JURUSAN AKUNTANSI

Fakultas Ekonomi Universitas Malikussaleh

Jurnal

Akuntansi

dan Keuangan

1

The Relation of Corporate Governance to Firm Performance and Management Compensation as Mediating VariableEndang Surasetyo Ningsih, Wida Fadhlia dan Rahmawaty

11

Akuntabilitas sebagai Alat Pengukuran Kinerja Pemerintah Daerah Yusri Hazmi, Faisal dan Zuarni17

Keputusan Perusahaan Melakukan Share Repurchase:Free Cash Flow Hypothesis ataukah Signaling Theory

Eddy Suranta, Pratana Puspa Midiastuty dan R. Ryan Mulya Wijaya

31

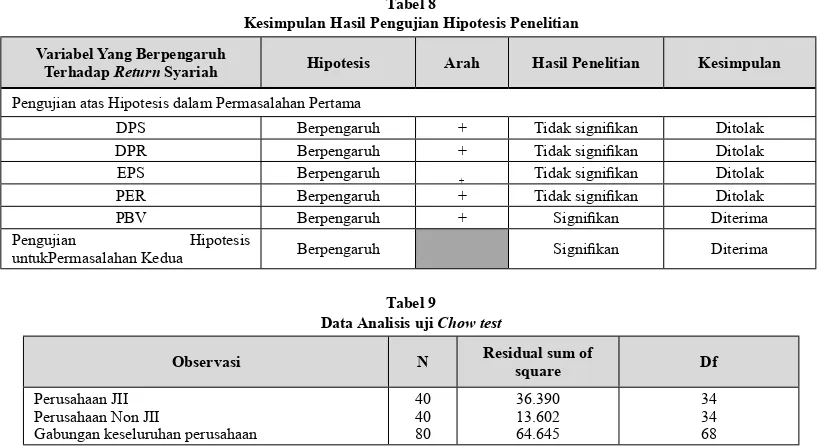

Pengaruh Rasio Analisis Fundamental Terhadap Return Saham:Perbedaan Pengaruh Antara Saham Syariah dan Non Syariah Dedy Oktri Hadi Saputra dan Rini Indriani

49

Pengaruh Kualitas Pelayanan Terhadap Kepuasan Pasien dan Dampaknyapada Proitabilitas (Pemulihan Pembiayaan) Rumah Sakit di Kota Bengkulu Silke Wulandari dan Fachruzzaman

69

Analisis Potensi Keuangan Daerah Pemerintah Kota Lhokseumawe dalam Pelaksanaan Otonomi dan Desentralisasi DaerahM. Haykal

89

Pengaruh Kepemilikan Manajerial, Komite Audit, Leverage, dan Umur Perusahaan Terhadap Pengungkapan Modal Intelektual Syawal HariantoJurnal

Akuntansi

HALAMAN 1 – 101

Terbit 2 kali dalam setahun pada setiap bulan Februari dan Agustus, berisi tulisan yang di-angkat dari hasil-hasil penelitian maupun pemikiran bidang akuntansi dan atau keuangan yang relevan bagi pengembangan profesi dan praktek akuntansi di Indonesia

EDITORS

M. Haykal (Chief of Editor) Hilmi (Managing Editor) Muammar Khaddai, Amru Usman

Hendra Raza, Mursyidah Rita Mutia, Naz’aina

Iswadi, Yurina

REVIEWERS

Ade Fatma Lubis Adi Zakaria Afif Universitas Sumatera Utara Universitas Indonesia

Erlina Fachruzzaman

Universitas Sumatera Utara Universitas Bengkulu

Julli Mursyida Islahuddin

Universitas Malikussaleh Universitas Syiah Kuala

Kamil Md. Idris Murhaban

School of Accountancy UUM-Malaysia Universitas Malikussaleh

Rini Indriani Syukri Abdullah

Universitas Bengkulu Universitas Syiah Kuala

TB. Ismail Wahyuddin

Universitas Tirtayasa Universitas Malikussaleh

Zaafri Husodo Universitas Indonesia

EDITORIAL SECRETARY Rayyan Firdaus Harry Hassan Masyarafah

Kusnandar Zainuddin

EDITORIAL OFFICE

Gedung Jurusan Akuntansi FE-Unimal Kampus Bukit Indah, Lhokseumawe

Telp/Fax. 0645-40210/0645-40211 Email: [email protected]

JURNAL AKUNTANSI DAN KEUANGAN diterbitkan sejak Februari 2011 Oleh Jurusan Akuntansi FE-Unimal

Redaksi menerima sumbangan tulisan yang belum pernah diterbitkan dalam media lain. Naskah diketik rapi sesuai kebijakan editorial (lihat dihalaman belakang jurnal)

The Relation of Corporate Governance to Firm Performance and 1-10 Management Compensation as Mediating Variable

Endang Surasetyo Ningsih, Wida Fadhlia dan Rahmawaty

Akuntabilitas sebagai Alat Pengukuran Kinerja Pemerintah Daerah 11-16 Yusri Hazmi, Faisal dan Zuarni

Keputusan Perusahaan Melakukan Share Repurchase: 17-29

Free Cash Flow Hypothesis ataukah Signaling Theory

Eddy Suranta, Pratana Puspa Midiastuty dan R. Ryan Mulya Wijaya

Pengaruh Rasio Analisis Fundamental Terhadap Return Saham: 31-47

Perbedaan Pengaruh Antara Saham Syariah dan Non Syariah Dedy Oktri Hadi Saputra dan Rini Indriani

Pengaruh Kualitas Pelayanan Terhadap Kepuasan Pasien dan Dampaknya 49-68

pada Proitabilitas (Pemulihan Pembiayaan) Rumah Sakit di Kota Bengkulu Silke Wulandari dan Fachruzzaman

Analisis Potensi Keuangan Daerah Pemerintah Kota Lhokseumawe 69-88 dalam Pelaksanaan Otonomi dan Desentralisasi Daerah

M. Haykal

Pengaruh Kepemilikan Manajerial, Komite Audit, Leverage, dan 89-101 Umur Perusahaan Terhadap Pengungkapan Modal Intelektual

THE RELATION OF CORPORATE GOVERNANCE

TO FIRM PERFORMANCE AND MANAGEMENT

COMPENSATION AS MEDIATING VARIABLE

eNdANg surAsetyo NiNgsih1, WidA FAdhliA1 dAN rAhmAWAty1

1Dosen Pada Fakultas Ekonomi Universitas Syiah Kuala

The objective of this research is to investigate inluence of corporate governance to management compensation and subsequent irm performance. This study uses data from manufacture companies that listed in Jakarta Stock Exchange for the inancial reporting in 2003 – 2005 periods. The sample consists of 198 observations over a three-year period for 66 publicly traded irms. The mechanism of corporate governance is to be proxy by managerial ownership and number of commissioner proportion board. Management compensation is measured using sum of remuneration that reported in audited inancial reporting. Firm performance is to be proxy by return on assets (ROA) and return on equity (ROE) after compensation is awarded. The result was showed that managerial ownership and number of commissioner proportion board giving signiicant positive impact to management compensation. Even though, managerial ownership as one of mechanism of corporate governance has negative coeficient to management compensation. This study was ind that corporate governance and management compensation was not impact to subsequent irm performance. This result was indicated that compensation did not designed optimally and corporate governance did not work effectively.

Keywords: corporate governance, management compensation, subsequent irm performance

BACKGROUND

the indonesian for Corporate governance

(IICG) together with SWA Magazine were leading a rate survey to companies applying good corporate governance (GCG) for corporate governance perception index 2005 (CGPI). Good corporate governance (GCG) application success in a company could not be separated from the stakeholders’ role, especially the primary ones such as the employees and managers. The stakeholders were motivated to work actively and cooperate with the company to increase the performance, job opportunity and the company continually. This closely related to the employees

and managers and might created balanced value

between the company owner and the stakeholders. The company would professionally give some

kinds of compensation based on their performance

and integrity. The torch participant number in the last 5 active years would create a question; if the good corporate governance (GCG) application in the company value creation had no relation with

optimal compensation value?

Indonesian monetary crisis directly affected in conviction and inancial crisis in trading world. The inancial crisis was once caused by the less transparency and accountability, and this made the information manipulation possibly done by a company. Later, this created a good arrangement concept known as good corporate governance (GCG) mechanism. The important matter often become a debate in corporate governance was the chosen compensation contract. The main point of the debate was the existence and function of the remuneration committee. According to

the corporate governance and corporate ethics

published by the BUMN State Ministry ofice in 1999, a duty of the remuneration committee function was to examine and recommend the remuneration system changes of the management, commissaries, and employees in order to show the relationship between the irm performance

target achievement and accepted compensation

whether the decision to apply the corporate governance and optimal compensation were not closely related to the company occupation in the following year?

Eisenhardt (1989) stated three assumptions related to the agency theory as the based theory in the owner and management contract. They were: (1) human nature behavior generally

put personal importance above the others’

(self interest); (2) man basically had limited imagination to the future perception (bounded rationality) and (3) man always avoided the risk over him though there were others to sacriice (risk averse). Gibbon and Murphy (1992) showed that the optimal compensation contract was an incentive combination implicitly related to the compensation contract which was capable to motivate and give direction to the company manager to a maximal company occupation.

Some people realized the importance of the

application of the good corporate governance

(GCG) principal convinced to be able to create conducive condition and irm base to perform the company operational right, eficient, and proitable; to increase and create balanced value between the shareholders and stakeholders. This study was attractive because of several reasons.

First, indonesian economic condition disturbed

by a multidimensional crisis, made the good

governance reading more become a benchmark

in recovered and stability in the economic condition especially in corporation management. Second, the good corporate governance (GCG) pressuring was more aimed to protect the minority stockholders’ right and importance. In

the other side, the good corporate governance

(GCG) application success could not be separated from all company stakeholders’ role, so that the compensation to the achievement was needed to increase the conviction and also the company value and a value creation to the shareholders. Third, this study was a reaction to the surveyed year by year member decrease phenomenon.

The research was aimed to investigate if there was a positive relationship in the good corporate governance (GCG) application to the management compensation. More over, this research wanted to investigate if there were a relationship between

the good corporate governance (GCG) application

and the management compensation to the next

company occupation.

OVERVIEw OF THEORETICAL

Agency relationship perspective was a base used to view corporate governance. The main point of the agency relationship was the existence of the separation between the owned (in principal / investor side) and control (in agent / manager side). Investor had their expectation to earn return from their invested money. Therefore, a good contract between the investor and the management was a contract which was able to explain detail speciications should be performed by the manager in managing the investor’s fund, and speciication related to the return distribution between the manager and the investor. Agency relationship was a contract between the principal and agent developed by Jensen and Meckling (1976); and Fama and Jensen (1983).

Agency relationship was emphasized to overcome two main problems occasionally appear in the agency relationship. According to Eisenhardt (1989), the irst problem was a problem appeared when: (a) the desire and purpose of the principal and agent were opposite and (b) it was a hard or expensive to the principal to verify the agent real tasks. The problem appears when the principal could not verify the agent real tasks precisely. The second problem was the risk sharing problem appeared when the principal and agent had different action preference caused by their different preference toward the risks.

Shleiver and Vishny (1997) stated that the

corporate governance concept based on the

agency theory was expected to be functioned as the tools to solve all agency problems and also give the conviction to the investor that they would gain the appropriate return of the fund invested.

resource management strategy to create a job harmonious which had different importance for different person. Some took compensation as a return from the service given by the human resources gained as an organization, or a value addicted by the company to the human resource competence and ability, or, an appreciation given by the company to dedicated person (Simamora, 1995).

Jensen and Meckling (1976) stated that compensation was a service value given by the owner to the management. Compensation contract showed the service response value given by the principal to the management. Formally, the compensation contract was a bundle between the

manager and principal to perform some activities

in the name of the principal, aimed to maximally the company value in order to increase the shareholders prosperity at the end. Therefore, the management compensation contract was designed to motivate the management to fulill the job occupation determined previously by the principal.

Among the mentioned factor to motivate the

creation of the effective company management creation, the commissaries council (management structure) was a main factor affected the manager behavior in the company management. In a modern corporation, compensation policy was delegated to the commissaries council. When the compensation designed optimally, the

compensation contract could be a motivation

tools to maximally all stakeholders’ prosperity. Jensen (1993) stated that several problems appeared in the internal mechanism system (management structure) was started with the

existence of the commissaries council possessing

inal responsibility in the company. The commissaries council possessed the authority

to make rules to the manager in managing

the company, employing, iring, and creating compensation policy and also giving some strategic advices. More number of commissaries would increase the service and control function because there were more skilful persons and more valuable advices in the company strategy and management. According to Kusumawati and Riyanto (2005), the relationship between the

number of commissaries council member and

the company value were supported by control and service function perspective given by the commissaries council. Consultation and advice given were valuable services to the management never been given by the market. Their research also found that the investor’s will to give more premiums was supported by the service and control given by the commissaries.

Several researches showed that the council structure would be able to explain cross-sectional variation in management compensation. hallock (1997) in his research on 500 companies in 1992 discovered that the council with interlocking

relationship and council measurement had an

effect to the higher management compensation. Core, holthausen and Larcker (1999) observed

the compensation rate to 205 companies and discovered that the council composition variable

(council head variable was CEO, council number, council came from the internal company, council came from the external company, council with interlock relationship, council member with age above 69, and busy council) had positive and signiicant relationship to the company compensation level.

Cyert, Kang, and Kumar (2002) in their

research about compensation determinant in

public companies in the beginning of 1990, stated

that Ceo or also the head of the council, and the number of the council, had positive relationship

to the compensation. Grinstein and hribar (2004) stated that CEO would affect the new council member election process, CEO was also the head

of the council and the number of the council

would signiicantly affect the compensation. Chhaochharia and Grinstein (2006) in their

observation result found that the council structure

was a signiicant determinant to the measure and structure of the CEO compensation.

h1: there was a positive relationship between the

number of the commissaries and management

compensation.

that the company with more dispersed ownership gave more payment to the management compared to the company with concentrated ownership. In this type of company ownership we could ind two categories of stockholders named controlling interest and minority interest (shareholders). (3) BUMN ownership.

Core, haolthausen and Larcker (1999) in their research found that management ownership

structure had a substantive cross-sectional

relationship to the management compensation. Empiric research led by Xu and Wang (1999) in hastuti (2005) explained more the research result as followed: (1) There was signiicantly a positive relationship between the concentrated ownership and productivity as a proxy of the company occupation. (2) The concentrated ownership affection was stronger for companies dominated by legal person shareholders compared to those dominated by company. (3) The company proitability positively related to the stock ownership proxy by a legal person but negatively related to the stock ownership by the company. (4) Employee productivity tended to decrease when the stock ownership proportion by the company was increased. Stock ownership by legal person shareholders could monitor the management effectively through the supervision of the board of directors, the company employee election and the compensation award to the chief corporate oficer.

h2: there was a positive relationship between the ownership structure and management compensation.

The distinction deinition of good corporate governance (GCG) did not affect the distinction of meaning and purpose. Forum for corporate governance in Indonesia (2001) used the deinition of Cadbury Committees named: a set of rules

arrange the relationship among the stockholders,

company management (manager), creditor, government, employee, and other internal and

external interest holder related to their rights and

also responsibilities. In the other word, a system arranged and controlled the company. More details, the good corporate governance (GCG) terminology could be used in order to explain

the role and behavior of the direction council,

commissaries council, the company manager and the stockholders.

Empirically, result of the observation of corporate governance applied in a company related to the company occupation was remained inconsistent. Several others researches showed that there were no relationship between the corporate governance and the company occupation, such as daily and friends (1998) and CBI survey result, deloitte and Touche (1996), as copied in darmawati, Khomsiyah and Rahayu research (2004).

McKinsey research, as copied by Lukuhay (2002) and Raick (2002), had proved that investor in the advanced countries willing to give a quite high premium, nearly take the average of 28% to the company consistently applying the corporate governance principal. As an addition,

evidences proved that the stocks of the companies

enjoyed the market valuation among 10% to 12% were founded. Gompers and friends (2003) in

their observation found a positive relationship

between the corporate governance index and long-term company occupation. darmawati and friends (2004) in their analysis showed that corporate governance would statistically and signiicantly affect the return on equity. This proved the hypothesis that corporate governance would affect the company internal occupation.

Klapper and Love (2002) founded the positive relationship between the corporate governance and company occupation measured using the return in assets (ROA) and Tobin’s Q. Other

important result gained from their observation

was that the corporate governance application in the company level had more importance in the

development countries that those in the advanced

countries.

ownership with accounting proit level for 511 largest companies in United States.

holderness and Sheehan (1988) analyzed 144 listed companies in NySE with stocks ownership more than 50,1% and found that Tobin’s Q result was higher when the company was owned by majority stockholders. Tobin’s Q was signiicantly lower for companies with individual majority stockholders. McConnell and Servaes (1990) took samples of more that 1000 companies discovered that Tobin’s Q positively related to the stocks ownership proxy by individual investor.

the commissaries council service and control function as corporate governance mechanism could be seen as a signal to the investor that the

company had managed as its required (positive signal). Investors were expected to accept this signal and willingly paid higher premium for well-governed companies in Indonesia. Thus, the good corporate governance (GCG) application would relate positively with the company occupation in the investors’ view (Labelle, 2002 in Kusumawati and Riyanto, 2005).

Executive manager skills and ability were closely related to the inancial performance in an organization. Therefore, a good understanding was needed between the executive compensation level and monetary success measurement. The stockholders used the company compensation

scheme as a tool to monitor and or to motivate

the manager. Jensen and Murphy (1990) stated

that the stockholders demanded the executive

to act maximally the organization value to the owner and other stockholders in the company.

the stockholders and other stakeholders needed

to ind out if the executive salary at present commonly related to the company occupation and if there was a possibility to motivate the

executive to make some decisions in order to

increase the organization value.

Some researches showed signiicant

relationship among the managerial compensation

and the monetary occupation, the market occupation and the company measurement. Leonard (1990) tested the executive compensation and organization structure policy inluence to the company occupation. The result showed that the companies with

long-term incentive plan signiicantly enjoyed larger return of equity, compared to the companies without long-term incentive plan. Abowd (1990) tested the managerial compensation sensitively to the company occupation in a year positive relationship with the company occupation in the following year. The occupation measure based on the accounting resulted in a weak relationship while the occupation based on the economy and market created stronger support.

Ely (1990) analyzed the relationship between

the compensation and occupation of four major

industries (utility, bank, oil and gas, and retail) and

discovered that the Ceo compensation to bank

industry was directly related to the accountant variable. Shim, Lee and Corrigan (1999)

observed the Ceo compensation determiner in

monetary institute by testing the relationship between the CEO compensation and occupation based on the accounting and based on the market. The result showed that the CEO compensation would signiicantly and positively related to the ROA with lower degree and related to the ROE and market-to-book assets. The company measurement showed a positive relationship with

Ceo compensation total and cash compensation

(salary and bonus). Magnan and St-Onge (1997) tested how the relationship between the bank

occupation and executive compensation tended to be related to the bank occupation in higher

managerial policy context.

h3: there was a positive relationship between

the management compensation and corporate

governance with the following company occupation.

RESEARCH METHODS

Indonesian Capital Market directory 2003-2005. The company management compensation was the

numeric data of commissaries and management

stated in the annual report of the audit monetary report note 2003-2005.

Management compensation was a return of the service given by human resources for the organization, or value closely put by the company to the ability and human resources talent. Management compensation was measured by the level of remuneration achieved by the commissaries and management in a year of observation. The remuneration number listed covered total salary and bonus achieved.

Corporate governance was a relationship, system and process pattern led by the company organs (management, commissaries council, RUPS) in order to give additional value to the stockholders as a long term period continuously, which also considering the other stakeholders

importance based on the governmental rules and

valid norms. Corporate governance was proxy using the ownership structure variable and the number of the commissaries.

Firm Performance was a company ability sketch to produce its proit in the past and could be projected to the future to see the company ability

to gain more in the present period, so that the

investor might read the part of total proitability

that could be allocated to the stockholders’

hands. In this research, the irm performance was measured using both the ROA (Net Proit / Total Assets) and ROE (Net Proit / Total Equity).

The company assets composition was measured using the ratio between the constant assets to the total sales (Klapper and Love, 2002). The growth opportunity was proxy used IOS counted with MV/BV. hartono (2005) stated that when the MV/BV value was above 1, the company would be classiied prospected or developed, oppositely when the MV/BV value was less than or equal to 1, the company would be classiied unprospected or undeveloped. The company measurement was measured from the natural log of the sales. Incentive was given to the management based on its capability in increasing the sales, which was the key to cost the company activities (Lewellen and huntsman, 1970).

DATA ANALYSIS

in order to gain a common sketch of the research

data sample, we could see the research descriptive statistic as seen in table 2. dependent variable in model 1 was management compensation in 2004 which showed approximately 9.4372 with standard deviation of 0.55370. Management ownership had approximately 47.1855 with standard deviation of 19.79762. The commissaries number had approximately 3.9394 with standard deviation of 1.58725.

dependent variable in model 2 was the company occupation in 2005 measured using ROA and ROE with average 0.5462 and 0.9874 with standard deviation of 0.59378 and 0.64947.

2004 management Compensation independent Variable, the number of commissaries and

management ownership in 2004 had average 9.4372, 3.82 and 46.7400 with standard deviation of 0.55370, 1.424 and 19.9516.

hypothesis 1 and 2 Test Result showed number R square of 0.491, meant that 49.1% total compensation in 2004 could be explained by the number of commissaries, management ownership, company measure, growth opportunity, assets composition, and company occupation measured by ROA and ROE in 2003, meanwhile the rest would be explained by other factors outside the research model. F-stat value of 8.001 with signiication level of 0.000 which was less than 0.05 indicated that regression model totally explained the signiicant compensation in 2004.

The commissaries number had coeficient of 0.178 and positive signal 0.000 less than 0.05

meant that greater number of commissaries council meant greater number of management

compensation. This meant that based on the

sample of the research, the commissaries number

variable positively and signiicantly affected the management compensation. Therefore, the irst hypothesis stated that the commissaries number positively affected the management compensation was failed to be rejected.

sample was not a variable which was able to decide the management compensation. Therefore, the second hypothesis stated that there was a positive relationship between the managerial ownership and management compensation was failed to be supported.

The third hypothesis test result, dependent variable measured with ROA and ROE in 2005. In ROA test, the R square number was 0.068 meant that 6.8% ROA in 2005 could be explained by compensation in 2004, commissaries number, management ownership, company measure, growth opportunity and assets composition in 2004, while the others were explained by other factors outside the research model. F-stat value was 0.715 with signiicantly level of 0.639 or greater than 0.05 indicated that the regression model was not entirely signiicant, and this condition would statistically explain the ROA in 2005.

R square number of ROE test was 0.168 meant that 16% ROE in 2005 could be explained by compensation in 2004, number, management

ownership, company measure, growth

opportunity and assets composition in 2004, while the others were explained by other factors outside the research model. F-stat value was 1.988 with signiicantly level of 0.082 or greater than 0.05 indicated that the regression model was not entirely signiicant, and this condition would statistically explain the ROE in 2005.

Regression result showed that the

compensation variable, corporate governance and economic determiner variables of the

company occupation would not statistically affect the next company occupation. Therefore, the third hypothesis stated that compensation and

corporate governance had positive relationship

with the company occupation in the following year could not be supported. This result supported Core, holthausen, Larcker (1999) research.

The research tested also the company occupation in 2004. The compensation variable,

corporate governance and economic determiner

variables of the company occupation would not statistically affect the company occupation in the year of 2004.

DISCUSSION

the commissaries number in this research

was positively related to the management compensation. This indicated that the management compensation was able to catch their duties, authority, and strategic decisions created by the commissaries council. Viewed from the perspective of agency, the positive relationship would show us that the principal and agent

relationship had a contract to bundle the agent to

service based on their knowledge, experiences, skill and ability. Watts and Zimmerman (1986) in their positive accounting theory stated that the owner and management relationship, commonly hypnotized in bonus plans was a bundle between the owner and management shaped in a contract.

Walker (1992) stated that compensation was a strategic key to human resource management purposed to create job harmony to achieve the objective and target decided at the irst place.

therefore, the management compensation contract

was designed to motivate the management to achieve the occupation target decided previously by the principal.

Ownership structure measured by managerial ownership negatively related to the management compensation. This condition showed that the management compensation was not affected by the importance of management possesses company stocks. The entity theory viewed the company as an entity separated from the owner

and creditor, separated management from the

company owner. This condition showed that there was a function separation between the managerial as owner and as agent.

The irm Performance in some researches showed the existence of positive relationship with the compensation or corporate governance. The hypothesis test result of the research showed different results. Observed from the statistic

descriptive model 2, average roA 2005 from

the research sample company was 0.5462% possessing positive correlation sign which was not signiicant to the compensation 2004 and negative for both measurement of corporate governance. This condition showed the low ability of the company to gain proit from the assets utility. Average ROE in 2005 was 0.9874, possessing positive correlation sign which was not signiicant

to the compensation 2004 and negative for both

measurement of corporate governance. This also showed that the ability of the research sample of company to distribute the gained proit to the stockholders was low. Therefore, compensation and corporate governance were explicitly unable to be reserved for subsequent irm performance.

The result of model 2 was consistent with several researches showed that there was no relationship between the corporate governance and company occupation, such as daily and friends (1999) result, CBI survey result, deloitte and Touche (1996) in darmawati, Khomsiyah and Rahayu (2004).

According to Kakabadse and friends (2001) in darmawati, Khomsiyah and Rahayu (2004), the difference result of the researches was caused by several reasons. There were: 1) decided perspective theoretic, 2) Research methodology, 3) Occupation measure, and 4) Opinion distinction towards the council participation in the decision making.

The research result showed also that the compensation contract was not yet optimal to be a motivation to the company occupation in the following year. Compensation in 2004 which had positive relationship with the corporate governance showed that there was no signiicant relationship with the subsequent irm performance.

Consistent to the research, Core, holthausen,

Larcker (1999) that the compensation component had negative association was signiicant to the ownership and council structure variable, the management council did not actively supervised

and this was an opposite interpretation with the company request of the CEO quality.

CONCLUSION

The goal of this research was to give

evidence that the corporate governance affected the management compensation and subsequent

irm performance. This research was expected to be able to answer some research questions

related to the corporate governance, management

compensation and subsequent irm performance. Based on the research result performed in the

manufacture companies listed in Jakarta stock

Exchange fulilled the sample election criteria, we could take several conclusions as follow: 1. The result of this research showed that the

commissaries number would positively and signiicantly affect the management compensation in 2004. This fact answered

the research question that the corporate

governance application to create the company value positively related with the management compensation. This fact showed also that compensation as a company human resource strategy gave reward to the service given by the commissaries council.

2. The result of this research also gave evidence that the ownership structure measured by the managerial ownership had no positive relationship with the managerial compensation. This condition indicated that the control function of the ownership structure did not work effectively yet.

3. The result of this research answered the

research question that the compensation

and corporate governance did not positively related to the subsequent irm performance. This condition showed that the compensation did not design optimally and the corporate governance did not work effectively.

SUGGESTION

in this research, mistake might happen

management in the strategic level that made this research used remuneration data for all

the commissaries and management council. 2. The samples used were manufacture

companies only, stated the remuneration number in their inancial report without differentiate the company participation in the corporate governance performance survey.

this fact occurred since the research did not use the perception index of corporate

governance performed by IICG together with SWA magazine.

The research was expected to give idea to develop the next researches. Based on the present existed limits, the following researches might give several considerations as follow:

1. Surveying the management compensation

to gain the compensation data for each

management level.

2. Made the good corporate governance (GCG)

index in order to explain all good corporate

governance (GCG) variables so that the good corporate governance (GCG) application success measure could be more measurable.

REFERENCES

Abowd, J. M. 1990. Does Performance-based

Managerial Compensation Affect Corporate Governance?. industrial and labor relations

Review, 43.

Chhaochharia, V., and Grinstein, y. 2006. CEO

Compensation and Board Structure. Journal

of Finance. Version 2006.

Core, John E., holthausen, Robert W., and Larcker,

david F. 1999. Corporate Governance,

Chief Executive Oficer Compensation, and

Firm Performance. Journal of Financial

Economics.

Cyert, R., Kang, S., Kumar, P. 2002. Corporate

Governance, Takeovers, and Top Management Compensation: Theory and Evidence.

Manegement Science 48.

darmawati, deni, Khomsiyah, and Rahayu, Gelar

R. 2004. Hubungan Corporate Governance

dan Kinerja Perusahaan. Seminar Nasional

Akuntansi VII. denpasar – Bali.

Eisenhardt, Kathleen M. 1989. Agency Theory:

An Assesment and Review. Academic of

Management Review. Vol. 14.

Ely, Kirsten M. 1991. Interindustry Differences

in the Relation between Compensation and Firm Performance Variables. Journal of

Accounting Research. Vol 29.

Fama, Eugene F and M. C. Jensen. 1983.

Separation of Ownership and Control. Journal

of Law and Economics. Vol. XXVI.

Grinstein, y., dan hribar, P. 2004. CEO

Compensation and Incentives: Evidence from M&A bonuses. Journal of Financial

Economics 73.

Gibbons, R., and Muphy, K. J. 1992. Optimal

Incentive Contracts in The Presence of Career Concern: Theori and Evidence. Journal of

Political Economy.

Gompers, Paul A., Ishii, Joy L., and Metrick

Andrew. 2003. Corporate Governance

and Equity Prices. Quarterly Journal of

Economics.

hallock, K. F. 1997. Reciprocally Interlocking

Boards of directors and Executive Compensation. Journal of Financial and

Quantitative Analysis 32.

hartono, Jogiyanto. 2005. Pasar Eisien Secara

Keputusan. Gramedia Pustaka Utama.

Jakarta.

hastuti, dwi., T. 2005. Hubungan antara

Good Corporate Governance dan Struktur Kepemilikan dengan Kinerja Keuangan.

Simposium Nasional Akuntansi VIII. Solo.

husnan, Suad. 2000. Corporate Governance:

Pengamatan terhadap Sektor Korporat dan Keuangan. Seminar Sosialisasi Corporate Governance. UGM. yogayakarta.

holdernest, C. G., and Sheehan, d. P. 1988. The

Role of Majority Shareholders in Publicly Held Corporation: An Exploratory Analysis.

Jensen, M. C., and Meckling, W. h. 1976. Theory of The Firm: Managerial Behavior, Agency Cost and Ownership Structure. Journal of

Financial Economics 3.

Jensen, M. 1993. The Modern Industrial

Revolution, Exit, and The Failure of Internal Control Systems. Journal of Finance 48.

Klapper, Leora F. and I. Love. 2002. Corporate

Governance, Investor Protection and Performamnce in Emerging Markets. World

Bank Working Paper.

Kusumawati, d. W. and Riyanto, B. 2005.

“Corporate Governance dan Kinerja: Analisis Pengaruh Compliance Reporting dan Struktur Dewan terhadap Kinerja.”

Simposium Nasional Akuntansi VIII, 248-261.

Lawellen, W. G., and huntsman, B. 1970. Managerial Pay and Corporate Performamnce. American Economic Review 60.

Leonard, Jonathan S. 1990. Executive Pay and

Firm Performance. Industrial and Labor

Relations Review. Vol. 43.

Lukuhay, Jos. 2002. Tata Pamong dan Nilai

Perusahaan. Warta Ekonomi, No. 21/XIV/2

September.

Magnan, Michel L and Sylvie St-Onge. 1997. Bank

Performance and Executive Compensation: A

Managerial Discretion Perspective. Strategic

Management Journal. Vol 18.

McConnel, J. and Servaes, h. 1990. Additional

Evidence on Equity Ownership and Corporate Value. Journal of Financial Economics 27.

Raick, Ishack. 2002. Menggugat Fungsi

Komisaris Independen. SWA, No. 15/XVII/15

Juli-7 Agustus.

shim, eunsup “daniel”, John lee, and thomas

Corrigan. 1999. An Empirical Examination of

Top Executive Compensation and Economic Performamnce in Financial Service Firms.

Advances in Management Accounting. Vol 8.

Shleiver, A. and R. W. Vishny. 1997. A Survey

of Corporate Governance. Journal of Finance

52.

Simamora, h. 1995. Manajemen Sumber Daya

Manusia. STIE yKPN. yogyakarta.

Walker, J. W. 1992. Human Resource Strategy.

Mc Graw-hill, Inc. New york.

Watts, R., and J. Zimmerman. 1986. Positive

Accounting Theory. Englewood Cliffs NJ:

Prenctice hall.

Xu, Xiaonian., and Wang, yang. 1999. Ownership

AKUNTABILITAS SEBAGAI ALAT PENGUKURAN

KINERjA PEMERINTAH DAERAH

yUSRI hAZMI1, FAisAl1 dAN ZUARNI1

1Dosen Tata Niaga Pada Politeknik Negeri Lhokseumawe

This paper attempts to explain the importance of accountability in order to realize good governance (good governance). Accountability is one essential element in achieving good governance. As a manifestation of the implementation of APBN / APBd, the government

is obliged to report on achievements that have been implemented, so that people understand

and can assess whether the government has been working according to plan that has been set, and load the working principles of effective, eficient. Approach to accountability in inancial management is the embodiment of creating good government. Accountability can be seen from

various perspectives such as: perfective accounting, functional perspective and the perspective

of accountability systems. Some of the techniques developed to strengthen the accountability system is strongly inluenced by the method that is widely used in accounting, management and research, such as management by objectives, performance-based budgeting, operations research and others. Performance measurement can be grouped into three indicators, namely: (1) Efforts indicator measurement service, (2) indicators measuring service accomplishment, and (3) indicators that connects between Efforts with accomplishment. In addition it needs to be delivered is also an additional explanation relating to the reporting of this performance.

Keywords: accountability, performance measurement

LATAR BELAKANG

Tata kelola pemerintahan yang baik (Good

governance) dapat diartikan sebagai suatu

penyelenggaraan pengelolaan pembangunan yang bertanggung jawab dengan prinsip demokrasi, eisien, efetiitas dan pencegahan

korupsi baik secara politik maupun administrasi, menjalanan disiplin anggaran serta penciptaan

legal dan politikal framework bagi tumbuhnya aktivitas usaha. Terdapat beberapa karateristik

good governance, meliputi: (1). Partisipation, (2) Rule of law, (3) Responsiveness, (4) Consensus

oreintation, (5) Equity, (6) Eficiency and

Effectiveness, (7) Accountability and (8) Stategic vision. Ada beberapa kriteria dalam mewujukan good governance, seperti: keterbukaan ( trans-parency), eisiensi (eficiency), tanggung jawab

(responsibility) dan kewajaran (fairness).

Pemerintah sebagai pelaku utama dalam

pelaksanaan good governance, dituntut dapat

memberikan pertanggungjawaban secara trans-paran dan akurat. Saat ini akuntabilitas masih

berfokus pada pengelolaan keuangan negara

(APBN) dan daerah (APBd). Untuk mewujudkan

good governance diperlukan reformasi

kelembagaan dan manajemen publik. Reformasi kelembagaan menyangkut pembenahan seluruh

alat-alat pemerintah di daerah baik struktur

maupun infrastuktur. Sedangkan reformasi

manajemen publik terkait dengan sistem

pengelolaan keuangan pemerintah daerah, yang

meliputi: sistem anggaran, sistem akuntansi, sistem pemeriksaan dan sistem manajemen

keuangan daerah.

Fenomena yang dapat diamati dalam

perkembangan sektor keuangan publik adalah

semakin menguatnya tuntuan pelaksanaan

akuntabilitas publik oleh organiasi sektor publik

(seperti: pemerintah pusat dan daerah, unit-unit

kerja pemerintah, departemen dan

lembaga-lembaga negara). Tuntutan akuntabilitas sektor publik terkait dengan perlunya dilakukan

transparansi dan pemberian informasi kepada

publik dalam rangka pemenuhan hak-hak publik. Akuntabilitas publik adalah kewajiban

pihak pemegang amanah (agent) untuk

memberikan pertanggung jawaban, menyajikan,

melaporkan dan mengungkapan segala ativitas

kepada pihak pemberi amanah (principal) yang memiliki hak dan kewenangan untuk meminta pertanggungjawaban tersebut. dalam kontek

pemerintahan, akuntabilitas publik adalah pemberian informasi dan disclosure atas ativitas

dan kinerja inancial permerintah kepada pihak-pihak yang berkepentingan dengan laporan keuangan tersebut.

Akuntabilitas dapat dipandang dari berbagai perspektif, baik akuntansi, fungsional, maupun

sistem akuntabilitas. dari perspektif akuntansi,

American Accounting Association menyatakan

bahwa akuntabilitas suatu entitas pemerintahan dapat dibagi dalam empat kelompok, yaitu

akuntabilitas terhadap:

1. Sumber daya inansial

2. Kepatuhan terhadap aturan hukum dan

kebijaksanaan administratif

3. Eisiensi dan efektiitas suatu kegiatan 4. hasil program dan kegiatan pemerintah yang

tercermin dalam pencapaian tujuan, manfaat

dan efektivitas.

sedangkan dari perspektif fungsional, akuntabilitas dilihat sebagai suatu tingkatan

dengan lima tahap yang berbeda yang diawali dari tahap yang lebih banyak membutuhkan

ukuran-ukuran obyektif (legal compliance) ke

tahap yang membutuhkan lebih banyak ukuran-ukuran subyektif . Tahap-tahap tersebut adalah: 1. Probity and legality accountability, hal ini

menyangkut pertanggungjawaban

peng-gunaan dana sesuai dengan anggaran

yang telah disetujui dan sesuai dengan peraturan perundang-undangan yang berlaku (compliance).

2. Process accountability, dalam hal ini digunakan proses, prosedur, atau ukuran-ukuran dalam melaksanakan kegiatan

yang ditentukan (planning, allocating and

managing).

3. Performance accountability, Pada level ini

dilihat apakah kegiatan yang dilakukan sudah

eisien (eficient andeconomy).

4. Program accountability, di sini akan disoroti

penetapan dan pencapaian tujuan yang

telah ditetapkan tersebut (outcomes and

effectiveness).

5. Policy accountability, dalam tahap ini

dilakukan pemilihan berbagai kebijakan yang

akan diterapkan atau tidak (value).

dari perspektif sistem akuntabilitas, terdapat beberapa karakteristik pokok sistem akuntabilitas,

yaitu :

1. Berfokus pada hasil (outcomes)

2. Menggunakan beberapa indikator yang telah

dipilih untuk mengukur kinerja

3. Menghasilkan informasi yang berguna bagi

pengambilan keputusan atas suatu program atau kebijakan jawabannya atas semua aktivitasnya kepada masyarakat. Seiring dengan meningkatnya aktivitas pemerintah dan timbul kesadaran yang

luas untuk menciptakan sistem

pertanggung-jawaban yang lebih komprehensif. Ternyata dalam pelaksanaannya, keingintahuan masyarakat

tentang akuntabilitas pemerintahan tidak dapat

dipenuhi hanya dengan informasi keuangan saja. Masyarakat ingin tahu lebih jauh apakah pemerintah yang dipilihnya telah beroperasi dengan ekonomis, eisien dan efektif. Beberapa teknik yang dikembangkan untuk memperkuat

sistem akuntabilitas sangat dipengaruhi oleh

metode yang banyak dipakai dalam akuntansi,

manajemen dan riset, seperti management by objectives, anggaran kinerja, riset operasi, audit

kepatuhan dan kinerja, akuntansi biaya, analisis keuangan dan survey yang dilakukan terhadap masyarakat sendiri.

Pelaporan pengukuran kinerja (performance

measurement) berkaitan dengan proses yang dinamakan managing for results (pengelolaan pencapaian). Proses ini timbul dari meningkatnya

tuntutan, yang bahwa manajemen pemerintahan perlu memakai pendekatan yang sama dengan manajemen di sektor swasta maupun organisasi nir laba lainnya. Proses ini merupakan

pendekatan komprehensif untuk memfokuskan

(goals ) dan tujuan (objectives).

Kewajiban pemerintah untuk

mempertanggungjawabkan kinerjanya dengan

menyampaikan informasi yang relevan

sehubungan dengan hasil dari program yang dilaksanakan kepada wakil rakyat dan juga kelompok-kelompok masyarakat yang memang ingin menilai kinerja pemerintah. Pelaporan keuangan pemerintah pada umumnya hanya menekankan pada pertanggungjawaban apakah sumber daya yang diperoleh sudah digunakan

sesuai dengan anggaran atau

perundang-undangan yang berlaku.

dengan demikian pelaporan keuangan yang ada hanya menjelaskan informasi yang berkaitan

dengan sumber pendapatan pemerintah,

bagaimana penggunaannya dan posisi keuangan.

Jika hal ini dikaitkan dengan perspektif fungsional

akuntabilitas, maka yang dilakukan masih

pada tahap probity and legality accountability (compliance). harus diingat, tahap ini barulah

tahap awal dari lima tahap akuntabilitas sesuai perspektif fungsional.

Pembandingan tujuan pelaporan keuangan non pemerintah yang dalam pelaporan keuangan harus menyediakan informasi sehubungan

dengan kinerja keuangan (inancial performance)

dalam periode tertentu. yang berfokus pada

mengukur pendapatan (comprehensive income)

dan komponen-komponennya. Sedangkan pada

organisasi nir laba, pelaporan keuangan harus

menyediakan informasi sehubungan dengan

kinerja (performance) dalam periode tertentu.

Informasi yang paling dibutuhkan untuk menilai

kinerja ini adalah pengukuran periodik atas perubahan jumlah dan sifat net resources dari

organisasi yang bersangkutan dan informasi

mengenai service efforts and accomplishment.

Pengukuran kinerja sektor publik adalah sistem yang bertujuan untuk membantu manajer

publik menilai pencapaian suatu strategi melalui alat ukur inancial dan non inancial. sistem pengukuran kinerja dapat dijadikan sebagai alat pengedalian organisasi, karena pengukuran kinerja diperkuat dengan menetapkan reward dan punishment system.

Pengkuran kinerja sektor publik dilakuan untuk memenuhi tiga maksud, yaitu: (1)

pengukuran kinerja dimaksudkan untuk membantu

memperbaiki kinerja pemerintah. Ukuran kinerja

dimaksudkan untuk dapat membantu pemerintah berfokus pada tujuan dan sasaran program unit

kerja. hal ini pada akhirnya akan meningkatan eisiensi dan efetiitas organisasi sektor publik dalam pemberian pelayanan publik. (2) ukuran

kinerja digunakan untuk pengalokkasian

sumber daya dan pembuatan keputusan. dan (3) ukuran kinerja dimaksudkan untuk mewujukan pertanggungjawaban publik dan memperbaiki komunikasi kelembagaan.

oleh pihak, ukuran kinerja digunakan untuk

menentukan kelayakan biaya pelayanan (cost

of service) yang dibebankan kepada masyaraat

pengguna jasa publik. Masyarakat tentunya tidak

mau terus-menerus ditarik pengutan, sementara

pelayanan yang mereka terima tida ada peningkatan secara kuantitas maupun kualitas. Oleh karena itu, pemerintah berkewajiban untuk meningkatkan eisiensi dan efetiitas pelayanan publik. Masyarakat menghendaki pemeritah dapat memberikan pelayanan dengan biaya yang

murah (do more with less).

secara umum, tujuan sistem pengukuran kinerja adalah untuk mengkomunikasikan strategi

yang lebih baik, untuk mengukur kinerja inancial

dan non inancial secara berimbang sehingga dapat ditelusuri perkembangan pencapaian strategi, untuk mengakomodasikan pemahaman kepentingan manajer level mengengah dan

bawah serta memotivasik untuk mencapai goal

congruence dan sebagai alat untuk mencapai kepuasan berdasaran pendeatan individual dan

kemampuan koletif yang rasional.

Pengukuran kinerja dapat dilakukan dengan menggunaan tiga indikator, yaitu (1) indikator

pengukuran service efforts, (2) indikator pengukuran service accomplishment, dan (3)

indikator yang menghubungkan antara efforts

dengan accomplishment. Service efforts berarti

bagaimana sumber daya digunakan untuk

melaksanakan berbagai program atau pelayanan

jasa yang beragam. Service accomplishment

diartikan sebagai prestasi dari program tertentu. di samping itu perlu disampaikan juga penjelasan tertentu berkaitan dengan pelaporan kinerja

Pengukuran-pengukuran ini melaporkan jasa apa saja yang

disediakan oleh pemerintah, apakah jasa tersebut

sudah memenuhi tujuan yang ditentukan dan apakah efek yang ditimbulkan terhadap penerima layanan/jasa tersebut.

Pembandingan service efforts dengan service

accomplishment merupakan dasar penilaian

eisiensi operasi pemerintah (GASB, 1994), yang

terdiri dari:

1. Measure of Efforts

Efforts (usaha) adalah jumlah sumber daya

keuangan dan non keuangan yang dinyatakan dalam uang atau satuan lainnya, yang dipakai

dalam pelaksanaan suatu program atau jasa

pelayanan. Pengukuran service efforts meliputi

pemakaian rasio yang membandingkan sumber daya keuangan dan non keuangan dengan ukuran lain yang menunjukkan permintaan potensial atas jasa yang diberikan seperti populasi umum, populasi jasa atau panjang jalan raya. Contoh sumber daya non keuangan yang paling utama adalah jumlah personalia pemerintah. Ukuran yang paling sering dipakai adalah jumlah pegawai (ekuivalen dengan pegawai dengan jam kerja penuh) atau jumlah jam kerja per jasa yang diberikan.

2. Measures of Accomplishment

Ada dua jenis ukuran accomplishment atau

prestasi, yaitu: outputs dan outcomes. Outputs

befokus pada mengukur kuantitas jasa yang disediakan, dan outcomes mengukur hasil dari

penyediaan outputs tersebut. Outputs dapat

mengukur hanya sebatas kuantitas jasa yang

disediakan. Outcomes akan lebih berguna jika

dalam penggunaannya dapat dibandingkan

dengan outcomes tahun-tahun sebelumnya atau

dibandingkan dengan target yang telah ditetapkan sebelumnya.

3. Measures that relates efforts to accomplishment

Pembandingan yang pertama adalah

pembandingan antara efforts dengan outputs

untuk mengukur eisiensi. Informasi yang ingin diberikan adalah sejauh mana hasil yang diperoleh sehubungan dengan penggunaan sumber daya yang dipakai. Pembandingan yang kedua adalah

pembandingan antara efforts dengan outcomes.

Pembandingan ini juga untuk mengukur eisiensi

namun dalam target tertentu. Informasi ini juga akan lebih berguna jika dibandingkan dengan tingkat eisiensi tahun sebelumnya dan dibandingkan dengan target pencapaian tingkat

eisiensi tertentu. hal ini dikenal juga dengan

istilah indeks produktivitas atauindeks eisiensi. indeks ini dihitung dengan mengaitkan rasio produktivitas atau eisiensi tahun sekarang

dengan satu tahun dasar tertentu. 4. Explanatory Information

dalam hal ini kepada para pengguna laporan diberitahukan juga explanatory information atau

berbagai macam informasi yang relevan dengan

layanan yang diberikan dan faktor-faktor yang

mempengaruhi kinerja organisasi pemerintah,

yang dikelompokkan dalam dua elemen sebagai berikut.

- elemen di luar kontrol pemerintah seperti

kondisi demograi dan lingkungan.

- Elemen yang dapat dikontrol oleh pemerintah secara signiikan seperti pola dan komposisi personalia.

Wayne C. Parker (1996:3) menyebutkan lima manfaat dengan adanya pengukuran kinerja suatu entitas pemerintahan, yaitu:

1. Pengukuran kinerja dapat meningkatkan mutu pengambilan keputusan. Seringkali keputusan yang diambil pemerintah dilakukan dalam

keterbatasan data, informasi, pertimbangan

politik serta tekanan dari pihak-pihak yang berkepentingan.

2. Pengukuran kinerja meningkatkan akun-tabilitas internal.

dengan adanya pengukuran kinerja ini, secara

otomatis akan tercipta akuntabilitas di seluruh

lini pemerintahan. dalam hal ini disarankan pemakaian system pengukuran standar seperti

halnya management by objectives untuk

mengukur outputs dan outcomes.

3. Pengukuran kinerja meningkatkan akun-tabilitas publik. dengan keterlibatan masyarakat dalam pembuatan kebijakan pemerintah, akan menrorong kepercayaan masyaraat.

4. Pengukuran kinerja dan mendukung peren-canaan stategi dan penetapan tujuan. Proses

kurang berarti tanpa adanya kemampuan

untuk mengukur kinerja dan kemajuan

suatu program. Tanpa ukuran-ukuran ini,

kesuksesan suatu program juga tidak pernah

akan dinilai dengan obyektif.

5. Pengukuran kinerja memungkinkan suatu

entitas untuk menentukan penggunaan sumber

daya secara efektif. Masyarakat semakin

kritis untuk menilai program-program pokok

pemerintah sehubungan dengan meningkatnya pajak yang dikenakan kepada mereka. Evaluasi yang dilakukan cenderung mengarah

kepada penilaian apakah pemerintah memang

dapat memberikan pelayanan yang terbaik kepada masyarakat.

dengan adanya pengukuran, analisis dan evaluasi terhadap data yang berkaitan dengan

kinerja, pemerintah dapat menentukan strategi untuk mempertahankan atau meningkatkan

eisiensi dan efektivitas suatu kegiatan dan sekaligus memberikan informasi obyektif kepada

publik mengenai pencapaian hasil (results) yang

diperoleh.

Penilaian laporan kinerja dapat diukur

baik dengan pendekatan keuangan maupun

non keuangan. Pendekatan keuangan, kinerja diukur berdasaran pada anggaran yang telah dibuat. Penilaian tersebut dilakukan dengan menganalisa variance (selisih atau perbedaan) antara kinerja aktual dengan yang dianggaran.

secara garis besar analisis varian berfokus pada varian pendapatan (revenue) dan pengekuaran (exfenditure). dan Pendekatan non keuangan, informasi non keuangan dapat dijadikan sebagai

tolak ukur lainnya. Informasi non keuangan dapat menambah keyakinan terhadap kualitas proses pengendalian manajemen. Teknik pengukuran kinerja yang komfrehensif yang banyak diembangan oleh berbagai organisasi dewasa ini

adalah Balance Scorecard.

Pengukuran kinerja bukan merupakan satu-satunya alat yang dipakai untuk menilai akuntabilitas pemerintahan. terdapat beberapa

keterbatasan atas pelaporan pengukuran berbasis

kinerja, yaitu:

1. Pemakaian satu ukuran tertentu tidak disarankan mengingat satu ukuran yang

dipakai tidak dapat menggambarkan secara

lengkap hasil yang dicapai oleh pemerintah. Pengguna laporan pengukuran kinerja

diharapkan menggunakan juga lebih dari satu

ukuran.

2. Informasi kinerja tidak menjelaskan alasan

pemerintah bagaimana mencapai prestasi

tersebut, bagaimana meningkatkannya dan

sejauh mana pengaruh faktor-faktor lain

dalam pencapaian kinerja tersebut.

3. Proses dan strategi yang dipakai untuk

menyediakan jasa seringkali tidak

disampaikan dalam pelaporan. Walaupun

hal tersebut merupakan informasi penting

untuk memahami mengapa pemerintah hanya mencapai prestasi tertentu.

KESIMPULAN

Tata kelola pemerintahan yang baik (Good

governance) dapat diartikan sebagai suatu

penyelenggaraan pengelolaan pembangunan yang bertanggung jawab dengan prinsip demokrasi, eisien, efetiitas dan pencegahan korupsi baik

secara politik maupun administrasi, menjalanan disiplin anggaran serta penciptaan legal dan

politikal framework bagi tumbuhnya aktivitas usaha.

Akuntabilitas publik adalah kewajiban pihak pemegang amanah (agent) untuk memberikan pertanggung jawaban, menyajikan, melaporkan

dan mengungkapan segala ativitas dan kegiatan

yang menjadi tanggung jawabnya kepada pihak pemeberi amanah (principal) yang memiliki hak dan kewenangan untuk meminta pertanggungjawaban tersebut.

dalam kontek pemerintahan, akuntabilitas publik adalah pemberian informasi dan disclosure

atas ativitas dan kinerja inancial permerintah kepada pihak-pihak yang berkepentingan dengan laporan keuangan tersebut.

hanya menekankan pada pertanggungjawaban apakah sumber daya yang diperoleh sudah

digunakan sesuai dengan anggaran atau

perundang-undangan yang berlaku.

REFERENSI

Beams, Floyd A., John A. Brozovsky dan Craig

d. Shoulders (2000). Advanced Accounting.

Edisi ketujuh. New Jersey: Prentice hall International Inc.

damanik, Usman (2000), Paradigma Baru

Pengawasan Keuangan Negara. Makalah, Kongres Nasional Akuntan indonesia iV.

Jakarta.

Govermental Accounting Standard Board (1994).

Concepts Statements No. 2, Service Efforts and Accomplishment Reporting. www.

rutgers.edu/Accounting/raw/seagov/ pmg/

perfmeasure, September 2000.

handjari J. (2000). Paradigma Baru dalam

Akuntansi Sektor Publik. Makalah, Kongres Nasional Akuntan indonesia iV. Jakarta.

Jones, Rowan dan Maurice Pendlebury (1996).

Public Sector Accounting. Edisi keempat.

London: Pitman Publishing.

McMahon, Tom (1996). “Access to Government

Information: A New Instrument for Public

Accountability” Government Information in

Canada, Volume 3, Number 1.

Parker, Wayne C. (1993). Performance

Measurement in the Public Sector. State of

Utah. www.rutgers.edu/Accounting/raw/

seagov/pmg/perfmeasure, September 2000.

Prodjoharjono, Soepomo (2000). Redeinisi

Akuntan Sektor Publik dalam Upaya Penciptaan Good Government Governance. makalah, Kongres Nasional Akuntan

Indonesia IV. Jakarta.

Soelendro, Ari (2000). Paradigma Baru Aparat

Pengawasan Intern Pemerintah. makalah, Kongres Nasional Akuntan indonesia iV.

Jakarta.

Undang-undang Nomor 22 Tahun 1999 tentang Pemerintahan daerah. Jakarta: Sinar Graika.

KEPUTUSAN PERUSAHAAN MELAKUKAN

SHARE

REPURCHASE

:

FREE CASH FLOW HYPOTHESIS

ATAUKAH

SIGNALING THEORY

eddy surANtA1, PRATANA PUSPA MIdIASTUTy1 dAN

R. RyAN MULyA WIJAyA1

1Dosen Pada Fakultas Ekonomi Universitas Bengkulu

This study aims to examine the factors that affect companies doing share repurchase with free cash low as dependent variable, irm value, irm size, leverage, earnings per share, and dividends. The sample in this study are the companies that make share repurchase and the comparison companies listed on the Indonesia Stock Exchange in 2004 until 2009. data used in this research is secondary data obtained from inancial data on the website www. idx.com. The number of samples in this study were as many as 38 companies consisting of 19 companies doing share repurchase and 19 comparison companies are not doing share repurchase. data analysis was performed with logistic regression using SPSS version 16.0. Results of hypothesis testing showed the inluence of a low irm value (undervalued) more inluence corporate decisions to share repurchase and signiicant (Signiicant = 0034). Free cash low in order to reduce the agency problem does not show signiicant results to inluence the company’s decision to share repurchase (Signiicant = 0141). Furthermore, earnings per share showed a negative and signiicant inluence but the dividends show a positive inluence and not signiicant where the second hypothesis is also rejected. Free cash low, earnings per share, and dividends is a variable that hypothesis is rejected Size also affects the company and leverage the company’s decision to share repurchase.

Keywords: Share Repurchase, Free Cash Flow, Signaling Theory, Leverage, Earnings per share, Dividend

LATAR BELAKANG

Sartono (2001) menyatakan perusahaan akan

melakukan share repurchase ketika memiliki

kelebihan kas dan tidak mempunyai kesempatan investasi yang menguntungkan. Jika berdasarkan pertimbangan bahwa perusahaan tidak memiliki

investment opportunity set yang menguntungkan maka perusahaan dapat menggunakan free cash

low tersebut untuk dibayarkan dalam bentuk

dividen. Akan tetapi, jika pembayaran dividen tersebut dianggap tidak memberikan sinyal yang

positif terhadap kinerja perusahaan dan tidak dapat mempengaruhi harga sekuritas perusahaan serta saham perusahaan cenderung undervaluation maka manajemen perusahaan memutuskan menggunakan free cash low untuk melakukan program share repurchase (Mauboussin, 2006).

dua penjelasan yang paling populer

menjelaskan keputusan perusahaan memutuskan melakukan share repurchase adalah hipotesis

free cash low dan teori sinyal (signaling theory). hipotesis free cash low yang dijelaskan didalam

teori keagenan menyatakan secara tidak langsung,

perusahaan dengan kelebihan aliran kas dan

pembayaran hutang yang kecil akan melakukan

share repurchase yang lebih besar. dittmar (1999) mengemukakan, apabila perusahaan memiliki kelebihan aliran kas, maka perusahaan dapat

menahan laba tersebut atau mendistribusikannya kepada pemegang saham. Perusahaan dengan aliran kas yang tinggi berada pada risiko yang

tinggi untuk investasi berlebih, danFree cash

low memberikan reaksi konlik antara pemegang

saham maupun manajer ketika aliran kas berlebih

dan tidak digunakan sesuai dengan kegunaannya

(Jensen, 1986). dengan mengembalikan free cash

low kepada pemegang saham, share repurchase

akan mengurangi konlik tersebut.

Chen et al., (2007) mengemukakan