Sturdy and Strong

Facing the Sky

CHAPTER

II

GLOBAL ECONOMIC RECOVERY

AND CHALLENGES FOR THE

Global Economic Recovery and

Challenges for the Future

2009 marked the beginning of the global economic recovery. The inancial market turmoil, which intensiied at the end of 2008 and the irst quarter of 2009, began to improve within the second half of 2009. Various risk indicators point towards reduced pressure for the inancial market. This development supported the beginning of improved economic condiions in 2009. Economic acivity within the real sector, both within the developed naions as well as in the developing naions, also showed signs of a recovery. In spite of the fact that the economy, in general, coninued to contract, global economic growth began to show signs of a recovery within the second quarter of 2009.

The global economy will coninue to face various challenges going forward. These challenges are paricularly related to the consequences of a response to policies that were aggressively implemented during the crisis. The irst challenge is related to the impact of a strategy to end policies that were applied during imes of crisis (exit strategy) including, among others, relaxing liquidity and iscal expansion in the developing naions. This challenge needs to be addressed to avoid a backlash on the global economic recovery process. The second challenge is a tendency towards polariziion in the world trade. This needs to be monitored in line with eforts to reduce distorions in world trade, given the fact that a number of countries have resorted to protecive policies during the crisis. Another challenge that needs to be monitored is the existence of global imbalance. All the aformenioned challenges may afect the sustainability of Indonesia’s economic recovery process and therefore, needs to be efecively addressed.

2.1

Monetary and Fiscal Policy

to Overcome the Global Crisis

Many countries responded to the global economic

uncertainty and pressure by implemening signiicantly intensive policies, both of convenional and non-convenional policies. Prior to Lehman Brothers

bankruptcy in September 2008, central banks of many

countries largely focused its eforts on reducing the ight liquidity by injecing substanial funds to inancial system. At the same ime, central banks of the developed and developing naions also strived to maintain

macroeconomic stability by lowering their benchmark rates, in some countries close to zero percent (Chart

2.1 and Chart 2.2). Nevertheless, following Lehman Brothers bankruptcy, the policy-making authoriies of many countries considered that the convenional policies it adopted proved to be inadequate in overcoming the slump in demand and the credit crunch.

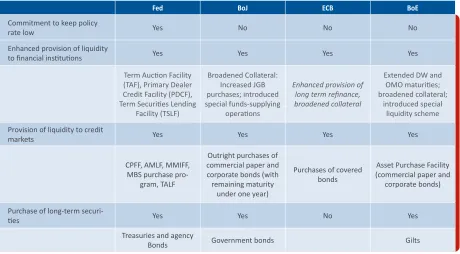

The post-Lehman Brothers bankruptcy period was characterized by the prevalence of non-convenional

policy measures that were implemented by policymaking

authoriies of a number of developed naions (Table

2.1). These non-convenional policies speciically sought

spiraling process that eventually afects inancial and real sectors.

In addiion, monetary authoriies also strived to maintain liquidity in the inancial markets. The high level of counterparty risk as well as the cauious aitude of the banking sector towards the efects of the crisis resulted in limited funds that were available for interbank loans.

The presence of money market loans with in longer

period compared with its normal condiion as well as a substanially wider insituional coverage helped maintain adequate liquidity in the inancial markets. In the meanime, to support adequacy of US dollars liquidity in many regions, the Federal Reserve, the Bank of England, the European Central Bank, the Bank of Japan, and the Swiss Naional Bank also engaged in currency swap

agreements.

Monetary authoriies also relaxed policies towards paries that receive loans from the Central Bank as part of their eforts to support the money market’s stalled funcion. Intervenion in credit markets was carried out by acquiring private sector assets and widening the opions in terms of the types of guarantee/securiies that the Central Bank can secure as collateral. This policy helped sectors that were directly afected by the crisis as well as provided a strong signal to the markets of the Central Bank’s willingness to push for an economic recovery.

A number of important policies were subsequently taken to guarantee bank deposits, recapitalize inancial insituions, and limit banking sector porfolio losses. Some countries also increased the maximum amount of insured deposits so as to adequately guarantee depositor

funds within the banking system. In the meanime, as part of eforts to stabilize inancial system as well as

prevent its worsening impact on the economy, a number of central banks in the developed countries, including the

US and Europe, took steps to rescue inancial insituions. (See Box: 2.1 The Role of Bailout in Global Economic Recovery Process).

From iscal side, governments in the developed and developing countries launched simulus packages to simulate the weakening economy. This policy was

taken mainly due to more limited room for lowering

interest rates while aggregate demand coninued to fall in the midst of rising unemployment. Fiscal simulus expansion, in the form of increased expenditure and tax cuts, were carried out to protect against the efects of declining domesic demand, for both household as well as business sector consumpion. In addiion, governments

of a number of countries also increased investment by

implemening infrastructure projects which has large muliplier efects on the economy.

The amount of iscal simulus to overcome the crisis is quite diverse across countries. The US iscal simulus amounted to USD 787 billion (5.5% of GDP), of which USD 287 billion were allocated to reduce taxes and USD 500 billion were allocated for infrastructure projects and other social programs. In Europe, the iscal policies of four major countries (Germany, UK, France, and Italy) amounted to 1% of GDP, while the three simulus packages that were released by Japanese government amounted to 12 trillion Yen, or equivalent to USD 122 billion. China’s government, on the other hand, disbursed 4 trillion Yuan, or the equivalent of USD 586

Chart 2.2 Monetary Policy in Developing Countries Chart 2.1 Monetary Policy in Developed Countries

percent

billion or 13.3% of GDP, which were mainly allocated to infrastructure development.

Despite the size of the simulus package that was recently

carried in response to the crisis varies from one country

to another, there were some similariies and diferences in terms of its composiion. The role of government expenditure within iscal simulus in many countries increased in 2009. Meanwhile, the size of the simulus in the form of tax cuts signiicantly varies across countries. For example, the simulus in the form of tax cuts in the US amounted to an average of 45 percent, while the iscal

simulus in other countries—such as Argenina, China, and India—were almost enirely in the form of expenditures. Countries such as Brazil, Russia, and the UK, on the other hand, had simulus packages that were almost enirely in the form of tax cuts.30 The efeciveness of the diferent

iscal simulus is sill debatable and depends on the economic condiions of each country.

30 Prasad, Eswar, and Isaac Srkin (2009), ”Assessing the G-20 Economic Simulus Plans: a Deeper Look,” Mimeo, Brooking Insituions, March 2009.

Source: IMF Staf Posiion Note, Unconvenional Choices for Unconvenional Times: Credit and Quanitaive Easing in Advanced Economies, 2009.

Table 2.1. Unconvenional Measures Undertaken by G-7 Central Banks

Fed BoJ ECB BoE

Commitment to keep policy

rate low Yes No No No

Enhanced provision of liquidity

to inancial insituions Yes Yes Yes Yes

Term Aucion Facility (TAF), Primary Dealer Credit Facility (PDCF), Term Securiies Lending

Facility (TSLF)

Broadened Collateral: Increased JGB

purchases; introduced

special funds-supplying operaions

Enhanced provision of long term reinance, broadened collateral

Extended DW and OMO maturiies;

broadened collateral; introduced special

liquidity scheme Provision of liquidity to credit

markets Yes Yes Yes Yes

CPFF, AMLF, MMIFF, MBS purchase

pro-gram, TALF

Outright purchases of commercial paper and corporate bonds (with remaining maturity

under one year)

Purchases of covered bonds

Asset Purchase Facility (commercial paper and

corporate bonds)

Purchase of long-term

securi-ies Yes Yes No Yes

Treasuries and agency

2.2

Cooperaion towards Global Economic

and Financial Stability

In dealing with the global crisis, various internaional cooperaion iniiaives were implemented. Among these iniiaives, the most signiicant ones were those that were implemented by the G-20 naions.31 The G-20 carried

out a number of high-level meeings that sought to intensify eforts to overcome the global crisis. The irst G-20 Heads of State meeing since the global crisis was

held in November 2008 (the Washington Summit), which

was followed by two other meeings, that is, the London Summit on 2 April 2009, and the Pitsburgh Summit on

24-25 September 2009. The G-20 focused on their eforts at tackling global issues, paricularly in response to the global crisis, which is classiied into three groups: (i) economic growth recovery; (ii) inancial sector restructurisaion; and (iii) internaional inancial insituion reforms.

g

The G-20 and the Commitment to

Strengthen Economic Growth

At their meeing in Pitsburgh on 20 September 2009, the G-20 naions revealed plans to strengthen sustainable and

balance global economic growth. Leaders of the G-20 naions expressed their commitment to work together to formulate and implement iscal, monetary, trade, and

structural policies that are consistent with sustainable

and balance global economic growth. To prevent asset

price and credit cycle from disturbing instability, the

G-20 naions also expressed their commitment towards implemening macro-prudenial policies and regulaions.

One of the issues stressed out from implemening

sustainable economic growth model is taking social and environmental dimension of economic development into

account. To achieve this objecive, the G-20 requested IMF’s assistance to help inance ministers and Central

Bank governors with a mutual assessment process by developing a forward-looking analysis regarding the

policies taken by the G-20 countries. In the meanime, the World Bank has been asked to support eforts to enhance development and poverty eradicaion as part of its eforts towards balancing global growth.

g

The G-20 and Commitment towards

Global Financial Stability

To achieve and strengthen global inancial system, in the G-20 meeing held in November 2008, a proposal was made to expand the Financial Stability Forum’s (FSF) membership. Formed in 1999 by inance ministers and central bank governors of the G-7 naions, the FSF iniially comprised of the G-7 member naions. Following the G-20 Heads of State Meeing held in Pitsburgh in April 2009, the FSF’s membership was subsequently expanded by including all the countries within the G-20. Through this expansion, the FSF was transformed into

the Financial Stability Board (FSB). The membership’s

expansion was meant to strengthen the forum’s efeciveness as a mechanism for naional authoriies, standard determining agencies, and internaional inancial insituions to address vulnerability as well as to develop and implement regulaions, supervision, and other policies regarding inancial stability.

The G-20 countries had taken, since the beginning of the crisis, various measures such as strengthening prudential supervision, improving risk management, enhancing transparency, improving market’s integrity, establishing supervisory colleges, and strengthening

international cooperation. In this regard, the G-20 countries intensified and expanded the scope of

regulation and supervision through stronger regulations

on Over The Counter (OTC) derivatives transactions,

securitization markets, rating agencies, and hedge

funds. In this case, the FSB also monitored the implementation of the measures.

At their meeing held in Pitsburgh in September 2009,

the leaders of the G-20 countries agreed to implement

measures aimed at enhancing naional and internaional standards. In the meanime, authoriies at the naional

level were asked to consistently implement global

standards so as to ensure a level playing ield and avoid market fragmentaion, protecionism, and regulatory arbitraion. Speciically, in strengthening the internaional inancial system, the leaders of the G-20 naions asked the G-20’s inance ministers and central bank governors to achieve an agreement on an internaional framework that is aimed at the following aspects.

First, developing high quality bank’s capital and reducing capital procyclicality. The G-20 naions were commited to developing internaionally agreed upon regulaions that sought to improve the quality and quanity of bank capital and avoid excess leverage.

Second, implemening eforts to reform compensaion pracices of inancial insituions needed to ensure inancial system’s stability. Excessive compensaion in the inancial sector is relecive of and leads to excessive risk taking. As a result, reforming policies and compensaion pracices are important elements for enhancing inancial stability.

Third, enhancing the OTC derivaive markets. All OTC derivaive contracts must be traded through the exchange

markets (bourses) or through an electronic trading

plaform, and clearing must be done through a central counterparty before end of 2012.

Fourth, addressing resoluion between naions and

Systemically Important Financial Insituions (SIFI). Financial insituions that are systemically important must develop irm-speciic and internaionally consistent resoluions and coningency plans.

will be completed before June 2011. In addiion to this,

there is also a commitment to maintaining the momentum

for handling maters pertaining to tax havens,money

laundering, corrupion, terrorist inancing, and prudenial standards. The countermeasures against tax havens will begin in March 2010. In the meanime, the Financial Acion Task Force (FATF) was requested to reveal to the public a list of high-risk jurisdicions prior to February 2010.

One of the progresses achieved by the Basel Commitee

for Banking Supervision (BCBS) accords, up to November

2009, is the formulaion of concrete proposals to

reduce procyclicality from Basel II and introduce a

bufer counter-cyclical mechanism that comprise four elements, which are: (i) reduce cyclicality of capital adequacy requirements; (ii) provide provisions that are forward-looking; (iii) create bufer capital for individual

banks and the banking sector that can be used during

imes of distress or crisis; and (iv) achieve substanially wider macro-prudenial objecives to limit excessive loan

growth and protect the banking sector from systemic

risk. A compreshensive package that is used to resolve procyclicality issues will be resolved prior to 2010.

Apart from the developments pertaining to bank’s capital, the FSB has also reported progress in other

issues, such as strengthening accouning standards, reforming compensaion policies, improving the OTC derivaives market, resoluion on vital systemic transnaional and inancial insituions low of funds, and

strengthening compliance towards regulatory standards

and internaional monitoring. Furthermore, the FSB and its members also coninually strived to develop quanitaive tools and indicators to monitor and measure macroprudenial risks within the inancial system.32

During the meeing of the G-20 inance ministers and

Central Bank governors that was held in November 2009,

the IMF, BIS and the FSB submited their views on the formulaion of guidelines regarding the methods by which respecive countries measure systemic levels of inancial insituions, markets, and instruments.33 This view

contains the framework used to idenify issues that are

Too Big Too Failin relaion to vital inancial insituions.

32 In line with eforts towards strengthening accouning standards as well the development of quanitaive tools and indicators to monitor and measure macroprudenial risks within the inancial system, Bank Indonesia coninuously updates Monthly Report of Commercial Banks (Laporan Bulanan Bank Umum or LBU), which is a inancial report of banks that must be submited to Bank Indonesia monthly. 33 “Guidance to Assess the Systemic Importance of Financial

Insituions, Markets, and Instruments: Iniial Condiions”

Aside from these issues, the FSB also reported the

progress made pertaining to hedge funds, credit raing agencies, supervisory colleges, and crisis management. In relaion to this, the main issues focused on the iniiaive’s consistency among naions or regions and steps to avoid instances of regulatory arbitraion. For this area, the FSB has formed the Implementaion Monitoring Network to monitor the implementaion of the G-20 and FSB’s recommendaions, as well as idenify diferent policies taken by various countries to resolve the issues.

g

The Role of the IMF

During the global inancial crisis, the G-20 countries also implemented a number of iniiaives that they considered

necessary to enhance the IMF’s role in reducing the

damaging efects of the crisis. The leaders of the G-20 naions expressed their commitment to increase funds available for the IMF to enhance its ability to miigate spreading of the global inancial crisis to the emerging markets and developing countries. The G-20 countries are commited to increasing the IMF’s funds by USD 750 billion through renewing and extending IMFNew

Arrangements to Borrow (NAB) amouning to USD 500 billion. The proceeds from the IMF’s gold sales, along with the IMF’s internal funds and other sources, are expected

to increase the IMF’s capacity to provide medium-term

loan by more than twice.

As part of its eforts to handle the crisis, the IMF has launched a new loan facility (Flexible Credit Line) which is more lexible and not restricted with condiionality

for countries with a good track record that need to

strengthen their balance of payments (BOP). In the meanime, to strengthen their roles in crisis prevenion, the G-20 countries have requested the IMF and the FSB to

cooperate in providing early warning system for

macro-economic and inancial risks, as well as eforts required to anicipate such risks.

The IMF has also allocated Special Drawing Rights (SDR)

amouning to USD 283 billion to strengthen global liquidity in 2009.34 More than USD 100 billion of this

amount will be used as addiional reserves for emerging markets and developing naions. The realizaion of the

general allocaion of SDR was simultaneously allocated to IMF member countries on 28 August 2009. Meanwhile, speciic allocaion of SDR was allocated on 9 September 2009. The allocaion was made on the basis of the quota proporion of each member countries. Overall, the increase in general allocaion of SDR has increased each country’s allocaion of SDR to 74% of their quota.

To date, there are two types of SDR allocaions carried out by the IMF for its 186 member countries, which are:(i)general allocaion amouning to a total SDR of

161.19 billion, equivalent to USD 250 billion. This type of allocaion is part of the IMF’s eforts to overcome the global crisis that can signiicantly afect global liquidity; and (ii) special allocaion amouning to a total SDR of 21.5 billion, equivalent to USD 33.0 billion, that serves as part of a previous agreement (1997) that has just been fulilled this year. For Indonesia, the SDR allocaion is beneicial to strengthen the reserve bufer for its external liquidity by increasing Indonesia’s foreign exchange reserves by SDR 1.74 billion, or the equivalent of USD 2.70 billion, of which SDR 1.54 billion comes from general allocaion and SDR 200.1 million comes from special allocaion.

Apart from eforts aimed at intensifying the IMF’s role

in facing crisis, the G-20 also took measures to enhance

the role of Mulilateral Development Banks. At their meeing in April 2009, the G-20 countries had requested the Mulilateral Development Banks to intensify loan disbursements needed to reduce the efects of the crisis

on the world’s poorest countries by providing them access

to simpliied faciliies, new faciliies and equipments, and promptly increasing the amount of available fund.

Regarding the IMF governance, the leaders of the G-20

countries agreed on the importance of eforts towards improving IMF’s credibility, legiimacy, and efeciveness (see Box: 2.2 Insituional Reforms in Global Recovery: Breton Woods Insituion). These countries agreed that the IMF must coninue to funcion as an organizaion that is based on a quota with distribuion relecing the relaive weight of the respecive countries within the global economy, which has witnessed signiicant changes since the IMF was founded. The G-20 Heads of State expressed their commitment to increase the quotas of the emerging markets and developing countries by at least 5 percent. The quota reform is part of the IMF’s governance reforms that covers, among others: (i) harmonizing quota and voice; (ii) size and composiion of the Execuive Board; (iii) ways of enhancing the Board’s efeciveness; and (iv) Fund

governor’s involvement in strategic supervision of the IMF. The acceleraion of the review of the IMF’s quotas from 2013 to 2011 will be part of the IMF’s quota reforms.

Apart from improving governance within the IMF, the G-20 leaders also agreed to improve governance and

the operaional efeciveness of the World Bank. They also stressed the need to change the voing system within the World Bank through a formula that relects a

country’s economic weight and the development mission

of the World Bank. In this regard, voing rights of the developing countries are expected to increase by at least 3 percent, in addiion to the 1.4 percent increase that was granted to under-represented countries. This agreement is expected to be achieved prior to the the spring meeing in 2010.

g

Internaional Trade Finance Iniiaive

Various factors resulted in a more limited source of global

trade inance. Receding liquidity and low demand from the global economy, along with ight liquidity from banks

as a result of the losses incurred by the banking sector,

as well as rising risk factors in internaional trade due to rising country risk, led to a drasic reducion in the sources of trade inancing. Based on the IMF-BAFT (Banker’s Associaion for Trade and Finance) survey, the low of trade inancing from developed countries declined by 6% (y-o-y).35 In the meanime, the low of global trade

inance was esimated to decline by 10% in 2009.

Numerous eforts were made to increase sources of trade inance. Concerns on increasingly limited sources of internaional trade inance have led governments, internaional insituions, as well as the private sector to engage in various policies and cooperaion to facilitate global trade inancing. This was made through various measures as follows:

- Enhancing the value of trade inance faciliies by

regional development banks such as the IDB, EBRD,

ADB, and AfDB.

- Short-term inancing, in the form of Working Capital Loans and loan guarantees from various export credit inancing insituions, speciically aimed at exports to

countries such as Germany, Japan, Korea, China, and

the US.

- Providing currency by central bank that possesses

large foreign exchange reserves to provide a suicient amount required by banks for export and import

through a repurchase agreement. This policy was implemented by, among others, Brazil, South Korea,

South Africa, India, and Argenina.

- Cooperaion package in accordance with the G-20 Agreement (G-20 London Summit) to accelerate global trade amouning to USD 250 billion within a period of 2 (two) years (2009-2010) through export credit inancing programs as well as Mulilateral Development Banks.

This Agreement is expected to be implemented through

the support and commitment from all of the governments

of the G-20 countries, export credit agencies, and mulilateral/regional (MDBs) insituions. This iniiaive

was agreed upon the basis of the need to urgently engage

in collecive and coordinated measures by all of the G-20

countries to overcome the decline in the trade volume as

a consequence of the efects of the global economic and inancial crisis. Limited inancing support is perceived to be one of the factors of fall in global trade. Therefore, the availability of suicient trade inancing is expected to revive global trade aciviies and growth.

The agreement of the G-20 leaders was followed up by a

meeing at technical-level, that is, G-20’s Working Groups on Trade and Finance which is one of the ive G-20’s

working groups formed within the framework of resolving

the global crisis.36 This meeing successfully agreed on a

number of important issues on trade inance:

- Signiicantly increase the amount of commitment for trade inance, from USD 250 billion (as agreed upon within the London Summit), to USD 402.2 billion. This increase largely comes from the updated indicaive

36 Prior to this, as a follow up to the outcome of the G-20 Leaders’ Summit 2008 held in Washington DC, 4 (four) Working Groups (WG) related to the implementaion of the Washington Acion Plan (WAP) were formed: (i) WG on Strengthening Transparency and Enhancing Sound Regulaion (WG 1); (ii) WG on Internaional Cooperaion and Market Integrity (WG 2); (iii) WG on Reforming the IMF (WG 3); (iv) WG on Reforming the World Bank and Mulilateral Development Banks Reform (WG 4). In line with the formaion of these working groups, Indonesia was appointed to serve as the co-chair for WG4 along with France.

commitment that was submited by the G-20 countries (bilateral contribuion).

- The government and MDBs will update or submit (for

those that have not) an indicaive commitment within this iniiaive, including uilizing the commitment that was submited.

- Submit the progress of the trade inance iniiaive at the Pitsburgh Summit (September 2009).

The commitment that was submited by the G-20 member

countries comprised the total amount of the facility

or various policies that can generate export/import inancing during imes of global inancial turmoil. In addiion, this commitment is also intended to increase market conidence on the G-20 governments’ ability to support global trade recovery. In this regard, Indonesia is commited to provide trade inancing of USD 2.5 billion. By assuming that changes for two years amounts to four imes through the approach used by the G-20, then this commitment approximately amounts to around USD 10 billion. This amount is supported by Bank Indonesia’s commitment amounts to USD 0.59 billion, the government’s commitment (in the form of iniial capital and LPEI’s addiional funds) amounts to USD 0.6 billion, JBIC’s loan amounts to USD 0.5 billion, and state-owned bank loans amounts to USD 0.83 billion.

Towards the end of 2009, the sources of trade inancing coninued to show improvement. Based on the ICC’s

2.3

Global condiions that began to recover and a beter

economic prospect brought about a number of consequences, which, among others, is in the form

of exit strategies for iscal simulus as well as relaxed

monetary policies that were carried out in response to the crisis. To anicipate rising inlaion caused by relaxed

policies introduced at the ime of the global inancial

crisis, the central banks of the developed and developing

naions implemented various monetary policy measures in accordance with its respecive domesic economic condiions. In the meanime, to manage risks during the

course of the economic recovery, the exit strategy needs

to be implemented at the right ime and stage. In this

regard, the IMF has issued the following seven principles for exit policy:37

- Timeframe for exit policy must be based on the

state of the economy and the inancial system. The communicaion strategy and coningencies will help anchor market expectaions and miigate market fear.

- Through a number of excepions, iscal consolidaion must be a main priority. In the meanime, monetary policy can be adjusted more lexibly if normalizaion is

required.

- Exit strategy for iscal policies must be transparent,

comprehensive, and clearly communicated with the

objecive of reducing government debt to a prudenial level within a clearly speciied imeframe.

37 IMF (2009), “Global Economic Prospects and Principles for Policy Exit,” Group of Twenty, Meeings of G-20 Finance Ministers and Central Bank Governors, St. Andrews, United Kingdom, November 6-7, 2009.

- A stronger primary balance should be the prime driver

in iscal adjustment that begins with acions to ensure that iscal simulus undertaken to handle the crisis is a

temporary measure.

- Non-convenional monetary policy should not be concluded before a convenional monetary policy begins to be ightened.

- Economic condiions, inancial market stability, and market mechanism must determine the ime and method by which the inancial support policy is

terminated.

- Consistently formulaing an exit policy will improve results for all countries. Coordinaion is required but this does not imply the need for synchronizaion. The lack of policy coordinaion can create bad spillovers.

Throughout its path, economic cycles across countries

or region are diferent in such a way that each of them may need diferent exit strategy. On the one hand, an

exit strategy that is prematurely applied runs the risk of encountering a ‘false dawn’ that can bring the world’s

economy to the brink of a deepening recession. On the other hand, if the iscal and monetary simulus are let to

swell within the long-term, then there are two types of

risks that may potenially arise (monetary risk and iscal risk) and intensify inlaionary pressure while economic

growth experiences a ‘crowding out’(Diagram 2.1).

The irst risk occurs loosening monetary policies coninues. Risks associated with a prolonged loose

monetary policy can lead to asset price bubbles, rising

inlaionary expectaions, and increased carry trade from developed naions to developing naions. This condiion will ulimately lead to rising inlaion. The second risk occurs as a consequence of prolonged loose iscal policy in the form of rising iscal deicit as well as government debt. On the one hand, even though concerns on the sustainability of iscal policies of developed naions are minimal, however, this condiion may lead to long-term

real interest rate increase. This increase in interest rates

will ulimately cause investments to decline (crowd out),

which leads to a decline in economic growth. The worst

efect that can happen is in the event of a payment default by iscal authoriies, maturity of debt will be shorter, leading to higher risk premiums that afect overall inancing. This condiion can be avoided when iscal authoriies possess a credibility to implement medium and long-term iscal consolidaion.

Other iming, another important issue regarding exit strategy is management of expectaions on how the exit strategy will be implemented. In this regard, efecive communicaions is needed to explain the background of

the decision to implement the exit policy. If this is not

communicated properly, inancial markets may overreact to the decision on the exit policy. This may ulimately lead

Diagram 2.1 Exit Strategy Risks

The Risk of a second round of crisis

the central bank to postpone its decision to implement the exit policy which, indeed, is urgently required.

g

Implicaions of the Exit Strategy on

Developing Countries

The impact of the developed naion’s exit strategy on the economies of the developing naions, including Indonesia,

depends on the level of their economic transparency

and openness in terms of inancial transparency as well as trade. One of the challenges that developing naions face is the ability to manage the low of short-term

capital that arises as a result of asymetrical economic recovery between the developed countries and those of the developing countries. In this regard, a policy’s

efeciveness will naturally depend on the speed of the

recovery itself as well as the exit strategy applied by the

developed naions, paricularly the US.

The rapid inlow of short-term capital led to the appreciaion of both foreign exchange and asset prices that rose sharply. On the other hand, the sterilizaion of the foreign exchange market will increase the inancial

market’s liquidity, which in turn will drive interest rates

to decline to levels lower than their opimal level. In the meanime, ight monetary policy is also a diicult

choice for the central bank as this may subsequently

lead to increased foreign exchange appreciaion that is considered hindering recovery process. On the other hand, eforts made by the developing naions to reduce the appreciaion of currency leads lower export compeiiveness of countries that undergo a slower rate of

recovery, such as the US and Europe, thereby delaying the exit strategy process within these countries.

Limiing capital inlow directly does not also seem to be the right alternaive for the developing countries. The general view for a policy that limits capital inlow is that it is efecive only if it is equitably and simultaneously applied among countries. Given that diferent countries possess diferent economic agendas even though it

is conceptually possible, the policy to uniformly and

simultaneously apply a policy to limit capital inlow does not seem pracically feasible. Coordinaion on exchange

rate policy does not also seem applicable given that

emerging market naions sill require a compeiive

currency exchange rate.

Apart from economic transparency, other economic

characterisics, in addiion to its economic policy system, also afected the exit strategy’s impact on the economies of developing naions. Economic characterisics such as the producion and demand structure, the exchange rate pass-through, the formaion of expected inlaion,

Diagram 2.2 Exit Policy Transmission Mechanism Convenional Policy

pressure on exchange rate

Pressure on Current Account

Output Inflaion

interest rate

Privaizaion Stock PriceDecrease Risk appeitesubside

and the level of inlaionary persistence play a key

role in determining how policies -including exit policy-

implemented in developed countries are transmited to

the developing countries.

Speciically, the mechanism for transmiing the exit policy of the developed countries, paricularly of that

of the US, to Indonesia’s economy is expected to go

through two main channels, that is capital low and trade channels (Diagram 2.2). Regarding capital low mechanism, the exit policy is relected by the US policy on

rising interest rates, which subsequently results in capital

ouflow from Indonesia and other developing naions

to the US. As a result, the US dollar strengthens while the rupiah weakens. The weakening exchange rate will

have a signiicant impact in the form of rising inlaionary

pressure (direct pass-through). The policy transmission mechanism through trade, on the other hand, occurs

once non-convenional policies are relaxed in the form of liquidity facility and iscal ightening that is relected

by higher tax and decline in government spending. This

condiion pushes US economic growth lower whereby US

imports for products from Indonesia and other developing

countries will also decline. This will subsequently afect

2.4

Polarizaion of Global Trade

g

Dynamics Protecionism Policies in

Global Trade

During 2009, number of issues regarding global trade

coninued to increase.A number of iscal simulus

packages as well as monetary policies that were meant

to spur economic growth did not seem enirely capable of reviving global trade to its pre-crisis levels. Tight global liquidity condiion as well as high-risk indicators within the inancial sector further weakened funding sources for global trade. Meanwhile, the fall in the global economy and global demand had a negaive impact on export

growth and businesses’ performance that had already

coninued to worsen. To reduce the impact of this global inancial crisis, as well as to ensure that various domesic producion sectors coninued to operate, many countries ended up implemening protecionism policies on their trade.

Despite the fact that internaional trade cooperaion coninues to grow, its impact on the economic recovery during the crisis remained minimal. At the end of 2009, the phenomenon of Asian economic growth, paricularly that of China’s which coninues to experience high economic growth, had a posiive impact on the growth of intra-regional Chinese trade with Asia. This condiion

reduces Asian economies dependency on the developed

Worsening economic performance led iscal authoriies to undertake various policies that tended to be protecionist.

The declining volume of the global trade as a result of the weakening demand as well as limited access to funding

caused various economic sectors to face diiculies. To ensure that the economy did not deteriorate further,

many naions resorted to protecionism policies. However, negaive seniment towards these protecionist measures coninued to grow too. This is paricularly due to the fact that protecionist policies during the previous

crises were proven worsening global economic and trade

condiions.

There are diferences as to how these protecionist policies are implemented by the developed naions and the developing naions. For developed naions, protecionist policy towards the domesic industrial

sectors are directly implemented through subsidies, bailed

out companies that are deemed to have a signiicant impact on the economy, or indirectly through domesic consumpion simulus for the purchases of domesic products. In the meanime, for developing naions that have limited budget for subsidies, their protecionist policy for domesic industries largely focus on relaxing regulaions, determining tarif for similar imported goods, as well as other indirect policies (Diagram 2.3).

Other forms of protecionism, speciically related to non-tarif protecion, that seemed to be on the rise in 2009 involves protecionist policies on imports in the form of

ani-dumping invesigaion (AD), global safeguards (SG), ani subsidy (CVG), and PRC-speciic safeguard (CSG).38

Based on the data obtained from the WTO, invesigaion of ani-dumping and others had coninued to increase since the global inancial crisis began (Table 2.2). This

policy was not only implemented by the developing

naions but also by the developed naions (Chart 2.3). One form of import restricion that seems to have grown signiicantly in 2009 was Global Safeguards (SG) that are intended to protect local products from substanial losses as a result of imports of similar products. In contrast to the import restricions implemented during normal economic condiions that focus only on certain products/sectors with the aim of maintaining domesic compeiiveness, the import restricions implemented in 2009 covered a much wider span of industrial sectors. In the meanime, countries that were most afected by the import restricions was China, which accounted for 67% of the total 37 import restricion invesigaions conducted in 2009.39

A large number of the global protecionist policies did not have a signiicant impact on the global economy

38 Anidumping invesigaion refers to the invesigaion carried out by a country towards imported goods that are suspected to be subsidized or whose export prices are lower than the normal price within the exporing country (dumping). Countervailing Duies refers to tax that is applied towards goods that are subsidized by the imporing country.

39 The World Bank (2009), “The Patern of Anidumping and Other Types of Coningent Protecion” PREM Notes No.144.

N = 35 N = 12

Developed Countries Developing Countries

Source: Research and Publicaion of World Bank

Subsidies

and the volume of trade up to the end of 2009. As the

deadlines for these protecionist policies approached, their impacts on trade are largely expected to be felt by 2010. In the meanime, concerns stemming from price distorions or ineiciencies as a result of protecionism are expected to be minimal. Aside from its objecives to maintain domesic industrial sectors and the economy as a result of the inancial crisis, protecionist policies are also expected to coninue to be implemented by many countries up unil economic condiions returns to normal. To date, the impact and concerns towards the protecionist policies are expected to be minimal,

given that there are various forms of corridor for world

trade through the World Trade Organizaion (WTO) and the prevalence of free trade forums such as the North America Free Trade Area (NAFTA) and the ASEAN Free Trade Area (AFTA).

g

Internaional Trade Cooperaion

Despite the fact that the WTO comprises most of the

world’s naions, the increasingly complex nature of global trade cooperaion, however, has led to the emergence of an increasing number of other alternaive forms of trade cooperaion. To coninuously boosing economic growth through export growth, various countries iniiated eforts aimed at cooperaion that are largely limited to

Regional Trade Agreements (RTAs) as well as Free Trade

Agreements (FTAs) that coninuously increase every year

(Chart 2.4).

RTA and FTA are expected to have a posiive impact on domesic economy. The beneits of an RTA and FTA for a country largely deals with the eliminaion of trade barriers, reducion of prices for imported goods (eliminaion of tarifs), increasing volume of trade, as well as improving eiciency throughout the producion process so as to enhance its compeiiveness. In the meanime, the indirect impact includes, among others, the reducion/ eliminaion of various tarifs that enhances and eicient global trade.

Apart from the numerous types and coverage of trade

cooperaion, the reducion in tarif and other import costs

that reduces prices for imported goods/products serves

as another form of economic simulus. In the meanime, other forms of cooperaion carried out between naions through various forums enhanced compeiiveness as well transferred technology at a much faster pace.

Chart 2.3 Number of Invesigaion Iniiated by Developing

Countries vs by Developed Countries

Table 2.2 Invesigaion of Non-Tarif Policy

Source: Global Anidumping Database

Chart 2.4 Regional Trade Agreement, 2001-2009

number of invesigaion

Source: Global Anidumping Database

Iniiated by Developing Countries Iniiated by Developed Countries

FTA & RTA

However, cooperaion among countries that have diferent economic scale, such as those between an industrial naion and a developing naion, can lead to disparity in terms of the beneits enjoyed from such a venture. Export-oriented developing naions that generally export raw materials/commodiies will tend to reap beneits that are by far lower than beneits obtained by countries exporing processed goods. Cost of input factors such as labor and producion equipments can cause developing naions to import at a higher value. At the same ime, cooperaion in the form of an RTA and FTA can also result in trade diversions as well as a reducion in terms of trade.

On the other hand, certain concessions made on rules

of origin (ROO) within the context of trade cooperaion

can create problems. ROO is implemented through three methods, which are: change of tarif heading, value-added criteria, and speciic manufacturing process requirement.

In the midst of the global producion interlink

phenomenon, the ROO qualiicaion, as well as diferent

criteria among trading blocs, can be disadvantageous for a country that is grouped within various trading blocs or

groupings. Moreover, this can hamper the trade low due to the presence of ROO procedures that are deemed ime-consuming and costly.

The recent crisis will certainly afect the implementaion of various plans towards internaional cooperaion. The presence of protecionist policies implemented by various countries to protect their economies is expected to afect the implementaion of various forms of trade cooperaion. In addiion, as a result of weakening global demand that resulted in declining exports and imports, various regulaions on sectors that are considered less compeiive will likely coninue.

g

China’s Role in Asian Trade

In contrast to other Asian countries, apart from its

dominant posiion as one of the countries with the largest share of the world’s GDP, China’s sizeable populaion also serves as a potenial export market for global trade. This development provides the expectaion that Asia’s economic prospects will likely coninue to grow with China as the main driver through intra-regional trade (Chart 2.5). In spite of the decline experienced in the previous year,

China’s volume of trade with Asia in 2009 grew and in

fact enjoyed substanial growth compared to the previous years. The posiive growth in trade between China and

Asia was also supported by the dominant share of other

Asian countries volume of trade (both exports as well as imports) with China (Chart 2.6 and 2.7). The coninued

growth and stability in the volume of trade with China Chart 2.5 Growth of China Export and Import

Aciviies with Asia

Chart 2.7 Import of China by Origin Chart 2.6 Export of China by Desinaion

billions of USD billions of USD

Source: CEIC (processed)

Imports Exports (Rhs)

Source: CEIC (processed) percent

Oceania North America Lain America Europe Africa Asia

Source: CEIC (processed) percent

in recent years indicates a more important role of other

Asian naions in China’s trade and economy.

China will likely play a more important role as a growth

catalyst for other Asian naions if China does not only serve as a producion or assembler of raw or semi-inished goods that are exported by Asian naions but it also serves as an importer of inished goods from other Asian countries. As shown by the structure of its commodiies, share of Asian exports for semi-inished goods to China since 2001 have coninued to decline, while share of Asia’s exports for inal products to China have increased (Chart 2.8).

Looking forward, changes in trading patern (exports and imports) between China and the Asian region indicates China’s substanial potenial to support intra-regional economy and trade. However, China’s high investment

and economic growth also poses a challenge for other

Asian naions in which China’s potenial as a major compeitor for exports of other Asian countries.

g

ASEAN-China Free Trade Agreement

(ACFTA)

In line with the increasing role of Chinese economy in the

global economy, trade between China and ASEAN naions also coninues to grow. The volume of trade between China and ASEAN in 2000 was only USD 39.2 billion, and grew signiicantly to USD 212.7 billion in 2009 (Chart 2.9 & 2.10). The coninued rise of China’s role as ASEAN’s trading

partner along with its sizeable market share that China

stands to gain with its large populaion, has pushed for the need for a more intensive cooperaion between China and ASEAN. Despite the fact that it has been proposed since 2001, the ASEAN - China Trade Agreement, which is also referred to as ACFTA, was only launched in 2004. Through

this agreement, Indonesia agreed to eliminate + 8,000 Chart 2.8 China Export and Import Aciviies with the Neighboring Countries

Source: CEIC (processed) year

Export Import

Source: CEIC (processed) biliions of USD

Trade Volume

Source: ASIAN Development Outlook 2009

Final Goods Raw Materials

Construcions material

Components

percent

Export

Source: ASIAN Development Outlook 2009

Final Goods Raw Materials

Construcions material

Components

percent

Import

import tarif posts (represening most of the tarif posts) from China that are classiied within the normal track goods by 2010. In the meanime, for the other ASEAN naions, this policy will be implemented by 2015.

From economic point of view, free trade cooperaion between ASEAN with China is the largest free trade cooperaion that covers consumers amouning to (populaion) 1.7 billion people. Through this cooperaion, ASEAN-China’s economy and volume of trade will likely coninue to grow. ASEAN can import raw materials from China at much lower prices while, at the same ime, expand its reach of the global markets through China given that China currently has 14 FTA with other countries around the world. In addiion, the Agreement reached on investment is expected to result in increasing Chinese investment in ASEAN, including Indonesia. China’s

investment has the potenial to provide substanial beneits for ASEAN. China’s direct investment ouflow in 2008 amounted to USD 53 billion, of which only 0.26% was received by Indonesia. As a result, Indonesia must coninuously strive to provide required regional

infrastructure needed to support the entry of such

2.5

Balancing Economic Growth

in the Midst of Global Imbalance

One of the challenges facing global economy is rebalancing global economic growth. On the one hand, the US and

other industrial naions coninue to record high domesic demand and low savings rate while the role of domesic

demand in a number of emerging markets needs to be improved and their dependence on exports needs to be reduced. Despite the fact that the issue of rebalancing the global economy has become increasingly apparent since the recent crisis began, the issue of rebalancing the global economy is related to the phenomenon of global imbalance that has appeared since the 1990’s. Therefore, the reducing global imbalance cannot be apart from the process of global economic recovery.

g

The Global Imbalance Phenomenon

The global inancial crisis in 2007/2008 has proven to be

unable to end global imbalance. Despite the fact that this imbalance has somewhat receded as a result of the global crisis, global imbalance has, however, persisted up to the

end of 2009 (Chart 2.11). Various policies that efecively addresses the various distorions, either domesic or

foreign, that causes this global imbalance needs to be applied. Failure to formulate and implement policies to address global imbalance can threaten the current global economic recovery.

The current account data shown in Table 2.3 indicate that the characterisics of this global economic imbalance have

somewhat changed since 1996. Japan’s surplus, which

this period, the existence of a global imbalance was also

caused by the appreciaion in the US dollar. The high level of producivity enjoyed by the US in comparison to the producivity rate of other countries played a part in the US dollar’s appreciaion and rising deicit of the US current account, especially during the period of 1996-2000. At the same ime, paricularly ater the Asian crisis, investment to developing Asian countries sufered a drasic decline.

During the periods of 2001-2004, the US current account deicit on average grew by 1.4% of GDP. This increase

was mainly caused by the decline in the level of savings in

the US as relected in the deterioraion of household and

government savings throughout this period. The decline in the level of household savings was mainly caused by

the increase in household loans as a result of the inlated

prices for housing and other assets. On the other hand,

current account surplus occurred in many Asian naions throughout this period, while oil-exporing countries also

experienced an increase in surplus as a result of the oil price increase.

During 2005-2008 periods, China’s current account surplus increased dramaically. Its foreign exchange reserves also increased dramaically throughout the 2005-2008, recorded an increase of over US$1.5 trillion. In spite of the growth in investment enjoyed by China and oil exporing countries throughout the 2005-2008 periods,

the level of savings growth far surpasses growth in investment.

In inancial markets, inancial excesses characterized

the years leading up to the global economic crisis. This

is relected in inlated asset prices as well as in the low

level of saving and high investment in countries that

experienced deicit, not only in the US but also in a number

of European countries such as Ireland, Spain, the UK, and

other Central and Eastern European countries (CEE). On

Chart 2.11 Global Imbalance

Developing Asia Advanced ex United States Advanced economies

Source: WEO, October 2009 (IMF) billions of USD

Tabel 2.3 Average Current Account Balances (in percent of world GDP)

Source: Blanchard & Milessi-Ferrei (2009)

1) EUR deicit: Greece, Ireland, Italy, Portugal, Spain, United Kingdom, Bulgaria, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovak Republic, Turkey, Ukraine. 2) Emerging Asia: Hong

Kong S.A.R. of China, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan province of China,

Thailand. 3) Oil exporters: Algeria, Angola, Azerbaijan, Bahrain, Republic of Congo, Ecuador, Equatorial Guinea, Gabon, Iran, Kazakhstan, Kuwait, Libya, Nigeria, Norway, Oman, Qatar, Russia, Saudi Arabia, Sudan, Syria, Trinidad and Tobago, United Arab Emirates, Venezuela, Yemen. 4) Core Europe : Austria, Belgium, Denmark, Finland, Germany, Luxembourg, Netherlands, Sweden, Switzerland.

1996-2000 2001-2004 2005-2008 2009

United States -0.8 -1.4 -1.4 -0.6

Deicit Europe1) -0.1 -0.4 -0.8 -0.5

Rest of the world -0.3 0 -0.3 -0.4

China 0.1 0.1 0.6 0.6

Emerging Asia2) 0.1 0.2 0.2 0.3

Japan 0.3 0.3 0.3 0.2

Oil Exporters3) 0.2 0.4 1 0.3

Core Europe4) 0.2 0.4 0.7 0.4

the other hand, surplus in China, a number of European

naions, as well as the oil exporing countries coninued to grow. In the meanime, foreign investor appeite towards US debt instruments also coninued to increase.

Conceptually, imbalances do not always have to be a problem for the economy.40 Imbalance is not a problem if

it is a natural relecion of the diferences in the level of development, demographic proile, and other economic fundamentals. Countries with populaion that is aging

at a much faster pace than their trading partners tend

to have substanially higher savings and current account surplus. Similarly, countries that provide atracive investment opportuniies for foreign investors can fund

their investments by using foreign savings.

In contrast, imbalances can be a problem if it is a

relecion of the distorion, externality, or risk, either at local or foreign level. In the meanime, the low level of saving can be a result of inlated asset prices, or expectaions that exceed actual economic growth. In addiion, imbalances can also occur as a result of very

low investment due to the lack or absence of trade or

copywrite protecion or lack of compeiion within the inancial system.

Meanwhile, paricularly ater the Asian crisis in 1997/1998, many emerging markets have accumulated substanial foreign exchange reserves. One of the main objecives for emerging markets to hold substanial

amount of foreign exchange reserves is as self-insurance

against a currency crisis. In addiion, many countries also

accumulated foreign exchange reserves as part of their strategy to spur growth in an export-oriented economy. Most of the world’s central bank reserves are currently

denominated in US dollars, which is relecive of the

trust placed by many foreign investors towards the US

dollar and the US dollar’s dominance of internaional transacions.

g

The Global Financial Crisis and Global

Economic Imbalance

One of the major issues facing global economy prior to the global inancial crisis in 2007/2008 is global imbalance. The main concern at that ime was a drasic stop in capital

40 Blanchard, Olivier and Gian Maria Milesi-Ferrei (2009), “Global Imbalances: In Midstream?” IMF Staf Posiion Note, SPN/09/29.

inlows to the US that may result in a recession that does not merely afect the US economy but also the world economy. The recent global inancial crisis was not caused by the adjustments made to overcome global imbalances, as many concerned prior to the crisis. The global inancial

crisis was largely driven by the failure of the global

inancial system. Foreign investors that placed their funds

in US assets that turned out to be toxic assets played a

role in funding the US deicit.

Even as global imbalance itself is not the cause of the global crisis, many economists believe that this global

inancial crisis was also due to the global imbalances

that occurred since the second half of the 1990’s. Some

believe that the high savings rate enjoyed by China and the oil exporing countries caused low interest

rates, which in turn led investors to invest in high-yield

investments despite the relaively high risks involved with

such investments. In contrast, there are some who believe

that a strong associaion between the global inancial

crisis and global imbalance was due to America’s ability to fund its economic imbalance with overseas capital that it easily obtains.41 In terms of external US funding, foreign purchases of US debt instruments—such as Treasury

securiies and corporate bonds—played a signiicant role

in the imbalance.

Overall, the associaion between the global inancial crisis and global imbalances is evident with the reducion

in global imbalances that occurred as a result of the receding pressure brought about by the global economic

crisis in 2009. A number of factors can explain this

phenomenon.42 Firstly, oil prices that fell from its average

levels in 2008 has caused substanial depreciaion in current account surplus of oil-exporing countries as well as improved the current account of oil-imporing

countries. Secondly, the fall in asset prices resulted in

the fall in domesic demand, which in turn reduced the current account deicit of countries that were sufering from the efects of the crisis (Chart 2.12). Thirdly, the global inancial crisis was perceived to have led investor seniment towards home-biased investments. This implies that foreign inancing towards external imbalances has receded. Fourthly, the global inancial crisis had a signiicant impact towards demands for imported durable

41 Obsfeld, Maurice and Kenneth Rogof (2009), “Global Imbalances and the Financial Crisis: Products of Common Causes”, Mimeo. 42 Obsfeld, Maurice and Kenneth Rogof (2009), “Global Imbalances

consumer goods and investment products. This caused a

fall in the current account surplus of exporing countries for such goods and reduces the current account deicit of countries with substanial current account deicits, such as

those of the US.

Going forward, global imbalances will largely be

determined by developments of the above-menioned

factors. The IMF’s recent reports indicated the reasons as to why global imbalances will likely decline in future.43 Firstly, asset prices and value of household wealth is

not expected to return to its pre-crisis levels any ime

43 Blanchard, Olivier and Gian Maria Milesi-Ferrei (2009), “Global Imbalances: In Midstream?” IMF Staf Posiion Note, SPN/09/29.

soon. This will result in a higher level of private sector savings compared to the level during pre-crisis period. Global imbalance is expected to decline in the event that

the saving levels in the US increases relaive to those of other countries, given the fact that the relaively low

level of saving in the US was a factor behind the global imbalance.

Secondly, ightening inancial system regulaions will

increase intermediary and capital expenses. Therefore,

investments in the housing sector—paricularly in

countries that experienced a housing boom prior to

the crisis—will likely coninue to be low. This will likely reduce the current account deicit in countries that have substanial deicit, which in turn reduces

global imbalances. Thirdly, the rise in risk premiums on

internaional capital lows will result in higher capital expenses. This is expected to limit the sources of inancing for substanial current account deicit, which in turn

reduces global imbalances.

Apart from the factors that support the existence of

a reducion of global imbalances, as described above,

there are also a number of challenges that remains. In spite of the increase in private sector savings in the US,

the US iscal deicit, on the other hand, coninues to grow signiicantly. In addiion, even as China’s current account deicit has undergone adjustments in 2009, this adjustment could be temporarily. Meanwhile, a number of emerging markets coninue to record current account

surpluses and higher foreign exchange reserves. Chart 2.12 Nominal Asset Price in USA

index percent, yoy

Source: Bloomberg

2.6

Conclusion

Various policies and exit strategies implemented by developed and developing countries have impacts on Indonesian economy, as an open economy. The success

of the policies and exit strategy of the developed naions will afect condiion of the global economic recovery process, which in turn will inluence Indonesia’s economic condiion. Meanwhile, various eforts towards global and regional cooperaion as well as various global economic challenges—such as protecionism and global imbalances—cannot be averted and will afect sustainability of the Indonesia’s economic recovery

process.

The mechanism by which developed countries paricularly the US, transmited exit strategy into Indonesia’s economy

is expected to occur through two main channels, that

is, trade and capital low. Through capital lows, the exit strategy that is relected by policies towards rising interest rates in the US will result in a capital ouflow from

emerging markets, including Indonesia, to the US. As a result, the US dollar is expected to strengthen, while the rupiah will weaken. The weakening of rupiah may result

in higher inlaionary pressures (direct pass-through). The

transmission through trade occurs as a result of ending

non-convenional policies such as liquidity facility and iscal ightening that is relected in increased taxaion and reducion in government spending. This condiion can lead to declining US economic growth, and consequently to a

decline in the US imports for Indonesian products. This,

in turn, will afect Indonesia’s balance of payments and

Apart from policies and the exit strategy adopted by the

developed countries, Indonesia’s economic recovery in the years to come is also afected by the implementaion of various global and regional cooperaions. The recent global inancial crisis shows the need for Indonesia to have a solid and eicient inancial system that can withstand

external and internal pressures, as well as supports

real sector aciviies and sustainable naional economic growth. Since inancial crisis can occur at any ime and

from any place, Indonesia needs to have a framework for

anicipaing the impact of the crisis.

On one hand, as a member of the G-20, Indonesia’s posiion in formulaing global measures and policies

needed to intensify and maintain global economic

and inancial stability has strengthened. On the other hand, Indonesia’s obligaions on various internaional regulaions have intensiied. In this regard, the challenges faced include synchronizaion of domesic regulaions and standards with internaional regulaions and standards. In addiion, as the only ASEAN countries that is a member of the G-20, Indonesia must also serve the interests of other ASEAN countries.

Coordinated policies to maintain macroeconomic stability and maintain the momentum of economic growth

will bring Indonesia’s economy to be in line with the commitments made within the G-20 forum concerning

the global framework for achieving solid, sustainable, and balanced economic growth. In this regard, the implemented policies should always be in line with the

exising condiions within the respecive countries.

In response to the crisis, there is a tendency towards

increased protecionism, which of course can afect Indonesia’s trade. Protecionist policies implemented by

a number of countries intended to protect their economy

are expected to impact the implementaion of various free trade cooperaion iniiaives. In addiion to the

decline in global demand that is expected to result in a corresponding decline in exports and imports, various

regulaions on sectors that are less compeiive will likely to coninue.

On the other hand, in line with the improved global

economic and trade condiion, the growing number of internaional cooperaion is expected to have a posiive

impact. In addiion to the various forms and scope of

cooperaion, reducion in tarif and other expense will be beneicial in supporing a more eicient economy. Meanwhile, various forms of cooperaion made with other naions, either bilaterally or on a regional basis, even through diferent forums, are expected to enhance compeiiveness as well as promote technology transfer.

A concern shared by many developing naions prior to the global crisis is the possibility of a relaively sharp depreciaion of the US Dollar due to rough adjustments of global imbalances. If such depreciaion occurs then exports to developed naions, paricularly to the US,

is predicted to fall. In fact, what had been predicted

before the crisis did not occur, at least up unil the end of 2009. However, it does not mean that the challenges from a rough global imbalances adjustment have

been disappeared. The progress made to address the

global imbalances in the years to come coninues to

Box 2.1

: The Role of Bailout within the Global Economic Recovery Process

The process of global economic recovery that is currently felt is largely a result of policies implemented by various

naions in response to the pressures on the world’s inancial stability. These policies were generally aimed at minimizing the impact of the inancial market’s instability as well as to maintain macroeconomic stability. One of

the implemented major policies was providing bailout

funds to the banking system through a recapitalizaion process. There were many countries, including the United States (US) and UK, which implemented bailout programs (Table 1). In banking, bailout refers to inancial

support that is extended by a government or central

bank to banks or saving-loan insituions that are at the brink of bankruptcy, insolvency, or liquidaion as a result of : (i) substanial amount of problem loans; (ii) deterioraing situaion as a result of the inancial

market’s instability; and (iii) drasic and sizeable funds ouflow resuling in panic among depositors. These bailouts are provided to systemaically and rapidly avert a contagion efect across banks within the banking industry, which potenially can give a disastrous impact on the economy.

The bailout program for problem banks is not a new concept. The US extended its irst bailout in 1792, as a result of eforts by a businessman and speculator named William Duer to force the Bank of New York (BONY)

share prices to drop with the aim of obtaining ownership

of the Bank at its lowest price which turned out to be failed. Duer speculated with funds borrowed from banks and in turn used these funds to buy government bonds.

Table 1. Bailout Program during Global Financial Crisis 2008 - 2009*

No Year Countries

Number of Banks in Bailout Program

Bailout amount for banking sector (billion

USD)

Financial System Rescue

Plan (billion USD) Bailout return value

GDP Growth during Bailout

program (%)

1 2008 USA 212**) 177 700 USD 165 billion 0.4

2 2009 USA 479**) 27.6 -2.4

3 2008 South Korea 3 40.9 130 - 2.2

4 2008 Switzerland 1 54 60 - 1.6

5 2008 France 6 82 492 - 0.4

6 2008 United Arab Emirates - 36.7 52,6 - 7.4

7 2008 Netherland 1 13 13

5 billion Euro + 606 million Euro as

interest (2010)

2.1

8 2008 Russia 50 11.2 200 - 7.3

9 2008 Germany 2 138 640 - 1.3

10 2008 UK 3 64 691 - 0.7

11 2008 Ireland 3 6.12 544 - -2.3

12 2008 Norway 3 55 57 - 2.0

Source: from many sources

**) U.S Treasury Department has invested about USD 200 billion to hundred of banks through capital purchase program as an efort to increase bank’s capital and support intermediaion program (new lending)