Full Terms & Conditions of access and use can be found at

http://www.tandfonline.com/action/journalInformation?journalCode=vjeb20

Download by: [Universitas Maritim Raja Ali Haji] Date: 11 January 2016, At: 20:42

Journal of Education for Business

ISSN: 0883-2323 (Print) 1940-3356 (Online) Journal homepage: http://www.tandfonline.com/loi/vjeb20

What Makes a Top-Selling Textbook? Comparing

Characteristics of AIS Textbooks

Frank Badua, Mohsen Sharifi & Francis Mendez Mediavilla

To cite this article: Frank Badua, Mohsen Sharifi & Francis Mendez Mediavilla (2014) What Makes a Top-Selling Textbook? Comparing Characteristics of AIS Textbooks, Journal of Education for Business, 89:5, 257-262, DOI: 10.1080/08832323.2013.869531

To link to this article: http://dx.doi.org/10.1080/08832323.2013.869531

Published online: 03 Jul 2014.

Submit your article to this journal

Article views: 86

View related articles

What Makes a Top-Selling Textbook? Comparing

Characteristics of AIS Textbooks

Frank Badua

Lamar University, Beaumont, Texas, USA

Mohsen Sharifi

California State University, Fullerton, California, USA

Francis Mendez Mediavilla

Texas State University, San Marcos, Texas, USA

The factors involved in the selection of accounting textbooks are under-investigated, and most of the research is survey-based, largely ignoring the information that could be analyzed by direct inspection of textbook content and its impact on textbook selection. In this study the authors fill this lacuna by deploying content analysis of the textbook content and devising new measures of textbook quality that may impact their ultimate selection by accounting information systems (AIS) instructors. These novel measures are discussed in the light of textbook market share information gleaned from three sources: a survey of AIS instructors, and executives at two leading educational publishers. The authors conclude with a consideration of pedagogical policy implications of the findings.

Keywords: AIS, content, selection, texts, topics

Agrawal, Chakraborty, Gollapudi, Kannan, and Kenthapadi (2012) stated “Textbooks are. . . most consistently associ-ated with gains in student learning” (p. 1). Unfortunately, Bargate (2012) noted, “there is limited empirical research that focuses on the selection criteria used by accounting faculty when prescribing textbooks” (p. 114). Despite repeated calls for more research into accounting textbook adoption (Cornachione, 2004; Ferguson, Collison, Power, & Stevenson, 2007; Stevens, Clow, McConkey, & Silver, 2010) the literature remains scant, comprised mostly of sur-vey studies, which only indirectly measure textbook attrib-utes. This lack is exacerbated in accounting information systems (AIS), by AIS instructors’ dependence on text-books (Badua, Sharifi, & Watkins, 2011; Doost, McCombs, & Sharifi, 2002). Therefore this paper deploys content anal-ysis of AIS textbooks, devising new objective measures of textbook quality that impact their selection by instructors,

and guides how instructors could best use the chosen textbook.

Survey-based research by K. J. Smith and DeRidder (1997); Mehta, Mehta, and Aun (1999); Stevens et al. (2007); and Elbeck, Williams, Peters, and Frankforter (2009) all found that textbook currency is a highly ranked determining factor in textbook adoption decisions. Plausi-bly, this results from constant evolution in business, the economy, generally accepted accounting principles, and technology (Badua, 2008).

Other surveys focusing on the impact of ancillary mate-rial on textbook adoption decisions yield mixed findings. Earlier research by DeRidder (1997), K. J. Smith and Muller (1998), and Mehta et al. (1999) reported that ancil-lary materials were ranked low among criteria for the text-book selection decision. In contrast, later research by Stevens et al. (2007) and Elbeck et al. (2009), which found that availability of ancillary materials was a highly ranked determinant of textbook adoption. This may be a function of increased availability of such material, particularly those in digital format (Bargate, 2012).

Correspondence should be addressed to Frank Badua, Lamar Univer-sity, College of Business, 4400 MLK Parkway, Beaumont, TX 77710, USA. E-mail: [email protected]

ISSN: 0883-2323 print / 1940-3356 online DOI: 10.1080/08832323.2013.869531

Bargate (2012) took this research in a new direction, focusing on the content of the main body of the textbook itself, surveying faculty on the effect of innate textbook characteristics on the adoption decision. Bargate found that clarity and comprehensibility primarily drove textbook adoption.

In this study we followed Bargate (2012), focusing on textbook content, not currency or supplements. Currency is irrelevant when instructors have the latest editions of text-books, and Toerner (2006) stated that students ignore supplemental materials. Thus, this article focuses on char-acteristics that more directly impact student learning. More-over, while Bargate relied on surveys, this paper will measure textbook characteristics by direct inspection. This research method yielded objective rather subjective meas-ures of textbook attributes, making this paper distinct from previous research using faculty and student surveys.

DATA AND METHODOLOGY

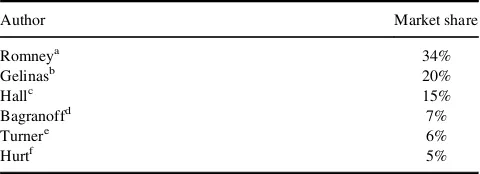

Six AIS textbooks provided the data. The texts used were the latest and second latest editions of three widely used AIS books, first-authored by Romney, Hall, and Gelinas. According to correspondence with executives at two aca-demic publishing firms, Wiley and Cengage (J. Cruz, per-sonal communication, March 27, 2013; K. Dan, perper-sonal communication, March 27, 2013), as well as a survey con-ducted at the AIS Educators’ Conference in 2012 (Preru-moso, 2012) these three textbooks are the most widely adopted, accounting for 70% of the AIS textbook market. Romney is consistently cited as the top seller, with Gelinas and Hall cited as being in second and third place, respec-tively (J. Cruz, personal communication, March 27, 2013; K. Dan, personal communication, March 27, 2013), and in fourth and second place, respectively, by Prerumoso (2012). Here we give greater credence to Romney being cited as the top seller with Gelinas and Hall in second and third place, respectively (J. Cruz, personal communication,

March 27, 2013; K. Dan, personal communication, March 27, 2013). The findings of that study are summarized in Table 1.

Texts will be used to refer to the specific editions (of which there are six in the data population), andbookor text-bookrefer to the three textbook series (Romney, Hall, and Gelinas). Data were gathered from the table of contents and indices of the texts, as a means of content analysis, a research method in which the object of study is text, and the data of interest may be any component part of a (usually) written verbal artifact, such as words, phrases, or sentences. The analysis was used for various research objectives including identifying the main characteristics and foci of communications or the attributes and intentions of the communicator (Berelson, 1971).

Content analysis has been used extensively in accounting. For example it has been used in accounting historical research (Previts & Brown, 1993), to investigate corporate communi-cations (Abrahamson & Amir, 1996; M. Smith & Taffler, 2000), to evaluate corporate disclosure (Cormier & Mangan, 1999; Hughes, 2000; Wiseman, 1982), and to characterize accounting pedagogy as reflected in textbooks (Tietz, 2007).

To facilitate content analysis, a list of AIS topics was created. The pages in which these topics were mentioned or discussed in each of the six texts in the population, as indicated in the tables of content and indices, were recorded.

ANALYSIS AND FINDINGS

Measures were devised to determine desirability or useful-ness. These measures included emphasis, diversity, integra-tion, and sequentiality.

Emphasis was defined as the extent to which a textbook stressed either conceptual or technical AIS topics. The dis-tinction between conceptual and technical topics follows roughly the dialectic established in classical Western philosophy, as stated in the Stanford Encyclopedia of Philosophy (2013).

Conceptual knowledge explains the principles of a sub-ject, linking different aspects of that subsub-ject, and relating them to its essential objectives. Technical knowledge guides performance on particular tasks found in professions based on the subject, and is intimately tied to the use of physical technology used in performing tasks.

Conceptual AIS topics comprise its basic concepts and objectives, the relationship between digital and manual accounting, the role of accounting professionals in AIS-related endeavors, and the models that guide those profes-sionals. These topics are usually abstractions, without phys-ical form. Examples of conceptual topics are the various business processes (i.e., transaction cycles) that group together various accounting transactions and management procedures, the system documentation techniques used to

TABLE 1

Gelinas, Dull, and Wheeler (2012). c

Hall (2011). d

Bagranoff, Simkin, and Norman (2009). e

Turner and Weickgennant (2008). f

Hurt (2012).

258 F. BADUA ET AL.

depict these processes, and most topics related to controls and to systems design and development.

Technical AIS topics consist of knowledge about the preferred way to use computer and telecommunications technology for accounting tasks. These topics are linked to physical artifacts. Hence, hardware falls under this defini-tion, as they are tangible objects, but even software, a set of abstract instructions, is classified because it is implemented by specific hardware designed to receive and execute those instructions. Examples include internet telecommunication protocols; specific hardware or software such as different computers and peripherals, programming languages, sys-tems auditing and engineering tools; and specific methods of implementing controls in certain technological environ-ments, including methods employed by cybercriminals to overcome these.

Certain topics are both conceptual and technical, as they contain knowledge related to both the fundamentals of AIS, and to more technologically grounded matters. These include enterprise resource planning systems, data commu-nications within and between networks, the relationship between systems documentation models such as the entity relationship/resource-event-agent model and their imple-mentation as databases, and certain aspects of computer security, systems analysis, and project management for sys-tems development.

A text’s emphasis on conceptual versus technical topics was operationalized as the proportion of pages devoted to a textbook topic that was defined as conceptual or technical. Page counts must be interpreted with caution as certain topics may be more succinctly explained than others. Some conceptual topics may be fully explained in one page, but technical topics, such as instructions for the use of hardware or software, may entail several pages of images and explan-atory text. Nevertheless, page, lines of text, and sentence counts have been used widely in content analysis of docu-ments for the purpose of determining emphasis even when these documents contained different formats of disclosure (Neu, Warsame & Pedwell, 1998; Patten, 2002; Tuwajiri, Christensen & Hughes, 2004).

A comparison of the classifications made by the authors led to an interrater agreement rate of 92%, or 156 of 170

topics. The numbers of pages focused on certain topics that were deemed to be both conceptual and technical in nature were divided equally between the conceptual and technical page counts. The page counts and the proportions of pages discussing conceptual and technical topics for all texts in the population are shown in Table 2.

The results reveal that the ratios of conceptual to techni-cal topics in all three texts is consistent between the latest two editions, and that the Hall and Gelinas texts have a greater proportion of pages devoted to conceptual topics than the Romney text. The Hall and Gelinas texts allocated 86% (14%) and 85% (15%) of their pages to conceptual (technical) topics, respectively. On the other hand, the Romney text assigned 75% and 25% to conceptual and technical topics, respectively.

These findings show that there is a greater focus on con-ceptual topics than technical topics, and that instructors pre-ferring a greater proportion of technical topics could choose the Romney text than the Hall or Gelinas texts. Unfortu-nately, it is difficult to make any claims beyond these two initial statements, as there is no consensus among stake-holders in the AIS field as to whether a conceptual, techni-cal, or perfectly balanced emphasis would be optimal.

Perfect balance between conceptual and technical topics seems ideal, but measures of emphasis, such as page counts, are imprecise proxies. Furthermore, different stakeholders desire different emphases. Historically, AIS curricula have been comprised of conceptual and technical topics (Badua, 2008). However, Welch, Madison, and Welch (2010) docu-mented diverging demand for information systems related conceptual and technical knowledge among audit firms ver-sus non–audit firms and government entities, with the for-mer seeking students with more software knowledge (technical), and the latter employing those with more data analysis and project management skills (conceptual). To add to the controversy, in AIS’s related field, management information systems (MIS), there has been a recent call for more conceptual coverage in the curriculum. Gackowski (2004, 2010) have criticized the MIS curriculum in general and MIS textbooks in particular as “overly technology laden but lacking the fundamentals” (Gackowski, 2010, p. 169).

TABLE 2

Page Counts and Proportions of Pages Discussing Conceptual and Technical Topics for All Texts

Romney 11 Romney 12 Hall 7 Hall 8 Gelinas 8 Gelinas 9

Pages C T C T C T C T C T C T

No. of pages per topic type 354 128 412 132 668.5 107.5 730.5 122.5 402.5 77.5 434.5 66.5 % of pages per topic type 73.44% 26.56% 75.74% 24.26% 86.15% 13.85% 85.64% 14.36% 83.85% 16.15% 86.73% 13.27% Ave. % of pages discussing conceptual

topics, both editions

74.59% 85.89% 85.29%

Ave. % of pages discussing technical topics, both editions

25.41% 14.11% 14.71%

Note:CDconceptual; TDtechnical.

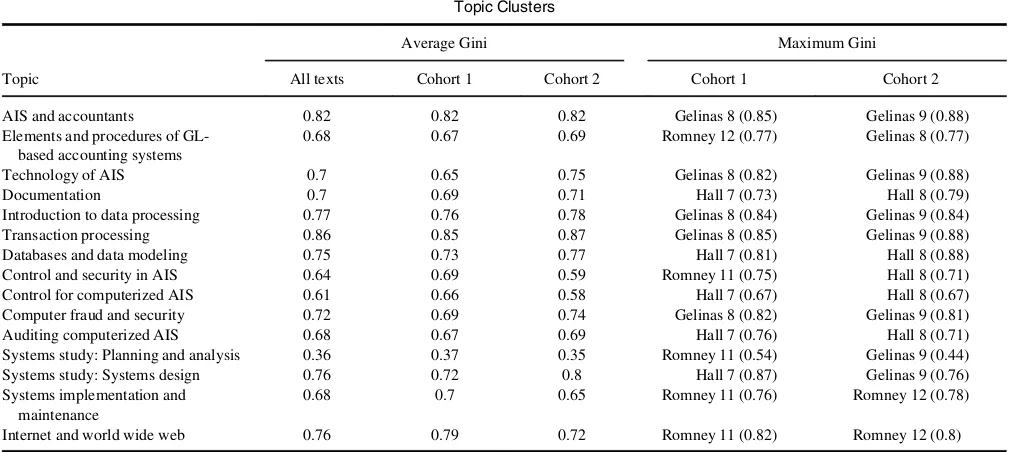

Diversity of topic coverage is the extent the discussion is more evenly distributed among a broader array of topics, operationalized as the Gini score computed over the num-ber of pages devoted to each topic and its relationship to the total number of pages devoted to that topic and related topics in a topic cluster. The Gini metric is typically com-puted asDAPSwere estimated by:

100X Xi

N

2

where,XXiDN.

That is, the Gini index equals 100 times the sum square of a distribution of proportions, which together make up one whole. It is named for the Italian economist and statisti-cian, Stigler (1994), who developed it as an index of diver-sity. Small Xi is the number of pages discussing a topic, andNis the number of pages of all related topics forming a topic cluster.

Computed thus, the metric generates a score on a 100-point scale that is lower (higher) for distributions that are more (less) equal and diverse (Stigler, 1994). However, to have a Gini score that is increasing in topic diversity, the scores presented in Table 3 were computed as the comple-ment of the Gini metric, that is:

1¡100 X Xi

N

2

where,XXiDN.

As may be seen from Table 3, the three topic clusters that were most diversely treated throughout the population were transaction processing with a Gini score of .86, the relationship between AIS and accountants (.82), and intro-duction to data processing (.77).

The text which consistently appears as having the most diverse discussion of these topics is the Hall text, which was shown to have the highest Gini score in nine topic clus-ters (four in the seventh edition, five in the eighth edition), followed by the Gelinas text with eight maximal Ginis (three in the eighth edition, five in the ninth edition), and with the Romney text having the least diverse, or most focused coverage of topics with six maximal Ginis (four in the 11th edition, two in the 12th).

It is difficult to state whether diversity or concentration is best. A diverse set of AIS knowledge and skills may be valued differently by different employers, with more focused and detailed expertise demanded by audit firms, and a broader, though perhaps less in-depth appreciation sought by other firms. Similarly, instructors of lower level undergraduate AIS courses might structure their courses as a survey of the subject, while instructors of senior-level or master of accountancy AIS courses, whose graduates are certified public accountant (CPA) candidates, would teach more specialized knowledge in greater detail.

Integration is operationalized as the number of chapters in which a topic is discussed. Discussion of a topic in multi-ple chapters may be viewed as positive because it provides a more comprehensive and cohesive narrative than a text that treats topics in isolation, and because repetition reinfor-ces student learning.

TABLE 3 Topic Clusters

Average Gini Maximum Gini

Topic All texts Cohort 1 Cohort 2 Cohort 1 Cohort 2

AIS and accountants 0.82 0.82 0.82 Gelinas 8 (0.85) Gelinas 9 (0.88)

Elements and procedures of GL-based accounting systems

0.68 0.67 0.69 Romney 12 (0.77) Gelinas 8 (0.77)

Technology of AIS 0.7 0.65 0.75 Gelinas 8 (0.82) Gelinas 9 (0.88)

Documentation 0.7 0.69 0.71 Hall 7 (0.73) Hall 8 (0.79)

Introduction to data processing 0.77 0.76 0.78 Gelinas 8 (0.84) Gelinas 9 (0.84)

Transaction processing 0.86 0.85 0.87 Gelinas 8 (0.85) Gelinas 9 (0.88)

Databases and data modeling 0.75 0.73 0.77 Hall 7 (0.81) Hall 8 (0.88)

Control and security in AIS 0.64 0.69 0.59 Romney 11 (0.75) Hall 8 (0.71)

Control for computerized AIS 0.61 0.66 0.58 Hall 7 (0.67) Hall 8 (0.67)

Computer fraud and security 0.72 0.69 0.74 Gelinas 8 (0.82) Gelinas 9 (0.81)

Auditing computerized AIS 0.68 0.67 0.69 Hall 7 (0.76) Hall 8 (0.71)

Systems study: Planning and analysis 0.36 0.37 0.35 Romney 11 (0.54) Gelinas 9 (0.44)

Systems study: Systems design 0.76 0.72 0.8 Hall 7 (0.87) Gelinas 9 (0.76)

Systems implementation and maintenance

0.68 0.7 0.65 Romney 11 (0.76) Romney 12 (0.78)

Internet and world wide web 0.76 0.79 0.72 Romney 11 (0.82) Romney 12 (0.8)

Note:AISDaccounting information systems; GLDgeneral ledger. 260 F. BADUA ET AL.

Table 4 summarizes the average number of chapters devoted to each topic, as well as the number of topics dis-cussed in greater than 1–4 chapters for each of the two edi-tions of the three texts in the study.

As can be seen from Table 4, the Hall texts have the highest integration measure, with an average of 1.21 between the two editions included in this data set. The Geli-nas and Romney texts are the second most and least inte-grated, respectively, with average integration measures of 1.14 and 1.12. The Hall text also leads the other two in topic integration whether the latest editions (Romney 12th, Hall eighth, and Gelinas ninth) or the second to the latest editions (Romney 11th, Hall seventh, and Gelinas eighth) were compared. Curiously, although the Romney text increased its level of topic integration between editions, the integration measures of the Hall and Gelinas texts declined between editions.

Sequentiality is the proximity of subsequent mentions of a topic to the chapter where it is first discussed, operational-ized as the number of chapters between the initial mention of a topic and the next chapter where it is subsequently dis-cussed. For topics that are mentioned in more than two chapters, the average number of chapters between the chap-ters in which the topic is discussed is used. In either case, the smaller that number, the more sequential the text. Sequentiality allows the reader to review basic information about a topic easily when that topic is mentioned again or its relationship to other topics is discussed, assuming the text is read in chapter order.

Table 5 shows the number of topics that were men-tioned in more than one chapter, and the average number of intervening chapters between those mentions (chapter distance).

As can be seen from Table 5, the Gelinas texts had the smallest average chapter distance (4.31), followed by the Hall texts with 5.29, while the Romney texts were the least sequential with an average chapter distance of 6.46. It

should be noted that if the latest editions were compared, the Romney text (12th edition) would be the most sequential.

CONCLUSION

When the findings are compared with the market shares of the texts, patterns of preference emerge. The top-selling Romney text has consistently the greatest proportion of technical topics, and the most focused topic selection. This suggests that instructors adopt a text that prepares the stu-dent for more specific, procedural, technologically aug-mented tasks encountered in the workplace. They discount a broader, more discursive treatment of topics in favor of a narrower focus on a small number of relatively more impor-tant topics.

The findings regarding integration and sequentiality are ambiguous. The differences in the integration metric are very small, on average ranging from 1.12 to 1.21, and instructors may find this number to be insignificant. Sequentiality is also hard to assess because instructors may base their selection on Romney’s historical nonsequential-ity, or its most recent, maximally sequential edition. There-fore, future researchers should focus on finer measures of integration, and testing the selection relevance of sequen-tiality on a larger sample. Another research ramification emanates from the apparent dissonance between calls for a greater focus on conceptual topics coming from MIS and the technical orientation inherent in AIS instructors’ choices.

The findings indicate several pedagogical implications. Whether a text is more conceptual or technical, instructors have to incorporate other material from other sources to provide a more balanced curriculum. Diverse texts might be taught with greater sensitivity to topic prioritization. Courses using texts that are less sequential have to make

TABLE 5

Number of Topics Mentioned in More Than One Chapter, and the Average Number of Intervening Chapters Between Those Mentions (Chapter Distance)

Text Romney 11 Romney 12 Hall 7 Hall 8 Gelinas 8 Gelinas 9

Topics mentioned in>1 chapter 6 11 20 17 15 8

Ave. chapter distances for topics mentioned in>1 chapter 9 3.91 5.32 5.25 3.53 5.08

TABLE 4

Summary of the Average Number of Chapters Devoted to Each Topic

Item Romney 11 Romney 12 Hall 7 Hall 8 Gelinas 8 Gelinas 9

Secular ave. # of ch. per topic 1.06 1.17 1.22 1.19 1.17 1.12

# of topics w/ ch. disc.>1 6 11 20 15 15 8

# of topics w/ ch. disc.>2 0 5 4 5 0 2

# of topics w/ ch. disc.>3 0 0 1 1 0 1

# of topics w/ ch. disc.>4 0 0 0 0 0 0

use of periodic review sessions, particularly immediately preceding midterms and finals.

Thought should be given to the text appropriate to the level at which AIS is taught, whether at the undergraduate level catering to students who are going to work as manage-ment of their organizations, or at the graduate level with a view to training CPA-track students. Again, differences in textbook characteristics, particularly in the balance of con-ceptual and technical material, will have to be carefully considered. Instructors of lower level undergraduate AIS courses would choose more diverse, conceptual texts, while instructors of upper level CPA track courses, would use more focused, technical texts.

Therefore, by employing content analysis instead of fac-ulty or student surveys, in this study we developed new met-rics that objectively rather than subjectively characterize qualities that influence AIS textbook adoption. These met-rics also guide instructors of various types of AIS courses, in choosing textbooks, and the manner in which they might administer the course given a particular textbook choice.

REFERENCES

Abrahamson, E., & Amir, E. (1996). The information content of the Presi-dent’s letter to shareholders.Journal of Business, Finance, and Account-ing,23, 1157–1182.

Agrawal, R., Chakraborty, S., Gollapudi, S., Kannan, A., & Kenthapadi, K. (2012).Quality of textbooks, and empirical study. Paper presented at ACM DEV 2012, Atlanta, GA.

Badua, F., Sharifi, M., & Watkins, A. (2011). The topics are a-changing. Accounting Educators Journal,21, 89–106.

Bagranoff, N., Simkin, M., & Norman, C. (2009). Core concepts of accounting information systems(11th ed.). Hoboken, NJ: Wiley. Bargate, K. (2012). Criteria considered by accounting faculty when

select-ing and prescribselect-ing textbooks, a South African study. International Journal of Humanities and Social Sciences,2, 114–123.

Berelson, B. (1971).Content analysis in communication research. New York, NY: Hafner.

Cormier, D., & Magnan, M. (1999). Corporate environmental disclosure strategies: Determinants, costs, and benefits. Journal of Accounting, Auditing, and Finance,14, 429–451.

Cornachione, E. (2004). Quality of accounting textbooks: Measuring students’ comprehension with the cloze procedure.Paper presented at the Southern African Accounting Association, Durban, South Africa. Doost, R., McCombs, G., & Sharifi, M. (2003). The state of teaching

accounting information systems: Is there a gap? Review of Business Information Systems,7, 61–67.

Elbeck, M., Williams, R., Peters, C. O., & Frankforter, S. (2009). What marketing educators look for when adopting a principles of marketing textbook.Marketing Education Review,19, 49–62.

Ferguson, J., Collison, D., Power, D., & Stevenson, L. (2007). Explor-ing lecturers’ perceptions of the emphasis given to different stake-holders in introductory accounting textbooks.Accounting Forum,31, 113–127.

Gackowski, Z. J. (2004). What to teach business students in MIS courses about data and information.Issues in Informing Science and Information Technology,1, 845–878.

Gackowski, Z. J. (2010). Informing as a discipline, an initial proposal. Informing Science, the International Journal of an Emerging Transdisci-pline,13, 165–176.

Gelinas, U., Dull, R., & Wheeler, P. (2012).Accounting information sys-tems(9th ed.). Mason, OH: South-Western Cengage Learning. Hall, J. (2011).Accounting information systems(8th ed.). Cincinnati, OH:

South-Western.

Hurt, R. (2012).Accounting information systems(3rd ed.). New York, NY: McGraw-Hill.

Mehta, S. C., Mehta, S. S., & Aun, B. L. (1999). The evaluation of business textbooks: An international perspective.Journal of Professional Serv-ices Marketing,19, 141–149.

Neu, D., Warsame, H., & Pedwell, K. (1998). Managing public impres-sions: Environmental disclosures in annual reports.Accounting Organi-zations and Society,23(3), 265–282.

Patten, D. (2002). The relation between environmental performance and environmental disclosure. Accounting Organizations and Society, 27(8), 763–773.

Prerumoso, R. (2012) Untitled working paper.

Previts, G., & Brown, R. (1993). Development of government accounting: A content analysis of Journal of Accountancy.Accounting Historians Journal,20, 119–139.

Romney, M. B., & Steinbart, P. J. (2000).Accounting information systems (8th ed.). Upper Saddle River, NJ: Prentice Hall.

Romney, M. B., & Steinbart, P. J. (2012).Accounting information systems (12th ed.). Upper Saddle River, NJ: Prentice Hall.

Smith, K. J., & DeRidder, J. J. (1997). The selection process for accounting textbooks: General criteria and publisher incentives A survey.Issues in Accounting Education,12, 367–384.

Smith, K. J., & Muller, H. R. (1998). The ethics of publisher incentives in the marketing textbook selection decision.Journal of Marketing Educa-tion,20, 258–267.

Smith, M., & Taffler, R. (2000). The Chairman’s statement: A content analysis of discretionary narrative disclosures.Accounting, Auditing, & Accountability Journal,13, 624–646.

Stanford Encyclopedia of Philosophy. (2013). Epistme and techne. Retrieved from http://plato.stanford.edu/entries/episteme-techne/ Stevens, R. E., Clow, K. E., McConkey, C. W., & Silver, L. S. (2010).

Dif-ferences in accounting and marketing professors’ criteria for textbook adoptions and preferred communications methods.The Accounting Edu-cators’ Journal,20, 33–45.

Stigler, S. (1994). Citation patterns in the Journal of Statistics and Proba-bility.Statistical Science, 9, 94–108.

Tietz, W. (2007). Women and men in accounting textbooks: Exploring the hidden curriculum. Issues in Accounting Education, 22, 459–480.

Toerner, M. C. (2006). Student readership of supplemental in-chapter material in introductory accounting textbooks.Journal of Education for Business,82, 112–117.

Turner, L., & Weickgennant, A. (2008).Accounting information systems controls and processes(1st ed.). Hoboken, NJ: Wiley.

Tuwajiri, S., Christensen, T., & Hughes, K. (2004). The relations among environmental disclosure, environmental performance, and economic performance.Accounting Organizations and Society,29 (5), 447–471.

Welch, O. J., Madison, T., & Welch, S. (2010). Accounting professionals’ value assessment of entry level IT skills and topics: A comparison of the differences between CPA firms and industry/government organizations. Issues in Information Systems,11, 211–215.

Wiseman, J. (1982). An evaluation of environmental disclosures made in corporate annual reports. Accounting Organizations and Society, 7, 53–63.

262 F. BADUA ET AL.