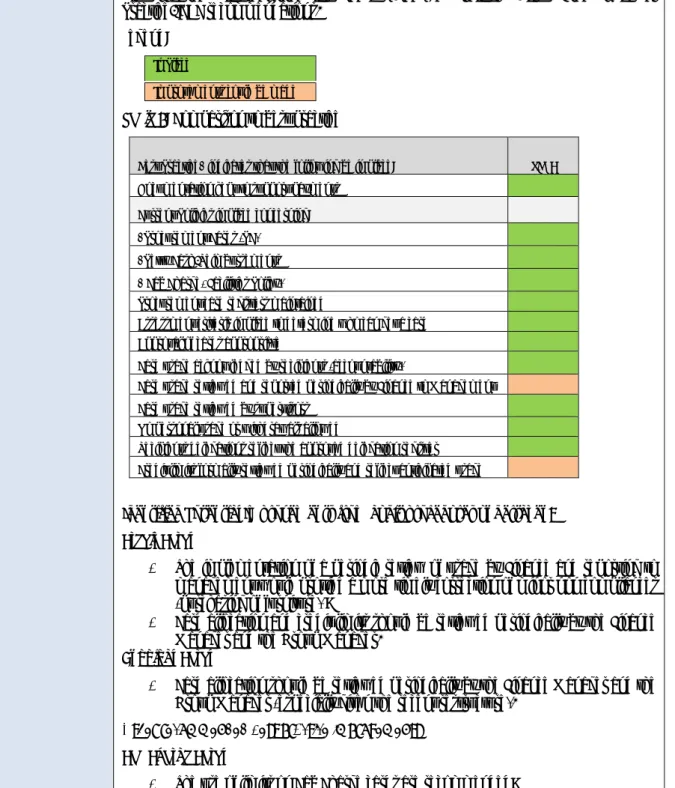

The purpose of this program is to provide assurance that the audit work is in accordance with the Standards for the Professional Practice of Internal Auditing, the Charter of Internal Auditing and is both cost effective and efficient. The implementation of the identified practices will be reported to the audit committee and will be monitored through the Internal Audit Report. Internal Audit is a key governance mechanism which ensures that the Council is accountable to the community.

Independent Quality Assessment of Internal Audit at Hills Shire Council (distributed under separate cover). The purpose, authority and responsibility of the internal audit activity must be formally defined in an internal audit charter that is consistent with the definition of internal audit, the code of ethics and the standards. The head of audit must periodically review the internal audit charter and submit it to senior management and the board for approval.”.

The internal audit charter is a formal document that defines the purpose, authority, and responsibility of the internal audit activity. The Audit Charter – Internal Auditor forms the broad working framework for the Internal Audit (IA) function within the Board.

AUDIT CHARTER – INTERNAL AUDITOR

- Role and Authority

- Objectivity, Independence and Organisational Status

- Scope of Work

- The scope of work may include

- Internal Audit Methodology

- Operating Principles

- Internal Audit shall

- Internal Audit staff shall

- Reporting Arrangements

- Planning Requirements

- Quality Assurance & Improvement Program

- Co-ordination with External Audit

- Review of the Internal Audit Charter

- Evaluation of Internal Audit

- Conflict of Interests

Internal Audit will be independent of the audited activities, and therefore will not assume any operational responsibility outside of internal audit work. Internal Audit staff and contractors should report to the internal auditor any situation where they feel that their objectivity may be impaired. Internal Audit work does not relieve Council staff of their responsibility to carry out their responsibilities.

In addition to the normal reporting process for work undertaken by Internal Audit, the Head of Internal Audit will bring to the attention of the Audit Committee all matters which, in the opinion of the Internal Auditor, warrant reporting in this manner. The Internal Auditor will review the Internal Audit Charter annually to ensure that it remains up-to-date and reflects the current scope of internal audit work. The Internal Auditor will develop performance measures (key performance indicators) for consideration and approval by the Audit Committee as a means of periodically evaluating Internal Audit's performance.

Such review must be in accordance with the Standards for the Professional Practice of Internal Audit and is mandated by and reports to the Audit Committee. Any perceived or actual conflict of interest by the internal auditor or internal audit personnel and contractors must be promptly reported by the internal auditor to the audit committee.

AUDIT CHARTER – INTERNAL AUDITOR

A strategic audit plan will be developed by the internal auditor and approved by the audit committee, identifying areas to be audited in future years. Any changes to the plan will be submitted to the audit committee for consideration and approval. The work program is approved by the general director and approved by the audit committee.

At the end of each audit, a copy of the report on the audit outcome will be issued to the relevant Department and to the General Manager. The report will present the audit objectives, scope, the audit opinion based on the outcome of the audit and an agreed implementation timetable for audit recommendations. As soon as practicable after the end of each quarter, the Internal Auditor will submit a report to the Audit Committee summarizing all audit activities undertaken during that quarter.

This process should be performed by the internal auditor who, regardless of whether changes are proposed, must then submit the revised charter to the audit committee for review and approval. The approved Charter of the Audit Committee and a recommendation in the independent quality review of the internal audit at THSC dated October 2018 (2.1, page 49) indicate that the Audit Committee should develop a plan for the future to improve their coverage of the Board's activities during the year balance. The purpose of a future plan is to assign certain tasks for the Audit Committee to consider at certain meetings during the year so that the workload is balanced.

This also ensures that the audit committee can be sure that it has fulfilled all duties and obligations during the year. To address opportunities for improvement and Section 2 (k) of the Audit Committee Charter, a forward-looking plan has been prepared and is attached for consideration by the Audit Committee. The planned plan in Annex 1 is considered by the audit committee and after the identified changes, it is adopted.

Summarizes the work performed by the internal audit function and the audit committee during the period; It provides the Audit Committee with an overview of the status of the Council's internal control, risk management and management processes. Attached is the internal audit report, which describes the audit tasks performed by the internal audit in the period up to November 1, 2018.

Internal Audit Report

November 2018

The Structure of the Internal Audit Report is as follows

Part A: Executive Summary

Internal audit work undertaken in the period to the date of this report

- Detailed Findings of the actual internal audit work undertaken in the period

The results of this exercise are reported to the audit committee and to the community (through the annual community report). The results were most recently reported to the audit committee in the internal audit report submitted to the audit committee regarding February 2018). These will be reviewed in detail and reported to the Audit Committee as part of the Governance Health check exercise and the follow-up of outstanding audit recommendations.

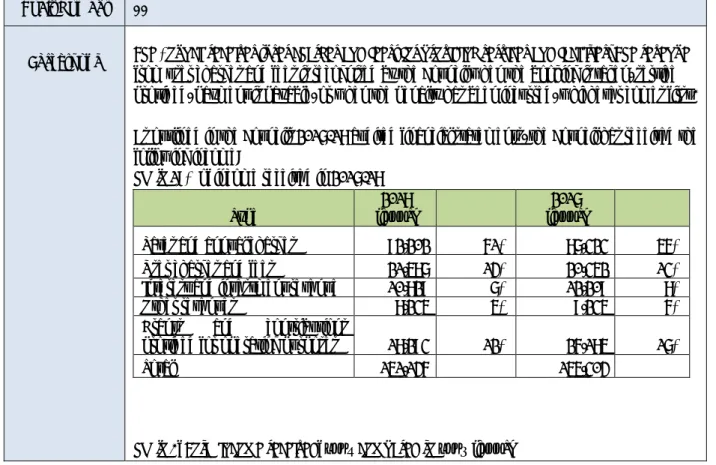

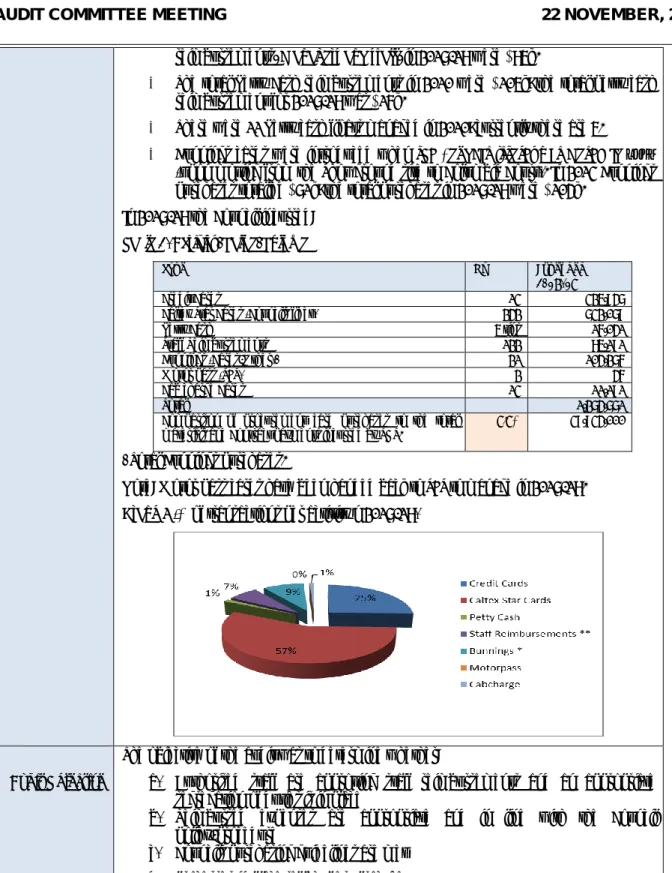

Since 2010, the audit topic Credit Cards/Procurement Cards/Employee Expense Reimbursement/Petty Cash has been reviewed periodically. In the period from 2010, important improvements have been made with regard to the management of these purchases. As described in the 2017/18 annual accounts audited by the Board, the Board received the following income:.

Scope As identified above, the Audit Office has reviewed the Council's user fees and charges for the period to 30 June 2018 as part of their external audit. Based on the test performed, the Council's fees and charges document is applied correctly and reflected in the Council's ledger. As identified in the Audit Plan, time is allocated annually to review KPIs outlined in the Council Enterprise Agreement to ensure that the calculations are complete, accurate and valid.

In August 2018, Audit reviewed the KPIs set out in the Council's enterprise agreement, particularly those KPIs relating to sick leave. As set out in the audit plan, audit reviewed the Council's management of IT assets/mobile devices. .. 5 recommendations resulted from the review and these were agreed with the Management. As instructed by the OLG, the Audit Office (AO) is the Council's external auditor from 2016 (refer circular 16-35).

Action to be taken: As part of Board processes, the results of these reports (in particular the report on internal controls and governance) are reviewed in detail to identify key improvements that can be made in the Board. As previously reported to the Audit Committee, the Minister for Local Government, the Hon. The following information is set out in the annual report on Local Government and other state government sectors and the type of reporting and the subjects reported on.

It also confirms that the functions complained about and reflected in the Council Risk Register as a high corruption risk remain relevant. The results set out in the ICAC annual report will be reviewed against the Council's risk register, the Council's corruption prevention strategy and the Internal Audit Plan.

Internal Audit and Audit Committee Key Performance Measures

Audit Committee Forward Plan

- Legislative Change

- Best Practice

- The Strategic Audit Plan

- Reporting

Background of the: Internal Audit function; the Audit Committee; and the audit reporting practices at The Hills Shire Council. The role of internal audit is primarily to provide independent assurance about the board's internal controls and risk management framework. Within THSC, the functions, powers and responsibilities of Internal Audit are set out in the Internal Audit Charter adopted by the Board.

Projects can be implemented with the help of a risk management coordinator or experts where necessary. It provides the Council with independent oversight and monitoring of the Council's audit processes, including the Council's internal control activities. Given the key role of the audit committee, it is important for its most effective functioning that it is properly composed of suitably qualified independent members.

At the beginning of each Council term, the Council undertakes to obtain an EOI to obtain the interest of suitably qualified community members to be part of the Audit Committee. The functions, powers and responsibilities of the audit committee are defined in the statute of the audit committee adopted by the council. This guideline (guideline) defines best practices in local government in relation to internal audit and the audit committee.

As identified at 3.5 of the DLG Internal Audit Guideline, the Internal Audit function within THSC has a strategic plan in place supported by annual plans. Internal audit regularly communicates its findings and recommendations to the Audit Committee, General Manager and management of the areas audited by the Internal Audit Report. The format of the report has been modified to meet the requirements of the Audit Committee and to reflect the guidelines.

Internal audit working papers are shared with the council's external auditor where requested to assist them in the course of their work. Council members and the community have access to the audit committee's minutes (and the internal audit report), as these are published on the council's website. The internal audit report (and audit committee papers) are also referred to Council for adoption to provide greater transparency and accountability.

The reconciliation of the recommendations of the independent quality assessment at the date of this report was an internal audit of the ReportTotalRecommendations expressed by the recommendations of the IIA Raised during the periodTotalTotalRecommendations carried out by the IA. December 2018 Note: IT presents a report on its IT security policy at a Councilors workshop on The world's enterprise systems should be tested annually for disaster recovery to ensure that processes and contracts meet the enterprise's requirements to meet customer requirements in the event of a disaster within reasonable time frames.

COUNCILLORS QUESTIONS WITHOUT NOTICE

AUGUST 2018

SCHEDULE OF OUTSTANDING RESOLUTIONS