Full Terms & Conditions of access and use can be found at

http://www.tandfonline.com/action/journalInformation?journalCode=vjeb20

Download by: [Universitas Maritim Raja Ali Haji], [UNIVERSITAS MARITIM RAJA ALI HAJI

TANJUNGPINANG, KEPULAUAN RIAU] Date: 13 January 2016, At: 17:33

Journal of Education for Business

ISSN: 0883-2323 (Print) 1940-3356 (Online) Journal homepage: http://www.tandfonline.com/loi/vjeb20

Using an Investment Project to Develop

Professional Competencies in Introduction to

Financial Accounting

Lola Woodard Dudley , Henry H. Davis & David G. McGrady

To cite this article: Lola Woodard Dudley , Henry H. Davis & David G. McGrady (2001) Using an Investment Project to Develop Professional Competencies in Introduction to Financial Accounting, Journal of Education for Business, 76:3, 125-131, DOI: 10.1080/08832320109601299

To link to this article: http://dx.doi.org/10.1080/08832320109601299

Published online: 31 Mar 2010.

Submit your article to this journal

Article views: 23

View related articles

Using an

Develop Pro

nvestment Project to

‘essional Competencies

in Introduction to Financial

Accounting

LOLA WOODARD DUDLEY

HENRY H. DAVIS

DAVID G. MCGRADY

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Eastern Illinois University Charleston, Illinois

ntroductory Financial Accounting

I

may be viewed as either students’firstaccounting course or their

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

last account-ing course. The difference between the objectives and emphasis of these two views is profound. Introductory Finan- cial Accounting has traditionally been viewed as the first accounting course, so faculty have stressed preparing entries and financial statements to lay a foun- dation for continued study in account- ing. By using the preparer approach, the course has emphasized bookkeeping and neglected the use of accounting as a decisionmaking tool.

On the other hand, if Introductory Financial Accounting is viewed as the last accounting course a student will complete, its emphasis must be on using accounting to support economic deci- sionmaking. The Accounting Education Change Commission emphasized this point in its position statement on the course:

The primary objective

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

. . .

is for studentsto learn about accounting as an informa- tion development and communication function that supports economic decision-

making. The knowledge and

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

skills pro-vided by the first course in accounting should facilitate subsequent learning even if the student takes no additional academ- ic work in accounting or directly related disciplines. (AECC, 1992)

Because the vast majority of students taking Introductory Financial Account-

ABSTRACT.

This article describes an investment project used to stimu- late student interest in and understand- ing of business, economics, finance, and the uses and limitations of accounting information. Student groups invest in a portfolio of stocks after completing an analysis of finan- cial information. Project success is evaluated through assessment of eco- nomic decisionmaking skills, financial statement analysis, understanding of underlying accounting concepts and procedures, portfolio outcome, portfo- lio goals, effectiveness of cornmunica- tion, and oral presentations. In com- pleting the project, students develop competencies needed for success in business careers.ing are not accounting majors, the course should be viewed as the last accounting course and, therefore, have a user emphasis. In fact, accounting majors also would be served better by this approach. Success in the accounting profession requires skill sets different from those needed by bookkeepers, which suggests that accounting students should experience situations faced by accountants-rather than the problems facing bookkeepers.

A user-focused course concentrates on building competencies that graduates need to be successful in a business career (Gordon & Howell, 1959; Muse, 1983; Pierson, 1959; Porter & McKib- bin, 1988). Accounting professionals

have provided inventories of the capa- bilities needed for success in an accounting career in the Bedford Com- mittee Report (1986), the Big Eight

White Paper (Perspectives on Educa- tion, 1989), and the AECC’s Position

Statement No. One ( 1 990).

In the most ambitious and promising effort to date, a task force associated with the American Institute of Certified Public Accountants (AICPA) developed the AICPA Core Competency Frame- work for Entry Into the Accounting Pro- fession (AICPA, 1999), which identifies

core functional, personal, and broad business competencies needed by entry- level accountants. Though focused on students majoring in accounting, many of these competencies are equally applicable to all business graduates. In fact, one section deals with “broad busi- ness perspective competencies.”

To develop these competencies, stu- dents must be active learners. Active learning experiences dramatically influ- ence student perceptions of business (Baldwin & Ingram, 1991), enhance the

acquisition and retention of accounting information (Costin, 1972; Eble, 1983;

McKeachie & Kulik, 1975), increase

student “buy-in” (internalization) and commitment to course assignments, and develop students’ higher cognitive abili- ties (NIE, 1984).

In this article, we describe an active

January/February 2001 125

learning project that develops the research, computer, communication, and decisionmaking skills of students. Students develop research skills while obtaining information via the World Wide Web (WWW) and the library. (In Appendix A, we provide a list of poten- tial WWW class exercises relevant to particular phases of the project.) Stu- dents’ computer skills are enhanced through the use of spreadsheet and word processing software and e-mail to com- municate the results of their inquiries or maintain contact with group members and the instructor. Decisionmaking skills are developed because students “self-discover” the usefulness and limi- tations of accounting information in an investment scenario.

This project, therefore, mimics real- world uses of accounting information. Actively engaged students must evalu- ate the usefulness and limitations of accounting information in completing each task. Students learn and under- stand accounting principles and proce- dures as a by-product of task comple- tion rather than as an objective itself.

The Investment Project is used to stimulate student interest in business, economics, finance, and the uses and limitations of accounting information. Each student group invests a given lump sum in a portfolio of stocks. Project suc- cess is evaluated on the basis of eco- nomic decisionmaking skills, financial statement analysis, understanding of underlying accounting concepts and procedures, portfolio outcome, portfolio goals, effectiveness of communication, and oral presentations.

By integrating the analysis of finan- cial information contained in annual reports with the selection of a stock portfolio, students get timely feedback from the financial markets on the wis- dom of their analysis. This not only sharpens their skills in financial state- ment analysis, but also develops their confidence in their ability to construct a stock portfolio matching their threshold

for investment risk.

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Investment Project

Introductory accounting students are fascinated with the stock market, invest- ments, and their potential for producing

126

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Journal of EducationzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

for Businessvast wealth (with little overt effort). This project uses such student “hot but- tons” to introduce them to the uses and preparation of accounting information. The project work is completed outside of class, after the underlying concepts have been covered. In Table 1, we pre- sent an outline of the project and the competencies it develops.

Project Implementation

tor poses the following questions: On the first day of class, the instruc-

What is accounting?

Who uses accounting information? How is accounting information used?

The questions underscore for students the view that accounting information is used for decisionmaking, which is the fundamental premise underlying this project. This concept is reinforced throughout the semester. Understanding the uses of accounting information is critical even for accounting majors. To provide useful information, accountants must understand the decisions that users are making and how accounting informa- tion fits into the decisionmaking process.

Phase 1-Company Selection

As the initial project assignment, stu- dents must select a company and obtain its annual report for the most recent year. They are encouraged to pick a company that interests them. If a stu- dent has received stock as a gift, she or he often will choose that company for evaluation. Students’ and their families’ present and past employers are also good candidates. Alternatively, they may select a firm from annual reports available from the Wall Street Journal Annual Reports Service. No duplication is allowed; as soon as a firm is selected, the student must announce it on the class e-mail account.

One by-product of this assignment is

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

a discussion of service, merchandising, and manufacturing firms. Many stu- dents are more comfortable with service and merchandising concerns because financial accounting textbooks general- ly focus on them. Knowledge of the complexities of manufacturing account-

ing, however, is not a prerequisite for analysis of manufacturers’ financial statements.

Inclusion of manufacturers makes interfirm comparisons more diverse and interesting. Selection of foreign-based companies is discouraged, however, because their complexities can frustrate students in their first financial account- ing course. If foreign company annual reports can be obtained, however, they offer many opportunities to internation- alize the course (Ramaglia, 1998).

Phase 2-Preliminary Analysis

During coverage of the accounting cycle or upon its completion, students are introduced to financial statement analysis. This introduction includes mea- sures of liquidity, profitability, and sol- vency. Each student then performs a pre- liminary analysis on her or his company. In addition to analyzing the financial statements, students obtain current information regarding their company from the World Wide Web, including the 52-week high and low prices for the company’s stock, projected current year’s earnings per share, price-earnings ratio, stock analysts‘ recommendations, and the stock’s beta. This information is obtained by entering the company’s ticker symbol at <www.yahoo.com> or a similar Web site. During this informa- tion-gathering stage, students complete in-class exercises designed to develop research skills required to evaluate the quality of data.

It is important to spend time helping students understand the information they have gathered that is not covered in their textbook. For example, once students understand how a stock’s beta measures its volatility, they can make more informed decisions when constructing either an aggressive or a conservative portfolio. Also, students need to under- stand the role of stock analysts’ recom- mendations and earnings-per-share pro- jections on stock price changes.

We generally spend a great deal of time discussing the role of analysts and ethical considerations (such as analysts’ “tweaking” of financial statements and “whispering” of EPS estimates). Stu- dents gradually recognize the focus of the stock market and of decisionmakers

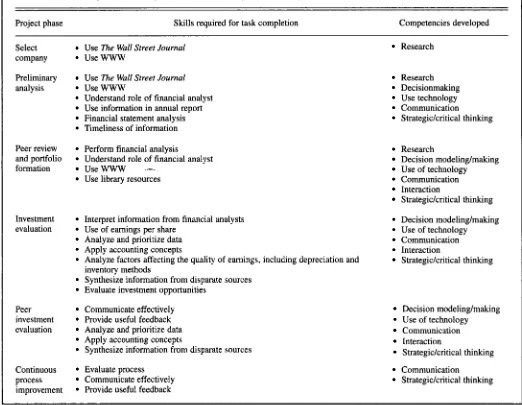

TABLE 1. Skills Required to Complete Investment Project and Competencies Developed

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Project phase Skills required for task completion Competencies developed

Select company

Preliminary analysis

Peer review and portfolio formation

Investment evaluation

Peer investment evaluation

Continuous process improvement

Use

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

The Wall Street JournalUseWWW

Research Use The Wall Street Journal

UseWWW

Understand role of financial analyst Use information in annual report Financial statement analysis Timeliness of information Perform financial analysis

Understand role of financial analyst Use library resources

Use WWW

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

..--Interpret information from financial analysts Use of earnings per share

Analyze and prioritize data Apply accounting concepts

Analyze factors affecting the quality of earnings, including depreciation and Synthesize information from disparate sources

Evaluate investment opportunities Communicate effectively Provide useful feedback Analyze and prioritize data Apply accounting concepts

Synthesize information from disparate sources Evaluate process

Communicate effectively Provide useful feedback inventory methods

Research Decisionmaking Use technology Communication

Strategic/critical thinking Research

Decision modeling/making Use of technology Communication Interaction

Strategic/critical thinking Decision modeling/making Use of technology Communication Interaction

Strategic/critical thinking Decision modeling/making Use of technology Communication Interaction

Strategic/critical thinking Communication

Strategic/critical thinking

on future events. Many questions are raised about the usefulness of financial statements’ historical information in decisionmaking for future events.

Phase 3-Portfolio Formation

After the first exam, when class enrollment is stabilized, students are assigned to heterogeneous teams based on first test grade, selected companies, and other grouping factors. For some

factors, we

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

try to increase diversity (e.g.,major), and for others to minimize diver- sity (e.g., industry). Teams are not final- ized until after the first exam, to mini- mize wholesale reconfiguring due to student drops andor student inactivity.

After the groups have been formed by the instructor, each student exchanges annual reports with a classmate who is

not a member of his

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

or her group. Thepurpose of this exchange is twofold. First, early in the project students will see the wide variety of information that they will encounter when looking at ratios of two different companies. Sec- ond, each company is analyzed by members of two different groups, so both groups have the opportunity to invest in that stock. Later in the semes- ter, this exchange diminishes com- plaints that one group was blessed with a “hot stock” that no other group had the opportunity to purchase.

Each group then compiles the infor- mation contained in its preliminary analysis for the 8-10 stocks that group members have evaluated. The groups spend a class day discussing the invest- ment attributes of their stocks and then allocate the hypothetical $100,000 that

each group has available to invest. The parameters for their investment alloca- tion are relatively simple. They can invest the $100,000 in any fashion they desire, but they must invest the entire $100,000. They cannot place a portion of their funds in “cash.” They can invest any amount they desire in a particular stock, from nothing to the entire $100,000. Each stock can be selected by two groups, not just one.

In some semesters, the instructor has entered the groups’ stock portfolio information into a Web page established at <http://www.my.yahoo.com>. The

portfolios are recorded when the market is closed to ensure that each portfolio begins with a $100,000 balance. Be- cause the instructor was responsible for entering selections of students, no trad-

ing was allowed. Students “lived or

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

January/February 2001

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

127 [image:4.612.44.566.62.467.2]died” with their original analysis and

stock selection(s). Lacking

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

an option totrade, students had to make decision(s) without the possibility of revision. The remainder of the semester focused on the rationale for their decisions and evaluation of alternative information sources and how students used them.

In other semesters, the class partici- pated in the Final Bell investment game found at <http://www.sandbox.net/ finalbell/>. Student groups were al- lowed to trade securities according to the Final Bell rules. Weekly, each stu- dent group submitted a memo to the instructor describing the value of the group portfolio, explaining changes in its value and reasons for any trades. Each group was required to include a “linked” spreadsheet graph showing the value of the student portfolio for each

week. In Table

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

2, we identify “portfo-lio” sites recently available on the Web. Because information available on the Web changes frequently, the portfolio sites included may vary. The site

<http://directory.netscape.com/Business

/Investing/Games> provides a directory of investing games.

In both the trading and nontrading approaches, the daily gyrations of each group’s portfolio become a great source of pride and frustration as the group members see their portfolios rise and sink in relation to those of their peers. When no trading is allowed, the instruc- tor distributes information about the value of all portfolios at the start of

class. Many students track the value of their portfolio independently and come to class with a smile on their face when they know their stocks are up $3,000 that morning. Because the portfolios are generally selected 1 month into the semester, the students have roughly 2 months to monitor the performance of their selections. Groups tend to gel as members unite behind their success, or lack of it, with their portfolio. These groups function more effectively on group assignments throughout the

remainder of the semester.

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Phase 4 -Investment Evaluation

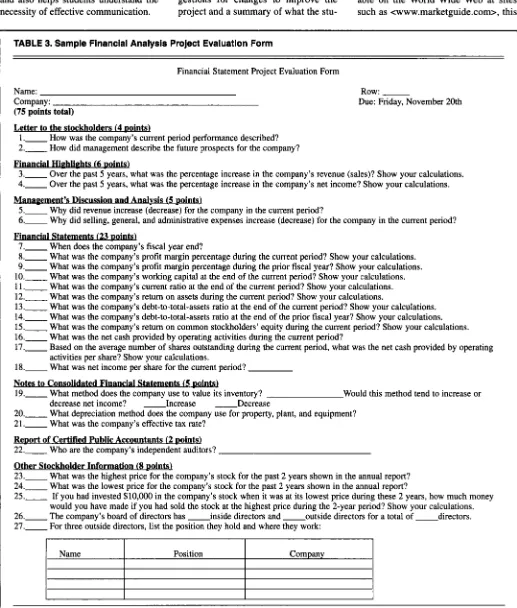

Each student prepares a comprehen- sive analysis of her or his company (see Table 3 for evaluation form). The analy-

sis includes qualitative as well as quan- titative information from the company’s annual report. For example, students summarize prospects for the coming year as discussed in the letter to share- holders, the sources of increased rev- enue during the current period as explained in management’s discussion, articles from the financial press about the company, and the composition of the corporate board in terms of inside and outside directors.

The analysis also includes an evalua- tion of the quality of the earnings andor earnings per share reported by the com- pany. By the end of the semester, most students understand the implications of accounting choices-such as accelerat-

ed depreciation and the LIFO inventory method on earnings per share-because they have been the basis of discussions and exercises. Knapp (1998) includes excellent coverage of the process of assessing earnings quality in his finan- cial accounting text.

The students also include their rec- ommendations regarding the investment potential of that stock. Because by this time they have reviewed the company’s financial statements, gathered informa- tion on expected future earnings, and followed the performance of the stock throughout the semester, most students will feel capable of making such informed decisions on investment.

Phase 5-Peer Evaluation of Individual Company Analysis

The comprehensive analysis, annual reports, and supporting materials are exchanged during the last week of class. Each student reviews another student’s report and independently verifies the quantitative content and the qualitative assessments of the report. The peer evaluation requires the students to apply critical thinking skills when assessing the work of their peers and provides additional exposure to the writing and analysis skills of others. In addition, the quantitative analysis serves as a review for components of the final exam.

Student projects are evaluated through the instrument shown in Table 3. In completing this evaluation, stu-

TABLE 2.

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Www Portfolio SitesName URL Can set up class account Investment Challenge

Investsmart Market Simulation Smart Stocks

Stock Trak E*Trade Edustock

Fantasy stock market Final Bell

League of American Investors Mainxchange

Nordby Stock Contest Virtual Stock Exchange Vstock

Yahoo Investment Challenge

www.ichallenge.net

library.advanced.org/10326/market-simulation/index.html www.smartstocks.com/

www.stocktrak.com/ game.etrade.com library.advanced.org/30 www.fantasystockmarket.com

www.sandbox.net/finalbell/pub-dochome. html investorsleague.com/

www.mainxchange.com

www.nordby.com/challenges/thegame/

www.virtualstockexchange.com/

www.vstock.com/cgi-bin/w3-msql/user.htm contest.finance.yahoo.com/t 1 ?u

Yes Yes Yes Yes No No No No

No No

No No No No

128

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

JournalzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

of Education for Businessdents use skills ranging from rote recall dent learned. Past suggestions have

to analysis and synthesis. Instructor

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Improvement included (a) inclusionzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

of industryevaluation of the Investment Project is ratios in the project and (b) permitting limited to written materials. This The peer evaluation and comprehen- students to trade stocks. (Because

reduces the time required for grading sive analysis components require sug- industry ratios are

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

now readily avail-and also helps students understand the gestions for changes to improve the able on the World Wide Web at sites necessity of effective communication. project and a summary of what the stu- such as <www.marketguide.com>, this

Phase &Continuous Process

TABLE 3. Sample Financial Analysis Project Evaluation Form

Financial Statement Project Evaluation Form

Name: Company:

(75 points total)

Row:

Due: Friday, November 20th

Letter to the stockholders (4 points)

1

.-

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

How was the company’s current period performance described? 2.- How did management describe the future prospects for the company?3.- Over the past

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

5 years, what was the percentage increase in the company’s revenue (sales)? Show your calculations.4.- Over the past 5 years, what was the percentage increase in the company’s net income? Show your calculations.

5.- Why did revenue increase (decrease) for the company in the current period?

6.- Why did selling, general, and administrative expenses increase (decrease) for the company in the current period?

7.- When does the company’s fiscal year end?

8.- What was the company’s profit margin percentage during the current period? Show your calculations. 9.- What was the company’s profit margin percentage during the prior fiscal year? Show your calculations.

Financial Hiphlights (6 points)

Management’s Discussion and Analvsis (5 points) Financial Statements (23 points)

10.- What was the company’s working capital at the end of the current period? Show your calculations. 11

.-

What was the company’s current ratio at the end of the current period? Show your calculations. 12.- What was the company’s return on assets during the current period? Show your calculations.13.- What was the company’s debt-to-total-assets ratio at the end of the current period? Show your calculations.

14.- What was the company’s debt-to-total-assets ratio at the end of the prior fiscal year? Show your calculations.

15.- What was the company’s return on common stockholders’ equity during the current period? Show your calculations. 16.- What was the net cash provided by operating activities during the current period?

17.- Based on the average number of shares outstanding during the current period, what was the net cash provided by operating activities per share? Show your calculations.

18.- What was net income per share for the current period?

Notes to Consolidated Financial Statements (5 points]

19.- What method does the company use to value its inventory?

20.- What depreciation method does the company use for property, plant, and equipment? 21

.-

What was the company’s effective tax rate?Report of Certified Pu blic Accountants (2 points)

22.- Who are the company’s independent auditors?

Other Stockholder Information (8 points)

23.- What was the highest price for the company’s stock for the past 2 years shown in the annual report?

24.- What was the lowest price for the company’s stock for the past 2 years shown in the annual report?

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

25.- If you had invested $10,000 in the company’s stock when it was at its lowest price during these 2 years, how much money would you have made if you had sold the stock at the highest price during the 2-year period? Show your calculations. 26.- The company’s board of directors has -inside directors and - outside directors for a total of - directors. 27.- For three outside directors, list the position they hold and where they work

Would this method tend to increase or

decrease net income? - Increase __ Decrease

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

(Table comiimues)

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

January/February 2001

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

129 [image:6.612.47.564.109.717.2]TABLE

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

3zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

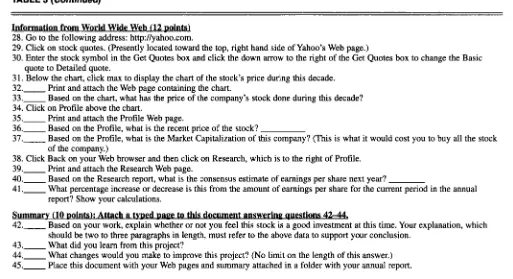

(Conf/nued)Information from World Wide Web (12 points)

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

28. Go to the following address: http://yahoo.com.

29. Click on stock quotes. (Presently located toward the top, right hand side of Yahoo’s Web page.)

30. Enter the stock symbol in the Get Quotes box and click the down arrow to the right of the Get Quotes box to change the Basic

3 1.

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Below the chart, click max to display the chart of the stock’s price during this decade.32.- Print and attach the Web page containing the chart.

33.- Based on the chart, what has the price of the company’s stock done during this decade? 34. Click on Profile above the chart.

35.- Print and attach the Profile Web page.

36.- Based on the Profile, what is the recent price of the stock?

37.- Based on the Profile, what is the Market Capitalization of this company? (This is what it would cost you to buy all the stock

38. Click Back on your Web browser and then click on Research, which is to the right of Profile. 39.- Print and attach the Research Web page.

40.- Based on the Research report, what is the consensus estimate of earnings per share next year?

41.- What percentage increase or decrease is this from the amount of earnings per share for the current period in the annual

Summary (10 Doints): Attach a tvDed Daee t o this document answering auestions 42-44.

42.- Based on your work, explain whether or not you feel this stock is a good investment at this time. Your explanation, which 43.- What did you learn from this project?

44.- What changes would you make to improve this project? (No limit on the length of this answer.)

45.- Place this document with your Web pages and summary attached in a folder with your annual report. quote to Detailed quote.

of the company.)

report? Show your calculations.

should be two to three paragraphs in length, must refer to the above data to support your conclusion. suggestion will be implemented this

semester.)

Allowing students to buy and sell stocks adds administrative complexity to the project. When students have been permitted to do this, they tend to abandon their “losers” quickly and buy the “hot” stock of the week for no other reason than its sharp rise. Although this some- times may be a very successful method of selecting stocks, students may find that a red-hot stock can become ice cold quickly. On occasion, these plunges have been caused by the exposure of account- ing irregularities, which has resulted in some lively class discussion. However, this type of speculation is not consistent with the type of thoughtful financial statement analysis that students should develop in the accounting course. There- fore, some instructors may choose to prohibit trading.

Other Considerations

At our school-a regional, AACSB- accredited, comprehensive state univer- sity-introductory accounting students have taken (or are concurrently taking) an introductory economics course. This course provides students with a rudi- mentary understanding of the impact of

130

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

JournalzyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

of Education for Businesschange in interest rates on the economy and some familiarity with the concept of supply and demand. Technical skills required for this project are ratio com- putation and analysis covered in the textbook. Students compute these ratios and make investment decisions using their analysis. Instructors can adapt requirements to the specific capabilities of their students by varying the depth of analysis involved. We believe that, although the analysis is not very deep in introductory accounting, students learn an important lesson through it: Always look below the surface.

Although some Web sites factor in trading lags, students may try to achieve superior returns by using real-time quote sources (such as E-Trade). Because investment success or failure is not an important factor in assessing student per- formance on this project (see grading sheet), there is little incentive for stu- dents to engage in such “real-time cheat- ing.” In addition, opportunities for this behavior are limited because students can only invest in stocks of companies that they or a classmate are evaluating. If “real-time cheating” should occur, it would provide a great opportunity to dis- cuss ethical behavior, perhaps leading to a discussion of insider trading.

At first glance, this project appears to require a great deal of faculty time. However the peer evaluation component substantially reduces the time required for grading because the peer evaluator has verified the quantitative content of the report and reviewed the qualitative assessments. Therefore, the instructor can concentrate most of the grading time on the student’s summary.

Neither does the project consume much class time. Besides the day devot- ed to portfolio formation, students work on the project outside of class. Covering the concepts related to making invest- ment decisions requires no additional class time because they are covered in class anyway, with or without the pro- ject. However, students’ understanding of the concepts is enhanced by the pro- ject, because they see how these con- cepts affect “their” firms.

Conclusion

In this article, we have presented an active learning project that develops the strategic and critical thinking, research, technology, interaction, communica- tion, and decisionmaking competencies of students. The investment project brings financial statement analysis to

[image:7.612.49.562.57.336.2]life and gives students a chance t o com- pare their conclusions about a company with the judgment that the stock market makes about that company each day. Although the project may be time con- suming and challenging f o r students, few of them leave the course wondering

“Why do I need to know

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

this stuff?”zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

REFERENCES

Accounting Education Change Commission

(AECC). (1990). Position Statement

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

No. One:Objectives of education for accountants. New

York: American Accounting Association. Accounting Education Change Commission

(AECC). (1992). Position Satement No. Two:

The first course in accounting. New York:

American Accounting Association.

American Institute of Certified Public Accoun- tants (AICPA). (1999). AICPA core competency

framework for entry into the accounting profes- sion. New York: AICPA.

Baldwin, B. A,, &

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

Ingram, R. W. (1991). Rethink-ing the objectives and content of elementary accounting. Journal of Accounting Education,

Bedford Committee. (1986). American Account- ing Association Committee on the Future Struc- ture, Content and Scope of Accounting Educa- tion. Future accounting education: Preparing for the expanding profession. Issues in

Accounting Education, Spring, 168-195.

Costin, F. (1972). Lecturing versus other methods of teaching: A review of research. British Jour-

nal of Educational Technology, 3, 4-30.

Eble, K. (1983). The aims of college teaching. San Francisco: Jossey-Bass.

Gordon, R. A,, & Howell, J. E. (1959). Higher 9, 1-14.

education for business. New York: Columbia

University Press.

Knapp, M. C. (1998). Financial accounting: A

focus

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

on decision making (2nd ed.). Cincinnati:South-Westem College Publishing.

McKeachie, W. J., & Kulik, J. (1975). Effective

college teaching.

zyxwvutsrqponmlkjihgfedcbaZYXWVUTSRQPONMLKJIHGFEDCBA

In F. Kerlinger (Ed.), Reviewof Research in Education. Itasca, IL: Peacock. Muse, W. V. (1982 p. 2). If all the business schools

in the country were eliminated.

. .

Would anyone notice. Collegiate News & views, Spring, 1-5.National Institute of Education (NIE). (1984). Study group on the conditions of excellence in American higher education. Involvement in

learning: Realizing the potential of American hinher education. Washington, DC: ME.

businessmen: A study of university-college pro- grams in business administration. New York:

McGraw-Hill.

Porter, L. W., & McKibbin, L. E. (1988). Man-

agement education and development. New

York McGraw-Hill.

Perspectives on education: Capabilities for suc- cess in the accounting profession (The White

Paper). (1989). New York, NY Arthur Ander- sen & Co., Arthur Young, Coopers & Lybrand, Deloitte Haskins & Sells, Emst & Whinney, Peat Manvick Main & Co., Price Waterhouse,

& Touche Ross.

Ramaglia, J. (1998, November). How to integrate

international accounting into your course. Pre-

sentation at The Colloquium on Change in Pierson, F. C. (1959). The eiucation ofAmerican Accounting Education, Scottsdale, Arizon;.

APPENDIX. WWW Class Exercises to Assign During Investment Project Phases

Phase I-Company Selection

Phase 2--Preliminary Analysis

Search and identify WWW sites to obtain annual reports.

* Search and identify Web sites to obtain firm-specific information.

Search Web to obtain examples of companies with conflicting recommendations from analysts.

Phase &Investment Evaluation

* Search and identify WWW sites to obtain examples of good and poor manage- Evaluate firms’ boards by comparing the composition of boards within their Search and identify WWW sites to compare and contrast management discussion Identify current examples of “earnings management” or “accounting irregulari- ment discussion and analysis (MD&A).

group.

& analysis with analysts’ evaluations. ties.”