORM AND PAYMENT TO:

.

HELDREF PUBLICATIONS, Journal of Education for Business

1319 EIGHTEENTH ST., NW, WASHINGTON, DC 20036-1802 PHONE (202) 296-6267 FAX (202) 293-6130

SUBSCRIPTION ORDERS 1(800)365-9753, www.heldref.org

The Journal of Education

for Business readership

includes instructors, supervi-

sors, and administrators at

the secondary, post- secondary, and collegiate levels. The Journal features basic and applied research- based articles in accounting, communications, economics, finance, information sys- tems, management, market- ing, and other business dis- ciplines. Articles report or share successful innovations, propose theoretical formula- tions, or advocate positions on important controversial issues and are selected on a blind, peer-reviewed basis.