Perusahaan Gas Negara

Bloomberg: PGAS.IJ | Reuters: PGAS.JK

Samuel Equity Research 31 January 2017

www.samuel.co.id

Energy holding for future prospect

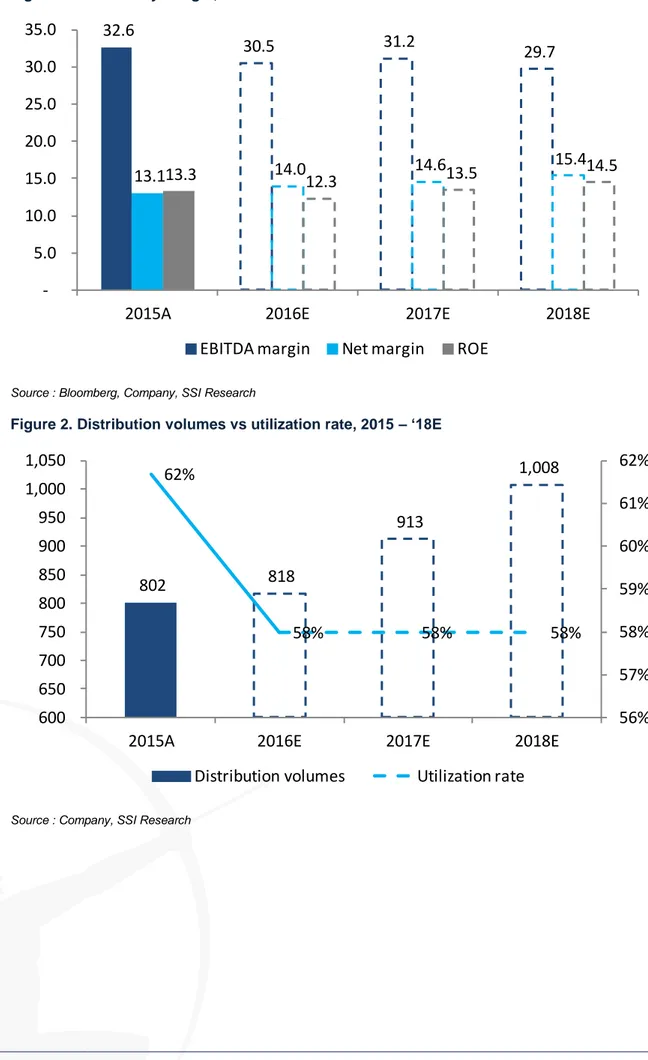

Laba bersih diperkirakan tumbuh 21% y-y. Pembentukan energy holding disinyalir akan terealisasi. Mempertahankan BUY untuk PGAS, dengan TP Rp 3,375/lembar saham, 17E’PE: 12.1x, dan PBV: 1.6x). Laba bersih kami estimasi tumbuh 21% y-y di 2017, dengan … Kami estimasikan laba bersih PGAS 2017 tumbuh 21% y-y menjadi US$487 juta, merefleksikan ekspektasi marjin gas distribusi perseroan sebesar US$3.1/mmbtu. Saat ini, kami belum memasukkan prospek Pertagas dalam valuasi kami, menunggu kejelasan skema pembentukan holding energi ini. … estimasi kenaikan volume distribusi 12% y-y. Ekonom kami memperkirakan, kenaikan harga beberapa komoditas utama akan mampu mendorong pertumbuhan ekonomi (SSI GDP17F: 5.2%), sehingga Perseroan yang 97% pelanggan utamanya adalah kalangan industri, kami estimasi mampu mencetak 12% y-y pertumbuhan volume distribusi.

Ekspektasi realisasinya pembentukan holding energi. Direktur Utama PT Pertamina (Persero) Dwi Soetjipto, menyatakan pembentukan energy

holding tinggal menunggu terbitnya peraturan pemerintah (PP). Sosialisasi

internal antara Pertamina dan perseroan sejak Desember 2016 memberikan sinyal kelanjutan dari realisasi energy holding.

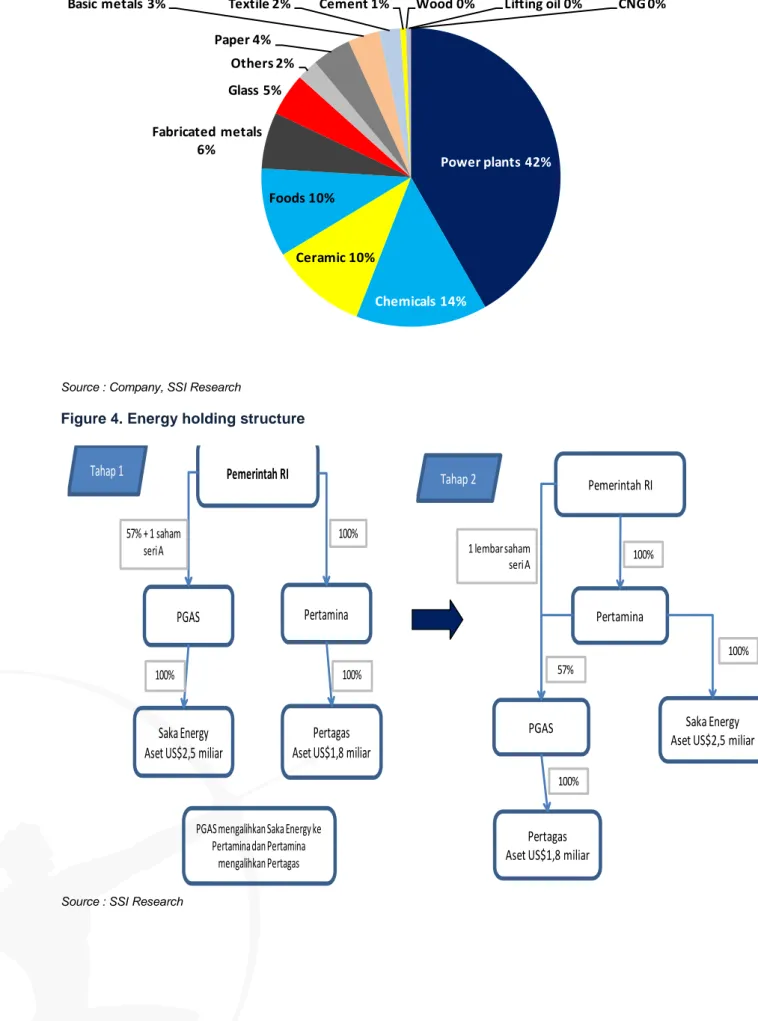

Pertukaran Saka – Pertagas meminimalisir dana akuisisi PGAS. Di 2015, Saka Energi memiliki asset sebelum eliminasi sebesar US$2,5 miliar sedangkan Pertagas US$1,8 miliar, sehingga transaksi ini memungkinkan PGAS untuk seminim mungkin mengeluarkan dana dalam akuisisi Pertagas. Belanja modal terfokus untuk pengembangan infrastruktur gas. Di 2017, perseroan mengalokasikan US$500 juta belanja modal dengan 50% dari anggaran untuk ekspansi hulu, sehingga apabila aset hulu dialihkan ke Pertamina, perseroan memiliki ruang dana lebih besar untuk memenuhi target pembangunan 1.685km pipa gas bumi hingga 2019.

Mempertahankan BUY dengan TP Rp 3.375: Kami mempertahankan rekomendasi BUY dengan target price (TP) di Rp 3.375, merefleksikan P/E ‘17 12x dan potensi upside 17%. Resiko dari rekomendasi kami adalah lebih buruknya volume distribusi dan berlarutnya pembentukan energy holding.

Target Price Rp 3,375 Last Price Rp 2,880 Potential Upside 17.2% JCI Index 5,400 Share Issued (m n) 24,242 Market Cap. (Rp bn) 64,967 52-Weeks High/Low 3,520/ 2,170 Avg Daily Vol (m n) 51.97

Free Float 43%

Nom inal Value 100

EPS 2017 Rp 281

Relative to JCI Chart

Com pany Background

Shareholder Structure

Republik Indonesia 57.0%

Capital group 14.3%

Public 28.8%

Buy (Maintain)

PT Perusahaan Gas Negara Tbk beroperasi di bidang distribusi dan transmisi gas alam untuk pengguna industri, komersial dan rumah tangga. Belakangan, perusahaan juga masuk ke bisnis hulu migas dengan mengakuisisi beberapa blok migas.

-80% -60% -40% -20% 0% 20%

Jan-15 Jun-15 Nov-15 Apr-16 Sep-16

PGAS JCI

Y/E Dec (US$ mn) 15A 16E 17E 18E

Revenue 3,069 2,885 3,339 3,785 EBIT 565 565 668 778 EBITDA 1,002 880 1,041 1,126 Net Profit 401 404 487 582 EPS (Rp/share) 232 233 281 336 Book value per share 1,744 1,892 2,088 2,317 DPS (Rp/share) 154.4 88.4 82.6 99.7 Dividend Yield (%) 5.4 3.1 2.9 3.5 EV/EBITDA (x) 7.5 8.5 7.2 6.7 P/E Ratio (x) 12.4 12.3 10.2 8.6 P/BV Ratio (x) 1.7 1.5 1.4 1.2 Net Gearing (%) 52.0 44.0 24.5 3.9 Forecast and Valuation (at closing price Rp2,880 per share)

Arandi Ariantara +62 21 2854 8148

www.samuel.co.id Page 2 of 6

Figure 1. Profitability margin, 2015 – ‘18E

Source : Bloomberg, Company, SSI Research

Figure 2. Distribution volumes vs utilization rate, 2015 – ‘18E

Source : Company, SSI Research

32.6

30.5

31.2

29.7

13.1

13.3

14.0

12.3

14.6

13.5

15.4

14.5

-5.0

10.0

15.0

20.0

25.0

30.0

35.0

2015A

2016E

2017E

2018E

EBITDA margin

Net margin

ROE

802

818

913

1,008

62%

58%

58%

58%

56%

57%

58%

59%

60%

61%

62%

600

650

700

750

800

850

900

950

1,000

1,050

2015A

2016E

2017E

2018E

www.samuel.co.id Page 3 of 6

Figure 3. 9M16 Gas Distribution Customers

Source : Company, SSI Research

Figure 4. Energy holding structure

Source : SSI Research

Power plants 42% Chemicals 14% Ceramic 10% Foods 10% Fabricated metals 6% Glass 5% Others 2% Paper 4%

Basic metals 3% Textile 2% Cement 1% Wood 0% Lifting oil 0% CNG 0%

Tahap 1

Pemerintah RI

PGAS

Pertamina

Saka Energy

Aset US$2,5 miliar

Pertagas

Aset US$1,8 miliar

57% + 1 sahamseriA

100%

100% 100%

PGAS mengalihkan SakaEnergy ke Pertamina dan Pertamina

mengalihkan Pertagas

Tahap 2 Pemerintah RI

Pertamina

PGAS Saka Energy

Aset US$2,5 miliar

Pertagas Aset US$1,8 miliar 1 lembar saham

seri A 100%

57%

100%

www.samuel.co.id Page 4 of 6

Figure 5. Capex realization (US$mn), 2011 – 2017E

Source : Company, SSI Research

Figure 5. Pertagas & PGAS summary, 2015

Source : Company, SSI Research

102.5

139.6

880.7

2,676.0

972.0

400.0 - 500.0

500.0

0

500

1,000

1,500

2,000

2,500

3,000

2011

2012

2013

2014

2015

2016E

2017E

Prior

upstream

business

Description

Unit

Pertagas

PGAS

Market share

Distribution pipeline

%

81

Transmission pipeline

%

49

Length

km

1,962

7,059

Sales volume

mmscfd

1,455

1,567

Revenue

USDmn

624

3,069

Gross profit margin

%

41.9

31.4

EBIT margin

%

33.5

18.4

Net income margin

%

24.2

13.1

Interest coverage ratio

x

9

5

Assets

USDmn

1,840

6,495

Net gearing

%

35.9

52.0

Business operation

Pertagas focused on

the transport of gas

through open access

pipeline

infrastructure

PGAS focused on the

trade and

distribution of gas

20

www.samuel.co.id Page 5 of 6

Key Financials

Profit and Loss Cash Flow

(US$ mn) 15A 16E 17E 18E Yr-end Dec (US$ mn) 15A 16E 17E 18E Gas Distribution Revenue 2,613 2,536 2,886 3,255 EBIT 565 565 668 778 Other Revenue 456 348 454 530 Depreciation & amort. 436 316 373 348

Total Operating Revenue 3,069 2,885 3,339 3,785 Others (101) (2) 5 (59) Operating Expenses 2,503 2,320 2,672 3,007 Working capital (78) 19 (38) (24)

Operating profit 565 565 668 778 Operating cash flow 528 738 822 905

Operating margin (%) 18.4 19.6 20.0 20.6 Net - Capital expenditure (751) (469) (116) 12

EBITDA 1,002 880 1,041 1,126 Investing cash flow (222) 270 706 918

EBITDA margin (%) 32.6 30.5 31.2 29.7 Net -Borrowings 856 (69) (51) (32) Other income (expenses)(559) (361) (413) (377) Other financing (629) (141) (148) (187) Pre-tax profit 443 520 627 749 Financing cash flow 227 (210) (199) (219)

Income tax - net (40) (114) (138) (165) Net - Cash flow 5 60 507 699 Net profit 401 404 487 582 Cash at beginning 1,131 1,136 1,196 1,703 Net profit margin (%) 13.1 14.0 14.6 15.4 Cash at ending 1,136 1,196 1,703 2,401

Balance Sheet Key Ratios

Yr-end Dec (US$ mn) 15A 16E 17E 18E Yr-end Dec 15A 16E 17E 18E

Cash & ST Investment 1,136 1,196 1,703 2,401 ROE (%) 13.6 12.8 14.1 15.3 Receivables 287 271 314 355 ROA (%) 6.6 6.1 7.1 8.1 Inventories 43 65 75 82 Revenue growth (%) (5.7) (6.0) 15.8 13.3 Others 65 65 65 65 EBITDA growth (%) 2.3 (12.1) 18.2 8.2

Total current assets 1,530 1,596 2,156 2,903 EPS growth (% ) (39.5) 0.7 20.6 19.4

Net fixed assets 3,565 3,720 3,469 3,116 Interest coverage (x) 4.7 4.9 6.0 7.0 Other assets 1,400 1,390 1,384 1,378 Debt to equity (%) 89.7 80.6 71.6 63.7

Total assets 6,495 6,706 7,009 7,397 Net gearing (% ) 52.1 44.1 24.5 3.9

Payables 117 108 125 136

Debt 2,709 2,639 2,588 2,556 Major Assumptions

Other long term liabilities 646 680 678 691 Yr-end Dec 15A 16E 17E 18E

Total liabilities 3,472 3,427 3,391 3,383 Distribution Vol. (mmscfd) 802 818 913 1,008

Minority interest 2 2 2 2 Rate margin (USD/mmbtu) 3.4 3.1 3.1 3.3

Total equity 3,020 3,276 3,615 4,011

Distribution capacity

www.samuel.co.id Page 6 of 6

Research Team

Andy Ferdinand, CFA Head Of Equity Research, Strategy,

Banking, Consumer andy.ferdinand@samuel.co.id +6221 2854 8148

Rangga Cipta Economist rangga.cipta@samuel.co.id +6221 2854 8396

Muhamad Makky Dandytra, CFTe Technical Analyst makky.dandytra@samuel.co.id +6221 2854 8382 Akhmad Nurcahyadi, CSA Auto, Aviation, Cigarette, Construction

Healthcare, Heavy Equipment, Property akhmad.nurcahyadi@samuel.co.id +6221 2854 8144 Arandi Ariantara Cement, Telecommunication, Utility arandi.ariantara@samuel.co.id +6221 2854 8392 Marlene Tanumihardja Poultry, Retail, Small Caps marlene@samuel.co.id +6221 2854 8387 Sharlita Lutfiah Malik Mining, Plantation sharlita.malik@samuel.co.id +6221 2854 8339 Adde Chandra Kurniawan Research Associate adde.kurniawan@samuel.co.id +6221 2854 8338

Private Wealth Management

Evelyn Satyono Head of PWM / Institutional Sales evelyn.satyono@samuel.co.id +6221 2854 8380 Muhamad Alfatih CSA, CTA, CFTe Senior Technical Portfolio Advisor m.alfatih@samuel.co.id +6221 2854 8129 Ronny Ardianto Institutional Equity Sales ronny.ardianto@samuel.co.id +6221 2854 8399 Clarice Wijana Institutional Equity Sales clarice.wijana@samuel.co.id +6221 2854 8395 Fachruly Fiater Institutional Equity Sales fachruly.fiater@samuel.co.id +6221 2854 8325

Equity Sales Team

Kelvin Long Head of Equities kelvin.long@samuel.co.id +6221 2854 8150

Yulianah Institutional Equity Sales yulianah@samuel.co.id +6221 2854 8146

Lucia Irawati Retail Equity Sales lucia.irawati@samuel.co.id +6221 2854 8173

Online Trading Sales Team

Nugroho Nuswantoro Head of Marketing Online Trading nugroho.nuswantoro@samuel.co.id +6221 2854 8372

Wahyu Widodo Marketing wahyu.widodo@samuel.co.id +6221 2854 8371