THE REFLECTION OF EUROPEAN CENTRAL BANK MONETARY POLICY APPLICATIONS ON CENTRAL BANK OF THE REPUBLIC OF TURKEY

Res.Asst.Nihat ALTUNTEPE

Suleyman Demirel University/Faculty of Economic and Administrative Sciences Department of Economics Postal Address: Suleyman Demirel University Faculty of Economic and Administrative Sciences

Department of Economics Çünür/ISPARTA E-mail: [email protected]

Lect. Selen IŞIK MADEN

Suleyman Demirel University Gonen Vocational School

Postal Address: Suleyman Demirel University Gonen Vocational School Gonen/ISPARTA

E-mail: [email protected]

─Abstract ─

One of the instruments which is used to perform economic policy is monetary policy. The changes which has appeared in the monetary policy can affect macroeconomic variables positively or negatively. Monetary policies which have been carried out in the national economies also have been influenced by developments in the world economy. The institutions in the economies which carry out monetary policies are Central Banks. So, functions of central banks are very important.

The aim of this study is to display the reflections of European Central Bank’s monetary policy applications on the Central Bank of the Republic of Turkey’s monetary policy applications in Turkey which has been improving under the process of European Union membership. In this study, the monetary policies of the two central banks will be studied.

Key Words: Monetary Policy, Central Bank, Monetary Union JEL Classification: E42

1. INTRODUCTION

2. DEFINITION AND OBJECTIVES OF MONETARY POLICY 2.1. Definition of Monetary Policy

Monetary policy is the process by which governments and central banks manipulate the quantity of money in the economy to achieve certain macroeconomic and political objectives. The targets are usually: economic growth, changes in the rate of inflation, higher level of employment, and adjustment of the exchange rate. Monetary policy can be categorized into two types: contractionary and expansionary. Contractionary (tight) monetary policy aims to reduce the amount of money circulating through the economy, and reduce short-term economic growth in exchange for higher long-short-term growth. Expansionary (loose) policy, on the other hand, aims to increase the money supply and increase short-term economic activity at the expense of long-term economic activity.

Central bankers control interest rates in an effort to stabilize output and inflation. Changes in interest rates affect most of us directly through increases or decreases in the cost of borrowing, while stable prices and steady real growth make our economic and financial planning much easier. In most countries today, the central bankers are the only governmental authorities engaged in stabilization policy. Economists and policy makers now agree that fiscal policy, once thought to be capable of helping to smooth fluctuations in real growth, is not up to the task. Central banks are the sole remaining policy making bodies thought capable of reducing business-cycle fluctuations. (Cecchetti,2000: 43-44)

2.2. Objectives of Monetary Policy

In this section, various reasons why central banks stabilize prices and output will be discussed. It will be also discussed at some length why it is that they smooth interest rates, and how this is a consequence of their actions, not an objective in and of itself.

2.2.1. Stabilizing Prices

The most common response dissatisfaction with inflation is that inflation is responsible for declines in real income. There are many reasons that we can identify why high inflation is inherently unstable.

One cost of inflation is the tax on the money that is holded. More specifically, it is a tax on the monetary base. A second cost of inflation relates to taxes. The tax system in most countries is not properly indexed, and so there are welfare losses associated with inflation. The papers in Feldstein (Felstein,1996: 9) show that these effects can be quite substantial, and so it may be worth paying a fairly high price to reduce inflation to near zero .Beyond tax distortions, inflation creates disturbance in the price system. When there is aggregate price inflation, it becomes more difficult to discern changes in relative prices. Fourth cost of inflation is that at high levels of inflation, people tend to invest substantial time and effort into finding ways to reduce its costs. Finally, there is the empirical fact that high inflation is uncertain inflation. Overall, central bankers now agree that the costs of inflation are high, and that variable inflation entails significant social losses. As a result, the primary objective of monetary policy, and the one that appears to be within the grasp of the policy makers, is to stabilize inflation about a level that is low enough that it becomes irrelevant for household and firm decision making. (Cecchetti,2000: 47)

2.2.2. Stabilizing Output

Economists have long recognized that some sources of economic fluctuations imply that output stability and inflation stability are mutually reinforcing. For example, if there is a negative shock to aggregate demand households will cut spending. The drop in demand leads, in turn, to a decline in actual output relative to its potential. As a result of increased slack in the economy, future inflation will fall below levels consistent with price stability. The central bank will pursue an expansionary policy to keep inflation from falling. This expansionary policy will result in an increase in demand that boosts output toward its potential to return inflation to a level consistent with price stability. Stabilizing output stabilizes inflation under these conditions. (Mishkin, 2008: 3-4)

2.2.3. Stabilizing Interest Rates

There are several possible explanations about where does this interest rate smoothing come from. One is that the central bank takes it as an explicit objective to keep interest rates smooth in order to insure financial stability. Another explanation is that smooth interest rates enhance credibility. The objective of monetary policy should be the stabilization of the domestic economy through the reduction in the variability of prices and output growth. Optimal monetary policy may entail interest rate smoothing, but there is no justification for this to be an explicit objective. (Cecchetti,2000: 50)

3. EUROPEAN CENTRAL BANK – OBJECTIVES AND INSTRUMENTS OF MONETARY POLICY

The creation of Economic and Monetary Union (EMU), with a supranational monetary authority and a common currency is a key point of the Maastricht Reforms, which came to the forefront of attention to the European Union and with preparations for joining EMU. Responsibility for monetary policy in the framework of the European Union lies with two institutions (Article 8 of the Maastricht Treaty), the European System of Central Banks (ESCB) and the European Central Bank (ECB). The legislative framework for their activity is contained in Title VI of the Treaty – Economic and Monetary Policy and in the Protocol on the Statute of the ESCB and ECB. (EC,1999:20) The European System of Central Banks (Article 107 of the Treaty) has, from the formal aspect, two levels, the European Central Bank and the 15 national central banks of the member states of the European Union. The European Central Bank, together with the 12 national central banks of the eurozone, constitutes the eurosystem. The ESCB is governed by decision-making bodies of the European Central Bank.

The European Central Bank is responsible for an area that comprises 12 countries. For achieving the aims of the ECB, it is important to transparently and comprehensively inform the public of steps taken by the ECB and the tasks it sets itself. The Maastricht Treaty creates a mechanism for ensuring that monetary union, together with the single currency, forms a stable alignment. The institutional predecessor of the ECB was the European Monetary Institute, which operated from 1 January 1994. Through the establishment of EMU on 1 January 1999 responsibility for monetary policy passed from the national central banks of member states to the ECB. The ECB shall have a legal personality. Its first President was the Dutchman Willem F. Duisenberg and on 1 November 2003 the office passed to the Frenchman Jean-Claude Trichet. The ECB is situated in Frankfurt am Main in Germany. (Tancosova,2004: 2)

3.1. The Organisation of The European Central Bank

In Article 105 of the Treaty on the European Union it is stated that the primary objective of the ESCB is to maintain price stability. Without prejudice to this objective the ESCB shall support “general economic policies in the Community with the objective of contributing to achieving the Community’s aims”, which are defined in Article 2 of the Treaty. Through such a normative delimitation of the objective, the stability of the euro's purchasing power has been made an absolute priority. The Governing Council of the ECB has quantitatively defined price stability as “a year-on-year increase in the harmonised index of consumer prices (HICP) in the eurozone of less than 2%.” (ECB,2004:9-10)

On the basis of Article 106 of the Treaty the European Central Bank has the exclusive right to authorise the issue of banknotes in the Community. Banknotes issued by the ECB and national central banks are the sole banknotes in the Community having the exclusive status of legal tender. Member states may issue only coins in a certain volume approved by the ECB. (Official Journal of the European Communities,2002:8)

3.2. Monetary Policy of the ECB

In October 1998, the ECB presented its strategy. It is based on price stability. The objective of price stability refers to the general level of prices in the economy and implies avoiding both prolonged inflation and deflation. ( Hagen and Brückner, 2001: 7) Inflation leads to uncertainty about relative prices and the future price level, making it harder for firms and individuals to make appropriate decisions, thereby decreasing economic efficiency (Lucas, 1972: 112; Briault, 1995: 34).

There are several ways in which price stability contributes to achieving high levels of economic activity and employment. First, price stability makes it easier for people to recognize changes in relative prices. As a result, firms and consumers do not misinterpret general price level changes as being relative price changes and can make better informed consumption and investment decisions. Second, if creditors can be sure that prices will remain stable in the future, they will not demand an inflation risk premium to compensate them for the risks associated with holding nominal assets over the longer term. Third, the credible maintenance of price stability also makes it less likely that individuals and firms will divert resources from productive uses in order to hedge against inflation. Fourth, tax and welfare systems can create perverse incentives which distort economic behavior. Fifth, inflation acts as a tax on holdings of cash. This reduces household demand for cash and consequently generates higher transaction costs. Sixth, maintaining price stability prevents the considerable and arbitrary redistribution of wealth and income that arises in inflationary as well as deflationary environments, where price trends change in unpredictable ways. (ECB,2004:11-12)

All these arguments suggest that a central bank that maintains price stability makes a substantial contribution to the achievement of broader economic goals, such as higher standards of living, high levels of economic activity and better employment prospects.

3.3. General Principles of the ECB’s Monetary Policy Strategy

There are various monetary policy strategies which have been pursued by central banks. One such strategy is monetary targeting, another strategy is direct inflation targeting and the third strategy is exchange rate targeting.

While central bank experiences with the design of the ECB’s strategy, the ECB decided not to adopt monetary targeting. This decision acknowledged the existence of information in macroeconomic variables other than money that is important for monetary policy decisions aimed at price stability. (ECB,2008: 33) Direct inflation targeting focuses on developments in inflation itself relative to a published inflation target. The central bank’s forecast for inflation is therefore placed at the centre of policy analysis and discussions, both within the central bank and in its presentations to the public. Focusing entirely on a forecast inflation figure does not provide an encompassing and reliable framework for identifying the nature of threats to price stability. The ECB considers that relying on a single forecast would be unwise. (CBRT,2004:17-18)

Thirdly, exchange rate targeting, which was pursued by several European countries prior to Monetary Union in the context of the exchange rate mechanism of the European Monetary System. An exchange rate targeting strategy was not considered appropriate for the euro area, as it is a large and relatively closed economy where the impact of exchange rate developments on the price level is more modest. (ECB,2008: 33)

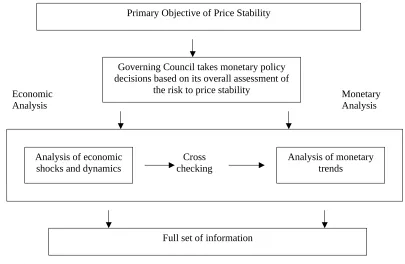

The challenge faced by the ECB while carrying out the monetary policy can be stated as follows: the Governing Council of the ECB has to influence conditions in the money market, and thereby the level of short-term interest rates, to ensure that price stability is maintained over the medium term. In so doing, the central bank is continuously confronted with a high level of uncertainty regarding both the nature of the economic shocks hitting the economy and the existence and strength of the relationships that link macroeconomic variables.

Primary Objective of Price Stability

Governing Council takes monetary policy decisions based on its overall assessment of

the risk to price stability

Analysis of economic shocks and dynamics

Analysis of monetary trends

Full set of information Economic

Analysis Monetary Analysis

Cross checking 3.3.1. The ECB’s Quantitative Definition of Price Stability

The Governing Council of the ECB announced the following quantitative definition in 1998: “Price stability shall be defined as a year-on-year increase in the Harmonised Index of Consumer Prices (HICP) for the euro area of below 2%. Price stability is to be maintained over the medium term”. The Governing Council decided to publicly announce a quantitative definition of price stability for a number of reasons. First, by clarifying how the Governing Council interprets the goal it has been assigned by the Treaty, the definition helps to make the monetary policy framework easier to understand. Second, the definition of price stability provides a clear and measurable yardstick against which the public can hold the ECB accountable. Finally, the definition provides guidance to the public for forming expectations of future price developments. All these positive features of the definition were even further enhanced by the clarification of the Governing Council that it aims, within the definition, at inflation rates of close to 2%. (ECB,2008:35)

3.3.2. The Two Pillars of the ECB’s Monetary Policy Strategy

The ECB’s approach to organising, evaluating and cross-checking the information relevant for assessing the risks to price stability is based on two analytical perspectives, referred to as the two pillars. This approach was confirmed and further clarified by the Governing Council of the ECB in May 2003. (ECB,2008:36) The two-pillar approach is designed to ensure that no relevant information is lost in the assessment of the risks to price stability and that appropriate attention is paid to different perspectives and the cross-checking of information in order to come to an overall judgement on the risks to price stability.

Table 1: The Two Pillars of the ECB’s Monetary Policy Strategy

Source: ECB:2008:39

3.3.2.1. Economic Analysis

and the National Central Banks(NCB)s, play an important role in the economic analysis. The Governing Council evaluates them together with many other pieces of information and forms of analysis organised within the two-pillar framework; but it does not assume responsibility for the projections. The published projections are the result of a scenario based on a set of technical assumptions, including the assumption of unchanged short term interest rates. In view of this, the projections represent a scenario that is unlikely to materialise since monetary policy will always act to address any threats to price stability. (ECB,2004:61-62) 3.3.2.2. Monetary Analisis

The ECB’s monetary analysis relies on the fact that monetary growth and inflation are closely related in the medium to long run. Assigning money a prominent role therefore underpins the medium-term orientation of the ECB’s monetary policy strategy. Indeed, by taking policy decisions not only on the basis of the short to medium-term indications stemming from the economic analysis, but also on the basis of money and liquidity considerations, the ECB is able to see beyond the transient impact of the various shocks and avoids any temptation to take an overly activist course.

To signal its commitment to monetary analysis and provide a benchmark for the assessment of monetary developments, the ECB has announced a reference value for the growth of the broad monetary aggregate M3. This reference value refers to the rate of M3 growth that is deemed to be compatible with price stability over the medium term. In December 1998 the Governing Council set this reference value at 4½% per annum and confirmed it in subsequent reviews. The reference value is based on the definition of price stability and on the medium term assumptions of potential real GDP growth of 2-2½% and a decline in the velocity of circulation of money of between ½% and 1%.

The ECB’s monetary analysis is not limited to the assessment of M3 growth in relation to its reference value. Many other monetary and financial variables are closely analysed on a regular basis. In this respect, narrower aggregates such as M1 may contain some information about real activity. Similarly, changes in credit extended to the private sector can be informative about financial conditions and, through the monetary financial institutions (MFI) balance sheet, can provide additional information about money. Such analysis helps to provide both a better insight into the behaviour of M3 in relation to the reference value and a broad picture of the liquidity conditions in the economy and their consequences in terms of risks to price stability. (Scheller,2006:85)

Table2: Average M3,Inflation Rate and Interest Rates in Euroarea

199

Source: 1998-2000 Monthly Bulletin 10th Anniversary of the ECB p.149

The aim of ECB’s monetary policy strategy is to maintain price stability. As seen in Table 2 Euroarea has also been affected by global economic developments. Especially M3 and interest rates rose. From 1999 to 2007, the inflation rate has remained substantially near to the 2% target, remaining most of the time below 2.5%.

(Altimari,2001:28) In fact, since 2001 euro area M3 has been growing at rates well above its reference value of 4,5%, while HICP inflation has remained broadly stable at rates around 2%. This observation seems to confirm the view that M3 growth has not been a reliable indicator for future price developments in the euro area recently. (Hofmann,2008:7)

4. Central Bank of the Republic of Turkey and Monetary Policy Strategies After 1999

In this part of the study, monetary policies of Central Bank of Republic of Turkey after 1999 will be examined. As we are trying to see the reflections of ECB’ a monetary policy strategy on the Central Bank of Republic of Turkey, year 1999 (establishment of ECB) is chosen as beginning.

4.1. Central Bank of the Republic of Turkey and Duties

The Bank was established on October 3, 1931 and opened officially on January 1, 1932. The Bank had, originally, a privilege of issuing banknotes for a period of 30 years. In 1955 this privilege was extended until 1999. Finally it was prolonged indefinitely in 1994.

According to the Law No: 1715, the basic aim of the Bank was to support economic development of the Country. In order to fulfill this aim, the Bank was given the following duties (CBRT,2008):

To set rediscount ratios and to regulate money markets,

To execute Treasury operations,

To take, jointly with the Government, all measures to protect the value of Turkish currency. With the introduction of economic development plans in Turkey in the Sixties, several changes were made in the Central Bank Law.

In the second half of the Eighties, the Bank inaugurated interbank money market, foreign exchange money market and started to make use of open market operations.

In 2001, Central Bank Law No:1715 article 4, amended. According to amendend article 4: The primary objective of the Bank shall be to achieve and maintain price stability. The Bank shall determine on its own discretion the monetary policy that it shall implement and the monetary policy instruments that it is going to use in order to achieve and maintain price stability. The Bank shall, provided that it shall not be in confliction with the objective of achieving and maintaining price stability, support the growth and employment policies of the Government. (CBRT, 2008)

The fundamental duties and powers of the Bank shall be to carry out open market operations, to conduct rediscount and advance transactions, to manage the gold and foreign exchange reserves of the country, to regulate the volume and circulation of Turkish Lira, to establish payment, to monitor the financial markets, etc. Fundamental powers of the Bank are, privilege of issuing banknotes,determine the inflation target together with the Government and adopt the monetary policy, utilize monetary policy instruments, carry out the operations of extending credits to banks, etc (CBRT, 2008)

4.2. General Principles of Central Bank of the Republic of Turkey’s Monetary Policy Strategy

In this section the monetary policies of Central Bank of the Republic of Turkey will be examined in three periods of 1999-2002, 2002-2005 and after 2005. In these 3 periods the monetary policy strategies differ from eachother.

4.2.1. Period of 1999-2002

Monetary and exchange rate policies for 2001 were announced at the end of 2000. Accordingly, the exchange rate policy would be carried out within the same framework.. While the main principles of monetary policy for 2000 were maintained, new targets were set for Net Domestic Assets and Net International Reserves. The unfavorable developments of November and February have compelled the Central Bank to follow policies that have been formulated to re-establish stability in financial markets after the crisis. All with this, “Transition to Strong Economy Program" was announced together with its measures and legal regulations. The program has emphasized on structural reforms and legal regulations rather than conjunctural policies. Abandonment of the existing exchange rate regime necessitated changing of the monetary policy strategy. For this purpose, a more active monetary policy has been designed and new performance criterion have been mentioned. Since the exchange rate anchor was abandoned, Base Money has been determined both as an intermediate target and a nominal anchor to provide a criterion to the economic agents to form their inflationary expectations. (CBRT,2001:8)

The Central Bank had formerly announced that inflation targeting regime would be implemented starting from the beginning of 2002. However, the conduct of inflation targeting was postponed because of the disturbances in money and foreign exchange markets arising from terrorist attacks of September 11, uncertainty atmosphere created by external financing needs, and high inflation level and rigid inflationary expectations. During this period, which will be a transition stage to inflation targeting system, the Central Bank will formulate the monetary policy towards reestablishing the price stability in the economy. In this framework, base money aggregate consistent with growth and inflation targets has been fixed as a performance criterion as of 2001. Similar to 2001, the aggregates related to net domestic assets and net international reserves will closely be monitored and short-term interest rates will effectively be used towards the inflation target. Moreover, priority will be given to enlightening of public and transparency issues. Announcements will regularly be made on the implementation of the monetary policy. With the signs of favorable progress in preconditions, transition to the inflation targeting system will come into effect. (CBRT,2001:9)

4.2.2. Period of 2002-2005

The monetary policy, which was launched at the beginning of year 2002, with Base Money as the nominal anchor and the interests as monetary policy instruments under floating exchange regime, has been pursued in this period too. In the said period, the CBRT has carried on with its implementations intended for attaining its final goal of price stability and enhancing financial stability in accordance with this goal. (CBRT:2002: 3) Implicit inflation targeting and Base Money were the basic nominal anchors of the monetary policy in 2002. The short-term interest rates, which are the main policy instruments of the Central Bank for stability objective, have been set after a comprehensive assessment of the effects of various macroeconomic variables on the future inflation developments. (CBRT,2003:1)

Implicit inflation targeting policy, which has been put into practice in 2002, is maintained in 2003. In accordance with this policy while short term interest rates are employed as the primary policy tool, monetary performance criteria and indicative targets are monitored within the framework of the program carried out with IMF. All criteria and targets set for the end of Arpil, June and September 2003 were achieved. Nevertheless, developments in October and November brought forth the possibility of exceeding the upper limit of end-year money base target. (CBRT,2003:23)

Achieving the inflation targets in both 2002 and 2003 demonstrates the success of the economic program and disinflation efforts. In the first quarter of 2004, favorable cost conditions persisted, the level of domestic demand did not put pressure on prices by forcing production capacity and the inflation expectations were consistent with the year-end target. (CBRT,2004 a: 4)

Therefore, interest rate decisions are made by taking into account the evaluations of the Monetary Policy Committee on the economy, the meeting days of which are announced in advance, and the decisions are publicized in the morning of the following working day. In addition, a further press release is issued with the title of “Inflation and Outlook” within two days of the meeting, explaining the rationale behind the decision, as well as CBRT’s general evaluations of the economic outlook. (CBRT, 2005: 20)

Due to the currency reform in 2005 six zeros were removed from the Turkish lira, enabling the borrowing instruments denominated in the New Turkish lira to be kept under the custody of international clearing houses. Together with the favorable economic developments, foreign finance institutions with high credit ratings began to issue bonds denominated in the New Turkish lira. These issues extended maturities and enhanced financial depth, created a potential to expand credit supply without causing maturity mismatch, as well as increased the capability of the Treasury for long-term bond issues. (CBRT, 2006 a : 41)

4.2.3. After 2005

The Central Bank of the Republic of Turkey (CBRT) adopted an inflation targeting regime starting in January 2006. Within the framework of the implicit inflation targeting strategy during 2003-2005, end-year inflation targets were announced and realizations undershot the targets. The favorable outcome of inflation rates remaining below the targeted rates in recent years led to perceptions that the targets announced by the CBRT were the upper limit, which was a reasonable strategy under the disinflation period. However, from now on, the CBRT will treat any upward or downward deviations from the target symmetrically. In other words, a significant downward shift of inflation from the target will be treated as seriously as an upward deviation. As it takes time for monetary policy decisions to influence the economy, monetary policy will focus on the consistency of the future, as opposed to the current, rate of inflation with the respective targets. (CBRT, 2006 b :51)

In the first year of the inflation-targeting regime, some supply-side shocks were experienced, which caused inflation to materialize above the path consistent with the target but important steps were taken in 2006 on the way to transparency, accountability and predictability, which are the main principles of the inflation targeting regime. (CBRT, 2006 b: 1)

CBRT has continued implement the monetary policy in 2007 based on the principles of inflation targeting regime. The Monetary Policy Committee meetings were held in line with the pre-announced annual timetable. Inflation in the first quarter of 2007, as foreseen, remained within the uncertainty band set around the path consistent with the target, whereas the decline in inflation stagnated in the last quarter due to both considerable increases in food prices, arising from drought as well as global conjuncture, and adjustments in administered prices. Thus, it has become obvious that the year-end inflation would remain outside the uncertainty band. (CBRT, 2007: 1)

Food, energy and other commodity prices continued to have adverse effects on inflation in the first quarter of 2008. Oil prices continued to rise. Moreover, rising financial volatility and declining risk appetite on the back of ongoing global uncertainties have led to exchange rate movements which had first round effects on March inflation. Consequently, inflation rose to 9,15 percent at the end of the first quarter, breaching the upper limit of the uncertainty band. (CBRT,2008 a: 1) The inflation target for 2008 was 4% but in the end of June inflation rose to10,61%. (CBRT,2008 b: 1) With these assessments together CBRT propose to revise the targets for 2009 and 2010 to 7.5 and 6.5 percent, respectively; and to set the target for the year 2011 at 5.5 percent.

Table 3: Inflation Targets and ex-post Values

200

2 2003 2004 2005 6200 2007 2008 2009 2010 2011

Target 35 20 12 8 5 4 4 4 4

Ex-post 29.7 18.4 9.3 7.7 9.6 8.39 10.61* - -

-Revised

* Inflation in June Source: CBRT

In the table above inflation targets and ex-post values are seen during the period of inflation targeting regime. During the period of implicit inflation targeting ex-post values are below the target value but during the inflation targeting period ex-post values are higher than the target. Also revised target values are shown for 2009-2011 period.

5. CONCLUSION

The main objective of the ECB is to maintain price stability has not changed to any significant extent since its establisment in 1999. Rather than taking direct responsibility for elimination of any output gap, the ECB purports to provide an environment in which the economy can naturally close the gap and that is done mostly through maintaining inflation near to 2% annually. The ECB’s strategies for achieving price stability are based on the two pillars approach: 1) assessing the short to medium-term determinants of price developments, with a focus on real activity and financial conditions in the economy (economic analysis); 2) focusing on a longerterm horizon, exploiting the long-run link between money and prices (monetary analysis). The ECB decided not to adopt strict price targets because, in its view, this is too mechanical and, like the monetary rule, does not take into consideration other relevant variables. The European central bank believes that, in the medium long term, monetary policy can be conducted by controlling M3.

Exchange Rate-Based Disinflation Program introduced in 1999 was the key element that shaped the framework of monetary policy and economic developments in 2000 for The Central Bank of the Republic of Turkey. . The program aimed at increasing primary surplus via tight fiscal policy, realizing structural reforms, accelerating privatization and implementing an incomes policy consistent with the inflation target. However, the basic policy instruments of the program have been the exchange rate and monetary policy. Under the global developments and with the idea of controling the inflation more effectively to maintain price stability The Central Bank had formerly announced that inflation targeting regime would be implemented starting from the beginning of 2002. Implicit inflation targeting and Base Money were the basic nominal anchors of the monetary policy between 2002 and 2005. The Central Bank of the Republic of Turkey adopted an inflation targeting regime starting in January 2006. In the first year of the inflation-targeting regime, some supply-side shocks were experienced, which caused inflation to materialize above the path consistent with the target but important steps were taken in 2006 on the way to transparency, accountability and predictability, which are the main principles of the inflation targeting regime.

Considering two central banks, the aim of the monetary poicy is same as maintaining pirce stability. But the monetary poicy strategies are different. The ECB’s monetary policy strategy comprises a quantitative definition of price stability, and a two-pillar approach to the analysis of the risks to price stability. CBRT’s monetary policy startegy is inflation targeting to maintain price stability.

BIBLIOGRAPHY

Altimari, Nicoletti (2001), “Does Money Lead Inflation in the Euro Area?”, ECB Working Paper No.63. Brand, Claus, Nuno Cassola (2000), “A Money Demand System for the Euro Area M3”, ECB Working Paper No.39.

Briault, Clive (1995), “The Costs of Inflation,” Bank of England Quarterly Bulletin, Vol. 35 February, pp. 33-45.

Calza, Alessandro, C. Gartner, J. Sousa (2001), “Modeling the Demand for Loans to the Private Sector in the Euro Area”, ECB Working Paper No.55.

Calza, Alessandro, Dieter Gerdesmeier, Joaquim Levy (2001), “Euro Area Money Demand : Measuring the Opportunity Cost Appropriately”, IMF Working Paper No.01/179.

CBRT (2001), Monetary Policy Report, Periodic Publications, November. CBRT (2002), Monetary Policy Report,Periodic Publications, October. CBRT (2003), Monetary Policy Report,Periodic Publications, October. CBRT (2004,a), Monetary Policy Report,Periodic Publications-I. CBRT (2004,b), Monetary Policy Report,Periodic Publications- IV. CBRT (2005), Monetary Policy Report,Periodic Publications-I. CBRT (2006a), Inflation Report-I.

CBRT (2006b), 2007 Monetary and Exchange Rate Policy. CBRT (2007), 2008 Monetary and Exchange Rate Policy.

CBRT, (2008), CBRT Law, www.tcmb.gov.tr [Accessed 30.05.2008] CBRT (2008a), 2008 Inflation Report-II.

CBRT (2008b), June 2008 Price Developments.

CBRT (2004), Inflation Targeting, www.tcmb.gov.tr , [Accessed 13.5.2008]

Cecchettı, Stephen G. (2000), “Makıng Monetary Polıcy: Objectıves And Rules”, Oxford Revıew Of Economıc Polıcy, Vol. 16, No. 4, pp.43-59.

Coenen, Günter, Juan-Luis Vega (1999), “The Demand for M3 in the Euro Area.” ECB Working Paper No.6. EC (1999), Compilation of Community Legislation, http://aei.pitt.edu/4910/01/003951_1.pdf [Accessed 12.05.2008]

ECB (1999), Euro Area Monetary Aggregates and Their Role in the Eurosystaem’s Monetary Policy Strategy, ECB Monthly Bulletin, February, pp.29-46

ECB(2002),Official Journal of the European Communities

http://mineco.fgov.be/euro_archives/euro_belgium/BCE_en.pdf [Accessed 5.5.2008]

ECB (2004), The Monetary Policy of The European Central Bank

ECB (2008), 1998-2008 Monthly Bulletin 10Th Anniversary of The ECB

EU, (2008), Treaty of Maastricht on European Union,http://europa.eu/scadplus/treaties/maastricht_en.htm , [Accessed 10.5.2008]

Feldstein, Martin (1996), The Costs and Benefits of Price Stability. University of Chicago: NBER.

Lucas, Robert E. (1972), “Expectations and the Neutrality of Money,” Journal of Economic Theory, Vol. 4 April, pp. 103-24.

Mishkin, Frederich (2008), “Does Stabilizing Inflation Contribute to Stabilizing Economic

Activity?”, Nber Working Paper 13970

Scheller, Hans Peter (2006), History,Role and Functions, ECB, Second Revised Edition.