This development, which is a private-public partnership, also aims to attract new industries to the region and unlock further employment and business opportunities for locals. The development activity started during January 2015 with the Malda Pack facility of 15,000 m2 that had started business activity; Mr Price's new 60,000 m2 National Distribution Center is complete, with construction of Pepkor's new 85,000 m2 Distribution Center completed in December 2017. The city and developer are currently in discussions regarding financing for the development of the interchange.

COUNCIL RESOLUTIONS

- BUDGET RELATED RESOLUTIONS

- ESTIMATES OF INCOME AND EXPENDITURE

- RECAPITULATION: VALUATION OF RATEABLE PROPERTY

- EXEMPTIONS, REBATES AND REDUCTIONS

- RESIDENTIAL PROPERTY

- PUBLIC BENEFIT ORGANISATIONS

- LIFE RIGHTS SCHEMES AND RETIREMENT COMPLEXES

- SCHOOLS NOT FOR GAIN

- BED AND BREAKFAST UNDERTAKINGS

- GUEST HOUSE UNDERTAKINGS

- BACK–PACKER LODGES, HOLIDAY ACCOMODATION AND STUDENT ACCOMMODATION

- VACANT LAND

- PROPERTIES IN THE OWNERSHIP OF THE MUNICIPALITY OR MUNICIPAL ENTITIES

- NATURE RESERVES AND CONSERVATION AREAS

- ECONOMIC DEVELOPMENT

- SPECIAL RATING AREAS

- CONSULATES

- GREEN CERTIFIED BUILDINGS

- PHASING IN OF RATES

- FLAT SERVICE CHARGE RATE FOR FORMAL PROPERTIES VALUED BELOW R 185 000 AND INFORMAL SETTLEMENTS WHERE WATER AND ABLUTION FACILITIES HAVE BEEN PROVIDED

- DATE OF OPERATION OF DETERMINATION OF RATES That this determination comes into operation on 1 July 2019

- FINAL DATE FOR PAYMENT OF RATES

- ADMINISTRATION CHARGE ON ARREAR RATES

- DOMESTIC WATER DEBT RELIEF PROGRAM

- BUDGET RELATED POLICIES (i) RATES POLICY

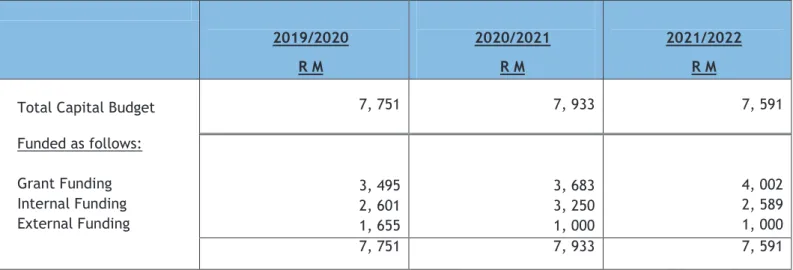

- CAPITAL EXPENDITURE ESTIMATE

- BORROWINGS TO FINANCE THE CAPITAL BUDGET

- HOUSING/HOSTELS DEFICIT

- NEW FUNCTIONS/ SERVICES

- INTEGRATED DEVELOPMENT PLAN (IDP)

- PARTICULARS OF INVESTMENTS

- REMUNERATION OF COUNCILLORS AND SENIOR OFFICIALS

- UNFUNDED MANDATES

- IMPACT OF HOUSING EXPENDITURE ON THE CASH RESERVES

- EXPENDITURE CONTROL, AUSTERITY MEASURES & TARIFFS IN THE CURRENT STATE OF THE ECONOMY

- FREE BASIC SERVICES

- OFF BALANCE SHEET FINANCING

- FOOD AID PROGRAM (SOUP KITCHENS)

- HOSTEL COLLECTIONS

- METER READING STRATEGY

- DESTINATION MARKETING PROGRAMS

That authorization is granted to the City Manager to conclude contracts with the owners in terms of the partnership investment. In the past they also had connections with the various local leadership of the City's in the UK.

EXECUTIVE SUMMARY 1

INTRODUCTION

OVERVIEW OF THE 2019/20 MTREF

The objectives of the program are starting and growing entrepreneurs who are active in the value chain of sustainable food. The municipality believes in empowering young people to ensure they contribute to the economic growth and development of the city.

KEY ISSUES & CHALLENGES

- SERVICE DELIVERY

- SERVICE DELIVERY STANDARDS, LEVELS OF SERVICES, OUTCOMES, TIMETABLE FOR ACHIEVEMENTS AND FINANCIAL IMPLICATIONS

Limited funding and exponential growth in the municipality have also increased the level of arrears. The Municipality is making great progress with the massive rollout of the program for incremental services aimed at improving the lives of residents in informal settlements.

FINANCIAL PERFORMANCE (2017/18 AND 2018/19): PARENT MUNICIPALITY

- OPERATING BUDGET

- CAPITAL BUDGET

The municipality is making great strides in electrifying informal settlements with informal households earmarked for electrification this year. With regard to the 2017/18 financial year, expenditures amounting to R 32.9 billion were fully financed from the revenues of the municipality and grants and subsidies from the national and provincial governments.

ALIGNMENT WITH NATIONAL AND PROVINCIAL PRIORITIES

The following graph compares the actual spending on capital with the total approved capital budget of the Mother Municipality. Approximately R 5.1 billion from all sources has been received to date, which represents 55.5% of the amount budgeted for.

FINANCIAL STRATEGY, ONGOING VIABILITY AND SUSTAINABILITY

- FINANCIAL STRATEGY

- BUILT ENVIRONMENT PERFORMANCE PLAN ( BEPPS )

- FINANCE MANAGEMENT CAPACITY MATURITY MODEL (FMCMM)

Insufficient capital investment in the park in recent years has had a negative impact on revenues. Ushaka has grown to become a key catalyst for the growth of other hospitality businesses in the district, contributing more than R2 billion to the city's economy.

- SOURCES OF FUNDING

Therefore, Ushaka Marine World is set to undergo a major facelift to make it the ultimate African theme park experience for the next 20 years. Ushaka Marine World has enabled the creation and growth of related hospitality businesses and contributed to the overall growth of tourism in the city and province.

OPERATING EXPENDITURE FRAMEWORK OPERATING EXPENDITURE FRAMEWORK

In line with the approach of recent years, the 2019/20 budget allocations again foresee increases above the CPI level for this cost component. The cost associated with the remuneration of councilors is determined by the Minister of Cooperative Governance and Traditional Affairs in accordance with the Remuneration of Public Office Holders Act, 1998 (Act 20 of 1998). Financial charges consist mainly of interest repayments for long-term borrowings (cost of capital) and are equal to 2.3% of operating expenses.

CAPITAL EXPENDITURE CAPITAL EXPENDITURE

- CAPITAL BUDGET

The municipality recognizes its obligation to optimally preserve its extensive asset base, as underspending on maintenance can shorten the life of assets, increase long-term maintenance and renovation costs, and degrade the reliability of services. However, due to the unstable economic conditions during the fiscal year, it was most beneficial for the municipality to postpone the shooting until July 2018. To this end, the municipality appointed a lead arranger to help set up the program.

Economic Development Trends

Durban Film Office: R 5.1m Reforestation Projects: R 10.3m Business Support Projects: R 38.2m Travel & Tourism Trade Shows: R 17.4m Durban Business Fair & Regional Fair: R 34.3m Support Offers & Presentations: R 5.1m Tourism Events : R 41.1m Advertising of the Durban tourism brand &.

ETA Trends

HOUSING TREND ANALYSIS

Refuse Removal Trends

SANITATION TREND ANALYSIS

Focus on the design and implementation of main road projects, road renovation projects, plant constructions, road upgrades, surface gravel and maintenance of existing road networks.

WATER TREND ANALYSIS

ROAD TREND ANALYSIS

- HUMAN SETTLEMENTS, ENGINEERING, TRANSPORT AND INFRASTRUCTURE

- CORPORATE AND HUMAN RESOURCES

- SUSTAINABLE DEVELOPMENT AND CITY ENTERPRISES

- ANNUAL BUDGET TABLES

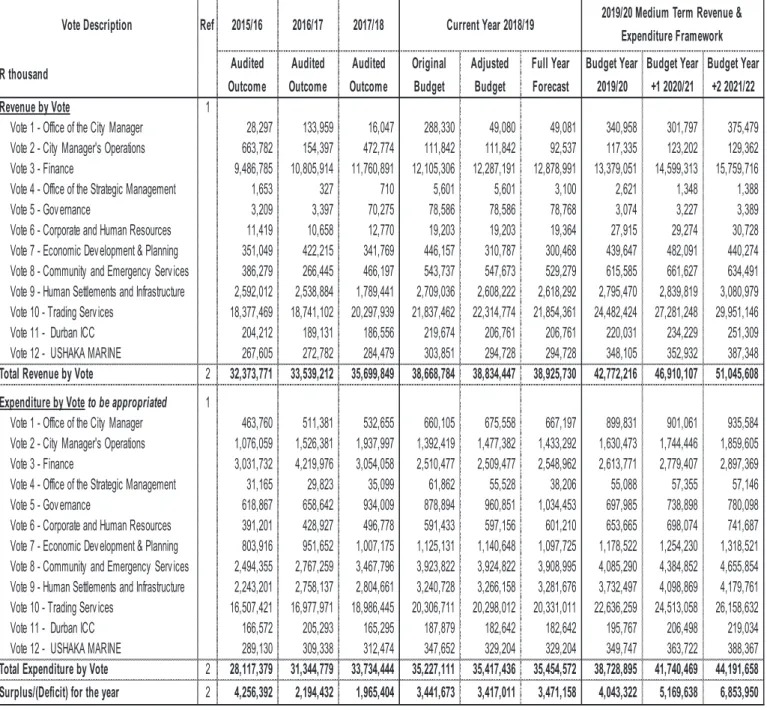

The ten main budget tables as required in terms of Article 8 of the Municipal Budget and Reporting Regulations follow. The table provides an overview of the amounts that will be approved for operational performance, as well as the municipality's commitment to eliminate basic differences in service delivery. This table facilitates the visualization of budgeted operational performance in relation to the organizational structure of the city.

ETH eThekwini - Table A3 Consolidated Budgeted Financial Performance (revenue and expenditure by municipal vote)

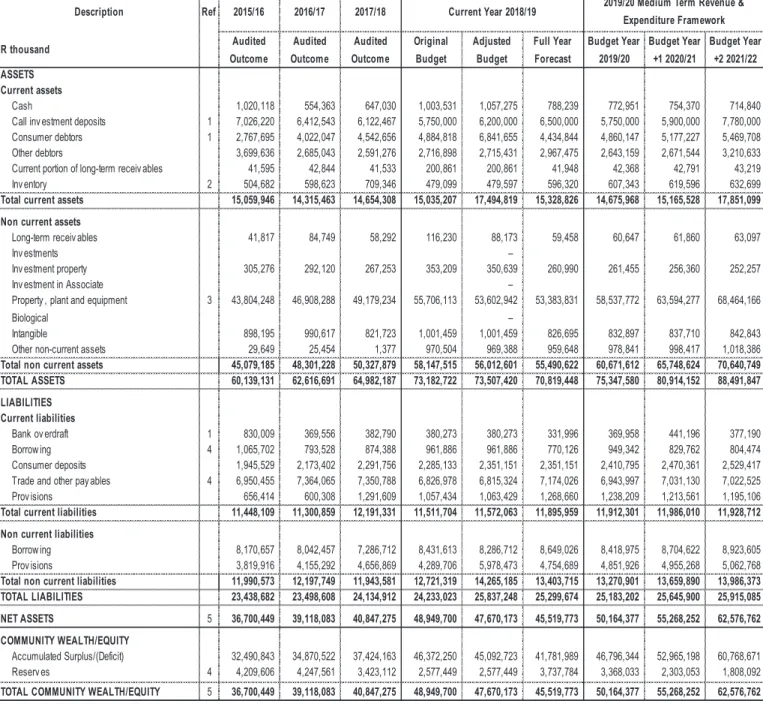

The reason is that the ownership and the municipality's net assets belong to the community. For example, the collection rate assumption will affect the municipality's liquidity and subsequently inform about the level of cash and cash equivalents at the end of the year. The cashback reserves/accumulated surplus reconciliation is aligned with the requirements of MFMA circular 42.

ETH eThekwini - Table A8 Consolidated Cash backed reserves/accumulated surplus reconciliation

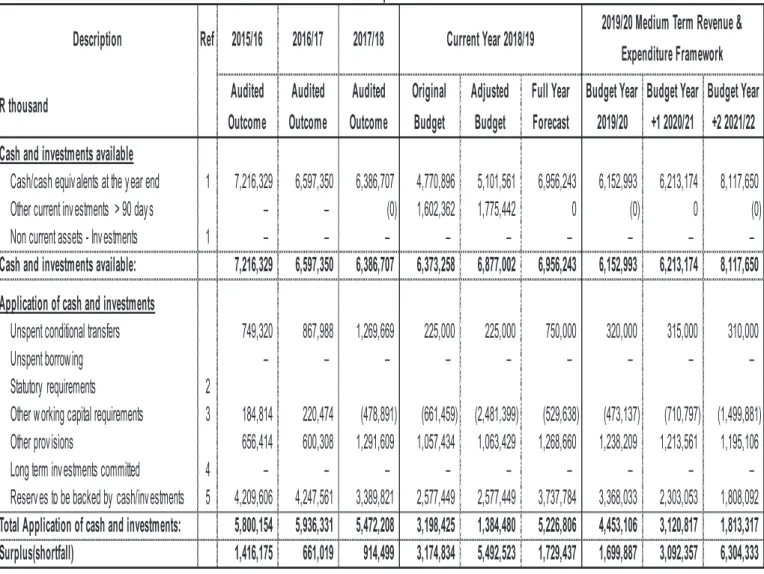

Essentially, the table evaluates the funding levels of the budget by first forecasting year-end cash and capital expenditures and then matching available funding to existing liabilities/liabilities. This shows that available cash and investments exceed requests indicating compliance with MFMA requirements that the council's budget be "funded". As part of the budgeting and planning guidelines that formed the composition of the 2019/20 MTREF, the medium-term framework's end goal was to ensure that the budget is funded and aligned with Article 18 of the MFMA.

Outcome

Audited Outcome

Original Budget

Adjusted Budget

Full Year Forecast

Budget Year 2019/20

Budget Year +1 2020/21

Budget Year +2 2021/22

2019/20 Medium Term Revenue &

Expenditure FrameworkCurrent Year 2018/19

OVERVIEW OF THE ANNUAL BUDGET PROCESS 2

OVERVIEW

The IDMS supports the infrastructure asset management principle of continuous improvement by monitoring and reviewing the outcomes described in the control system. The key to strengthening the link between priorities and spending plans lies in strengthening political oversight of the budget process. Political oversight of the budget process enables the government, and in particular the municipality, to manage the tension between competing policy priorities and fiscal realities.

PROCESS FOR CONSULTATIONS WITH EACH GROUP OF STAKEHOLDERS AND OUTCOMES

Strengthening the link between government priorities and spending plans is not a goal in itself, but the goal should be increased service delivery with the aim of improving the quality of life for all people in the city. MFMA section 53, subsection 1, letter a, states that a municipality's mayor must provide political guidance on the budget process and the priorities that must guide the preparation of the budget.

SCHEDULE OF KEY DEADLINES RELATING TO THE BUDGET PROCESS

OVERVIEW OF ALIGNMENT OF BUDGET WITH IDP OVERVIEW OF ALIGNMENT OF BUDGET WITH IDP

- KEY INTERNATIONAL, NATIONAL AND PROVINCIAL GUIDING DOCUMENTS

- DEVELOPMENT CHALLENGES

- MUNICIPAL STRATEGIC PRIORITY AREAS

- IDP OVERVIEW AND KEY AMENDMENTS

- IDP REVIEW PROCESS AND STAKEHOLDER PARTICPATION

- LINK BETWEEN THE IDP AND THE BUDGET

Given the strategic framework that has been outlined, it is clear that the city's budget should be a pro-growth budget that meets basic needs and builds on existing skills and technology. The municipality's delivery plan is organized into eight separate but linked plans. These priorities lead to the creation of structures that support, house and accompany other actions and activities – the building blocks around which actions and prioritization take place. The review of the five-year plan in 2019/20 offers further opportunities for citizens to actively participate in the development of the IDP.

- KEY FINANCIAL RATIOS / INDICATORS

- FREE AND SUBSIDISED BASIC SERVICES

To take care of the poor, the municipality, as part of its welfare package, provides a basket of free basic services in accordance with a certain level of service. The estimated cost of the welfare package (ie forgone revenue) amounts to around R3.9 billion for the 2019/20 budget year. Additionally, a free basic service is also available to poor consumer units with VIP, urine diversion toilets and informal settlements serviced by a toilet/ablution block within 200m.

OVERVIEW OF BUDGET RELATED POLICIES OVERVIEW OF BUDGET RELATED POLICIES

- ASSESSMENT RATES POLICY

- CREDIT CONTROL AND DEBT COLLECTION POLICY

- TARIFF POLICY

- WATER POLICY

- INVESTMENT / CASH MANAGEMENT AND BORROWING POLICIES

- INFRASTRUCTURE ASSET MANAGEMENT POLICY

- ACCOUNTING POLICY

- FUNDING AND RESERVES POLICY

To ensure compliance with Article 28 of the MFMA, and with the Municipal Budget and Reporting Regulation, procedures have been formulated regarding the transfer of funds and the reporting of the adjusted budget. An infrastructure asset management plan technically analyzes five facilities and strategies of the infrastructure asset life cycle – acquisition, operation, maintenance, renewal and disposal – to predict which infrastructure assets facilities and activities are required to provide utility services in a sustainable manner. To preserve 98% of the value of the existing portfolio, it is important that modern equipment and infrastructure asset systems and practices are implemented across the portfolio in a consistent manner.

OVERVIEW OF BUDGET ASSUMPTIONS OVERVIEW OF BUDGET ASSUMPTIONS

- KEY FINANCIAL ASSUMPTIONS

- CREDIT RATING OUTLOOK

- BORROWING AND INVESTMENT OF FUNDS

- PRICE MOVEMENTS ON SPECIFICS

- TIMING OF REVENUE COLLECTION

- AVERAGE SALARY INCREASES

- CHANGING DEMAND CHARACTERISTICS (DEMAND FOR SERVICES)

- ABILITY OF THE MUNICIPALITY TO SPEND AND DELIVER ON THE PROGRAMS

- COST OF SERVICE DELIVERY VS AFFORDABILITY

The capital expenditure of the parent municipality has been financed by a mixture of public transfers, internally generated funds and external loans. The graphs show that the city will not break any of the supervisory conditions during the MTREF period. Over the past few years, the functions that the eThekwini Municipality is expected to perform have increased in line with the needs of the community.

OVERVIEW OF BUDGET FUNDING OVERVIEW OF BUDGET FUNDING

- SOURCES OF FUNDING

- SAVINGS AND EFFICIENCIES

- INVESTMENTS – CASH BACKED

- LEVELS OF RATES, SERVICE CHARGES AND OTHER FEES AND CHARGES

Investments for the municipality are carried out in accordance with the Regulation on Municipal Investments of the MFMA, the investment policy of municipalities and other relevant legislation. The current DSW tariff structure is being reviewed to ensure that it is based on operating costs and volume. Senior Citizens Project (Adhoc) – Vendors and deliverables should be verified against agreed specifications (once a year).

In accordance with the provisions of the Municipal Property Tax Act (MPRA), the eThekwini Municipality has undertaken a general valuation of all properties across the Metro. A general valuation must be undertaken at least once every four years in terms of the Municipal Property Tax Act. The tariff increases are necessary due to the increase in the cost of bulk purchases, maintenance of existing infrastructure, new infrastructure provision and to ensure the financial sustainability of the services.

LEGISLATION COMPLIANCE STATUS LEGISLATION COMPLIANCE STATUS

This annual budget has been developed in accordance with the requirements prescribed by the MFMA, Municipal Budgeting and Reporting Regulations, National Treasury and mSCOA regulations. The annual report for 2017/18 has been developed taking into account the requirements of the MFMA and the National Treasury. A budget and finance office has been established in accordance with MFMA and National Treasury requirements.

STATISTICAL INFORMATIONSTATISTICAL INFORMATION

CONSOLIDATED BUDGET

DETAILED

7+H7KHNZLQL7DEOH$&RQVROLGDWHG%XGJHWHG)LQDQFLDO3HUIRUPDQFHUHYHQXHDQGH[SHQGLWXUHE\PXQLFLSDOYRWH$ .. 9RWH2IILFHRIWKH&LWHIIDQD\LWHIIDQH&LWHIIDQ. . &LW\,QWHUJULW\DQG,QYHVWLJDWLRQV ± ,QWHUQDO$XGLWDQG5LVN0DQDJHPHQW. 9RWH(FRQRPLF'HYHORSPHQW 3ODQQLQJ 'HSXW\&LW\0DQDJHU ±. XVLQHVV6XSSRUW 5HWDLO0DUNHWV 'HYHORSPHQW3ODQQLQJ 0DQDJHPHQWWW. 9RWHWHQ UH 'HSXW\&LW\0DQDJHU +RXVLQJ (QJLQHHULQJ H7KHNZLQL7UDQVSRUW$XWKRULW\ . )RUPDO+RXVLQJ.

BUDGET SUPPORTING TABLES

7+H7KHNZLQL6XSSRUWLQJ7DEOH6$D3URSHUW\UDWHVE\FDWHJRU\FXUUHQW\HDU 'HVFULSWLRQ 5HVL,QGXVW%XV &RPP)DUPSURSV6WDWHRZQHG0XQLSURSVULZHLL )RUPDO ,QIRUPDO 6HWWOH .. amp;RPP /DQG 6WDWHWUXVW ODQG6HFWLRQ QQRWH 3URWHFW $UHDV1DWLRQDO 0RQXPWV3XEOLF EHQHILW RUJDQV. 7+h7khnzlql6xssruwlqj7deoH6 $ e3urshuw \ udwhve \ fdwhjru \ exgjhw \ hdu 'hvfulswlrq 5hvl, qgxvw%xv & rpp) dupsursv6wdwh rzqhg0xqlsv3xeolfsfsflf Vhuylfhwwh rzqhg0xqlsv3xeolf VhuyLfdwh rzqhg0xqlsv3xeolf VhuYlfdwh rzqhg0xqlsv3xeolf VhuYlfdwh Rzqhg0xqlsv3xeolfs Wh rzqhg wrzqv) rupdo, qirupdo 6hwwoh. amp;RPP /DQG6WDWHWUXVW ODQG6HFWLRQ Q QRWH 3URWHFW $UHDV1DWLRQDO 0RQXPWV3XEOLF EHQHILW RUJDQV. 0LQLQJ 3URSV %XGJHW BUDGET RELATED CHARTS