KPA Key Performance Area BCMM Buffalo City Metropolitan Municipality KPI Key Performance Indicator BCDA Buffalo City Development Agency kWh Kilowatt time. HR Human Resources PTIS Public Transport Infrastructure System HSDG Human Settlement Development Grant SALGA South African Local Government Association HSRC Human Science Research Council SDBIP Service Delivery Budget Implementation Plan IDP Integrated Development Plan SMME Small Micro and Medium Enterprises.

EXECUTIVE MAYOR’S SUMMARY

Over the next three (3) years, R563 million has been earmarked for the construction and rehabilitation of roads and stormwater across the city. This includes an amount of own funds of R120 million specifically for the replacement and rehabilitation of existing infrastructure in the city core.

COUNCIL RESOLUTIONS

The Council of the Metropolitan Municipality of Buffalo City, acting under section 75A of the Local Government Act: Municipal Systems Act (Act 32 of 2000), approves and adopts with effect from 1 July 2014 the draft rates for other services as set out in Schedule E. That in terms of section 24(2)(c)(iv) of the Municipal Finance Management Act, 56 of 2003, amendments to the Integr approved development plan as set out in 17. chapter of the budget, which was agreed at the council workshop held on March 13 and 15, 2014.

EXECUTIVE SUMMARY

What remains a cause for concern is the potential financial impact of write-offs on the institution's operations. This is necessary to ensure the city's continued economic growth and allow for business confidence.

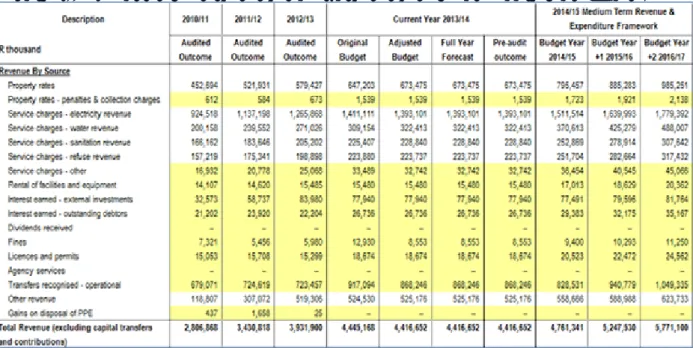

OPERATING REVENUE FRAMEWORK

It is anticipated that this will reduce water loss to a level comparable to the institution's peers. Page | 29 For the purposes of the MTREF budget, the electricity tariff structure has remained unchanged.

OPERATING EXPENDITURE FRAMEWORK

Budget appropriations in this regard total R710 million for the 2014/15 financial year and represent 15% of total operational expenditure. Financial costs mainly consist of long-term loan interest repayments (cost of capital).

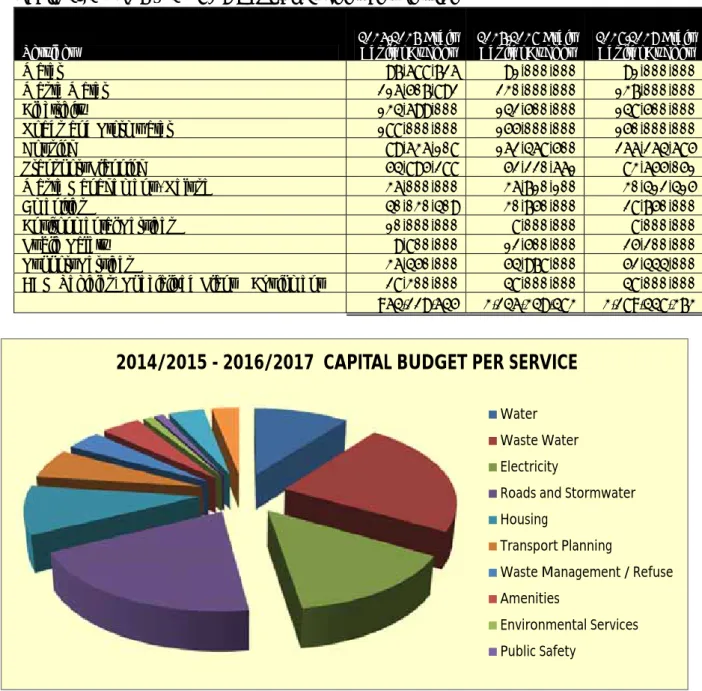

CAPITAL EXPENDITURE FRAMEWORK

The project is divided into 6 phases, the final phase of which is expected to be completed in 2017/18. The Quenera wastewater treatment works for approximately R200 million are progressing well and are expected to be completed by the end of the 2013/14 financial year.

ANNUAL BUDGET TABLES

This requires the simultaneous assessment of the Financial Performance Budget, Financial Position and Cash Flow, along with the Capital Budget. This table facilitates the visualization of budgeted operational performance in relation to the organizational structure of the city. The table below is an analysis of the surplus or deficit for electricity and water trading services.

It should be noted that the institution has made a strategic decision to use its own funds to mainly replace the existing infrastructure assets in the urban center of the city. The reasoning is that the ownership and net assets of the municipality belong to the community. As an example, the collection rate assumption will affect the municipality's cash position and then inform the level of cash and cash equivalents at the end of the year.

It is clear that the city's cash resources have grown significantly in the previous financial periods. Non-compliance with section 18 of the MFMA is presumed because a shortfall would indirectly indicate that the annual budget is not being properly funded.

SUPPORTING DOCUMENTATION

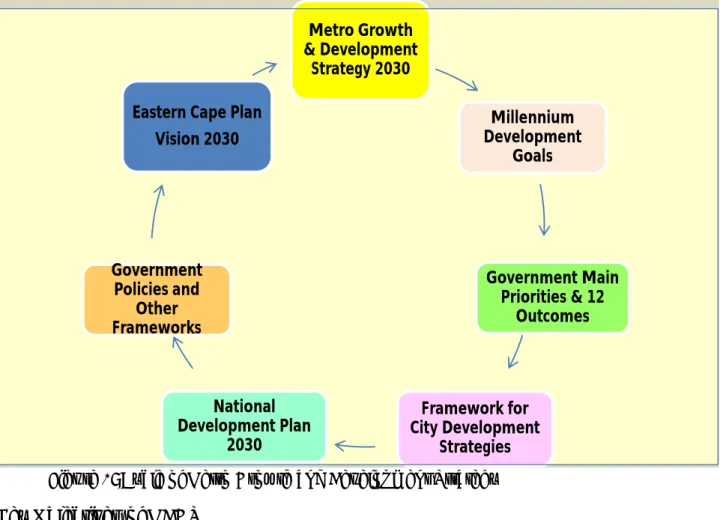

OVERVIEW OF ALIGNMENT OF ANNUAL BUDGET WITH IDP

Capital expenditure to operating expenditure is a measure of borrowing costs in relation to operating expenditure. Carrying out a general assessment every four years in accordance with the Municipal Property Rates Act. Review of the physical development plan to enable human resources to be closer to economic opportunities and job opportunities.

It must also be recognized in the local government environment that the resources that are accumulated must allow for the replacement of the asset that was originally created. The express purpose of the increase in cash resources is to enable the replacement of infrastructure assets in the future. Outlook Rand Positive June 2013 Positive The service provider will talk to the municipality as soon as possible to make an assessment of.

It is anticipated that with the establishment of the Enterprise Project Management Office (EPMO) the capital expenditures of the Office will improve in the KAS period. In analyzing the accumulated depreciation related to the identified infrastructure assets and comparing it with the net asset position of the institution, it has been determined that there is currently a financing deficit of 10 billion REA required for the future replacement of the infrastructure assets. Details of the City's strategy regarding asset management, repairs and maintenance are contained in SA34C.

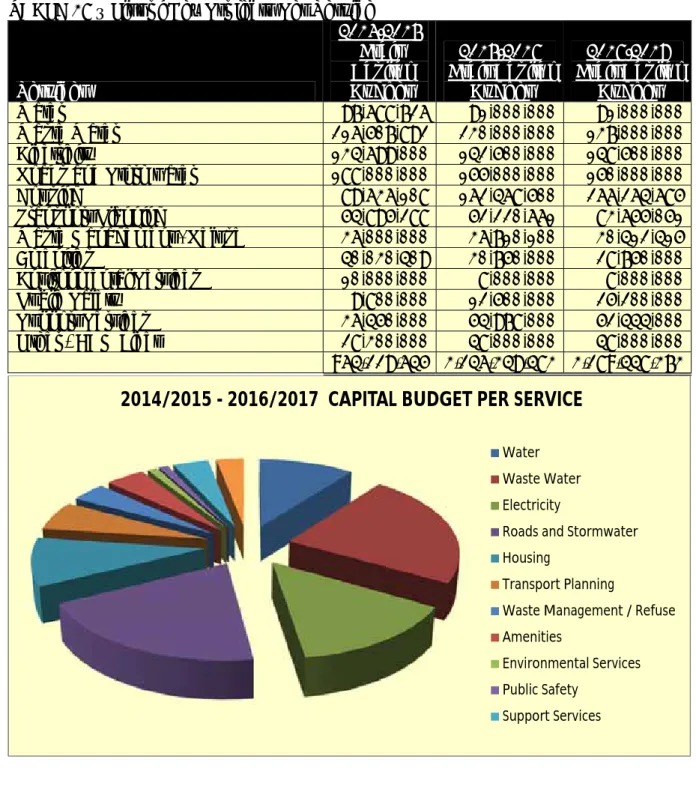

Details of the City's strategy in relation to asset management and repair and maintenance are contained in SA34B. In terms of the City's Supply Chain Management Policy, no contracts are awarded outside the medium-term revenue and expenditure framework (three years) unless MFMA Section 33 has been complied with. The following three tables present details of the City's capital expenditure programme, firstly on new assets, then the renewal of assets and finally on the repair and maintenance of assets.

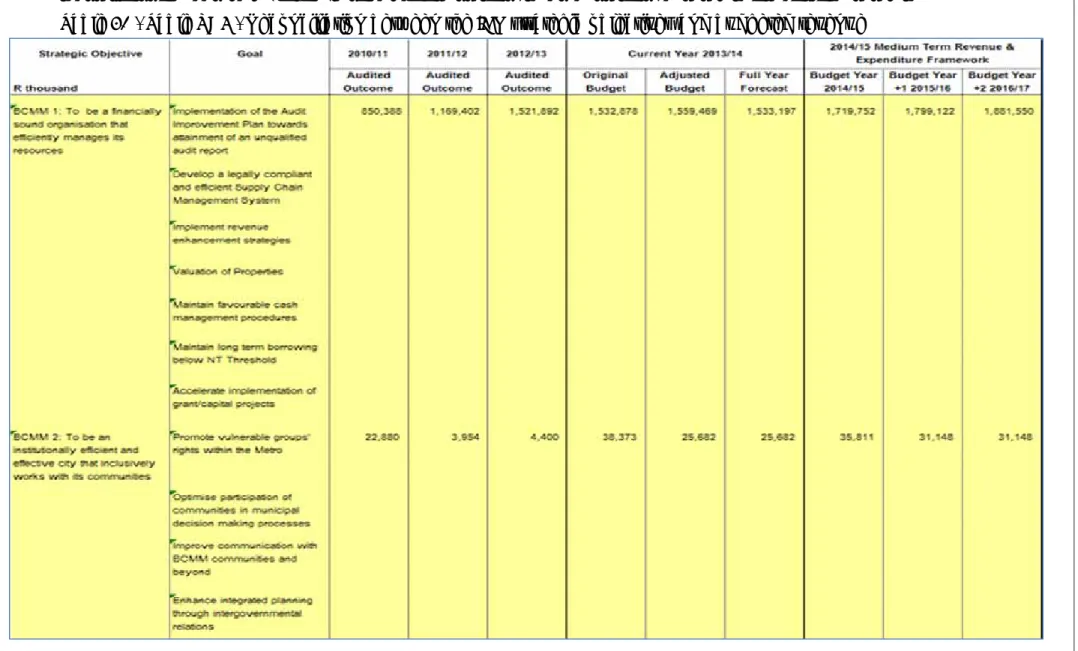

MEASURABLE PERFORMANCE OBJECTIVES AND INDICTORS

OVERVIEW OF BUDGET-RELATED POLICIES

Draft credit control and debt collection policy to be adopted by the council on March 26, 2014. The long-term borrowing policy was developed in accordance with the Act on Municipal Financing and Management no. 56 of 2003 and municipal budgets and debt disclosure reporting regulations. The policy was approved by the council on 29 May 2013.

The Asset Management policy was adopted on 29 May 2013 and provides direction for the management of real estate assets (infrastructure, community facilities, public facilities, investment properties and associated land and intangible assets). The capital infrastructure investment policy was approved on May 29, 2014, and the goal is adequate maintenance of assets to recoup the city's investment. The funding and reservation policy was approved by the Council on 29 May 2013 and aims to ensure that the municipality has sufficient and cost-effective funding to meet its long-term objectives through the medium-term execution of operating and capital budgets.

The Long-Term Financial Planning Policy was adopted by the Council on May 29, 2013 and includes the development, implementation and evaluation of a plan for the delivery of basic municipal services and capital goods. The Budget Implementation and Management Policy (Virement Policy) was adopted by the Council on 29 May 2013 and aims to manage budget transfers effectively and efficiently to ensure optimal service delivery.

OVERVIEW OF BUDGET ASSUMPTIONS

To adequately provide for the replacement of long-term assets in the future, and to reduce the risk placed on the National Government to allow for the replacement, Buffalo City Metropolitan Municipality has implemented the revaluation policy for long-term road assets. In the case of Buffalo City Metropolitan Municipality, there is a potential to increase the loan funding available to the institution to allow for the replacement of infrastructure assets as the institution is low leveraged. It is recognized that this will be part of a solution to adequately finance the replacement of the infrastructure assets going into the future, but it cannot be considered the complete solution.

The negative effect of this policy is that consumers are expected to pay a slightly higher monthly bill relative to its counterparts, but this policy is specifically implemented in an effort to allow for the replacement of infrastructure assets in the future. The institution recognizes that this is not a complete solution to the problem, however through a mix of local government resources, budgeted surpluses, long-term funding and grants from the National Government, all of which are strategically planned, the institution can allow for the replacement of existing aging infrastructure assets in the future. The reason for using this approach was specifically to allow the accumulation of additional funds for the replacement and/or renewal of these infrastructure assets in the future.

It must be recognized that if this approach were not followed, there would be significant risk to the national treasury and therefore the National Treasury being able to allow significant additional funding for the replacement of these assets in the future. What continues to be of concern are the high water losses which the institution will try to reduce in an effort to reduce the impact of tariffs on consumers in the future.

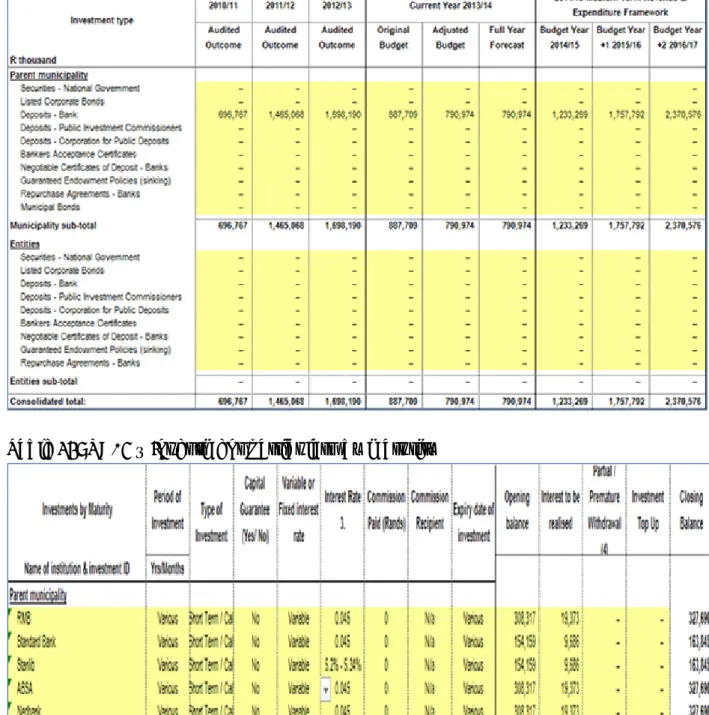

OVERVIEW OF BUDGET FUNDING

The table indicates available cash and investments increasing from R1.3 billion in FY 2014/15 to R2.4 billion in FY 2016/17. This resulted in a significant increase in the accumulated surplus associated with the acquisition of assets. The challenge for the city will be to ensure that the underlying planning and cash flow assumptions are carefully managed, especially performance against the collection rate.

The City has the ability to cover its ongoing operating costs for a period of 5 months in the 2014/15 fiscal year, increasing to 7.9 months in the 2016/17 fiscal year. The City has adopted an approach of recouping its depreciation year by year in order to renew and/or renew its existing infrastructure assets. In order for trading services to break even and/or generate a surplus, income growth in %age above inflation has ranged from 6% to 4.4% in recent years.

The stricter control measures of the Credit Control Policy are being implemented, the collection of arrears will be used as a source of additional cash inflows to finance future capital infrastructure projects. A contribution of R203 million towards bad debts is foreseen in the MTREF and is based on an average collection ratio of 92.8.

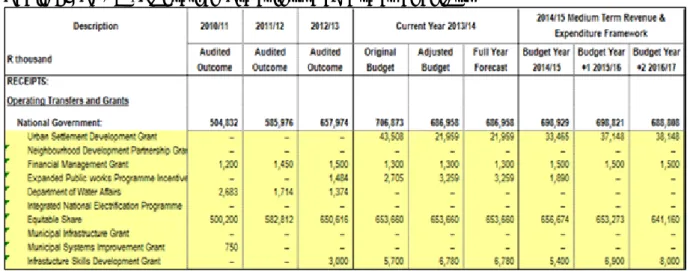

EXPENDITURE ON GRANTS AND RECONCILIATIONS OF UNSPENT FUNDS 114

MONTHLY TARGETS FOR REVENUE, EXPENDITURE AND CASH FLOW

ANNUAL BUDGET AND SDBIPs – INTERNAL DEPARTMENTS

ANNUAL BUDGET AND SDBIPs – MUNICIPAL ENTITIES AND OTHER

CONTRACTS HAVING FUTURE BUDGETARY IMPLICATIONS

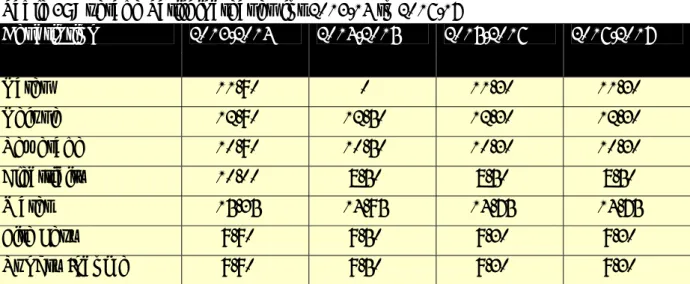

CAPITAL EXPENDITURE DETAILS

Page | 132 Table 64 - SA34b - Capital expenditure on the renewal of existing assets by asset class (continued).

LEGISLATION COMPLIANCE STATUS

OTHER SUPPORTING DOCUMENTS

CITY MANAGER’S QUALITY CERTIFICATE